UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2017

OR

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF

1934

For the transition period from to

Commission File Number Registrant; State of Incorporation; Address and Telephone Number

IRS Employer

Identification No.

001-38126

38-3980194

Altice USA, Inc.

Delaware

1 Court Square West

Long Island City, New York 11101

(516) 803-2300

Securities registered pursuant to section 12(b) of the Act:

Title of each class

Name of exchange which registered

Class A Common Stock, par value $.01

New York Stock Exchange

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No ý

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No ý

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No

o

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and

posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrants were required to submit

and post such files). Yes ý No o

Indicate by a check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of

the Registrants' knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether each Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth

company. See the definitions of "large accelerated filer", "accelerated filer", "smaller reporting company", and "emerging growth company" in Rule 12b-2 of the Exchange Act.

(Check one):

Large accelerated filer o

Accelerated filer o

Non-accelerated filer ý

Smaller reporting company o

(Do not check if a smaller reporting company)

Emerging growth company o

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial

accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes o No ý

Aggregate market value of the voting and non-voting common equity held by non-affiliates of Altice USA, Inc. computed by reference to the price at which the common equity

was last sold on the New York Stock Exchange as of June 30, 2017:$3,712,484,222

Number of shares of common stock outstanding as of February 16, 2018:

Class A common stock, par value $0.01 246,982,292

Class B common stock, par value $0.01 490,086,674

Documents incorporated by reference - Altice USA, Inc. intends to file with the Securities and Exchange Commission, not later than 120 days after the close of its fiscal year, a

definitive proxy statement or an amendment to this report filed under cover of Form 10-K/A containing the information required to be disclosed under Part III of Form 10-K.

TABLE OF CONTENTS

Page

Part I

1. Business 2

1A. Risk Factors 20

1B. Unresolved Staff Comments 43

2. Properties 43

3. Legal Proceedings 44

4. Mine Safety Disclosures 44

Part II

5. Market for the Registrants' Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities 44

6. Selected Financial Data 46

7. Management's Discussion and Analysis of Financial Condition and Results of Operations 50

7A. Quantitative and Qualitative Disclosures About Market Risk 81

8. Financial Statements and Supplementary Data 82

9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure 82

9A. Controls and Procedures 82

9B. Other Information 82

Part III

10. Directors and Executive Officers and Corporate Governance *

11. Executive Compensation *

12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholders Matters *

13. Certain Relationships and Related Transactions, and Director Independence *

14. Principal Accountant Fees and Services *

Part IV

15. Exhibits and Financial Statement Schedules 83

* Some or all of these items are omitted because Altice USA, Inc. intends to file with the Securities and Exchange Commission, not later than 120 days after the close of its

fiscal year, a definitive proxy statement or an amendment to this report filed under cover of Form 10-K/A containing the information required to be disclosed under Part III

of Form 10-K.

1

PART I

Item 1. Business

Altice USA, Inc. ("Altice USA" or the "Company") was incorporated in Delaware on September 14, 2015. As of December 31, 2017, Altice USA was majority‑owned by

Altice N.V., a public company with limited liability (naamloze vennootshcap) under Dutch law ("Altice N.V." and Altice N.V. and its subsidiaries, the "Altice Group"). Upon

the completion of the Altice N.V. distribution discussed below, the Company will no longer be majority-owned by Altice N.V.

Altice USA is one of the largest broadband communications and video services providers in the United States. We deliver broadband, pay television, telephony services,

proprietary content and advertising services to approximately 4.9 million residential and business customers. Our footprint extends across 21 states through a fiber-rich

broadband network with more than 8.6 million homes passed as of December 31, 2017.

We acquired Cequel Corporation ("Suddenlink" or "Cequel") on December 21, 2015 and Cablevision Systems Corporation ("Optimum" or "Cablevision") on June 21,

2016. These acquisitions are referred to throughout this document as the "Suddenlink Acquisition" (or the "Cequel Acquisition") and the "Optimum Acquisition (or the

"Cablevision Acquisition"), respectively, and collectively as the "Acquisitions." We are a holding company that does not conduct any business operations of our own. We serve

our customers through two business segments: Optimum, which operates in the New York metropolitan area, and Suddenlink, which principally operates in markets in the

south-central United States.

Following the Acquisitions, we began to simplify our organizational structure, reduce management layers, streamline decision-making processes and redeploy resources

with a focus on network investment, customer service enhancements and marketing support. As a result, we have made significant progress in integrating the operations of

Optimum and Suddenlink, centralizing our business functions, reorganizing our procurement processes, eliminating duplicative management functions, terminating lower-

return projects and non-essential consulting and third-party service arrangements, and investing in our employee relations and our culture. Improved operational efficiency has

allowed us to redeploy physical, technical and financial resources towards upgrading our network and enhancing the customer experience to drive customer growth. This focus

is demonstrated by reduced network outages since the Acquisitions, which we believe improves the consistency and quality of the customer experience. In addition, we have

expanded, and intend to continue expanding, our e-commerce channels for sales and marketing.

Since the Acquisitions, we have quadrupled the maximum available broadband speeds we are offering to our Optimum customers from 101 Mbps to 400 Mbps for

residential customers and 450 Mbps for business customers and expanded our 1 Gbps broadband service to approximately 72% of our Suddenlink footprint from approximately

40% prior to the Suddenlink Acquisition. In addition, we have commenced a plan to build a fiber-to-the-home ("FTTH") network, which will enable us to deliver more than 10

Gbps broadband speeds across our entire Optimum footprint and part of our Suddenlink footprint. We believe this FTTH network will be more resilient with reduced

maintenance requirements, fewer service outages and lower power usage, which we expect will drive further cost efficiencies in our business. In order to further enhance the

customer experience, during the fourth quarter, we introduced a new home communications hub, Altice One, and we have begun rolling it out across our Optimum footprint.

Our new home communications hub is an innovative, integrated platform with a dynamic and sophisticated user interface, combining a set-top box, Internet wireless router and

cable modem in one device, and is our most advanced home communications hub. We are also beginning to offer managed data and communications services to our business

customers and more advanced advertising services, such as targeted multi-screen advertising and data analytics, to our advertising and other business clients. In the fourth

quarter of 2017, we and Sprint Corporation ("Sprint") entered into a multi-year strategic agreement pursuant to which we will utilize Sprint's network to provide mobile voice

and data services to our customers throughout the nation, and our broadband network will be utilized to accelerate the densification of Sprint's network. We believe this

additional product offering will enable us to deliver greater value and more benefits to our customers.

