PANDEMIC: CAN THE LIFE INSURANCE INDUSTRY

SURVIVE THE AVIAN FLU?

Moderate influenza pandemic similar

to 1957 and 1968 outbreaks could cost

U.S. life insurers $15 billion in

additional claims

Severe pandemic similar to 1918

experience could cost up to $155

billion.

January 17, 2006

(Updated November 1, 2006)

Steven Weisbart, Ph.D., CLU,

Economist

Insurance Information Institute

110 William Street

New York, NY 10038

Tel: (212) 346-5540

Fax: (212) 732-1916

[email protected] www.iii.org

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

2

Overview

Widespread concern exists that the H5N1 influenza virus, a highly lethal virus that now largely

affects birds, could mutate into a form that could easily leap from birds to humans, and then from

humans to other humans, creating a worldwide pandemic. The virus has been tracked from China

(where the current outbreak originated in late 2003) to Asia, Europe, Africa, and Canada. To date,

no birds have tested positive for this virus in the United States.

Through June 6, 2006, 225 people in 10 countries are known to have been infected with the virus,

and 128 of them have died as a result, a mortality rate of 57 percent.

1

Experts believe that many of

the infected people got the flu from direct contact with infected birds, not from other infected people.

However, there is now some evidence that the virus might have been transmitted from one human

to another, but not necessarily easily transmitted.

2

The pandemic threat arises only if the virus

mutates so that humans can easily catch it from other humans.

In a typical year, 36,000 Americans die from the influenza strains that circulate.

3

But the H5N1

strain is far more lethal, so far, than a typical flu. Although many variables could affect the number

of people who could catch and die from the H5N1 flu, the U.S. Department of Health and Human

Services (HHS) projects that in a severe influenza pandemic 1.9 million people in the United States

could die, working largely from the experience of the 1918 pandemic—to date, the deadliest and

most infectious known influenza strain.

4

Laurie Garrett, extrapolating from the recent H5N1

outbreaks, calculates an “extreme… worst case scenario,” based on an assumption of 80 million

Americans infected and a mortality rate of 20 percent, namely 16 million deaths.

5

How would such a pandemic affect life insurance companies? Answering that is even more

challenging than predicting the potential damage from dozens of tropical storms that might make

landfall, because we have no modern experience with vast health disasters. It must also be pointed

out that there have been numerous public health alarms in recent years—from the effects of the

pesticide alar to mad cow disease to swine flu—that did not produce nearly the catastrophic results

that early media coverage had predicted. And, no matter what happens, the classic killers of

smoking, poor diet, lack of activity, teenage driving, alcohol, violence, pollution, etc., will continue to

take their heavy toll. However, based on assumptions described below, a severe influenza

pandemic might be projected to cause $155 billion in additional death claims. The sudden impact of

such unpredicted losses would clearly affect all life insurers, particularly the weaker ones. A

moderate pandemic, modeled on the outbreaks in 1957 and 1968, might cause additional death

claims of $15 billion industrywide.

1

World Health Organization Web site (www.who.int/csr/disease/avian_influenza/country/cases_table_2006_06_06/en/). The countries with deaths

are China (12), Indonesia (37), Viet Nam (42), Thailand (14), Azerbaijan (5), Cambodia (6), Turkey (4), Iraq (2) and Egypt (6). In 1997 Hong Kong

had 6 deaths from the H5N1 flu. The 225 total likely omits mild cases that weren’t reported. See “Fears of Undetected Bird-Flu Outbreaks Mount,”

Wall Street Journal, December 8, 2005, p. A14, and Elizabeth Rosenthal, “A Scientific Puzzle: Some Turks Have Bird Flu Virus but Aren’t Sick,”

New York Times, January 11, 2006, p. A10.

2

Donald G. McNeil, Jr., “Bird Flu Case May Be First Double Jump,” New York Times, May 24, 2006, p. A10 and Elisabeth Rosenthal, “W.H.O. to

Study Bird Flu Deaths in Family, New York Times, May 25, 2006, p. A 14.

3

CDC Web site at http://www.cdc.gov/flu/keyfacts.htm

4

This is the forecast under the “severe” scenario, modeled after the 1918 pandemic. HHS Pandemic Influenza Plan, U.S. Department of Health and

Human Services, November 2005, p. 18. Of course, the outcome could be worse than it was in 1918; see pp.2-3 infra.

5

Laurie Garrett, “Probable Cause,” Foreign Affairs, July/August 2005, p. 4. Garrett’s infection rate is about what was experienced in the U.S. 1918

flu pandemic.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

3

Influenza Mortality: Patterns and Life Insurance Implications

Normally, most influenza deaths occur among the very old and the very young—two populations not

likely to have large amounts of life insurance. However, in the 1918 influenza pandemic, which

killed roughly 675,000 people in the United States—and between 50 million and 100 million

worldwide—the age group with the highest number of deaths was ages 25 to 34, a population that

today has significant group and individual life insurance in force. (For more on the 1918 influenza

pandemic, see Appendix A.)

For at least two reasons, it is possible that most forecasts of deaths in a severe pandemic seriously

underestimate the likely number of deaths for the 65-and-over age group. First, it is possible that

fewer people in the 65-and-over age group died in the 1918 pandemic than would die today

because in 1918 some seniors had a limited immunity, derived from exposure to a similar influenza

epidemic several decades before.

6

However, there has never been an influenza virus of the H5

subtype before, so today’s seniors wouldn’t have any level of immunity to protect them.

7

Second, in

1918 people over 65 constituted a much smaller percentage of the population than they do today;

the number of deaths from this group was small in 1918 in part because the number of people in

this age group was smaller then. Since today the number of people in this age range is

considerably larger, the 1918 death rate applied to today’s senior population would produce many

more deaths.

Of course, much has changed in the 88 years since the 1918 influenza pandemic hit America.

Some of the changes might lead us to expect that an H5N1 pandemic today would not be as severe

as the 1918 flu. Indeed, many who hear about the Avian influenza threat remember that the recent

(2003) SARS outbreak was contained quickly; only 8,437 people became infected and 813 died.

8

In

the United States, eight people were diagnosed with SARS, but only one is thought to have been

infected here; the others had traveled to Canada and probably were infected there.

9

But the SARS

virus was not a flu virus (for more on this, see Appendix B). Here are some of the most obvious

changes regarding influenza from 1918 to today:

In 1918 there was a world war underway, which created higher-than-normal concentrations

of people in barracks and other assembly places, plus frequent and large-scale movement

of people to places where outbreaks had not occurred, facilitating the transmission of the

virus.

In 1918 a high proportion of U.S. medical resources were sent to Europe to serve the war

effort, further tilting the odds in favor of viral transmission in the United States because

medical resources here were unusually scarce.

The modern medical community now understands that influenza is a virus and has a better

understanding of how to constrain the spread of viruses.

Some of the deaths associated with the 1918 virus were due to bacterial pneumonia and

other conditions that “took advantage” of the weakened immune systems of those infected;

modern antibiotics can fight these secondary infections quite effectively.

