STATE OF NEVADA

LEGISLATIVE COUNSEL BUREAU

LEGISLATIVE COMMISSION (775) 684-6800

RANDOLPH J. TOWNSEND, Senator, Chairman

Lorne J. Malkiewich, Director, Secretary

LEGISLATIVE BUILDING

401 S, CARSON STREET

CARSON CITY, NEVADA 89701-4747

Fax No.: (775) 684-6600

LORNE J. MALKIEWICH, Director

(775) 684-6800

INTERIM FINANCE COMMITTEE (775) 684-6821

MORSE ARBERRY, JR., Assemblyman, Chairman

Mark W. Stevens, Fiscal Analyst

Gary L. Ghiggeri. Fiscal Analyst

PAUL V. TOWNSEND, Legislative Auditor (775) 684-6815

DONALD O. WILLIAMS, Research Director (775) 684-6825

BRENDA J. ERDOES, Legislative Counsel (775) 684-6830

Legislative Commission

Legislative Building

Carson City, Nevada

We have completed an audit of the Washoe County School District. This audit

was required by Chapter 5, Statutes of Nevada 2003, 20th Special Session. The

purpose of legislative audits is to improve government by providing the Legislature,

state and local officials, and Nevada citizens with independent and reliable information

about the operations of government agencies, programs, activities, and functions. The

results of our audit, including findings, conclusions, recommendations, and the District's

response, are presented in this report.

We wish to express our appreciation to the management and staff of the Washoe

County School District for their assistance during the audit.

Respectfully presented,

Paul V. Townsend, CPA

Legislative Auditor

September 3, 2004

Carson City, Nevada

(NSPO Rev. 1-04)

(OJ 1578E

STATE OF NEVADA

WASHOE COUNTY SCHOOL DISTRICT

AUDIT REPORT

Table of Contents

Page

Executive Summary ................................................................................................ 1

Introduction ............................................................................................................. 10

Background......................................................................................................... 10

General......................................................................................................... 10

Student Enrollment....................................................................................... 11

Expenditures and Staffing ............................................................................ 11

Sources of Funding ...................................................................................... 13

Scope and Objectives ......................................................................................... 15

Findings and Recommendations............................................................................. 17

Financial Management........................................................................................ 17

Federal Revenues From Medicaid Can Be Increased.................................. 17

Food Service Program Does Not Include All Revenues or Costs................. 20

Sufficient Controls Exist Over Legislative Funding ....................................... 25

Facilities Management ........................................................................................ 27

District’s Process for Cleaning Saves Money ............................................... 28

Construction Management Policies and Procedures Need Updating ........... 29

Capital Projects Planning Could Be Strengthened ....................................... 30

Improvements Needed in Energy Conservation Program ............................ 30

Maintenance and Housekeeping Lack Complete Policies and

Procedures...............................................................................................33

Personnel Management ...................................................................................... 35

Personnel Program Accomplishments.......................................................... 35

Improvements Needed in Planning and Evaluating Recruitment Efforts ...... 36

STATE OF NEVADA

WASHOE COUNTY SCHOOL DISTRICT

AUDIT REPORT

Table of Contents

(continued)

Page

Better Management Data Needed................................................................ 37

Position Control Could Be Improved............................................................. 38

Clearly Defined and Structured Training Program Is Needed....................... 38

Transportation..................................................................................................... 40

Bus Routing Could Increase Efficiency......................................................... 41

Bus Replacement Policy Needed ................................................................. 44

Vehicle Operating Information Not Available ................................................ 47

Fuel Usage Controls Could Be Improved ..................................................... 49

District Organization............................................................................................ 51

Staffing and Administrative Costs Per Pupil Were Reasonable.................... 51

Dollars to the Classroom Favorable ............................................................. 53

Opportunities for Better Governance............................................................ 54

Operating Oversight Could Be Strengthened ............................................... 55

Organizational Changes............................................................................... 58

Employee Health Plans....................................................................................... 59

Health Plans Have Reasonable Oversight ................................................... 59

Appendices

A. Audit Methodology........................................................................................ 61

B. Washoe County School District Personnel Survey....................................... 66

C. Survey of Exiting Teachers........................................................................... 86

D. Response From Washoe County School District.......................................... 89

1

LA04-19

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

Background

Washoe County School District (WCSD) is the second

largest school district in the State and, according to the

National Center for Education Statistics, the 65

th

largest

district in the country for fiscal year 2003. For fiscal year

2004, the WCSD operated 91 schools, excluding charter

schools. This includes 3 schools in Gerlach/Empire, 1 in

Wadsworth, 3 in Incline Village, and 84 in the Reno/Sparks

area. There are 61 elementary schools, 14 middle schools,

12 high schools, and a special education school. In addition,

the District operates Washoe High School (alternative high

school), Truckee Meadows Community College High School,

and the Regional Technical Institute.

Washoe County School District’s mission is to provide

each student the opportunity to achieve his or her potential

through a superior education in a safe and challenging

environment in order to develop responsible and productive

citizens for a diverse and rapidly changing community. A

seven-member Board of Trustees governs the District by

establishing District policies and employing the

superintendent to serve as the chief executive officer in

charge of day-to-day operations. Five board members

represent specific geographic areas and two other members

are elected at-large for 4-year terms.

Washoe County School District has experienced

moderate growth during the past 5 years. In that time, the

District’s student enrollment increased 12% to 58,903 in

fiscal year 2003. During the same period, the District’s

instructional staff increased 8% to 3,617. According to the

Nevada Department of Education’s (NDOE) NRS 387.303

report, the District had over 5,300 full-time equivalent (FTE)

positions in fiscal year 2003. The NDOE report does not

include over 1,000 employees that are paid from accounts

not reported to the State, such as nutrition services, federal

programs, and hourly/daily labor. In addition, the District had

over 1,600 substitute teachers.

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

The District received funding from two major sources:

the State Distributive School Account (DSA) and local

sources. The District’s basic support guarantees for fiscal

years 2004 and 2005 from the DSA are $4,161 and $4,301

per student, respectively. In addition, the District receives

state support for such areas as special education, class-size

reduction, adult diploma education, regional professional

development program, and remedial education. During

fiscal year 2003, the District had revenues of about $401.9

million excluding capital projects and the bond accounts.

Local revenues accounted for 63% of revenues, with state

sources accounting for a little over 29%.

Washoe County School District had expenditures of

about $393 million in fiscal year 2003, excluding capital

outlays and bond accounts. About 58% of these

expenditures were for regular, vocational, special, and other

instructional programs, while about 7% went for admin-

istration.

Purpose

This audit was required by Chapter 5, Statutes of

Nevada 2003, 20

th

Special Session, and was conducted

pursuant to the provisions of NRS 218.737 to 218.890. This

audit included a review of the District’s activities from July 1,

2002 through December 31, 2003. The purpose of the audit

was to evaluate the District’s operations in these six areas:

• Financial Management – Are there sufficient controls

to provide accountability for financial resources?

• Facilities Management – Are construction, main-

tenance, and facility usage programs properly

planned and controlled?

• Personnel Management – Are recruitment and

retention efforts adequate to ensure qualified staff?

2 LA04-19

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

• Transportation – Are student transportation

programs adequately planned to ensure the safe and

efficient transportation of students?

• District Organization – Does the organizational

structure enhance the effectiveness and efficiency of

Board governance and District management?

• Employee Health Plans – Is the health plan

appropriately managed?

Results in Brief

The District’s financial and administrative operations

compare favorably to other states’ best practices and peer

districts. Further, the District’s administrative staffing ratios

and costs appear reasonable when compared to other

districts’ averages, and the District has done a good job in

getting more of every dollar spent into the classroom.