2

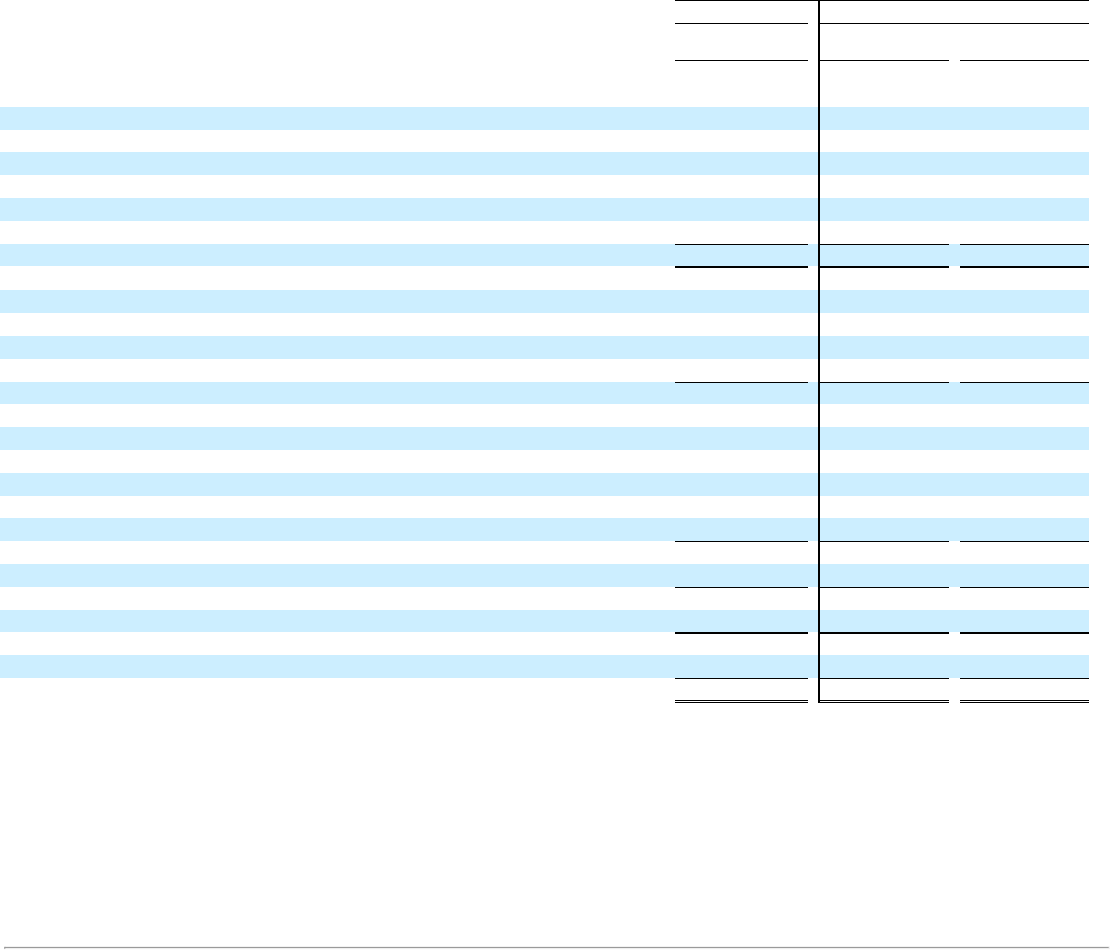

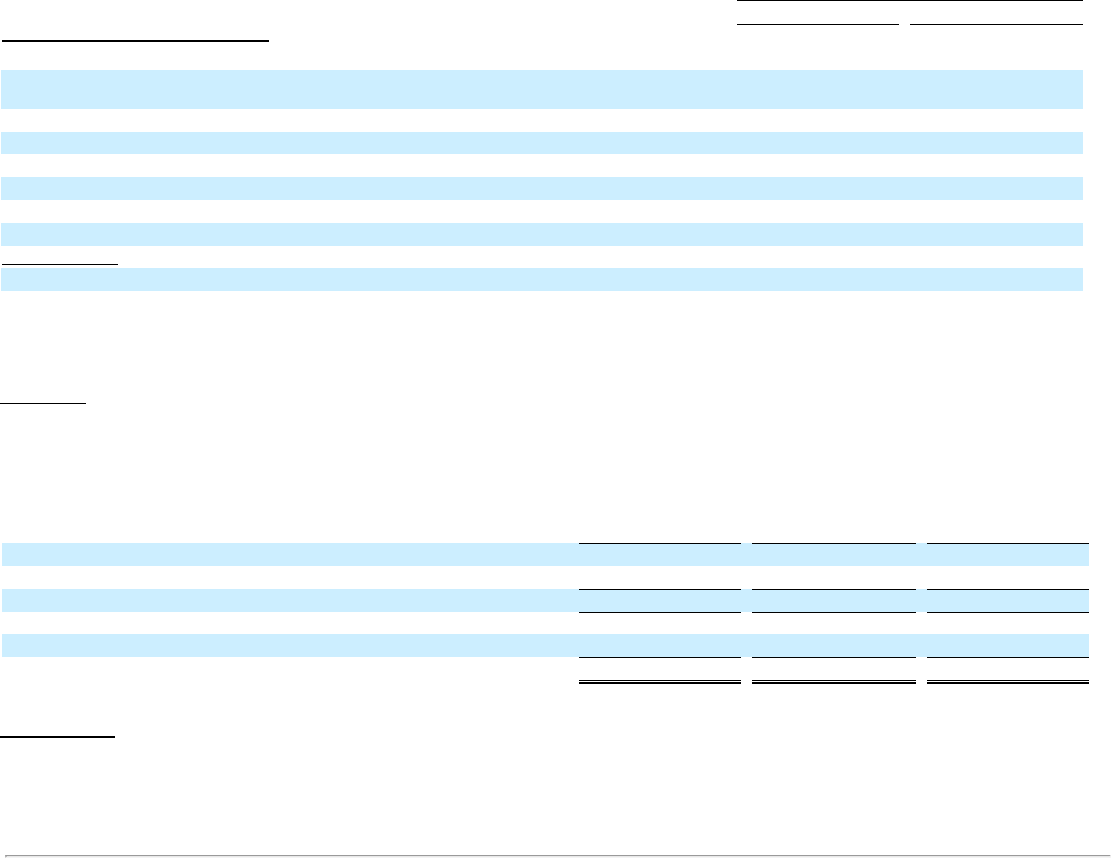

The following table presents certain financial data and metrics for the Company and its segments:

Years ended December 31,

Altice USA

Optimum Segment

Cequel Segment

(in thousands except percentage data) 2017

2016 (a)

2017

2016 (b)

2017

2016

Customer Relationships 4,906

4,892

3,156

3,141

1,750

1,751

% growth 0.3%

0.5%

(0.1)%

Revenue $ 9,326,570

$ 6,017,212

$ 6,664,788

$ 3,444,052

$ 2,664,574

$ 2,573,160

Adjusted EBITDA (c) $ 4,005,690

$ 2,414,735

$ 2,751,121

$ 1,259,844

$ 1,254,569

$ 1,154,891

% of Revenue 42.9%

40.1%

41.3%

36.6%

47.1 %

44.9%

Adjusted EBITDA less capital expenditures (c) $ 3,014,326

$ 1,789,194

$ 2,039,689

$ 961,487

$ 974,637

$ 827,707

% of Revenue 32.3%

29.7%

30.6%

27.9%

36.6 %

32.2%

Net income (loss) attributable to stockholders (d) $ 1,520,031

$ (832,030)

(a) The 2016 amounts for Altice USA include the operating results of Cablevision from the date of the Cablevision

Acquisition.

(b) Amounts reflect the operating results of Cablevision from the date of the Cablevision Acquisition and include results for Newsday Media Group ("Newsday"). Altice USA sold a 75%

stake in Newsday in July 2016. Newsday's revenue, for the period from June 21, 2016 through its sale in July 2016, was approximately $8.8 million.

(c) For additional information regarding Adjusted EBITDA, including a reconciliation of Adjusted EBITDA to Net Income (Loss), please refer to "Management's Discussion and Analysis of

Financial Condition and Results of Operations."

(d) Pursuant to the enactment of the Tax Cuts & Jobs Act ("Tax Reform") on December 22, 2017, the Company recorded a noncash deferred tax benefit of $2,337,900 to remeasure the net

deferred tax liability to adjust for the reduction in the corporate federal income tax rate from 35% to 21% which is effective on January 1, 2018.

Altice N.V. Distribution

On January 8, 2018, Altice N.V. announced plans for the separation of the Company from Altice N.V. Altice N.V. will distribute substantially all of its equity interest in the

Company through a distribution in kind to holders of Altice N.V.'s common shares A and common shares B (the “Distribution”). Following the Distribution, Altice N.V. will no

longer own a controlling equity interest in the Company, and the Company will operate independently from Altice N.V. Altice N.V. is ultimately controlled by Patrick Drahi

through Next Alt S.a.r.l. (‘‘Next Alt’’). As of December 31, 2017, Next Alt held 60.31% of the outstanding share capital and voting rights of Altice N.V., representing 49.5% of

the economic rights and 66% of the voting power in general meetings. Mr. Drahi has informed us that Next Alt will elect to receive 100% of the shares of Altice USA to which

it is entitled in the Distribution in the form of Altice USA Class B common stock and will be subject to proration, in the same manner as other Altice N.V. shareholders, in the

event the number of shares of Altice USA Class B common stock elected to be received by Altice N.V. shareholders exceeds a cap of 247.7 million shares (the "Class B Cap").

