THE AMERICAN

FAMILIES PLAN TAX

COMPLIANCE AGENDA

U.S. DEPARTMENT OF THE TREASURY

MAY 2021

The American Families Plan Tax Compliance Agenda I 1

I. Executive Summary and Introduction

President Biden recently proposed the American Families Plan, advancing comprehensive and necessary investments in American

children and families. To help support this important agenda and increase fairness in the tax system, the President also proposed a

set of tax compliance measures to foster a tax system where Americans pay the taxes they owe.

This report describes the President’s tax compliance initiatives that seek to close the “tax gap”—the dierence between taxes owed

to the government and actually paid. According to Treasury analysis, the tax gap totaled nearly $600 billion in 2019 and will rise to

about $7 trillion over the course of the next decade if le unaddressed—roughly equal to 15% of taxes owed. These unpaid taxes

come at a cost to American households and compliant taxpayers as policymakers choose rising deficits, lower spending on necessary

priorities, or further tax increases to compensate for the lost revenue.

The magnitude of the tax gap means that compliance initiatives have the potential to raise substantial revenue, but these reforms

also improve tax progressivity and economic eiciency. While roughly 99% of taxes due on wages are paid to the Internal Revenue

Service (IRS), compliance on less visible sources of income is estimated to be just 45%.

1

The tax gap disproportionately benefits

high earners who accrue more of their income from non-labor sources where misreporting is common. Further, the tax gap imposes

distortions because of the resources some expend to avoid paying taxes and the incentives created to shi economic activity into

certain areas where tax liabilities can be illegally evaded.

To raise revenue, improve eiciency, and build a more equitable tax system, investments in tax compliance are of first order

importance. The compliance proposals in the American Families Plan provide the IRS with the resources and information it needs

to overhaul and enhance tax administration. These policy changes are integral to addressing evasion, but they also prioritize

improving taxpayer service and the experience of Americans as they navigate the tax system. Taxpayers would benefit from eective

communication with the IRS, access to the tax credits to which they are entitled, and competent assistance as they file their taxes.

The President’s compliance agenda has several transformational elements:

1. Provide the IRS the resources it needs to address sophisticated tax evasion. The first step in the President’s tax

administration eorts is a sustained, multi-year commitment to rebuilding the IRS, including nearly $80 billion in additional

resources over the next decade. The IRS would grow manageably (no more than around 10% annually) but also have certain

funding in place to make investments with large fixed costs—like modernizing information technology, improving data analytic

approaches, and hiring and training agents dedicated to complex enforcement activities. This would make up the ground

that the IRS has lost over the last decade. During this time, the IRS budget fell by about 20%, leading to a sustained decline in

its workforce particularly among specialized auditors who conduct examinations of high-income and global high net worth

individuals and complex structures, like partnerships, multi-tier pass-through entities, and multinational corporations.

2. Provide the IRS with more complete information. When the IRS can verify taxpayer filings with third-party information reports,

such as the W-2 forms submitted by employers to report wages, compliance rates exceed 95%. Without third-party reporting,

compliance rates fall below 50% and thus lead to an inequitable asymmetry in tax collections depending on the form in which

income is accrued. The Government Accountability Oice (GAO) and IRS agree that strengthening third-party reporting is one of

1 IRS, 2019. “Federal Tax Compliance Research: Tax Gap Estimates for Tax Years 2011–2013.” Publication 1415 (Rev. 9-2019).

The American Families Plan Tax Compliance Agenda I 2

the most eective ways to improve tax compliance. The President’s proposal leverages the information that financial institutions

already know about the accounts that they house. Financial institutions would add information about total account outflows

and inflows to existing reporting on bank accounts. Importantly, there are no added requirements for taxpayers. The IRS will be

able to deploy this new information to better target enforcement activities, increasing scrutiny of wealthy evaders and decreasing

the likelihood that fully compliant taxpayers will be subject to costly audits. As a result, voluntary compliance will rise through

deterrence as would-be tax evaders realize that the IRS has an additional lens into previously unreported income streams.

3. Overhaul outdated technology to help the IRS identify tax evasion and serve customers. The IRS still relies on Individual

and Business File Systems that date back to the 1960s—the oldest in the federal government. The result is decades upon

decades of tax administration built upon a system that is written in a programming language that is no longer taught, and where

new functions are added in a patchwork rather than integrated manner. Modernization funding would allow the IRS to address

technology challenges and develop innovative machine learning that can be deployed to better identify suspect tax filings,

for example, by comparing returns to similarly situated taxpayers and historical filings in a way that the current IRS ecosystem

does not allow. These resources would also support eorts to meet threats to the security of the tax system, like the 1.4 billion

cyberattacks the IRS experiences annually. With a revitalized IRS, taxpayers would also be able to communicate with and receive

guidance from the IRS in a clear, timely manner when questions arise. Further, modernized IT would help improve taxpayer

service and ensure that the IRS is able to eectively and eiciently deliver tax credits to eligible families and workers, including

recent expansions to the Child Tax Credit, the Earned Income Tax Credit, and the Child and Dependent Care Tax Credit proposed

in the American Families Plan.

4. Regulating paid tax preparers and increasing penalties for those who commit or abet evasion. Taxpayers oen make use

of unregulated preparers who lack the training to provide accurate tax assistance. These preparers submit more returns than

all other preparers combined, and taxpayers rely on their guidance, in part because of challenges in reaching the IRS in a timely

manner when questions arise. In addition to the regulation of paid preparers and service improvements that would simplify tax

filing, the President’s proposal includes additional sanctions for so-called “ghost preparers” who fail to identify themselves on

the tax returns which they prepare.

Experts at the Treasury Oice of Tax Analysis estimate that these initiatives would raise $700billion in additional tax revenue over the

next decade. This revenue is backloaded in the 10-year budget window as several of these new investments—such as hiring revenue

agents capable of complex global high net-worth examinations and building the technological infrastructure to support a new

