Substantial Improvement/Damage 8-1

UNIT 8

SUBSTANTIAL IMPROVEMENT AND

SUBSTANTIAL DAMAGE

In this unit

This unit covers:

• The substantial improvement rule – how to regulate major additions and other

improvements to buildings in the floodplain.

• The substantial damage rule – how to regulate reconstruction and repairs to buildings

that have been severely damaged.

• Exceptions to the basic rules for some special cases.

Substantial Improvement/Damage 8-2

CONTENTS

INTRODUCTION.........................................................................................................8-3

A. SUBSTANTIAL IMPROVEMENT...........................................................................8-4

Projects Affected....................................................................................................8-4

Post-FIRM buildings.................................................................................................................... 8-5

The Formula...........................................................................................................8-5

Project cost..................................................................................................................................8-6

Market value................................................................................................................................8-6

Substantial Improvement Examples.....................................................................8-10

Example 1. Minor rehabilitation.................................................................................................8-10

Example 2. Substantial rehabilitation........................................................................................8-11

Example 3. Lateral addition—residential ..................................................................................8-12

Example 4. Lateral addition—nonresidential ............................................................................8-13

Example 5. Vertical addition—residential .................................................................................8-14

Example 6. Vertical addition—nonresidential ...........................................................................8-15

Example 7. Post-FIRM building—minor addition...................................................................... 8-16

Example 8. Post-FIRM building—substantial improvement...................................................... 8-17

B. SUBSTANTIAL DAMAGE....................................................................................8-18

Cost to Repair......................................................................................................8-18

Substantial Damage Examples............................................................................8-20

Example 1. Reconstruction of a destroyed building..................................................................8-20

Example 2. Substantially damaged structure............................................................................8-21

Substantial Damage Software..............................................................................8-22

Increased Cost of Compliance.............................................................................8-22

C. SPECIAL SITUATIONS .......................................................................................8-25

Exempt Costs.......................................................................................................8-25

Historic Structures................................................................................................8-25

Corrections of Code Violations.............................................................................8-26

Example .................................................................................................................................... 8-27

Substantial Improvement/Damage 8-3

INTRODUCTION

In previous units we focused on the rules and regulations that prevent or reduce damage from

floods to new buildings. But what happens when the owner wishes to make an improvement,

such as an addition, to an existing building? What if a building is damaged by a fire, flood or

other cause?

Basic rule: If the cost of improvements or the cost to repair the damage exceeds 50 percent of the

market value of the building, it must be brought up to current floodplain management standards.

That means an existing building must meet the requirements for new construction.

People who own existing buildings that are being substantially improved will be required to

make a major investment in them in order to bring them into compliance with the law. They will

not be happy. If the buildings have just been damaged, they will be financially strapped and your

elected officials will want to help them, not make life harder for them.

For these reasons, it is easy to see that this basic rule can be difficult to administer. It is also

the one time when your regulatory program can reduce flood damage to existing buildings.

That’s why this course devotes this unit to administering the substantial improvements and

substantial damage regulations.

In this reference guide, the term “building” is the same as the term “structure” in the NFIP

regulations. Your ordinance may use either term. The terms are reviewed in more detail in Unit 5,

Section E.

Substantial Improvement/Damage 8-4

A. SUBSTANTIAL IMPROVEMENT

44 CFR 59.1. Definitions: “Substantial improvement” means any reconstruction, rehabilitation,

addition or other improvement to a structure, the total cost of which equals or exceeds 50 percent of

the market value of the structure before the start of construction of the improvement.

This section provides information on determining whether a building has been substantially

improved and on what NFIP requirements apply.

PROJECTS AFFECTED

All building improvement projects worthy of a permit must be considered. These include:

• Remodeling projects.

• Rehabilitation projects.

• Building additions.

• Repair and reconstruction projects (these are addressed in more detail in Section B on

substantial damage)

If your community does not require permits for, say, reroofing, minor maintenance or

projects under a certain dollar amount, then such projects are not subject to the substantial

improvement requirements. However, if you have a larger project that includes reroofing, etc.,

then it must include the entire cost of the project.

One problem you may face is a builder trying to avoid the requirement by applying for a

permit for only part of the job and then later applying for another permit to finish the work. If

both applications are together worth more than 50% of the value of the building, the combined

project should be considered a substantial improvement and subject to the rules.

FEMA requires that the entire improvement project be counted as one. In order to help you

enforce this, you may want to count all applications submitted over, say, one year as one project.

Check with your attorney on whether your ordinance clearly gives you the authority to do this

and be sure to spell it out in the permit papers given to the applicant.

Some communities require that improvements be calculated cumulatively over several years.

All improvement and repair projects undertaken over a period of five years, 10 years or the life

of the structure are added up. When they total 50 percent, the building must be brought into

compliance as if it were new construction.

The Community Rating System credits keeping track of improvements

to enforce a cumulative substantial improvement requirement. It also

credits using a lower threshold than 50 percent. These credits are found

under Activity 430, Section 431.c and d in the CRS Coordinator’s Manual

and the CRS Application. See also CRS Credit for Higher Regulatory

Standards for example regulatory language.

Post-FIRM buildings

The rules do not address only pre-FIRM buildings—they cover all buildings, post-FIRM

ones included.