As a result of Next Alt’s intended election, and voting agreements that Next Alt will enter into with certain members of Altice N.V. and Altice USA management with respect to

all shares of Altice USA common stock they own, Mr. Drahi will control Altice USA immediately after giving effect to the Distribution regardless of the elections made by

other Altice N.V. shareholders.

The implementation of the Distribution is expected to be subject to certain conditions precedent being satisfied or waived. Although Altice N.V. and the Company have not yet

negotiated the final terms of the Distribution and related transactions, the Company expects that the following will be conditions to the Distribution:

•Approval of Altice N.V. shareholders of (i) the distribution in kind and (ii) the board resolution approving the change in identity and character of the business of Altice

N.V. resulting from the Distribution;

•Receipt of certain U.S. regulatory approvals, which could take up to 180

days;

•The Registration Statement filed on January 8, 2018, as amended, being declared effective by the U.S. Securities and Exchange Commission (the

‘‘Commission’’);

3

•The entry into a separation agreement (the "Master Separation Agreement") and the entry into, amendments to or termination of various arrangements between Altice

N.V. and the Company, such as a license to use the Altice brand, the stockholders’ agreement among Altice USA, Altice N.V. and certain other parties and the

management agreement pursuant to which the Company pays a quarterly management fee to Altice N.V.; and

•The declaration and payment of a one-time $1.5 billion dividend to Altice USA stockholders as of a record date prior to the Distribution (the ‘‘Pre-Distribution

Dividend’’).

Prior to Altice N.V.'s announcement of the Distribution, the Board of Directors of Altice USA, acting through its independent directors, approved in principle the payment of

the Pre-Distribution Dividend to all shareholders immediately prior to completion of the separation. Formal approval of the Pre-Distribution Dividend and setting of a record

date are expected to occur in the second quarter of 2018. The payment of the Pre-Distribution Dividend will be funded with available Cablevision revolving facility capacity and

available cash from new financings, completed in January 2018, at CSC Holdings LLC ("CSC Holdings"), a wholly-owned subsidiary of Cablevision. In addition, the Board of

Directors of Altice USA has authorized a share repurchase program of $2.0 billion, effective following completion of the separation.

Our Products and Services

We provide broadband, pay television and telephony services to both residential and business customers. We also provide enterprise-grade fiber connectivity, bandwidth

and managed services to enterprise customers through Optimum’s Lightpath business (also marketed as Altice Business) and advertising time to advertisers.

The prices we charge for our services vary based on the number of services and associated service level or tier our customers choose, coupled with any promotions we may

offer. As part of our marketing strategy our customers are increasingly choosing to bundle their subscriptions to two (‘‘double product’’) or three (‘‘triple product’’) of our

services at the same time. Customers who subscribe to a bundle generally receive a discount from the price of buying each of these services separately, as well as the

convenience of receiving multiple services from a single provider, all on a single monthly bill. For example, we offer an ‘‘Optimum Triple Play’’ package that is a special

promotion for new customers or eligible current customers where Optimum broadband, pay television and telephony services are each available at a reduced rate for a specified

period when purchased together. Approximately 50% of our residential customers were triple product customers as of December 31, 2017.

Residential Services

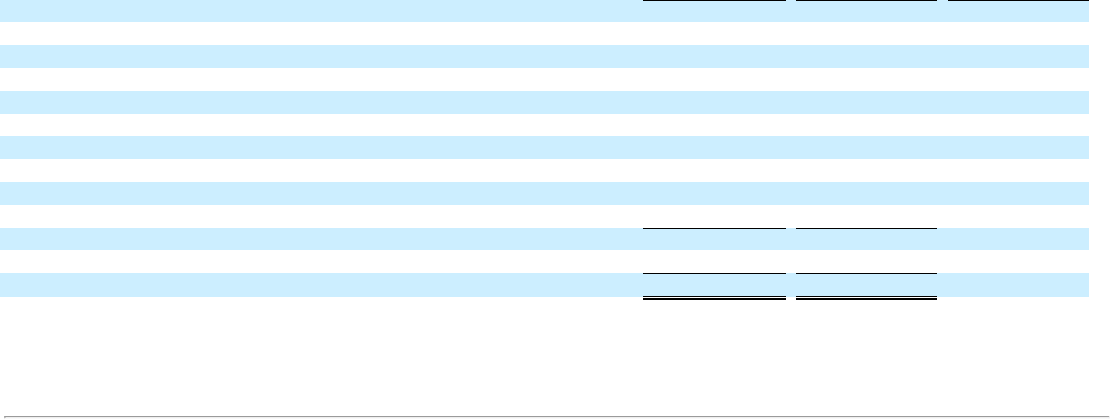

We offer broadband, pay television and telephony services to residential customers through both our Optimum and Suddenlink segments. The following tables show our

residential customer relationships and revenues by service offerings for each of our Optimum and Suddenlink segments as well as on a combined basis.

December 31, 2017

December 31, 2016

Optimum

Suddenlink

Total

Optimum

Suddenlink

Total

(in thousands)

Total Residential customers relationships 2,893

1,642

4,535

2,879

1,649

4,528

Pay TV 2,363

1,042

3,406

2,428

1,107

3,535

Broadband 2,670

1,376

4,046

2,619

1,344

3,963

Telephony 1,965

592

2,557

1,962

597

2,559

December 31, 2017

December 31, 2016

Optimum

Suddenlink

Total

Optimum

Suddenlink

Total

(dollars in thousands)

Residential revenue:

Pay TV $ 3,113,238

$ 1,101,507

$ 4,214,745

$ 1,638,691

$ 1,120,525

$ 2,759,216

Broadband 1,603,015

960,757

2,563,772

782,615

834,414

1,617,029

Telephony 693,478

130,503

823,981

376,034

153,939

529,973

4

Broadband Services

We offer a variety of broadband service tiers tailored to meet the different needs of our residential customers. Current customer offers include four tiers with download

speeds ranging from 60 Mbps to 400 Mbps for our Optimum residential customers and 50 Mbps to 1 Gbps for our Suddenlink residential customers. Our broadband services

also include the Optimum wireless router, as well as Internet security software, including anti-virus, anti-spyware, personal firewall and anti-spam protection. Substantially all

of our hybrid fiber-coaxial ("HFC") network is digital and data over cable service interface specification ("DOCSIS") 3.0 compatible, with approximately 275 homes per node

and a bandwidth capacity of at least 750 MHz throughout. This network allows us to provide our customers with advanced broadband, pay television and telephony services.

Since the Acquisitions, we have quadrupled the maximum available broadband speeds we are offering to our Optimum customers from 101 Mbps to 400 Mbps for residential

customers and 450 Mbps for business customers and expanded our 1 Gbps broadband service to approximately 72% of our Suddenlink footprint from approximately 40% prior

to the Suddenlink Acquisition. We have also commenced a plan to build a FTTH network, which will enable us to deliver more than 10 Gbps broadband speeds across our

entire Optimum footprint and part of our Suddenlink footprint.

In addition, we have deployed Wi-Fi across our Optimum service area with approximately 2.1 million Wi-Fi hotspots as of December 31, 2017. The Optimum Wi-Fi

network allows Optimum broadband customers to access the service while they are away from their home or office. Wi-Fi is delivered via wireless access points mounted on

our Optimum broadband network, in certain retail partner locations, certain NJ Transit rail stations, New York City parks and other public venues. Similarly, our "Optimum

wireless router" product includes a second network that enables all Optimum broadband customers to access the Optimum Wi-Fi network. Access to the Optimum Wi-Fi

network is offered as a free value-added benefit to Optimum broadband customers and for a fee to non-customers in certain locations. Our Wi-Fi service also allows our

Optimum broadband customers to access the Wi-Fi networks of Comcast Corporation ("Comcast"), Charter Communications, Inc. ("Charter")(within the legacy Time Warner

Cable and Bright House Networks footprints) and Cox Communications. Through these relationships we offer our Optimum customers access to approximately 350,000

additional hotspots nationwide.