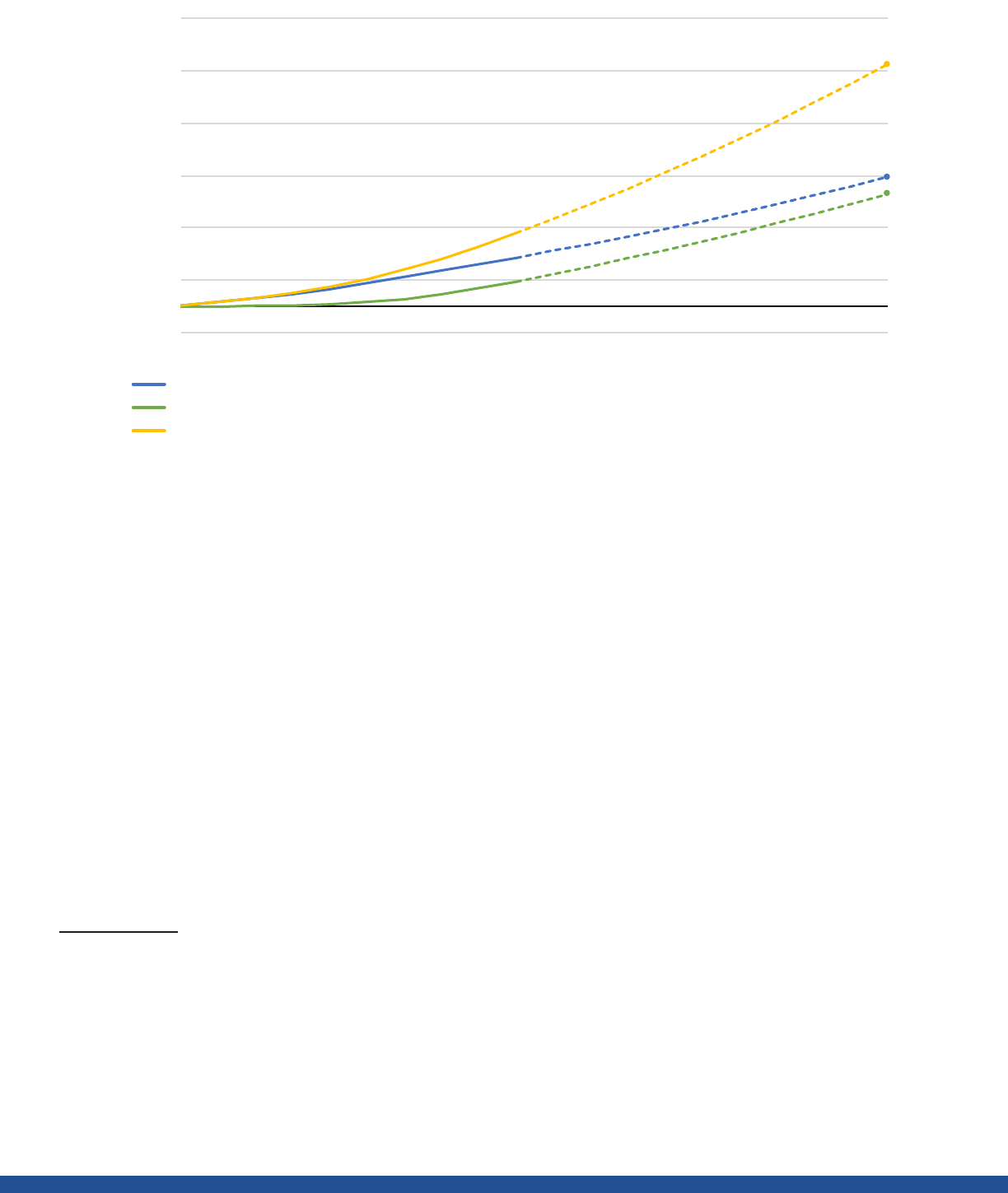

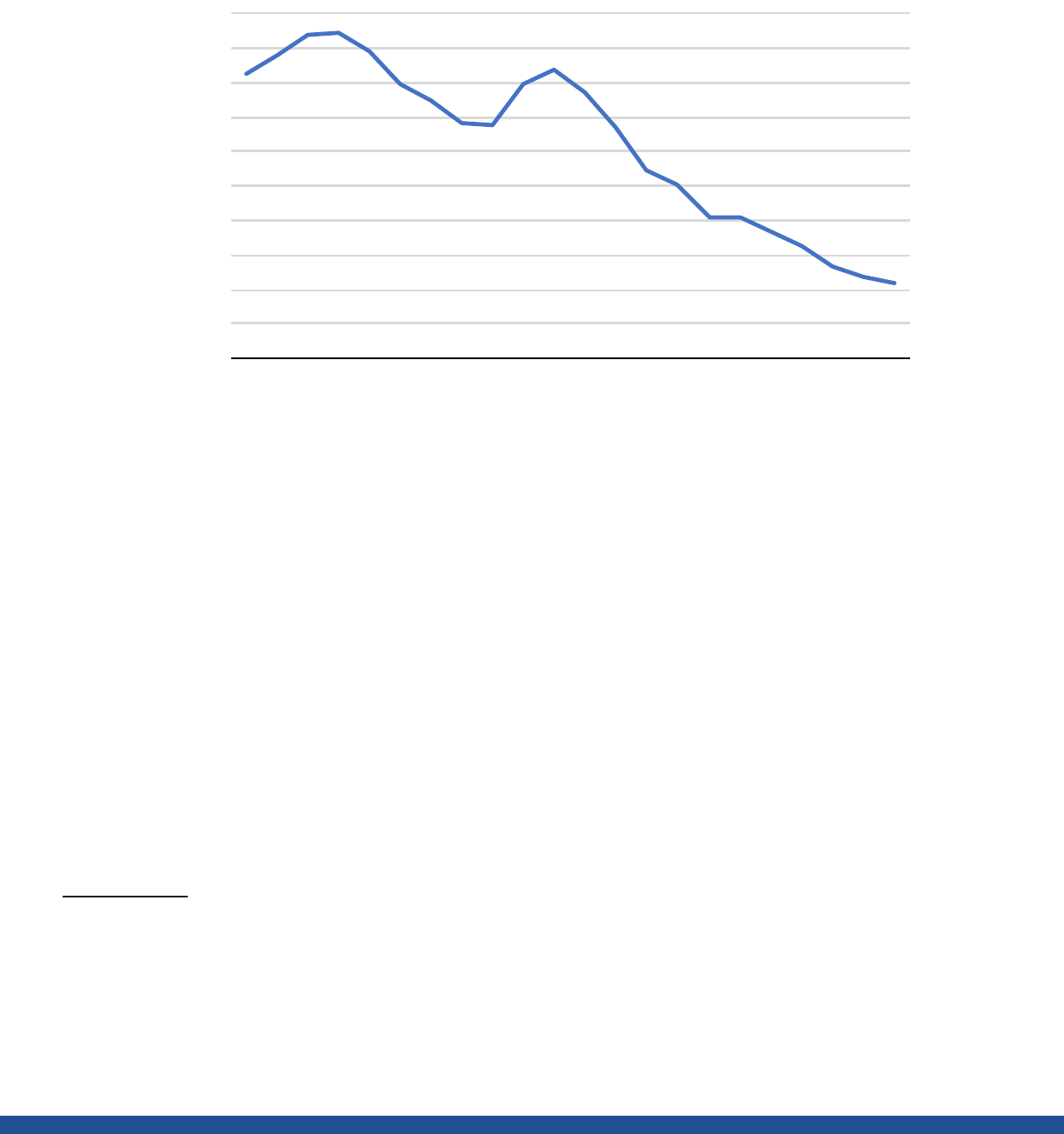

information reporting regime—take years to reach their full potential. As Figure 1 shows, the revenue raised in the second decade

amounts to $1.6 trillion.

These estimates are conservative because the revenue potential of additional resources for tax administration is based on return

on investment (ROI) estimates from the IRS that only exist for adjustments detected through current enforcement-related activities.

Benefits of other foundational shis in tax administration that would result from this proposal—for example, overhauling and

integrating IT systems and restoring trust in the IRS through timely support for taxpayers—are also unaccounted for. Moreover,

although revenue estimates for increased information reporting include the eects of this regime on voluntary compliance, estimates

for increased enforcement actions do not account for deterrent eects, which are generally considered qualitatively significant.

The American Families Plan Tax Compliance Agenda I 3

II. Dening and Measuring the Tax Gap

A well-functioning tax system requires that taxpayers make good on their tax obligations. An important measure of our tax system’s

administrative eectiveness is the “tax gap”—the aggregate dierence between federal taxes owed and taxes paid voluntarily and

on-time. The size of the tax gap has meaningful implications for fiscal policy, while the distribution of the tax gap across income

levels has important consequences for tax progressivity.

The IRS periodically releases estimates of the federal tax gap. The most recent estimates, covering years 2011–2013, showed an

average gross tax gap of $441 billion annually. Aer late payments and enforcement eorts are factored in, the net tax gap over

this period is estimated at $381 billion. Extrapolating for growth in the intervening years, for tax year 2019, the gross tax gap was

estimated at $584 billion, and is on pace to total $7 trillion over the course of the next decade. This is almost 3% of GDP on an

annualized basis. These estimates imply a voluntary compliance rate of around 84%, and a net compliance rate of around 86%.

2,3

The tax gap has three distinct elements: taxpayers who fail to file returns in a timely manner (the “nonfiling” tax gap, around 9% of

the gross tax gap); those who underreport income or overclaim deductions and credits on tax returns (the “underreporting” tax gap);

2 The voluntary compliance rate is defined as the amount of taxes paid “voluntarily and timely” divided by “total true tax,” and corresponds to the gross tax gap.

The net compliance rate is higher because it is the ratio corresponding to the net tax gap, aer “enforced and other late payments” are added to the numerator of

this ratio. Greater enforcement eorts increase both the voluntary compliance rate and taxes collected through enforced and other late payments. Ibid.

3 The IRS tax gap report shows that average annual federal taxes owed and voluntarily paid on time for 2011–2013 were about $2,242 billion and total estimated

annual tax liability was about $2,683 billion, for a voluntary compliance rate of about 84%. This rate has been relatively constant since the 1970s. Ibid.

1,238

1,078

2,315

-250

250

750

1,250

1,750

2,250

2,750

2022 2024 2026 2028 2030 2032 2034 2036 2038 2040

Estimated Revenue ($, billions)

Cumulative Compreh ensive Financial Account Reporting

Cumulative Program integrity Allocation Adjustment and Additional IRS Funding

Cumulative Total Revenue

Figure 1: Revenue Raised from Compliance Initiatives, 2022–2040

NOTE: Estimates outside the 10-year budget window are subject to greater uncertainty which is reflected by the dotted line.

Comprehensive Financial Account Reporting

Program Integrity Allocation Adjustment and Additional IRS Funding

Cumulative Total Revenue

The American Families Plan Tax Compliance Agenda I 4

and those who underpay taxes despite reporting obligations in a timely manner (the “underpayment” tax gap, around 11%). By far

the largest contributor to the tax gap is the underreporting gap—around 80%.

4

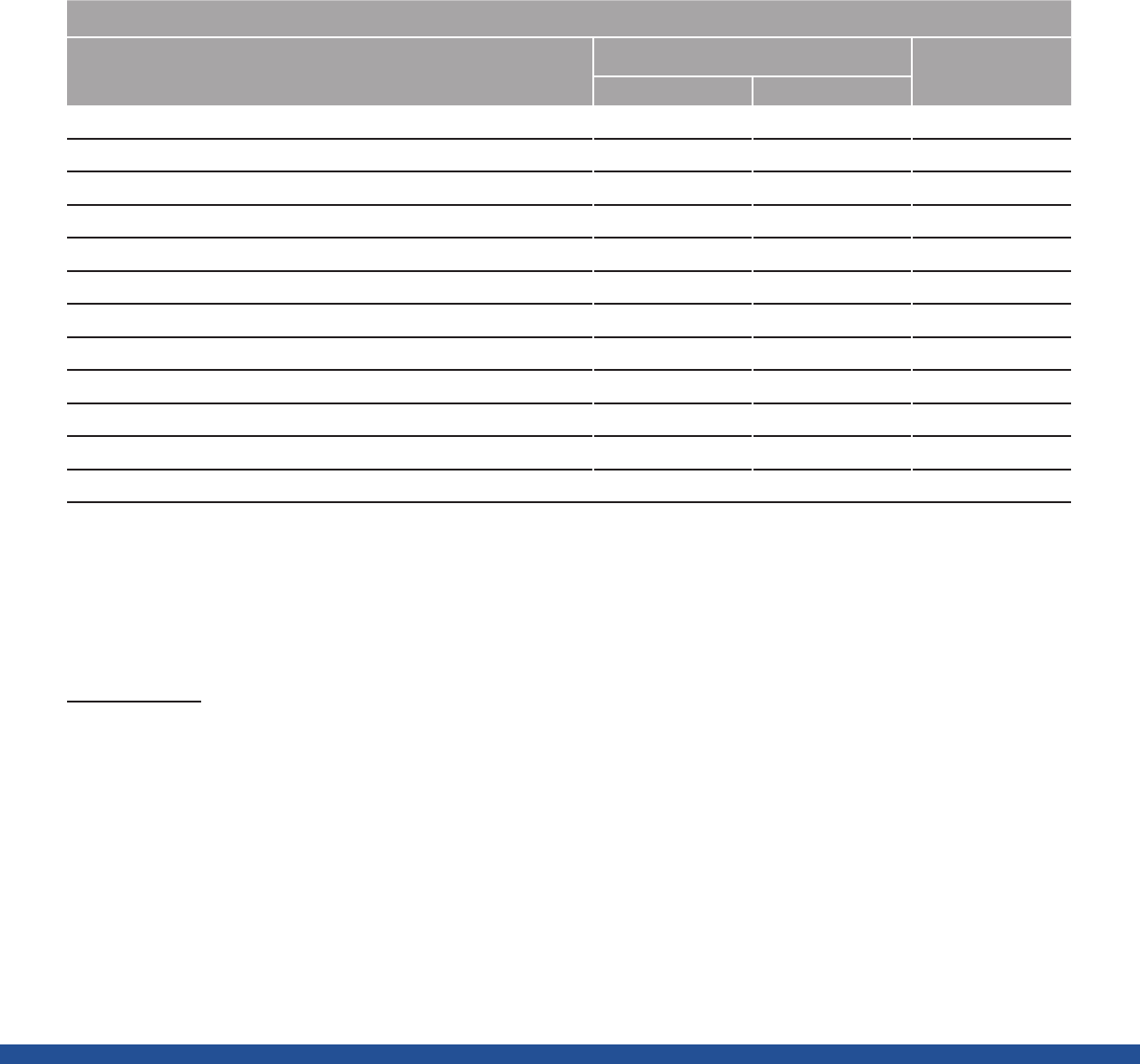

Table 1: Tax Gap Estimates over Time

Tax Gap Estimates and Projection

Tax Gap Component TY 2011–2013 Published TY 2019 Projection

[1]

TY 2019 Projection,

Adjusted

[2]

Estimated Total True Tax $2,683 $3,589 $3,635

Gross Tax Gap $441 $584 $630

Nonfiling Tax Gap $39 $52 $52

Underreporting Tax Gap $352 $466 $512

Underpayment Tax Gap $50 $66 $66

Voluntary Compliance Rate 83.6% 83.7% 82.7%

Enforced and Other Late Payments $60 $76 $76

Net Tax Gap $381 $508 $554

Net Compliance Rate 85.8% 85.8% 84.8%

[1] Estimates based on applying the tax gap projection technique (which assumes constant compliance rates by major component of income) to the TY 2011-2019

IRTF and BRTF data.

