Finance and Economics Discussion Series

Divisions of Research & Statistics and Monetary Affairs

Federal Reserve Board, Washington, D.C.

Redistribution and the Monetary–Fiscal Policy Mix

Saroj Bhattarai, Jae Won Lee, Choongryul Yang

2021-013

Please cite this paper as:

Bhattarai, Saroj, Jae Won Lee, and Choongryul Yang (2021). “Redistribu-

tion and the Monetary–Fiscal Policy Mix,” Finance and Economics Discussion Se-

ries 2021-013. Washington: Board of Governors of the Federal Reserve System,

https://doi.org/10.17016/FEDS.2021.013.

NOTE: Staff working papers in the Finance and Economics Discussion Series (FEDS) are preliminary

materials circulated to stimulate discussion and critical comment. The analysis and conclusions set forth

are those of the authors and do not indicate concurrence by other members of the research staff or the

Board of Governors. References in publications to the Finance and Economics Discussion Series (other than

acknowledgement) should be cleared with the author(s) to protect the tentative character of these papers.

Redistribution and the Monetary–Fiscal Policy Mix

∗

Saroj Bhattarai

†

Univ. of Texas-Austin

and CAMA

Jae Won Lee

‡

Univ. of Virginia

Choongryul Yang

§

Federal Reserve Board

Abstract

We show that the effectiveness of redistribution policy in stimulating the economy

and improving welfare is directly tied to how much inflation it generates, which in

turn hinges on monetary-fiscal adjustments that ultimately finance the transfers. We

compare two distinct types of monetary-fiscal adjustments: In the monetary regime, the

government eventually raises taxes to finance transfers, while in the fiscal regime, in-

flation rises, effectively imposing inflation taxes on public debt holders. We show ana-

lytically in a simple model how the fiscal regime generates larger and more persistent

inflation than the monetary regime. In a quantitative application, we use a two-sector,

two-agent New Keynesian model, situate the model economy in a COVID-19 reces-

sion, and quantify the effects of the transfer components of the Coronavirus Aid, Re-

lief, and Economic Security (CARES) Act. We find that the transfer multipliers are sig-

nificantly larger under the fiscal regime—which results in a milder contraction—than

under the monetary regime, primarily because inflationary pressures of this regime

counteract the deflationary forces during the recession. Moreover, redistribution pro-

duces a Pareto improvement under the fiscal regime.

JEL classification: E53; E62; E63

Keywords: Household heterogeneity, Redistribution, Monetary-fiscal policy mix, Trans-

fer multiplier, Welfare evaluation, COVID-19, CARES Act

∗

We thank Woong Yong Park for helpful comments. The views expressed here are those of the authors

and do not necessarily reflect those of the Federal Reserve Board or the Federal Reserve System. First

version: Dec 2020. This version: Jan 2021.

†

Department of Economics, University of Texas at Austin and CAMA, 2225 Speedway, Stop C3100,

Austin, TX 78712, U.S.A. Email: [email protected].

‡

Department of Economics, University of Virginia, PO BOX 400182, Charlottesville, VA 22904, U.S.A.

Email: [email protected].

§

Federal Reserve Board of Governors, 20th Street and Constitution Avenue NW, Washington, DC 20551,

U.S.A. Email: [email protected].

1

1 Introduction

What are the macroeconomic effects of redistribution policies that transfer resources from

one set of agents in the economy to another? What are the determinants of the transfer

multiplier? When is the transfer multiplier large? What are the welfare implications of

such redistribution policies?

Recently, the U.S. experienced the two largest contractions after World War II—the

Great Recession and the COVID-19 recession. The government responded to these con-

tractions with unprecedented fiscal measures—namely the American Recovery and Rein-

vestment Act of 2009 and the Coronavirus Aid, Relief, and Economic Security (CARES)

Act of 2020. These fiscal responses included significant transfer components, and they

have renewed interest in the effectiveness of transfer policies in terms of rebooting the

economy and improving household welfare.

In a dynamic general equilibrium model, one would have to take numerous factors

into account to answer the above questions.

1

In this paper, we focus on the source of

financing and show how the government finances transfers has a first-order importance

for their effectiveness. Our focus is motivated by the ongoing rapid increase in public

debt caused by the large-scale transfer programs. This eventually requires fiscal and/or

monetary adjustments, which would ultimately finance current transfers.

We compare two distinct ways to finance transfers in a two-agent New Keynesian

(TANK) model. In the model, a set of households are unable to borrow and lend to smooth

consumption over time. A transfer policy redistributes resources toward such "hand-to-

mouth" (HTM) households and away from "Ricardian" households that own government

bonds.

2

In the first policy regime, the government raises taxes. Inflation is then stabilized

in the usual way by the central bank. We call this case the "monetary regime." In the

second regime, the government commits itself to no adjustments in taxes, and the central

bank allows inflation to rise to stabilize the real value of debt, thereby imposing "inflation

taxes" on households that hold nominal government debt. In this "fiscal regime," the fiscal

theory of the price level operates.

We find that the effectiveness of transfer policy is directly tied to how much inflation

it generates. A transfer policy is inflationary irrespective of the policy regimes in the

model. It is, however, more inflationary in the fiscal regime than in the monetary regime.

1

We discuss previous findings in more detail later. Some well-known determinants of the fiscal mul-

tiplier are the marginal propensity to consume of targeted households and whether the economy is in a

liquidity trap.

2

As we describe in further detail later, in our application, we think of these HTM households as working

in the service sector that is affected by a large negative sectoral shock.

2

Therefore, inflation-financed transfers can be used to fight deflationary pressures during

recessions, thereby preventing output and consumption of both types of households from

dropping significantly. As a result, the welfare of both household types is higher when

transfers are inflation-financed than when they are tax-financed.

Furthermore, somewhat surprisingly, inflation-financed transfers can produce a Pareto

improvement relative to the no-transfer case. Notice that, since the model features stag-

gered Calvo-type price setting, inflation is not a free lunch: it generates, ceteris paribus,

significant resource misallocation, which leads to a decrease in labor productivity and

in welfare. These negative effects of inflation are, however, outweighed by the positive

effects of inflation in the low-inflation environment considered in this paper. In fact, with-

out an inflationary intervention, the economy would experience deflation, so there is little

cost of inflation.

Our paper starts with a simplified flexible-price version of the model that permits

analytical results, thereby allowing us to illuminate the mechanism of the fiscal theory

in a heterogeneous-household framework. This model also serves as a useful reference

point, as the two policy regimes produce exactly the same multipliers for output and

consumption and an identical level of household welfare, even if inflation dynamics are

different. This is due to two features. First, both conventional taxes, which are assumed

to be lump sum, and inflation taxes are non-distortionary. Second, price flexibility shuts

down any feedback effects from inflation on real variables.

3

For inflation, the fiscal regime gives rise to higher and more persistent inflation than

the monetary regime. In particular, transfers affect inflation through two channels in

this regime. First, an increase in transfers leads directly to an increase in public debt,

which accumulates over time. Consequently, inflation rises to stabilize the real value of

debt. Second, an increase in transfers may indirectly raise future public debt through an

interest rate channel. Redistribution changes Ricardian household consumption, which in

turn affects real interest rates and thus outstanding public debt in the following periods.

That is, redistribution generates a new valuation effect through real interest rate changes,

an effect that is absent in the standard one-agent model often used to analyze the fiscal

regime. This interest rate channel may lead to a further increase in inflation. Showing

these two effects explicitly in a nonlinear two-agent model is a contribution of our paper.

We then build on the analytical results and proceed to a quantitative analysis employ-

ing a two-sector TANK model. Relative to the simplified version, the quantitative model

3

The transfer multiplier for output is small yet still positive due to the classical labor supply channel.

Redistribution causes Ricardian household consumption to fall, creating a negative “wealth effect” on labor

supply. The households thus supply more hours for a given wage rate, which in turn raises output.

3

includes several realistic features that break the uniformity of the two regimes in terms of

the multipliers. The two most important are nominal rigidities and the "COVID shocks."

Sticky prices are important, as transfers now can increase output through the usual New

Keynesian channel by generating inflation—on top of the classical labor supply channel.

Introducing shocks is also consequential as the multipliers are generally state-dependent.

In particular, the COVID shocks cause the economy to fall into what we refer to as a

"COVID recession" as well as a liquidity trap, in which the effects of redistribution can be

different quantitatively. Finally, another difference from the analytical model is that the

government raises (gradually) labor taxes, rather than lump-sum taxes, in the monetary

regime, which, through distortionary effects, influences the transfer multipliers.

Specifically, in order to capture the salient characteristics of the COVID recession, we

suppose that the COVID shocks consist of adverse aggregate and sector-specific demand

shocks and sector-specific labor supply shocks. The sector-specific shocks intend to cap-

ture the observation that "locked out" of work and fear of "unsafe consumption" features

are more pronounced in certain sectors of the economy. We decompose the U.S. economy

into two sectors—(1) transportation, recreation, and food service sector and (2) the rest of

the economy—and let the HTM households work in the former sector in our model.

4

For

convenience, we call this sector the HTM sector.