Pay Television Services

We currently offer a variety of pay television services, which include delivery of broadcast stations and cable networks, and advanced digital pay television services, such

as video-on-demand ("VOD"), high-definition ("HD") channels, digital video recorder ("DVR") and pay-per-view, to our residential markets. Depending on the market and

level of service, our pay television services include, among other programming, local broadcast networks and independent television stations, news, information, sports and

entertainment channels, regional sports networks, international channels and premium services such as HBO, Showtime, Cinemax and The Movie Channel. Our residential

customers pay a monthly charge based on the pay television programming level of service, tier or package they receive and the type of equipment they select. Customers who

subscribe to seasonal sports packages, international channels and premium services may be charged an additional monthly amount. We may also charge additional fees for pay-

per-view programming, DVR and certain VOD services.

As of December 31, 2017, Optimum residential customers were able to receive up to 605 digital channels and Suddenlink residential customers were able to receive up to

438 digital channels depending on their market and level of service. Optimum offers up to 174 HD channels and Suddenlink offers up to 139 HD channels, which represent the

most widely watched programming, including all major broadcast networks, as well as most leading national cable networks, premium channels and regional sports networks.

HDTV features high-resolution picture quality, digital sound quality and a wide-screen, theater-like display when using an HDTV set and an HD-capable converter. We also

continue to launch additional HD channels to continuously improve our customer's viewing experience. As of December 31, 2017, approximately 95% of our residential

Optimum pay television customers subscribe to HDTV services. As of December 31, 2017, approximately 81% of Suddenlink pay television customers were digital pay

television customers and approximately 95% of those digital pay television customers subscribe to HDTV services.

We also provide advanced services, such as pay-per-view and VOD, that give residential pay television customers control over when they watch their favorite

programming. Our pay-per-view service allows customers to pay to view single showings of programming on an unedited, commercial-free basis, including feature films, live

sporting events,

5

concerts and other special events. Our VOD service provides on-demand access to movies, special events, free prime time content and general interest titles. Subscription-based

VOD premium content such as HBO and Showtime is made available to customers who subscribe to one of our premium programming packages. Our customers have the

ability to start the programs at whatever time is convenient, as well as pause, rewind and (for most content) fast forward both standard definition and HD VOD programming.

As of December 31, 2017, pay-per-view services were available for all Optimum and 99% of Suddenlink pay television customers and VOD services were available to all of our

Optimum pay television customers and 95% of our Suddenlink pay television customers, and we offered thousands of HD titles on-demand for Optimum and Suddenlink

customers, respectively.

For a monthly fee, we offer DVR services through the use of digital converters, the majority of which are HDTV-capable and have video recording capability. As of

December 31, 2017, approximately 50% of our residential Optimum pay television customers and 37% of our Suddenlink pay television customers utilized DVR services.

Optimum customers can choose either a set-top box DVR with the ability to record, pause and rewind live television or the Cloud DVR Plus with remote-storage capability to

record 15 shows simultaneously while watching any live or pre-recorded show, and pause and rewind live television. Depending on the market, Suddenlink customers have the

option to use a set-top box DVR or a TiVo HD/DVR converter, which delivers multi-room DVR capability using TiVo Mini devices that allow customers to pause and rewind

live television, manage recordings from different television locations and play them back throughout the home. In addition, TiVo Stream service, which allows customers to

stream live television channels and recorded programming wirelessly throughout their home to Android and iOS devices, and, subject to copyright restrictions, download

previously recorded content to these devices so that it can be viewed outside the home, is provided to current TiVo DVR customers.

We also introduced a new home communications and entertainment hub during the fourth quarter of 2017, Altice One, which is our most advanced home hub, and we have

begun rolling it out across our Optimum footprint. This new hub is an innovative, integrated platform with a dynamic and sophisticated user interface, combining a set-top box,

Internet wireless router and cable modem in one device. It is based on LaBox, which Altice N.V. has successfully deployed in France, the Dominican Republic and Israel, and is

initially offered to new customers subscribing to our double and triple-product packages. It is capable of delivering broadband Internet, Wi-Fi, digital television services, over-

the-top ("OTT") services and fixed-line telephony and supports 4K video and a remote-storage DVR with the capacity to record 15 television programs simultaneously and the

ability to rewind live television on the last two channels watched. Additional features include a point-anywhere voice-command remote control and a companion mobile app

that allows viewing of all television content including DVR streaming. Additional televisions will be paired with "minis," which can also act as Wi-Fi extenders for an advanced

Wi-Fi experience throughout the home.

We also offer alternative viewing platforms for our pay television programming through mobile applications. Our Optimum customers have access to Optimum App,

available for the iPad, iPhone, iPod touch, personal computers, Kindle Fire and select Android phones and tablets, and our Suddenlink customers have access to

Suddenlink2GO, available for personal computers and select phones and tablets. Depending on the platform, the Optimum App features include the ability to watch live

television, stream on-demand titles from various networks and use the device as a remote to control the customer's digital set-top box while inside the home. Suddenlink2GO

enables Suddenlink customers to watch over 300,000 movies, shows and clips from over 200 networks on a personal computer once authenticated via the Suddenlink customer

portal and select television shows and movies on their mobile devices.

Telephony Services

Through voice over Internet protocol ("VoIP") telephone service we also offer unlimited local, regional and long-distance calling within the United States, Puerto Rico,

Virgin Islands and Canada for a flat monthly rate, including popular calling features such as caller ID with name and number, call waiting, three-way calling, enhanced

emergency 911 dialing and television caller ID. We also offer additional options designed to meet our customers' needs, including directory assistance, voicemail services and

international calling. Discount and promotional pricing are available when our telephony services are combined with our other service offerings.

Mobile

In the fourth quarter of 2017, we and Sprint entered into a multi-year strategic agreement pursuant to which we will utilize Sprint's network to provide mobile voice and

data services to our customers throughout the nation, and our broadband network will be utilized to accelerate the densification of Sprint's network. We believe this additional

product

6

offering will enable us to deliver greater value and more benefits to our customers, including by offering "quad play" offerings that bundle broadband, pay television, telephony

and mobile voice and data services to our customers.

Business Services

Both our Optimum and Suddenlink segments offer a wide and growing variety of products and services to both large enterprise and small and medium-sized business

("SMB") customers, including broadband, telephony, networking and pay television services. For the year ended December 31, 2017, business services accounted for

approximately 14% of the revenue for both our Optimum and Suddenlink segments, respectively, and accounted for approximately 14% of our consolidated revenue. As of

December 31, 2017, our Optimum segment served approximately 263,000 SMB customers and our Suddenlink segment served 109,000 SMB customers. We serve enterprise

customers primarily through our Lightpath business, a subsidiary of Cablevision.

Enterprise Customers

Lightpath provides Ethernet, data transport, IP-based virtual private networks, Internet access, telephony services, including session initiated protocol ("SIP") trunking and

VoIP services to the business market. Our Lightpath bandwidth connectivity service offers download speeds up to 100 Gbps. Lightpath also provides managed services to

businesses, including hosted telephony services (cloud based SIP-based private branch exchange), managed Wi-Fi, managed desktop and server backup and managed

collaboration services including audio and web conferencing. Through Lightpath, we also offer fiber-to-the-tower ("FTTT") services to wireless carriers for cell tower backhaul

and enable wireline communications service providers to connect to customers that their own networks do not reach. Lightpath's customers include companies in health care,

financial, education, legal and professional services, and other industries, as well as the public sector and communication providers, incumbent local exchange carriers

("ILEC"), and competitive local exchange carriers ("CLEC"). As of December 31, 2017, Lightpath had over 9,100 locations connected to its fiber network. Our Lightpath

advanced fiber optic network extends more than 7,100 route miles, which includes approximately 361,000 miles of fiber, throughout the New York metropolitan area.

For enterprise and larger commercial customers, Suddenlink offers high capacity data services, including wide area networking and dedicated data access and advanced

services such as wireless mesh networks. Suddenlink also offers enterprise class telephone services which include traditional multi-line phone service over DOCSIS and

trunking solutions via SIP for our Primary Rate Interface and SIP trunking applications. Similar to Lightpath, Suddenlink also offers FTTT services. These Suddenlink services

are offered on a standalone basis or in bundles that are developed specifically for our commercial customers.

