WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 1 Last Updated 1/13/22

MATTHIESEN, WICKERT & LEHRER, S.C.

Hartford, WI ❖ New Orleans, LA ❖ Orange County, CA

❖ Austin, TX ❖ Jacksonville, FL ❖ Boston, MA

Phone: (800) 637-9176

gwickert@mwl-law.com

www.mwl-law.com

PAYMENT OF SALES TAX AFTER VEHICLE TOTAL LOSS IN ALL 50 STATES

Approximately 12% to 14% of all accidents result in a total loss, a number which has been trending upward since 2002. Insurance companies faced with first-party claims

on policies are responsible for paying the actual cash value (ACV) or market value of an insured’s vehicle so the insured can replace it with a similar vehicle. In addition,

they may also be responsible for other costs associated with purchasing a new vehicle, such as sales tax, title, and vehicle registration. Approximately two-thirds of the

states require insurance companies to pay for the sales tax after an insured replaces a crashed vehicle with a new or used one. However, that doesn't necessarily mean

insurers in those states are going to offer to pay sales tax up front. Nor does it mean insurers in states that don’t require those reimbursements will refuse to pay.

Insurers will generally reimburse for those costs on the total loss settlement for an insured’s original vehicle, not the replacement vehicle. For example, if the insured

receives $5,000 from the insurer for its old vehicle and uses that money toward the purchase of a new vehicle for $20,000, the insurance company might be responsible

for payment of sales tax on the $5,000, but not the $20,000. Frequently, the requirement to pay sales tax after a total loss is discussed within a state’s unfair claim

settlement practices laws and/or regulations.

A “total loss” occurs when the insured property is totally destroyed or is damaged in such a way that it can be neither recovered nor repaired for further use, or the

insured is irretrievably deprived of it. Put another way, a vehicle is considered a total loss when the cost to repair it and return it to its pre-loss condition is greater than

the pre-accident value of the vehicle. In some states, when a vehicle’s repair costs exceed a certain percentage of its ACV, it is deemed a total loss. In most, but not all

cases, a total loss vehicle is more expensive to repair than the vehicle’s ACV. Insurance companies also consider whether repairs can be safely completed on the vehicle.

Other factors that insurance companies take into consideration are the vehicle’s year, make, model, mileage, physical wear and tear, and extent of damage caused in

the accident. When and whether a vehicle involved in a collision is “totaled” for first-party insurance purposes or for purposes of handling salvage and branding titles of

vehicles which are “salvage” are two different but related concepts and practices within the insurance industry which are often conflated. A chart entitled “Automobile

Total Loss Thresholds In All 50 States” can be found HERE.

There are two types of claims which can be made following a total loss accident, first-party and third-party, both of which are discussed in this chart.

FIRST-PARTY CLAIMS

These are collision insurance claims made by the vehicle owner/policyholder against his own insurance company to recover an insurance payment under the terms of

the policy. First-party claim payments are governed by applicable policy language. The amount of the payment depends on the policy but could be the ACV or

Replacement Cost Value (RCV) in some cases. It might also include applicable state fees and sales tax. In most states, the maximum that will be paid for a totaled vehicle

will be the amount necessary to replace the vehicle with a comparable used vehicle (plus sales tax, title and registration fees). This is referred to as the vehicle’s ACV.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 2 Last Updated 1/13/22

An exception to this rule would be if the policy provides for RCV endorsement as part of the Collision and Comprehensive Coverage. Terms to be familiar with in first-

party insurance claims include:

Actual Cash Value (ACV): A measure insurance companies use when deciding how much to pay for a damaged vehicle. It is also sometimes referred to as “Actual

Cost Value.” It’s commonly defined as the cost of replacing the insured property, less depreciation for age, wear and tear. (“depreciated replacement cost”). Some

courts have held that ACV is equal to FMV, rather than the depreciated replacement cost.

Replacement Cost Value (RCV): This is the amount of money necessary to purchase the same or similar product at today’s prices, even if it’s more than the insured

paid for the product originally. With replacement cost coverage, many insurance companies will pay the ACV of an item and require the insured to submit a receipt

for the new item before paying you the remainder. “Replacement cost insurance” is optional additional coverage that may be purchased for casualty insurance to

insure against the possibility that the improvements will cost more than the ACV and that the insured cannot afford to pay the difference.

Fair Market Value (FMV): This is the reasonable sales price which a willing buyer and seller, knowing comparable prices in the market and knowing all relevant

facts related to the subject property being sold, would agree to. Three well-recognized guides to appraisal have evolved, all of which take the property’s pre-loss

physical depreciation into account: (1) the cost approach; (2) the comparable sales approach; and (3) the income or economic approach.

Whether or not to include sales tax in a first-party claim payment has been closely looked at in recent years. Sixteen states (AZ, CT, CA, CO, IL, KY, MD, NE, NJ, NV, OH,

OK, PA, VA, WA, and WI) have insurance commissioners/departments which have cited insurers for failing to include or properly calculate tax on their auto claim

payments. Most states do provide some guidance as to whether sales tax (possibly including title and registration fees) should be included in the payment of auto total

loss claims. However, many others (DE, DC, ID, LA, MA, MI, MT, NH, NM, NC, NE, TX, and WY) remain silent regarding whether, when, and in what amounts sales tax

must be paid when settling claims on auto total losses.

THIRD-PARTY CLAIMS

“Third-party claims” are auto liability claims made by the owner of a damaged vehicle against a third-party tortfeasor (person other than the insured and insurer) or his

liability insurance carrier for negligently causing damage to the owner’s vehicle. Third-party property damage recovery is governed by applicable state tort damage laws

and varies from state to state. Whether sales tax can be recovered in tort from a third party depends on the tort and damages laws of the state(s) involved. The third-

party liability insurance company will be responsible for damages caused by its insured. The extent of those damages depends on the damages law of the state(s) involved

as well as possible unfair claims settlement practices laws and/or regulations which may include such third-party claims. First-party RCV insurance claim payments cannot

be recovered as damages in third-party subrogation cases because the default rule for measuring direct damages from partial destruction of personal property is either

the reasonable cost of repairs or the difference in the market value immediately before and immediately after the damage to such property at the place where the

damage was occasioned. J & D Towing, LLC v. Am. Alternative Ins. Corp., 478 S.W.3d 649 (Tex. 2016). For both real and personal property losses, the general rule of

recovery in many jurisdictions is that a property owner can recover the cost of replacement, repair, or restoration of property, unless the damage is permanent, and the

restoration cost will exceed the diminution in the fair market value of the property, in which case the damages are limited to the diminution in fair market value. In other

jurisdictions, the damages rule allows recovery of the difference between the FMV of the property before the loss less the FMV of the property immediately after the

loss.

NOTE: On occasion, damaged property does not have a typical “market” in which such items are bought and sold, calculating damages becomes much more complicated

and confusing. Property such as municipal utility poles, signs, school buildings, landmarks, statues, etc., have a “service value” (a/k/a “use value”), but have no traditional

market to aid in determining the damages owed by someone who negligently damages such property. Intrinsic value is the reasonable value of property to the owner in

the condition the property was in when it was damaged, excluding any fanciful or sentimental consideration. Trinkets, etchings, books, pets, family documents,

household furniture, jewelry, silverware, family records, clothing, and personal effects are examples of property that do not have a realistic FMV because they are not

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 3 Last Updated 1/13/22

easily bought or sold on the market. Instead, they have an artistic or intrinsic value. Sentimental value is value over and above any market value or intrinsic value a piece

of personal property might have. Examples of such property include antiques, heirlooms, wedding memorabilia, photographs, handicrafts, and trophies, etc., although

almost anything could have sentimental value. For a chart showing the applicable state laws in all 50 states regarding damage to property without traditional market

value, see HERE. This chart, however, concerns itself primarily with the recovery of sales taxes in first-party and third-party claims.

SALES TAX EXEMPTIONS: It should be noted that most states provide vehicle sales tax exemptions for a variety of vehicles, depending on their intended uses – including

“commercial” vehicles. For example, Texas provides for sales tax exemptions for Church and Religious Societies, Consular Officers and Employees, Driver Training

Vehicles, Farm (Ranch) Exemptions for Specially Modified Motor Vehicles Used on a Farm or Ranch, Non-Exempt Vehicles Used on a Farm or Ranch, Farm Trailers, Farm-

Use Vehicles, Agricultural Tax Exemptions, Trailers Used for Timber Operations, Interstate Motor Vehicles, Licensed Child-Care Facilities, Nonprofit Organizations,

Orthopedically Handicapped Person, Disabled Veterans, or Former Prisoners of War, Public Agency, Lease to a Public Agency, License Plates Contractors, Other

Organizations Exempt by Statute, Federal Organizations, State Organizations, Volunteer Fire Department Vehicles Transported Out of State, Hydrogen-Powered Vehicles,

and Citrus Pest and Disease Management Corporation (Agriculture Code Chapter 80). Recovery of sales tax, whether first-party or third-party, would likely depend on

whether vehicle sales tax is going to be incurred in the first place. If no sales tax will be owed on the repurchase of a replacement vehicle, it is likely that no sales tax will

be owed on either first-party or third-party claims. However, such situations must be looked at on a case-by-case basis taking into consideration the detailed nuances of

the laws of damages and taxation in a particular state.

