©2020 Grant Thornton Ireland Ltd. All rights reserved.

Wednesday 25

th

November 2020

Aengus Burns

Partner, Grant Thornton

Ray McMahon

Director and CCO, Dilosk/ICS Mortgages

Enda McGuane

Managing Director – Winters Property

Purchasing Investment Property -

Opportunities and Challenges

Welcome to today’s webinar which will begin shortly.

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Aengus Burns

Partner

Grant Thornton

Acquiring Investment

Property through

Pension Structures

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Grant Thornton in Ireland

3

€150m

Turnover in 2019

1,450+ employees

Office locations

Dublin, Belfast, Cork,

Galway, Kildare, Limerick

and Longford

“Our clients choose us because of our commitment to addressing their

business needs in an innovative and collaborative manner.

Our client relationships are built on our passionate approach to providing

the highest quality of service at all times.”

Michael McAteer, Managing Partner Grant Thornton Ireland

A focus on Ireland

Grant Thornton is Ireland’s fastest growing professional services firm. We deliver solutions to all business challenges.

Clients choose us because the breadth of financial and business services they need is available, delivered innovatively and

always to the highest standards. At Grant Thornton we are committed to long term relationships. We are different. We are

Grant Thornton.

The firm comprises over 1,450 people operating from offices in Dublin, Belfast, Cork, Galway, Kildare, Limerick and

Longford.

54 partners in

Ireland

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Options for purchasing

Investment property

Personally

• tax on equity and income and gains

• reduced capital allowances

Company

• tax on income and gains in the company

• tax on distributions from company

Pension

• tax relief on contributions by employer

• no tax on equity or income or gains

• €2m Standard Fund Threshold

• transfer of assets to ARF continues to grow tax free

• tax on distributions from ARF after Tax Free Lump Sum

4

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Pension property investments

Standard pension offering

• choice of funds mainly limited to property funds,

ETF’s and REIT’s

Self-Administered pension offering

• more open architecture includes:

• direct property residential and commercial

• syndicated investment property

• loan notes and other investment vehicles

• jointly managed with Pensioneer Trustee

• debt available

5

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Self-administered options

6

Self-Employed

Employed

Retired

Self Administered

PRSA

Self Administered

SSAP

Self Administered

ARF

Personal

Contributions up to

40% NRE (€115K

cap)

Employer (multiple

times salary)

Employee

contributions

Transfer in from

most pensions

(except defined

benefit)

Investment Options the same for all – e.g. direct property, deposits,

shares, funds, etc.

Deferred Pensions

Self Administered

PRB

Transfer in from

past employment

©2020 Grant Thornton Ireland Ltd. All rights reserved.