In most cases, a post-FIRM building will be properly elevated or otherwise compliant with

regulations for new construction. However, sometimes a map change results in a higher BFE or

change in FIRM zone. A substantial improvement to a post-FIRM building may require that the

building be elevated to protect it from the new, higher, regulatory BFE.

It should be remembered that all additions to a post-FIRM building must be elevated at least

as high as the BFE in effect when the building was built. (You can’t allow a compliant building

to become noncompliant by allowing additions at grade.) If a new, higher BFE has been adopted

since the building was built, additions that are substantial improvements must be elevated to the

new BFE.

THE FORMULA

A project is a substantial improvement if:

Cost of improvement project > 50 percent

Market value of the building

For example, if a proposed improvement project will cost $30,000 and the value of the

building is $50,000:

$30,000 = 0.6 (60 percent)

$50,000

The cost of the project exceeds 50 percent of the building’s value, so it is a substantial

improvement. The floodplain regulations for new construction apply and the building must meet

Substantial Improvement/Damage 8-5

Substantial Improvement/Damage 8-6

the post-FIRM construction requirements. If the project is an addition, only the addition has to

be elevated (see the examples later in this section).

The formula is based on the cost of the project and the value of the building. These two

numbers must be reviewed in detail.

Project cost

The cost of the project means all structural costs, including

• all materials

• labor

• built-in appliances

• overhead

• profit

• repairs made to damaged parts of the building worked on at the same time

A more detailed list is included in Figure 8-1.

To determine substantial improvement, you need a detailed cost estimate for the project,

prepared by a licensed general contractor, professional construction estimator or your office.

Your office must review the estimate submitted by the permit applicant. To verify it, you can

use your professional judgment and knowledge of local and regional construction costs, or you

can use building code valuation tables published by the major building code groups. These

tables can be used for determining estimates for particular replacement items if the type of

structure in question is listed in the tables.

There are two possible exemptions you should be aware of: 1) improvements to correct code

violations do not have to be included in the cost of an improvement or repair project and 2)

historic buildings can be exempted from substantial improvement requirements. These are

explained in more detail later on.

Market value

In common parlance, market value is the price a willing buyer and seller agree upon. The

market value of a structure reflects its original quality, subsequent improvements, physical age

of building components and current condition.

Substantial Improvement/Damage 8-7

However, market value for property can be different than that of the building itself. Market

value of developed property varies widely due to the desirability of its location. For example,

two houses of similar size, quality and condition will have far different prices if one is on the

coast, or in the best school district, or closer to town than the other—but the value of the

building materials and labor that went into both houses will be nearly the same.

For the purposes of determining substantial improvement, market value pertains only to the

structure in question. It does not pertain to the land, landscaping or detached accessory structures

on the property. Any value resulting from the location of the property should be attributed to the

value of the land, not the building.

Substantial Improvement/Damage 8-8

Items to be included

— All structural elements, including:

— Spread or continuous foundation footings and pilings

— Monolithic or other types of concrete slabs

— Bearing walls, tie beams and trusses

— Floors and ceilings

— Attached decks and porches

— Interior partition walls

— Exterior wall finishes (brick, stucco, siding) including painting and moldings

— Windows and doors

— Reshingling or retiling a roof

— Hardware

— All interior finishing elements, including:

— Tiling, linoleum, stone, or carpet over subflooring

— Bathroom tiling and fixtures

— Wall finishes (drywall, painting, stucco, plaster, paneling, marble, etc.)

— Kitchen, utility and bathroom cabinets

— Built-in bookcases, cabinets, and furniture

— Hardware

— All utility and service equipment, including:

— HVAC equipment

— Plumbing and electrical services

— Light fixtures and ceiling fans

— Security systems

— Built-in kitchen appliances

— Central vacuum systems

— Water filtration, conditioning, or recirculation systems

— Cost to demolish storm-damaged building components

— --- Labor and other costs associated with moving or altering undamaged building

components to accommodate improvements or additions

— --- Overhead and profits

Items to be excluded

— Plans and specifications

— Survey costs

—

Permit fees

— Post-storm debris removal and clean up

— Outside improvements, including:

— Landscaping

— Sidewalks

— Fences

— Yard lights

— Swimming pools

— Screened pool enclosures

— Detached structures (including garages, sheds and gazebos)

— Landscape irrigation systems

Figure 8-1. Items included in calculating cost of the project

Substantial Improvement/Damage 8-9

Acceptable estimates of market value can be obtained from these sources:

• An independent appraisal by a professional appraiser. The appraisal must exclude the

value of the land and not use the “income capitalization approach” which bases value

on the use of the property, not the structure.

• Detailed estimates of the structure’s actual cash value— the replacement cost for a

building, minus a depreciation percentage based on age and condition. For most

situations, the building’s actual cash value should approximate its market value. Your

community may prefer to use actual cash value as a substitute for market value,

especially where there is not sufficient data or enough comparable sales.

• Property values used for tax assessment purposes with an adjustment recommended

by the tax appraiser to reflect current market conditions (adjusted assessed value).

• The value of buildings taken from NFIP claims data (usually actual cash value).

• Qualified estimates based on sound professional judgment made by the staff of the

local building department or tax assessor’s office.