6

John M. Barry, The Great Influenza: The Epic Story of the Deadliest Plague in History, Penguin Books, p. 408.

7

World Health Organization, Avian influenza: assessing the pandemic threat, January 2005, p. 19.

8

William Karesh and Robert Cook, “The Human-animal Link,” Foreign Affairs, July/August 2005, p. 41

9

Angela J. Peck et al, “Lack of SARS Transmission and U.S. SARS Case-Patient,” Emerging Infectious Diseases, Vol. 10, No. 2 (February 2004), at

the CDC Web site (www.cdc.gov/ncidod/EID/vol10no2/03-0746.htm

).

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

4

Although there is no “cure” for influenza, some antiviral drugs (such as Relenza and

Tamiflu) and vaccines have been developed (although testing has not been completed)

that could mitigate the effect of the H5N1 strain; furthermore, the science and technology

necessary to develop vaccines is much more advanced.

Detection and confirmation of the presence of a virus is more rapid today; the World Health

Organization has 133 centers in 84 countries to collect and analyze viruses.

Through the Internet, television, cell phones and other means of communication, we can

disseminate information about the virus more quickly to more people in more places than

was possible in 1918.

We have better, and more specialized, health care facilities and equipment—emergency

rooms, intensive care units, mechanical ventilators, etc.—that can mitigate secondary

effects.

Countries are actively taking measures to prevent the virus from spreading, including

destroying diseased birds, vaccinating healthy birds,

10

stockpiling antiviral medicines for

humans, planning quarantine scenarios, and conducting simulated outbreaks to train first

responders and medical professionals.

Indeed, two more recent influenza pandemics, in 1957 and 1968, were much milder than the 1918

outbreak. The 1957 flu is estimated to have caused more than 60,000 deaths beyond normal flu

mortality and the 1968 flu 34,000 deaths beyond normal flu mortality.

11

The World Health

Organization attributes some of the relatively diminished lethality of the 1957 and 1968 pandemics

to advances in modern medicine.

12

On the other hand, there are several reasons a new influenza pandemic could be as bad as, or

even worse, today than in 1918:

Widespread commercial air travel and extensive shipping of food (especially poultry

products) internationally create many more transmission opportunities and a means for

rapidly spreading contamination and infection.

13

The standard techniques for creating a vaccine for this virus might not work quickly enough

(it takes roughly six months using current technology), to produce a large enough supply

early enough to inoculate even the highest risk groups, particularly if two doses are

required for the vaccine to be effective,

14

(recognizing that for a vaccine to work at all, it

must be administered before a patient becomes ill from the virus).

10

China has begun a program to vaccinate every one of the “14.2 billion domesticated fowl that constitute what the government estimates is the total

bird population over a year’s time.” Howard W. French, “Bird by Bird, China Tackles Vast Flu Task,” New York Times, December 2, 2005.

11

World Health Organization, op/ cit., p. 24.

12

Ibid., pp 26-31.

13

For example, “once SARS emerged in rural China, it spread to five countries within 24 hours and to 30 countries on six continents within several

months.” Michael Osterholm, “Preparing for the Next Pandemic,” Foreign Affairs, July-August 2005, p. 28.

14

“Currently…each dose of seasonal vaccine contains 45 micrograms of antigen, the raw material from which vaccines are made. The best available

science indicates that two doses of vaccine, each requiring 90 micrograms of antigen, are necessary to protect against the H5N1 strain.”

Congressional Budget Office, A Potential Influenza Pandemic: Possible Macroeconomic Effects and Policy Issues, December 8, 2005, p. 22, citing

the November 2, 2005 statement of Michael Leavitt, Secretary of the U.S. Department of Health and Human Services, before the U.S. Senate

Subcommittee on Labor, Health and Human Services, and Education. So from a production viewpoint, we would need to produce for each person

vaccinated the equivalent of four times the amount of vaccine that is normally produced, since each dose would need to contain twice the antigen that

a normal seasonal dose has, and two of these stronger doses are needed to provide immunity.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

5

The U.S. government’s recently issued pandemic response plan calls for states and

localities to be the main providers of health and other services and to pay for 75 percent of

the cost; many states will be hard pressed to come up with the money or the services

needed.

For antiviral medicines (as opposed to vaccines) to be effective, they must be administered

within 48 hours of exposure to the virus, and must be taken for five days or else they are

ineffective—those infected might not be able to get the medicine quickly enough or obtain

a sufficient supply to maintain the medicine’s effectiveness.

As noted earlier, some people in 1918 had a limited immunity to the virus because of

exposure to similar viruses in the several decades that preceded its arrival; that is not the

case today.

With the spread of HIV

15

and the use of radiation and chemotherapy for cancer treatment,

many people today have compromised immune systems and may be less able to fight off a

virulent influenza strain.

The new virus could prove to be much more lethal than any previous virus.

16

Effect of an Avian influenza Pandemic on Business and Investment Values

Now suppose an outbreak of the H5N1 flu occurs in the United States. How would this affect life

insurance companies? Although the main risk would be claims in excess of expected mortality, a

serious coincident risk could be asset deterioration.

17

Considering first the pandemic’s effect on asset values, any organization whose business involves

gathering people together—movie theaters, restaurants, shopping malls and other stores, public

transportation, and sports events and concerts are some examples—would probably be shut down

for the length of any human quarantine, as happened in prior pandemics. If they follow historical

patterns, local quarantines would be short—perhaps a month—but some businesses, such as

intercity transportation, might be affected for longer periods.

Even if there were no quarantines, during a pandemic wave and for a time afterward, many people

would be reluctant to expose themselves to crowds. Internet and catalog shopping for many items

would likely replace some in-person shopping, but the unwillingness of employees of those

businesses to report to work might create long delays in filling orders. Michael T. Osterholm argues

that supplies of many items, both finished goods and intermediate goods, could be in short supply

because so much of what Americans buy is dependent on thriving overseas production, which

could also be devastated by a pandemic.

18

As for employees, those in businesses that involve substantial human proximity, such as health

care workers, teachers, bus drivers, barbers and hair stylists, and so forth, would likely be more

vulnerable to the flu than those in occupations that can be conducted with relatively little human

contact.

15

One estimate is that over 1 million people in the U.S. now have HIV/AIDS. See www.avert.org/statsum.htm. The majority of them are in the prime

insurance-owning ages, but it may be supposed that, as a group, they own little life insurance. This is because, until recently, life insurance was either

unavailable to these risks or was available only at substandard (i.e., higher than standard) rates.

16

This is a short list of why the pandemic could be worse than the 1918 outbreak. For a thorough analysis, see articles by Garrett, Osterholm, and

Karesh and Cook, in the July/August 2005 issue of Foreign Affairs.

17

Howell Pugh, “Pandemic: The Cost of Avian Influenza,” Contingencies, September/October 2005, p. 26.