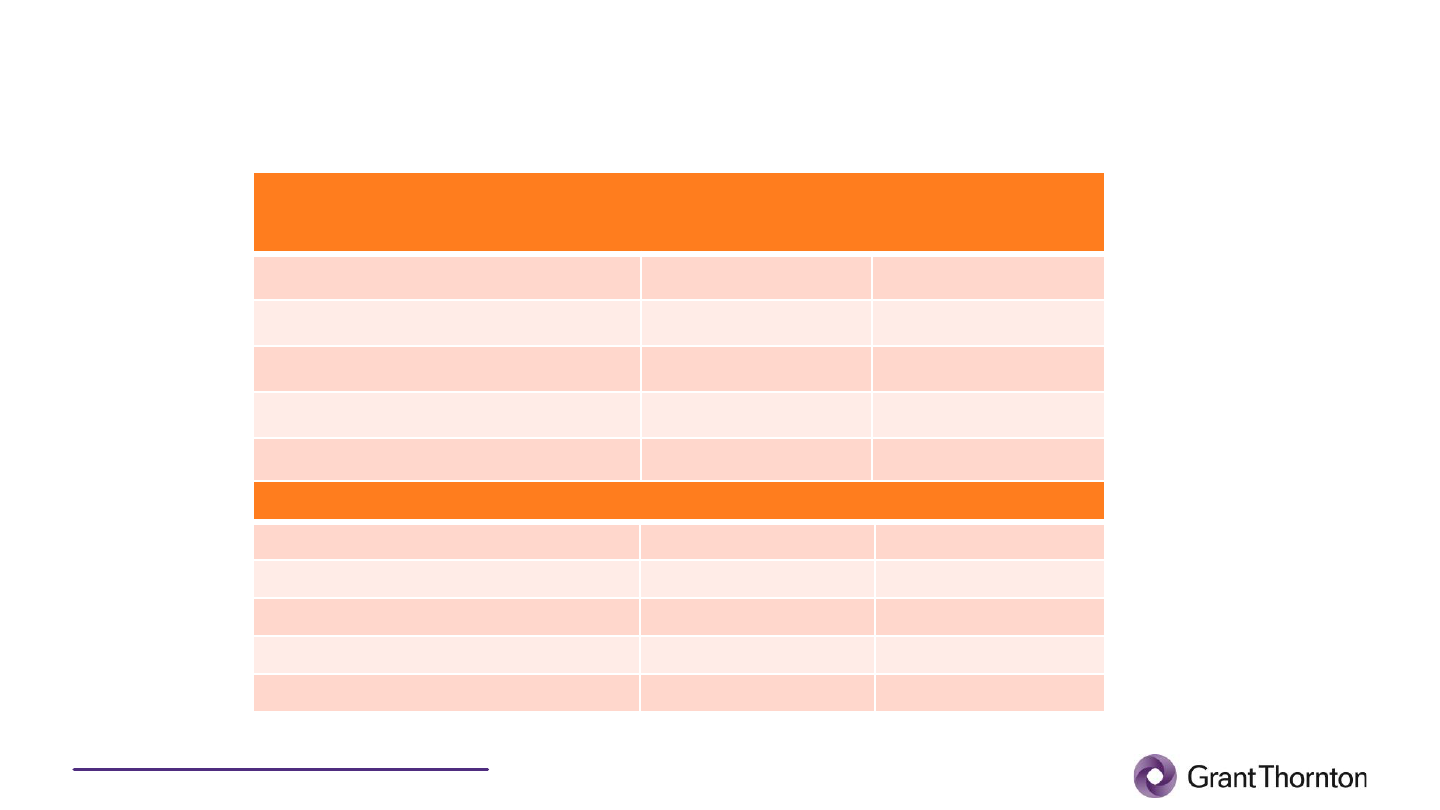

Direct property purchase case study

7

No borrowing

Property purchase example with €250,000 pre-tax funds

Personal Pension (SSAP)

Funds taken out of company €250,000 €250,000

Income tax €100,000 €0

USC/PRSI €37,500 €0

Amount available for investment* €112,500 €250,000

Comparison

Personal Pension (SSAP)

Purchase price €112,500 €250,000

Rental est. (p.a.) €7,200 €14,400

Property agent & trustee fee (p.a.) €0 €2,474

Rent net of tax (higher rate)* €3,240* €11,926

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Key revenue restrictions on property purchases

• arms length requirement (connected

parties rule)

• property development is not allowed

i.e. investing not trading

• direct investments in private

companies are limited

• scheme must have sufficient liquid

assets to provide benefits

8

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Direct geared property purchase case study

9

With Borrowing

Personal Pension (SSAP)

Equity €112,500 €250,000

Over 15 years @ 4.25% (55% LTV) €137,500 (50% LTV) €250,000

Amount available for investment €250,000 €500,000

Rental est. (p.a.) €14,400 €28,800

Property agent & Trustee fee (p.a.) €0 €4,948

Income Tax* €5,308 €0

Rent net of tax/agent/trustee (p.a.) €9,093 €23,852

C&I Bank Repayments p.a. €12,412 €22,568

Net (deficit)/return p.a. -€3,320 €1,284

*Income Tax after deduction for interest and other allowable costs

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Revenue borrowing guidelines

• no recourse to other assets

• no assignment of rental income

• no interest only loans

• no loans over 15 years

• no refinancing

• no direct borrowing in ARF

10

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Property opportunities

• multi tenanted properties

• residential/commercial properties

• commercial property

• social housing

• joint investors

• syndicated investments

• loan note investments

11

©2020 Grant Thornton Ireland Ltd. All rights reserved.

Takeaways

• company structure works best for pension

contributions

• self-administered structure more flexible than

insured pension

• property provides income in retirement

• when purchasing investment property explore

your pension options first

12

Dilosk DAC, trading as Dilosk and ICS Mortgages, is regulated by the Central Bank of Ireland

Ray McMahon

Chief Commercial Officer

Buy-to-Let Mortgages

25

th

November 2020

Dilosk DAC trading as Dilosk and ICS Mortgages is regulated by the Central Bank of Ireland.