Some market value estimates are often used only as screening tools (i.e., NFIP claims data

and property appraisals for tax assessment purposes) to identify those structures where the

substantial improvement ratios are obviously less than or greater than 50 percent (i.e., less than

40 percent or greater than 60 percent). For structures that fall in the 40 percent to 60 percent

range, more precise market value estimates are sometimes necessary.

SUBSTANTIAL IMPROVEMENT EXAMPLES

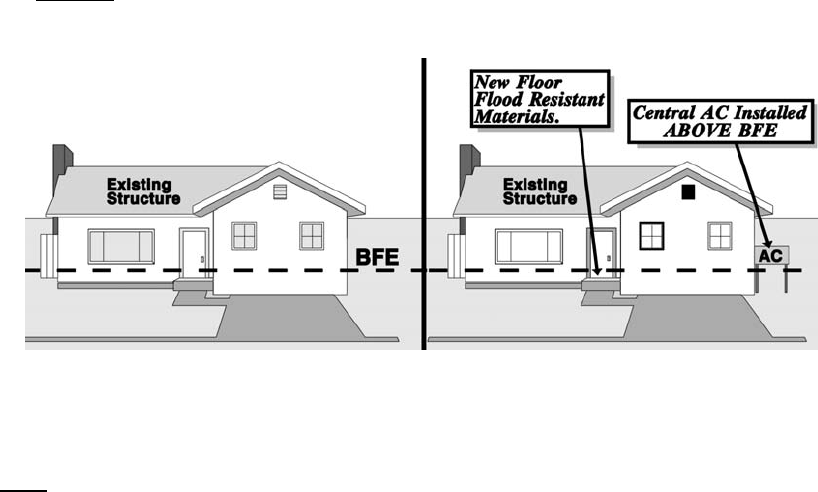

Example 1. Minor rehabilitation

A rehabilitation is defined as an improvement made to an existing structure which does not

affect the external dimensions of the structure.

If the cost of the rehabilitation is less than 50 percent of the structure’s market value, the

building does not have to be elevated or otherwise protected. However, it is advisable to

incorporate methods to reduce flood damage, such as use of flood-resistant materials and

installation of electrical, heating and air conditioning units above the BFE.

Figure 8-2 shows a building that had a small rehabilitation project. Central air conditioning

was installed and the electrical system was upgraded. The value of the building before the

project was $60,000. The value of the project was $12,000:

$12,000 = 0.2 (20 percent) The project costs less than 50 percent of the

$60,000 building, so this is not a substantial improvement.

Figure 8-2. Minor rehabilitations use flood-resistant methods and materials

Neither structure would benefit from post-FIRM flood insurance

rates because they are not elevated.

Note: To gauge what happens to flood insurance premiums if a substantially improved

building is not brought up to post-FIRM standards, see Figures 7-7 through 7-12.

Substantial Improvement/Damage 8-10

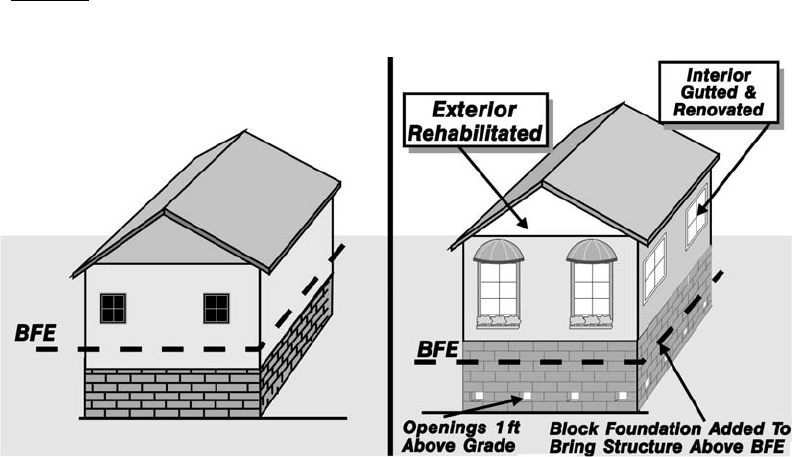

Example 2. Substantial rehabilitation

If the rehab costs more than 50 percent of the value of the building, your ordinance requires

that an existing structure be elevated and/or the basement filled to meet the elevation standard.

Figure 8-3 shows a building that has been allowed to run down. It’s market value is $35,000.

To rehab it will require gutting the interior and replacing all wallboard, built-in cabinets,

bathroom fixtures and furnace. The interior doors and flooring will be repaired. The house will

get new siding and a new roof. The cost of this rehab will be $25,000:

$25,000 = 71.4 percent Because total cost of the project is greater

$35,000 than 50 %the rehab is a substantial improvement

Figure 8-3. substantially rehabilitated building elevated above the BFE.

In A Zones, elevation may be on fill, crawlspace, columns, etc. In V Zones, only pilings, columns or

other open foundations are allowed. The new structure would benefit from post-FIRM flood insurance

rates.