18

Michael T. Osterholm, op. cit.,, pp. 31-32.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

6

It is easy to forecast that, under these conditions, the loss of business and a likely crash in

consumer confidence would cause corporate earnings to plunge and trigger defaults on corporate

debt. In turn, the drop in economic activity would decrease government tax receipts and increase

government income-support outlays, further exacerbating government budget problems and

possibly scrambling budget priorities. Taking all this together, the Congressional Budget Office

(CBO) estimates the macroeconomic effect of a severe influenza pandemic as roughly equivalent to

a typical recession—a loss of 4 ¼ percent of GDP compared to what it would otherwise have been.

The CBO cites a Canadian study that uses actual pandemic experience rather than models and

concludes that the economic effect of a severe pandemic would reduce GDP by from 0.3 to 1.1

percent, in the U.S. as well as Canada.

19

The extent and duration of any effect of these business implications on equity and bond

investments is impossible to predict, but the behavior of the U.S. stock market during previous

influenza outbreaks might be instructive. Of course, many factors affect stock market behavior, and

at the time of the 1918 pandemic, the economic world was very different from what it is today.

In the spring of 1918 the United States had been fighting in World War I for a year. The Dow Jones

Industrial Average (DJIA) had dropped from 93.9 in April 1917 (when the United States entered the

war) to 70.2 in December, then rebounded to 79.95 in February 1918. The first signs of a pandemic

appeared in March 1918, but that wave was mild. The DJIA, 78.05 in March, climbed gradually to

81.95 in August. The worst of the pandemic hit the United States in September through December,

but the stock market virtually ignored the staggering number of people infected and high death toll:

the DJIA hit 82.5 in September, 86.25 in October, 84.0 in November (when the war ended), and

82.5 in December.

The SARS outbreak in 2003 offers a more contemporary experience of the effect of a pandemic on

stock markets, although not on U.S. markets. There were virtually no SARS cases in the United

States; the two most affected areas were Canada and Southeast Asia. But in these cases, too, it is

difficult to discern an adverse impact of the pandemic on stock values. During the second quarter of

2003, which was the peak for the SARS outbreak, the Toronto Stock Exchange index rose

strongly—though more slowly than the S&P 500 in the U.S. The Shanghai composite was slightly

down for the quarter, but the Hang Seng index rose nearly as fast as the S&P, with about a one-

month lag. These results are consistent with the CBO and other studies that envision, at most, a

mild impact on the investment markets of a severe flu pandemic.

On December 30, 2005, President Bush signed into law the Public Readiness and Emergency

Preparedness Act. The act has two consequences for an Avian Flu pandemic. If the Secretary of

the Department of Health and Human Services (HHS) declares a public health emergency that

meets the requirements of the act, it provides immunity from lawsuits in state and federal courts for

manufacturers and “distributors” of vaccines and other “countermeasures.” The act also authorizes

the HHS Secretary to create a compensation fund to which those adversely affected by the

countermeasures can apply. The compensation program will “have the same elements, and be in

the same amount,” as the current smallpox vaccination victim fund.

20

19

Congressional Budget Office, A Potential Influenza Pandemic: Possible Macroeconomic Effects and Policy Issues, December 8, 2005, p. 12. The

update is dated July 27, 2006.

20

The Act is Division C of H.R. 2863; P.L. 109-148. The Compensation program is in Sec. 319F-4.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

7

Effect of an Avian influenza Pandemic on Life Insurance Companies

In terms of claims dollars, in 2004 (the latest data available from the American Council of Life

Insurers) U.S. life insurers paid $32.2 billion on individual policies, plus $18.7 billion in group life

insurance claims and about $0.6 billion in credit life insurance claims. The dollars paid to

beneficiaries in normal years grossly understate what would happen in a severe influenza

pandemic. This is because the average payment per policy in a typical recent year was about

$12,000. This reflects the fact that many death claims are from whole life policies for people quite

aged at death and issued many decades ago. In a pandemic like the one in 1918, claims on

individual policies would more likely be closer to the current average in-force amount, which is

estimated to be $81,800 in 2006

21

. Another indicator could be the current average amount issued in

the most recent several years. For term insurance, the issued amount is probably over $250,000;

for some companies, it is over $500,000. Comparable numbers from permanent life insurance

policies would be closer to $80,000, perhaps less. So if a half million insureds died from the flu and

if claims equaled only the average projected in-force amount per policy in 2006, life insurers would

likely pay claims from individual life insurance policies totaling $41 billion, which by itself is more

than.

The effect of a pandemic on a particular life insurance company will depend on many factors. These

include:

Where a company’s insureds are located in relation to outbreaks of the disease, including

exposure to certain foreign markets (especially Asia) where the outbreak may be more

severe.

22

The extent to which a company’s particular investments are affected by the spread of the

disease.

How easily a company can convert assets into cash for the purpose of paying benefits.

The diversification and character of a company’s products (e.g., whether it writes group life

insurance or whether it writes other lines of business that remain profitable).

How conservatively a company has calculated its reserves.

To what extent a company is able to raise additional capital under pandemic

circumstances.

In order to assess the mortality risk for life insurance companies, this paper uses the “moderate”

and “severe” forecasts from the U.S. Department of Health and Human Services (HHS). Both

assume 30 percent of the U.S. population—90 million people—would become ill; in the moderate

forecast, 209,000 would die and in the severe forecast, 1.9 million would die. Of course, some of

the dead would not be covered by any life insurance. Some would be covered by policies bought

long ago for what are, by today’s standards, small death benefits. This analysis assumes for

simplicity that no children are insured (since those who are insured are covered for nominal

amounts). Relatively few people are covered by both group and individual life insurance. The effect

on each of these lines of business is traced separately in the next two sections.

21

This is the published 2004 number increased by 0.6 percent per year (the growth rate from 2003 to 2004) to 2006.

22

For example, an article on page 12 in the November 2005 issue of Best’s Review notes that close to 70 percent of one large life insurer’s total

profits come from Japan, that another’s is in the 35 to 40 percent range, and that Japan is the largest life insurance market for a third large life insurer.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

8

Effect on a company’s book of business

Group life insurance

Virtually all group life insurance is effectively one-year term insurance. The people insured are

working age, and so a small number of deaths are expected in any normal year. Reserves are

generally low. Typical amounts of insurance are equal to an employee’s yearly salary. The very

largest groups—tens of thousands of employees—are experience rated, which means that the

employer’s premium directly reflects the claims experience of the group. The smaller the group, the

greater the extent to which the risk of higher-than-expected deaths is transferred to the insurance

company offering the group insurance.

Most companies that write group life insurance do so as one part of a portfolio of other lines of

business. Of the 30 largest writers of group life insurance as of the year-end 2004, only two had 90

percent or more of their business in that line. Of the other 28, one had 36 percent of its total

premiums in that line, one had 27 percent, and the rest had 20 percent or less of net written

premiums in group life insurance.