It should be remembered that the adjustment and/or payment of insurance claims, first-party or third-party, are dependent not only on state law and/or regulations, but

also on policy language. No decision regarding the payment of a claim should be made without consulting your policy terms and conditions as well as legal counsel. This

chart is simply a shorthand rendition of available (or unavailable) law on the subject, and is not a substitute for coverage and or claims legal advice.

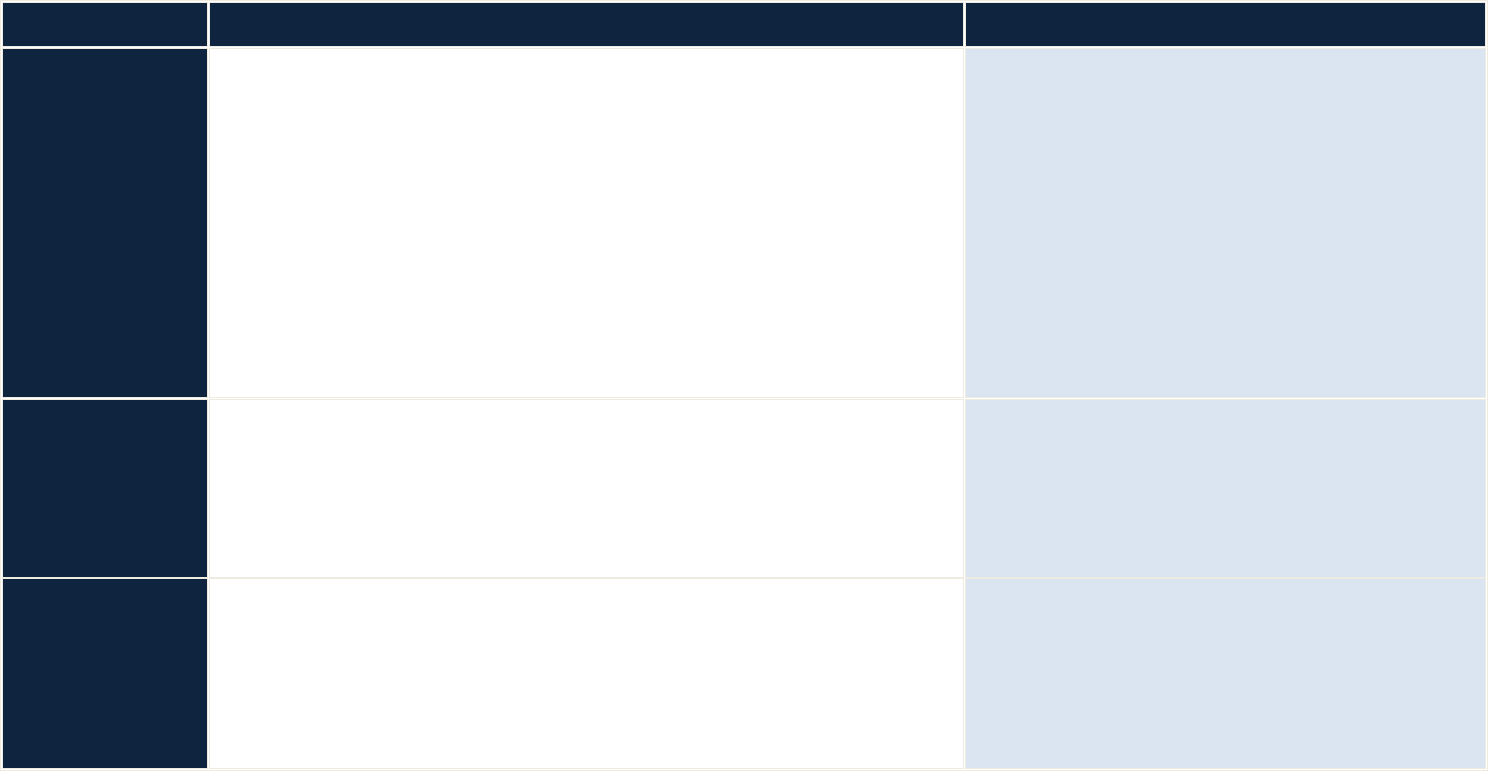

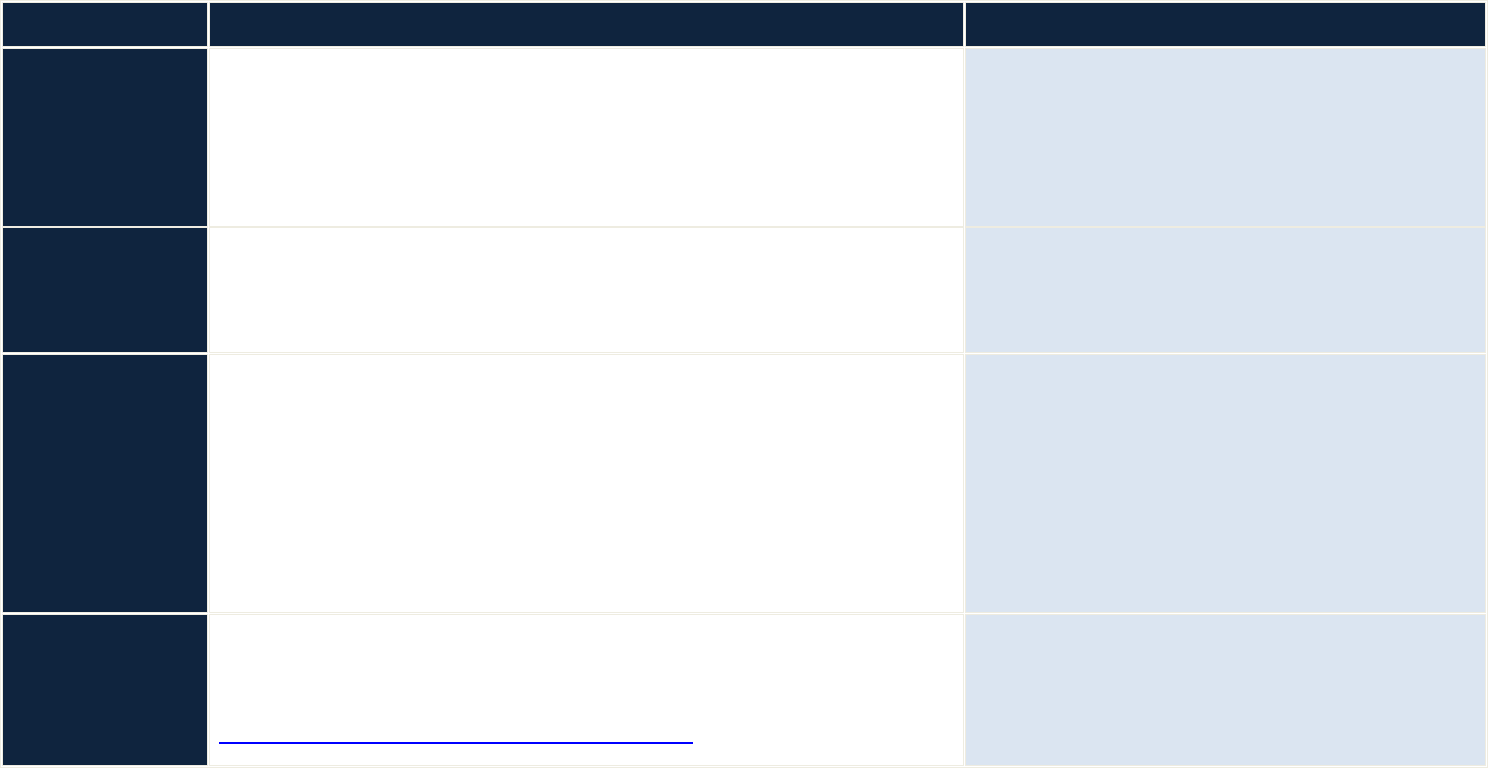

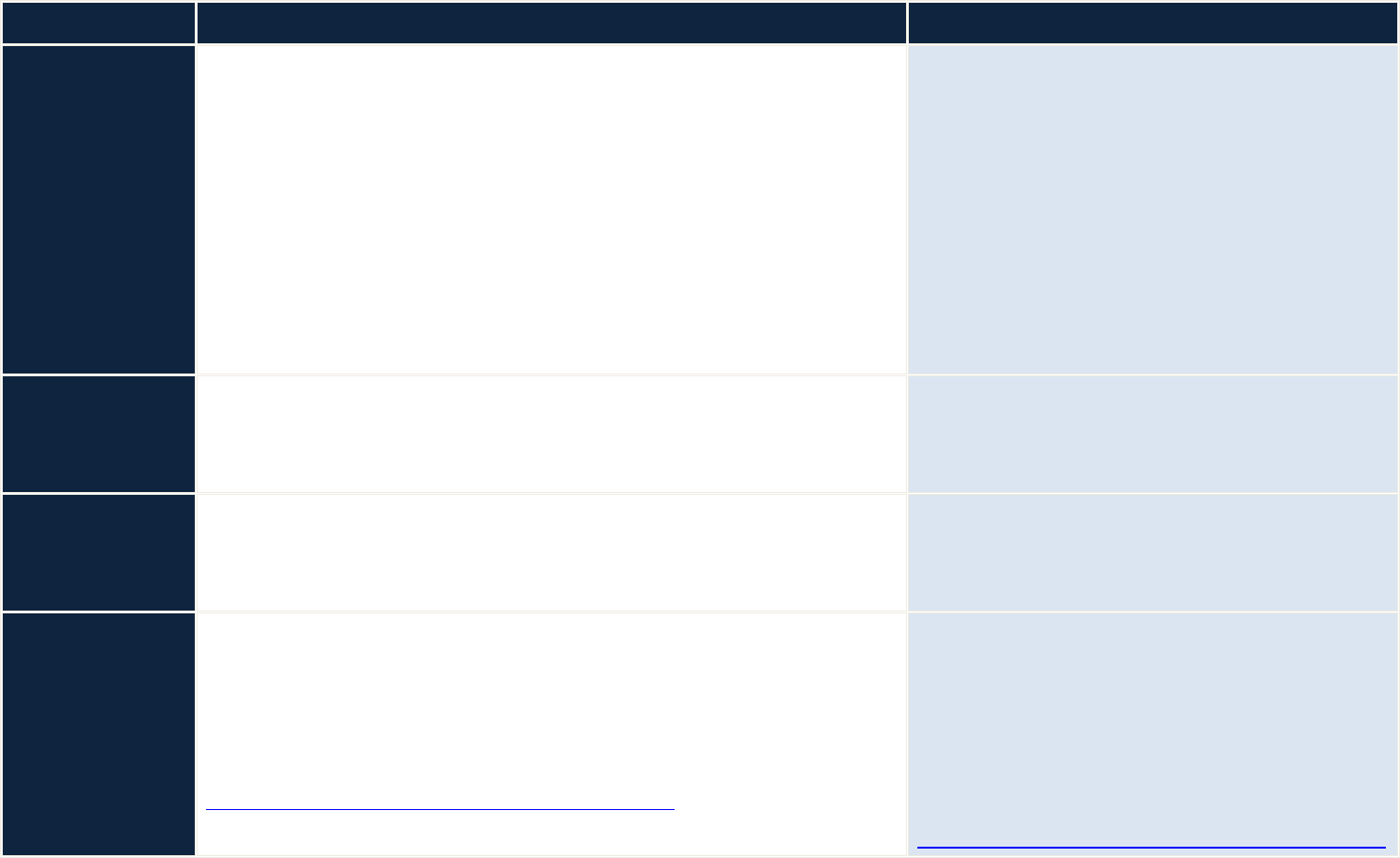

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

ALABAMA

When the insurance policy provides for the adjustment and settlement of first-

party auto total losses based on ACV or replacement with another of like kind and

quality, the insurer must pay all applicable taxes, license fees, and other fees. Ala.

Admin. Code § 482-1-125-.08.

Where policy provides that “If we pay for loss in money, our payment will include

the applicable sales tax”, sales tax is owed. Lary v. Valiant Ins. Co., 864 So.2d 1105

(Ala. Civ. App. 2002), overruled by Ex parte S & M, LLC, 120 So.3d 509 (Ala. 2012).

No applicable statute, case law, or regulation governing

recovery of sales tax.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 4 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

ALASKA

No state sales tax in Alaska. When the insurance policy provides for the adjustment

and settlement of first-party auto total loss based on ACV or replacement with

another of like kind and quality, the insurer must offer a comparable replacement

vehicle with all applicable taxes, license fees, and other fees paid. Alaska. Admin.

Code § 26.080.

If insured wants to retain the salvage following a total loss and seeks to settle on

an ACV basis, the correct calculation for the total loss is based on the actual cost to

purchase a comparable vehicle, including all applicable taxes, license fees,