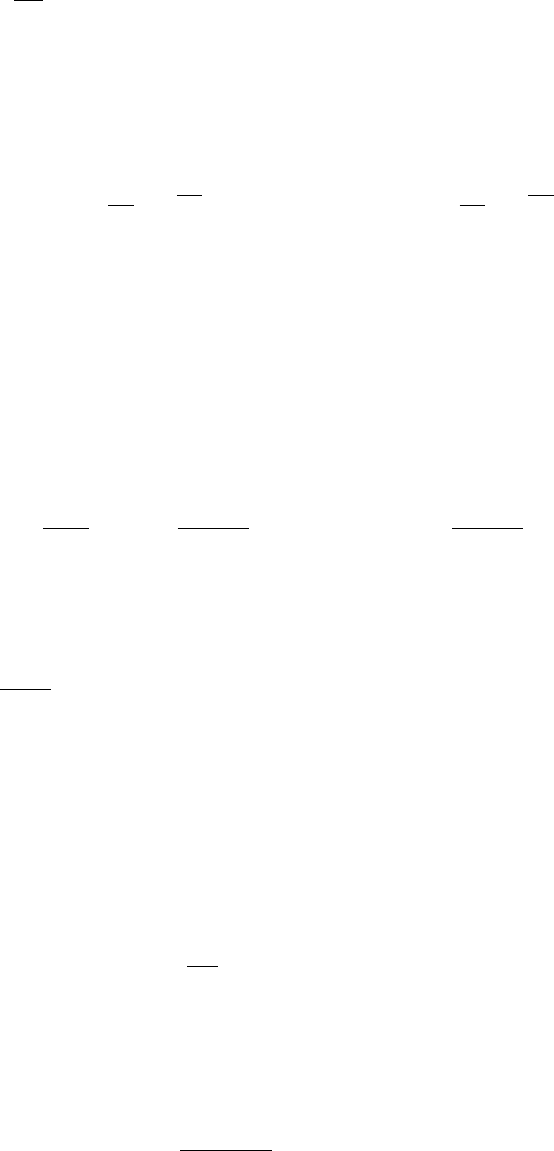

Figure 1 presents dynamics of employment, hours, inflation, and consumption based

on such a two-sector decomposition of the U.S. economy. As is clear, there was a sharp ad-

verse effect on employment/hours in the HTM sector following the COVID crisis. More-

over, inflation in this sector also fell. Finally, while the HTM sector was disproportionately

affected, there was also an aggregate, economy-wide contraction and fall in inflation as

well. We calibrate the COVID shocks to perfectly re-produce the dynamics of hours in

the two sectors and that of inflation in the HTM sector, thereby situating the model econ-

omy in a COVID-recession-like environment. We then calibrate the size of transfers to

match the transfer amount in the CARES Act and study how the economy responds to

the redistribution policy under several alternative scenarios.

5

We find that the transfer multipliers are significantly larger under the fiscal regime

than under the monetary regime, primarily because of the difference in inflation dynam-

ics as mentioned above. For instance, the four-year cumulative multiplier for aggregate

output is 1.126 in the monetary regime while it is 7.739 in the fiscal regime. Notice that

this multiplier is greater than unity even under the monetary regime, thanks to nom-

4

We assume that the Ricardian households work in the other sectors that are less affected by the COVID

pandemic.

5

We also show with the vertical dashed line in Figure 1 when transfer payments from the CARES Act

started to get mailed.

4

−−> CARES Act (Apr. 15)

−40

−30

−20

−10

0

Percent Deviation from Jan. 2020

1 2 3 4 5 6 7 8

2020

Total

Retail, Transportation,

Leisure and Hospitality

Others

Panel A: Employment

−40

−30

−20

−10

0

Percent Deviation from Jan. 2020

1 2 3 4 5 6 7 8

2020

Total

Retail, Transportation,

Leisure and Hospitality

Others

Panel B: Total Hours

−70

−60

−50

−40

−30

−20

−10

0

10

Percent Deviation from Jan. 2020

1 2 3 4 5 6 7 8

2020

Total

Transportation, Recreation,

and Food Services

Others

Panel C: Real PCE

−2

−1.5

−1

−.5

0

.5

1

Percent Deviation from Jan. 2020

1 2 3 4 5 6 7 8

2020

Total

Transportation, Recreation,

and Food Services

Others

Panel D: PCE Inflation

Figure 1: Aggregate and Sectoral Effects of COVID Crisis

Notes: This figure shows the dynamics of key variables from January 2020. Panels A and B show employ-

ment and total hours dynamics in U.S. Bureau of Labor Statistics, respectively. Black lines are dynamics

of total variable and red lines represent retail, transportation, leisure, and hospitality sector, and blue

lines represent all other sectors. Panels C and D present real personal consumption expenditure and

PCE inflation in U.S. Bureau of Economic Analysis, respectively. Black lines are dynamics of total vari-

able and red lines represent transportation, recreation and food services sector, and blue lines represent

all other sectors.

Sources: U.S. Bureau of Economic Analysis, U.S. Bureau of Labor Statistics

inal rigidities and the binding zero lower bound (ZLB). Just as strikingly different are

the four-year cumulative consumption multipliers. For the Ricardian households, it is

negative 0.244 in the monetary regime and 6.036 in the fiscal regime, while for the HTM

households, it is 5.609 in the monetary regime and 13.311 in the fiscal regime.

6

We isolate the role played by various model elements in driving our quantitative re-

6

The positive consumption multiplier for the Ricardian household is unique, even qualitatively so, in

the fiscal regime.

5

sults using counterfactual exercises. The unusually large multipliers reported above, es-

pecially under the fiscal regime, result from the economy being situated in the historically

severe COVID-recession with large deflationary pressures. For example, shutting down

the COVID shocks, the four-year cumulative multiplier for aggregate output is 0.96 in the

monetary regime, while it is 1.475 in the fiscal regime. This result underscores the state-

dependency of policy effects. Importantly, the difference in the multipliers for output

and consumption between the two regimes gets larger in the presence of COVID shocks,

which implies that while both labor-tax-financed transfers and inflation-financed trans-

fers are more effective in the COVID recession than in a normal environment, the latter is

even more so. In addition, we also find that relying on labor taxes rather than lump-sum

taxes in the monetary regime plays a role.

Overall, as a consequence, the contraction in output and consumption is much more

muted when transfers are financed by inflation taxes. Specifically, transfers, when inflation-

financed, would reduce the output loss caused by the COVID shocks by roughly 5 per-

centage points at the trough compared to no-intervention case. We also find that the

expansionary effects of inflation-financed transfers are so large that such redistribution

policy generates a Pareto improvement: It increases the welfare of both the recipients and

sources of transfers, even taking into account the resources taken away from the Ricar-

dian household and the fact that the Ricardian household’s leisure decreases as a result

of output increases and distortions generated by high and persistent inflation.

Our paper builds on several strands of the literature. It is related to the fiscal-monetary

interactions literature as originally developed in Leeper (1991), Sims (1994), Woodford

(1994), Cochrane (2001), Schmitt-Grohé and Uribe (2000), and Bassetto (2002).

7

Sims

(2011) introduced long-term debt under this regime in a sticky price model, while Cochrane

(2018) developed it further to analyze the inflation implications following the Great Re-

cession. Analytical characterization of the fiscal regime in a linearized sticky price model

is in Bhattarai, Lee and Park (2014).

Our additional analytical contribution here is to derive the fully nonlinear results of

this fiscal regime in a tractable two-agent model. Motivated by the COVID crisis and the

CARES Act, we then assess the quantitative effects of redistribution policy as well as its

welfare implications in a two-sector, two-agent nonlinear model.

We build on two-agent models as originally developed in Campbell and Mankiw

(1989), Galí, López-Salido and Vallés (2007), and Bilbiie (2018). Moreover, Bilbiie, Mona-

celli and Perotti (2013), closely related to this paper, show that different financing schemes

affect the size of the output transfer multiplier in a TANK model. However, they only

7

Canzoneri, Cumby and Diba (2010) and Leeper and Leith (2016) are recent surveys of this literature.

6

consider the monetary regime. Our main contribution is in assessing the effects of redis-

tribution policy in such an environment and showing how it depends critically on the

monetary-fiscal policy mix.

Recently there have been several contributions to an analysis of macroeconomic ef-

fects of the COVID crisis. Our quantitative two-sector, two-agent model is closest to the

important work of Guerrieri, Lorenzoni, Straub and Werning (2020). In assessing the

quantitative effects of fiscal policy during the pandemic using a model with household

heterogeneity, we are also related to Faria-e-Castro (2020) and Bayer, Born, Luetticke and

Müller (2020). Our relative contribution is in showing how the effects of redistribution

depend on the monetary-fiscal policy regime and then assessing both quantitative effects

and welfare implications by matching some important aggregate and sectoral aspects of

the U.S. data.

Our paper is also related to recent papers that analyze monetary-fiscal policy interac-

tions in TANK models—in particular, Bhattarai, Lee, Park and Yang (2020), Bianchi, Fac-

cini and Melosi (2020), and Motyovszki (2020). Bhattarai, Lee, Park and Yang (2020) study

the effects of one-time permanent capital tax rate changes in a model that also features

capital-skill complementarity. Bianchi, Faccini and Melosi (2020) and Motyovszki (2020)

are motivated by the COVID crisis and are closely related to our analysis.

8

Our relative

contribution analytically is a nonlinear solution of the simple TANK model under the two

regimes. On the quantitative side, while these studies focus on the positive implications

of transfers under the different regimes, we additionally provide welfare implications for

different types of households. We also emphasize that the positive and normative im-

plications of redistribution are state-dependent and that inflation-financed transfers are

disproportionately more effective than tax-financed transfers in a COVID-recession-like en-

vironment in which both sector-specific and aggregate shocks hit the economy.