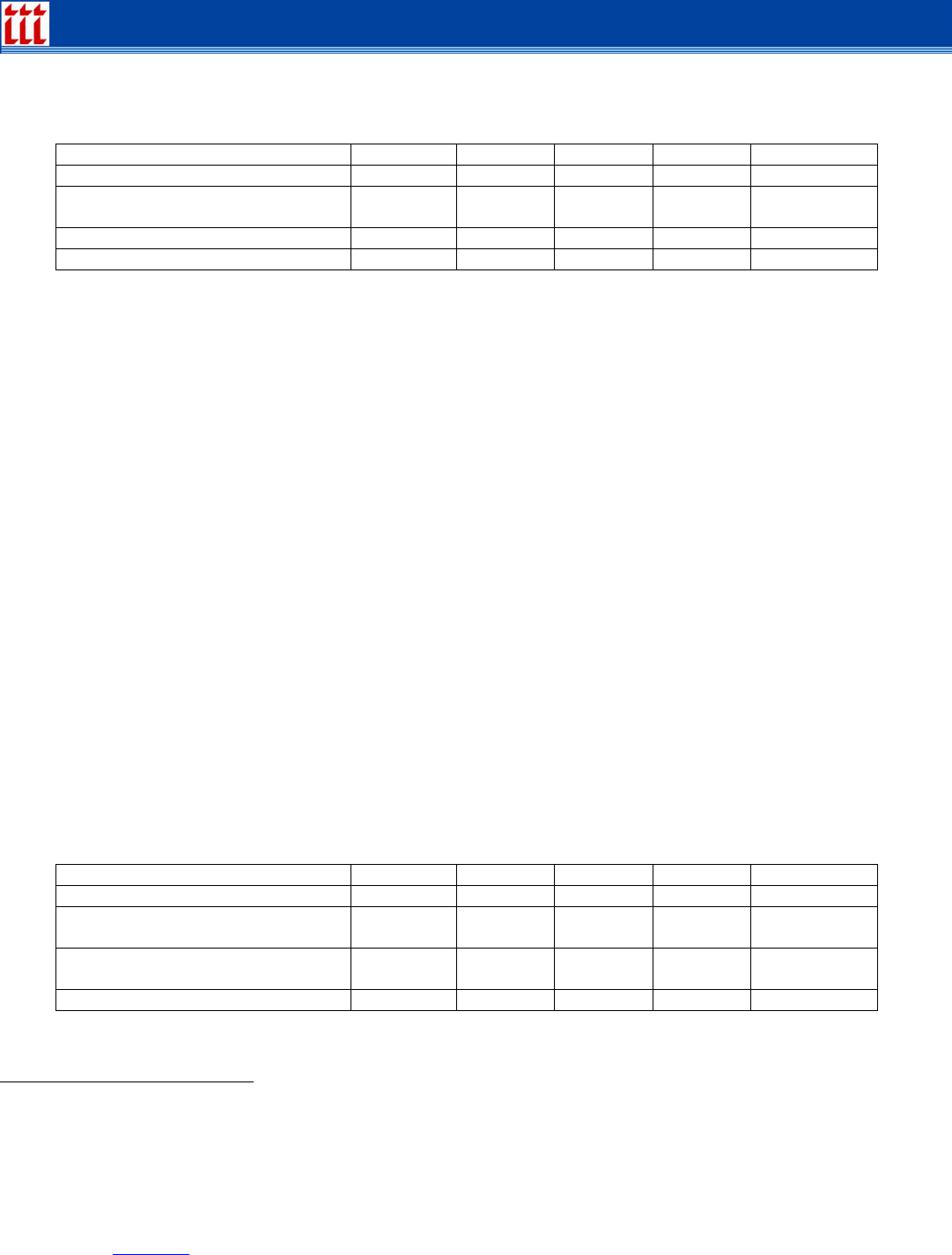

Table 1: Group Life Insurance Projected Death Claims, by Age Range, Severe Pandemic

Age range 25-34 35-44 45-54 55-64 65 and over

Projected deaths

23

378,650 268,600 44,000 123,450 526,700

Percent who own group life

insurance

46%

51%

48%

42%

20%

Mean group life benefit

$100,300 $210,300 $109,500 $99,200 $48,400

Projected claims (billions)

$17.5 $28.8 $2.3 $5.1 $5.1

Source for life insurance ownership data: LIMRA, Trends in Life Insurance Ownership Among U.S. Households, p. 18,

projected to benefits held in 2006.

The total projected death claims from group life insurance, from a severe influenza pandemic as

derived from data in the preceding table, is $58.8 billion. The projection is heavily dependent on the

mortality pattern observed in 1918.

Under these assumptions, virtually every company’s group life claims would surpass premiums,

dissolve any policyholder dividends and possibly force them to use some corporate surplus (which

is, of course, created precisely for this situation). Although many factors would affect the outcome,

we estimate that perhaps five to eight of the 30 leading group life insurance writers might struggle to

pay their group life claims, particularly if other lines of business, as well as their asset values, are

also under stress.

23

These data apply the mortality rates experienced by these age groups in the 1918 pandemic to the current U.S. population, except that the number of

deaths for the 65+ age group is increased by 100,000 to account for the lack of immunity that modern seniors have to H5N1 compared to the limited

immunity that seniors had in 1918 to that year’s flu pandemic.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