Substantial Improvement/Damage 8-11

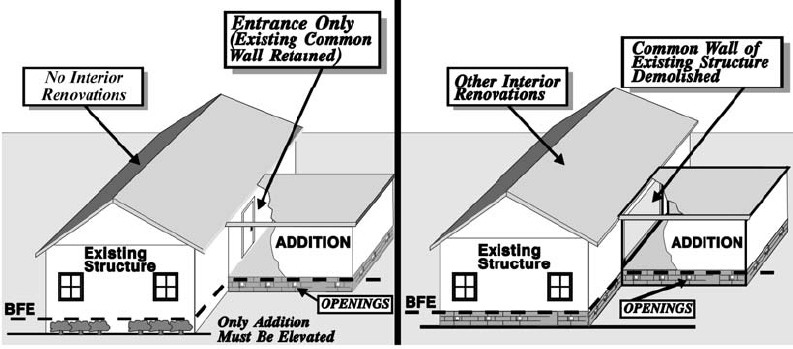

Example 3. Lateral addition—residential

Additions are improvements that increase the square footage of a structure. Commonly, this

includes the structural attachment of a bedroom, den, recreational room garage or other type of

addition to an existing structure. Note that if one building is attached to another through a

covered breezeway or similar connection, it is a separate building and not an addition.

When an addition is a substantial improvement, the addition must be elevated or

floodproofed, providing that improvements to the existing structure are minimal. Figures 8-4

and 8-5 illustrate lateral additions that are compliant.

Depending on the flood zone and details of the project, the existing building may not have to

be elevated. The determining factors are the common wall and what improvements are made to

the existing structure. If the common wall is demolished as part of the project, then the entire

structure must be elevated. If only a doorway is knocked through it and only minimal finishing is

done, then only the addition has to be elevated.

In A Zones only, if significant improvements are made to the existing structure (such as a

kitchen makeover), both it and the addition must be elevated and otherwise brought into

compliance. Some states and many communities require that both the existing structure and

lateral additions be elevated in all cases.

In V Zones, the existing structure always has to be elevated, placed on an engineered

foundation system, etc., when an addition is proposed that constitutes a substantial improvement.

This is due to the “free-of obstruction” standard whereby the lower existing structure would

obstruct the storm surge, causing damage to the addition.

Figure 8-4. Lateral additions to a residential building in an A Zone.

In V Zones, the entire building must be elevated on pilings, columns or other open foundations. The

Substantial Improvement/Damage 8-12

structure on the left would not benefit from post-FIRM flood insurance rates because it was not elevated.

Example 4. Lateral addition—nonresidential

A substantial improvement addition to a nonresidential building may be either elevated or

floodproofed. Otherwise, all the criteria for residential buildings reviewed in Example 3 must be

met.

If floodproofing is used, the builder must ensure that the wall between the addition and the

original building is floodproofed. Floodproofing is not allowed as a construction measure in V

Zones.

Figure 8-5. Lateral addition to a nonresidential building in an A Zone.

This approach is not allowed in V Zones. The structure would not benefit from post-FIRM flood

insurance rates because the original building was not elevated or flood-proofed.

Substantial Improvement/Damage 8-13

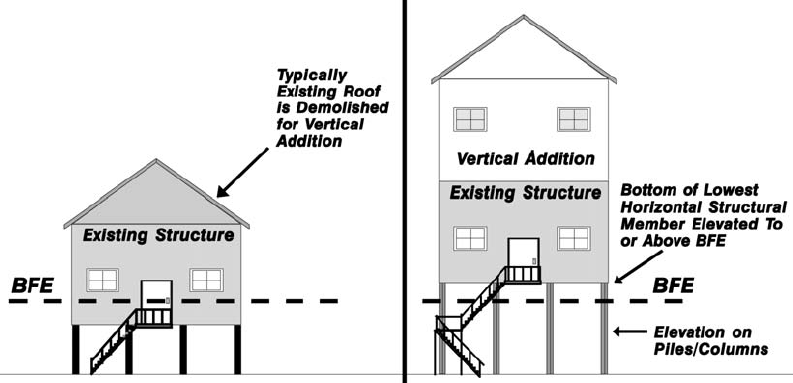

Example 5. Vertical addition—residential

When the proposed substantial improvement is a full or partial second floor, the entire

structure must be elevated (Figure 8-6). In this instance, the existing building provides the

foundation for the addition. Failure of the existing building would result in failure of the

addition, too.

Figure 8-6. Vertical addition to a residential building in a V Zone.

The new structure would benefit from post-FIRM flood insurance rates.