Finally, our paper is also related to the government spending multiplier literature, as

the effects of transfer policy in two-agent models share some common elements with the

effects of government spending policy in representative agent models. Thus, in connect-

ing the effects to the nature of monetary policy, the binding ZLB, and the monetary-fiscal

policy regime, our work builds on important contributions in the government spend-

ing multiplier literature by Woodford (2011), Christiano, Eichenbaum and Rebelo (2011),

Eggertsson (2011), Leeper, Traum and Walker (2017), and Jacobson, Leeper and Preston

(2019).

8

Bianchi, Faccini and Melosi (2020) show that inflating away a targeted fraction of debt will increase

the effectiveness of the fiscal stimulus in a rich medium-scale model while Motyovszki (2020) considers a

small-open economy environment.

7

2 Simple Model and Redistribution Policy

We present a simple model that yields analytical results on effects of redistribution policy.

2.1 Model

There are two types of households: Ricardian and HTM. The Ricardian household makes

optimal labor supply and consumption/savings decisions, while the HTM household

simply consumes government transfers every period. In this setup, we analytically show

the effects on inflation of transferring resources away from the Ricardian households to

the HTM households and point out that these effects depend critically on how the transfer

policy is financed.

2.1.1 Households

Ricardian Households. There are Ricardian households of measure 1 − λ. These house-

holds, taking prices as given, choose {C

R

t

, L

R

t

, B

R

t

} to maximize

∞

∑

t=0

β

t

"

log C

R

t

− χ

L

R

t

1+ϕ

1 + ϕ

#

subject to a standard No-ponzi-game constraint and a sequence of flow budget constraints

C

R

t

+

B

R

t

P

t

= R

t−1

B

R

t−1

P

t

+ w

t

L

R

t

+ Ψ

R

t

− τ

R

t

,

where C

R

t

is consumption, L

R

t

is hours, B

R

t

is nominal government debt, Ψ

R

t

is real profits,

τ

R

t

is lump-sum taxes, P

t

is the price level, w

t

is the real wage, and R

t

is the nominal gross

interest rate. The discount factor and the inverse of the Frisch elasticity are denoted by

β ∈ ( 0, 1) and ϕ ≥ 0 respectively. The superscript, R, represents “Ricardian”. The flow

budget constraints can be written as

C

R

t

+ b

R

t

= R

t−1

1

Π

t

b

R

t−1

+ w

t

L

R

t

+ Ψ

R

t

− τ

R

t

,

where b

R

t

=

B

R

t

P

t

is the real value of debt, and Π

t

=

P

t

P

t−1

is the gross rate of inflation.

Optimality conditions are given by the Euler equation, the intra-termporal labor sup-

ply condition, and the transversality condition (TVC):

C

R

t+1

C

R

t

= β

R

t

Π

t+1

, (2.1)

8

χ

L

R

t

ϕ

C

R

t

= w

t

, (2.2)

lim

t→∞

β

t

1

C

R

t

B

R

t

P

t

= 0. (2.3)

Hand-to-Mouth Households. The hand-to-mouth (HTM) households, of measure λ,

simply consume government transfers, s

H

t

, every period

C

H

t

= s

H

t

,

and have no optimization problem to solve. The superscript, H, represents “HTM”.

2.1.2 Firm

A representative firm in the competitive product market chooses hours, L

t

, in each period

to maximize profits:

Ψ

t

= Y

t

− w

t

L

t

,

subject to the production function

Y

t

= L

t

. (2.4)

Zero profit condition implies

w

t

= 1. (2.5)

2.1.3 Government

The government issues one-period nominal debt, B

t

. Its budget constraint (GBC) is

B

t

P

t

= R

t−1

B

t−1

P

t

− τ

t

+ s

t

,

where s

t

is transfers and τ

t

is taxes. It can be re-written as

b

t

=

R

t−1

Π

t

b

t−1

− τ

t

+ s

t

, (2.6)

where b

t

=

B

t

P

t

is the real value of debt. Transfer, s

t

, is exogenous and deterministic.

Monetary and tax policy rules are

R

t

¯

R

=

Π

t

¯

Π

φ

, (2.7)

(

τ

t

−

¯

τ

)

= ψ(b

t−1

−

¯

b), (2.8)

9

where φ and ψ determine the responsiveness of the policy instruments to inflation and

government indebtedness respectively. The steady-state values of inflation, debt, and

transfers,

¯

Π,

¯

b,

¯

s

, are set by policymakers and given exogenously.

2.1.4 Aggregation and the Resource Constraint

Aggregating the variables over the households yields s

t

= λs

H

t

, τ

t

=

(

1 − λ

)

τ

R

t

, b

t

=

(

1 − λ

)

b

R

t

, L

t

=

(

1 − λ

)

L

R

t

, and Ψ

t

=

(

1 − λ

)

Ψ

R

t

. Combining household and govern-

ment budget constraints gives:

(1 − λ)C

R

t

+ λC

H

t

= Y

t

.

The resource constraint above, together with the HTM household budget constraint, im-

plies that output is simply divided between the two types of households as:

C

H

t

=

1

λ

s

t

, C

R

t

=

1

1 − λ

Y

t

−

1

1 − λ

s

t

. (2.9)

2.2 Effects of Redistribution Policy

We now show the effects of transferring resources away from the Ricardian households

to the HTM households. The government can finance such a transfer program in two

distinct ways. In the first policy regime, the government raises taxes sufficiently. Inflation

is then stabilized in the usual way by the central bank. In the second regime, the govern-

ment does not raise taxes, and the central bank allows inflation to rise to stabilize the real

value of debt, thereby imposing “inflation taxes” on the Ricardian households that hold

nominal government debt. The fiscal theory of the price level operates in this case.

We solve for the equilibrium time path of

Y

t

, C

R

t

, C

H

t

, Π

t

, R

t

, b

t

, τ

t

given exogenous

{

s

t

}

. Output and consumption of the two households, and thus their welfare, are in-

dependent of whether the government relies on conventional or inflation taxes.

9

We

first consider those policy-invariant variables in Section 2.2.1. The alternative financing

schemes, however, generate quite different inflation dynamics, which is the main focus

of this simple model. The rise of inflation tends to be greater and more persistent in the

second regime. The determination of the rate of inflation is detailed in Section 2.2.2.

9

This “neutrality” result does not hold in a model with nominal rigidities, as discussed in detail later.

10

2.2.1 Output and Consumption

We start with output. Equation (2.2) can be written as

Y

t

= χ

−1

(

1 − λ

)

1+ϕ

Y

−ϕ

t

+ s

t

(2.10)

using Equations (2.4), (2.5), and (2.9). Equation (2.10) implicitly defines output as a func-

tion of transfers: Y

t

= Y

(

s

t

)

. Then, one can obtain the “transfer multiplier” as

dY

(

s

t

)

ds

t

=

1

1 +

(

1 − λ

)

1+ϕ

ϕ

χ

Y

−

(

1+ϕ

)

t

.

Notice that 0 ≤

dY

t

ds

t

≤ 1.

An increase in transfers raises output not for the Keynesian demand-side reason. The

channel here instead is purely classical and supply-side: An increase in s

t

causes Ricar-

dian household consumption to fall, creating a negative “wealth effect” on labor supply.

The households supply more hours for a given wage rate, which in turn raises output.

10

The multiplier is maximized (dY

t

/ds

t

= 1) when labor supply is perfectly elastic (ϕ = 0)

while it is minimized (dY

t

/ds

t

= 0) when the Ricardian household does not value leisure

(χ = 0), which shuts down the wealth effect.

The Ricardian household consumption is obtained from Equation (2.9) as

C

R

t

= C

R

(

s

t

)

≡

1

1 − λ

[

Y

(

s

t

)

− s

t

]

. (2.11)

The derivative is

dC

R

(

s

t

)

ds

t

=

1

1 − λ

dY

(

s

t

)

ds

t

− 1

≤ 0.

As will be clear below, how Ricardian household consumption depends on transfers mat-

ter for inflation dynamics as it affects the real interest rate. That is, there is a valuation

effect on government debt due to changes in the real interest rate. This interest rate channel

of transfers is absent in the model with a representative household, where transfers have

no redistributive role, or with a perfectly elastic labor supply.

Notice that both tax types are non-distorting in this model. Consequently, for given

{

s

t

}

, the alternative ways to finance transfers (i.e., the policy regimes) have no effect on

output and consumption, as seen above.

10

The channel thus is the same as the effect of government spending in a one-agent model.

11

2.2.2 Inflation

We now turn to the rest of the variables,

{

Π

t

, R

t

, b

t

, τ

t

}

∞

t=0

, with a focus on inflation de-

termination, given a path of

{

s

t

}

∞

t=0

. The equilibrium time path of

{

Π

t

, R

t

, b

t

, τ

t

}

satisfies

the following conditions:

• Difference Equations from (2.1), (2.6), (2.7) and (2.8):

Π

t+1

=

C

R

t

C

R

t+1

βR

t

, b

t

= R

t−1

b

t−1

1

Π

t

− τ

t

+ s

t

,

R

t

¯

R

=

Π

t

¯

Π

φ

,

(

τ

t

−

¯

τ

)

= ψ(b

t−1

−

¯

b).

• Terminal condition, as given by TVC from Equation (2.3):

lim

t→∞

β

t

1

C

R

t

b

t

= 0.

• Initial conditions:

b

−1

and R

−1

.