Contents:

(1)

Brief Company Overview

(2) Pension Unit

-Trust Buy-to-Let Mortgages

•

Our proposition and lending guidelines

•

Refinancing property portfolios

Company Overview

• Dilosk DAC is an Irish financial services company, regulated by the Central Bank of Ireland

• ICS is one of Ireland’s oldest and renowned mortgage brands with a heritage that dates back to 1864

• In 2017 we launched a specialist mortgage business for the Buy-to-Let market and have gained significant

market share with our innovative Buy-to-Let mortgage propositions

• In September 2019, we entered the market for owner-occupiers with highly competitive offerings for First-

Time Buyers, Movers and Switchers. Our niche segment is Public Sector employees

• All our Mortgages are originated through our direct channel and our network of appointed nationwide brokers

• We now have over €740 million of mortgages under management

Dilosk DAC trading as Dilosk and ICS Mortgages is regulated by the Central Bank of Ireland.

Buy-to-Let Mortgages

• Our Proposition and Lending Guidelines

• Refinancing Property Portfolios

Our Target Market:

Established Landlords Refinancing Property Portfolios

New Buy-to-Let Property Investors

Tailored Solutions for New Portfolios

We Lend to:

Individuals (up to 4 individuals on a mortgage)

Companies (including Special Purpose Vehicles)

Pension (Unit Trusts)

Buy-to-Let Mortgage Specialists

Buy-to-Let – (Pension Unit-Trust)

Loan Purpose

Purchase of Residential Investment Properties

Loan Structure Options

Up to 15 year Capital andInterest

LTV Up to 50% LTV

Loan Amount Minimum loan size€40,000 / Maximum loan size €500,000

Loan Term Minimum term 5 years / Maximum term 15 years

Rates 4.25% Variable rate

Property Value Minimum property value €100,000 / No maximum property value

Lending Criteria

Confirmation required that all letting/rent collection will be arranged and managed by a third-

party property management

company

Only one investor/beneficial owner allowed for each sub trust fund

Refinancing debt from existing pension funds, will require evidence of the original purchase transaction in the existing

fund

Under Revenue Guidelines, Interest only loans are not permissible.

A copy of the overall liquidity position, post the property transaction, to be provided prior to funds being released

Our recommended requirement is for 12 months mortgage repayments to be available within each fund

Up to date financials for each PUT must be provided on a yearly basis

Borrower Profile

• The applicant must reside in the EEA. Applicants from Non EEA may be considered by establishinga

Unit-Trust

• The BTL property must be located in the Republic of Ireland and not used as a principal private

residence

• All applicants must be the owner of at least one residential property in the ROI other than the

buy-to-let property being financed.

• Non- Recourse Lending for Pension (Unit Trusts) only

• A valuation of each property isrequired

Geographic

Locations

• We will lend for properties in urban centres in Ireland witha populationgreater than10,000 people

Lending Criteria

• A max of 75% of the gross rental income from the proposed property should equal or exceed 1.2

times the scheduled repayment

• A max of 75% of the gross rental income from the proposed property shouldequal or exceed 1

times the scheduled repayment at an interest rate of6%

• The gross rental income from the property, together with other surplus disposable income should

equal or exceed the scheduled repayment (please note for this test all contractual mortgage debt is

stressed at the contracted rate plus 2% - regulatory requirement)

• Concentration limits may apply on a case by case basis

Age Profile

Minimum age at application 21 years and Maximum age on maturity 75 years

20

21

CM076

Pension Unit Trust Mortgages

• Non-Recourse lending

• Administered in conjunction with Grant Thornton who are on our panel of approved Trustees

• Customers / Beneficiaries must get independent Pension advice to confirm this product is

suitable for their needs

• Appeals to individuals who are looking for more options regarding the management of their

pension and wish to acquire a Buy-to-Let property in a tax efficient manner.