SMB Customers

Both our Optimum and Suddenlink segments provide broadband, pay television and telephony services to SMB customers. In addition to these services, we also offer

managed services, including business e-mail, hosted private branch exchange, web space storage and network security monitoring for SMB customers. We also offer Optimum

Voice for Business, providing for up to 24 voice lines for SMB customers and 20 business calling features at no additional charge. Optimum Voice for Business offers business

trunking services with support for application programming interfaces. Optional add-on services, such as international calling, toll free calling and virtual receptionists, are also

available for business customers.

Advertising Sales

As part of the agreements under which we acquire pay television programming, we typically receive an allocation of scheduled advertising time during such programming,

generally two minutes per hour, into which our systems can insert commercials, subject, in some instances, to certain subject matter limitations. Our advertising sales

infrastructure includes in-house production facilities, production and administrative employees and a locally-based sales force, and is part of Altice Media Solutions ("AMS"),

the advertising sales division of Altice USA.

AMS offers data-driven television, digital and other multi-platform advertising to clients ranging from Fortune 500 brands to local businesses. AMS provides national and

local businesses with television and digital advertising opportunities targeted within specific geographies, including in New York City, and throughout the Suddenlink footprint.

AMS offers clients opportunities to use interactive television products to reach their customers and provide a deeper level of audience engagement.

7

In several of the markets in which we operate, we have entered into agreements commonly referred to as interconnects with other cable operators to jointly sell local

advertising, simplifying our clients' purchase of local advertising and expanding their geographic reach. In some of these markets, we represent the advertising sales efforts of

other cable operators; in other markets, other cable operators represent us. For instance, AMS manages the New York Interconnect, a partnership between AMS and Comcast

that provides national brands with television and digital advertising opportunities over a broader portion of the New York designated market area ("DMA") than AMS's local

offerings. The New York Interconnect is the largest interconnect in the country, with a footprint of over 3.2 million households. In the larger DMAs in the Suddenlink footprint,

we participate in a number of interconnects managed by others, such as the Houston and Dallas interconnects. In December 2017, Altice USA, Charter Communications and

Comcast announced a preliminary agreement to form a new Interconnect in the New York market that would provide a single solution to reach more than 6.2 million

households across the New York DMA. The new New York Interconnect is expected to launch in early second quarter 2018.

For the year ended December 31, 2017, advertising sales accounted for approximately 5% and 3% of the revenue for our Optimum and Suddenlink segments, respectively,

and accounted for approximately 4% of our consolidated revenue.

Data Analytics

The Advanced Data Analytics business, which was launched by Optimum in 2013, provides data-driven, audience-based advertising solutions to the media industry,

including AMS, programmers and multichannel video programming distributors ("MVPDs"). Total Audience Data, its flagship portfolio of products, consists of advanced

analytics tools providing granular measurement of consumer groups, accurate hyper-local ratings and other insights into target audience behavior not available through

traditional sample-based measurement services. These tools allow us and our clients to more precisely optimize our product offerings, target and deliver ads more efficiently,

and provide accurate measurement to our clients and partners.

Our March 2017 acquisition of Audience Partners, a leading provider of data-driven, audience-based digital advertising solutions, expands the scope of targeted advertising

solutions we offer from television to include digital, mobile and tablets. In addition, the acquisition expands our audience-based advertising services to include further advanced

analytics tools within key and growing segments, including political, advocacy, healthcare, automotive, and programming.

News 12 Networks

Our News 12 Networks consists of seven 24-hour local news channels in the New York metropolitan area—the Bronx, Brooklyn, Connecticut, Hudson Valley, Long

Island, New Jersey and Westchester—providing each with complete access to hyper-local breaking news, traffic, weather, sports, and more. In addition, News 12 Networks also

includes five traffic and weather channels that offer constantly updated information; the award-winning News12.com, the premier destination for local news on the web; News

12 Interactive, channel 612 on Optimum TV, providing local news on demand; and News 12 To Go, the network's mobile app for phones and tablets. Since launching in 1986,

News 12 Networks has been widely recognized by the news industry with numerous prestigious honors and awards, including over 230 Emmy Awards, plus multiple Edward

R. Murrow Awards, NY Press Club Awards, and more. We derive revenue from our News 12 Networks for the sale of advertising and affiliation fees paid by cable operators.

Advertising revenue is included in "Advertising" and affiliation fees charged for the programming are included in "Other."

Franchises

As of December 31, 2017, our systems operated in more than 1,300 communities pursuant to franchises, permits and similar authorizations issued by state and local

governmental authorities. Franchise agreements typically require the payment of franchise fees and contain regulatory provisions addressing, among other things, service

quality, cable service to schools and other public institutions, insurance and indemnity. Franchise authorities generally charge a franchise fee of not more than 5% of certain of

our cable service revenues that are derived from the operation of the system within such locality. We generally pass the franchise fee on to our customers.

Franchise agreements are usually for a term of 5 to 15 years from the date of grant (a majority of which are for 10 years), however, approximately 400 of Altice’s

communities are now served under perpetual state-issued franchises. Franchise agreements are usually terminable only if the cable operator fails to comply with material

provisions and then

8

only after the franchising authority complies with substantive and procedural protections afforded by the franchise agreement and federal and state law. Prior to the scheduled

expiration of most franchises, we generally initiate renewal proceedings with the granting authorities. This process usually takes less than three years but can take a longer

period of time. The Communications Act of 1934, as amended (the "Communications Act"), which is the primary federal statute regulating interstate communications, provides

for an orderly franchise renewal process in which granting authorities may not unreasonably withhold renewals. See "Regulation—Cable Television—Franchising." In

connection with the franchise renewal process, many governmental authorities require the cable operator to make certain commitments, such as building out certain franchise

areas, meeting customer service requirements and supporting and carrying public access channels.

Historically, we have been able to renew our franchises without incurring significant costs, although any particular franchise may not be renewed on commercially

favorable terms or otherwise. We expect to renew or continue to operate under all or substantially all of these franchises. For more information regarding risks related to our

franchises, see "Risk Factors—Risk Factors Relating to Regulatory and Legislative Matters—Our cable system franchises are subject to non-renewal or termination. The failure

to renew a franchise in one or more key markets could adversely affect our business." Proposals to streamline cable franchising recently have been adopted at both the federal

and state levels. For more information see "Regulation—Cable Television—Franchising."

Programming

We design our channel line-ups for each system according to demographics, programming contract requirements, market research, viewership, local programming

preferences, channel capacity, competition, price sensitivity and local regulation. We believe offering a wide variety of programming influences a customer's decision to

subscribe to and retain our pay television services. We obtain programming, including basic, expanded basic, digital, HD, VOD and broadband content, from a number of

suppliers, including broadcast and cable networks.

We generally carry cable networks pursuant to written programming contracts, which continue for a fixed period of time, usually from three to five years, and are subject to

negotiated renewal. Cable network programming is usually made available to us for a license fee, which is generally paid based on the number of customers who subscribe to

the level of service that provides such programming. Such license fees may include "volume" discounts available for higher numbers of customers, as well as discounts for

channel placement or service penetration. Where possible, we negotiate volume discount pricing structures. For home shopping channels, we receive a percentage of the revenue

attributable to our customers' purchases, as well as, in some instances, incentives for channel placement.

We typically seek flexible distribution terms that would permit services to be made available in a variety of retail packages and on a variety of platforms and devices in

order to maximize consumer choice. Suppliers typically insist that their most popular and attractive services be distributed to a minimum number or percentage of customers,

which limits our ability to provide consumers full purchasing flexibility. Suppliers also typically seek to control or limit the terms on which we are able to make their services

available on various platforms and devices yet this has become more flexible each year.

Our cable programming costs have increased in excess of customary inflationary and cost-of-living type increases. We expect programming costs to continue to increase

due to a variety of factors including annual increases imposed by stations and programmers and additional programming being provided to customers, including HD, digital and

VOD programming. In particular, broadcast and sports programming costs have increased significantly over the past several years. In addition, contracts to purchase sports

programming sometimes provide for optional additional programming to be available on a surcharge basis during the term of the contract. These increases have coincided with a

significant increase in the quality of the programming, from high production value original cable series to enhanced camera and statistical data technology in sports broadcasts,

and more flexible rights to make the content available on various platforms and devices.