We first solve for the deterministic steady state. When s

t

=

¯

s ∀t, the system of differ-

ence equations simplifies to

¯

R = β

−1

¯

Π,

¯

τ =

β

−1

− 1

¯

b +

¯

s,

with the TVC trivially satisfied. Given

¯

s,

¯

Π and

¯

b, which we assume exogenously deter-

mined by policymakers, the equations above determine

¯

R and

¯

τ. We set R

−1

=

¯

R and

b

−1

=

¯

b, without loss of generality.

The system of difference equations can be simplified as

11

:

Π

t+1

¯

Π

=

C

R

t

C

R

t+1

Π

t

¯

Π

φ

, (2.12)

b

t

−

¯

b

=

"

β

−1

C

R

t

C

R

t−1

− ψ

#

(b

t−1

−

¯

b) +

(

s

t

−

¯

s

)

+

¯

b

"

β

−1

C

R

t

C

R

t−1

− β

−1

#

∀t ≥ 1 (2.13)

b

0

−

¯

b

= β

−1

¯

Π

Π

0

− 1

¯

b +

(

s

0

−

¯

s

)

at t = 0, (2.14)

which determines

{

Π

t

, b

t

}

given

{

s

t

}

and

C

R

t

, where note that from Equation (2.11),

the latter is a simple function of transfers.

11

The online appendix provides detail.

12

Equation (2.12), obtained by combining the Euler equation and the monetary policy

rule, shows how future inflation (Π

t+1

) depends on current inflation (Π

t

) and the real

rate captured by C

R

t+1

/C

R

t

. Equation (2.13) is the GBC for t ≥ 1 after we substitute out the

nominal interest rate (R

t−1

) and taxes (τ

t

) using the Euler equation and the fiscal policy

rule. Equation (2.14) is the GBC at t = 0. This looks different from Equation (2.13) because

R

−1

is exogenous, and thus cannot be replaced by the Euler equation.

Equation (2.13) describes how the deviation of the real value of debt from the steady

state,

b

t

−

¯

b

, evolves over time. An increase in transfers over its steady state value

(s >

¯

s) affect debt dynamics directly and indirectly. First, ceteris paribus, such an increase

causes b

t

, debt carried over to the next period, to rise above

¯

b. This direct effect is captured

by the second term,

(

s

t

−

¯

s

)

, on the right hand side of Equation (2.13). Second, a change

in transfers affects Ricardian household consumption as shown in Equation (2.11) and

hence the real interest rate, which in turn influences debt dynamics. This indirect effect is

reflected by r

t−1

≡ β

−1

C

R

t

C

R

t−1

in Equation (2.13), and operates even when the current period

debt stays at the steady state (i.e. b

t−1

=

¯

b). The reason is a change in interest payments

for a given amount of debt—as shown in the last term,

¯

b

β

−1

C

R

t

C

R

t−1

− β

−1

.

In solving the system, we consider a redistribution program in which

{

s

t

}

∞

t=0

can have

arbitrary values greater than

¯

s until a time period T, and then s

t

=

¯

s for t ≥ T + 1. In this

case, regardless of the history until time T + 1, starting T + 2, Equation (2.13) becomes

b

t

−

¯

b

=

β

−1

− ψ

(b

t−1

−

¯

b).

How the TVC is satisfied depends on the fiscal policy parameter ψ. When ψ > 0, debt

dynamics satisfies the TVC regardless of the value of b

T+1

.

12

When ψ ≤ 0, however, the

TVC requires b

T+1

=

¯

b, which can be achieved when monetary policy allows inflation to

adjust by the required amount. Below, we discuss each case in turn.

Inflation under the Monetary Regime. When ψ > 0, , inflation is solely determined by

Equation (2.12) which becomes

Π

t+1

¯

Π

=

Π

t

¯

Π

φ

for t ≥ T + 1,

as C

R

t

, Ricardian household consumption, is constant. In this case, if we were to consider

φ < 1, the system of Equations (2.12)–(2.14) does not pin down initial inflation Π

0

, and

the model permits multiple non-explosive solutions.

12

In addition, ψ should not be too big. We do not explicitly consider such empirically irrelevant cases.

13

We therefore, instead consider the standard case, φ > 1, which we call the monetary

regime. This regime produces multiple equilibria in which inflation is unbounded and a

unique bounded equilibrium.

13

Here we focus on the bounded equilibrium. In this case,

it is necessary that

Π

T+1

¯

Π

= 1.

Given this “stability” condition on inflation, one can pin down Π

t

from t = 0 to T along

the saddle path. In particular, inflation before T + 1 can be solved backward using Equa-

tion (2.12). The initial inflation is given by

Π

0

¯

Π

= C

R

(

¯

s

)

1

φ

T+1

1

C

R

(

s

T

)

C

R

(

s

T−1

)

· · · C

R

(

s

0

)

1

φ

=

T

∏

t=0

C

R

(

¯

s

)

C

R

(

s

t

)

1

φ

. (2.15)

Inflation in the following periods is then determined by Equation (2.12).

Equation (2.15) shows that an increase in transfers is inflationary as the Ricardian

household consumption declines below the pre-transfer level. The magnitude of the ef-

fect depends on the response of monetary policy (measured by φ), the size of transfer

increases, and the duration of the redistribution program. Most importantly, the effect

is transitory: When the redistribution program ends, inflation returns immediately to the

steady-state value. Finally, redistribution programs with the same value of total transfer

payments, but with different payment schedules, have different implications for the real

interest rate and inflation dynamics. We discuss this in more detail below.

Inflation under the Fiscal Regime. We now consider the fiscal regime where ψ ≤ 0 and

φ < 1. Solving for inflation involves a similar procedure as in the monetary regime. We

first identify a terminal condition and follow the saddle path to pin down initial inflation.

As mentioned above, when ψ ≤ 0, the TVC requires b

T+1

=

¯

b. Given this terminal

condition, debt in preceding periods can be solved backward using Equation (2.13). Fi-

nally, given the solved b

0

, the time-0 GBC Equation (2.14) determines initial inflation Π

0

,

after which Equation (2.12) produces a non-explosive time path of inflation.

Before presenting the general solution, we consider a simple example that is helpful

to develop the intuition. Suppose transfers increase only for one period: s

0

>

¯

s and

s

t

=

¯

s afterwards. In the single-period redistribution program, it is necessary that b

1

=

¯

b;

13

We rule out the case in which the price level approaches zero by the TVC.

14

otherwise, the TVC would be violated. The GBC at t = 1 is then given as

b

1

−

¯

b

| {z }

=0

=

β

−1

C

R

(

¯

s

)

C

R

(

s

0

)

| {z }

>1

− ψ

(b

0

−

¯

b) +

(

s

1

−

¯

s

)

| {z }

=0

+

¯

b

β

−1

C

R

(

¯

s

)

C

R

(

s

0

)

| {z }

>1

− β

−1

, (2.16)

from which we can obtain the initial debt level b

0

ensuring that b

1

equals

¯

b:

b

0

=

¯

b −

¯

b

β

−1

C

R

(

¯

s

)

C

R

(

s

0

)

− ψ

−1

β

−1

C

R

(

¯

s

)

C

R

(

s

0

)

− β

−1

.

The terminal condition (b

1

=

¯

b) requires b

0

to decline below

¯

b. For this to happen, Π

0

adjusts according to Equation (2.14):

Π

0

¯

Π

=

1

1 −

β

¯

b

(

s

0

−

¯

s

)

− β

h

β

−1

C

R

(

¯

s

)

C

R

(

s

0

)

− ψ

i

−1

h

β

−1

C

R

(

¯

s

)

C

R

(

s

0

)

− β

−1

i

. (2.17)

The redistribution policy is more inflationary under the fiscal regime than under the

monetary regime. Inflation rises by more on impact: Π

0

in Equation (2.17) is greater than

Π

0

in Equation (2.15) even under the most dovish monetary regime (i.e. when φ → 1.)

More importantly, the one-time transitory increase in transfers has persistent effects on

inflation here, while the effect lasts only for one period under the monetary regime.

The result above holds without the interest rate channel. The presence of the third term

in the denominator, −β

[

r

0

− ψ

]

−1

[

r

0

−

¯

r

]

, however, does cause Π

0

to increase by more

than it would in an analogous model with a representative household where transfer

changes have no effect on the real interest rate.

14

This term results from increased interest

payments that exert an upward pressure on b

1

(see Equation (2.16)). The upward pressure

is offset by a further decrease in b

0

, which is generated by a greater increase in Π

0

.

The effects of the interest rate channel on inflation, however, is subtler in a multi-

period redistribution program. The initial inflation in the general case is given by

15

Π

0

¯

Π

=

1

1 −

β

¯

b

∑

T

k=0

Ω

k

(

s

k

−

¯

s

)

− β

∑

T+1

k=1

Ω

k

h

β

−1

C

R

(

s

k

)

C

R

(

s

k−1

)

− β

−1

i

, (2.18)

14

In that model, the term would drop because

C

R

1

C

R

0

= 1.

15

The online appendix provides detail.

15

where the “discount factor” Ω

k

is defined as:

Ω

k

≡ Ω

k−1

β

−1

C

R

(

s

k

)

C

R

(

s

k−1

)

− ψ

−1

=

(

k

∏

j=1

"

β

−1

C

R

s

j

C

R

s

j−1

− ψ

#)

−1

, Ω

0

≡ 1.

The solution (2.18) reveals that the interest rate channel can in principle, work in both

directions. On the one hand, as shown in the one-period transfer increase case, a redistri-

bution program that raises the real interest rate leads to an increase in interest payments

and a larger rise in inflation—as captured by the last term in the denominator. On the

other hand, such redistribution decreases the discount factor Ω

k

. The economy thus dis-

counts future primary surplus/deficits more heavily, which causes inflation to adjust by

less when future transfers rise.