Substantial Improvement/Damage 8-14

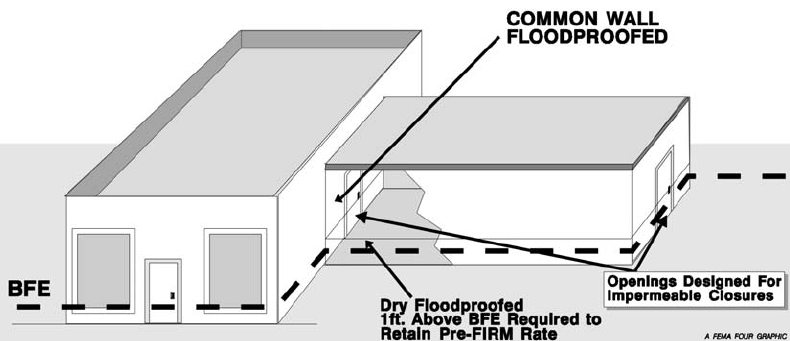

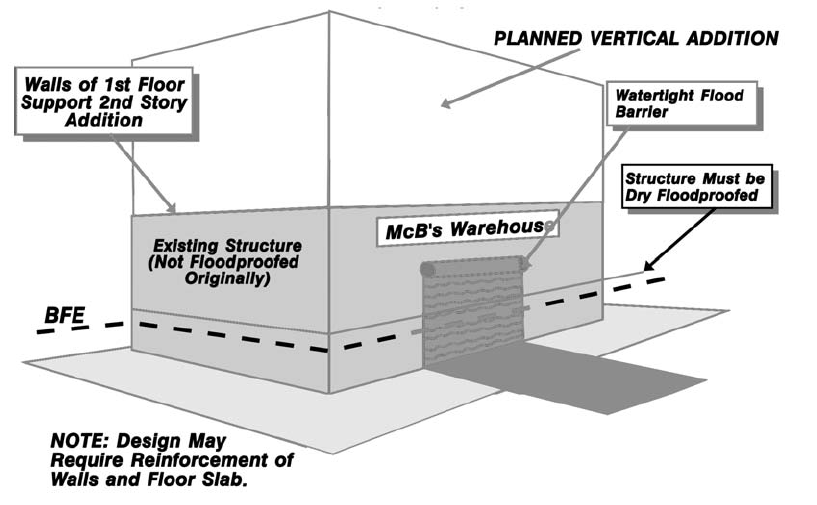

Example 6. Vertical addition—nonresidential

When the proposed substantial improvement is a full or partial second floor, the entire

structure must be elevated or floodproofed (Figure 8-7).

The owner could obtain post-FIRM rates on the building if it is floodproofed to one foot

above the BFE and he has a floodproofing certificate signed by a registered engineer. An

optional approach is to elevate the entire building and obtain an elevation certificate.

Figure 8-7. Vertical addition to a nonresidential building in an A Zone.

The new floodproofed structure would benefit from post-FIRM flood insurance rates.

Substantial Improvement/Damage 8-15

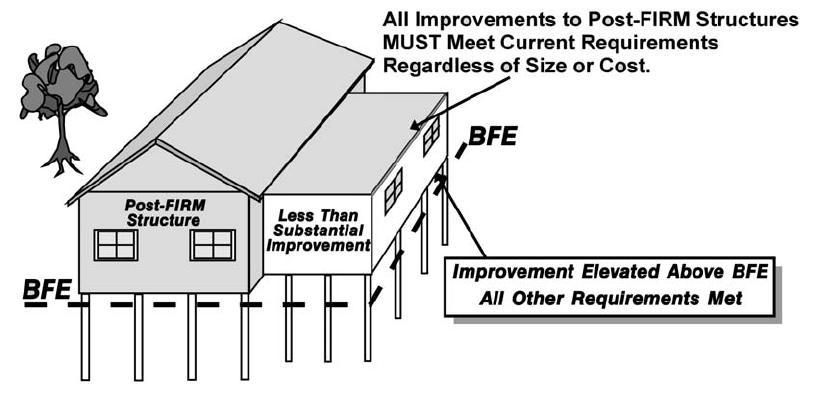

Example 7. Post-FIRM building—minor addition

All additions to post-FIRM buildings are defined as new construction and must meet the

requirements of your floodplain management ordinance regardless of the size or cost of the

addition (Figure 8-8). A small addition to a residential structure that is not a substantial

improvement must be elevated at least as high as the BFE in effect when the building was built.

Minor additions to nonresidential structures can be floodproofed to the BFE.

If a map revision has taken place and the BFE has increased, only additions that are

substantial improvements have to be elevated to the new BFE or flood-proofed (nonresidential

buildings only).

Figure 8-8. Small additions to post-FIRM buildings must be elevated.

Substantial Improvement/Damage 8-16

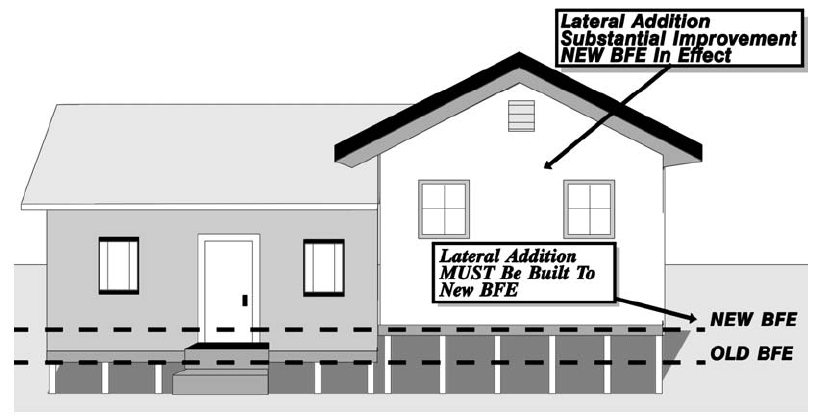

Example 8. Post-FIRM building—substantial improvement

Substantial improvements made to a post-FIRM structure must meet the requirements of the

current ordinance. Figure 8-9 shows a lateral addition made after a map revision took place and

the BFE was increased.