We have programming contracts that have expired and others that will expire in the near term. We will seek to renegotiate the terms of these agreements, but there can be

no assurance that these agreements will be renewed on favorable or comparable terms. To the extent that we are unable to reach agreement with certain programmers on terms

that we believe are reasonable, we have been, and may in the future be, forced to remove such programming channels from our line-up, which may result in a loss of customers.

For example, in 2017, we were unable to reach agreement with Starz on acceptable economic terms, and effective January 1, 2018, all Starz services were removed from our

lineups

9

in our Optimum and Suddenlink segments, and we launched alternative networks offered by other programmers under new long-term contracts. On February 13, 2018, we and

Starz reached a new carriage agreement and we started restoring the Starz services previously offered by Optimum and Suddenlink. Also in our Suddenlink segment, we were

unable to reach agreement with Viacom on acceptable economic terms for a long-term contract renewal, and effective October 1, 2014, all Viacom networks were removed

from our channel lineups in our Suddenlink segment, and we launched alternative networks offered by other programmers under new long-term contracts. We and Viacom did

not reach a new agreement to include certain Viacom networks in the Suddenlink channel lineup until May 2017. For more information, see "Risk Factors—Risk Factors

Relating to Our Business—Programming and retransmission costs are increasing and we may not have the ability to pass these increases on to our customers. Disputes with

programmers and the inability to retain or obtain popular programming can adversely affect our relationship with customers and lead to customer losses."

Sales and Marketing

Sales are managed centrally and multiple sales channels are leveraged to reach current and potential customers, including in-bound customer care centers, outbound

telemarketing, stores, field technician sales and door-to-door sales. E-commerce is also managed centrally on behalf of the organization and is a growing and dynamic part of

our business and is our fastest growing sales channel. For the three months ended December 31, 2017, 27% of our gross adds were via our online sales channel, compared to

14% for the three months ended December 31, 2016. We also use mass media, including broadcast television, digital media, radio, newspaper and outdoor advertising, to attract

customers and direct them to our in-bound customer care centers or website. Our sales and service employees use a variety of sales tools as they work to match customers' needs

with our best-in-class products, with a focus on building and enhancing customer relationships.

Because of our local presence and market knowledge, we invest heavily in targeted marketing. Our strategic focus is on building new customer relationships and bundling

broadband, pay television and telephony services. Our promotional materials and messaging focus on how our products and services deliver innovative solutions to customer

pain points. Much of our advertising is developed centrally and customized for our regions. Among other factors, we monitor customer perceptions, marketing tactic impact and

competition, to increase our responsiveness and the effectiveness of our efforts. Our footprint has several large college markets where we market specialized products and

services to students for multiple dwelling units ("MDUs"), such as dormitories and apartment complexes.

We have separate dedicated sales teams for our SMB and enterprise offerings and dedicated service teams to support SMB and enterprise clients.

Altice Technical Services

In January 2018, the Company acquired 70% of the equity interests in Altice Technical Services US Corp. ("ATS") for $1.00 (the "ATS Acquisition") and the Company

expects to become the owner of 100% of the equity interests in ATS prior to the Distribution. ATS was previously owned by Altice N.V. and a member of ATS's management

through a holding company. In light of Altice N.V.'s determination to focus on businesses other than the Company, we and Altice N.V. concluded it is in Altice N.V.'s and the

Company's interests for Altice USA to own and operate ATS. The ATS Acquisition was approved by our Audit Committee pursuant to the Company's related-party transaction

approval policy.

ATS has and will continue to provide technical operating services to the Company, including field services, such as dispatch, customer installations, disconnects, service

changes and other customer service visits, outside plant maintenance services and design and construction services for HFC and FTTH infrastructure pursuant to an Independent

Contractor Agreement and Transition Services Agreement with the Company.

Customer Experience

We believe customer service is the cornerstone of our business. Accordingly, we make a concerted effort to continually improve each customer's experience and have

made significant investments in our people, processes and technology to enhance our customers' experience and to reduce the number of times customers need to contact us. The

insights from operational metrics help us focus our improvement efforts. For example, we link internal sales incentives to early churn and product mix, as opposed to more

traditional criteria of new sales, in order to refocus our organization away from churn retention to churn prevention.

10

Our customer care centers are managed and operated locally, with the deployment and execution of end-to-end care strategies and initiatives conducted on a site-by-site

basis. We have residential and commercial customer care centers located throughout our footprint, including in Newark, NJ; Jericho, NY; Bronx, NY; Melville, NY; Tyler, TX;

and Lubbock, TX. Our customer care centers function as an integrated system and utilize software programs that provide increased efficiencies and limited wait-times for

customers requiring support.

We provide technical service to our customers 24 hours a day, seven days a week, and we have systems that allow our customer care centers to be accessed and managed

remotely in the event that systems functionality is temporarily lost, which provides our customers access to customer service with limited disruption.

We also utilize our customer portal to enable our customers to view and pay their bills online, obtain useful information and perform various equipment troubleshooting

procedures. Our customers may also obtain support through our online chat, e-mail functionality and social media websites, including Twitter and Facebook.

Network Management

Our cable systems are generally designed with an HFC architecture that has proven to be highly flexible in meeting the increasing needs of our customers. We deliver our

signals via laser-fed fiber optic cable from control centers known as headends and hubs to individual nodes. Each node is connected to the individual homes served by us. A

primary benefit of this design is that it pushes fiber optics closer to our customers' homes, which allows us to subdivide our systems into smaller service groups and make capital

investments only in service groups experiencing higher than average service growth.

As of December 31, 2017, approximately 96% of our basic pay television customers were served by systems with a capacity of at least 750 MHz and approximately 275

homes per node. Our Optimum network has been upgraded to nearly four times the maximum available broadband speeds and we have expanded our Gbps broadband service to

approximately 72% of our Suddenlink footprint, compared to approximately 40% prior to the Suddenlink Acquisition. More than 99% of our residential broadband Internet

customers are connected to our national backbone with a presence in major carrier access points in New York, Dallas, Chicago, San Jose, Washington D.C. and Phoenix. This

presence allows us to avoid significant Internet transit costs by establishing peering relationships with major Internet service and content providers enabling direct connectivity

with them at these access points.

We also have a networking caching architecture that places highly viewed Internet traffic from the largest Internet-based content providers at the edge of the network

closest to the customer to reduce bandwidth requirements across our national backbone, thus reducing operating expense. This collective network architecture also provides us

with the capability to manage traffic across several Internet access points, thus helping to ensure Internet access redundancy and quality of service for our customers.

Additionally, our national backbone connects most of our systems, which allows for an efficient and economical deployment of services from our centralized platforms that

include telephone, VOD, network DVR, common pay television content, broadband Internet, hosted business solutions, provisioning, e-mail and other related services.

We have also commenced a plan to build a FTTH network, which will enable us to deliver more than 10 Gbps broadband speeds across our entire Optimum footprint and

part of our Suddenlink footprint. We believe this FTTH network will be more resilient with reduced maintenance requirements, fewer service outages and lower power usage,

which we expect will drive further structural cost efficiencies.

We have also focused on system reliability and disaster recovery as part of our national backbone and primary system strategy. For example, to help ensure a high level of

reliability of our services, we implemented redundant power capability, as well as fiber route and carrier diversity in our networks serving most of our customers. With respect

to disaster recovery, we invested in our telephone platform architecture for geo-redundancy to minimize downtime in the event of a disaster to any single facility. Additionally,

we are working to implement a geo-redundant disaster recovery environment for our network operations center supporting both residential and business customers.

In addition, we have expanded and refined our bandwidth utilization in capacity constrained systems in order to meet demand for new and improved advanced services. A

key component to reclaim bandwidth was the digital delivery of pay television channels that were previously distributed in analog through the launch of digital simulcast, which

duplicates analog channels as digital channels. Additionally, the deployment of lower-cost digital customer premises equipment, such as HD digital transport adapters, enabled

the use of more efficient digital channels instead of analog

11

channels, thus allowing the reclamation of expanded basic analog bandwidth in the targeted systems. This reclaimed analog bandwidth could then be repurposed for other

advanced services such as additional HDTV services and faster Internet access speeds. This technology has the added benefit of providing improved picture and sound quality to

customers for most of their pay television programming.