16

Therefore, generally, the net effect on inflation through

the interest rate channel of a multi-period redistribution program is difficult to isolate

analytically, without further restrictions on the path of transfers.

17

In this paper, we focus on programs with constant s

t

for 0 ≤ t ≤ T. In such a case,

the interest rate channel works in the same way as described in the simple example, and

leads to a larger response of inflation. To show this, we use the property that the real

interest rate is constant throughout except for the last period of a program; that is, r

t

=

¯

r

for 0 ≤ t ≤ T − 1 and r

T

>

¯

r, if s

t

= s

0

>

¯

s for 0 ≤ t ≤ T. Equation (2.18) simplifies to

Π

0

¯

Π

=

1

1 −

β

¯

b

(

s

0

−

¯

s

)

∑

T

k=0

(

β

−1

− ψ

)

−k

− β

(

r

T

− ψ

)

−1

(

r

T

−

¯

r

) (

β

−1

− ψ

)

−T

,

which looks similar to Equation (2.17).

2.3 Summary and an Extension to Nominal Rigidities

To summarize, transferring resources from Ricardian to HTM households is inflationary

regardless of the financing schemes considered. The fiscal regime, in which the govern-

ment effectively imposes “inflation taxes” on Ricardian households that hold nominal

government debt, however, generates greater and more persistent inflation than the mone-

tary regime that finances transfers raising “conventional taxes.”

16

Equation (2.16) also provides intuition: To achieve a target level of b

1

, b

0

needs not decrease as much

when the coefficient (which is increasing in the real rate) is greater; consequently, inflation increases by less.

17

Moreover, there is a significant flexibility in the schedule of transfer payments when studying a multi-

period redistribution program. The time path of transfers

{

s

t

}

T

t=0

can be constant, (weakly) monotonic, or

neither. Depending on the time path, the real interest rate, β

−1

C

R

(

s

t

)

C

R

(

s

t−1

)

, need not be greater than or equal to

its steady-state value β

−1

for the entire duration of a redistribution program. Interest payments thus can be

lower than the pre-program level in some periods. Generally, different transfer schedules would result in

different dynamics of the real interest rate. A constant or monotonic schedule is however, most commonly

used in quantitative models.

16

When it comes to output, consumption, and hours, the policy regimes are “neutral.”

As we mentioned before, this result does not carry over to a model with nominal rigidi-

ties. In the online appendix, we provide a simple sticky-price model that permits some

analytical results with simplifying assumptions. The model nests the flexible-price model

presented so far as a special case.

18

The result on inflation is essentially the same in that

model. A redistribution program generates greater and more persistent inflation under

the fiscal regime. Analytical results on inflation are more difficult to obtain, as Ricar-

dian household consumption now also depends on inflation. Thus, the solution involves

finding a fixed point in an equation analogous to Equation (2.17). Nevertheless, the mech-

anisms discussed in Sections 2.2.1 and 2.2.2 still apply.

The policy regimes are no longer neutral for output, consumption, and hours with

sticky prices because of the short-run relationship between output and inflation. Abusing

the notation, and in comparison to output in Equation (2.10), it is convenient to regard

output now as a function of transfers and inflation, where inflation in turn is also a func-

tion of the entire schedule of transfers:

Y

t

= Y

s

t

, Π

t

{

s

t

}

T

t=0

.

Therefore, output would increase not only through the (labor) supply channel. When

wealth redistribution is inflationary, output would increase further due to the demand-

side channel. Consequently, Ricardian household consumption in Equation (2.9) would

not decrease as much as in the flexible-price case, while HTM household consumption

would still be unaffected.

Since inflation generally increases by more under the fiscal regime compared to the

monetary regime, alternative financing schemes now have different welfare implications.

With inflation taxes, Ricardian household consumption would not decrease as much,

which would increase their welfare. At the same time, the Ricardian households would

have to work more not only to produce more output but in addition, high and persistent

inflation in the fiscal regime produces resource misallocations, which increase labor hours

required to produce the same amount of final output. Therefore, it is unclear a priori that

inflation taxes are a better or worse way to finance a redistribution program compared to

other taxes. We explore this question in a quantitative model in the next section.

18

The next section presents a quantitative sticky-price model. In addition, the role of nominal rigidities

(in this simple model) is relatively easy to understand as discussed below. Therefore, for brevity, we do not

present this sticky price extension of the simple model in the main text.

17

3 Quantitative Model and COVID Application

We now present a quantitative version of the model with an application focused on the

economic crisis induced by COVID, modeled by introducing demand and supply shocks,

and subsequent transfer policy, as embedded in the CARES Act. Compared to the simple

model, the main extension is a development of a two-sector production structure with

sticky prices, as well as the introduction of distortionary taxes such that the trade-off be-

tween different sources of financing government debt is meaningful. We then analyze

how the implications of increasing transfers to HTM households, which are hit dispro-

portionately in a COVID crisis, depend on the monetary-fiscal policy mix.

3.1 Model

There are two distinct sectors where the two types of households work. Each sector pro-

duces a distinct good, which is in turn produced in differentiated varieties. Firms in both

sectors are owned by the Ricardian household. The government finances transfers to the

HTM household by levying distortionary labor taxes on the Ricardian household. In the

fiscal regime, partial financing also happens by inflating away nominal debt.

3.1.1 Ricardian Sector

Households. Ricardian (R) households, of measure 1 − λ, solve the problem

max

{C

R

t

,L

R

t

,

B

R

t

P

R

t

}

∞

∑

t=0

β

t

exp(η

ξ

t

)

"

C

R

t

1−σ

1 − σ

− χ

L

R

t

1+ϕ

1 + ϕ

#

subject to a standard No-ponzi-game constraint and sequence of flow budget constraints

C

R

t

+ b

R

t

= R

t−1

1

Π

R

t

b

R

t−1

+

1 − τ

R

L,t

w

R

t

L

R

t

+ Ψ

R

t

,

where σ is the coefficient of relative risk aversion, η

ξ

t

is a preference shock, C

R

t

is con-

sumption, L

R

t

is labor supply, b

R

t

=

B

R

t

P

R

t

is the real value of government issued debt, Π

R

t

is

inflation, R

t−1

is the nominal interest rate, w

R

t

is the real wage, and Ψ

R

t

is real profits (this

household owns firms in both sectors). Labor tax, (1 − τ

R

L,t

), constitutes one way in which

the government finances transfers to the Hand-to-mouth household.

Consumption good C

R

t

is a CES aggregator (ε > 0) of the consumption goods pro-

duced in the two sectors

C

R

t

=

(

α

)

1

ε

C

R

R,t

ε−1

ε

+

(

1 − α

)

1

ε

exp(ζ

H,t

)C

R

H,t

ε−1

ε

ε

ε−1

18

where C

R

R,t

and C

R

H,t

are R-household’s demand for R-sector and for HTM-sector goods,

respectively. α is Ricardian households’ consumption weight on R-sector goods and ζ

H,t

is a demand shock that is specific for HTM goods. Let us define for future use, one of the

relative prices, S

R,t

≡

P

R

R,t

P

R

t

, where P

R

R,t

is the R-sector’s good price while P

R

t

is the CPI

price index of the R-household.

Within each sector, differentiated varieties are produced under monopolistic competi-

tion. Thus, C

R

R,t

and C

R

H,t

are Dixit-Stiglitz aggregates of a continuum of varieties. That is,

with θ > 1,

C

R

R,t

=

Z

1

0

C

R

R,t

(i)

θ−1

θ

di

θ

θ−1

, C

R

H,t

=

Z

1

0

C

R

H,t

(i)

θ−1

θ

di

θ

θ−1

.

Firms. Firms produce differentiated varieties using the linear production function

Y

R,t

(

i

)

= L

R

t

(i) ,

and set prices according to the Calvo friction, where ω

R

is the probability of not getting a

chance to adjust prices. Firms that get to adjust prices solve the maximization problem

max

{P

R∗

R,t

(i)}

∞

∑

s=0

ω

R

β

s

C

R

t+s

C

R

t

!

−σ

"

P

R∗

R,t

(

i

)

P

R

R,t+s

!

S

R,t+s

− w

R

t+s

#

P

R∗

R,t

(

i

)

P

R

R,t+s

!

−θ

Y

R,t+s

where P

R∗

R,t

(

i

)

denotes the optimally chosen price. There is no price discrimination across

sectors for varieties and we impose the law of one price. Thus, we write demand directly

in terms of Y

R,t

(i) =

P

R

R,t

(i)

P

R

R,t

−θ

Y

R,t

, which is derived from the household’s expenditure

minimization problem across varieties.

3.1.2 Hand-to-Mouth Sector

Households. There are Hand-to-mouth (HTM) households of measure λ. HTM house-

hold’s labor endowment is exogenously fixed and can change with a shock. The HTM

household then consumes, every period, wage income and government transfers

C

H

t

= w

H

t

L

H

(1 + η

ξ

t

) + s

H

t

,

where η

ξ

t

is HTM labor supply shock.

The utility function of the HTM is (again, labor supply is inelastic)

C

H

t

1−σ

1 − σ

19

where the aggregate consumption C

H

t

is a CES aggregator of sector-specific goods

C

H

t

=

(

1 − α

)

1

ε

exp

(

ζ

H,t

)

C

H

H,t

ε−1

ε

+

(

α

)

1

ε

C

H

R,t

ε−1

ε

ε

ε−1

and where 1 − α is HTM households’ consumption weight on HTM-sector goods while

ζ

H,t

is a demand shock specific for HTM-sector goods.