22

Specialist Buy-to-Let Refinancing Unit

We have seen a significant demand in the number of clients wishing to refinance their Buy-to-Let

portfolios

We can refinance existing Buy-to-Let Mortgages in Pension Unit Trusts

We offer tailored solutions for property portfolio refinancing

Our portfolio investors are often:

• On terms with their existing lenders that are coming to an end (e.g. an interest only period

due to expire)

• Looking to release equity to purchase additional properties to add to their portfolio

• Looking for a more competitive offering

• Coming up to a break clause with their existing lender

• Those with unencumbered properties and they wish to release equity

We offer no cross security which allows for easier portfolio management

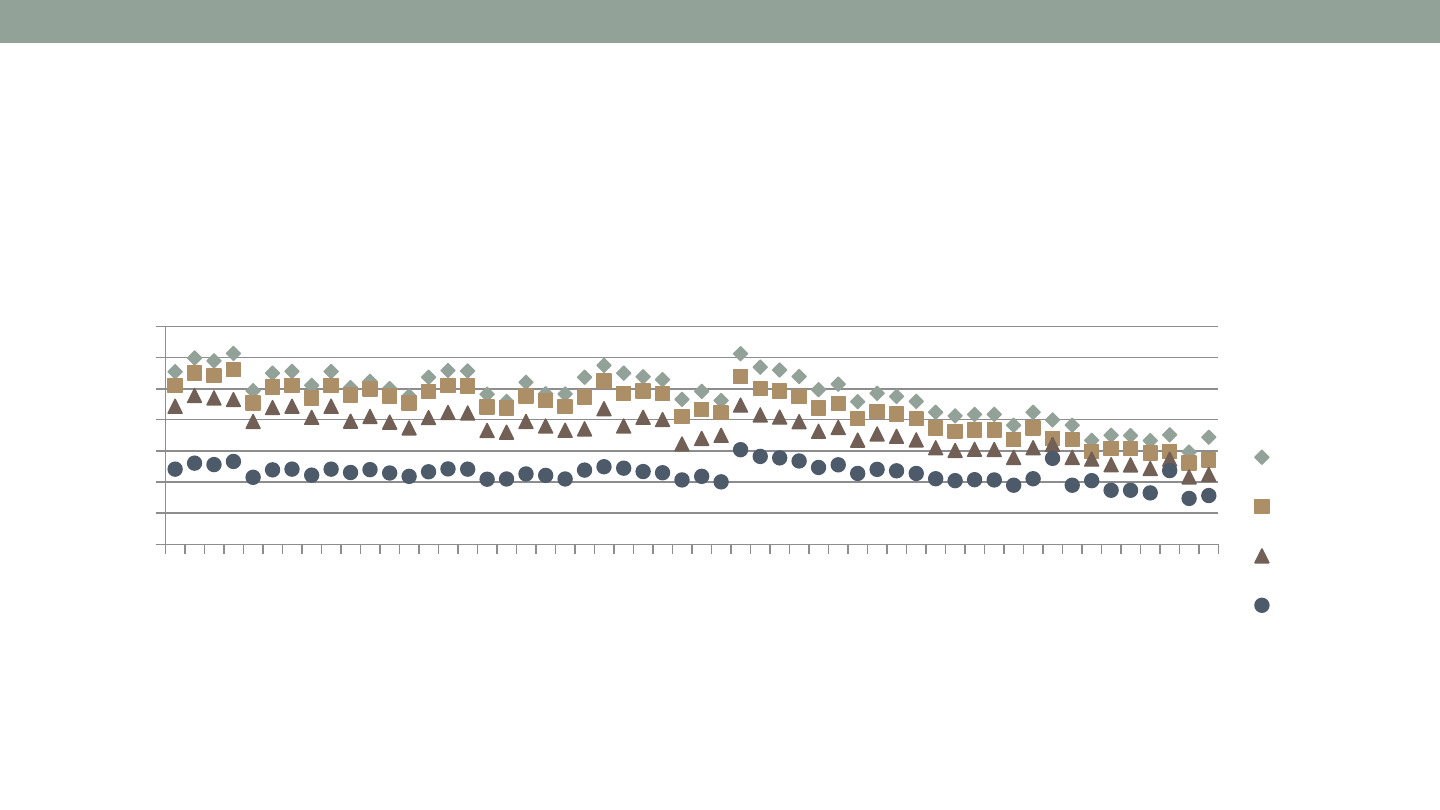

Gross yields on residential real estate vary dramatically by market, from over

10% for 1-beds in many locations to 4% or less for 4-beds in the dearest markets

0%

2%

4%

6%

8%

10%

12%

14%

Leitrim

Roscommon

Cavan

Longford

Donegal

Mayo

Sligo

Monaghan

Galway Co

Tipperary

Limerick Co

Clare

Kerry

Offaly

Carlow

Laois

Wexford

Waterford Co

Westmeath

Cork Co

Kilkenny

Waterford City

Louth

Limerick City

Meath

Kildare

Galway City

Cork City

Wicklow

Dublin 17

Dublin 22

Dublin 10

Dublin 24

West Dublin

Dublin 11

North Dublin

Dublin 15

Dublin 12

Dublin 20

Dublin 5

Dublin 13

Dublin 9

Dublin 7

Dublin 16

Dublin 8

Dublin 1

Dublin 18

Dublin 3

Dublin 14

Dublin 6W

South Dublin

Dublin 2

Dublin 6

Dublin 4

Average gross yield for residential real estate, 2020Q3, by property

size and location

1-bed

2-bed

3-bed

4-bed

Source: Analysis of Daft.ie Report; Markets are sorted from left to right by the 2020 price of a 3-bed semi-detached property