Information Technology

Our IT systems consist of billing, customer relationship management, business and operational support and sales force management systems. We are updating and

simplifying our IT infrastructure through further investments, focusing on cost efficiencies, improved system reliability, functionality and scalability and enhancing the ability

of our IT infrastructure to meet our ongoing business objectives. Further, we have made significant progress in integrating and consolidating the IT platforms and systems and

streamlining the processes of Optimum and Suddenlink, which has driven operating efficiencies. Additionally, through investment in our IT platforms and focus on process

improvement, we have simplified and harmonized our service offering bundles, optimized our technical service delivery and improved customer service.

Suppliers

Customer Premise and Network Equipment

We purchase set-top boxes and other customer premise equipment from a limited number of vendors because each of our cable systems uses one or two proprietary

technology architectures. We also buy HD, HD/DVRs and VOD equipment, routers, including the components of our new home communications hub, and other network

equipment from a limited number of suppliers, including Altice Labs, Altice N.V.'s technology, services and innovation center. See "Risk Factors—Risk Factors Relating to Our

Business—We rely on network and information systems for our operations and a disruption or failure of, or defects in, those systems may disrupt our operations, damage our

reputation with customers and adversely affect our results of operations."

Broadband and Telephone Connectivity

We deliver broadband and telephony services through our HFC network. We use circuits that are either owned by us or leased from third parties to connect to the Internet

and the public switched telephone network. We pay fees for leased circuits based on the amount of capacity available to it and pay for Internet connectivity based on the amount

of IP-based traffic received from and sent over the other carrier's network.

Competition

We operate in a highly competitive, consumer-driven industry and we compete against a variety of broadband, pay television and telephony providers and delivery systems,

including broadband communications companies, wireless data and telephony providers, satellite delivered video signals, Internet-delivered video content and broadcast

television signals available to residential and business customers in our service areas. We believe our leading market positions in our footprint, technologically advanced

network infrastructure, including our FTTH build-out, our new home communications hub and our focus on enhancing the customer experience favorably position us to

compete in our industry. See also "Risk Factors—Risk Factors Relating to Our Business—We operate in a highly competitive business environment which could materially

adversely affect our business, financial condition, results of operations and liquidity."

Broadband Services Competition

Our broadband services face competition from broadband communications companies' digital subscriber line ("DSL"), FTTH and wireless broadband offerings as well as

from a variety of companies that offer other forms of online services, including satellite-based broadband services. Current and future fixed and wireless Internet services, such

as 3G, 4G and 5G fixed and wireless broadband services and Wi-Fi networks, and devices such as wireless data cards, tablets and smartphones, and mobile wireless routers that

connect to such devices, may compete with our broadband services.

Pay Television Services Competition

We face intense competition from broadband communications companies with fiber-based networks, primarily Verizon Communications Inc. ("Verizon"), which has

constructed a FTTH network plant that passes a significant number of households in our Optimum service area. We estimate that Verizon is currently able to sell a fiber-based

pay television

12

service, as well as broadband and VoIP services, to at least half of the households in our Optimum service area. In addition, Frontier offers pay television service in competition

with us in most of our Connecticut service area.

We also compete with direct broadcast satellite ("DBS") providers, such as DirecTV (a subsidiary of AT&T Inc.) and DISH Network Corporation ("DISH Network").

DirecTV and DISH offer one-way satellite-delivered pre-packaged programming services that are received by relatively small and inexpensive receiving dishes. DirecTV has

exclusive arrangements with the National Football League that give it access to programming that we cannot offer. AT&T also has an agreement to acquire Time Warner Inc.,

which owns a number of cable networks, including TBS, CNN and HBO, and Warner Bros. Entertainment, which produces television, film and home-video content. However,

we believe cable-delivered VOD services, which include HD programming, offer a competitive advantage to DBS service because cable headends can provide two-way

communication to deliver a large volume of programming which customers can access and control independently, whereas DBS technology can only make available a much

smaller amount of programming with DVR-like customer control.

Our pay television services also face competition from a number of other sources, including companies that deliver movies, television shows and other pay television

programming over broadband Internet connections to televisions, computers, tablets and mobile devices, such as Hulu, iTunes, Amazon Prime, Netflix, YouTube, Playstation

Vue, DirecTV Now and Sling TV.

Telephony Services Competition

Our telephony service competes with wireline, wireless and OTT phone providers, such as Vonage, Skype, GoogleTalk, Facetime, WhatsApp and magicJack, as well as

companies that sell phone cards at a cost per minute for both national and international service. In addition, we compete with other forms of communication, such as text

messaging on cellular phones, instant messaging, social networking services, video conferencing and email. The increase in the number of different technologies capable of

carrying telephony services and the number of alternative communication options available to customers as well as the replacement of wireline services by wireless have

intensified the competitive environment in which we operate our telephony services.

Business Services Competition

We operate in highly competitive business telecommunications market and compete primarily with local incumbent telephone companies, especially AT&T, CenturyLink,

Inc. ("Centurylink"), Frontier and Verizon, as well as from a variety of other national and regional business services competitors.

Advertising Sales Competition

We face intense competition for advertising revenue across many different platforms and from a wide range of local and national competitors. Advertising competition has

increased and will likely continue to increase as new formats seek to attract the same advertisers. We compete for advertising revenue against, among others, local broadcast

stations, national cable and broadcast networks, radio stations, print media and online advertising companies and content providers.

Regulation

Our cable and related services are subject to a variety of federal, state and local law and regulations. The Communications Act, and the rules, regulations and policies of the

Federal Communications Commission ("FCC"), as well as other federal and state laws governing cable television, communications, consumer protection, privacy and related

matters, affect significant aspects of our cable system and services operations.

The following paragraphs describe the existing legal and regulatory requirements we believe are most significant to our cable system operations today. Our business can be

dramatically impacted by changes to the existing regulatory framework, whether triggered by legislative, administrative or judicial rulings.

Cable Television

Franchising. The Communications Act requires cable operators to obtain a non-exclusive franchise from state or local franchising authorities to provide cable service.

Although the terms of franchise agreements differ from jurisdiction to jurisdiction, they typically require payment of franchise fees and contain regulatory provisions

addressing, among other things, use of the right of way, service quality, cable service to schools and other public institutions, insurance, indemnity and sales of assets or

changes in ownership. State and local franchising authority, however, must be exercised consistent

13

with the Communications Act, which sets limits on franchising authorities' powers, including limiting franchise fees to no more than 5% of gross revenues from the provision of

cable service, prohibiting franchising authorities from requiring us to carry specific programming services, and protecting the renewal expectation of franchisees by limiting the

factors a franchising authority may consider and requiring a due process hearing before denying renewal. Even when franchises are renewed, however, the franchise authority

may, except where prohibited by applicable law, seek to impose new and more onerous requirements as a condition of renewal. Similarly, if a franchising authority's consent is

required for the purchase or sale of a cable system, the franchising authority may attempt to impose more burdensome requirements as a condition for providing its consent.

Cable franchises generally are granted for fixed terms and in many cases include monetary penalties for noncompliance. They may also be terminable if the franchisee fails to

comply with material provisions.

In recent years, the traditional local cable franchising regime underwent significant change as a result of various federal and state actions. Several states have reduced or

eliminated the role of local, municipal government in franchising in favor of state or system-wide franchises, and the trend has been toward consolidation of franchising

authority at the state level, in part to accommodate the interests of new broadband and cable entrants over the last decade. At the same time, the FCC has adopted rules that

streamline entry for new competitors (such as those affiliated with broadband communications companies) and reduce certain franchising burdens for these new entrants. The

FCC adopted more modest relief for existing cable operators, but a recent federal court decision curtailed a portion of this relief that relates to the cap on in-kind payments to

franchising authorities.

Pricing and Packaging. The Communications Act and the FCC's rules limit the scope of price regulation for cable television services. Among other limitations,

franchising authorities may regulate rates for only "basic" cable service. In 2015, the FCC adopted an order reversing its historic approach to this local rate regulation.