19

Let us define for future use one

of the relative prices, S

H,t

≡

P

H

H,t

P

H

t

, where P

H

H,t

is the HTM sector’s good price while P

H

t

is

the CPI price index of the HTM household. C

HH,t

and C

HR,t

are Dixit-Stiglitz aggregates

of a continuum of varieties. That is, with θ > 1,

C

H

H,t

=

Z

1

0

C

H

H,t

(

i

)

θ−1

θ

di

θ

θ−1

, C

H

R,t

=

Z

1

0

C

H

R,t

(

i

)

θ−1

θ

di

θ

θ−1

.

Firms. Firms produce differentiated varieties using the linear production function

Y

H,t

(

i

)

= L

H

t

(i)

and set prices according to the Calvo friction, where ω

H

is the probability of not getting

a chance to adjust prices. Firms that get to adjust prices solve the maximization problem

max

{P

H∗

H,t

(i)}

∞

∑

s=0

ω

H

β

s

C

R

t+s

C

R

t

!

−σ

"

P

H∗

H,t

(

i

)

P

H

H,t+s

!

P

H

t+s

P

R

t+s

S

H,t+s

−

P

H

t+s

P

R

t+s

w

H

t+s

#

P

H∗

H,t

(

i

)

P

H

H,t+s

!

−θ

Y

H,t+s

where P

H∗

H,t

(

i

)

denotes the optimally chosen price.

3.1.3 Government

The government flow budget constraint is

B

t

+ T

L

t

= R

t−1

B

t−1

+ P

R

t

s

t

,

where tax revenues T

L

t

=

(

1 − λ

)

τ

R

L,t

P

R

t

w

R

t

L

R

t

. Transfer (deflated by CPI of the Ricardian

household), s

t

, is exogenous and deterministic. Note that, s

t

= λs

H

t

and b

t

=

(

1 − λ

)

b

R

t

.

Monetary and tax policy rules are of the feedback types given by

R

t

¯

R

= max

(

1

¯

R

,

(

1 − λ

)

Π

R

t

+ λΠ

H

t

¯

Π

φ

)

, τ

R

L,t

−

¯

τ

R

L

= ψ

L

(b

t−1

−

¯

b),

where the zero lower bound on the nominal rate applies. As in the simple model, the

monetary regime will feature a large enough monetary and tax rule response coefficients,

19

Our modeling choice of the same consumption basket for the two types of households is driven by the

data, as we discuss later. This implies that CPI of the two households is the same.

20

φ and ψ

L

, such that government debt sustainability is not ensured via inflation. In con-

trast, in the fiscal regime, a low enough tax rule coefficient, ψ

L

, implies that monetary

policy has to be accommodative via a low enough φ, such that debt is (at least partly)

financed via inflation.

3.1.4 Market Clearing, Aggregation, Resource Constraints

We now discuss market clearing conditions as well as some key aggregate relationships.

20

Labor market clearing conditions are

(

1 − λ

)

L

R

t

=

Z

L

R,t

(

i

)

di, λL

H

(1 + η

ξ

t

) =

Z

L

H,t

(

i

)

di,

while the goods market clearing conditions, imposing law of one price, are

Y

j,t

(

i

)

=

(

1 − λ

)

C

R

j,t

(

i

)

+ λC

H

j,t

(

i

)

=

P

j,t

(

i

)

P

j,t

!

−θ

Y

j,t

,

where Y

j,t

=

(

1 − λ

)

C

R

j,t

+ λC

H

j,t

for j ∈ {R, H}.

Define economy-wide consumption as C

t

=

(

1 − λ

)

C

R

t

+ λC

H

t

. To derive an aggre-

gate resource constraint, we combine households’ budget constraints, government bud-

get constraint, and goods market clearing condition to obtain

C

t

= S

R,t

Y

R,t

+ S

H,t

Y

H,t

.

To derive aggregate sectoral outputs, we aggregate firms’ product functions and get

(

1 − λ

)

L

R

t

= Y

R,t

Ξ

R,t

, λL

H

(1 + η

ξ

t

) = Y

H,t

Ξ

H,t

, (3.1)

where Ξ

j,t

for j ∈ {R, H} is price dispersion term given by

Ξ

j,t

=

1 − ω

j

P

∗

j,t

P

j,t

!

−θ

+ ω

j

π

j,t

θ

Ξ

j,t−1

.

3.2 Data and Calibration

Our parameterization strategy is to pick values based on long-run averages or from the

literature for the structural and policy parameters while calibrating the shocks to match

employment and inflation dynamics during the COVID crisis. Table 1 presents our cali-

bration. The data are described in detail in Appendix Section A.

20

All equilibrium conditions are derived in detail in the online appendix.

21

Table 1: Calibration

Value Description Sources

Households

β 0.9932 Time preference 2-month frequency

σ 1.7 Inverse of EIS Del Negro et al. (2015)

ϕ 2.2 Inverse of Frisch elasticity Del Negro et al. (2015)

χ 94.6 Labor supply disutility parameter Steady-state

¯

L

R

= 0.3

λ 0.23 Fraction of HTM households

Employment share of retail,

transportation, leisure/hospitality

α 0.72

Consumption weight

Consumer Expenditure Surveys data

on Ricardian goods

Firms

θ 6.0 Elasticity of substitution across firms Steady-state markup: 20% (Hall, 2018)

ε 0.8

Elasticity of substitution between

Assigned

Ricardian and HTM goods

ω

R

0.833 Calvo parameter for Ricardian sector Del Negro et al. (2015)

ω

H

0.0 Calvo parameter for HTM sector Assigned

Government

¯

b

¯

Y

0.509 Steady-state debt to GDP Data (1990Q1–2020Q1)

¯

T

L

¯

Y

0.122 Steady-state labor tax revenue to GDP Data (1990Q1–2020Q1)

¯

s

¯

Y

0.127 Steady-state transfers to GDP Data (1990Q1–2020Q1)

Monetary and Fiscal Policy Rules

φ (1.3, 0.0) Interest rate response to inflation Del Negro et al. (2015)

ψ

L

(0.6, 0.0) Labor tax rate response to debt Assigned

Shocks

η

H

t

(-17%, -19%, -13%) Size of HTM labor supply shock

Total hours for retail,

transportation, leisure/hospitality

η

ξ

t

(-41%, -42%, -17%) Size of preference shock

Total hours excluding retail,

transportation, leisure/hospitality

ζ

H,t

(-21%, -16%, 4.7%) Size of HTM sector demand shock

PCE Inflation for recreation,

transportation, food services

s

t

26.8% Size of transfer distribution 2020 CARES Act

Notes: This table shows model parameter values we use for our baseline model simulation. See Section 3.2 for details.

Our benchmark model is calibrated at a two-month frequency with a time discount

factor of β = 0.9932. We set the inverse of the Frisch elasticity (ϕ) to be 2.2 and the inverse

of the elasticity of intertemporal substitution (σ) to be 1.7, which are the estimates in Del

Negro, Giannoni and Schorfheide (2015). We set the elasticity of substitution across firms

to be six (θ = 6), which corresponds to a recent estimate of average markup of 20 percent

(Hall, 2018). We assume that the Ricardian and HTM goods are complements by setting

the elasticity (e ) as 0.8, which is broadly consistent with the estimates in Hobijn and Ne-

chio (2018).

21

We assume flexible prices in the HTM sector for simplicity, while we set

21

Hobijn and Nechio (2018) estimate the elasticity to be 1 at a level of aggregation that distinguishes

22

the Calvo parameter for the Ricardian sector to be 0.833, which implies a 12-month dura-

tion of price changes, consistent with estimates in Del Negro, Giannoni and Schorfheide

(2015). Finally, the steady-state gross inflation is 1.

We set the fraction of HTM households (λ) to be 0.23, based on employment share of

retail trade, transportation and warehousing, and leisure and hospitality sectors in the

U.S. Bureau of Labor Statistics (BLS). We use the 2019 Consumer Expenditure Surveys

(CEX) data to calibrate α, the share parameters in the consumption baskets. We assume

households in the top 80 percentile of the income distribution as Ricardian households

and set 1 − α as 0.28 to match their consumption share for transportation, entertainment,

and food away from home.

22

For the steady-state of fiscal variables, we use federal debts, federal receipts, and gov-

ernment current transfer payments data from 1990:Q1 through 2020:Q1. We set the Taylor

rule parameter under the monetary regime to be 1.3, as estimated in Del Negro, Giannoni

and Schorfheide (2015). We set the tax rule parameter (ψ

L

) to be 0.6 under the monetary

regime, and we perform a sensitivity analysis later. We assume both the Taylor rule (φ)

and tax rule parameters (ψ

L

) to be zero under the fiscal regime, which is the parameteri-

zation often used in the literature.

To examine the dynamic effects of transfer policy, we calibrate the size of transfer

distribution using the transfer amounts specified in the CARES Act, which came into

operation in mid-April. In particular, we target the sum of three key components of the

Act: $293 billion to provide one-time tax rebates to individuals; (ii) $268 billion to expand

unemployment benefits; and (iii) $150 billion in transfers to state and local governments.

These three components of the CARES Act consist of around 3.4 percent of GDP. Given

our calibration of steady-state government transfers, this in turn amounts to an increase

in transfers of 26.8 percent.