9

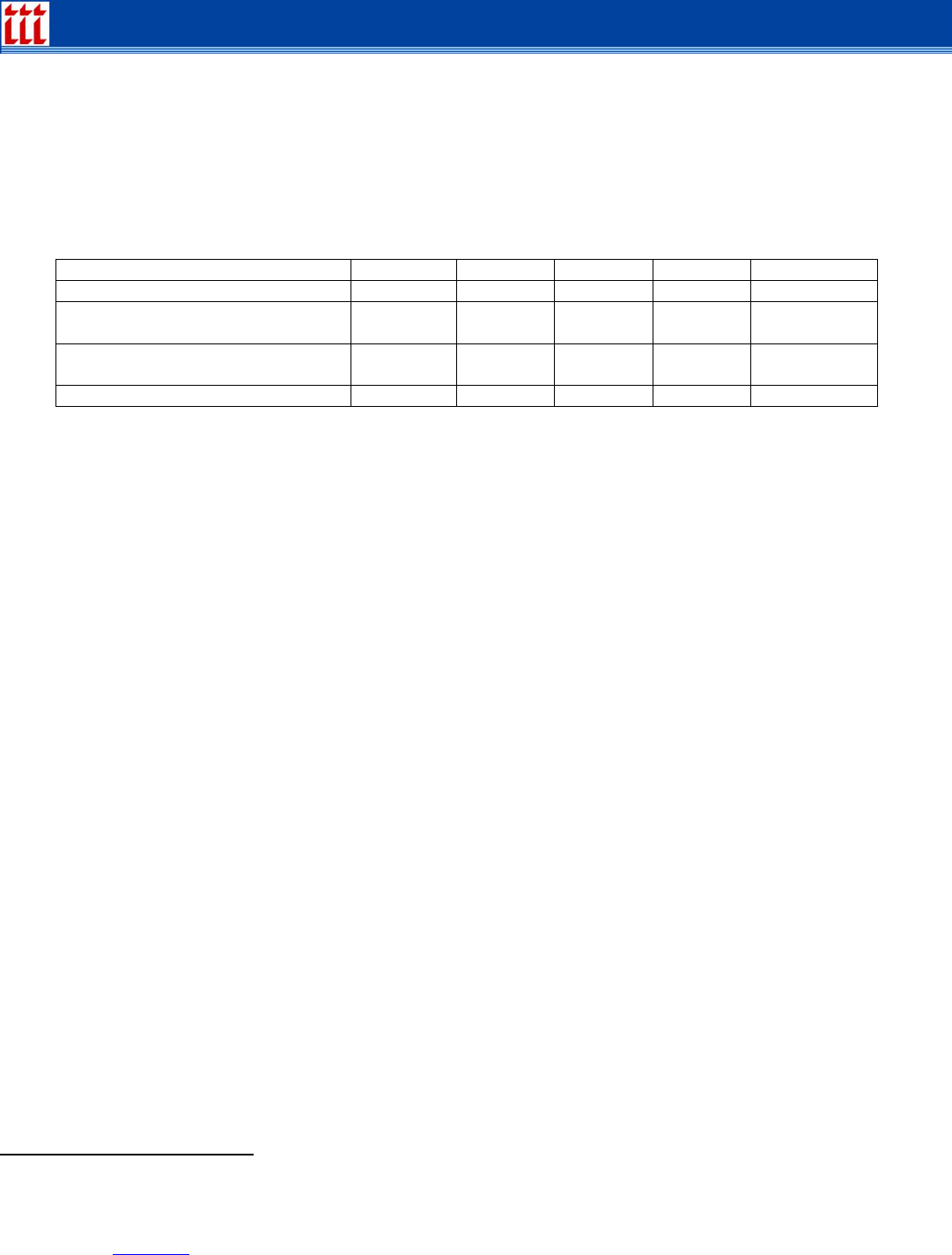

Table 2: Group Life Insurance Projected Death Claims, by Age Range, Moderate Pandemic

Age range 25-34 35-44 45-54 55-64 65 and over

Projected deaths

24

10,000 15,000 20,000 35,000 65,000

Percent who own group life

insurance

46%

51%

48%

42%

20%

Mean group life benefit

$100,300 $210,300 $109,500 $99,200 $48,400

Projected claims (billions)

$0.5 $1.6 $1.1 $1.5 $0.6

Source for life insurance ownership data: LIMRA, Trends in Life Insurance Ownership Among U.S. Households, p. 18,

projected to benefits held in 2006.

The total projected death claims from group life insurance from a moderate influenza pandemic as

derived from data in the preceding table is $5.2 billion.

Individual life insurance

In the individual life insurance line of business, the greatest vulnerability to “excess” deaths from a

influenza pandemic would arise from term insurance and periodic-payment whole life insurance

policies in their first few years of existence. For these policies, the reserves are typically quite small

in relation to the potential death benefits, so claims would have to be paid mainly from assets that

match existing reserves, from “gains from operations” on blocks of policies without claims and on

other lines of business, and from assets matching surplus funds, net of payments from reinsurance.

On this basis, some companies would seem to be more vulnerable than others to a influenza

pandemic. For seven of the 25 largest writers of individual life insurance

25

, term insurance

constitutes three-fourths or more of the insurance in force. For another six, it constitutes between

half and three-fourths of the individual life in force. For the remaining dozen, term insurance

constitutes from 8 to 47 percent of their individual life insurance in force.

LIMRA’s data show that in 2004 only one household in three with a head under age 35 owned an

individual life insurance policy. Among the 35 to 44 age group, 46 percent did and over age 45,

roughly 60 percent of households owned individual life insurance. The mean death benefit from

individual life policies owned by all members of the household in 2004 was as follows:

Table 3: Individual Life Insurance Projected Death Claims, by Age Range, Severe Pandemic

Age range 25-34 35-44 45-54 55-64 65 and over

Projected deaths

26

378,650 268,600 44,000 123,450 526,700

Percent who own individual life

insurance

27%

43%

52%

46%

51%

Mean individual life insurance

benefit

$173,500

$400,250

$150,950

$126,200

$81,850

Projected claims (billions)

$17.5 $28.8 $2.3 $5.1 $5.1

Source for life insurance ownership data: LIMRA, Trends in Life Insurance Ownership Among U.S. Households, p. 18,

projected to benefits held in 2006.

24

These data apply the mortality rates experienced by these age groups in the 1957 and 1968 pandemics to the current U.S. population.

25

The unit of measure here is a corporate group, not a life insurance company. Virtually all life insurers are organized in groups, and it is assumed

that if one member of the group gets into financial trouble, the group will help. The calculations cited are based on data for 2004.

26

see footnote 26.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

10

The total projected death claims from individual life insurance, from a severe influenza pandemic as

derived from data in the preceding table, is $96.6 billion. It is heavily dependent on the mortality

pattern observed in 1918.

Table 4: Individual Life Insurance Projected Death Claims, by Age Range, Moderate

Pandemic

Age range 25-34 35-44 45-54 55-64 65 and over

Projected deaths

27

10,000 15,000 20,000 35,000 65,000

Percent who own group life

insurance

27%

43%

52%

46%

51%

Mean group life benefit

$173,500

$400,250

$150,950

$126,200

$81,850

Projected claims (billions)

$0.5 $2.6 $1.6 $2.0 $2.7

Source for life insurance ownership data: LIMRA, Trends in Life Insurance Ownership Among U.S. Households, p. 18,

projected to benefits held in 2006.

The total projected death claims from individual life insurance from a moderate influenza pandemic

as derived from data in the preceding table is $9.4 billion.

If a pandemic occurs, it might have some positive effects on books of individual life insurance

business. For example, policy lapses and surrenders would likely decrease drastically, as insureds

make every effort to keep their life insurance in effect in case they become infected and die. This

would be particularly significant for companies whose business focuses on whole life and universal

life, since often their payments for surrenders and lapses are larger than payments for deaths.

Furthermore, after the first wave of the flu had passed, there would likely be a substantial increase

in the number of people applying for new life insurance policies. In 1919, stories on the experience

of major life insurers routinely reported record sales in 1918, driven in part by people who came to

have a fresh appreciation of the value of owning life insurance. It is reasonable to expect similar

thinking after (and maybe during) an H5N1 pandemic.

However, with their surplus funds down from paying influenza claims, reinsurers raising rates

dramatically and wary of the effects of a second or third wave of the flu, at least some insurers may

be reluctant or financially unable to write many new policies. State regulators might have their

hands full dealing with insolvent insurers and calls for an industrywide reassessment of the

adequacy of risk-based capital requirements and measures of book-of-business risk. Many publicly

held insurers and reinsurers may find it necessary to raise additional capital from investors.

Individual life insurance

The preceding analysis does not take into account the effect of reinsurance arrangements these

insurers might have to protect against spiking claims levels. However, virtually all U.S. life

reinsurance is provided by 10 companies, all of which also have large books of business in other

countries, which might also be affected by a global influenza pandemic. Although these companies

are financially strong, there is no comparable previous experience against which to measure what

27

see footnote 30.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

11

might happen. Howell Pugh quotes one actuary as predicting that, if there is a pandemic on the

scale of the 1918 flu, “Reinsurers would drop faster than people.”

