Annual Income

Single Family Housing Guaranteed Loan Program

1

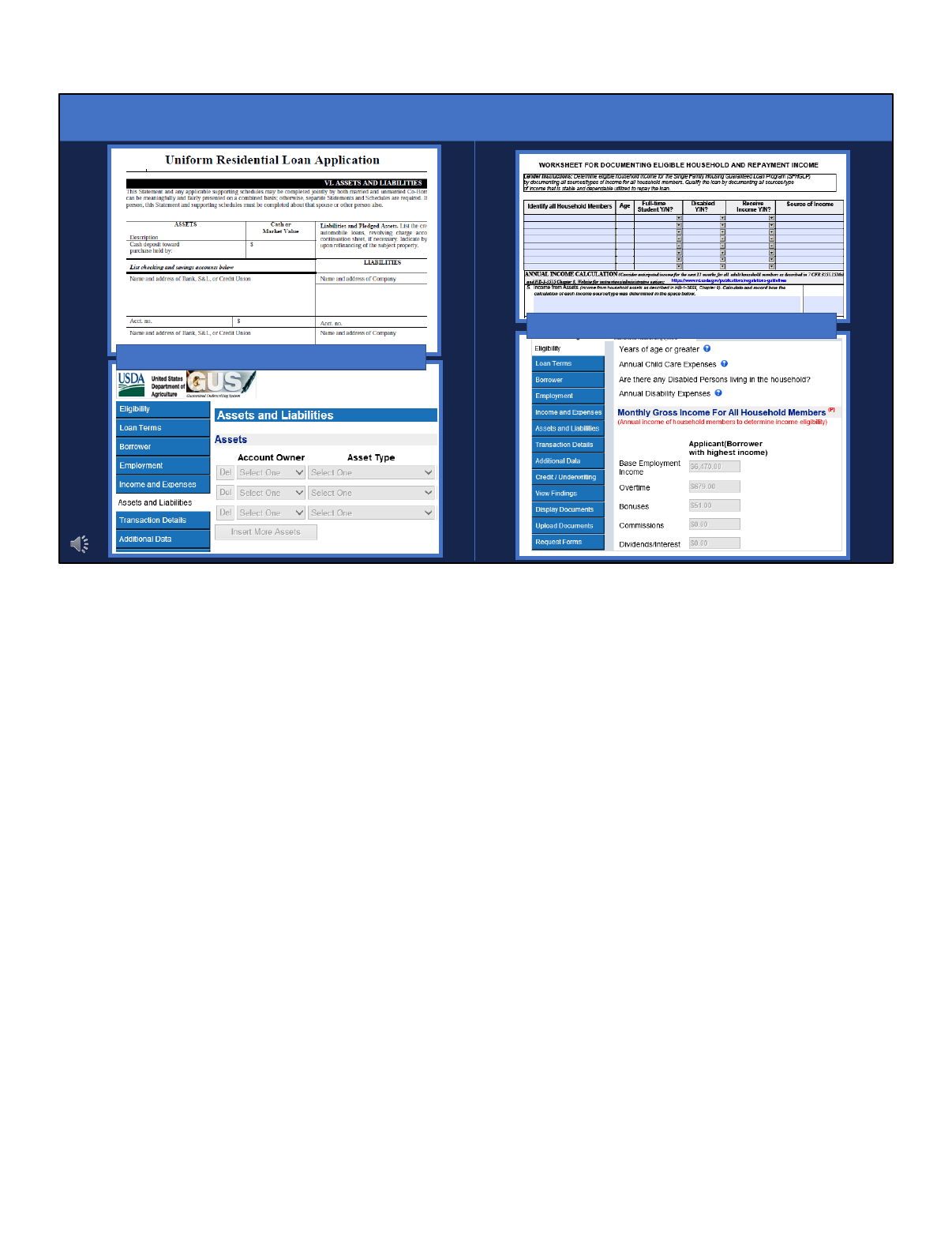

Assets

Single Family Housing Guaranteed Loan Program

(SFHGLP)

09/2020

Welcome to the Assets online training module presented by USDA’s Single Family Housing

Guaranteed Loan Program.

1

2

Verify

Document

Calculate

ASSETS

Assets are an important piece of an applicant’s financial puzzle. Understanding different

asset types and how they affect your applicant’s single-family housing guaranteed loan is

essential. This module will assist you in determining how to verify and document assets

and how to calculate asset income when necessary.