Despite these efforts, we identified some opportunities for

cost savings and increased revenues of about $3.6 million

annually. These opportunities exist because Medicaid

reimbursements are not maximized, food service operations

could collect more fees, and bus routing could be more

efficient. Additional opportunities exist for savings by

implementing an energy management plan, better analyzing

energy retrofitting contracts, and monitoring vehicle

operating information.

The District can also improve its accountability by

increasing planning efforts and compiling operational data to

manage its personnel resources more effectively. Further,

accountability and governance enhancements could occur

by continuing to develop a capital improvement plan and

expanding the focus of the internal audit section.

Developing complete policies and procedures and

periodically reviewing them in accordance with Board policy

would also strengthen the District’s governance.

3 LA04-19

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

Principal Findings

• The District is not collecting all available Medicaid

funding. For example, the District collected

substantially less per student than Clark County

School District in the last 3 years and did not seek

reimbursement for outreach activities until April 2004.

With improved oversight of the Medicaid

reimbursement process, WCSD could realize about

$2 million annually in additional federal revenues.

(page 17)

• Opportunities exist for improving the food service

program that would reduce the burden on the General

Fund. The District could collect about $300,000

annually by charging a small fee to students that

qualify for reduced-price meals. Fourteen of the 17

Nevada school districts and 2 of 3 peer districts

surveyed charge eligible students for reduced-price

meals. One peer district indicated their Board policy

is to not charge for these meals. Washoe County

School District officials stated the Board of Trustees

made the decision not to charge for reduced-price

meals over 10 to 15 years ago. However,

documentation to support the Board’s decision was

not provided. We recognize the sensitivity of this

issue, but believe the Board needs to formally decide

whether to continue the current practice of not

charging for reduced-price meals. (page 21)

• In fiscal year 2002, the Plant Facilities Department

developed a process for cleaning District buildings

that District records indicate saved over $600,000

annually. The concept is known as Process Cleaning

and recently received the Cashman Good

Government Award. (page 28)

• Although the District’s construction and bond

transactions are well documented, the policies and

procedures governing this area could be improved to

4 LA04-19

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

ensure good business practices are followed. For

example, construction management does not have

procedures addressing allowable construction costs,

use of bond funds, and project management. In

addition, change order review and authorization

procedures have not been formally developed and the

Plant Facilities Department lacks procedures to

ensure it is awarded reimbursements from utility and

road construction. (page 29)

• The District has made some efforts to be energy

conscious, but more work needs to be done.

Specifically, the District can improve its planning to

achieve greater energy conservation. In addition,

some energy conservation agreements were not

competitively bid and some did not accomplish

significant energy savings. (page 30)

• The WCSD has developed programs to improve

recruitment and retention of employees. For

example, WCSD is in the process of implementing an

online application system. This system should

streamline the process and enable better tracking of

recruiting efforts. In addition, the District has taken

action to identify why teachers leave the District.

(page 35)

• The Human Resources Division would benefit from a

formal recruitment and retention plan. Prior audit,

consultant, and internal reports advised the Division

to develop a recruitment and retention plan. In 1999,

it drafted a document containing the components of a

recruitment plan. However, the plan was not

completed. A plan is important because the District

faces recruitment challenges when having to hire 400

to 500 new teachers each year. (page 36)

• The District does not currently compile data on the

results of its recruitment efforts. Monitoring results of

efforts would allow the District to more efficiently

utilize its scarce resources. For example, with the

historical data the District could evaluate the results of

5 LA04-19

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

various job fairs, and then eliminate those non-

producing recruiting locations. (page 37)

• The District’s human resources information system

does not provide basic data needed by personnel

managers to effectively manage operations. The

information system cannot provide accurate position

counts, calculate turnover rates without significant

effort, and produce vacancy reports. (page 37)

• The District needs to implement a better district-wide

position control system. A position control system

acts as a budgetary control, helping to ensure

personnel expenditures do not exceed budgets.

Accurate position information is also essential for

budget preparation, trend analysis, and workforce

forecasting. (page 38)

• The District does not have a comprehensive plan

regarding district-wide training goals and objectives.

Prior audit recommendations and studies have

pointed out the need to develop a consolidated

training plan that addresses not just teachers and

administrators but all District staff development.

(page 38)

• Despite positive changes in recent years, the

reporting structure and responsibilities of WCSD’s

training program are still unclear. This past year, the

District reorganized its training program to be in effect

for the 2004-2005 school year. Although this

structure appears to be a good start, it could be more

clearly structured and the responsibilities more clearly

defined. (page 39)

• The Transportation Department can increase

efficiency in bus routing through several best

practices from other states and the student

transportation industry. These best practices include

the use of computerized routing software and

staggered school start times. They could generate

6 LA04-19

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

savings to the District of over $1.3 million annually.

(page 41)

• The District has made some efforts in recent years to

replace buses in a timely manner, but further

improvements are needed. Older buses cost

significantly more to operate and are less likely to

have the latest safety features. Over 60% of the

District’s buses are older than 14 years and have

been driven an average of 270,000 miles. (page 44)

• The Transportation Department does not have vehicle

operating information in a usable format. While fuel

usage for two of the District’s three transportation

facilities has been entered into the new fleet

management system, vehicle maintenance records

have not. This information is in paper files at the

various facilities. In addition, historical information

prior to August 2003 cannot be loaded to the new

database. As such, the Department is unable to

determine and analyze vehicle operating costs.

(page 47)

• In fiscal year 2004, the District purchased over

670,000 gallons of fuel at a cost of over $850,000.

However, the District’s controls over vehicle fuel at its

transportation facilities are not adequate. In addition,

the District does not have the vehicle operating

information to analyze vehicle fuel consumption to

identify variances and fluctuations. (page 49)

• According to the National Center for Educational

Statistics’ latest information for 2003, the District

ranks favorably with its peer districts in administrative

staff and teacher per pupil ratios. For example, there

are 343 students per every administrator and 16

students per teacher. The District’s administrative

costs of $771 per pupil also are reasonable when

compared to others. (page 51)

• The District has done a good job in getting more of

every dollar spent into the classroom. For fiscal year

7 LA04-19

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

2001, WCSD had 61.3 cents of every dollar going into

the classroom, while peer districts averaged 60.1

cents. (page 53)

• Although policies and procedures have been

developed, many date back to 1997 and 1998.

District policy requires the Board to review policies on

a four-year cycle, one-quarter being reviewed

annually. We found the Board reviews policies as

presented by staff for amendment, but found no

evidence of a routine policy review as required.

(page 55)

• The internal auditor spends most of the time auditing

the student activity funds. Although auditing the

activity funds is important, the internal auditor should

expand her review to include district-wide operations.

(page 56)

• The processes used by District staff and others are

reasonable to provide good oversight of the health

plans. Health coverage represents a considerable

cost to the District. As such, oversight by the District

is necessary to ensure its fiduciary responsibility to its

employees and taxpayers. (page 59)

Recommendations

This report contains 29 recommendations to improve

the financial and administrative operations of the Washoe

County School District. The recommendations identify

opportunities to increase revenues, reduce costs, and

improve accountability. Our report contains five

recommendations on financial management, including

procedures to increase federal revenues and improve food

service controls. We also identified six recommendations to

improve the management of the District’s facilities. Six

recommendations were made to help with the recruitment,

retention, and training of personnel. In addition, we made

six recommendations to help operate the Transportation

8 LA04-19

EXECUTIVE SUMMARY

WASHOE COUNTY SCHOOL DISTRICT

Department more efficiently. The report also has five

recommendations concerning the District’s organization to

enhance accountability to the Board and the public. Finally,

we made one recommendation concerning the District’s

employee health plans. (page 102)

Washoe County School District Response

The School District, in its response to our report,

accepted all 29 recommendations. (page 89)

9 LA04-19

10

LA04-19

Introduction

Background

Throughout the nation, school districts are facing many challenges relating to

education delivery. Other states, including Florida, Texas, and Arizona, have

addressed these concerns through audits designed to promote efficiency. During the

2001 Legislative Session, AB 672 directed the Legislative Auditor to conduct a

preliminary performance audit survey of the Clark and Washoe County School Districts.