Ronan Lyons | Dilosk | November 2020

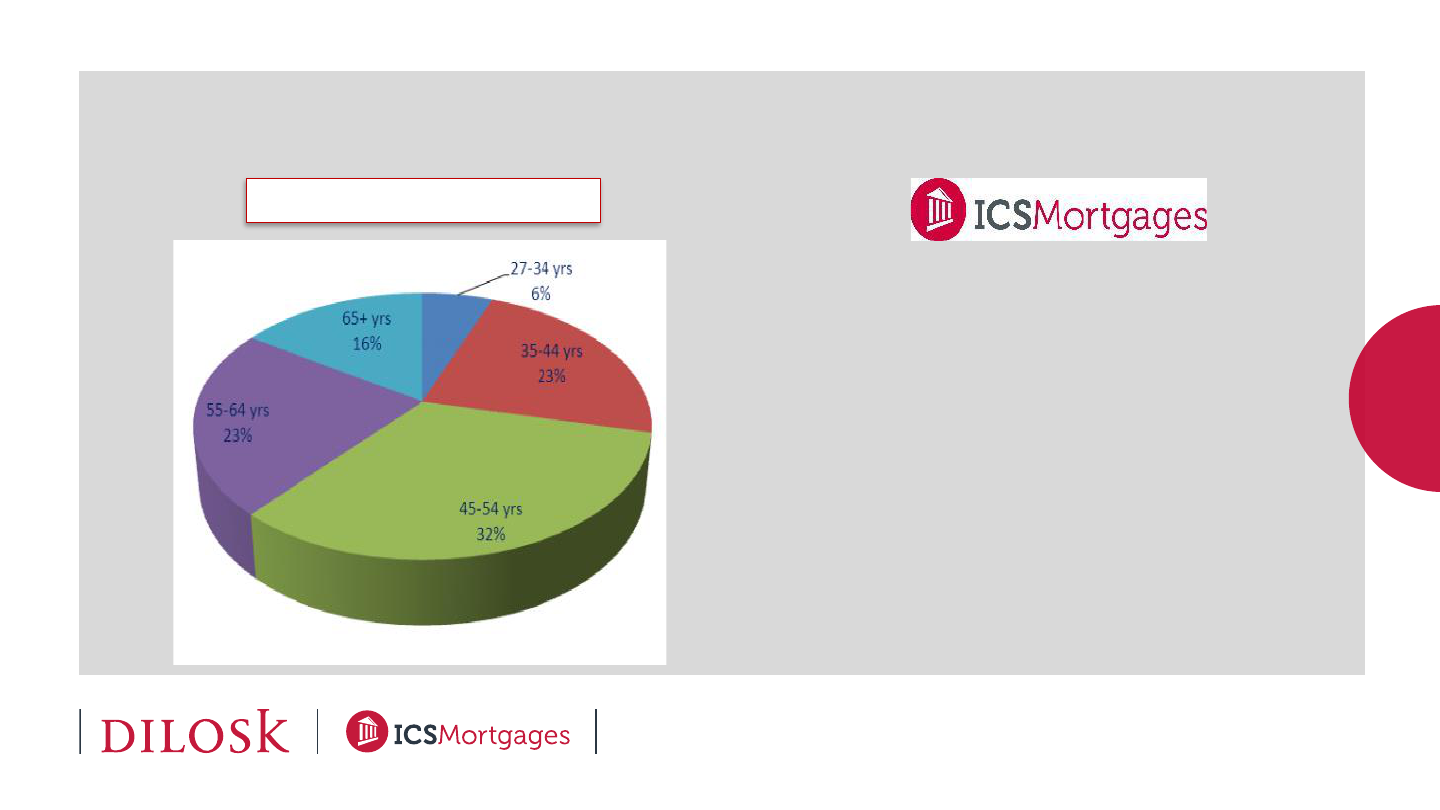

Age Profile of Landlords – Market v’s ICS Mortgages

The average age of our

borrower is 52 years

ESRI

Survey

MARKET