[2] Estimates based on adjusting compliance rates for Guyton et al. (2021) estimate that the published tax gap was understated by an annual average of $33 billion

(in 2012 dollars) in underreported income from oshore wealth and passthrough entities in TY 2006-2013, then applying constant compliance rates by major

component of income.

Many attempts to assess the tax gap rely on a sample of random audits that the IRS undertakes to estimate the share of unpaid

taxes. The most prominent of these studies examines individual income tax returns. Such random studies are generally thought of

as the “gold standard” for understanding tax evasion. However, these audits can struggle to capture the full extent of tax evasion

for high-income taxpayers because sophisticated taxpayers and those who advise them are well-positioned to shield unpaid taxes

from audit detection.

5

This has led some scholars to suggest that the results from studies based on IRS “National Research Program”

(NRP) random audit data may not satisfactorily capture tax evasion by the very wealthy taxpayers, and that tax gap estimates are

significantly understated because they do not fully reflect this sophisticated evasion.

6

The IRS attempts to mitigate this by adjusting for income undetected by audits through “Detection Controlled Estimation” (DCE),

a methodology under which detected evasion is used to estimate the magnitude of undetected evasion. DCE adjustments are

intended to bring the amounts of estimated non-compliance in line with the amounts detected by the most specialized auditors. In

the aggregate, these adjustments roughly triple the estimated amount of unreported income. But even DCE estimates may not fully

account for the most sophisticated evasion techniques, undetected income, and unidentified emerging issues. One estimate of the

4 Ibid.

5 For example, capital income accruing to oshore accounts have until recently not been subject to reporting requirements that make them easily traceable in

audits. In addition, passthrough income accrues disproportionately to high earners and can be challenging to attribute to its ultimate owner.

6 See, e.g., Alstadsæter, Annette, Niels Johannesen, and Gabriel Zucman, 2019. “Tax Evasion and Inequality.” American Economic Review, 109(6): 2073-2103.

The American Families Plan Tax Compliance Agenda I 5

magnitude of this issue is shown in Table 1, which illustrates that adjusting the tax gap for passthrough and oshore evasion increase

the tax gap significantly.

Research also finds that underreporting tends to rise with income when taxpayers are ranked by their total income, including the

unreported amount.

7

In part, tax evasion rises with higher incomes because higher-income taxpayers have sophisticated accountants

and tax preparers who can stake out aggressive tax positions that can help shield true tax liability. And because the IRS lacks the

number of specialized auditors needed to adequately detect and pursue these instances of noncompliance, the consequences of tax

underpayment are perceived to be minor, and voluntary compliance rates are lower.

But the distribution of the underreporting tax gap is also a byproduct of the current information reporting regime. For some, but

not all, categories of income, the IRS can crosscheck taxpayer filings because it receives information reports from third parties,

like employers, and this information can be used to verify that taxpayers are accurately reporting income and deductions. When

taxpayers know that their tax information is being reported to authorities, their voluntary compliance rate increases.

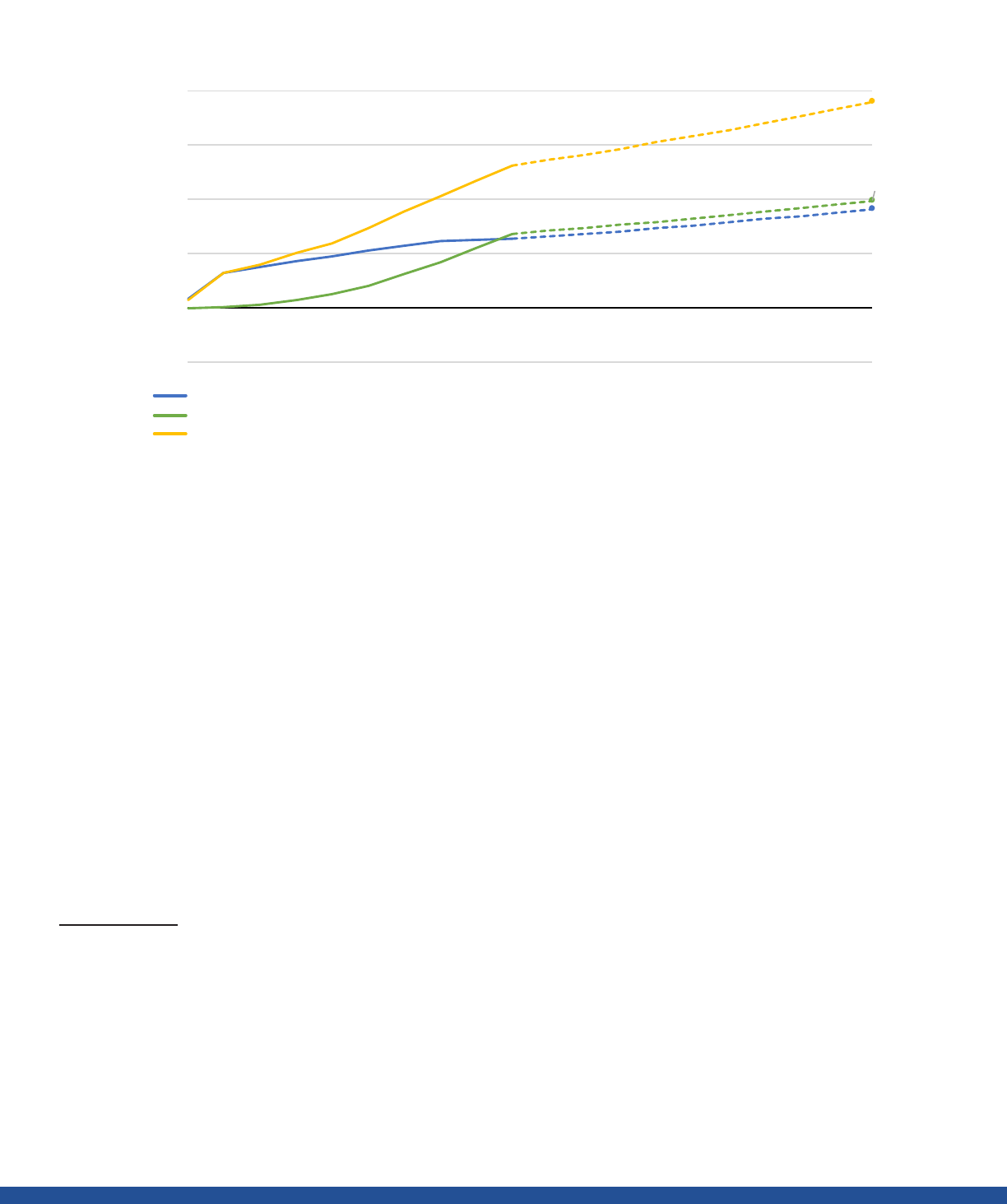

For ordinary wage and salary income, where employers share a Form W-2 with both employees and the IRS (as well as automatically

withhold income taxes), compliance is very high, with only an estimated 1% misreporting rate.

8

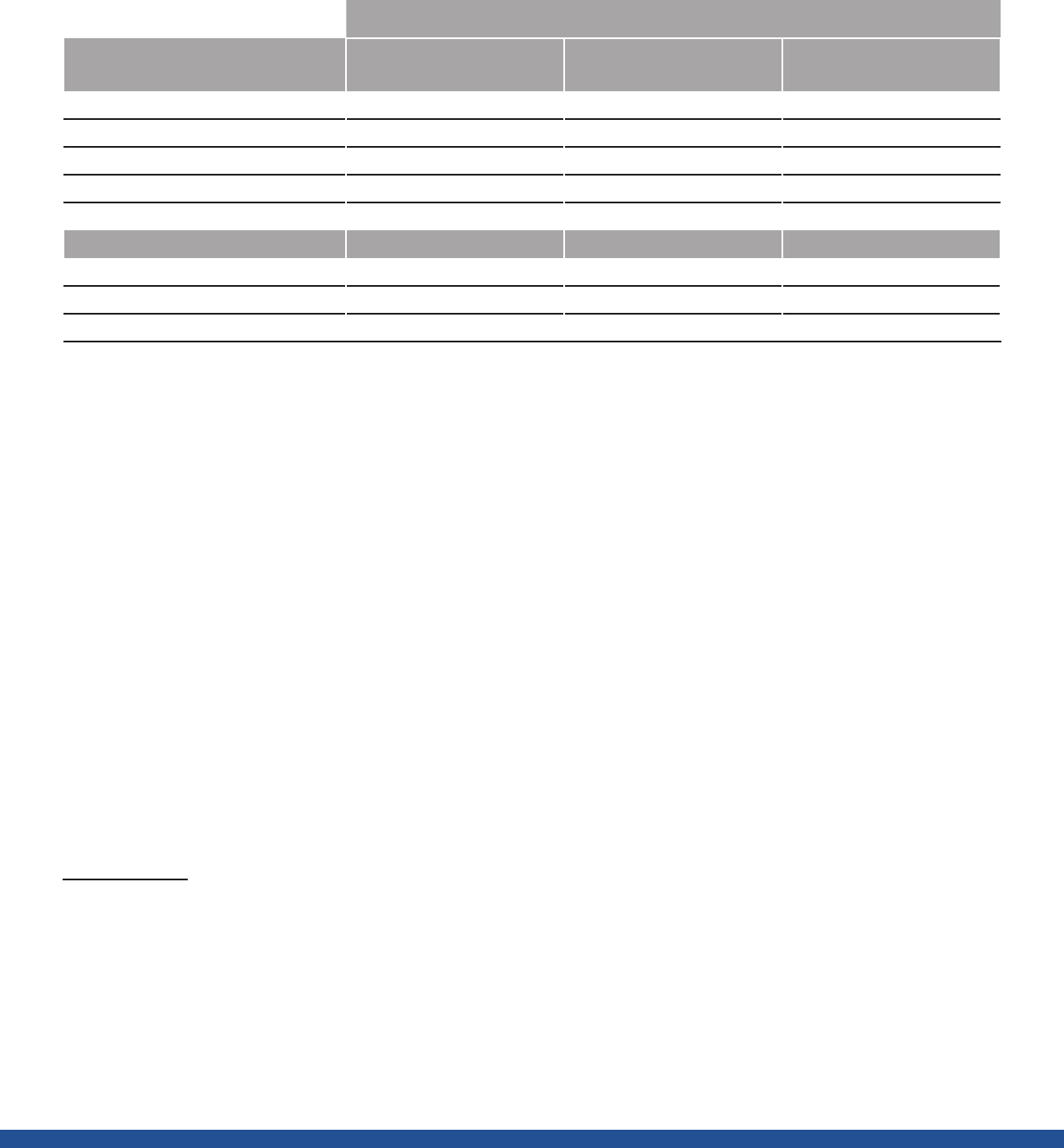

As Figure 2 shows, compliance drops

o with a decline in third party information reporting. For income subject to substantial information reporting, but not withholding,

estimated misreporting rates are 5%. For income subject to some limited information reporting, misreporting rises to 17%. In

stark contrast, for opaque income sources that accrue disproportionately to higher earners—like proprietorship income and rental

income—misreporting is estimated to be 55%. The IRS and GAO have identified increased information reporting as one of the best

ways to improve taxpayer compliance because providing the IRS with a lens into opaque income sources both improves enforcement

activities and encourages voluntary compliance by taxpayers who perceive that the IRS has information necessary to pursue them

should they not meet their tax obligations.