28

The analysis also ignores the effect of higher claims levels on the insurers’ income tax liability,

which would be driven down and in effect would become an additional source of funds for claims

payments. There might also be a drop-off in deaths from other causes; for example, if there were a

one- or two-month quarantine, motor vehicle-related deaths and work-related deaths might decline

during that period. But we should not take too much comfort from assuming a drop-off in deaths

from other causes. Indeed, the reverse might occur: Osterholm forecasts that an influenza

pandemic would create “shortages…of…medicines, including vaccines unrelated to the pandemic”

29

as well as shortages of hospital beds, medical equipment (such as mechanical ventilators) and

other material. Thus, deaths from nonflu illnesses might actually increase due to an influenza

pandemic.

Annuities

. The effect a pandemic has on annuities would vary depending on the type of annuity a

company sells. There are two basic types of annuities: deferred and immediate. Fundamentally,

deferred annuities are vehicles for accumulating money, while immediate annuities are vehicles for

paying money out. Most life insurers now derive a greater portion of their income and assets from

annuities than from life insurance.

Deferred annuities. Within the deferred annuity line of business, there are three basic types: fixed

annuities, equity-indexed annuities (which are a form of fixed annuities), and variable annuities.

One product feature that’s become popular in the last decade is a “guaranteed minimum death

benefit” (GMDB). The idea is that the annuity’s growth is tied to a stock or bond market fund. The

GMDB benefit assures annuity owners that if the market subsequently drops, the death benefit

remains at a level previously achieved when the market was higher. This creates a life insurance

amount at risk for the annuity company and there is some discussion in actuarial and regulatory

circles now as to appropriate reserves for this benefit.

There are at least three main designs for the GMDB and variations within each one. But the key

issue in the event of a pandemic is whether the stock market drops substantially after establishing a

particular level of death benefit and, if so, how much it drops and how long it stays down. As for the

effect on insurance companies that sell annuities with this feature, it depends, in the first instance,

on the extent to which buyers of a particular company’s product elected to add the GMDB feature

and how that feature is structured in those policies. There are no publicly available data that make it

possible to gauge any of these factors.

Immediate annuities. People who buy immediate annuities are generally over age 65 and are

interested in insuring themselves against the risk of “outliving their income.” In general, this group of

policyholders is healthier than the general population, since people in poor health would not have a

need for the product. Even among this healthier group, however, some people die earlier than

expected. When they do, some of the funds that might have gone to pay them an income go

instead to support the incomes of those who continue living, and some of those funds are profit for

the life insurance company.

28

Pugh, op. cit., p. 28.

29

Osterholm, op. cit., p. 32.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

12

Therefore, the effect of a influenza pandemic, particularly one that kills large numbers of people

over 65, could well be to increase the profits of life insurers on immediate annuity business.

Summary of the effect of a pandemic on life insurance companies

If the death pattern in the United States caused by an H5N1 influenza pandemic were to follow the

HHS severe forecast and the life insurance coverage situation remains as described above, it is

possible that the dollar value of death claims from the flu for group life insurance would be $58

billion and for individual life insurance $96.6 billion, for a total of $155.4 billion. As noted, this

depends heavily on the age pattern of deaths. At that level, every company’s surplus (the excess of

assets over liabilities) would “take a hit,” and dividends to policyholders and stockholders would

likely be cut, possibly to zero, for a year. Some companies—especially those most heavily into

group life insurance and individual term life insurance—might have to go into the capital markets to

raise additional funds for claims payments. Reinsurance might help, but since the life reinsurance

market is highly concentrated and all companies with reinsurance would be seeking

reimbursements at the same time, questions about some life reinsurers’ ability to pay will arise.

If, instead, the death pattern in the United States caused by an H5N1 influenza pandemic were to

follow the HHS moderate forecast and the life insurance coverage situation remained as described

above, it is possible that the dollar value of death claims from the flu for group life insurance would

be $5.2 billion and for individual life insurance $9.4 billion, for a total of $14.6 billion.

Other forecasts and studies

Risk Management Solutions, Inc. (RMS) in May 2004 estimated life insurance claims from an

influenza pandemic.

30

However, it created its own hypothetical mild outbreak, used unrealistic

assumptions (such as the ability to create a vaccine in a month), and derived a $9.1 billion total for

group and individual life insurance claims.

Standard & Poor’s released a report in November 2005 stating that, if there is a human influenza

pandemic, “every insurer might be at risk [but] on the life insurance side, it’s hard to determine the

exposure.” The majority of its report focuses on the property/casualty insurance industry.

31

A Fitch Ratings report, dated March 27, 2006, estimates that a moderate outbreak could cause

additional life insurance claims of $18 billion in the U.S.; this compares to our projection of $14.6

billion for that case.

32

The Fitch study is the first to estimate deaths and death claims in Europe from

a moderate outbreak: 400,000 deaths and claims of 20 billion British pounds.

On March 15, 2006 Morgan Stanley Equity Research published “Global Pandemic—Which Life

Insurers are Most Exposed.” The report took the industry analysis in an earlier version of this paper

30

Catastrophe, Injury, and Insurance: The Impact of Catastrophes on Workers Compensation, Life, and Health Insurance, Chapter 8 (Infectious

Disease), www.rms.com

. The November 2005 Best’s Review article that cited the RMS study (pp. 76-80) represents it as saying insured losses would

be $41 billion. That is correct, but it obscures the fact that $30.5 billion of the total are expected to be health insurance claims and another $0.25

billion are workers comp claims.

31

“Determining the Insurance Ramifications of a Possible Pandemic,” www.standardandpoors.com.

32

Bird Flu—Will It Ruffle The Industry’s Feathers? www.fitchratings.com

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

13

and extended it to focus on particular publicly-traded life insurance and reinsurance companies. The

report essentially follows and reinforces the analysis in this paper.

The Congressional Budget Office study released on December 8, 2005 and the update on May 24,

2006 focused on macroeconomic effects and did not estimate life insurance claims.

The January 2006 issue of Risk Alert, published by the Marsh & McLennan Companies, focused on

business continuity during an avian flu pandemic, and reviewed exposures under general liability,

workers’ compensation, and property insurance coverages.

33

Conclusion

Since the industry includes some companies that are financially very strong with conservative

balance sheets and others that are weaker with less conservative balance sheets, it is easy to

imagine that there could be some weaker companies that would struggle even if the industry as a

whole had adequate resources. The financially weakest companies probably would not survive a

severe pandemic, but these are generally small companies, with relatively few people insured. They

would be taken over by their home state’s insurance department, which would assess other

insurers operating in that state to make up any money needed to pay claims.

The H5N1 influenza pandemic would affect the U.S. life insurance industry in many ways beyond

death claims. As noted, it could shrink asset values, but this effect might be of short duration, since

the main effect of the outbreak might come and go in six to nine months (as two waves of the 1918

influenza pandemic did), and so the investment markets might rebound within a year of the flu’s

onset.

In the short term, a pandemic would likely affect insurers as employers, both because their

employees would miss workdays if they became sick—and some would die—and because the

workload would simultaneously increase dramatically, at least in the claims processing areas.