Figure 8-9. Substantial improvements to post-FIRM buildings must be elevated above the

new BFE. Nonresidential buildings may be floodproofed

Substantial Improvement/Damage 8-17

Substantial Improvement/Damage 8-18

B. SUBSTANTIAL DAMAGE

44 CFR 59.1. Definitions: "Substantial damage" means damage of any origin sustained by a

structure whereby the cost of restoring the structure to its before damaged condition would equal or

exceed 50 percent of the market value of the structure before the damage occurred.

Two key points:

• The damage can be from any cause—flood, fire, earthquake, wind, rain, or other

natural or human-induced hazard.

• The substantial damage rule applies to all buildings in a flood hazard area, regardless

of whether the building was covered by flood insurance.

The formula is essentially the same as for substantial improvements:

Cost to repair > 50 percent

Market value of the building

Market value is calculated in the same way as for substantial improvements. Use the pre-

damage market value.

COST TO REPAIR

Notice that the formula uses “cost to repair,” not “cost of repairs.” The cost to repair the

structure must be calculated for full repair to the building’s before-damage condition, even if the

owner elects to do less. It must also include the cost of any improvements that the owner has

opted to include during the repair project.

The total cost to repair includes the same items listed in Figure 8-1. As shown in Example 2

below, properly repairing a flooded building can be more expensive than people realize. The

owner may opt not to pay for all of the items needed. The owner may:

• Do some of the work, such as removing and discarding wallboard.

• Obtain some of the materials free.

• Have a volunteer organization, such as the Mennonites, do some of the work.

• Decide not to do some repairs, such as choosing to nail down warped flooring rather

than replace it.

Substantial Improvement/Damage 8-19

Basic rule: Substantial damage is determined regardless of the actual cost to the owner. You must

figure the true cost of bringing the building back to its pre-damage condition using qualified labor and

materials obtained at market prices.

The permit office and the owner may have serious disagreements over the total list of needed

repairs and their cost, as the owner has a great incentive to show less damage than actually

occurred in order to avoid the cost of bringing the building into compliance. Here are four things

that can help you:

• Get the cost to repair from an objective third-party or undebatable source, such as:

- A licensed general contractor.

- A professional construction estimator.

- Insurance adjustment papers (exclude damage to contents).

- Damage assessment field surveys conducted by building inspection,

emergency management or tax assessment agencies after a disaster.

- Your office.

• Even if your office does not prepare the cost estimate, it needs to review the estimate

submitted by the permit applicant. You can use your professional judgment and

knowledge of local and regional construction costs. Or, you can use building code

valuation tables published by the major building code groups.

• Use an objective system that does not rely on varying estimates of market value or

different opinions of what needs to be repaired. The Substantial Damage Estimator

Program discussed later in this section will do this.

• Publicize the need for the regulations and the benefits of protecting buildings from

future flooding. A well-educated public won’t argue as much as one that sees no need

for the requirement.

• Help the owner find financial assistance to meet the extra cost of complying with the

code. If there was a disaster declaration, there may be sources of financial assistance

as discussed in the next unit. If the owner had flood insurance and the building was

substantially damaged by a flood, the new Increased Cost of Compliance coverage

will help (see next section).

SUBSTANTIAL DAMAGE EXAMPLES

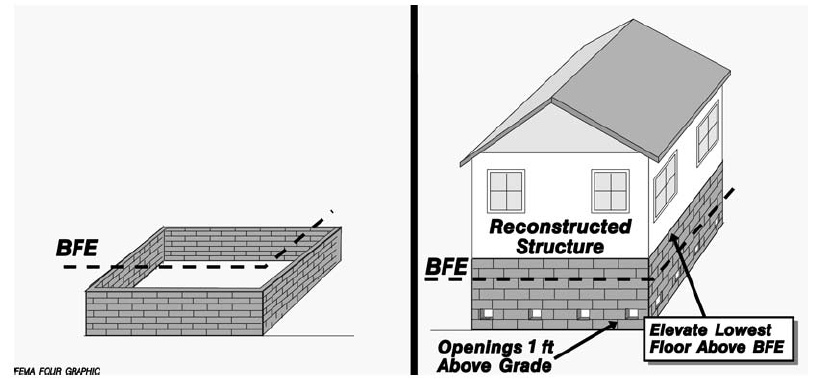

Example 1. Reconstruction of a destroyed building

Reconstructions are cases where an entire structure is destroyed, damaged, purposefully

demolished or razed, and a new structure is built on the old foundation or slab. The term also

applies when an existing structure is moved to a new site.

Reconstructions are, quite simply, “new construction.” They must be treated as new

buildings.

Razed or “totaled” building Reconstruction on

with remaining foundation existing foundation

Figure 8-10. A reconstructed house is new construction.

This example is for A Zones only. A new building in the V Zone must be elevated on piles or columns.

Substantial Improvement/Damage 8-20

Substantial Improvement/Damage 8-21

Example 2. Substantially damaged structure

To determine if a damaged structure meets the threshold for substantial damage, the cost of

repairing the structure to its before-damaged condition is compared to the market value of the

structure prior to the damage. The estimated cost of the repairs must include all costs necessary

to fully repair the structure to its before-damaged condition.

If equal to or greater than 50 percent of that structure’s market value before damage, then the

structure must be elevated (or floodproofed if it is nonresidential) to or above the level of the

base flood, and meet other applicable local ordinance requirements. This is the basic requirement

for substantial damage.