2

3

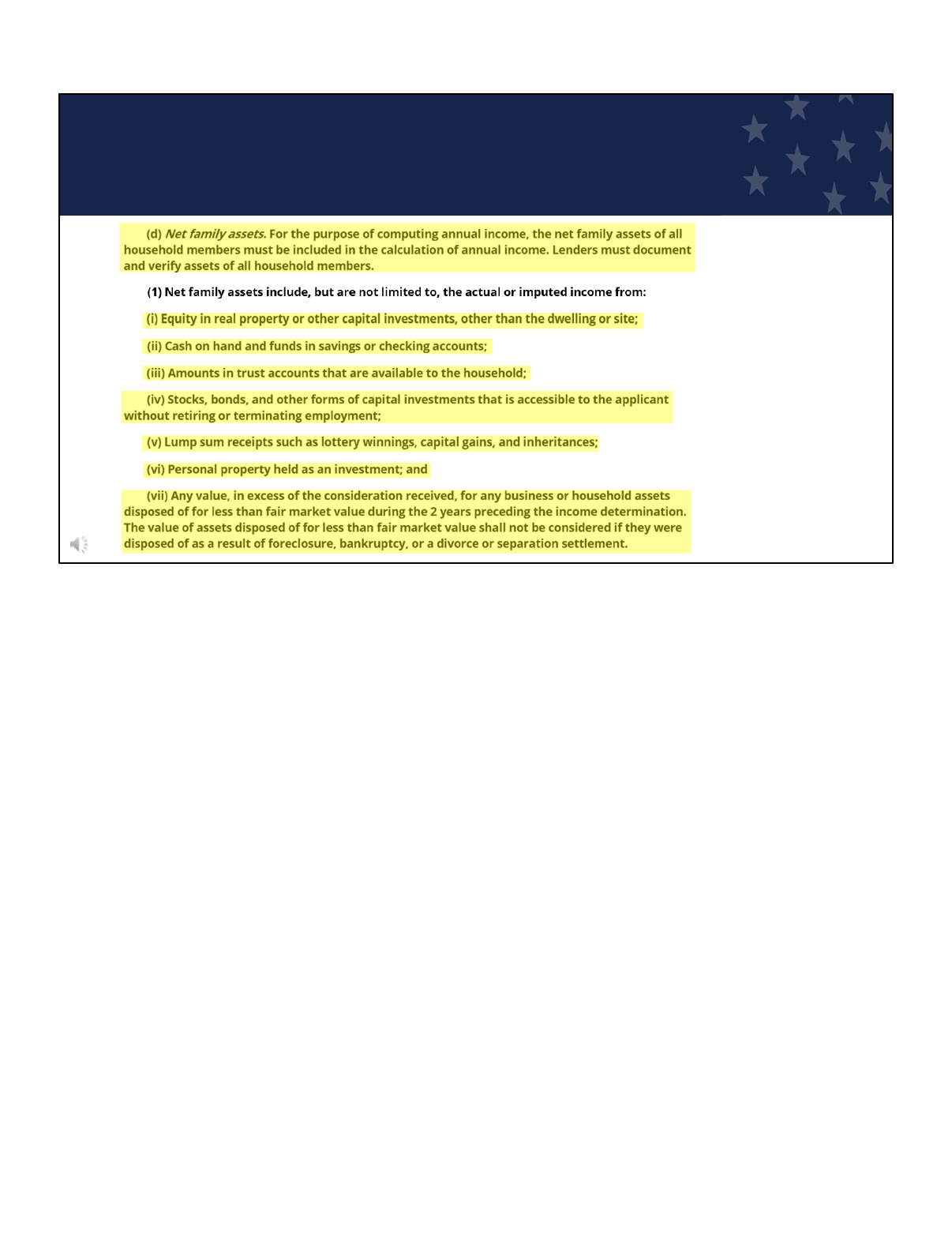

7 CFR Part 3555: 3555.152 (d)

• 3555.152(d) requires net family assets of all household members (adults age 18 and up)

to be included in the calculation of annual income.

• It is specifically the income derived from the net family assets that must be included in

the annual income calculation.

• This income may be derived from equity in real property, cash on hand and funds in

savings and checking accounts, trust account funds available to the household, and non-

retirement investments.

• Other net family assets that may derive income include lump sum amounts, personal

property that is held as an investment, and any asset disposed of for less than fair

market value during the preceding two years, unless the assets were disposed of as a

result of foreclosure, bankruptcy, divorce or separation settlement.