23

In our baseline exercise of transfer policy, we assume that

the total amount of transfer is equally distributed over six months—that is, three periods.

A key component of our calibration is how we choose the shock sizes. The size of

the three shocks (η

H

t

, η

ξ

t

, ξ

H,t

) are estimated to match the dynamics, under the monetary

regime without transfer policy, of total hours for both the HTM and Ricardian sectors

and inflation for the HTM sector, as given in our motivating Figure 1. In our baseline

calibration, we assume that the three shocks in the model are over after three periods.

across 10 categories of goods and services. Since we only have two sectors in the model, we set an elasticity

slightly below 1 as the baseline. Then, in a sensitivity analysis, we do an alternate calibration of 1.2.

22

This value of α is the same if we assume households in the bottom 20 percentile of the income distribu-

tion as HTM households and target their consumption share for these sectors. For this reason, we modeled

the same consumption basket for the two households.

23

In a sensitivity analysis we drop the tax rebate component of the CARES Act while calibrating the

transfer increase.

23

In particular, we set the size of HTM sector labor supply shocks to match BLS total

hours changes from April through August in HTM sectors (retail trade, transportation

and warehousing, and leisure and hospitality sectors). We then calibrate the size of the

preference shocks to match BLS total hours changes for sectors excluding HTM sectors,

also from April through August. Finally, we set the size of HTM sector-specific demand

shocks to match the PCE inflation for recreation, transportation, and food services sectors

from the U.S. Bureau of Economic Analysis. The three shocks series can perfectly match

the dynamics of total hours and inflation from April through August, as reported in detail

in Panel A of Appendix Table B.1.

24

Moreover, Panel B of Table B.1 shows that our calibration is also reasonable at match-

ing several non-targeted moments. For example, our model-implied dynamics of aggre-

gate output is quite close to the data, even though we did not use any output data in our

calibration. Moreover, model dynamics of consumption in the HTM sector is also fairly

close to the dynamics of the real PCE data, even though our calibration only targets the

dynamics of PCE inflation for the HTM sector.

3.3 Quantitative Results

We now present quantitative results on positive and normative implications of redistri-

bution policy during a crisis.

3.3.1 Dynamic Effects of Transfer Policy

We show how key variables evolve over time in response to the COVID shocks—a com-

bination of aggregate and sector-specific demand and supply shocks as discussed above.

We then illustrate the effects of an increase in transfers for the two regimes. These re-