destination or delivery charges, and other fees incident to transfer of ownership.

This calculation is not contingent on salvage, nor does calculation of ACV change if

the insured seeks to keep the salvage rather than have the salvage turned over to

the insurer for disposition. Bulletin 93-8, 1993 WL 13563685 (AK INS BUL), 2.

No applicable statute, case law, or regulation governing

recovery of sales tax.

ARIZONA

All insurance policies must make prompt, fair, and equitable settlements applicable

to both first and third-party total loss claims. This includes either (1) offering a

replacement auto with all applicable “taxes, license fees, and other fees” paid, or

(2) making cash settlement which includes all applicable taxes, license fees, and

other fees. Ariz. Admin. Code § R20-6-801(H)(1).

Third-party insurers must follow the same rules as first-

party insurers. Any deviation from those rules must be

supported by documentation giving particulars of the

vehicle’s condition, and all deviations must be

“measurable, discernible, itemized, and specified as to

dollar amount.” Ariz. Admin. Code § R20-6-801(H)(1)(C).

ARKANSAS

When the insurance policy provides for the adjustment and settlement of a first-

party auto total loss, the insurer must either (1) offer a replacement auto with all

applicable “taxes, license fees, and other fees” paid, or (2) make a cash settlement

which includes all applicable taxes, license fees, and other fees. If the insurer

deviates from the methods above, they must include an itemized list stating the

amount of the claim attributable to the value of the auto and the amount

attributable to the sales tax. Ark. Admin. Code § 054.00.43-10(A).

Third-party insurers must follow the same rules as first-

party insurers. Any deviation from those rules must be

supported by documentation giving particulars of the

vehicle’s condition, and all deviations must be

“measurable, discernible, and itemized as to dollar

amount.” Ark. Admin. Code § 054.00.43-10(A)(3).