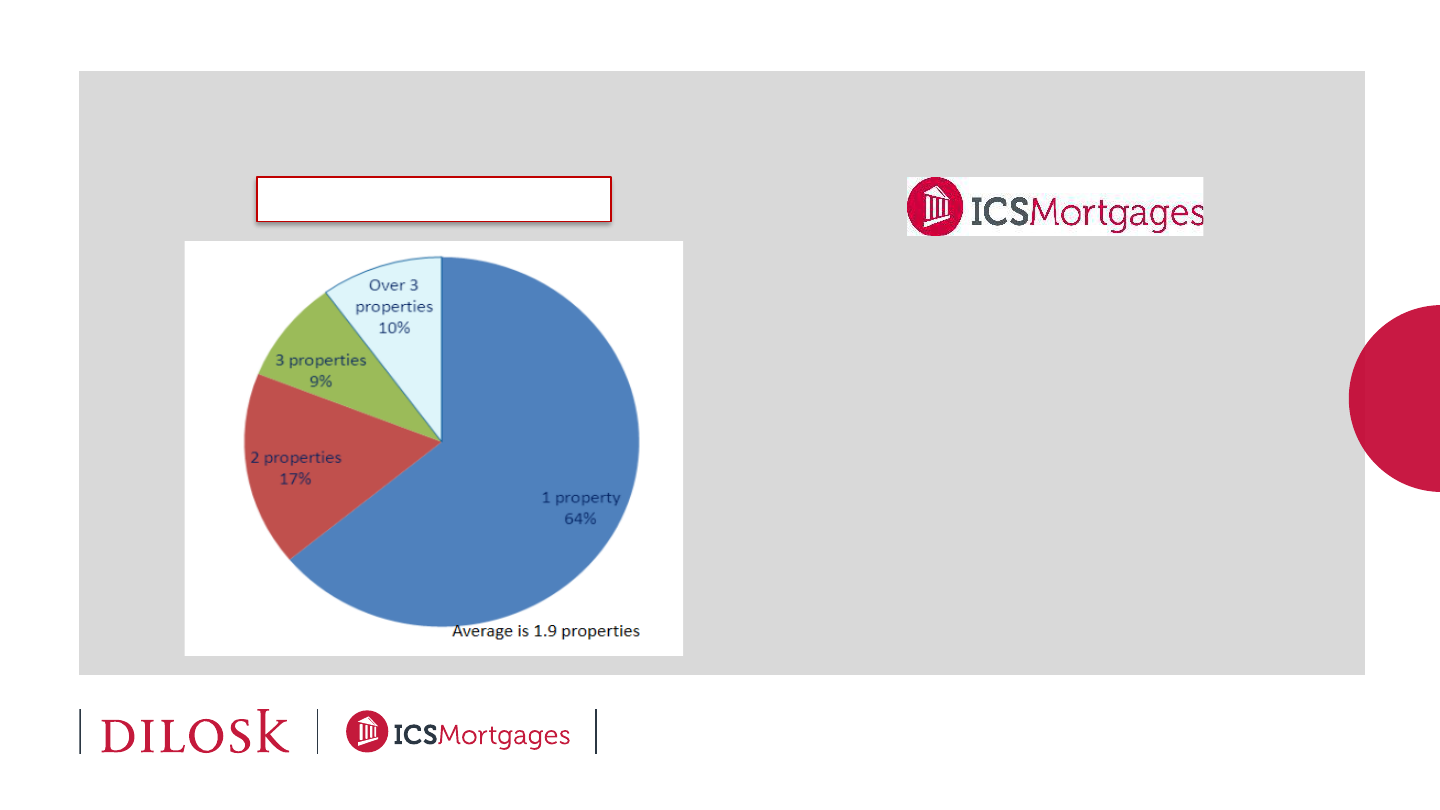

No. of investment properties – Market v’s ICS Mortgages

ESRI Survey

42% of our customers

have 3 or more

investment properties

MARKET

We would be delighted to do business with you !