9

7 See, e.g., Guyton, John, Patrick Langetieg, Daniel Reck, Max Risch, and Gabriel Zucman, 2021. “Tax Evasion at the Top of the Income Distribution: Theory and

Evidence,” NBER Working Paper No. 28542. The estimates in Guyton et al. (2021) are based on imputations of undetected evasion using multipliers developed

from earlier audit data. The advisability of so-called “detection-controlled estimation” (DCE) adjustments are debated in the literature, especially with respect

to understanding the distribution of noncompliance (see also DeBacker, Jason et al., 2020. “Tax Noncompliance and Measures of Income Inequality,” Tax Notes

Federal, 17 February; and Johns, Andrew and Joel Slemrod, 2010. “The Distribution of Income Tax Noncompliance,” National Tax Journal, 63(3)).

8 IRS, 2019. “Federal Tax Compliance Research: Tax Gap Estimates for Tax Years 2011-2013.”

9 GAO, 2019. “Multiple Strategies are Needed to Reduce Noncompliance: Statement of James R. McTigue, Jr., Director, Strategic Issues,” GAO-19-558T.

The American Families Plan Tax Compliance Agenda I 6

Although less is known about the distribution of the nonfiling and underpayment tax gaps, a recent Treasury Inspector General

report highlights the importance of high-income nonfilers

10

as contributors to the tax gap. The report notes that since 2010, the

estimated number of high-income non-filers has risen by nearly 50% as a resource-constrained IRS lacked the ability to pursue all of

these cases. Between 2014–2016, the Inspector General’s report identified nearly 900,000 high-income nonfilers, of which 400,000

cases (44% of cases) were never investigated due to resource constraints. Of these 400,000 cases, 300 of the most egregious evaders

cost the federal government $10 billion in unpaid tax liabilities over this period.

11

The IRS is already working to address this issue: In

2018, it established a program to pursue all high-income nonfilers for tax years from 2016 through 2019, and it intends to select all

high-income nonfiling cases for enforcement action for tax years 2020 and beyond.

III. IRS Challenges with Compliance

Given the current magnitude of the tax gap in the United States, large compliance initiatives will have benefits that far exceed costs.

One illustration of the large potential return on these resource investments is provided by the IRS, which estimates that $1 spent

on tax enforcement typically yields at least $4 in direct revenue (for example, increased tax payments collected from high-income

10 A high-income nonfiler is any nonfiler with total income greater than or equal to $100,000.

11 TIGTA, 2020. “High-Income Nonfilers Owing Billions of Dollars Are Note Being Worked by the Internal Revenue Service,” 2020-30-015. Since 2020, the IRS has

committed to a new strategy for handling non-filing cases and aims to prioritize those involving high-income taxpayers (see Eric Hylton, “How the IRS Prioritizes

Compliance Work on High-Income Non-Filers Through National and International Eorts,” CL-20-08, IRS.)

¹ Includes wages and salaries

² Includes pensions and annuities, unemployment compensation, dividend income, interest income, and taxable Social Security benefits

³ Includes partnership/S corp income, capital gains, and alimony income

⁴ Includes nonfarm proprietor income, other income, rents and royalties, farm income, and Form 4797 income

Figure 2: Misreporting by Income Category

0

20

40

60

80

100

120

140

160

0

0.1

0.2

0.3

0.4

0.5

0.6

Income Subject to Information

Reporting and Withholding¹

Income Subject to Information

Reporting ²

Income Subject to Some

Information Reporting ³

Income Subject to Little or No

Information Reporting⁴

Underreporting Tax Gap (Tax, billions)

Net Misreporting Percentage (Income)

Net Misreporting Percentage (Income) Underreporting Ta x Gap ($, Billio ns)

Income Subject to

Information Reporting

and Withholding

1

Income Subject

to Information

Reporting

2

Income Subject to

Some Information

Reporting

3

Income Subject

to Little or No

Information Reporting

4

Net Misreporting Percentage (Income) Underreporting Tax Gap ($, Billions)

Underreporting Tax Gap ($, billions)

Net Misreporting Percentage (Income)

The American Families Plan Tax Compliance Agenda I 7

nonfiler audits).

12

This direct increase in additional tax revenue that the IRS is able to collect from compliance eorts does not include

the indirect eects of greater enforcement activities, as evidence suggests that taxpayers are more likely to be compliant in the

presence of visible, robust enforcement eorts.

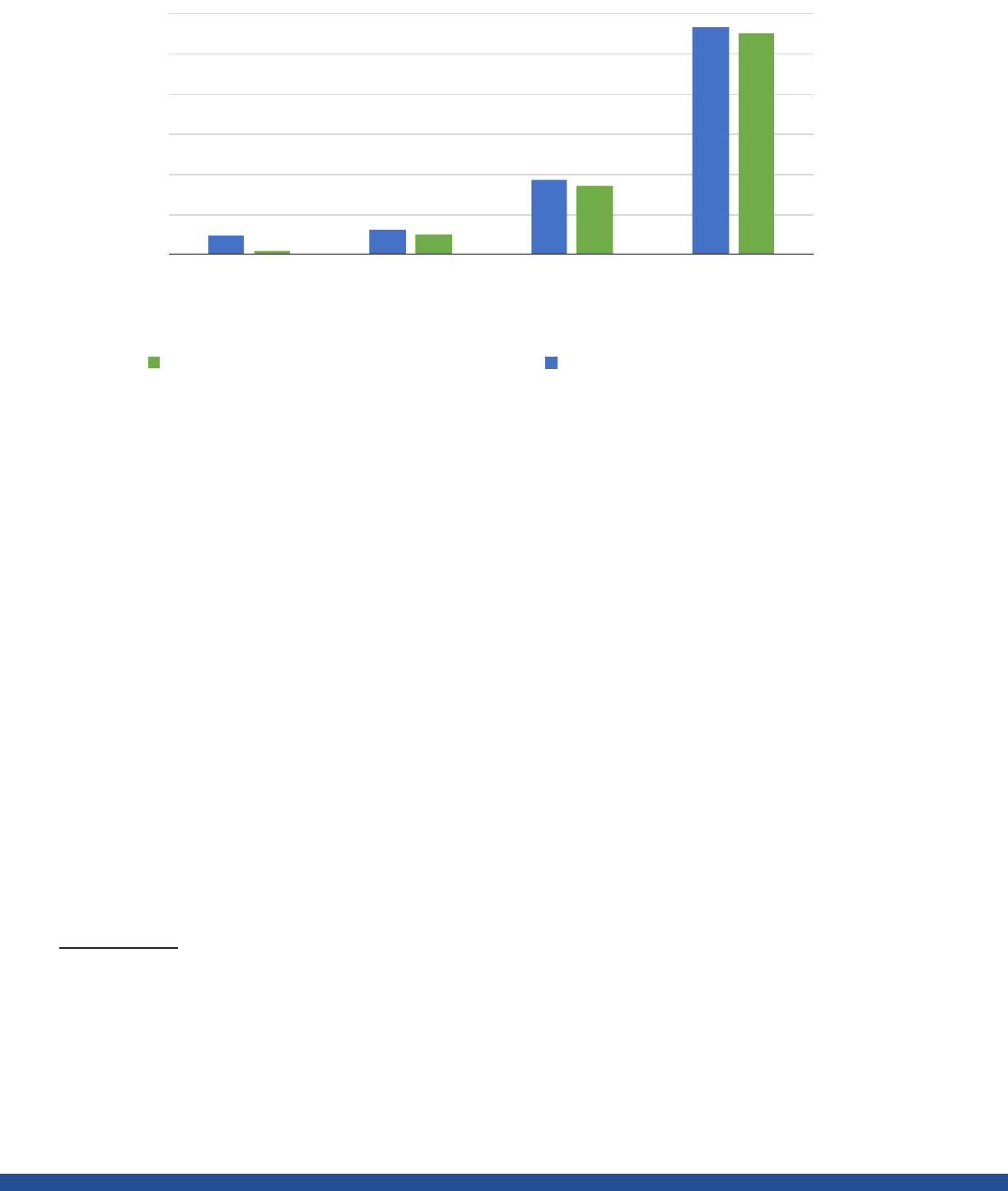

Technology (and, in theory, the ability to detect tax evasion) has developed significantly in recent years. In the late 1990s, only about

10% of individual income tax returns were filed electronically and the vast majority of the IRS’s enforcement activities focused on

returns filed on paper. The Internal Revenue Service Restructuring and Reform Act of 1998 helped change this by setting an ambitious

goal of reaching an 80% electronic filing rate over the course of the decade following 1998. The IRS furthered the transition away from

paper returns by providing electronic filing options for all of the major tax filing categories, and by 2011, the electronic filing rate for

individual income tax returns was 78% and continued to rise to 93% in 2019. For business returns, the electronic filing rate has more

than doubled (from 33% to 70%) since 2011.

Enhanced electronic filing should help the IRS improve compliance in an eicient manner.

13

In addition to reducing processing burden,

data from electronically filed returns are easier to match against data contained on third-party information returns, prior year’s returns,

and similarly situated returns to help identify the most productive tax returns to audit. This work can also help avoid unnecessary,

costly and burdensome audits of compliant taxpayers. Yet, tax compliance has not improved. This is because the IRS operates outdated

systems and lacks the ability to fully take advantage of the benefits of more modern technology due to its resource constraints. Further,

noncompliance has been exacerbated by enhanced opportunities to shield income from tax liability, and even from audits. These

opportunities are particularly available for those in the top end of the income distribution who can avoid taxes through sophisticated

strategies such as oshoring, creating complex partnership structures, or moving taxable assets into the crypto economy.

14

12 IRS estimates. For direct enforcement agents and associated staing, the ROI is much higher. The IRS provides a range of ROI estimates for dierent types of

activities, informed by how collections have risen historically across categories. These range from 2 to 11, and increase over time as new initiatives become more

productive. IRS, 2020. “Congressional Budget Justification & Annual Performance Report and Plan.” Publication 4450 (Rev. 2-2020).

13 GAO, 2019. “Multiple Strategies are Needed to Reduce Noncompliance: Statement of James R. McTigue, Jr., Director, Strategic Issues.”

14 The diiculty of tracking down oshore income is why some countries have adopted amnesty agreements that incentivize individual taxpayers to voluntarily

disclose foreign wealth. These tend to increase tax revenue, reflecting a large gap between true taxable income and what is taxed. Langenmayr, Dominika, 2017.