Figure 8-11 graphically illustrates the amount of damage that can occur to a building flooded

only four feet deep. Even though the structure appears sound and there are no cracks or breaks in

the foundation, the total cost of repair can be significant.

The cost of repair after a flood that simply soaked the building will typically include the

following structural items:

— Remove all wallboard and insulation.

— Install new wallboard and insulation.

— Tape and paint.

— Remove carpeting and vinyl flooring.

— Dry floor, replace warped flooring.

— Replace cabinets in the kitchen and bathroom.

— Replace built-in appliances.

— Replace hollow-core interior doors.

— Replace furnace and water heater.

— Clean and disinfect duct work.

— Repair porch flooring and front steps.

— Clean and test plumbing (licensed plumber may be required).

— Replace outlets and switches, clean and test wiring (licensed electrician may be

required).

Note: See also Figures 7-7 through 7-12 for what happens to flood insurance premiums if a

substantially damaged building is granted a variance and is not brought up to post-FIRM

standards.

Figure 8-11. Even slow moving floodwater can cause substantial damage.

SUBSTANTIAL DAMAGE SOFTWARE

FEMA has developed a software program to help local officials make substantial damage

determinations. The software is based on Microsoft Access, but is self-contained and does not

require any software in addition to a Windows operating system.

The software comes with a manual, Guide on Estimating Substantial Damage Using the

NFIP Residential Substantial Damage Estimator, FEMA 311. This includes a user’s manual and

worksheets that allow the calculations to be done manually.

Contact your FEMA Regional Office for a copy of the software package and help in using it.

Following a major disaster declaration, training sessions and technical assistance may be

available.

INCREASED COST OF COMPLIANCE

On June 1, 1997, the NFIP began offering additional coverage to all holders of structural

flood insurance policies. This coverage is called Increased Cost of Compliance or ICC.

Substantial Improvement/Damage 8-22

The name refers to cases where the local floodplain management ordinance requires

elevation or retrofitting of a substantially damaged building. Under ICC, the flood insurance

policy will not only pay for repairs to the flooded building, it will pay up to $30,000 to help

cover the additional cost of complying with the ordinance. This is available for any flood

insurance claim and, therefore, is not dependent on the community receiving a disaster

declaration.

There are some limitations to ICC:

• It’s only available if there was a flood insurance policy on the building before the

flood.

• It covers only damage caused by a flood.

• Claims are limited to $30,000 per structure.

• Claims must be accompanied by a substantial damage determination by the

floodplain ordinance administrator.

It should also be mentioned that a portion of the rest of the claim payment may help meet the

cost of bringing the building up to code. For example, if there was foundation damage, the

regular claim will pay for the cost of repairing or replacing the foundation. The ICC funds would

only be needed for the extra costs of raising the foundation higher than it was before.

An ICC claim cannot be paid unless the community has determined the building to be

substantially damaged and requires that the building comply with local ordinance requirements.

For further information on how ICC coverage works and how you can help policyholders in your

community qualify for the coverage, refer to National Flood Insurance Program’s Increased

Cost of Compliance Coverage: Guidance for State and Local Officials, FEMA 301.

In certain cases, an ICC claim can be filed if the building is repetitively flooded, and has had

two or more claims averaging 25% or more of building value within a ten-year period, provided

the community has language in the flood damage ordinance that implements the substantial

damage rule in these cases.

Figure 8-12 has example ordinance language. This language exceeds the minimum NFIP

requirements, but would be needed if you wanted to trigger the ICC provision for repetitively

damaged buildings.

The Community Rating System credits keeping track of improvements

to enforce a cumulative substantial improvement requirement. The 1999

CRS Coordinator’s Manual credits the ordinance language in Figure 8-12.

These credits are found under Activity 430, Section 431.c in the CRS

Coordinator’s Manual and the CRS Application.

Substantial Improvement/Damage 8-23

Substantial Improvement/Damage 8-24

Option 1

A. Adopt the Following Definition:

“Repetitive Loss” means flood-related damage sustained by a structure on two separate

occasions during a 10-year period for which the cost of repairs at the time of each such flood

event, on the average, equals or exceeds 25 percent of the market value of the structure before

the damage occurred.

B. And modify the “substantial improvement” definition as follows:

“Substantial Improvement” means any reconstruction, rehabilitation, addition, or other

improvement of a structure, the cost of which equals or exceeds 50 percent of the market value

of the structure before the “start of construction” of the improvement. This term includes

structures which have incurred “repetitive loss” or “substantial damage”, regardless of the actual

repair work performed.

--------------------------------------------------------------------------------------------------------------------------------

Option 2

Modify the substantial damage definition as follows:

“Substantial Damage” means damage of any origin sustained by a structure whereby the cost of

restoring the structure to its before damaged condition would equal or exceed 50 percent of the

market value of the structure before the dam-age occurred. Substantial damage also means

flood-related damage sustained by a structure on two separate occasions during a 10-year

period for which the cost of repairs at the time of each such flood event, on the average, equals

or exceeds 25 percent of the market value of the structure before the damage occurred.

--------------------------------------------------------------------------------------------------------------------------------

NOTE 1: Communities need to make sure that these definitions are tied to the floodplain

management requirements for new construction and substantial improvements and to any other

requirements of the ordinance, such as the permit requirements, in order to enforce this

provision.