The purpose of the survey was to identify potential audit issues in these districts. As a

result of the survey, the 2003 Legislature, during the 20

th

Special Session, directed the

Legislative Auditor to conduct a performance audit of Washoe County School District.

General

Washoe County School District (WCSD) is the second largest school district in

the State. According to the National Center for Education Statistics, it was the 65

th

largest district in the country for fiscal year 2003. For fiscal year 2004, the District

operated 91 schools, excluding charter schools. This includes 84 schools in the

Reno/Sparks area, 3 in Incline Village, 3 in Gerlach/Empire, and 1 in Wadsworth. There

are 61 elementary schools, 14 middle schools, 12 high schools, and a special education

school. In addition, the District operates Washoe High School (an alternative high

school), Truckee Meadows Community College High School, and the Regional

Technical Institute.

The District’s mission is to provide each student the opportunity to achieve his or

her potential through a superior education in a safe and challenging environment in

order to develop responsible and productive citizens for a diverse and rapidly changing

community. A seven-member Board of Trustees governs the District by establishing

District policies and employing the superintendent to serve as the chief executive officer

in charge of daily operations. Five board members represent specific geographic areas

and two other members are elected at-large for 4-year terms.

Over the last 2 years, 15 of the 21 schools in Nevada that were recognized by

the Nevada Department of Education for outstanding student academic performance

11

LA04-19

were in WCSD. In addition, all three exemplary schools recognized in fiscal year 2003

by the Department were in WCSD. Further, the U.S. Department of Education

recognized seven other schools in the District as “Blue Ribbon Schools”. Finally, a

national publication recently recognized five of the District’s high schools as being

among the best public high schools in the nation at preparing students for college.

Student Enrollment

Washoe County School District has experienced moderate growth in student

enrollment during the past 5 years. The District’s student enrollment increased 12%

from fiscal year 1999 to 2003. Exhibit 1 shows student enrollment for WCSD for the last

5 years, as determined in September of the fiscal year.

Exhibit 1

Student Enrollment

Fiscal Years 1999-2003

1999

2000

2001

2002

2003

1999-2003

52,641 54,053 55,651 57,583 58,903 12%

Source: Nevada Department of Education, NRS 387.303 Reports.

Expenditures and Staffing

WCSD had expenditures of about $393 million in fiscal year 2003, excluding

capital outlays and the bond accounts. About 58% of these expenditures were for

regular, vocational, special, and other instructional programs, while about 7% went for

administration. Exhibit 2 shows the District’s expenditures for fiscal year 2003.

12 LA04-19

Exhibit 2

Expenditures (Millions)

Fiscal Year 2003

Operation and

Maintenance

$33.2

(8%)

Student

Transportation

$12.6

(3%)

Food Service

Operations

$13.5

(3%)

Debt Service

$39.2

(10%)

General and

School

Administration

$25.8

(7%)

Student and

Instructional

Support

$33.6

(9%)

Other Support

and Community

Service

$9.5

(2)

(2%)

Program Instruction

$225.6

(1)

(58%)

Source: Washoe County School District Comprehensive Annual Financial Report, Fiscal

Year 2003.

Note: Exhibit excludes capital outlays and bond accounts.

(1)

Includes regular, special, vocational, adult, and other instructional programs.

(2)

Includes business and central services support, other support, and community service.

According to the Nevada Department of Education’s (NDOE) NRS 387.303

report, the District had over 5,300 full-time equivalent (FTE) positions in fiscal year

2003. The NDOE report does not include over 1,000 employees that are paid from

accounts not reported to the State, such as nutrition services, federal programs and

hourly/daily labor. In addition, the District had over 1,600 substitute teachers. Teachers

represent almost 70% of the District’s staff and have increased about 8% from fiscal

year 1999 to 2003. Exhibit 3 shows a breakdown of employees by function as reported

to NDOE for fiscal year 2003, and exhibit 4 shows the instructional staff growth from

fiscal year 1999 to 2003.

13 LA04-19

Exhibit 3

FTE Employees by Function

Fiscal Year 2003

Function

Instructional Staff 3,617 67%

Instructional Support Staff 440 8

Administrative Staff 427 8

Other Staff 882 17

Total

5,366 100%

% of TotalNumber

Source: Nevada Department of Education, NRS 387.303 Report.

Exhibit 4

Instructional Staff

Fiscal Years 1999 - 2003

1999

2000

2001

2002

2003

1999-2003

3,349 3,356 3,436 3,584 3,617 8%

Source: Nevada Department of Education, NRS 387.303 Reports.

Sources of Funding

School districts receive funding from two major sources: the State Distributive

School Account (DSA) and local sources. Local sources provide the largest share of

school district revenue. These include the Ad Valorem Property Tax, Local School

Support Tax, Government Services Tax, and other sources. In addition, school districts

receive revenues for specific purposes, such as class-size reduction, special education,

and adult diploma education. The 2003 Legislature approved statewide appropriations

to the DSA of $1.63 billion for the 2003-2005 biennium. This is a $325 million increase,

or about 25%, over the previous biennium.

The Nevada Plan is the means used to finance elementary and secondary

education in the State’s public schools. A basic level of financial support is guaranteed

to each school district by the State through this Plan. The goal of the Nevada Plan is to

14

LA04-19

ensure adequate educational opportunity for all students regardless of the wealth of the

school district. The state’s share of the Nevada Plan’s funding is distributed through the

DSA. The amount of state aid received by each district is developed by a formula that

allows for differences in costs and local wealth. As such, the basic support is adjusted

for each district based on economic and geographic characteristics and a wealth

adjustment. This results in districts with fewer resources getting a higher per-pupil

allocation of state money than districts with more resources.

WCSD’s basic support guarantees for fiscal years 2004 and 2005 from the DSA

are $4,161 and $4,301 per student, respectively. In addition, the District receives state

support for such areas as special education, class-size reduction, adult diploma

education, regional professional development program, and remedial education. The

District received about $36.5 million in fiscal year 2003 for these programs.

During fiscal year 2003, Washoe County School District had revenues of about

$401.9 million, excluding capital projects and the bond accounts. Local revenues

accounted for 63% of the District’s revenue, with state sources accounting for a little

over 29%. Exhibit 5 shows the District’s revenue sources between local, state, and

federal sources.

15 LA04-19

Exhibit 5

Revenue Sources and Amounts (Millions)

Fiscal Year 2003

Government

Service Tax

$11.3

(2.8%)

Local Food

Service

$6.2

(1.5%)

Local School

Support Tax

$117.0

(29.1%)

Other Local

Sources

$7.1

(1.8%)

Federal

$31.0

(7.7%)

State

$117.8

(29.3%)

Other

$1.3

(.3%)

Property Taxes

$110.2

(27.5%)

Source: Washoe County School District Comprehensive Annual Financial Report,

Fiscal Year 2003.

Note: Exhibit excludes capital projects and bond accounts.

Scope and Objectives

This audit was required by Chapter 5, Statutes of Nevada 2003, 20

th

Special

Session, and was conducted pursuant to the provisions of NRS 218.737 to 218.890.

The Legislative Auditor conducts audits as part of the Legislature’s oversight

responsibility for public programs. The purpose of legislative audits is to improve

government by providing the Legislature, state and local officials, and Nevada citizens

with independent and reliable information about the operations of government agencies,

programs, activities, and functions.