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 5 Last Updated 1/13/22

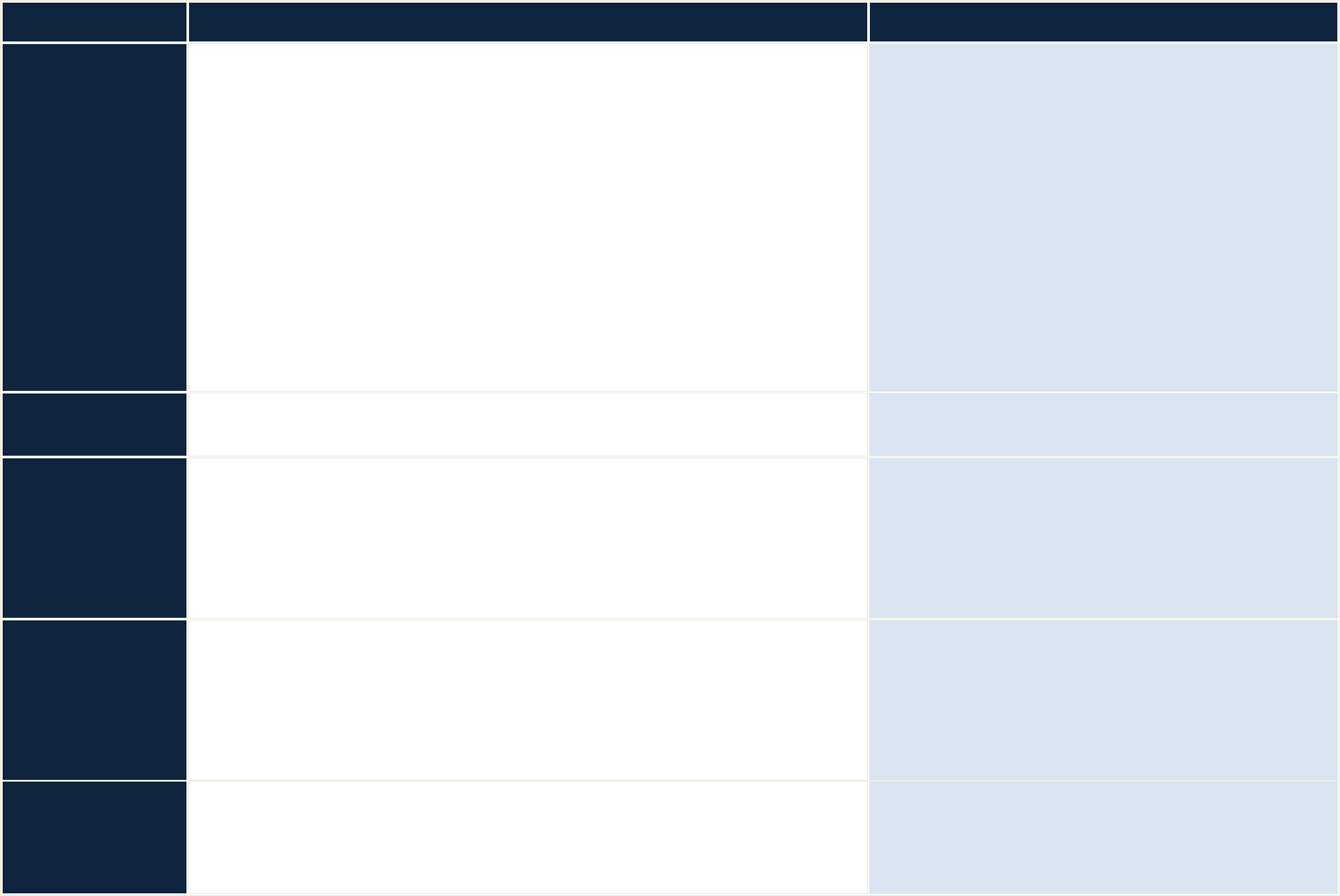

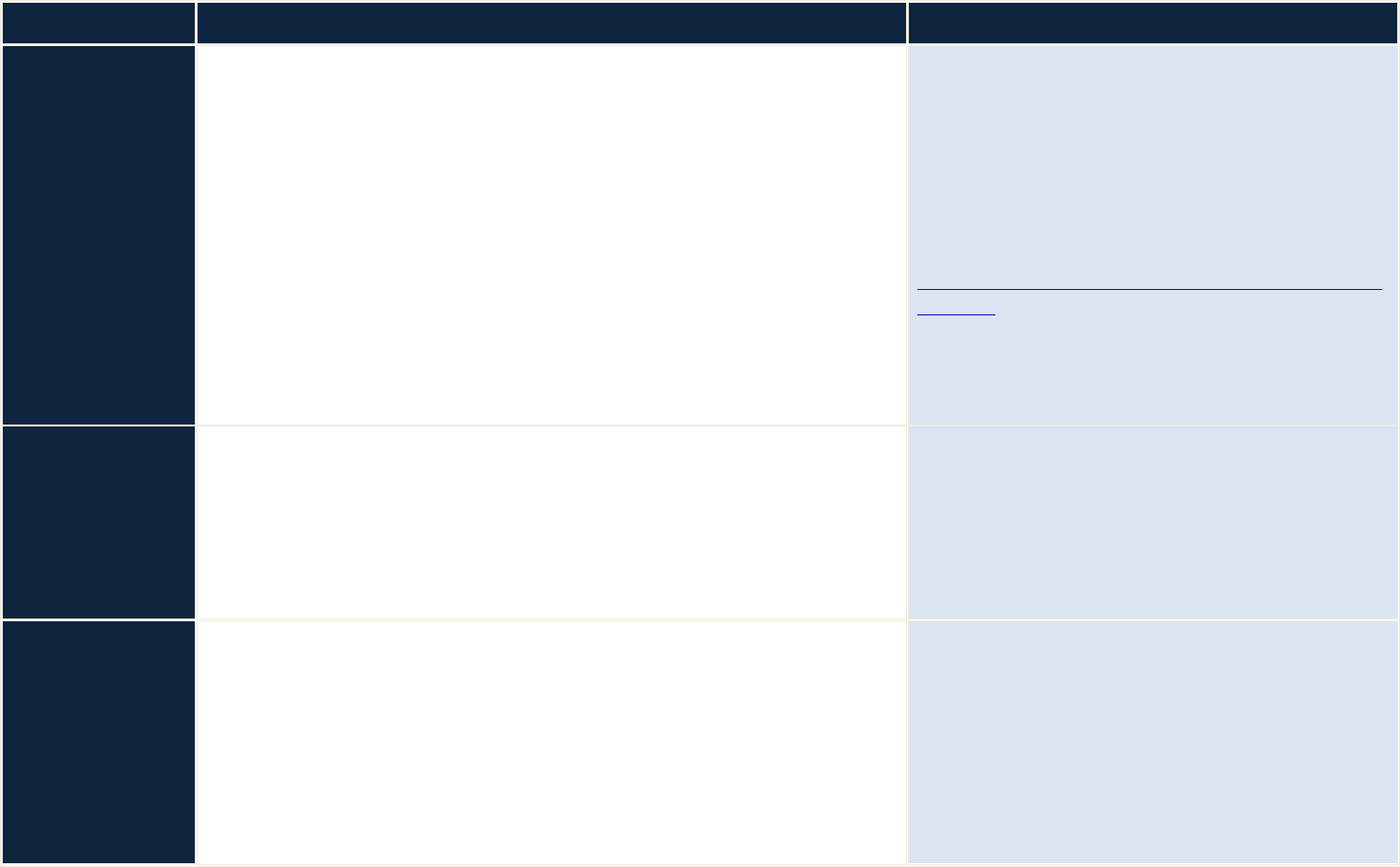

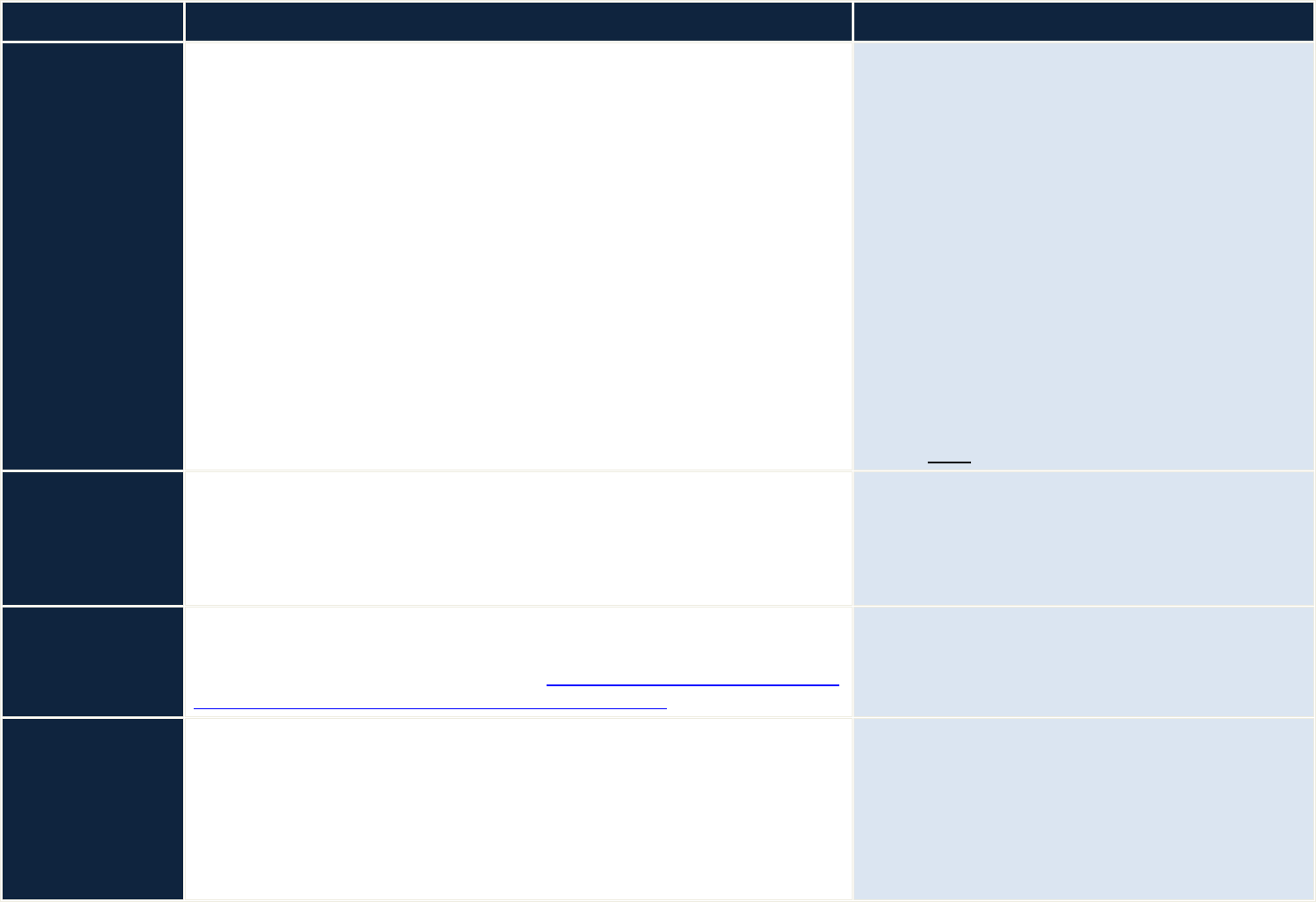

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

CALIFORNIA

Insurer must (1) offer a cash settlement based upon the actual cost of a

“comparable auto” including all applicable taxes and other fees, or (2) offer a

replacement comparable auto including all applicable taxes, license fees, and other

fees. Cal. Code of Regs. Tit. 10 § 2695.8(b).