“Voluntary Disclosure of Evaded Taxes—Increasing Revenue, or Increasing Incentives to Evade?” Journal of Public Economics, 151: 110-125.

The American Families Plan Tax Compliance Agenda I 8

A. Consequences of Technology Shortfalls

Due in part to the IRS’s reliance on outdated technological platforms, the compliance benefits of the transition to electronic tax

return filing have yet to be fully realized. Without adequate technology, the IRS is unable to make use of 21st century data analytic

approaches to verify the accuracy of taxpayer filings.

The IRS’s core tax processing system for over 150 million individual tax returns and $1.2trillion in annual revenue—known as

Individual Master File (IMF)—is written in programming languages that date back to more than half a century ago, making IMF

among the oldest IT systems in the federal government.

15

Designed in 1962, IMF is one of the highest risk systems in the Federal

government, exposing a major weakness to the IRS’s ability to administer and collect taxes. (The system for processing business tax

returns is similarly antiquated.) Annual changes have been made to the system since its development to address tax code changes

and to improve processes and, where possible, to update the underlying hardware. The result today is decades of tax law written in

a programming language that is no longer taught, a data platform that is highly complex to maintain, and an outdated system with a

limited number of employees supporting it—about half of whom are eligible to retire.

The IRS’s legacy computing infrastructure cannot keep pace with the preferences of today’s taxpayers for instantaneous data access,

real-time interactions, and other customer-centric services. The cost to operate the IRS’s current technology ecosystem continues to

increase as well. The GAO has pointed out that the use of such an antiquated systems is more costly for the IRS than replacing with

modern technology since “procurement and operating costs associated with this [programming] language will steadily rise, because

15 GAO, 2019. “IRS Needs to Take Additional Actions to Address Significant Risks to Tax Processing,” GAO-18-298.

0.931

0.702

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1

2011 2012 2013 2014 2015 2016 2017 2018 2019 2020

Individual Electronic Filing Rate Busines s Electronic Filing Ra te

Figure 3: Electronic Filing Rates, CY 2011–2020

Individual Electronic Filing Rate Business Electronic Filing Rate

The American Families Plan Tax Compliance Agenda I 9

fewer people with the proper skill sets are available to support [it].”

16

Outdated technology is a problem that extends beyond the 1960s

Master File architecture. As of the end of 2020, 30% of soware in use was “aged”, meaning behind the most up-to-date version.

17

Without the resources to modernize its underlying technological infrastructure the IRS is required to layer new IT systems on top

of an obsolete base infrastructure.

18

The result is a patchwork approach that poses a threat to the stability of the tax system. As

the National Taxpayer Advocate warned, “By analogy, the IRS has erected a 50-story oice building on top of a creaky, 60-year-

old foundation, and it is adding a few more floors each year. There are inherent limitations on the functionality of a 60-year-old

infrastructure, and at some point, the entire edifice is likely to collapse.”

19

To illustrate the danger, in the peak of the 2017 tax filing

season, the IRS system crashed on the day of the filing deadline and forced a last-minute national federal tax filing extension.

20

An

added risk exposure caused by outdated technology is that it is ill-suited to meet new and expanding challenges. The IRS defends

against approximately 1.4 billion sophisticated cyberattacks annually as criminals seek access to a significant volume of sensitive

taxpayer data which would be better protected by more modern infrastructure.

21

The limitations of outdated technology are well understood by Treasury and the IRS. The Taxpayer First Act of 2019 included a push

to modernize information technology and move toward rebuilding IRS computer systems and implementing machine learning

approaches to help give tax enforcement agents a clearer picture of the most suspect filers.

22

The ability to make progress on these

eorts will be dependent on a sustained, timely multi-year budget commitment to cover the large fixed costs associated with

transitioning away from legacy systems toward a modern, integrated platform.

In addition to hindering compliance eorts, IRS technological deficiencies have broad consequences for taxpayer service as well.

The National Taxpayer Advocate reports that the IRS has struggled to provide adequate and reliable customer service. For example,

the IRS had the resources to answer only 29% of the 100 million telephone calls received in FY 2019, and during many months of the

COVID-19 pandemic, the combination of resource constraints and a shi to remote operations further complicated service eorts and

reduced service levels.

23

B. Budget Shortfalls Worsening over Time, Leading to a Decline in Enforcement Activity

The magnitude of the U.S. tax gap is the byproduct of many factors, including long-term IRS resource constraints. Since the early

2000s, the IRS budget as a share of GDP has been trending downward.

24

This decline masks the severity of the funding shortfall

because the pressure for enforcement resources due to a growth in sophisticated evasion opportunities is rising even more rapidly

than GDP. Examples of advanced evasion techniques include the use of foreign bank accounts to shield income from IRS scrutiny and

16 Ibid.

17 IRS, 2021. “Information Technology Annual Key Insights Report.” Publication 5453 (3-2021).

18 IRS, 2021. “IRS, Treasury Disburse 25 Million More Economic Impact Payments Under the American Rescue Plan,” IR-2021-77.

19 National Taxpayer Advocate, 2018. “Annual Report to Congress 2018.”

20 Rappeport, Alan. “IRS Website Crashes on Tax Day as Millions Tried to File Returns,” New York Times, April 17, 2018.

21 Treasury, 2019. “Treasury Announces IRS Integrated Modernization Business Plan Promoting Cost Eiciency, Improved Taxpayer Service, and Protection.”

22 IRS, 2018. “Criminal Investigation Annual Report 2018,” IRS-2018-219.

23 See National Taxpayer Advocate, 2019. “Annual Report to Congress 2019”; National Taxpayer Advocate, 2020. “Annual Report to Congress 2020.”

24 IRS Statistics of Income, 2019. “Table 31: Collection Costs, Personnel, and US Population,” Databook.

The American Families Plan Tax Compliance Agenda I 10

the adoption of international, intra-company dealings that shi income solely for tax purposes but can be made to appear legitimate

in ways challenging for the IRS to detect.

Over this same time period, there has been a rise in complex business structures, such as partnerships, which also require

significant eorts by IRS agents to obtain a complete understanding of interrelated business activities. Partnership income as

a share of total income grew from less than 5% to more than 35% since 1990. More than 4.2million partnership returns were

filed in calendar year 2018, which is more than double the number of corporate returns filed the same year; however, the IRS

audited only 140 of these returns.

25

Examining these returns is resource-intensive for the IRS because many partnerships use

tiered organizational structures where multiple levels of domestic and sometimes foreign business entities combine to obscure

the ultimate beneficiaries of the business operations. Some recent research suggests that 30% of partnership income cannot

unambiguously be traced to the ultimate owner.

26

The IRS, like all federal agencies, is best suited to provide the services Americans deserve when it has the resources it needs to do

so. At present, IRS funding deficiencies have directly resulted in an inability for the IRS to meet its mission of administering a fair and

eective tax system.

Despite preexisting needs to modernize outdated systems and to detect increasingly complex evasion, the last decade shows a

decrease—rather than an increase—in IRS resources. In real terms, the IRS’s overall budget declined by 18.5% between FY 2010 and

25 This translates to an audit rate of less than 0.00004%. Similarly, just 397 of the 4.8 million S-corporation returns were audited. IRS Statistics of Income, 2019.

“Table 17a: Examination Coverage and Recommended Additional Tax Aer Examination, by Type and Size of Return,” IRS Databook.

26 Cooper, Michael et al., 2016. “Business in the United States: Who Owns It, and How Much Tax Do They Pay?” Tax Policy and the Economy, 30(1): 91-128.

Figure 4: IRS Budget as Percent of GDP

0.0004

0.00045

0.0005

0.00055

0.0006

0.00065

0.0007

0.00075

0.0008

0.00085

0.0009

2000 2002 2004 2006 2008 2010 2012 2014 2016 2018 2020

IRS Budget as Per cent of GDP

0.090%

0.085%

0.080%

0.075%

0.070%

0.065%

0.060%

0.055%

0.050%

0.045%

0.040%

The American Families Plan Tax Compliance Agenda I 11

FY 2021.

27

The IRS’s enforcement budget decreased by 15% over this time period, leading to a 20% decline in the IRS workforce.

28

These losses have been most significant for revenue oicers who collect taxes (50% decrease) and revenue agents who audit

complex returns (35% decrease). Today, the IRS has fewer auditors than at any time since World War II.

29

As experienced employees

have retired, the IRS has been unable to replace departing workers with new revenue oicers and with agents of comparable training

and skills necessary to pursue the most complicated noncompliance cases.

Consequently, the share of audited returns has declined by nearly 45% between 2010–2018.

30

There has also been a contemporaneous

steep decline in audit rates across all filing categories. The share of corporate income tax, individual income tax, estate tax, and

employment tax returns examined by auditors have all dropped in the last decade.

Decline in Audit Rates by Filer Category

Filer Category

Percent Audited

Percent Decline

2010 2018

All Filers 0.93% 0.51% -45.39%

Individuals 1.11% 0.59% -46.30%

EITC recipients 2.39% 1.41% -41.10%

With annual income over $1 million 8.36% 3.23% -61.35%

$1 million - $ 5 million 6.67% 2.21% -66.87%

$5 million - $ 10 million 11.55% 4.21% -63.55%

$ 10 million + 18.38% 6.66% -63.76%

Corporations 1.39% 0.88% -36.54%

With assets over $20 billion 97.99% 49.29% -49.70%

Employment 0.21% 0.14% -33.63%

Estates 10.12% 8.60% -15.01%

With assets over $5 million 24.31% 18.71% -23.07%

Source: IRS Statistics of Income Databook. Audit rates by annual income are imputed from Table 9b; all other data are from Table 9a.

27 IRS Statistics of Income, 2019. “Table 31: Collection Costs, Personnel, and US Population,” IRS Databook; Congressional Research Service, 2021. “Internal Revenue

Service Appropriations, FY2021.”

28 IRS Statistics of Income, 2010. “Table 28: Costs Incurred by Budget Activity,” IRS Databook. IRS Statistics of Income, 2019. “Table 31: Collection Costs, Personnel,

and US Population,” IRS Databook.

29 Sarin, Natasha and Lawrence Summers, 2019. “Shrinking the Tax Gap: Approaches and Revenue Potential,” Tax Notes Federal, 18 November.

30 IRS Statistics of Income, 2019. “Table 17b: Examination Coverage: Recommended and Average Recommended Additional Tax Aer Examination,” IRS Databook.

IRS Statistics of Income, 2010. “Table 9a: Examination Coverage: Recommended and Average Recommended Additional Tax Aer Examination,” IRS Databook.

Table 2: Audit Rates, 2010 vs. 2018

The American Families Plan Tax Compliance Agenda I 12

The decreases in audit rates are most pronounced for highly complex audits performed by experienced agents. Among individual

taxpayers, audits of taxpayers with income over $1million have fallen by over 60% between 2010–2018, with the audit rate decreasing

from 8.4% to 3.2%.