Q&A

Dilosk DAC, trading as Dilosk and ICS Mortgages, is regulated by the Central Bank of Ireland

GT Purchasing Property with your Pension

Seminar - Market Analysis

Presented by - Enda Mc Guane

25th November 2020

Content

• Context – Who, What and COVID!

• Trends – Office, Industrial, Retail, Residential

• Residential Case Studies – Cork, Limerick, Galway

and Waterford

• Due Diligence

About WPM

• 50 Staff employed in 5 Offices.

• 7,000 residential/commercial units under Facilities/Estate Management.

• 800 Units Let and Managed.

• Manage/Oversee operations on over 3,000 student beds

• Provided Consultancy services - Operational Planning, Development

Appraisals

• Residential and Commercial - Sales/Valuations

• Recognised Expertise – 12 National awards in the last five years.

Context

Context

Office

• Galway Standing stock rents, at €301 per sq.

m,

• Vacancy rate of 4.9%

• Supply Issue, Covid Pause

• Cork - Prime Office €350 per sq.m

• Limerick - Prime Office €243 per sq.m

• Dublin City Centre €673.00 per m

• Dublin - South Suburbs €296.00

• Dublin - North Suburbs €221.00

• Dublin - West Suburbs €193.68

lndustrial

• Galway 5.3 per cent vacancy rate

• Prime Industrial units - €85 per sq.m

• Cork - Prime Industrial €91.50 per sq m.

• Limerick - Prime Industrial €70 per sq m

• Dublin - Prime Industrial €113 per sq m.

• Suburban Logistics and warehousing spaces

yields in demand.

• Online Retailing/ Last Mile

Retail

• ???????????

• Location

• Mixed Use

• Trend Acceleration

Residential

• Galway Metropolitan Area

• Average price: €1,164

• Year-on-year change: 2.4% (4.8%

Daft)

• Rent Protection Zone

• DATA

Case Study 1. - Galway

• Dunaras Student Village (PBSA)

• 3 Bed Apartment

• Sale Agreed August 2020 €190,000

• Rent 19/20 (pre covid) Gross €25,247

Net €16,488

• Rental Yield Gross 13.29% Net 8.68%

Case Study 2. - Galway

• Mervue Business & Technology Park

• Industrial Unit 19,287 sq.ft

• On Market €3.75m

• Annual rent of €187,209 increasing to

€298,871 in August 2021

• initial yield 5.% rising to 8% in August

2021

Case Study 3. - Galway

• Manor Court (West of City)

• 2 identical 2 bed

apartments

• Rent Pressure Zone

• Recently rented €9,672

p.a & €12,780 p.a

• Market Value €190,000

• Yields 5.1% & 6.7%

Case Study 4. - Cork

• Lee Vista, Cork City

• 2 Bed Apartment

• On Market €179,000

• Market Rent €17,400 p.a

• Rental Yield 9.7%

Case Study 5. - Limerick

• Dock Rd, City Centre

• 2 bed apartment

• Rent €12,000 p.a

• Market Value €115,000

• Yield 10.4%

Case Study 6. - Waterford

• Keizer House, High St,

Waterford

• On Market €120,000

• Market Rent €12,600p.a

• Rental Yield 10.5%

State Rental Supports and Conditions

Considerations – Cost of Building v Cost of

Buying

CITY

Public Build

Purchase

Galway

U

K

352,700

Sligo

253,900

156,400

Limerick

209,100

127,500

Cork

266,300

306,800

Waterford

170,100

178,000

Due Diligence

• Property Survey – Fire/Building Defects

• Title

• Leases

• Legislation – RPZ Expiry?

• Auctions – Read the small print!

• Service Charges/Maintenance Budget

• Research, Research, Research

48

Thank you

Q&A