Pro-rata refund of Vehicle License Fee (VLF) portion of the registration fees (in lieu

of property tax) is required when one (1) vehicle is stolen and not recovered within

60 days after police report, Cal. Rev. and Tax. Code § 10902; (2) total loss, Cal. Veh.

Code § 11515 & Cal. Rev. and Tax. Code § 10902, or (3) vehicle completely stripped

or burned.

When a carrier elects to repair the car to its pre-accident condition, it’s not required

to pay for any loss of value to the vehicle, which can occur after a seriously damaged

vehicle is fully repaired. Carson v. Mercury Ins. Co., 148 Cal. Rptr. 3d 518 (Cal. App.

2012).

Third-party total loss claims are evaluated in the same

way as first-party claims. Cal. Code of Regs. Tit. 10 §

2695.8(b)(6). It provides:

(6) Subsection 2695.8(b) applies to the evaluation of third

party automobile total loss claims, but does not change

existing law with respect to the obligations of an insurer

in settling such claims with a third party.

COLORADO

Insurer shall pay title fees, sales tax, and any other transfer or registration fee

associated with the total loss of a motor vehicle. C.R.S. § 10-4-639.

Third-party total loss claims are evaluated in the same

way as first-party total loss claims. C.R.S. § 10-4-639.

CONNECTICUT

Insurer must pay an amount equal to (A) the settlement amount on such vehicle

plus, (B) whenever the insurer takes title, an amount determined by multiplying the

settlement amount by the current tax rate percentage. C.G.S.A. § 38a-816.

No authority requiring payments of sales tax to third-

party total loss claims. Insurers have no duty of good

faith to third parties since their relationship is adversarial

and not fiduciary in character. Asmus Elc., Inc. v. G.M.K.

Contractors, LLC, WL 758126 (2005); Sherrick v.

Belanger, 43 Conn. L. Rptr. 878 (2007).

DELAWARE

No state sales tax in Delaware. No applicable statute, case law, or regulation

governing recovery of sales tax. 21 Del. C. § 2118 (A)(4) describes only the following

benefits: “Compensation for damage to the insured motor vehicle, including loss

of use of the motor vehicle, not to exceed the actual cash value of the vehicle at

the time of the loss and $10 per day, with the maximum payment of $300, for loss

of use of such vehicle.” 21 Del. C. § 2118 (A) (4). Look at policy language.

No applicable statute, case law, or regulation governing

recovery of sales tax.

DISTRICT OF

COLUMBIA

No applicable statute, case law, or regulation governing recovery of sales tax.

However, an insured can recover damages suffered as a result of being without a

vehicle for a reasonable amount of time necessary to replace or repair the damaged

vehicle. Gamble v. Smith, 386 A.2d 692, 694 (1978). Look at policy language.

No applicable statute, case law, or regulation governing

recovery of sales tax.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 6 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

FLORIDA

When the insurance policy provides for the adjustment and settlement of first-

party auto total losses based on ACV or replacement with another of like kind and

quality, the insurer must pay sales tax. Any deviation from this method must be

supported by documentation. The insurer must include an itemized list stating the

amount of the claim attributable to the value of the auto and the amount

attributable to the sales tax. F.S.A. § 626.9743.

Third-party insurers must follow the same rules as first-

party insurers. Any deviation from those rules must be

supported by documentation giving particulars of the

auto condition, and all deviations must be “measurable,

discernible, itemized and specified as to dollar amount.”

F.S.A. § 626.9743(5)(C).

GEORGIA

Insurer must (1) offer a cash equivalent settlement based upon the ACV of a

“comparable auto” including all applicable taxes and other fees, or (2) offer a

replacement auto including all applicable taxes, license fees and other fees. Ga.

Comp. R. & Regs. § 120-2-52-.06.

No applicable statute, case law, or regulation governing

recovery of sales tax.

HAWAII

Insurer must (1) offer a cash settlement based upon the ACV of a “comparable

auto”, if within 30 days the insured purchases a new car, the insurer must

reimburse for excise tax and ownership fees, or (2) offer a replacement comparable

auto including all excise taxes and ownership fees. Haw. Rev. Stat. § 431:10C-312.

No applicable statute, case law, or regulation governing

recovery of sales tax. However, courts have applied

various measures of damages to personal property. All

these measures are merely guides to common sense

aimed to ultimately fully compensate the injured party.

The assessment of property damage must rest on its own

facts and circumstances. Richards v. Kailua Auto Mach.

Serv., 10 Haw. App. 613, 623, 880 P.2d 1233, 1238

(1994).

IDAHO

No applicable statute, case law, or regulation governing recovery of sales tax.

However, Idaho Department of Insurance’s website states that an insured can

recover sales tax, title fees, and release of liability fees.

http://www.doi.idaho.gov/consumer/claim_faq.aspx

No applicable statute, case law, or regulation governing

recovery of sales tax. A claim against an insurer for

breach of duty of good faith is only available to first-party

insured parties. Idaho State Ins. Fund v. Van Tine, 132

Idaho 902, 908, 980 P.2d 566, 572 (1999).

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 7 Last Updated 1/13/22

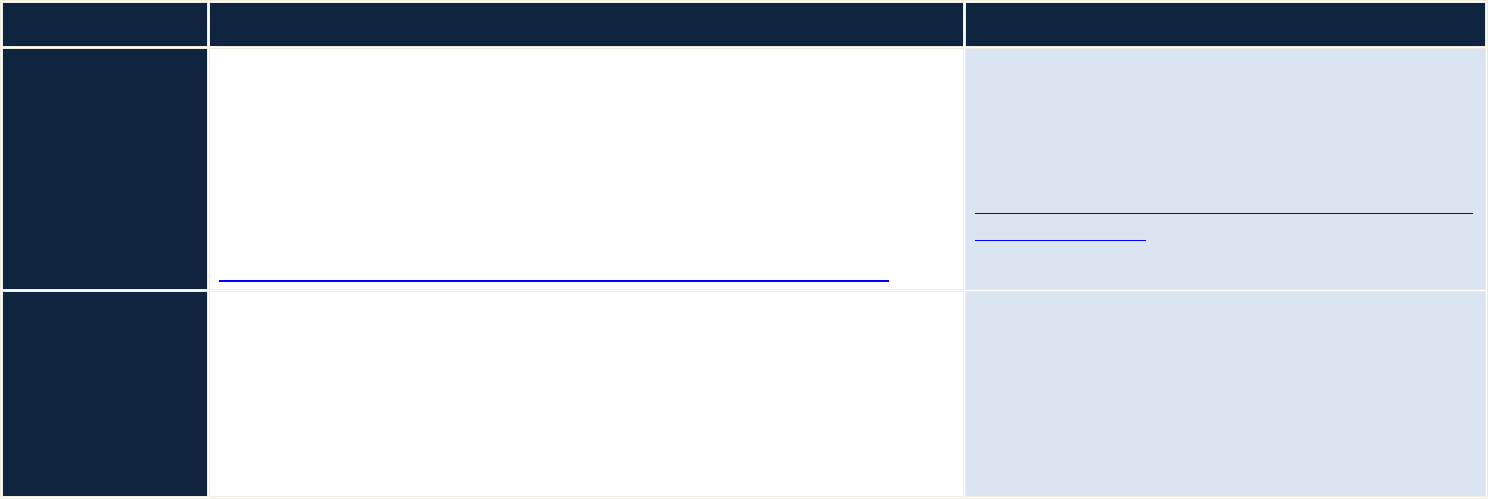

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

ILLINOIS

Insurer must (1) offer a cash settlement based upon the ACV of a “comparable

auto”, If within 30 days the insured buys or leases a new vehicle, the carrier must

pay the applicable sales tax, transfer, and title fees in an amount equivalent to the

value of the total loss vehicle, or (2) offer a replacement comparable auto including

all applicable taxes, license fees, and other fees, if the insured purchases a vehicle

with a market value less than the amount previously settled upon, the company

must pay only the amount of sales tax actually incurred and include transfer and

title fees. Ill. Admin. Code tit. 50, § 919.80(C).

Exhibit A to § 919 states: “If within 30 days of a cash settlement, you can prove that

you have purchased another vehicle, the company must pay the applicable sales

tax, transfer and title fees in an amount equivalent to the value of the total loss

vehicle. If you purchase a vehicle with a market value less than the amount

previously settled upon, the company must pay you only the amount of sales tax

that you actually incurred and include transfer and title fees.”

No applicable statute, case law, or regulation governing

recovery of sales tax. In a third-party claim, you do not

have a direct contract with the party you are seeking to

recover from and their primary obligation is to their own

policyholder.

http://insurance.illinois.gov/autoinsurance/auto_own_

claim.pdf; Cramer v. Ins. Exch. Agency, 174 Ill.2d 513,

531, 675 N.E.2d 897, 906 (1996).

INDIANA

Insurer must pay sales tax in addition to the fair market value of the totaled vehicle.