31

Audit coverage for large corporations has been cut in half over the last decade. as coverage for companies with $20 billion or more in

assets decreased from 98% in FY 2010 to around 50%.

32

This is the result of sta attrition and budget stringency, which both diminish

the resources that the IRS can dedicate to auditing high-income taxpayers and large corporations. During the past 10-year period,

global high wealth examinations have taken roughly two years on average to complete and have averaged around 284 hours per

return. The same is true for partnerships, where audits average around 333 hours per return. In contrast, routine field audits of less

complex taxpayers average approximately 40 hours per return.

33

In order for the IRS to appropriately focus enforcement scrutiny on high-income taxpayers and the businesses they own—which

research has shown is a primary source of the tax gap—its budget must be replenished. IRS agents cannot simply be assigned to

global high wealth, partnership, or large and complex business examinations without the requisite skills, training, and experience

to analyze returns that are highly complex: For large corporations, the average number of pages per tax filing has risen from slightly

under 4,000 to nearly 6,000 since FY 2012.

34

The vast majority of taxpayers timely file their returns and pay the tax liabilities they owe. However, declining examination

coverage has real consequences. There is a direct correlation between the number of audits that the IRS is able to perform and

the revenue that the IRS collects from examinations.

35

In addition, if certain compliant taxpayers come to believe that there is

little to lose or much to gain from underpaying tax liabilities, overall compliance levels will decline.

36

Visible enforcement eorts

can help keep taxpayers compliant.

Falling revenue due to fewer audits imposes added real costs passed on to non-evaders. In the long run, either taxes must be raised

on compliers or government expenditures must be limited. The lack of enforcement thus leads to a de facto punitive tax on compliant

taxpayers as those who pay their fair share will have their taxes increased or government services reduced because evaders are not

paying. The costs can be particularly high for compliant direct competitors of tax evaders.

37

Evasion opportunities essentially impose

an even greater tax on compliant taxpayers because direct competitor businesses who abide by the tax laws are put at a competitive

disadvantage. As taxes rise to meet revenue needs, this disadvantage is made more pronounced since only law-abiding taxpayers bear

the burden of tax changes.

The consequences of these shortfalls have been exacerbated by expanding responsibility, as these consequential budget cuts have

been matched with calls for the IRS to take on new functions. While these new functions are related to the IRS’ core mission of tax

administration, the increased workload spreads limited resources even more thinly. Indeed, many parts of the Aordable Care Act

31 Ibid.

32 Ibid.

33 IRS data.

34 Ibid.

35 Sarin, Natasha and Lawrence Summers, 2019. “Shrinking the Tax Gap: Approaches and Revenue Potential,” Tax Notes Federal, 18 November.

36 Ibid.

37 Slemrod, Joel, 2007. “Cheating Ourselves: The Economics of Tax Evasion,” Journal of Economic Perspectives 21, 1 (2007): 25-48.

The American Families Plan Tax Compliance Agenda I 13

are administered through the IRS. And recently, the IRS has been pivotal in facilitating support for American families in the COVID-19

pandemic: For example, it has administered three rounds of Economic Impact Payments, most recently sending out over 160 million

payments totaling nearly $400 billion within weeks of the American Rescue Plan’s passage.

38

The IRS also has been charged by Congress

with providing periodic advance payments of the Child Tax Credit for the first time in history, and proposals in the American Families Plan

call on the IRS to administer credits that provide expanded support for families, childcare, and low-income individuals in the coming years.

C. Inequities in Tax Enforcement

Although the tax code redistributes income in a way that mitigates racial and income inequality, it also can function in ways that

exacerbate it.

39

Indeed, research has highlighted ways in which aspects of tax policy can advantage upper-income taxpayers, while

also identifying aspects that burden low-income individuals. In addition, scholars have increasingly focused on aspects of the tax

code that disadvantage Black and Hispanic families in particular.

40

IRS enforcement eorts can have similar eects. Recently, a stream of research has begun to identify disparities in tax enforcement

activities.

41

Historically, this inquiry has been complicated by the absence of data on taxpayers’ race or ethnicity.

42

The Biden Administration recently launched an Equitable Data Working Group that seeks to address these data limitations across

federal datasets. At the same time, the Treasury Department is currently undertaking research to study the relationship between

the tax code and racial inequities. This multi-year project will require close engagement between federal agencies and those in the

research and advocacy communities.

Over the last decade, a reduction in resources available to the IRS exacerbated inequities in predictable ways. In particular, diminished

resources made it diicult to maintain a cadre of the most specialized auditors, which in turn depressed audits rates for high-income

taxpayers relative to those in the lower part of the income distribution. Indeed, although audits of those claiming the Earned Income

Tax Credit (EITC), have fallen by around 40% since 2010, income tax audits of those earning $10 million or more annually have fallen

by closer to 65% (See Table 3).

While it is true that audit rates generally rise with income levels so that high earners are audited with a

greater probability than those of low or moderate income, the level dierences mask a significant shi in the trend.

Inequities in enforcement are not solely the result of a reduction in the number of audits of high-income taxpayers. Rules and

regulations governing tax procedures can advantage well-resourced and corporate taxpayers who have access to tax experts in ways

lower-income taxpayers do not. For instance, wealthy taxpayers oen rely on tax opinions provided by advisors to avoid penalties

and have their representatives negotiate terms to obtain more favorable outcomes.

43

38 Treasury, 2021. “More than 1.1 Million Additional Economic Impact Payments Disbursed Under the American Rescue Plan; Payments Total Approximately 164

Million,” IR-2021-103, 5 May.

39 For example, until recently, the vast majority of children living in poverty were ineligible for the Child Tax Credit (CTC). Because of the concentration of poverty in

minority communities, this meant that although three-quarters of white and Asian children were eligible for the full CTC, only about half of Black and Hispanic

children were. Goldin, Jacob and Katherine Michelmore. “Who Benefits from the Child Tax Credit?” National Tax Journal, forthcoming. The Biden Administration’s

reforms are focused on redressing this inequity.

40

Brown, Dorothy A. “The Whiteness of Wealth: How the Tax System Impoverishes Black Americans--And How We Can Fix It.” Crown Publishing Group, New York City, 2021.

41 Work by former IRS economist Kim Bloomquist points out that the five counties with the highest audit rates are predominantly African-American, rural counties in

the South. Bloomquist, Kim M. “Regional Bias in IRS Audit Selection.” Tax Notes Federal, March 4. A number of other promising research projects are underway.

42 Bearer-Friend, Jeremy, 2019. “Should the IRS Know Your Race? The Challenge of Colorblind Tax Data.” Tax L. Rev. 73 (2019): 1.

43 Blank, Joshua D., and Ari D. Glogower, 2021. “Progressive Tax Procedure.” 96 New York University Law Review, forthcoming. .

The American Families Plan Tax Compliance Agenda I 14

It is important to note that the President’s compliance proposals are designed to ameliorate existing inequities by focusing on

high-end evasion. Audit rates will not rise relative to recent years for those with less than $400,000 in actual income. This focus is

justified by the composition of the tax gap, which accrues disproportionately to those at the top of the distribution, who earn income

in opaque categories like partnership and proprietorship income, where misreporting rates are high. While the impact on racial

disparities from future enforcement eorts remains to be seen and will be the byproduct of a broader set of policy initiatives, the

Biden Administration’s commitment to racial equity was a key factor in the design of the current proposal.

For these reasons, investments in tax compliance do more than raise revenue to fund necessary investments or improve our fiscal

position. They also work to address inequities by increasing the share of IRS enforcement attention that is focused on high-income

noncompliers. Further, improvements in taxpayer services and other enhancements to tax administration such as the tighter

regulation of tax preparers can decrease disparities in the treatment of dierent groups of taxpayers.

IV. The President’s Compliance Proposals

The President’s proposals would overhaul tax administration in the United States to create a more equitable tax regime. These

proposals, taken as a whole, would generate revenue from taxes that are owed but not paid and through improved voluntary

compliance. Increased funding for the IRS would also improve how taxpayers are served by the IRS—making sure that all taxpayers

are able to take advantage of the tax benefits to which they are entitled and are able to communicate eectively and eiciently with

the IRS when questions arise.

The compliance initiative has several elements, including:

• increasing the resources of the IRS to pursue noncompliant taxpayers and better serve the vast majority who are

fully compliant;

• leveraging information that financial institutions already collect to shed light on those taxpayers who misreport income

derived from opaque categories;

• overhauling antiquated technology to help IRS leverage 21st century data analytic tools; and

• regulating paid tax preparers and increasing penalties for those who those who intentionally commit malfeasance.

While it will take time and substantial eort to achieve these goals, even modest progress would translate into a substantial increase

in revenue. Treasury’s Oice of Tax Analysis estimate that over the next decade, these changes would shrink the tax gap by about

10%, raising $700 billion in additional tax collections over the next 10 years net of investments. The revenue raised is even larger in

the second decade aer enactment at about $1.6 trillion. Revenue raised is backloaded in part because investments in the IRS oen

take several years to reach their ultimate payo.

The American Families Plan Tax Compliance Agenda I 15

In addition to raising substantial revenue, investments in tax compliance would improve the eiciency and fairness of the tax code.

Evasion imposes economic distortions because the resources taxpayers expend to implement and hide income from tax authorities

create no social benefits. Tax evasion also can shi economic activity into certain areas like proprietorship or cash-based businesses

due to their evasion advantage.

In addition, the same tax rates raise more revenue once evasion is made more diicult, and economic

distortions caused by disparate tax treatments of honest versus evasive businesses, among other examples, would be decreased.

Further, the tax code will be fairer when it no longer benefits opaque sources of income relative to wage labor. In sum, eectively

tackling tax evasion can decrease the amount of resources expended on underpaying tax liabilities, limit distortions, and encourage

more socially responsible behavior.

The uneven distribution of the tax gap implies that evasion contributes to aer-tax income inequality. Prior empirical evidence

demonstrates that the tax gap can be tied disproportionately to people in the top end of the income distribution,

44

and recent

research emphasizes the importance that income misreporting has for understanding income inequality trends.

45

Further,

asymmetric compliance rates between labor wage income and more opaque sources of income, especially for high-income earners,

has important horizontal and vertical equity implications. As such, the fairness and progressivity of the tax code can be enhanced

through more equal compliance rates that ensure those with high incomes pay what they owe.

44 See, e.g., Alm, James and Keith Finlay, 2013. “Who Benefits from Tax Evasion?” Economic Analysis & Policy, 43(2). This is true outside of the United States as well:

recent evidence in Scandinavia based on the Panama Papers revelations finds that although 3% of personal taxes are evaded on average, this figure rises close

to 30% in the top 0.01% of the distribution. Annette Alstadsæter, Niels Johannesen, and Gabriel Zucman, “Tax Evasion and Tax Avoidance,” Journal of Public

Economics (under review).