NOTE 2: An ICC Claim Payment is ONLY made for flood-related damage. The substantial

damage part of the definition must still include “damage of any origin” to be compliant with the

minimum NFIP Floodplain Management Regulations.

Figure 8-12. Sample ordinance language for ICC repetitive loss definitions

Source: -- Increased Cost of Compliance Coverage: Guidance for State and Local

Officials, FEMA-301, September 2003. This language is only needed to trigger an ICC

payment for a repetitive loss. No ordinance changes are needed for the ICC coverage

for substantial damage.

Substantial Improvement/Damage 8-25

C. SPECIAL SITUATIONS

As explained in previous sections, the substantial improvement and substantial damage

requirements affect all buildings regardless of the reason for the improvement or the cause of the

damage. There are three special situations you should be aware of: exempt costs, historic

buildings and corrections of code violations.

EXEMPT COSTS

Certain costs related to making improvements or repairing damaged buildings do not have to

be counted toward the cost of the improvement or repairs. These include:

• Plans and specifications.

• Surveying costs.

• Permit fees.

• Demolition or emergency repairs made for health or safety reasons or to prevent

further damage to the building.

• Improvements or repairs to items outside the building, such as the driveway, fencing,

landscaping and detached structures.

HISTORIC STRUCTURES

Historic structures are exempted from the substantial improvement requirements subject to

the criteria listed below. The exemption can be granted administratively if the current NFIP

definitions of substantial improvement and historic structure are included in your ordinance, or

they can be granted through a variance procedure.

In either case, they are usually granted subject to conditions.

If the improvements to a historic structure meet the following three criteria and are approved

by the community, the building will not have to be elevated or floodproofed. It can also retain its

pre-FIRM flood insurance rating status.

1. The building must be a bona fide “historic structure.” Figure 7-13 has the definition

that must be followed.

Substantial Improvement/Damage 8-26

2. The project must maintain the historic status of the structure. If the proposed

improvements to the structure will result in it being removed from or ineligible for the National

Register or federally-certified state or local inventory, then the proposal cannot be granted an

exemption from the substantial improvement rule.

The best way to make such determinations is to seek written review and approval of

proposed plans by the local historic preservation board, if it is federally-certified, or by the state

historic preservation office. If the plans are approved, you can grant the exemption. If not, no

exemption can be permitted.

3. Take all possible flood damage reduction measures. Even though the exemption to the

substantial improvement rule means the building does not have to be elevated to or above BFE,

or be renovated with flood-resistant materials that are not historically sensitive, many things can

and should be done to reduce the flood damage potential. Examples include:

• Locating mechanical and electrical equipment above the BFE or flood-proofing it.

• Elevating the lowest floor of an addition to or above the BFE with the change in floor

elevation disguised externally.

CORRECTIONS OF CODE VIOLATIONS

The NFIP definition of substantial improvement includes another exemption:

44 CFR 59.1 Definitions: "Substantial improvement" means …. The term does not, however,

include … Any project for improvement of a structure to correct existing violations of state or local

health, sanitary, or safety code specifications which have been identified by the local code

enforcement official and which are the minimum necessary to assure safe living conditions

Note the key words in this exemption: correct existing violations, identified by the local

official, and minimum necessary to assure safe conditions. This language was included in order

to avoid penalizing property owners who had no choice but to make improvements to their

buildings or face condemnation or revocation of a business license.

This exemption was intended for involuntary improvements or violations that existed before

the improvement permit was applied for or before the damage occurred—for example, a

restaurant owner who must upgrade the wiring in his kitchen in order to meet current local and

state health and safety codes.

You can only exempt the items specifically required by code. For example, if a single stair

tread was defective and had to be replaced, do not exempt the cost of rebuilding the entire

stairway. Similarly, count only replacement in like kind and what is minimally necessary. If the

Substantial Improvement/Damage 8-27

owner chooses to upgrade the quality of a code-required item, the extra cost is not exempt from

the formula—it’s added to the true cost of the improvement or repairs.

Unfortunately, many property owners and builders pressure local building official to exclude

“code violation corrections” from their voluntary improvement proposals. There are “code

violations” in all structures built before the current code was enacted. In many cases, those

elements must be brought up to code as part of an improvement project.

This is very different from a code violation citation that forces a property owner to correct

those violations and make improvements that were otherwise not planned. The building official

must know about and document the violations before or at the time the permit is issued.

Example

A small business in a 40-year old building was damaged by a fire. The building’s pre-fire

market value was $100,000. The insurance adjuster and the permit office concluded that the total

cost to repair would be $45,000.

However, the community’s building code states that whenever an applicant applies for a

permit to modify or improve a building, the building must be brought up to code. This building

would need the following additional work:

• Replace unsafe electrical wiring.

• Install missing fire exit signs, smoke detectors and emergency lighting.

• Widen the front door and install a ramp to make the business accessible to

handicapped and mobility-impaired people.

The total cost of these code requirements would be $8,000. However, since these were

required by the code before the fire occurred, they would not have to be counted toward the cost

to repair. Based on the basic formula:

$45,000 = 0.45 or 45% The building is not declared

$100,000 substantially damaged

In this example, the building can be repaired without elevating or floodproofing. However,

the permit office should strongly recommend incorporating flood protection measures and flood

resistant materials in the repair project (as in the example in Figure 8-2).