This is necessary for the insured to be “made whole” for the loss. Sales tax must be

paid at the time of compensating the insured for the loss of the vehicle. Indiana

Insurance Bulletin 82, 2/25/94. In 2014, Indiana Dept. of Ins. General Counsel Tina

Korty explained that, “The Department views payment of sales tax to be a

necessary component of a fair and equitable settlement.” 1/9/15 e-mail to Gary

Wickert.

The Indiana Dept. of Ins. General Counsel says the

position of the Department is that of Indiana Insurance

Bulletin 82. Indiana law requires insurers to effectuate

prompt, fair, and equitable settlement of claims. I.C. §

27-4-1-4.5. The Department views payment of sales tax

to be a necessary component of a fair and equitable

settlement. No case law to support, however.

IOWA

Insurer may (1) offer a replacement auto that is at least comparable including all

applicable taxes, license fees, or other fees, or (2) offer a cash settlement based on

the ACV of a comparable vehicle including all applicable taxes, license fees, or other

fees. Iowa A.D.C. § 191-15.43(507B).

No applicable statute, case law, or regulation governing

recovery of sales tax. The Supreme Court has simply said

that “When the motor vehicle is totally destroyed or the

reasonable cost of repair exceeds the difference in

reasonable market value before and after the injury, the

measure of damages is the lost market value plus the

reasonable value of the use of the vehicle for the time

reasonably required to obtain a replacement.” Long v.

McAllister, 319 N.W.2d 256 (Iowa 1982).

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 8 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

KANSAS

Insurer may (1) offer owner a comparable replacement vehicle, “with all applicable

taxes, license fees, and other fees incident to transfer of evidence of ownership ...”

or (2) pay owner a cash settlement equal to the actual cost required to purchase a

comparable vehicle “including all applicable taxes, license fees and other fees

incident to transfer of evidence of ownership ...” Sales tax is calculated by

multiplying the ACV of the comparable vehicle by state and local income tax. Kan.

Admin. Regs. § 40-1-34.

http://www.ksinsurance.org/department/LegalIssues/bulletins/2013-1.pdf

Kansas Insurance Department Bulletin 2013-01 states

that insurers have an obligation to pay sales tax and fees

for all total loss claims.

http://www.ksinsurance.org/department/LegalIssues/b

ulletins/2013-1.pdf

KENTUCKY

If the policy provides for the settlement of first-party auto total loss, the insurer

may elect to either (1) offer a replacement auto that is at least comparable

including all applicable taxes, license fees, or other fees, or (2) offer a cash

settlement based on the actual cost of a comparable vehicle including all applicable

taxes, license fees, or other fees. 806 Ky. Admin. Regs. § 12:095.

806 Ky. Admin. Regs. § 12:095 defines “claimant” as a

first-party claimant, a third-party claimant, or both.

Bulletin 81-DM-007, 1981 states “it is necessary for sales

tax to be included in establishing the value of damage

when such tax is obviously an obligation of the claimant

upon replacement of total losses.” However, no other

applicable statute or case law.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 9 Last Updated 1/13/22

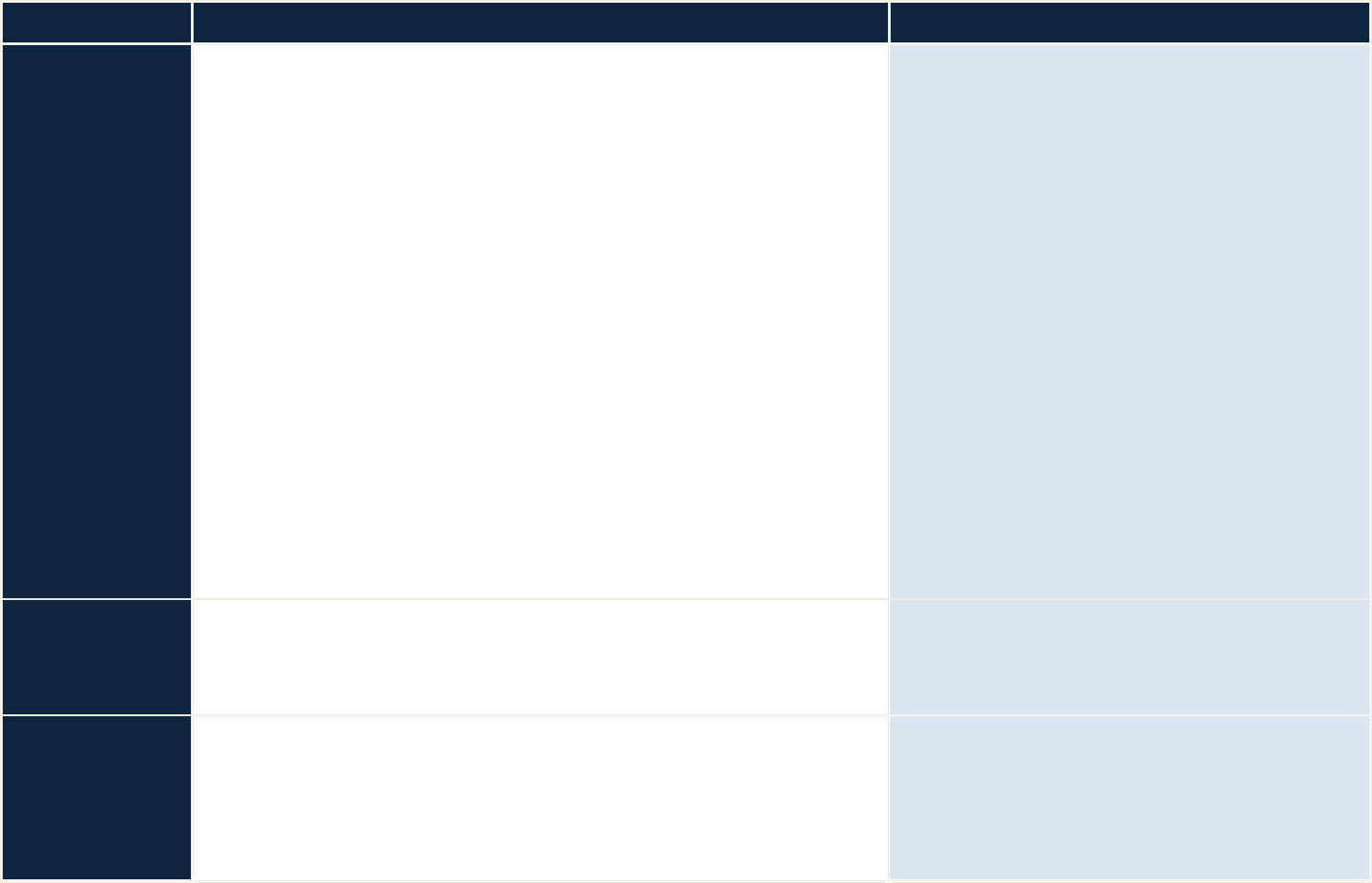

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

LOUISIANA

Insured truck owner was not entitled to recover sales tax on vehicle under terms of

the policy as result of his truck being stolen and/or damaged, where policy provided

for “actual cash value” of the damaged property; fact that insured paid sales tax on

the truck did not increase its value. Clark v. Clarendon Ins. Co., 841 So.2d 1039 (La.

App. 2003).

State Farm’s insured suffered total loss to vehicle. State

Farm paid insured sales tax and sought to subrogate the

damages from the tortfeasor. The third party refused to

reimburse State Farm for the sales tax. The Supreme

Court denied State Farm’s claim, holding that, despite §

2315, below, State Farm was subrogated only to those

rights its insured had, and only to the extent of first-party

coverage it provided. Section 1830 says the subrogee

cannot recover more than the extent of its performance

under the policy. The State Farm policy did not obligate

it to pay sales tax, so it could not recover sales tax from

the tortfeasor. State Farm Mut. Auto. Ins. Co. v.

Berthelot, 732 So.2d 1230 (La. 1999).

Vehicle owner can recover sales tax. If the first-party

policy requires payment of sales tax, such tax may be

recovered in third-party action by subrogated insurer.

Section 2315 (“Liability For Acts Causing Damages”) is

known as the “fountainhead” of tort law in Louisiana,

and as of a 2001 amendment, now provides in part,

“Damages shall include any sales taxes paid by the owner

on the repair or replacement of the property damaged.”

MAINE

“All contracts of motor vehicle casualty insurance ... shall provide coverage for the

value of the sales tax credit that would have been available upon trade thereof at

the highest book value at the time of loss or destruction of the insured vehicle.” 24-

A M.R.S.A. § 2907.

No applicable statute, case law, or regulation governing

recovery of sales tax.

MARYLAND

Insurer may (1) offer a replacement auto that is substantially similar (does not

address if sales tax and fees are included). Md. Code Regs. § 31.15.12.07, or (2)

offer a cash settlement based on the actual cost of a substantially similar vehicle

including all applicable taxes and transfer fees. Md. Code Regs. § 31.15.12.04.