45 DeBacker, Jason et al., 2020. “Tax Noncompliance and Measures of Income Inequality,” Tax Notes Federal, 17 February; and Johns, Andrew and Joel Slemrod,

2010. “The Distribution of Income Tax Noncompliance,” National Tax Journal, 63(3).

91

99

190

-50

0

50

100

150

200

2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 2032 2033 2034 2035 2036 2037 2038 2039 2040 2041

Estimated Revenue ($, billions)

Compreh ensive Financial Account Reporting

Program Integrity Alloca tion Adjustment and Additional IRS Funding

Yearly Total Revenue

Comprehensive Financial Account Reporting

Program Integrity Allocation Adjustment and Additional IRS Funding

Yearly Total Revenue

Figure 5: Revenue Raised Each Year

IRS Compliance Proposals, FY 2022 - 2041 ($, billions)

NOTE: Estimates outside the 10-year budget window are subject to greater uncertainty which is reflected through the dotted line.

The American Families Plan Tax Compliance Agenda I 16

A. Restoring IRS Resources

The first step in the President’s eorts to restore IRS enforcement capability is a sustained, multi-year commitment to rebuilding

the IRS. This involves spending nearly $80 billion on IRS priorities over the course of the decade including hiring new specialized

enforcement sta, modernizing antiquated information technology, and investing in meaningful taxpayer service—including

the implementation of the newly expanded credits aimed at providing support to American families. Importantly, the additional

resources will go toward enforcement against those with the highest incomes, and audit rates will not rise relative to recent years for

those earning less than $400,000 in actual income.

The President’s proposal includes two components: a dedicated stream of mandatory funds ($72.5 billion over a decade) and a

program integrity allocation ($6.7 billion over a decade).

46

These mechanisms provide for a sustained, multi-year commitment to

revitalizing the IRS that will give the agency the certainty it needs to rebuild.

The IRS proposal includes year-by-year estimates of the additional resources that will be directed toward the agency as well as

the specific activities that these resources would support. The design ensures that the IRS is able to absorb and usefully deploy

additional resources over the entire 10-year horizon and keeps budget growth manageable at around 10 % per year.

Table 3: IRS Proposal and Revenue Raised, 2022–2031

Return on Investing in the IRS (inflation adjusted)

$M 2022 2023 2024 2025 2026 2027 2028 2029 2030 2031 Total

Mandatory

Cost 1,142 2,095 3,035 4,174 5,563 7,189 9,203 11,405 14,115 14,546 72,467

FTE 2,642 6,729 13,326 20,874 29,783 39,803 51,770 64,770 80,349 81,743

Direct Revenue - 631 3,098 6,959 12,435 19,758 29,903 40,730 53,721 63,780 231,015 3.2

Revenue Protected - - 214 603 1,402 2,584 4,178 6,211 8,532 11,157 34,881

Direct & Protected Revenue - 631 3,312 7,562 13,837 22,342 34,081 46,941 62,253 74,937 265,896 3.7

Program Integrity Cap Adjustment

Cost 417 647 643 660 677 694 712 731 750 769 6,700

FTE 2,555 5,109 5,109 5,109 5,109 5,109 5,109 5,109 5,109 5,109

Direct Revenue 334 1,690 2,826 3,538 4,099 4,565 4,954 5,279 5,554 5,794 38,633 5.8

Revenue Protected - 168 339 517 795 1,324 1,641 1,964 2,242 2,657 11,647

Direct & Protected Revenue 334 1,858 3,165 4,055 4,894 5,889 6,595 7,243 7,796 8,451 50,280 7.5

Mandatory and Cap Adjustment Combined

Cost 1,559 2,742 3,678 4,834 6,240 7,883 9,915 12,136 14,865 15,315 79,167

FTE 5,197 11,838 18,435

25,983 34,892 44,912 56,879 69,879 85,458 86,852

Direct Revenue 334 2,321 5,924 10,497 16,534 24,323 34,857 46,009 59,275 69,574 269,648 3.4

Revenue Protected - 168 553 1,120 2,197 3,908 5,819 8,175 10,774 13,814 46,528

Direct & Protected Revenue* 334 2,489 6,477 11,617 18,731 28,231 40,676 54,184 70,049 83,388 316,176 4.0

Return

Per Dollar

Invested

46 The congressional budget resolution allows for additional appropriations to the IRS in the form of be multi-year commitments to fund “program integrity”

activities that are estimated to save more than they cost, as is the case with IRS enforcement eorts.

The American Families Plan Tax Compliance Agenda I 17

The $6.7 billion program integrity allocation allows for increases in base discretionary funding for boosting eective enforcement of

taxpayer compliance. This eort will support the hiring and retention of at least 5,000 new enforcement personnel.

The mandatory funds are allocated over a 10-year horizon. They provide enforcement resources, including a significant investment

in revitalizing the IRS’s examination of large corporations, partnerships, and global high-wealth and high-income individuals.

Mandatory funds are also directed toward other important IRS priorities. For example, nearly $6 billion is dedicated to IT

modernization. Modernization funding will allow the IRS to address core technology challenges and transform IRS provision of

meaningful taxpayer services and tax enforcement eorts. Tax processing technology today is supported by an ineicient and

inflexible batch processing architecture that delays the provision of tax administration data to IRS systems, employees, and

taxpayers. Modernized technology will allow the IRS to make data more easily available for service and enforcement purposes and to

move toward near real-time tax processing. The existing case management system supported by more than 60 dierent components

could be integrated to provide a more comprehensive view of enforcement case information and taxpayer data and real-time tax

processing. The result would be a more interactive tax processing experience that will allow for an improved taxpayer experience and

for the IRS to focus resources on redressing noncompliance.

Additional IT tools will help support a sta capable of deploying new analytical techniques; investing in developing machine learning

capabilities will enable the IRS to leverage the information it collects to better identify tax returns for compliance review. The

proposed IT investment includes $4.5 billion to implement a new information reporting regime. New resources would also support

eorts to meet imminent threats to the security of the tax system, like cyberattacks.

Revitalizing the IRS requires more than building up the IRS’s enforcement eorts and technological systems. Revitalization

also demands a renewed commitment to meaningful taxpayer service. The President’s proposal will enable taxpayers to

communicate with the IRS securely and eiciently, and the IRS’s new workforce would include additional dedicated customer

service representatives ready to assist taxpayers as they navigate newly expanded programs like the Child Tax Credit, the Child and

Dependent Care Tax Credit, and the Earned Income Tax Credit.

Because the expansion in the IRS’s budget is phased in over a 10-year horizon, each year the IRS’s workforce should grow by no

more than a manageable 15%. By the end of the decade, however, the IRS’s budget would be roughly 40% above 2011 levels in real

terms as a result of this proposal.

47

This is a sizable increase, but a necessary one given that the IRS’s responsibilities have grown

dramatically over the intervening period. Yet even with this increase, the IRS budget would still not return to early 1990s levels as a

share of gross collections.

The IRS estimates the marginal return on investment (ROI) for most of its enforcement activity based on historical tax enforcement

data. Average ROIs for the mandatory and program integrity allocations are shown in Table 3 above. The Oice of Tax Analysis’ revenue

estimate for the IRS funding proposal is projected based on these ROI estimates. Total additional revenue generated from the $80 billion

increase in the IRS budget over 10 years is estimated to be around $320 billion during this horizon, which suggests roughly a 4-to-1 ROI.

These numbers are conservative because IRS ROI estimates are only available for the subset of enforcement investments, and not

technology or service improvements that are likely to improve compliance. As a result, revenue estimates do not take into account

increases in enforcement eiciency or taxpayer compliance that will arise from non-enforcement investments such as the benefits

47 This calculation assumes that the IRS discretionary budget over time will approximately resemble the real resource levels indicated by the FY 2022 discretionary

budget request.

The American Families Plan Tax Compliance Agenda I 18

of widespread use of machine learning technologies. Further, these estimates do not account for increases in voluntary compliance

attributable to improvements in taxpayer service. For example, when taxpayer questions are answered in a timely manner, taxes tend

to be paid more accurately plus the fact that an eective system of tax administration increases taxpayer trust and compliance.

48

Further, because standard IRS methodologies focus on enforcement cases and the associated revenue and costs, they are not

capable of arriving at an ROI for large-scale IT investments. Although researchers understand that the potential of better IRS

technology to improve collections eorts is sizable, these gains are diicult to attribute in revenue estimation.

Moreover, these estimates do not take into account the deterrent eects associated with dierent types of enforcement activities

which are generally considered to be quite significant.

49

More recent empirical work provides a way to start to try and understand the

importance of the indirect eects in understanding the revenue potential of compliance initiatives. A recent peer-reviewed study found,

for example, that increased income reported in the five to eight years following a random audit is about 1.5 times the audit revenue.

50

Another peer-reviewed study noted that in-person collection visits raise as much revenue from firms that share a tax preparer with

the visited firm as they do from the visited firm itself.

51

Although more research is needed to arrive at a better understanding of the

magnitude of deterrent eects, revenue estimates that fail to include noncompliance deterrence are conservatively low.

For the purposes of the Oice of Tax Analysis’ estimation, revenue is counted when it accrues to the IRS, and a collection stream for

enforcement revenue is built into these estimates: For example, even for an audit closed in FY 2022 with adjustments, collections

will be realized over time. This is part of the reason why revenue from this proposal is backloaded in the traditional 10-year budget

window. Further, estimates incorporate the fact that new hires take several years to reach their full potential. Revenue estimates also

assume a declining marginal return for enforcement activity as the level of enforcement rises. Revenue generated reaches its steady

state shortly aer the end of the 10-year horizon, and the backloaded nature of additional tax collections results in a second-decade

revenue estimate that is more than twice as large as the first (See Figure 5).

B. Increased Information Reporting

The second step in the compliance agenda involves shining light on opaque income streams, including proprietorship and

partnership business income. Bolstering information reporting is regarded by the IRS and GAO as one of the best ways to increase the

overall compliance rate,

52

and existing empirical evidence confirms that introducing third party reporting requirements is eective.

53

48 See, e.g. Williamson, Vanessa S. “Read My Lips: Why Americans are Proud to Pay Taxes.” Princeton University Press, 2017.

49 A longstanding Treasury estimate suggests that the deterrent eects of compliance activities are likely at least three times as large as the direct eects. IRS, 2018.

“Budget in Brief FY 2019.”

50 Jason DeBacker et al., 2018. “Once Bitten, Twice Shy? The Lasting Impact of Enforcement on Tax Compliance,” The Journal of Law and Economics, 61, 1 (2018).

51 Boning, William, et al., 2020. “Heard it through the grapevine: The direct and network eects of a tax enforcement field experiment on firms.” Journal of Public

Economics 190 (2020): 104261.