Previously, rate regulation was in effect in a community unless and until a cable operator successfully petitioned the FCC for relief by showing the existence of "effective

competition" (as defined under federal law) in the community. The FCC reversed that presumption, barring franchise authority rate regulation absent an affirmative showing by

the franchising authority that there is an absence of effective competition. As none of our franchise authorities have filed the necessary rate regulation certification, none of our

pay television customers are currently subject to rate regulation.

There have been frequent calls to impose further rate regulation on the cable industry. It is possible that Congress or the FCC may adopt new constraints on the retail

pricing or packaging of cable programming. For example, there has been legislative and regulatory interest in requiring cable operators to offer historically bundled

programming services on an à la carte basis. In addition, the FCC recently initiated a proceeding exploring how programming practices involving MVPDs affect the availability

of diverse and independent programming. As we attempt to respond to a changing marketplace with competitive marketing and pricing practices, we may face regulations that

impede our ability to compete.

Must-Carry/Retransmission Consent. Cable operators are required to carry, without compensation, programming transmitted by most local commercial and

noncommercial broadcast television stations that elect "must carry" status.

Alternatively, local commercial broadcast television stations may elect "retransmission consent," giving up their must-carry right and instead negotiating with cable

systems the terms on which the cable systems may carry the station's programming content. Cable systems generally may not carry a broadcast station that has elected

retransmission consent without the station's consent. The terms of retransmission consent agreements frequently include the payment of compensation to the station.

Broadcast stations must elect "must carry" or retransmission consent every three years. A substantial number of local broadcast stations currently carried by our cable

systems have elected to negotiate for retransmission consent. In the most recent retransmission consent negotiations, popular television stations have demanded substantial

compensation increases, thereby increasing our operating costs.

Ownership Limitations. Federal regulation of the communications field traditionally included a host of ownership restrictions, which limited the size of certain media

entities and restricted their ability to enter into competing enterprises. Through a series of legislative, regulatory, and judicial actions, most of these restrictions have been either

eliminated or substantially relaxed. The FCC is currently considering substantial changes in this area, which could alter the business environment in which we operate.

Set-Top Boxes. The Communications Act includes a provision that requires the FCC to take certain steps to support the development of a retail market for "navigation

devices," such as cable set-top boxes. As a result, the FCC has adopted certain mandates, from time to time, to require cable operators to accommodate third party navigation

devices, sometimes imposing substantial development and operating requirements on the industry. From time to time, the FCC has proposed additional rules to effectuate this

mandate, though there is no currently active effort to advance these proposals. Nevertheless, the FCC may in the future consider implementing other measures to promote the

competitive availability of retail set-top boxes or third party navigation options that could impact our customers' experience, our ability to capture user interactions to refine and

enhance our services, and our ability to provide a consistent customer support environment.

14

PEG and Leased Access. Franchising authorities may require that we support the delivery and support for public, educational, or governmental ("PEG") channels on our

cable systems. In addition to providing PEG channels, we must make a limited number of commercial leased access channels available to third parties (including parties with

potentially competitive pay television services) at regulated rates. The FCC adopted revised rules several years ago mandating a significant reduction in the rates that operators

can charge commercial leased access users. These rules were stayed, however, by a federal court, pending a cable industry appeal. This matter currently remains pending, and

the revised rules are not yet in effect. Although commercial leased access activity historically has been relatively limited, increased activity in this area could further burden the

channel capacity of our cable systems.

Pole Attachments. The company makes extensive use of utility poles and conduit owned by other utilities to attach and install the facilities that are integral to our network

and services. The Communications Act requires most utilities to provide cable systems with access to poles and conduits for access to attach such facilities at regulated rates.

States (or, where states choose not to regulate, the FCC) regulate utility company rates for the rental of pole and conduit space used by companies, including operators like us, to

provide cable, telecommunications services, and Internet access services, unless states establish their own regulations in this area. Many states in which we operate have elected

to set their own pole attachment rules.

In 2011 and again in 2015, the FCC amended its pole attachment rules to promote broadband deployment. The 2011 order allows for new penalties in certain cases

involving unauthorized attachments, but generally strengthens the cable industry's ability to access investor-owned utility poles on reasonable rates, terms and conditions.

Additionally, the 2011 order reduces the federal rate formula previously applicable to "telecommunications" attachments to closely approximate the more favorable rate formula

applicable to "cable" attachments. The 2015 Order continues this rate reconciliation, effectively closing a remaining "loophole" that potentially allowed for significantly higher

rates for telecommunications attachments in certain scenarios. Neither the 2011 order nor the 2015 Order directly affects the rate in states that self-regulate (rather than allowing

the FCC to regulate) pole rates, but many of those states have substantially the same rate for cable and telecommunications attachments. Adverse changes to the pole attachment

rate structure, rate, and classifications could significantly increase our annual pole attachment costs.

Program Access. The program access rules generally prohibit a cable operator from improperly influencing an affiliated satellite-delivered cable programming service to

discriminate unfairly against an unaffiliated distributor where the purpose or effect of such influence is to significantly hinder or prevent the competitor from providing satellite-

delivered cable programming. FCC rules also allow a competing distributor to bring a complaint against a cable-affiliated terrestrially-delivered programmer or its affiliated

cable operator for alleged violations of this rule, and seek reformed terms of carriage as remedy.

Program Carriage. The FCC's program carriage rules prohibit us from requiring that an unaffiliated programmer grant us a financial interest or exclusive carriage rights

as a condition of its carriage on our cable systems and prohibit us from unfairly discriminating against unaffiliated programmers in the terms and conditions of carriage on the

basis of their nonaffiliation.

On October 12, 2011, Game Show Network ("GSN") filed a program carriage complaint against Cablevision, alleging that we discriminated against it in the terms and

conditions of carriage based on GSN's lack of affiliation with us. Although the Enforcement Bureau of the FCC recommended on October 15, 2015, that the administrative law

judge adjudicating this dispute find in our favor because GSN had not satisfied its burden of proving that we discriminated against it on the basis of affiliation, the

administrative law judge issued his initial decision in GSN's favor on November 23, 2016, requiring that we restore GSN to the expanded basic tier. The FCC reversed that

decision and denied GSN's complaint on July 13, 2017. GSN initiated review of that decision in a federal appeals court on September 11, 2017. We believe GSN's claims are

without merit and intervened in GSN's appeal to support the FCC's decision on October 11, 2017. On December 28, 2017, we entered into a binding settlement agreement with

GSN. On January 25, 2018, the federal court of appeals entered dismissal of the action.

Exclusive Access to Multitenant Buildings. The FCC has prohibited cable operators from entering into or enforcing exclusive agreements with owners of multitenant

buildings under which the operator is the only MVPD with access to the building.

CALM Act. The FCC's rules require us to ensure that all commercials carried on our cable service comply with specified volume standards.

Privacy and Data Security. In the course of providing our services, we collect certain information about our customers and their use of our services. We also collect

certain information regarding potential customers and other individuals. Our collection, use, disclosure and other handling of information is subject to a variety of federal and

state privacy requirements, including those imposed specifically on cable operators and telecommunications service providers by the Communications Act. We are also subject

to data security obligations, as well as requirements to provide notice to individuals and governmental

15

entities in the event of certain data security breaches, and such breaches, depending on their scope and consequences, may lead to litigation and enforcement actions with the

potential of substantial monetary forfeitures or to adversely affect our brand.

As cable operators provide interactive and other advanced services, additional privacy and data security requirements may arise through legislation, regulation or judicial

decisions. For example, the Video Privacy Protection Act of 1988 has been extended to cover online interactive services through which customers can buy or rent movies. In

addition, Congress, the Federal Trade Commission ("FTC"), and other lawmakers and regulators are all considering whether to adopt additional measures that could impact the

collection, use, and disclosure of customer information in connection with the delivery of advertising and other services to consumers customized to their interests. In October

2016, the FCC adopted new privacy and data security rules governing the use of customer information by broadband ISPs, including cable ISPs and providers of VoIP. These

new rules permit the collection and use of non-sensitive customer information subject to the customers' ability to opt out, but require the customers' opt-in before access, use or