This audit included a review of the District’s activities from July 1, 2002, through

December 31, 2003. The objectives of the audit were to evaluate the District’s

operations in these six areas:

• Financial Management – Are there sufficient controls to provide accountability

for financial resources?

16

LA04-19

• Facilities Management – Are construction, maintenance, and facility usage

programs properly planned and controlled?

• Personnel Management – Are recruitment and retention efforts adequate to

ensure qualified staff?

• Transportation – Are student transportation programs adequately planned to

ensure the safe and efficient transportation of students?

• District Organization – Does the organizational structure enhance the

effectiveness and efficiency of Board governance and District management?

• Employee Health Plans – Is the health plan appropriately managed?

17

LA04-19

Findings and Recommendations

The District’s financial and administrative operations compare favorably to other

states’ best practices and peer districts. Further, the District’s administrative staffing

ratios and costs appear reasonable when compared to other districts’ averages, and the

District has done a good job in getting more of every dollar spent into the classroom.

Despite these efforts, we identified some opportunities for cost savings and increased

revenues of about $3.6 million annually. These opportunities exist because Medicaid

reimbursements are not maximized, food service operations could collect more fees,

and bus routing could be more efficient. Additional opportunities exist for savings by

implementing an energy management plan, better analyzing energy retrofitting

contracts, and monitoring vehicle operating information.

The District can also improve its accountability by increasing planning efforts and

compiling operational data to manage its personnel resources more effectively. Further,

accountability and governance enhancements could occur by continuing to develop a

capital improvement plan and expanding the focus of the internal audit section.

Developing complete policies and procedures and periodically reviewing them in

accordance with Board policy would also strengthen the District’s governance.

Financial Management

We found that financial management practices were generally sound. However,

there are opportunities to increase revenues and improve accountability. For example,

the District could increase collections from Medicaid about $2 million annually by

ensuring all Medicaid reimbursements are billed and received. In addition, the food

service program could collect an additional $300,000 annually by charging for reduced-

price meals, and should account for all its costs.

Federal Revenues From Medicaid Can Be Increased

Washoe County School District (WCSD) is not collecting all available Medicaid

funding. WCSD has collected substantially less per student from Medicaid than Clark

18 LA04-19

County School District (CCSD) in the last 3 years. In addition, WCSD did not seek

reimbursement for Medicaid outreach activities until April 2004, 3 years after CCSD first

sought reimbursement. With improved oversight of the Medicaid reimbursement

process, WCSD could realize about $2 million annually in additional federal revenues.

Furthermore, the District should explore with State Medicaid personnel the opportunity

of obtaining reimbursement for unbilled services previously provided. Medicaid

generally permits retroactive billing for 2 years.

The Medicaid Program allows school districts to enroll as providers of Medicaid

services for school-based, health services provided to disabled students. These

services are referred to as Direct Services. Typical services include speech therapy,

physical therapy, and psychological counseling. Individual claims are submitted to

Medicaid for services provided to eligible students, with the assistance of an

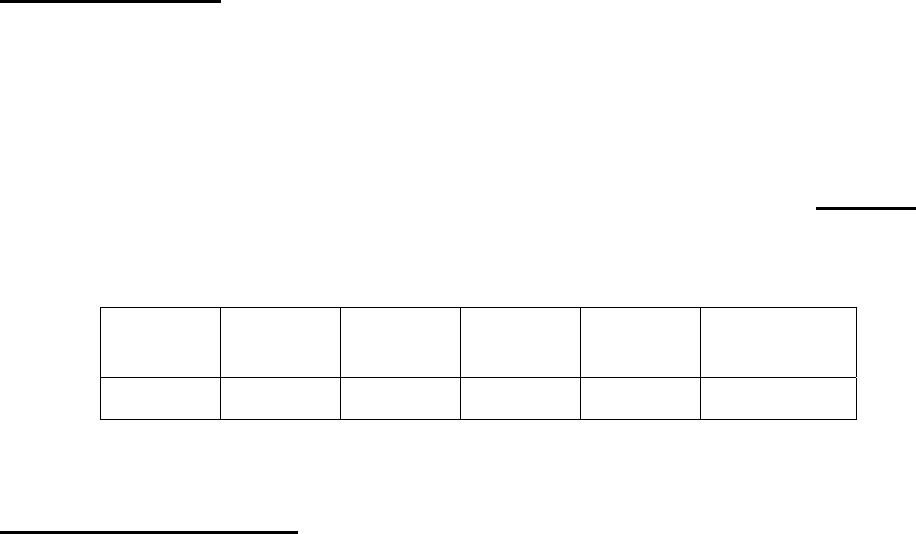

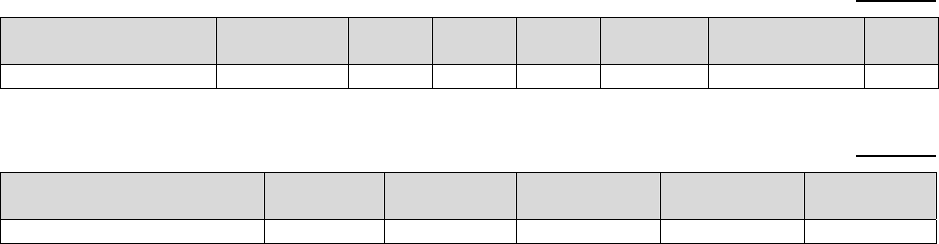

independent contractor. CCSD collected five times the amount WCSD did on a per

pupil basis for Direct Services over the past three fiscal years. Exhibit 6 shows the

amounts per pupil received by WCSD and CCSD from Medicaid for Direct Services

from fiscal years 2001 to 2003.

Exhibit 6

Medicaid Revenues Per Pupil

Direct Services

Fiscal Years 2001 to 2003

2001 2002 2003

A

vg.

WCSD

0.86$ 3.24$ 5.08$ 3.10$

CCSD

10.24$ 18.48$ 20.24$ 16.48$

Source: Auditor calculations based on WCSD and

CCSD accounting records and NRS 387.303

reports.

Note: The average column is based on the total direct

services provided per pupil for fiscal years 2001 to

2003, not on the average of the yearly amounts

shown in the exhibit.

Medicaid also reimburses school districts for medical outreach activities provided

to students and their families. This is referred to as Administrative Claiming. A

quarterly claim to Medicaid is generated following a time sampling of staff activities.

Reimbursable activities include:

19

LA04-19

• referral of students/families for Medicaid eligibility determinations

• provision of health care information and interagency coordination of

medical services

• referral, coordination, and monitoring of health services

However, WCSD did not seek reimbursement for Administrative Claiming activities until

April 2004, while CCSD began its administrative claiming process in April 2001. CCSD

collected over $7.7 million in fiscal years 2002 and 2003 from Medicaid for

Administrative Claiming.

Based on the amount received per pupil by CCSD in fiscal year 2003, we

estimate WCSD could be collecting about $2 million annually in additional revenue from

Medicaid. In addition to assisting school districts in meeting the costs of providing

health-related services, student health can be improved through increased student and

family awareness of available community services.

The District has not provided adequate fiscal oversight of the Medicaid

reimbursement process for medical services provided to eligible students. Specifically,

one WCSD staff person and the independent contractor largely perform the

reimbursement process with little oversight. WCSD fiscal managers indicated they were

not involved in the Medicaid process, leaving oversight to special education program

managers. However, discussions with program managers also found a lack of

involvement with the reimbursement process. As stated by the contractor’s

representative, WCSD has not placed a high priority on Medicaid reimbursements and

the clerical staff involved has no authority to require program staff to submit service

records and other information needed to bill Medicaid. The representative agreed that

WCSD’s process needed more management oversight.