Communications, financial management and other functions would also have heavier workloads

both during the outbreak and afterward.

However, if the example of 1918 is any guide, in the year following the pandemic, a record number

of people would apply for new life insurance policies, vividly convinced of the value of the

protection.

33

Avian Flu: Preparing for a Pandemic, Volume V, Issue 1.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

14

Appendix A

Appendix A—The 1918 influenza Pandemic

The influenza pandemic in 1918 caused a dramatic spike in deaths in the United States and around

the world. The table below shows crude death rates

34

in the U.S. from influenza per 100,000 of

population for the six years preceding the influenza outbreak, for the year of the outbreak and for

the five years afterward.

Table 1: U.S. Crude Death Rates Per 100,000 Population Before, During and After the 1918

influenza Pandemic

Year 1912 1913 1914 1915 1916 1917 1918 1919 1920 1921 1922 1923

Rate

10.0 12.3 8.9 15.7 27.0 17.4 301.8 99.0 70.5 11.3 31.0 44.1

It seems evident from these data that the effect of the 1918 outbreak lingered at least into 1919 and

1920. According to Pugh, “the virus affected between 25 percent and 30 percent of the population.

The overall mortality rate was about 2.5 percent of those infected; hardest hit were pregnant

women. … For the entire United States, the death toll is estimated at more than 600,000.”

35

Normally, most influenza deaths occur among the very old and the very young, but the age

distribution of death rates from the 1918 influenza pandemic was different. The data below show

age-specific death rates per 100,000 for deaths from pneumonia or influenza. To indicate the effect

of the flu in 1918, we have shown rates for the year before and the two years after; we assume that

the only significant change from year to year was the occurrence of the flu.

Table 2: Age-Specific Death Rates Per 100,000 in Age Group from Influenza and Pneumonia

Before, During and After the 1918 influenza Pandemic

Age

Group/

Year

Under

1

1 to 4 5 to

14

15 to

24

25 to

34

35 to

44

45 to

54

55 to

64

65 to

74

75 to

84

85 and

over

1917

1474.5 211.5 24.0 38.9 59.3 98.1 148.8 281.8 614.6 1503.0 3187.4

1918

2273.3 718.0 176.2 580.5 992.6 554.8 347.8 381.9 646.3 1179.0 2230.6

1919

1594.2 293.9 63.3 141.4 235.9 181.0 163.9 233.2 450.6 913.9 1842.2

1920

1495.0 283.7 45.1 101.3 180.6 164.0 164.9 255.8 545.9 1191.3 2379.1

We can make at least two interesting observations from these data.

For people 65 and over the death rates from pneumonia and influenza in 1918,

1919 and 1920 actually went down compared to the rates for that age group in the

1917 base year.

36

34

A “crude death rate” in a year is simply number of deaths that year divided by the average number of people alive that year. It is not adjusted for

age, sex or other characteristics that could affect the number from year to year, so comparing one year to another should be done cautiously.

However, it is unlikely that the population characteristics changed so substantially from one year to the next that these data cannot be useful for

indicating the effect of the flu pandemic.

35

Howell Pugh, “Pandemic: The Cost of Avian Influenza,” Contingencies, September/October 2005, p. 24.

36

Of course, in 1918 the over-65 population in the United States constituted a much smaller percentage of the total population than it does today. As a

result, only one percent of deaths in the U.S. from the 1918-19 influenza pandemic were people over 65.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

15

In 1919 and 1920 the death rates from pneumonia and influenza returned to

roughly their 1917 levels for children under age 5 and for adults 45 and over.

However, the death rates remained elevated in 1919 and 1920 (compared to 1917

rates) particularly for the 15 to 24 and 25 to 34 age groups, and, to a lesser extent,

for the 5 to 14 and 35 to 44 age groups.

Max Rudolph notes that “other flu outbreaks have had fewer than 10 percent of the deaths at ages

16 to 40. In 1918 over half the deaths occurred in this age range, with ages 21 to 30 the worst hit.”

37

Furthermore, as John M. Barry points out:

Those most vulnerable of all to influenza, those most likely of the most

likely to die, were pregnant women. … In thirteen studies of hospitalized

pregnant women during the 1918 pandemic, the death rate ranged from

23 percent to 71 percent. Of the pregnant women who survived, 26

percent lost the child. And these women were the most likely group to

already have other children, so an unknown but enormous number of

children lost their mothers.

38

As in any data collection/analysis exercise, it is good to see the forest as well as the trees. About

the 1918-19 pandemic, Rudolph writes:

The 1918 influenza strain appears to have left residual effects on many

who recovered, leaving them tired and susceptible to heart and

neurological problems. Many who had flu died early in 1919 of

secondary causes and were not recorded as flu deaths.

39

With people in the prime life insurance buying ages so affected by this influenza, was the life

insurance industry financially challenged? Buley reported that:

Some of the companies showed as high as 245 percent of expected

mortality as compared to 54 percent for the highest October in the

preceding six years; the New York Life for the last three months of 1918

showed 188 percent of expected mortality or 95 percent for the year, the

highest in the recorded history of the company. A number of companies

had greater losses from the influenza in the month of October than from

war losses since the beginning of the war. Actuaries estimated that to the

end of the year the legal reserve life insurance companies paid

$110,000,000 in influenza and pneumonia claims, and that it would be

five years before mortality averages would be restored to normal. Since

37

Max J. Rudolph, “Influenza Pandemics: Are We Ready for the Next One?” Risk Management, July 2004, p. 28. However, John Barry suggests that

the elderly population fared unusually well not because the virus affected mainly younger people but because the elderly had had immunity from a

decades-earlier flu wave. See John M. Barry, The Great Influenza: The Epic Story of the Deadliest Plague in History, Penguin Books, p. 408.

38

Ibid., pp. 239-40.

39

Rudolph, op. cit., p. 27.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

16

about one-fourth of the death policies were new—had paid only two or

three premiums—reserves were depleted and dividends were passed.

40

Did any life insurer fail? It is hard to tell. Buley notes:

Some of the insurance journals contained suggestions to the effect that

the younger life insurance companies were facing bankruptcy. … The

Insurance Press of New York in an editorial entitled “Get Well Without

Doctors” stated that some of the “smaller and younger life insurance

companies made appeals for [state insurance] departmental aid.”

Pfeffer and Klock summarized that:

life insurance benefits vastly exceeded premiums that had been collected.

New companies were so severely affected that reserve practices and

patterns of reinsurance were tightened to a degree never before

observed. That this catastrophe was not even more financially disastrous

is attributable to the enormous spread of the business risk and to the fact

that most policyholders had relatively small policies in force.

41

Nevertheless, “about three quarters of the companies either omitted or reduced their dividend.”

42

Several other reasons account for why the influenza pandemic did not hit the life insurance industry

harder than it actually did.

It is possible that some men bought government life insurance instead of buying from

private life insurance companies, thereby blunting the effect of influenza deaths on the

industry.

There was virtually no group life insurance then.