Insurers have been cited for refusing to reimburse sales tax on a total loss claim

under Md. Code Ann., Ins. § 27-303 and § 27-304.

Insurer may only offer a cash settlement based on the

actual cost of a substantially similar vehicle including all

applicable taxes and transfer fees. Md. Code Regs. §§

31.15.12.03 and 31.15.12.04. MD Ins. Order 11-25-80.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 10 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

MASSACHUSETTS

Insurer is only required to pay for the ACV of a vehicle as of the day of the loss, not

the cost to replace it. 211 Mass. Code Regs. § 133.05.

http://www.mass.gov/ocabr/insurance/vehicle/auto-insurance/faq.html#q2.

No applicable statute, case law, or regulation governing

recovery of sales tax.

MICHIGAN

No applicable statute, case law, or regulation governing recovery of sales tax.

No third-party collision litigation allowed due to no fault.

MINNESOTA

If the policy provides for the settlement of first-party auto total loss, the insurer

may (1) offer a comparable and available replacement vehicle including all

applicable taxes, license fees, or other fees, or (2) offer a cash settlement based on

the actual cost of a comparable vehicle including all applicable taxes, license fees,

or other fees. M.S.A. § 72A.201.

No applicable statute, case law, or regulation governing

recovery of sales tax.

MISSISSIPPI

The insurer must pay sales taxes, title fees, or license fees unless the policy

unambiguously excludes this recovery for total loss claims. MS Bulletin 2007-4.

Jay Evey (Mississippi Department of Insurance) states

that MS Bulletin 2007-4 does extend to third parties

based on public policy of making the injured party whole.

No applicable statute, case law, or regulation governing

recovery of sales tax.

MISSOURI

Unless stated in the policy language, an insurer is not required to reimburse for

sales tax. The insured must file a request with the state to have their sales tax

refunded.

https://insurance.mo.gov/Contribute%20Documents/autoclaimbrochure_002.pdf

No applicable statute, case law, or regulation governing

recovery of sales tax.

MONTANA

No state sales tax. No applicable statute, case law, or regulation governing recovery

of sales tax. Mont. Code Ann. § 27-1-306 states that the insured can only recover

the cash value of the vehicle immediately prior to the accident.

No applicable statute, case law, or regulation governing

recovery of sales tax.

NEBRASKA

Insurer must pay sales tax to put the injured party back into the position they were

in before the injury. NE Bulletin CB-49.

Third-party total loss claims are evaluated in the same

way as first-party total loss claims. NE Bulletin CB-49.

NEVADA

Insurer must (1) offer a cash settlement based upon the actual cost of a

“comparable auto” including all applicable taxes and other fees, or (2) offer a

replacement comparable auto including all applicable taxes, license fees, and other

fees. Nev. Admin. Code § 686A.680.

No applicable statute, case law, or regulation governing

recovery of sales tax.

NEW HAMPSHIRE

No state sales tax. No applicable statute, case law, or regulation governing recovery

of sales tax. N.H. A.D.C. Ins. § 1002.15 describes how to determine reimbursement

for total loss claims but does not speak on the topic of sales tax.

No applicable statute, case law, or regulation governing

recovery of sales tax.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 11 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

NEW JERSEY

Insurer must offer a cash settlement based upon (1) average retail of substantially

similar vehicle, (2) a quotation for a substantially similar vehicle from a dealer

located within a reasonable distance, or (3) fair market value, plus applicable sales

tax. N.J. Admin. Code § 11:3-10.4.

The requirements for auto physical damage first-party

claims found in N.J.A.C. §§ 11:3–10.1 through 10.4 shall

also be construed to apply to automobile property

damage third-party claims from the time that liability

becomes reasonably clear. N.J. Admin. Code § 11:2-

17.10.

NEW MEXICO

No applicable statute, case law, or regulation governing recovery of sales tax.

However, New Mexico Public Regulation Commission states that after a cash

settlement, the insurer must reimburse the state’s excise tax, any title fees, and

any registration charges. http://www.nmprc.state.nm.us/consumer-

relations/docs/settlement-total-loss.pdf.

No applicable statute, case law, or regulation governing

recovery of sales tax.

NEW YORK

Insurer is required to reimburse the insured with the ACV. This means either

repairing the damaged item or replacing it with an item substantially identical

including sales tax (sales tax added to the value of the auto prior to the accident

before salvage value is taken). N.Y. Comp. Codes R. & Regs. tit. 11, § 216.6. An

insurer is not required to include transfer or title fees.

http://www.dfs.ny.gov/insurance/ogco2008/rg081013.html.

Third-party insurers must follow the same rules as first-

party insurers. N.Y. Comp. Codes R. & Regs. tit. 11, §

216.0 (Standards for Prompt, Fair and Equitable

Settlement of Motor Vehicle Physical Damage Claims)

states that these claim practice rules apply to both first

and third-party claims.

On 5/1/02, the N.Y. Office of General Counsel issued a

formal opinion which says that in adjusting a third-party

claim for a total loss of a vehicle, the third-party insurer

must comply with the requirements in N.Y. Comp. Codes

R. & Regs. tit. 11, § 216.7(c)(1), (3), (4) (1999), which

specifies how the insurer’s minimum offer, subject to

applicable deductions, should be computed.

NORTH CAROLINA

No applicable statute, case law, or regulation governing recovery of sales tax.

No applicable statute, case law, or regulation governing

recovery of sales tax.

NORTH DAKOTA

No applicable statute, case law, or regulation governing recovery of sales tax. The

payment on a total loss would be the ACV less the deductible. ACV is defined as an

amount equivalent to the replacement cost of lost or damaged property at the time

of the loss, less depreciation. http://www.nd.gov/ndins/consumers/auto/

http://www.nd.gov/ndins/consumers/auto/glossary/.

No applicable statute, case law, or regulation governing

recovery of sales tax.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 12 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

OHIO

Insurer may (1) offer a replacement of like kind and quality including all applicable

taxes, license fees, or other fees if the insured provides documentation of the

purchase of a replacement auto within 30 days, or (2) offer a cash settlement based

on the ACV of a comparable vehicle including all applicable taxes, license fees, or

other fees. Insurers must only reimburse sales tax for claim amount, not the

replacement vehicle cost. Ohio Admin. Code 3901-1-54.

Ohio Admin. Code 3901-1-54 (C)(3) defines “Claimant”

as a first-party claimant or a third-party claimant. Third-

party insurers must follow the same rules as first-party

insurers.

OKLAHOMA

If the policy provides for the settlement of first-party auto total loss, insurer may

(1) offer a replacement of like kind and quality including all applicable taxes, license

fees, or other fees, or (2) offer a cash settlement based on the ACV of a comparable

vehicle including all applicable taxes, license fees, or other fees. Okla. Stat. Ann. tit.

36, § 1250.8.

No applicable statute, case law, or regulation governing

recovery of sales tax.

OREGON

No state sales tax in Oregon. If the policy provides for the settlement of first-party

auto total loss, insurer may (1) offer a replacement comparable vehicle including

all applicable taxes, license fees, or other fees, or (2) offer a cash settlement based

on the ACV of a comparable vehicle including all applicable taxes, license fees, or

other fees. Or. Admin. R. § 836-080-0240.

Insurer is only required to offer a cash settlement to

third-parties including all applicable taxes, license fees,

or other fees. Or. Admin. R. § 836-080-0240 (14).

PENNSYLVANIA

A total loss is settled based upon the pre-loss fair market value of the damaged

vehicle plus the state sales tax on the cost of a replacement vehicle. 27

Pennsylvania Bulletin 306131; Pa. Code § 62.3 (E)(4).

31 Pa. Code § 146.2 defines “claimant” as a first-party

claimant, a third-party claimant, or both. However, no

other applicable statute, or case law governing recovery

of sales tax.

RHODE ISLAND

When the policy provides for the adjustment and settlement of first-party total

losses, the Insurer may (1) offer a replacement of like kind and quality including all

applicable taxes, license fees, or other fees, or (2) offer a cash settlement based on

the ACV of a comparable vehicle including all applicable taxes, license fees, or other

fees. R.I. Code R. § 11-5-73:8.

R.I. Code R. § 11-5-73:3 defines “claimant” as a first-

party claimant, a third-party claimant, or both. “In order

to fully compensate for the loss to the consumer, the

insurer must include applicable sales tax in its calculation

of settlement value in any total loss claim.”

http://www.dbr.ri.gov/documents/rules/insurance/Insu

ranceRegulation73.pdf.

http://www.dbr.state.ri.us/documents/rules/proposed/

2013-propd73.pdf.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 13 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

SOUTH CAROLINA

Insurers are not required to reimburse for the sales tax unless the policy specifically

states otherwise. Schulmeyer v. State Farm Fire & Cas. Co., 353 S.C. 491, 498, 579

S.E.2d 132, 135 (2003). No applicable statute, case law, or regulation governing

recovery of sales tax.