In addition, we identified several weaknesses with the District’s process for billing

Medicaid. For example:

• WCSD has very few written policies and procedures on the process.

• There is very little oversight of the staff person involved with the process.

• Staff is not monitoring the independent contractor’s process for Medicaid

billings and payments.

20

LA04-19

Good internal controls are important in any organization to ensure management’s

directives are carried out. Controls are an integral part of an organization’s

accountability of government resources and achieving effective results. As shown,

because of limited controls over the Medicaid process, the District has not received its

fair share of federal Medicaid funding.

Additional opportunities exist to increase federal reimbursement when the State

Medicaid Plan is amended. Transportation services provided to eligible students that

need specially equipped vehicles are reimbursable Medicaid expenses. However, the

federal regulations regarding transportation expenses were revised, requiring more

detailed documentation in order to receive reimbursement. As such, until the State

Medicaid agency develops the methodology for claiming special needs transportation

services, school districts cannot get reimbursed. The State has committed to the

districts that the State Plan amendment will be effective January 2005. Once the State

Plan is amended, the District needs to incorporate the requirements into the Medicaid

process and begin collecting for eligible transportation services. Reimbursement for

transportation services may be substantial. Prior to the federal regulation being revised

and reimbursements being stopped to the districts, CCSD collected about $800,000

during calendar year 2001. Therefore, it is important a process is in place to ensure the

District receives reimbursement from Medicaid for eligible transportation services.

Food Service Program Does Not Include All Revenues or Costs

Opportunities exist for improving the food service program that would reduce the

burden on the General Fund, resulting in more money available for the classroom or

other operations. The District could collect about $300,000 annually by charging a

small fee to students that qualify for reduced-price meals. In addition, accounting

records indicate that food operations has shown a profit for the last several years.

However, in fiscal year 2003, at least $900,000 in food service costs were not charged

to this account. Finally, the District could do a better job in monitoring the food service

contractor.

An effective school food service program provides students with nutritional,

reasonably-priced meals. During fiscal year 2003, the food service program collected

over $13 million, averaging about 28,000 meals a day. The District operates a central

21

LA04-19

kitchen and several self-contained kitchens at various school sites. The central kitchen

provides meals for elementary schools, while middle and high schools have self-

contained kitchens.

Opportunities for Revenue From Reduced-Price Meals

The District is not realizing all revenues available from food service operations.

We found the District is not charging any fee to students that received a reduced-price

lunch or breakfast. The District could have collected about $300,000 during fiscal year

2003 by charging a fee allowed under the federal lunch and breakfast programs.

The National School Lunch Program (NSLP) and School Breakfast Program

(SBP) subsidize school districts for meals served to eligible children. The federal meal

programs provide federal funds through the Nevada Department of Education.

Depending on household income, children may qualify for either a free or reduced-price

meal. Children that do not qualify for free or reduced-price meals can pay the full meal

price. Exhibit 7 shows the meal prices charged by the District and related federal

reimbursement rates for fiscal year 2003.

22 LA04-19

Exhibit 7

Washoe County School District

Meal Pricing Schedule

for Fiscal Year 2003

Student

Paid

Revenue to

District

Student

Paid

Revenue

to District

Paid 1.00 0.22$ 1.22$ 1.75 0.20$ 1.95$

Reduced $ .87-$1.10* $ .87-$1.10 1.74$ 1.74$

Free $1.17-$1.40* $1.17-$1.40 2.14$ 2.14$

Paid 1.00 0.22$ 1.22$ 2.00 0.20$ 2.20$

Reduced $ .87-$1.10* $ .87-$1.10 1.74$ 1.74$

Free $1.17-$1.40* $1.17-$1.40 2.14$ 2.14$

Paid 1.00 0.22$ 1.22$ 2.00 0.20$ 2.20$

Reduced $ .87-$1.10* $ .87-$1.10 1.74$ 1.74$

Free $1.17-$1.40* $1.17-$1.40 2.14$ 2.14$

Adult

1.50 1.50$ 2.50 2.50$

High School

Breakfast Lunch

Elementary

Middle School

Federal

Reimbursement

Federal

Reimbursement

$

$

$

$

$

$

$

$

$

$

$

$

$

-

-

-

-

-

-

-

-

-

-

-

-

-

$

$

$

$

$

$

$

$$-

Source: District records and Federal Register.

* Breakfast reimbursement rates vary depending on the percentage of children eligible for free

and reduced-price status at the school level.

The federal programs allow districts to charge up to 40 cents for reduced-price

lunches and 30 cents for reduced-price breakfasts. The District served about 624,000

reduced-price lunches during fiscal year 2003 and 191,000 reduced-price breakfasts

during the same period. If the District had charged the maximum fee allowed for these

meals, it would have collected about $300,000. According to the Nevada Department of

Education, 14 of the 17 Nevada school districts charge eligible students for reduced-

price meals. In addition, two of three peer districts surveyed indicated they charge

eligible students for reduced-price meals. The other peer district indicated their Board

policy is to not charge for these meals. Although the food service operation is reported

to be operating at a profit, as we discuss later in this chapter, not all costs are being

23 LA04-19

charged to this area. This additional revenue would help offset these costs making

more General Fund money available for other uses.

According to District officials and nutrition services management, the Board of

Trustees made the decision not to charge for reduced-price meals over 10 to 15 years

ago. However, District staff could not provide any documentation of the Board decision.

We recognize the sensitivity of this issue, but believe the Board needs to formally

decide whether to continue the current practice of not charging for reduced-price meals.

All Program Costs Not Charged

Even though the District reports food service operations have been profitable, all

costs associated with its operations are not charged to the Nutrition Services Fund.

District policy 3546 states the nutrition program will recover the cost of labor, food and

supplies from those served, except in special cases where students qualify for free or

reduced-price meals. However, we identified at least $900,000 in food service costs not

being charged to the food service account. As we have stated, General Fund dollars

used for food services takes money away from the classroom or other general

operations.

We reviewed the food service’s operating information for fiscal year 2003 and

identified at least $433,000 of costs directly attributable to the program that were being

paid by the District’s General Fund. In addition, every school incurs costs for

maintenance, janitorial, utility, and insurance of its cafeteria. These costs should also

be allocated to the food service program. Exhibit 8 summarizes the unallocated costs

we identified for FY 2003. Most of the costs shown are attributable to the central

kitchen only and do not include nutrition services costs at the individual schools.