Life insurance, when it was bought at all, was generally bought for funeral/burial purposes,

so the death benefit amounts were relatively small. (The concept that people should buy

life insurance to protect their “human life value”—that is, the present value of their income-

earning capacity—had been published by a young professor, S.S. Huebner, at the

University of Pennsylvania only seven years before the outbreak began.)

At the end of April 1917, just after the United States entered World War I, with the support

of the National Convention of Insurance Commissioners, life insurance companies were

advised to insert a military clause in new policies and to charge an extra $37.50 per $1,000

(or more) of insurance. The extra premium was to be collected starting 31 days after

entering service, and was not to be returned if death occurred as a result of military service

(though regular premiums were, in lieu of the stated death benefit).

43

However, many

40

R. Carlyle Buley, The American Life Convention: 1906-1952 A Study in the History of Life Insurance, Appleton-Century-Crofts, 1953. Vol. 1, p.

538.

41

Irving Pfeffer and David Klock, Perspectives on Insurance, Prentice-Hall, 1974, p. 48.

42

Rudolph, op. cit., p. 30.

43

Buley, op. cit., p. 491. Without knowing what the “military clause” said it is hard to know its effect. If it excluded coverage for death while in the

military, without regard to death by hostile action, then the life insurance bought after the clause was inserted by soldiers who died of the flu would

have returned the premiums instead of paying the death benefit, thereby lessening the life insurer’s exposure to influenza deaths.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

17

policies written before 1915 contained no different treatment for deaths related to military

service.

44

In October 1917, the U.S. Congress passed, and President Wilson signed, a government

life insurance program for men in the U.S. military. “By May [1918] there were more than

2,000,000 policies with a total of almost $17,000,000,000 of insurance. Whereas it had

been estimated that the average policy would be for $2,500 it came to $8,200. Applications

were increasing at the rate of $150,000,000 per day. Already the insurance in force

exceeded that of the five largest life insurance companies combined.”

45

“At the time of the

Armistice [November 11, 1918] the War Risk Bureau had written 4,152,767 life insurance

policies for a total of $36,348,849,500.”

46

On the other hand, financing the war took resources that the life insurance industry might have

had available for influenza-related deaths. On October 3, 1917, Congress passed a bill with an

excess profits tax with rates ranging from 20 to 60 percent and a tax of 8 cents on each $100, or

fraction thereof, of life insurance. Furthermore, companies were “passing up investments on

bonds yielding 5½ to 6½ percent for Liberty Bonds yielding half as much, making donations to Red

Cross and other organizations.”

47

The bottom line? “No beneficiary of a single policyholder had been compelled by any legal reserve

life insurance company to wait a single day for payment beyond the necessary time for filing proof

of death.”

48

Disability effects of the flu

Barry asserts that the 1918 flu caused severe mental problems to many who caught yet survived

the flu. He writes:

[To physicians in 1918,] the connection between influenza and various

mental instabilities seemed clear. … Contemporary observers also linked

influenza to an increase in Parkinson’s disease a decade later. … and in

1926, Karl Menninger studied links between influenza and schizophrenia.

His study was considered … a “classic” article. … Menninger spoke of the

‘almost unequalled neurotoxicity of influenza….’ In 1927 the American

Medical Association’s review of hundreds of medical journal articles from

around the world concluded, ‘There seems to be general agreement that

influenza may act on the brain. … From the delirium accompanying many

acute attacks to the psychoses that develop as ‘post-influenzal’

manifestations, there is no doubt that the effect of the influenza virus on

the nervous system is hardly second to its effect on the respiratory tract.

49

44

Ibid., p. 488.

45

Ibid., p. 523.

46

Ibid., p. 542.

47

Ibid., pp. 507-8. Buley comments that “the excess profits tax as of doubtful validity since wars yielded life insurance companies no profits, and the

tax on undistributed income as of questionable soundness since it would tend to prevent companies from accumulating contingency reserves in a

period in which many would suffer losses on policies not containing war clauses.”

48

Ibid., p. 540, quoting Blackburn, secretary of the American Life Convention, in a letter to the editor of the Insurance Press.

49

Barry, op. cit., pp. 378-80.

Insurance Information Institute

110 William Street New York, NY 10038

(212) 346-5500 www.iii.org

18

Appendix B

The 2003 SARS outbreak

In early 2003, the world was focused on a potential pandemic from another virus, Severe Acute

Respiratory Syndrome (SARS, or, more formally, SARS-associated coronavirus). That virus was

contained fairly quickly and is no longer perceived as a threat.

50

Consequently, it’s natural to ask

why an H5N1 influenza that mutates into a strain that allows person-to-person transmission poses a

threat. Why, in other words, will it not be contained as SARS was?

The SARS experience isn’t a useful model on which to base expectations regarding the H5N1

threat. This is because the SARS virus was a coronavirus, not an influenza virus. “Coronaviruses

(the cause of the common cold as well as SARS), parainfluenza viruses and many other viruses all

cause symptoms akin to influenza, and all are often confused with it. As a result, sometimes people

designate mild respiratory infections as ‘flu’ and dismiss them. But influenza is not simply a bad

cold. It is a quite specific disease….”

51

SARS was less dangerous than influenza virus for at least three reasons. “First, SARS requires

close contact to spread, while influenza is among the most contagious of all diseases.”

52

The

Centers for Disease Control and Prevention (CDC) defines “close contact” as “having cared for, or

lived with, someone with SARS or having direct contact with respiratory secretions or bodily fluids of

a patient with SARS. … Close contact does not include activities like walking by a person or briefly

sitting across a waiting room or office.”

53

“Also, in SARS, the virus reaches maximum concentration in the upper respiratory tract, where

coughs and sneezes are most likely to spread the virus, a week or longer after symptoms develop.

This gives public health officials time to find, identify, and isolate cases.” “[P]ersons with SARS are

most likely to be contagious only when they have symptoms, such as fever or cough.”

54

“By

contrast, the influenza virus can spread from person to person before any symptoms develop,

before a victim knows he or she is sick.”

55

And it lodges more deeply into the lungs. Further, “SARS

tended to spare children, rarely causing severe illness, and was never considered a paediatric [sic]

disease.”

56

The World Health Organization summarizes the comparison of SARS versus an influenza outbreak

as follows: “Many of the public health interventions that successfully contained SARS will not be

effective against a disease that is far more contagious, has a very short incubation period, and can

be transmitted prior to the onset of symptoms.”

57

In sum, “many of the public health interventions that successfully contained SARS will not be

effective against a disease that is far more contagious, has a very short incubation period [unlike

SARS], and can be transmitted prior to the onset of symptoms [unlike SARS].”

58

50

Centers for Disease Control and Prevention (CDC) SARS Web site, http://www.cdc.gov/ncidod/sars/, “Basic Information about SARS.”

51

Barry, op. cit., p. 102.

52

Ibid.

53

CDC, op. cit.

54

Ibid., “Frequently Asked Questions about SARS”

55

Barry, op. cit.,. pp. 449-50.

56

World Health Organization, Avian influenza: assessing the pandemic threat, January 2005, p 9.

57

Ibid, p. 19.

58

World Health Organization, Avian influenza: assessing the pandemic threat, January 2005, p. 19.