3

4

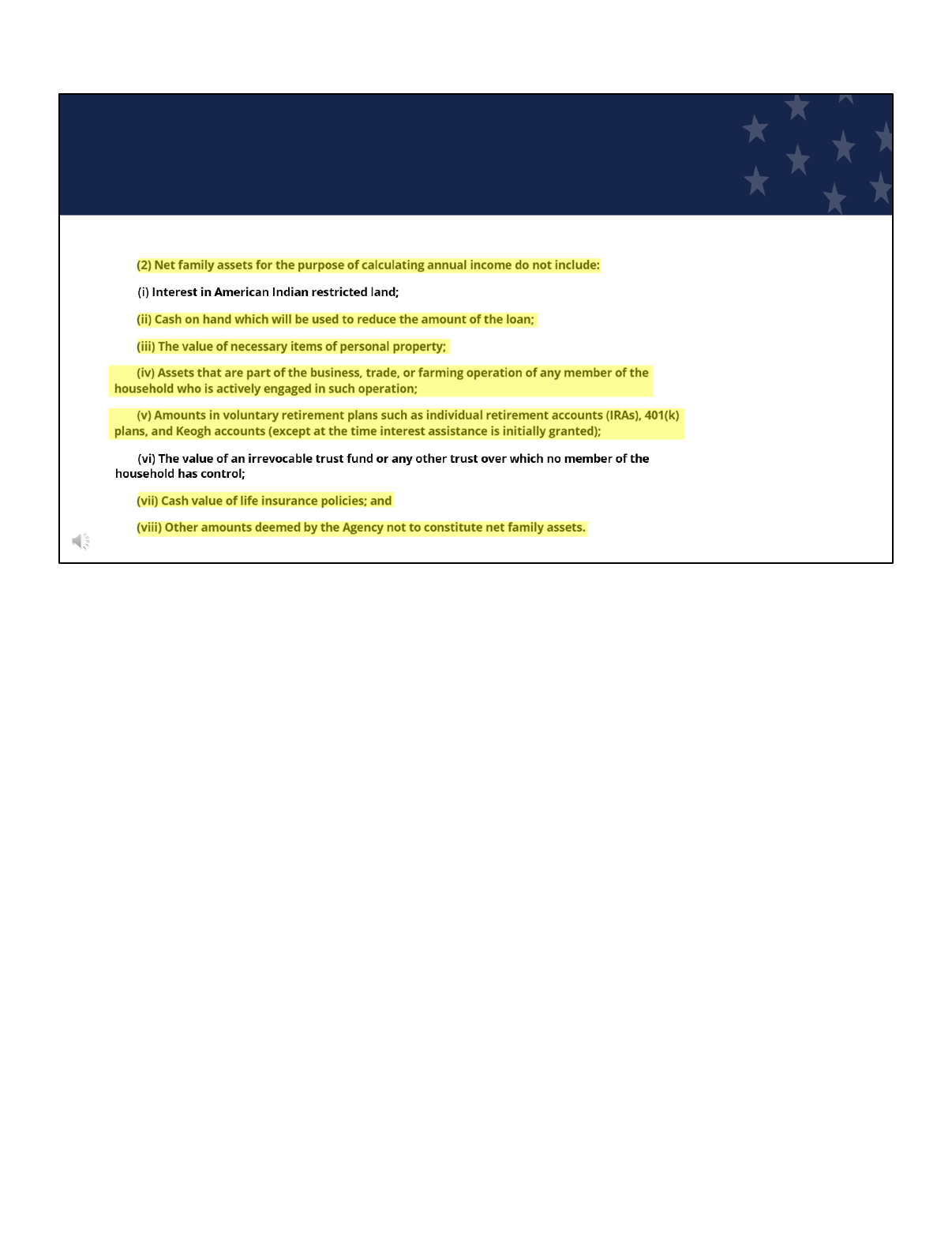

7 CFR Part 3555: 3555.152 (d)

• 3555.152(d)(2) lists net family assets that do not have to be considered in the annual

income calculation.

• These include assets such as cash on hand that will reduce the loan amount, personal

property, and business assets.

• Other net family assets that are excluded when calculating annual income include

voluntary retirement accounts, cash value of life insurance policies, and any other

amount deemed by the agency not to constitute net family assets.

4

5

7 CFR Part 3555: 3555.152 (d)

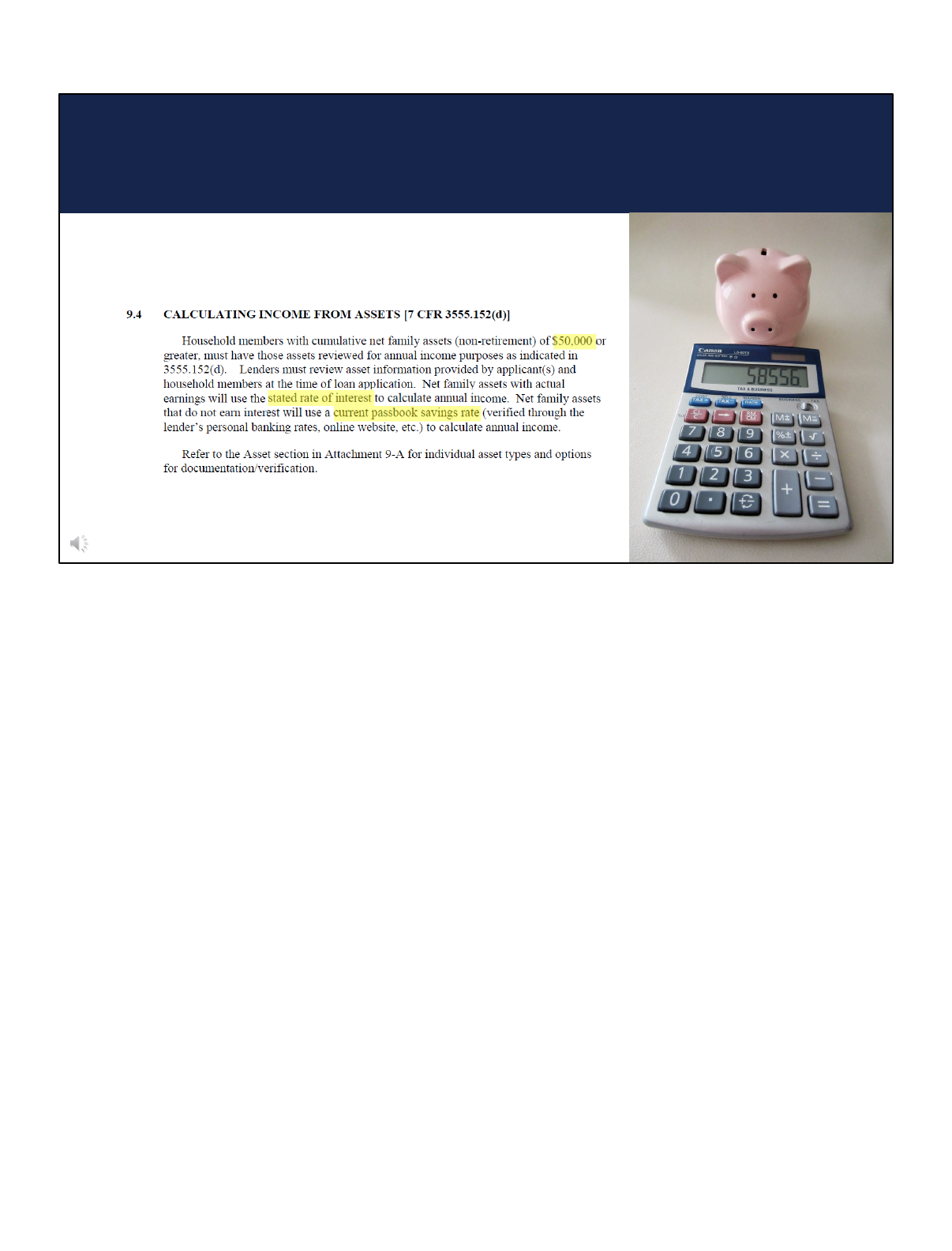

When is an asset calculation required?

• An asset calculation must be performed when the household has cumulative net family

assets of $50,000 or more.