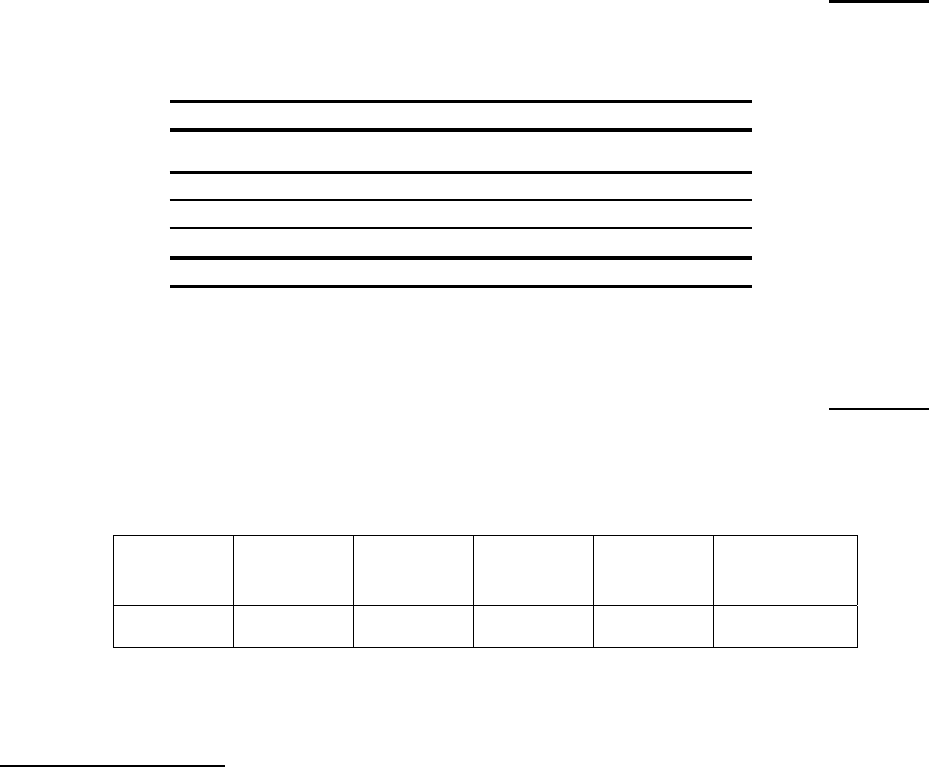

Exhibit 8

Unallocated Food Service Costs

Fiscal Year 2003

Cost Description FY 2003 Costs

Utilities 214,747$

Insurance 4,197

Interest on Debt Service 214,585

Total Unallocated Costs 433,529$

Source: Auditor analysis of District records.

24

LA04-19

In addition, depreciation charges on food service equipment and indirect costs

totaling at least $490,000 for fiscal year 2003 were not fully recovered from the

program. According to District records, depreciation on food service equipment and the

central kitchen facility was about $200,000. Further, many federal programs allow

indirect costs at around 2% to 3.65%. Indirect costs are those central service costs not

directly attributable to food services. For fiscal year 2003, this projects to about

$280,000 to $500,000 of indirect costs that central services should recover from the

food service operations. However, the central office allocated only about $25,000 a

year for indirect costs.

District accounting methods do not report what nutrition services actually costs to

operate. To report the actual costs to operate food services programs, many school

districts, including Clark County School District, use enterprise fund accounting. We

surveyed the five peer districts provided to us by the WCSD. Three of the five peer

districts use enterprise fund accounting. Enterprise fund accounting is useful to

governments because it helps focus on the cost of providing services and the portion of

those costs being paid by the user fees. At present, the District uses a special revenue

fund that does not provide information on what nutrition services actually costs to

operate. Therefore, District management may not have the information to make

informed decisions regarding the food service operation.

By accurately tracking program revenue and costs, the District could better

monitor and adjust fees, supported by detailed program analyses. Although the District

does also consider market and political constraints, policy makers would be better able

to make informed decisions if provided with complete cost data.

Better Food Service Contract Monitoring Needed

Since November 2000, the District has contracted the management of food

services. However, the District needs better monitoring controls over the food service

contract. For example, contractor billings lacked supporting documentation and

evidence of review. Although the billing we examined appeared reasonable, we had to

obtain the supporting information from the contractor.

Currently, the food services operation is a shared responsibility. The

management company is responsible for managing the food service operations and

25

LA04-19

supervising all food service employees. The District is responsible for paying all food

service operating costs, certain costs incurred by the management company, and a

management fee based on meals served. In addition, the District provides all food

service staff.

We reviewed a billing from the management company totaling $59,000. The

billing reviewed had no evidence of District review and the District could not provide

documents to support the amounts being charged. The management company was

paid approximately $674,000 in fiscal year 2003 or about 5% of food service

expenditures. As such, it is important to ensure the propriety of the billings. Internal

control standards require that transactions be properly reviewed and authorized prior to

payment. Further, control standards require significant transactions to be documented,

and the documentation should be readily available for examination.

Sufficient Controls Exist Over Legislative Funding

The District has sufficient controls in place over the textbooks, instructional

supplies and instructional hardware appropriation, and additional funding provided

during the 2001 and 2003 Legislative Sessions to help ensure the monies are used as

required. We reviewed the District’s request and expenditure process applicable to the

additional legislative funding. We also reviewed the controls the District has to ensure

textbooks, instructional supplies, and instructional hardware funds are appropriately

spent. We found the District had controls in place to ensure the money spent, to date,

was used for its stipulated purpose. Exhibit 9 provides information about special

legislative funding from the 2001 and 2003 Legislative Sessions.

26 LA04-19

Exhibit 9

Washoe County School District

Special Legislative Funding

2001 and 2003 Legislative Sessions

Session

Year

Bill

Number Purpose

A

mount

Available

Statewide

Amount to

District

2001 SB 8

Provides additional funding for

unexpected energy costs.

$ 6.5 Million $ 1 Million

2001 SB 9

Provides additional funding for

programs that are at risk of termination.

$ 5 Million $ 750,000

2003 SB 1

Provides additional funding for

Educational Technology.

$9.95 Million $1.1 Million

2003 SB 8

Provides funding to the DSA for

textbooks, instructional supplies, and

instructional hardware, including an

additional amount of $50 per student

approved by the Legislature. $131 Million

(1)

$ 18 Million

(1)

Source: Auditor analysis of 2001 and 2003 Special Legislative Funding.

(1)

Estimate based on student counts. Amount may be adjusted when Department of

Education completes student count audit.

Recommendations

1. Develop procedures and increase fiscal management oversight

over the process for obtaining reimbursement from the Medicaid

Program for school-based health services.

2. Adopt a policy to establish the fee charged for reduced-price

meals.

3. Consider amending policy to require all direct and indirect costs

be recovered by food service operations.

4. Consider establishing food service operations as an enterprise

fund.

5. Develop monitoring procedures to ensure monthly billings from

the food service contractor are appropriate.

27

LA04-19

Facilities Management

Aspects of the Plant Facilities Department operate effectively; for example, the

District has implemented a housekeeping method that has resulted in significant

savings. However, other areas could be improved. The District’s growth requires

significant construction management, but comprehensive construction management

policies and procedures have not been developed and capital projects planning could

be strengthened. Further, the District has made some efforts to be energy conscious,

but more work needs to be done. Finally, the Maintenance and Housekeeping Divisions

need more complete policies and procedures to provide reasonable assurance that

goals will be met.

The Plant Facilities Department is responsible for 91 schools, excluding charter

schools, and approximately 6.5 million square feet of building space, including portable

classrooms. Exhibit 10 shows the increase in schools over the past 5 years in the

District.

Exhibit 10

Number of Schools by Type

Fiscal Years 2000-2004

School Type 2000 2001 2002 2003 2004

Growth

2000-2004

Elementary Schools 58 59 59 61 61 5%

Middle Schools 13 13 13 13 14 8%

High Schools

(1)

12 12 14 14 15 25%

Special Education 1 1 1 1 1 0%

Total

84 85 87 89 91 8%

Source: Washoe County School District facility records.

(1) Includes Truckee Meadows Community College High School, Washoe High School, and Regional

Technical Institute.

In addition to the schools already serving Washoe County, the District will open

Shaw Middle School in Sparks in the fall of 2004. Over the next 5 years, the District is

planning the following:

• renovations to older schools

• 2 new middle schools

• 3 new elementary schools

28

LA04-19

• additions to 3 high schools as needed

• a modern technology and communication system

• phase II completion of the new Incline Elementary School

In November 2002, voters approved a rollover bond program to continue

financing capital improvements. To provide oversight of the bond rollover program, the

Plant Facilities Department was divided into two separate sections. The Plant Facilities

Administrator has oversight of maintenance, housekeeping, and regulated systems.