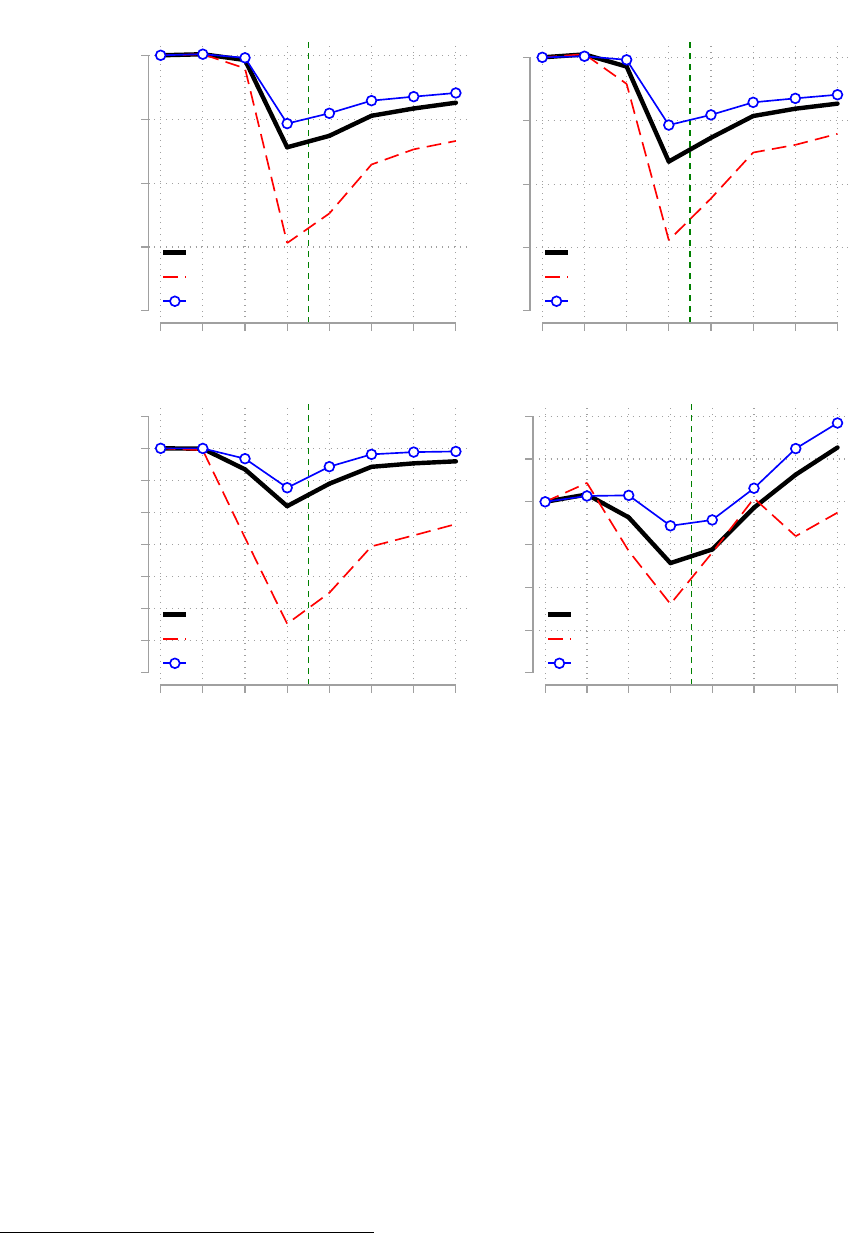

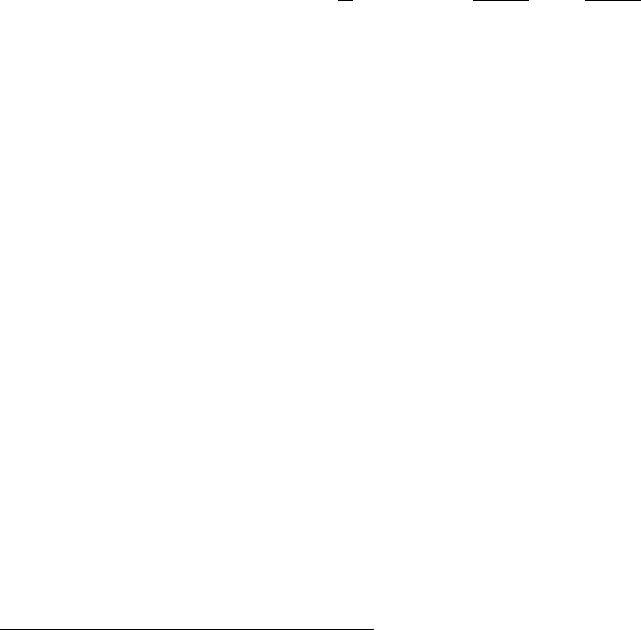

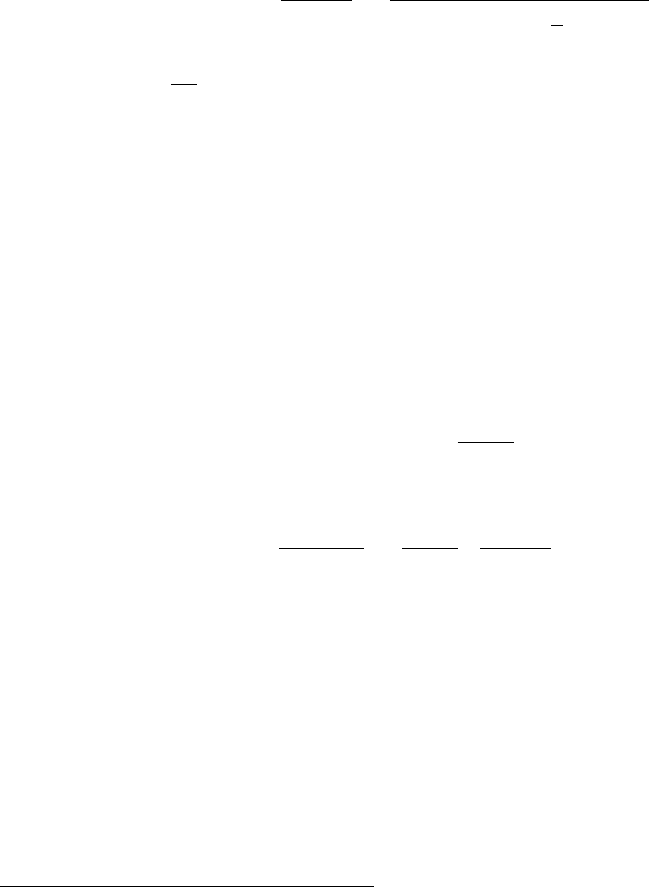

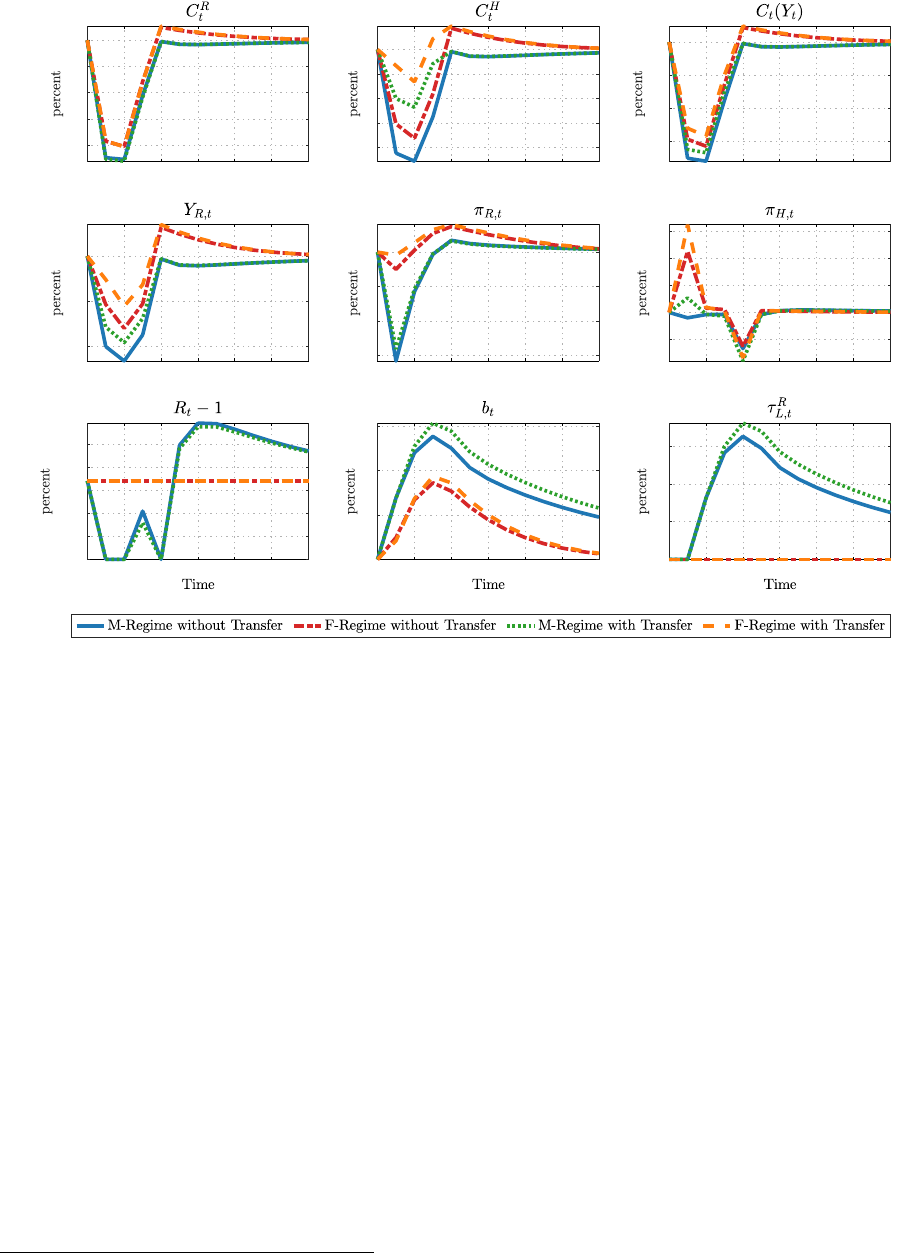

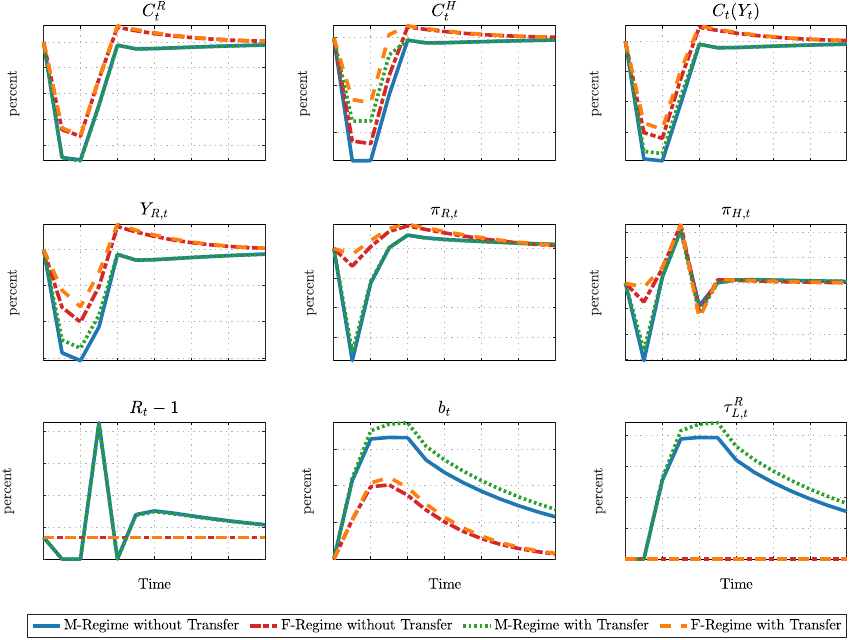

sults are in Figure 2, which presents four different scenarios: the monetary regime with

and without transfers to the HTM households and the fiscal regime with and without

transfers. As mentioned before, we calibrate the COVID shocks to match the targeted

moments under the monetary regime in the absence of transfers. This case thus serves as

our baseline. Throughout, the duration of the redistribution policy is three periods (six

months), which coincides with the duration of the shocks.

25

24

Since the transfer payments from the CARES Act started in mid-April while our calibration strategy

matches model dynamics without transfer policy to the data, there is a slight mismatch between the data

and model counterparts, especially for August.

25

We solve the model non-linearly under perfect foresight. All the model variables converge back to the

steady state in the long run.

24

0 2 4 6 8 10 12

-20

-15

-10

-5

0

0 2 4 6 8 10 12

-8

-6

-4

-2

0

0 2 4 6 8 10 12

-15

-10

-5

0

0 2 4 6 8 10 12

-10

-5

0

0 2 4 6 8 10 12

-6

-4

-2

0

0 2 4 6 8 10 12

-5

0

5

10

15

0 2 4 6 8 10 12

0

0.002

0.004

0.006

0.008

0.01

0 2 4 6 8 10 12

0

10

20

30

0 2 4 6 8 10 12

0

5

10

15

Figure 2: Redistribution Policy with Different Policy Regimes

Notes: This figure shows dynamics of key variables in response to the COVID shocks under different

regimes. Blue solid lines represent the baseline case: the monetary regime without transfers. Red dashed

lines, green dotted lines, and orange dashed lines represent respectively the fiscal regime without trans-

fers, the monetary regime with transfers, and the fiscal regime with transfers.

In the baseline, where the policymakers just stick to the usual policy, the COVID

shocks generate significant short-run contractions in aggregate output and household

consumption of both types, as shown by the solid blue lines in the first row of the fig-

ure. The contraction leads to a decline in inflation (as shown in the second row) and

in labor tax revenues, both of which in turn increase the real value of government debt.

The government responds by increasing the tax rate to stabilize debt under this standard

monetary regime. Meanwhile, the central bank decreases the nominal interest rate in re-

sponse to the decline in inflation. These policy responses are shown in the bottom row of

the figure. Notice that the ZLB binds in our model during the pandemic.

Now, let us introduce the redistribution program to the monetary regime baseline

case, the results of which are shown by the dotted green lines in Figure 2.

26

Overall, the

26

As we discussed in the calibration section, transfers increase by 26.8 percent in total, and here, they are

25

effects of the redistribution program are largely in line with what we have shown using

the simple model in Section 2. One major difference from the simple model is that the

redistribution program is more expansionary here because both the classical labor supply

channel and the Keynesian channel operate thanks to nominal rigidities, as we discussed

in Section 2.3.

Clearly, transfers increase HTM household consumption and decrease Ricardian house-

hold consumption (due to the resulting increase in the tax rate) relative to the baseline.

These are the direct effects of the redistribution. As discussed in Section 2, however, the

redistribution program is inflationary, as shown by the difference between the solid blue

lines and the dotted green lines in the second row. This indirectly has a positive effect on

household consumption of both types through general equilibrium. In particular, the de-

cline of Ricardian household consumption caused by the redistribution is very small, and

in fact in this parameterization it is nearly indistinguishable visually from the baseline

case.

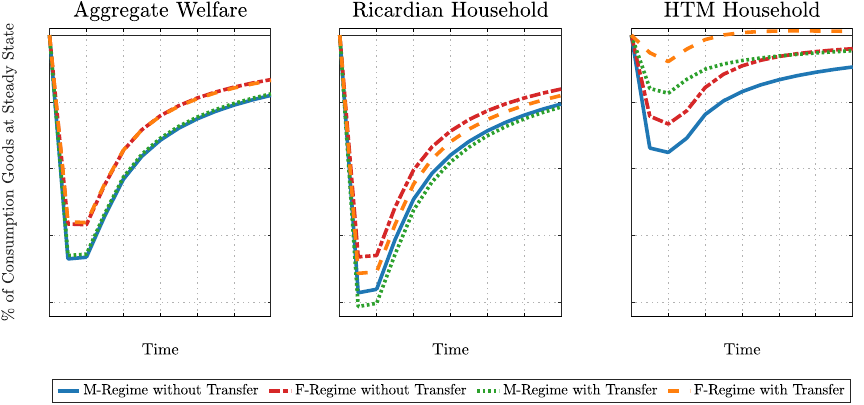

Let us now turn to the fiscal regime where neither the tax rate nor the nominal inter-