• If the total value of eligible assets is less than $50,000, then no calculation is required to

be added to the annual income calculation.

• If the total value is $50,000 or more, then the lender must use the greater of actual

income earned on the asset, or perform a calculation utilizing a passbook savings rate.

• An asset earning zero interest will require a local passbook savings rate.

5

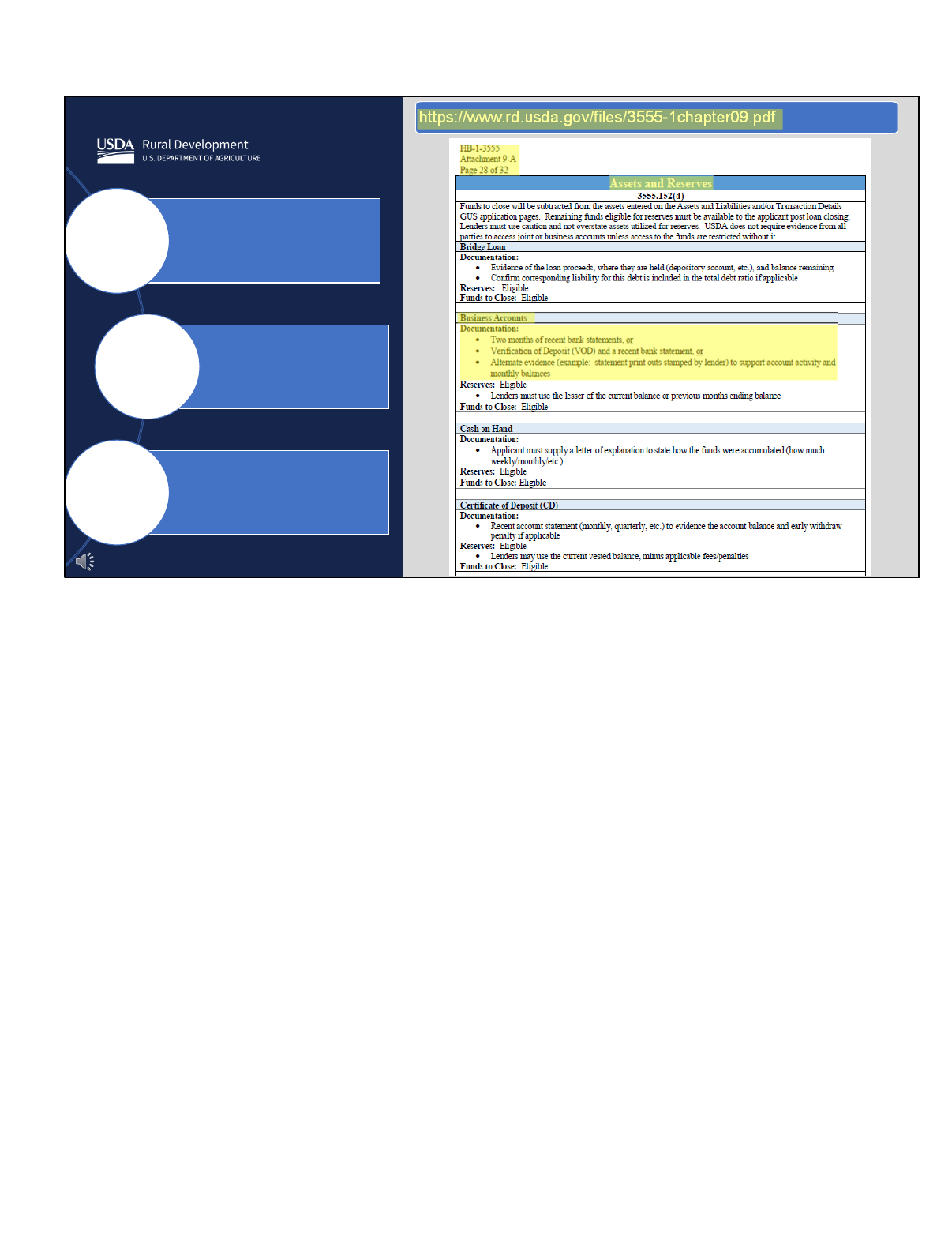

https://www.rd.usda.gov/files/3555-1chapter09.pdf

6

Review Attachment 9-A

Pages 28-32

Verify & Document

Calculate Asset Income

If cumulative total is

$50,000 or more

• To better assist with income review and documentation, Chapter 9 includes Attachment 9-A:

“Income and Documentation Matrix.”

• The matrix was designed to assist lenders and USDA in efficiently locating many income sources,

annual income adjustments, and asset guidance.

• Pages 28-32 specifically address Assets and Reserves.

• Under each asset type there are documentation options to assist the lender when obtaining a

complete loan file and to support their calculations.

• Please note that not every documentation item listed is required.

• USDA is providing flexibility to the lender to determine the best documentation option.

6

7

7 CFR Part 3555: 3555.152 (d)

Things to keep in mind:

• Income from eligible assets may be

required to be included in annual income.

• Assets are considered a compensating

factor which do impact underwriting

recommendations in the GUS.

• Lenders will determine if assets are to be

included in the underwriting analysis.

When reviewing the assets of an applicant and other adult household members please

keep the following in mind:

• Income from eligible assets may be required to be included in the annual income

calculation. The technical handbook provides flexibility in asset amounts held by the

household to help determine when a calculation is required.

• Assets are important because they may be a compensating factor. Compensating factors

strengthen the loan file and may affect underwriting recommendations rendered by GUS.

• Assets documented by the lender are not required to be included in the loan application.

If a lender wishes to obtain a conservative underwriting recommendation or perform a

conservative underwriting analysis, the assets do not have to be included on the loan

application. However, the lender must include income from an asset in the annual income

calculation, if applicable.