The Bond Program Administrator is responsible for construction, architecture, planning,

and remodeling. In total, the Plant Facilities Department had non-bond expenditures of

approximately $33 million in fiscal year 2003.

District’s Process for Cleaning Saves Money

In fiscal year 2002, the Plant Facilities Department developed a process for

cleaning District buildings that District records indicate saved over $600,000 annually.

The concept is known as Process Cleaning and recently received the Cashman Good

Government Award. A number of other governmental entities have requested the

District provide training on the Process Cleaning method.

Process Cleaning uses a systematic cleaning method that focuses on sanitizing

student and staff spaces. As a result of the new method, the District was able to reduce

its janitorial staff by 25 full-time equivalents (FTEs), saving the District about $610,000

annually. Currently, 80 of the District’s 97 schools and non-school sites have

implemented the Process Cleaning method. According to housekeeping officials, the

remaining sites should implement the new method during fiscal year 2005.

Housekeeping officials do not anticipate additional savings when the remaining sites

implement the new method because these sites are already staffed using the Process

Cleaning method staffing levels. However as new schools are constructed, the reduced

staffing levels required by the new method should continue to generate savings to the

District.

An efficiency achieved from the Process Cleaning method was to increase the

square footage staff custodians cleaned. As shown in Exhibit 11, the area cleaned per

staff custodian increased from about 24,500 square feet to about 27,200 or an increase

of over 11%. This occurred with a decrease in staff of 4% and a 6.6% increase in total

29

LA04-19

square footage. Exhibit 11 shows the increase in cleaning area resulting from the

Process Cleaning method.

Exhibit 11

Staff Custodian Cleaning Square Footage

Fiscal Years 2002-2004

2002 2003 2004

Percent Change

2002 - 2004

Cleaning Square Footage

Per Staff Custodian

24,561 27,152 27,284 11.1%

Total Staff Cleaning Square

Footage District-wide

5,507,703 5,593,316 5,872,780 6.6%

Number of Staff Custodians

(FTEs)

224.25 206 215.25 -4%

Source: Washoe County School District Housekeeping Division.

Furthermore, the Process Cleaning method appears to be effective despite the

larger cleaning areas and less staff. We surveyed District employees and found that

customer feedback was positive.

1

Our survey found that 73% of 422 respondents felt

the buildings are adequately cleaned.

Construction Management Policies and Procedures Need Updating

Although the District’s construction and bond transactions are well documented,

the policies and procedures governing this area could be improved to ensure good

business practices are followed. For example, District staff indicated they follow NRS

393.220 to 393.3293 that provide detailed guidance for the sale, exchange, and lease of

property. These statutes provide the framework for the District to follow, but not the

detailed procedures the District uses to comply with them. Further, the Board has

developed a policy and administrative regulation for the acquisition and disposition of

real property, but the policy and regulation are not comprehensive. Examples of other

areas where comprehensive policies and procedures should be developed include the

following:

• Construction management does not have procedures addressing allowable

construction costs, use of bond funds, and project management.

1

Appendix B summarizes our survey of District employees.

30

LA04-19

• Change order review and authorization procedures have not been formally

developed.

• The Plant Facilities Department lacks procedures to ensure the District is

awarded reimbursements from utility and road construction.

Much of this guidance has been handed down by legal opinion or other

memorandum form, but has not been formally adopted to help ensure staff are aware

and follow the requirements. The District indicated they are in the process of

developing more detailed policies and procedures using Clark County School District as

a model.

Capital Projects Planning Could Be Strengthened

The District has developed a Long-Range Facilities Plan; however, the last Plan

approved by the Board was in 1997. This plan identifies the District’s facilities needs

through 2015. Although the Plan is comprehensive, only minimal updates have

occurred and the Board has not approved these changes. Given the growth in the

District, periodic review and update of the plan would help ensure it still meets the

facilities needs of the District. Facility plans provide the framework for identifying and

allocating resources, evaluating and prioritizing projects, and considering alternatives.

Even though the District’s Long-Range Facilities Plan is comprehensive, it does

not give project specific information for the short-range. Generally, a formal capital

improvement plan (CIP) identifies the capital projects to be completed, and coordinates

financing and timing of completion. Currently, the District’s capital projects planning

comprises various components of a capital improvement plan. These components

include rollover bond information, technology plan, technical team recommendations,

and 2 year plan and 7 year needs forecast summaries. The District is currently in the

process of combining the Long-Range Facilities Plan and the various components of its

capital projects planning into a formal CIP. District officials indicated this plan should be

completed by February 2005, and will be updated annually and presented to the Board

of Trustees.

Improvements Needed in Energy Conservation Program

The District has made some efforts to be energy conscious, but more work

needs to be done. Specifically, the District can improve its planning to achieve greater

31

LA04-19

energy conservation. In addition, some energy conservation projects were not

competitively bid and some did not accomplish significant energy savings. Energy costs

across the State and nation have increased to levels requiring close monitoring and

management. The 2001 Legislature appropriated $6.5 million to assist school districts

in meeting the demands of rising energy costs. Of that amount, Washoe County School

District received $1 million. In fiscal year 2003, the District spent $10.9 million on

utilities.

Energy Conservation Plan Is Lacking

An energy conservation plan guides the school district in ways to lower energy

use and utility costs. Not only do such plans minimize waste, they encourage energy

awareness across the District. Although the District has implemented some energy

conservation measures, it has not developed an energy conservation plan.

Furthermore, our survey of District employees found only 26% of 422 respondents felt

the District has an effective energy conservation program. Only 41% of respondents felt

the District informed them of the energy program and their role in cost savings.

Development of a comprehensive energy plan would help inform staff and could provide

additional savings to the District.

Other states’ best practices recommend the adoption of energy conservation

plans. According to Clark County School District’s budget highlights, their energy

program achieved significant savings in fiscal year 2004. With the addition of more

monitoring staff, the savings are expected to increase in fiscal year 2005.

The following are some of the suggested items to include in a comprehensive

energy plan:

• realistic energy saving goals

• ways to keep the plan visible and linked to the budget

• commitment from the School Board and Superintendent

• designation of an energy manager

Conservation Agreements Were Not Competitively Bid

To help control energy costs, the District has contracted with an energy

retrofitting company. Between 1997 and fiscal year 2003, the District has entered a

pilot program agreement with four program extension agreements (phases 1 through 4)

32

LA04-19

with this company totaling about $15 million. Competitive bids were not obtained for

any of the agreements, as required by state law. NRS 338 provides bidding guidelines

for governmental agencies. More recently, the 2003 Legislative Session amended NRS

Chapter 332 to include a section for performance contracts for operating cost-savings

measures. This amendment requires the local entity to issue a request for qualifications

(RFQ) to not less than three potential qualified service companies. It also requires the

local entity to compile a list from the RFQs of those companies it determines satisfy the

requirements of qualified service companies. If the local entity wants to enter into a

performance contract, it must notify each appropriate qualified service company.

District personnel believed the agreements were for professional services, and

therefore were exempt from the bidding requirements. However, the agreements were

not exclusively for professional services. The energy conservation measures

implemented through these agreements included lighting retrofits, HVAC retrofits, roof

replacements, boiler retrofits, and ventilation upgrades.

Energy Savings Were Insufficient for Projects

Energy savings were sufficient to recover the costs of retrofitting for only two of

the four program extension agreements entered into by the District since 1997. NRS

sections and industry standards suggest that energy conservation projects be evaluated

to ensure the savings will justify the retrofit costs. For an energy conservation retrofit

project to be paid for with savings from reductions in energy usage, those savings

should occur within the useful life of the project. The energy services company

contracted by the District to undertake various energy conservation retrofit projects

guaranteed energy savings over a 10-year period. The U.S. Environmental Protection

Agency also recommends using a 10-year period when evaluating the worth of energy

conservation retrofit projects. Exhibit 12 shows the project cost, guaranteed annual

savings, and years to recover the costs (payback) for the four projects.