52 GAO, 2019. “Multiple Strategies are Needed to Reduce Noncompliance: Statement of James R. McTigue, Jr., Director, Strategic Issues,” GAO-19-558T, Washington,

DC: GAO, 2019; and IRS, 2019. “Understanding the Tax Gap and Taxpayer Noncompliance, Written Testimony of Dr. Benjamin D. Herndon, Chief Research and

Analytics Oicer, Internal Revenue Service, Before the House Ways and Means Committee on the Tax Gap.”

53 Pomeranz, Dina, 2015. “No Taxation Without Information: Deterrence and Self-Enforcement in the Value Added Tax.” American Economic Review, 105(8); Phillips,

Mark D., 2014. “Individual Income Tax Compliance and Information Reporting: What Do the US Data Show?” National Tax Journal, 67(3); Marchase, Carla,

2009. “Rewarding the Consumer for Curbing the Evasion of Commodity Taxes,” Public Finance Analysis, 65(4); Johannesen, Niels, 2014. “Tax Evasion and Swiss

Bank Deposits,” Journal of Public Economics, 111; Adhikari, Bibek et al., 2016. “Taxpayer Responses to Third-Party Income Reporting: Evidence From a Natural

Experiment in the Taxicab Industry,” IRS Research Bulletin, 6th Annual Joint Research Conference on Tax Administration, IRS and the Urban-Brookings Tax Policy

Center; Naritomi, Joana, 2019. “Consumers as Tax Auditors,” American Economic Review, 109(9). (See also Kleven, Henrik et al., 2011. “Unwilling or Unable to

The American Families Plan Tax Compliance Agenda I 19

Previous changes to information reporting shed light on the significant potential of such eorts but also on pitfalls that can arise

when reporting requirements are imprecisely designed. It is important to implement comprehensive information reporting regimes,

as partial reforms can simply shi tax evasion into other areas.

54

Further, financial institutions house a lot of valuable information,

and indeed already provide third-party reports to the IRS. Leveraging this information—rather than introducing new requirements for

taxpayers

55

—is a proven way to improve compliance.

56

The President’s proposal requires information reporting on financial accounts to increase the visibility of gross receipts and expenses

to the IRS. Today, business income is subject to limited information reporting. Current reporting of gross receipts exists for only

certain types of revenue, and there is no information reporting on deductible expenses. This is why the tax gap for partnership,

S-corporation, and proprietorship income is estimated at around $200 billion annually with the net misreporting percentage for

certain income categories exceeding 50%.

Third party information reporting is already provided on primary income streams for the vast majority of Americans, such as wage,

pension, and unemployment income. The President’s proposal would help make tax administration more equitable by subjecting

financial flows, especially those that accrue disproportionately to those at the top of the income distribution, to third-party

reporting as well.

The new reporting regime would build from the framework of the Form 1099-INT reports that taxpayers already receive from financial

institutions when they earn more than $10 in interest from a bank, brokerage, or other financial institution. Financial institutions

would simply report additional data on the financial accounts of these existing information returns. Specifically, the annual return

would report gross inflows and outflows on all business and personal accounts from financial institutions, including bank, loan, and

investment accounts but carve out exceptions for accounts below a low de minimis gross flow threshold.

57

Other accounts that are similarly situated to financial institution accounts would also be covered under this new reporting regime—

for example, payment settlement entities would also be required to report gross receipts and gross purchases. The reporting regime

would also cover foreign financial institutions and crypto asset exchanges and custodians.

Cheat? Evidence from a Tax Audit Experiment in Denmark,” Econometrica, 79(3), finding that the tax evasion rate is close to zero for income subject to third-party

reporting, but substantial for self-reported income.)

54

For example, the introduction of Form 1099-K provided the IRS and taxpayers with information about businesses’ sales by payment card and other electronic means.

As a result, taxpayers increased reported receipts by up to 24% once they began to believe that the IRS could conceivably verify gross receipts. However, many business

taxpayers appeared to oset this change with simultaneously increased reported expenses. Slemrod, Joel et al., 2017, “Does Credit Card Information Reporting

Improve Small-Business Tax Compliance?” Journal of Public Economics, 149. See also Adhikari, Bibek et al., 2020. “Information Reporting and Tax Compliance,” AEA

Papers and Proceedings, 110.

55 As part of the Aordable Care Act, a new provision was introduced which would have required businesses to send Form 1099 information returns for all purchases

of goods and services over $600. It was set to go into eect in 2012 but repealed six months prior to enactment because of a concern about the burden imposed

on small businesses. National Taxpayer Advocate, 2010. “Fiscal Year 2011 Objectives Report to Congress.”

56 For example, in the international sphere, the Foreign Account Tax Compliance Act (FATCA) was enacted in 2010 to help combat tax evasion by those with oshore

accounts. Although it is diicult to draw full conclusions given the nascency of these eorts, research suggests that financial institutions play an important role in

providing information to the IRS that encourages increased compliance. De Simone, Lisa, Rebecca Lester, and Kevin Markle, 2020. “Transparency and Tax Evasion:

Evidence from the Foreign Account Tax Compliance Act (FATCA).” Journal of Accounting Research 58(1). This is in part attributable to amnesty programs that

were implemented around the same time as new reporting requirements and precipitated a significant increase in self-reported foreign dealings. Johannesen,

Niels, et al., 2020. “Taxing Hidden Wealth: the Consequences of US Enforcement Initiatives on Evasive Foreign Accounts,”American Economic Journal: Economic

Policy12(3).

57 The proposal preserves significant flexibility for the Secretary and the IRS to design the new reporting requirements in the way that will be most eective for tax

compliance eorts.

The American Families Plan Tax Compliance Agenda I 20

These new reporting requirements would come with no additional reconciliation requirement for taxpayers. For already compliant

taxpayers, the only eect of this regime is to provide easy access to summary information on financial accounts and to decrease the

likelihood of costly “no fault” examinations once the IRS is able to better target its enforcement eorts. For noncompliant taxpayers,

this regime would encourage voluntary compliance as evaders realize that the risk of evasion being detected has risen noticeably.

To arrive at a revenue estimate for the impact of a comprehensive information reporting regime, the Oice of Tax Analysis began

with an estimate of the tax gap for business income which included Schedule C proprietorship income, Schedule E rent and pass-

through income, and small corporation income as well as the portion of the employment tax gap associated with business incomes.

This tax gap estimate was then reduced to reflect the expected increase in voluntary compliance once taxpayers realize that the IRS

has a lens into business income. The revenue estimate added two assumptions: first, a reduction in the steady state share of the tax

gap due to increased voluntary compliance as taxpayers react to increased information reporting; and second, a gradual increase of

voluntary compliance that phases in over time.

The revenue estimates assume that the bank reporting proposal will become eective for tax year 2023, building in implementation

time for the IRS and for financial institutions. The Administration would concurrently seek out ways to reduce any new burden on

financial institutions associated with this information reporting requirement.

This additional information reporting would also enhance the eectiveness of enforcement measures, as it will provide a proxy measure

for a taxpayer’s potential income position, and suspect account flows could help the IRS better target its enforcement activities. This

would benefit compliant taxpayers, whose risk of costly no-fault audits would decrease as the IRS better targets enforcement actions.

According to the Oice of Tax Analysis, the increase in compliance that would result from this new reporting regime is estimated to

raise $460 billion over the next decade.

Challenges of Cash and Virtual Currencies

For a new information reporting regime to shed light on previously opaque income sources eectively, it is imperative to prevent

business income from being shielded from reporting requirements. This is why the new Form 1099 reports would also be required

from payment services providers so that businesses cannot shi out of traditional financial institutions to other kinds of platforms

and avoid making their income visible to the IRS.

Another concern is that an information reporting regime will shi taxpayers toward a greater use of cash. Although information

reporting may push some taxpayers to transact more in cash to avoid the reporting, it is unlikely that a substantial share of the

business tax gap will move to cash-based transactions. Businesses already have incentives to use cash as much as possible to

avoid detection via bank statements obtained in an audit, but there are practical barriers—such as security risks and the diiculty

of spending large amounts of cash for certain transactions—to expanding the use of cash without depositing it in a bank account.

Still another significant concern is virtual currencies, which have grown to $2 trillion in market capitalization.

58

Cryptocurrency

already poses a significant detection problem by facilitating illegal activity broadly including tax evasion.

59

58 Chavez-Dreyfuss, Gertrude. “Crypto Market Cap Surges to Record $2 Trillion, Bitcoin at $1.1 Trillion,” Reuters, April 5, 2021.

59 Early work suggested the significance of the challenges posed by the rise of virtual currencies: “To the extent that cryptocurrencies continue to gain momentum;

we could reasonably expect tax evaders—who traditionally executed their tax-evasion techniques through the use of oshore bank accounts in tax-heaven

jurisdictions—to opt out of traditional tax havens in favor of cryptocurrencies.” See, e.g. Marian, Omri, 2013. “Are Cryptocurrencies Super Tax Havens,”Michigan

The American Families Plan Tax Compliance Agenda I 21

This is why the President’s proposal includes additional resources for the IRS to address the growth of cryptoassets. Despite

constituting a relatively small portion of business income today, cryptocurrency transactions are likely to rise in importance in the next

decade, especially in the presence of a broad-based financial account reporting regime. Within the context of the new financial account

reporting regime, cryptocurrencies and cryptoasset exchange accounts and payment service accounts that accept cryptocurrencies

would be covered. Further, as with cash transactions, businesses that receive cryptoassets with a fair market value of more than $10,000

would also be reported on. Although cryptocurrency is a small share of current business transactions, such comprehensive reporting is

necessary to minimize the incentives and opportunity to shi income out of the new information reporting regime.

60

C. Other Compliance Proposals

The Administration’s compliance proposals include a number of other additional tools for the IRS that complement the

transformational nature of the investments and information reporting regime discussed above.

For example, the proposal provides the IRS with the authority to regulate and establish minimum competency standards for all

paid tax preparers.

61

Unregulated preparers submit more tax returns than all other preparers combined, and they oen make costly

mistakes that subject their customers to audits.

62

A recent GAO study shed light on the scope of this problem. During undercover visits

to 19 randomly selected unregulated preparers, only two calculated taxpayers’ refunds accurately.

63

The issues of unregulated tax

preparers go beyond the quality of services provided. Some unregulated preparers enrich themselves by ascribing to themselves a

portion of taxpayers’ refunds; or they commit fraud while failing to sign returns (so called, “ghost preparers”), leaving the taxpayers

who are audited without the ability to prove that fraudulent returns are the fault of unscrupulous preparers.

64

In addition to

establishing standards for unregulated tax preparers, the President’s proposal would include additional penalties for ghost preparers.

Other proposals identify opportunities in several areas to strengthen tax collection. An additional change would improve taxpayer

information accuracy by permitting the IRS to require payment recipients to certify their taxpayer identification numbers (TINs)

to payers who issue third-party information reports; another proposal imposes unpaid corporate tax liability on shareholders in

specified tax shelter cases.