7

8

Asset Verification is Always Required!

Required (if over $50,000)

Optional

• Lenders are not required to enter assets on the loan application or on the “Asset and

Liabilities” page in GUS.

• Lenders may underwrite the loan or receive an automated underwriting

recommendation that does not consider the assets as a compensating factor.

• But when the assets exceed the acceptable threshold as indicated in the regulation and

technical handbook then the income earned from the asset must be included on the

income worksheet submitted to USDA and on the GUS “Eligibility” page.

• It is important to be aware that asset verification is still required even when the amount

falls below the threshold requiring it to be used in GUS or entered into the URLA.

8

9

7 CFR Part 3555: 3555.152 (d)

Asset Inflation

• Invalid GUS underwriting

recommendations

• Invalid compensating factors

• Inaccurate annual income

calculation

• Potential fraud

• When assets are utilized in GUS or in manual underwriting it is important that the assets

are not inflated.

• Inflated assets will result in: Invalid GUS underwriting recommendations, invalid

compensating factors, inaccurate annual income calculations, and potential fraud.

• When assets are inflated or incorrectly calculated to achieve a GUS Accept underwriting

recommendation or loan approval, it will impact the validity of the Loan Note

Guarantee, loss claim payment, etc.

9

10

7 CFR Part 3555: 3555.152 (d)

Example: Calculating Income from Assets

• Checking account (non‐interest bearing): $17,000

• Savings account (.25% interest): $24,000

• Certificate of Deposit (3% interest): $15,000

Total Assets: $56,000 less $5,000 from checking used to

purchase the home

Remaining Assets = $51,000

• This is an example of when and how to calculate assets to be included in the total

household annual income.

• This applicant has a non-interest bearing checking account with a balance of $17,000 as

well as a savings account that earns .25% interest annually with a balance of $24,000.

• The applicant also has a Certificate of Deposit that earns 3% annual interest with a

current balance of $15,000.

• The applicant will use $5,000 from checking towards the purchase of the dwelling.

• The total of all eligible non-retirement assets is $56,000, minus the $5,000 that will be

used to purchase the home, bringing the remaining balance of assets to $51,000.

• This is more than the $50,000 threshold, therefore an income calculation is required.