33

LA04-19

Exhibit 12

Energy Retrofit Projects

Fiscal Years 1997 - 2003

Pilot Program

Extension Agreement

Project Cost

Guaranteed

Annual Savings

Payback

(Years)

Phase 1 $5,294,076 $481,798 11

Phase 2 $2,152,858 $204,948 11

Phase 3 $4,826,612 $234,995 21

Phase 4 $2,557,455 $ 34,141 75

Source: Washoe County School District Records.

As shown in Exhibit 12, the simple payback for the third and fourth phases were

21 and 75 years, respectively. This is well beyond the useful life of the projects. We

asked District staff if a formal financial analysis was conducted to determine the worth of

pursuing each phase of the energy conservation retrofit project. District staff indicated

they believe a financial analysis was conducted but could not provide an analysis for

any of the projects.

Maintenance and Housekeeping Lack Complete Policies and Procedures

The Maintenance and Housekeeping Divisions do not have complete policies

and procedures in place to help employees know their responsibilities and to ensure

good business practices are followed. Other states’ best practices acknowledge the

importance of comprehensive policies and procedures over maintenance and

housekeeping functions. In addition, internal control standards recommend policies and

procedures are documented.

Housekeeping Supplies

Housekeeping supplies are purchased and stored at a central location and

allocated to schools by the housekeeping supervisor. In addition, the Housekeeping

Division assumed control of housekeeping supply budgets for each school and non-

school site in fiscal year 2003. However, the Division has not developed procedures for

the inventorying, distributing, and safeguarding of the supplies. Procedures would help

to provide greater assurance that supplies are not stolen or wasted.

In addition, the Division tries to maintain 2 or 3 months of custodial supplies.

However, a review of the supplies inventory found about half the supplies had quantities

exceeding 5 months and nearly 25% had quantities exceeding 1 year. Although the

34

LA04-19

Division’s inventory listing identifies order points, no ordering guidelines have been

developed. In addition, many of the supply order points exceed the 2 or 3 month

quantity the Division tries to keep on hand. Although supply inventory costs are not

excessive, large amounts of supplies can reduce the District’s operating budget and

increase storage needs. Opportunities may exist for additional savings in this area.

Maintenance Division

The Maintenance Division has not developed complete policies and procedures

to assist employees in carrying out their duties. Establishing procedures helps promote

good administrative practices and efficient operations. In addition to a lack of a

complete policy manual, we also identified several instances where policies and

procedures could help improve Division operations. For example:

• The Division uses many types of large and small equipment and tool items.

Although equipment and tools are either recorded in a database or hand-

written records, there is no process to periodically count the items. These

items represent a significant value to the Division. Many of the items are

small and easily misplaced, lost, or stolen.

• The Division does not monitor deferred maintenance activity. The Division

indicated the list is reviewed quarterly by the plant facilities supervisor and

annually by the plant facilities administrator. Upon further review, we found

no evidence this routinely occurs.

• The Division has not established procedures for determining general work

order priority and estimating completion dates for input in the ACT1000

system. During our work on the Preliminary Survey Report, we were told

that priority guidelines existed. However, these guidelines are used to

assess the condition of District facilities as part of its periodic facilities

assessment program in the Facilities Condition Information System, not to

prioritize general maintenance.

Recommendations

6. Require all District schools to use the Process Cleaning method.

7. Continue developing the construction management procedures.

8. Continue developing the capital improvement plan and develop

procedures to periodically review and update the plan as needed.

9. Develop a comprehensive energy management plan.

35

LA04-19

10. Perform a cost benefit analysis for each energy retrofit contract

and competitively bid the contracts.

11. Develop maintenance policies and procedures, including

procedures for custodial supply inventories, maintenance

equipment and tools inventories, monitoring deferred

maintenance, and determining general work order priorities.

Personnel Management

We found the Human Resources Division has implemented some innovative

programs and, generally, meets the needs of the District employees and management.

However, some improvements are necessary to ensure its recruitment and retention

efforts maintain qualified staff. For example, the Division needs to improve its planning

efforts and compile operational data to manage its personnel resources effectively.

These and other personnel management issues have been mentioned in prior audits

and management reviews, but the District has not fully addressed them. Because

personnel costs comprise nearly 90% of the District’s budgeted expenditures,

improvements are needed to assist in making financial and operational decisions and

ensure management directives are followed.

Human Resources operations should be further enhanced when the District

completes efforts to develop comprehensive, consolidated procedures. In 2002, the

Division started to develop procedures by following guidelines set forth in a quality

management system. However, this process is not complete and, as a result, the

District still does not have all-inclusive procedures.

Personnel Program Accomplishments

The WCSD has developed programs intended to improve recruitment and

retention of employees. For example, WCSD is in the process of implementing an on-

line application system. This system should streamline the process and track recruiting

efforts. According to The New Teacher Project, a nonprofit group that helps some of

the largest school districts recruit teachers, Clark County School District (CCSD) has a

similar system that eliminated data entry and dramatically improved application

turnaround time.

36

LA04-19

WCSD has also implemented two programs in recent years in an effort to

maintain a stable and effective work force. Each of the programs is briefly described

below:

Mentor Teacher Program – The purpose is to train veteran teachers to serve as

mentors to novice teachers. According to District reports, between 1997 and 2001,

5.4% of new teachers in the mentor program resigned as compared to 10.5% of new

teachers not in the program. The District continues to assess and modify this program

not only to address teacher retention but to help impact teacher performance and

student achievement.

Teacher Performance Evaluation System (TPES) – WCSD is part of a five-year study

funded by the U.S. Department of Education to find connections between teacher and

administrator attitudes and behaviors, their evaluation scores, and student achievement.

After 3 years, the majority of teachers believed the evaluation process reflected good

teaching and the system could improve teaching. In addition, administrators felt that

TPES helped them frame evaluation discussions, provide useful feedback to teachers,

and generally augmented their instructional leadership.

Lastly, the District has taken action to identify why teachers leave the District,

including what job aspects were factors in leaving and what job aspects caused

dissatisfaction. According to a survey performed by the University of Wisconsin, over

half of the teachers exiting WCSD during or after the 2002-2003 school year cited

retirement as the reason for leaving. Key portions of the survey are summarized in

Appendix C.

Improvements Needed in Planning and Evaluating Recruitment Efforts

The WCSD would benefit from tracking recruitment efforts and integrating this

information into a formal recruitment and retention plan. Prior audit, consultant, and

internal reports advised the Human Resources Division to develop a recruitment and

retention plan. These reports also identified the need to improve the Division’s

information system to compile and evaluate efforts.

Recruitment and Retention Plan

In 1999, the Division drafted a document containing the components of a

recruitment plan. This document defined the Division’s goals, identified action steps,

established anticipated completion dates, and defined anticipated results. However,

this document was not completed. A plan is important because the District faces

recruitment challenges when having to hire 400 to 500 new teachers each year.

37

LA04-19

Planning is a basic, core element of management. Without a plan, the risk that efforts

are inefficient and ineffective increases.

The District relies primarily on the experience of its personnel to determine how it

will recruit. Techniques employed include:

• attending job fairs

• cultivating relationships with local colleges and universities

• utilizing a web-based recruitment service

• attending events that could generate potential job seekers

In an area related to recruitment, the District does not have a stated business

strategy addressing teacher retention. As part of its comprehensive human resources

plan, the District should develop a strategy for addressing teacher retention. The plan

should identify the District’s goals for teacher retention, define the measurable