As of July 1, 2017, owners of new vehicle owe an Infrastructure Maintenance Fee

(IMF) instead of sales tax. Under the new legislation known as the “Roads Bill”, if a

“vehicle or other item that is required to be registered” is purchased or leased and

will be titled and/or registered in North Carolina, the owner will owe an

Infrastructure Maintenance Fee (IMF) instead of sales tax. For dealers, the IMF will

be in the amount of 5% of the gross proceeds of sale price (not to exceed $500).

For private sales of vehicles, the cap is $250. Those who move to South Carolina

with a vehicle that needs to be registered in the state will automatically owe a $250

IMF per vehicle. Those who purchase a vehicle or other item in the state, that will

be registered in a different state, will not need to pay an Infrastructure

Maintenance Fee, but a sales tax instead. Salvage title applications are exempt from

the IMF. S.C. Stat. Ann. § 56-3-627 (A) through (D).

No applicable statute, case law, or regulation governing

recovery of sales tax.

SOUTH DAKOTA

“First-party claims are controlled by the relationship provided by the insurance

contract, so the results depend on the policy language.” E-mail from Frank Marnell

– South Dakota Department of Labor and Regulations. However, no applicable

statute, case law, or regulation governing recovery of sales tax.

“Third-party claims are controlled by tort law and sales

tax is generally payable on third-party total loss claims”.

Email from Frank Marnell – South Dakota Department of

Labor and Regulations. However, no applicable statute,

case law, or regulation governing recovery of sales tax

TENNESSEE

Sales tax is payable on the value of the damaged auto at the time the loss is owed

on all losses. TN Bulletin 9-1-89 (#3).

Third-party insurers must follow the same rules as first-

party insurers. TN Bulletin 9-1-89 (#3).

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 14 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

TEXAS

Motor vehicle sale and use tax is not due when insurer takes title to vehicle because

of a total loss. However, motor vehicle sale and use tax is due when the insurer

purchases a replacement vehicle for the insured on a total loss claim. 34 Tex.

Admin. Code § 3.62.

Where a policy provides that in the event of a total loss, the carrier’s liability would

be limited to the “actual cash value of the stolen or damaged property at the time

of the loss, reduced by the applicable deductible ... and by its salvage value if [the

policyholder] or the owner retain[ed] the salvage,” the term “actual cash value”

does not include taxes and fees remitted to the state. Taxes and fees paid by the

buyer to the state are irrelevant to the question of fair market value because those

amounts are not part of the price paid to the seller. Singleton v. Elephant Ins. Co.,

953 F.3d 334 (5

th

Cir. 2020).

No applicable statute, case law, or regulation directly

governing recovery of sales tax. However, in Adams v.

ABC Ins. Co., 264 S.W.3d 424 (Tex. App.–Dallas 2008), the

court held that the total loss settlement (which included

tax and fees) was some evidence of the pre-accident fair

market value of the car. Thus, a subrogated carrier has

essentially two arguments. Either the taxes and fees

should be considered actual damages (separate and

apart from FMV of the vehicle) or they should be

considered some evidence as to what the true fair

market value is of the vehicle. There is no law indicating

that they cannot be recovered.

UTAH

Insurer may (1) offer a replacement of like kind and quality including all applicable

taxes, license fees, or other fees, or (2) offer a cash settlement based on the actual

cost of a comparable vehicle including all applicable taxes, license fees, or other

fees. Utah Admin. Code r. § R590-190.

Third-party insurers must follow the same rules as first-

party insurers. Utah Admin. Code r. R590-190

VERMONT

Insurer may (1) offer a comparable motor vehicle including all applicable taxes,

license fees, or other fees, or (2) offer a cash settlement based on the ACV of a

comparable vehicle including all applicable taxes, license fees, or other fees. 4-3 Vt.

Code R. § 7:8.

Third-party insurers must follow the same rules as first-

party insurers. 4-3 Vt. Code R. § 7:9; VT Bulletin 58, 1982.

VIRGINIA

Insurer may (1) offer a replacement vehicle including all applicable taxes, license

fees, or other fees, or (2) offer a cash settlement based on the actual cost of a

comparable vehicle including all applicable taxes, license fees, or other fees.

Insurance Order No. 11607. Insurers have been cited for not promptly reimbursing

sales tax, license fees, and title fees under Va. Code Ann. § 38.2-510.

https://www.scc.virginia.gov/boi/adminords/11607.pdf.

“Insurers are only required to reimburse for sales tax,

title fees, and transfer fees in third-party claims if the

policy so requires.” E-mail from Virginia Bureau of

Insurance. However, no other applicable statute, case

law, or regulation governing recovery of sales tax besides

Insurance Order No. 11607. Insurers have been cited for

not reimbursing sales tax to a third-party total loss claim

under Va. Code Ann. § 38.2-510.

https://www.scc.virginia.gov/boi/adminords/11607.pdf

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 15 Last Updated 1/13/22

STATE

FIRST-PARTY CLAIMS

THIRD-PARTY CLAIMS

WASHINGTON

Insurer may (1) offer a comparable vehicle, including all applicable taxes, license

fees, or other fees, or (2) offer cash settlement including all applicable taxes, license

fees, or other fees. Wash. Admin. Code § 284-30-391. License fees, weight-based

fees, and other regional fees (urban areas of King, Pierce, or Snohomish counties,

an insured may be required to pay Regional Transit Authority (RTA) tax to pay for

their local transit-related projects) are calculated on a pro-rata basis so that the

insured is compensated for the “unused” portion of the annual taxes and fees. After

the ACV, sales tax and applicable pro-rated taxes and fees are added together, the

insurer deducts the salvage value from the total amount.

First-party coverage under clear ACV provision does not include sales tax because

replacement cost considerations apply only when the property is replaced. Holden

v. Farmers Ins. Co. of Wash., 175 P.3d 601 (Wash. App. 2008). However, if ACV

provision is ambiguous, policy must be read to include sales tax in calculating the

FMV of damaged property, regardless of whether insured replaced the damaged

property. Holden v. Farmers Ins. Co. of Wash., 239 P.3d 344 (Wash. 2010).

As part of settlement amount, include all applicable

government taxes and fees that would have been

incurred by the claimant if the claimant had purchased

the loss vehicle immediately prior to the loss. These

taxes and fees must be included in the settlement

amount whether the claimant retains or subsequently

transfers ownership of the loss vehicle. Wash. Admin.

Code 284-30-391(4)(e).

Sales tax must be dealt with by insurers “in good faith.”

Wash. Office of Ins. Comm., Bulletin No. 89-3 (Apr. 5,

1989). The bulletin notes that in ACV claims, “the cost of

repairing and restoring a building or other object to the

condition it was in before the loss is not only material,

but is the most persuasive evidence of the amount of

loss for which the insurer is liable. Obviously, such costs

will include sales tax.” WA Bulletin 89-3, 1989; see

Holden, supra.

WEST VIRGINIA

Insurer may (1) offer a substantially similar vehicle to claimant which does not

include the reimbursement of sales tax, or (2) offer cash settlement to claimant

based on the minimum cash value of the vehicle including an extra 5% of the cash

value as reimbursement for any excise tax imposed. W. Va. Code Ann. § 33-6-33;

W. Va. Code R. § 114-14-7.

Claimant is defined as a first-party, a third-party, or both.

W. Va. Code R. § 114-14-2. Third-party insurers must

follow the same rules as first-party insurers.

WISCONSIN

No applicable statute, case law, or regulation governing recovery of sales tax.

Insurers have been cited for not reimbursing sales tax in a total loss claim under

Wis. ADC § Ins. 6.11. http://oci.wi.gov/pub_list/pi-057.pdf;

http://oci.wi.gov/consumer/autohome-faqauto.htm#claims.

No applicable statute, case law, or regulation governing

recovery of sales tax.

WYOMING

No applicable statute, case law, or regulation governing recovery of sales tax.

No applicable statute, case law, or regulation governing

recovery of sales tax. It is the WY Dept. of Insurance’s

position that sales tax is included and is based on the

appraised value of the car prior to the accident/loss, but

there is no specific case law, statute, rule, or formal

opinion or statement that expressly supports that

position.

WORK PRODUCT OF MATTHIESEN, WICKERT & LEHRER, S.C. Page 16 Last Updated 1/13/22

These materials and other materials promulgated by Matthiesen, Wickert & Lehrer, S.C. may become outdated or superseded as time goes by. If you should have questions regarding

the current applicability of any topics contained in this publication or any publications distributed by Matthiesen, Wickert & Lehrer, S.C., please contact Gary Wickert at

gwickert@mwl-law.com. This publication is intended for the clients and friends of Matthiesen, Wickert & Lehrer, S.C. This information should not be construed as legal advice

concerning any factual situation and representation of insurance companies and\or individuals by Matthiesen, Wickert & Lehrer, S.C. on specific facts disclosed within the

attorney\client relationship. These materials should not be used in lieu thereof in anyway.