10

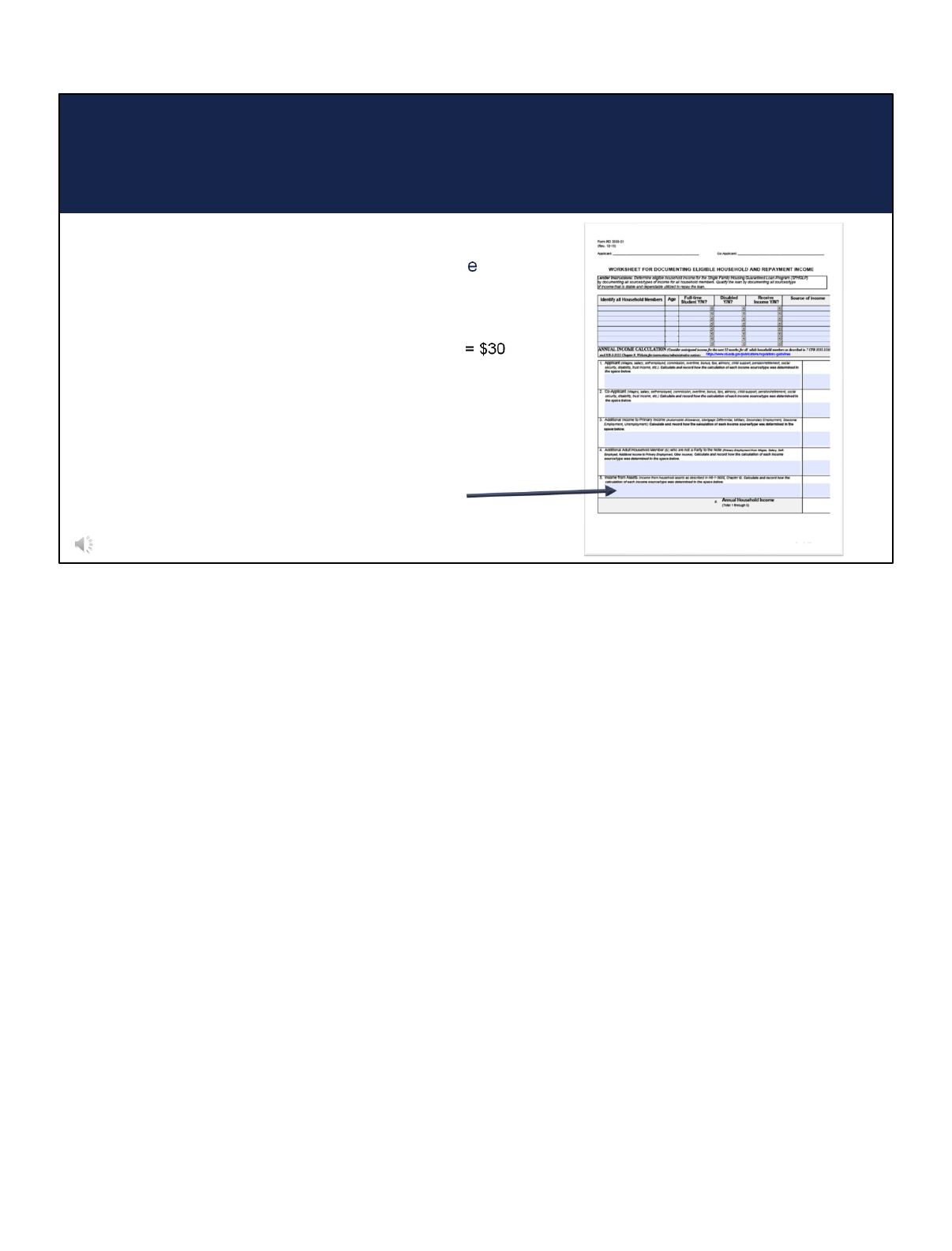

11

7 CFR Part 3555: 3555.152 (d)

Example (continued): Calculating Income

from Assets

• Checking: $17,000 ‐ $5,000 = $12,000 x .25% = $30

• Savings: $25,000 x .25% = $62.50

• CD: $15,000 x 3% = $450

Asset Calculation: 30 + 62.50 + 450 = $542.50

Include $542.50 in annual income calculation

• Continuing with the example from the previous slide, the checking account is

non-interest bearing and will have $12,000 remaining after closing costs are deducted.

• We will assume the passbook savings rate for this example is .25%.

• This results in $30 of interest.

• The savings account is earning .25% interest, which equals $62.50 of interest.

• The CD will earn $450.

• Add these calculations together and you get $542.50 of interest income that must be

included in the annual income calculation.

11

12

7 CFR Part 3555: 3555.152 (d)

Average Asset vs. Current Balance

• January Average Balance: $4,534.52

• February Average Balance: $354.23

• Current Balance: $1,456

• Two-month Balance: $2,444.38

Current Balance: $1,456

• When considering asset balances, any fluctuation should be evaluated carefully.

• In this example, the applicant had a balance of over $4,000 in January, the balance fell

below $400 in February, and then increased to $1,456 for the current reported balance.

• The two-month average balance for January and February is $2,444.38, which is more

than the current balance of $1,456.

• The lessor of the two figures, in this case, $1,456, should be used.

12

13

LEARNING CHECKS

7 CFR Part 3555 / HB-1-3555

The best way to learn information is to test your knowledge!

13

14

• Question will be bulleted with scenario, or

• Include a statement/question

TRUE/FALSE or other answer options will be displayed

QUESTION

Topic

The following question slides will list:

• The topic,

• A question or scenario, and

• potential responses.

14

15

Answer Slide

ANSWER

Topic

7 CFR Part 3555 and HB-1-3555 references provided

X. Correct Response

• Additional guidance for clarification may be provided

The answer slides will list:

• The topic,

• the reference to the answer from the regulation and handbook,

• the correct response, and

• any additional clarification that may be helpful.

15

16

LET’S GET

STARTED!

Ready?

Let’s get started!

16

17

QUESTION

Assets

Which of the following assets may be required in the annual income calculation?

SELECT ALL THAT APPLY:

A. Checking account

B. Net proceeds from sale of current home

C. Certificate of deposit

Read the question on the slide and select a response.

17

18

ANSWER

Assets

3555.152(d)(1), HB 9

A. Checking account

B. Net proceeds from sale of current home

C. Certificate of deposit

All of the above must be considered when determining the annual income

calculation.

• Answer: All of the Above.

• Each of the assets listed must be considered when evaluating the total household

annual income.

18

19

Which assets are excluded from a conventional credit test?

SELECT ALL THAT APPLY:

A. Checking account

B. Antiques and collectibles

C. Savings account

D. 401k/Retirement accounts

QUESTION

Assets

Read the question on the slide and select a response.

19

20

3555.152(d)(2), HB 9

• B. Antiques/Collectibles

• D. Retirement Plan

Exclude personal property such as antiques and collectibles, as well as

funds in a voluntary retirement account.

ANSWER

Assets

• Answer: B and D

• For the purpose of calculating annual income, net family assets do not include the value

of necessary items of personal property nor do they include amounts placed in a

voluntary retirement plans

20

21

QUESTION

Assets

What is the asset threshold when a calculation is required for annual income?

A. $5,000

B. $20,000

C. $50,000

D. $10,000

Read the question on the slide and select a response.

21

22

ANSWER

Assets

3555.152(d)(1), HB 9.4

C. $50,000

Net family assets of $50,000 or more must be reviewed for annual income

purposes.

• Answer: C. $50,000

• Household members with combined net family assets of $50,000 or more must have

those assets reviewed for annual income purposes.

• Lenders must review asset information provided by the applicant and other household

members at the time of loan application.

• Net family assets which have actual earnings will use the documented rate of interest to

calculate annual income.

• Net family assets that do not earn interest will use a current passbook savings rate to

calculate the annual income.

• Current passbook savings rates may be found through the lender’s own banking rates or

by an online website for current savings rate in the area.

22

23

QUESTION

Assets

Lenders must enter all assets into the GUS “Assets and Liabilities” application

page and the 1003 loan application.

A. TRUE B. FALSE

Read the question on the slide and select a response.

23

24

ANSWER

Assets

3555.152(d)(1), HB 9

B. FALSE

Assets are not required to be entered in GUS or on the URLA if below the

acceptable threshold

• Answer: B. False

• Lenders are not required to enter assets into the GUS or on the loan application.

• The lender may underwrite the loan or obtain an underwriting determination in the GUS

without assets being included as a compensating factor.

• However, when the net family assets exceed the acceptable threshold as indicated in

HB-3555, Section 9.4, then the income earned from the assets must be included as

annual income.

• Again, it is important to note that the lender is always required to verify the assets,

regardless of the amount or the exclusion in the GUS or on the URLA.

24

25

• Checking: $1,500, non‐interest, local passbook savings rate is .25%

• Savings: $15,000, earns .50% annually

• Certificate of Deposit: $65,000, earns 2% annually

What amount of income must be added to annual income?

A. $1,378.75 B. $0

QUESTION

Assets

Read the question on the slide and select a response.

25

26

3555.152(b)(4), HB 9

A. $1,378.75

• Assets are $50,000 or greater

− $1,500 x .25% (passbook rate)= $3.75

− $15,000 x .50% = $75.00

− $65,000 x 2% = $1,300

• $3.75 + $75.00 + $1,300 = $1,378.75

ANSWER

Assets

• Answer: A

• The total assets are greater than $50,000.

• Therefore, the greater of the actual income earned or a local passbook savings rate must

be used for the calculation.

• The $1,500 checking is non-interest bearing.

• Therefore the local passbook savings rate of .25% will be used, which equals $3.75

• The $15,000 savings earns .50% for an annual total of $75.00

• The $65,000 CD earns 2% for an annual amount of $1,300.

• Add these together for a total of $1,378.75. This amount must be included in the

household annual income.

26

27

Which of the following assets can be excluded when calculating annual

household income?

SELECT ALL THAT APPLY:

A. IRA Account

B. Money Market Savings Account

C. Trust Fund Controlled by Borrower’s Grandfather

D. $2,500 Lotto Winnings

E. 50 Shares of Stock Interest

QUESTION

Assets

Read the question on the slide and select a response.

27

28

3555.152(d)(2), HB 9

A. IRA Account

C. Trust Fund Controlled by Borrower’s Grandfather

D. $2,500 Lotto Winnings

Excluded assets include retirement accounts, trust funds that are not controlled by

a household member, and lump sum/one-time payments that are nonrecurring.

ANSWER

Assets

• Answer: A. IRA Account, C. Trust fund controlled by borrower’s grandfather, and D.

$2,500 lotto winnings.

• The IRA account is a retirement fund and therefore excluded from the income

calculation.

• Trust funds that are not controlled by the household are also excluded because the

borrower cannot actively access the funds at any time.

• Lump sum additions to the household assets that are nonrecurring are also not

considered in the annual income calculation.

• The lender should review the bank statements to ensure that winnings from gambling,

the lottery, or other such ventures are not occurring on a regular basis.

28

29

LEARNING CHECK

COMPLETED!

Way to Go!

Way to go! You have completed the learning checks!

29

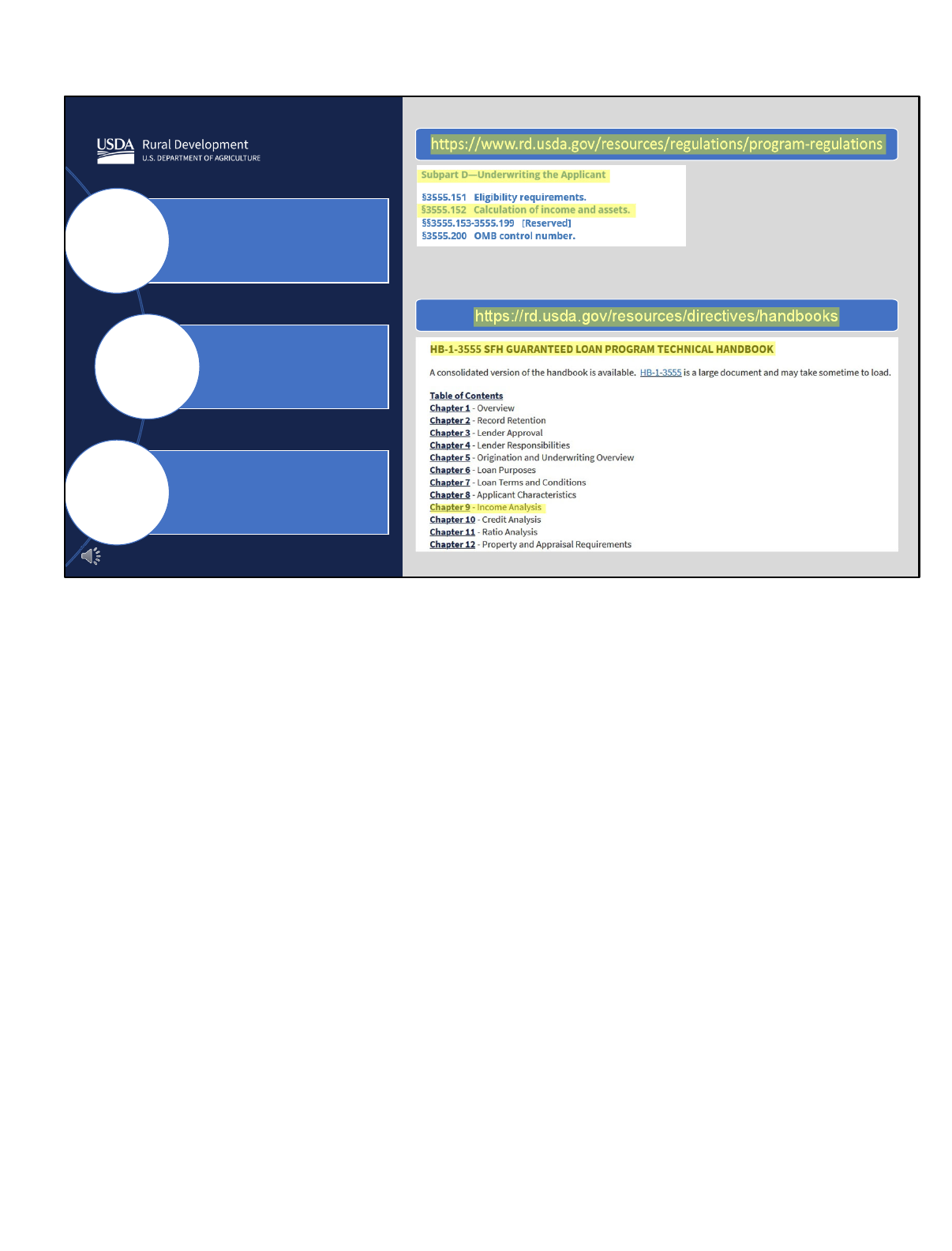

https://www.rd.usda.gov/resources/regulations/program-regulations

30

https://rd.usda.gov/resources/directives/handbooks

Navigate through these

resources and tools like

an expert!

Take the “Program

Overview Training”

Available on the USDA

LINC:

https://www.rd.usda.gov/page/u

sda-linc-training-resource-

library

• This training module has provided you with an overview of the key requirements of assets and

asset income.

• Complete program requirements and guidance can be found in 7 CFR Part 3555, Subpart D,

Section 3555.152(d) and Chapter 9, Paragraph 9.4 of HB-1-3555.

• Be sure to bookmark these references, save yourself valuable time by using Cntrl-F to quickly

search and find answers, and always ensure you are referencing the most current publications.

• The “Program Overview Training” module will assist you in learning how to navigate through all

the resources and tools Rural Development has created to assist you.

30

31

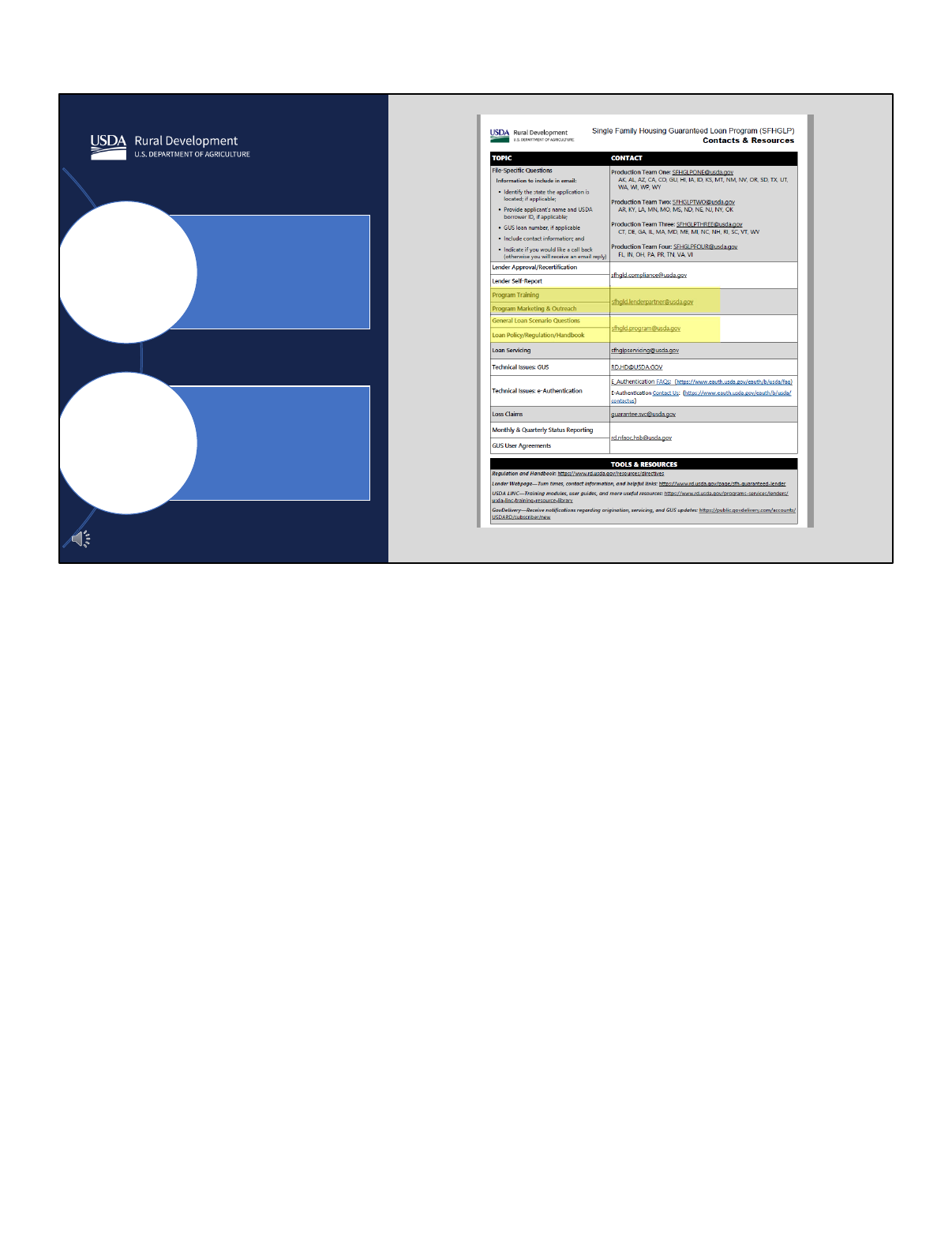

Can’t find your

answer in the

regulation or

handbook?

Contact the PAC

team!

Want additional live

program training?

Contact the LPA

team!

• Users should first look for answers to their questions in the regulation and handbook,

but if you still have a question after reviewing your resources, we’re here to help.

• All policy and regulation questions regarding the topic we just covered should be sent to

our Policy, Analysis, and Communications Branch and

• If you would like to request additional program training, contact our Lender and Partner

Activities Branch.

31

32

Thank you for supporting the USDA Single Family Housing Guaranteed Loan Program and America’s

rural homebuyers!

32

33

www.rd.usda.gov

1 (800) 800-670-6553

USDA is an equal opportunity provider, employer, and lender.

This will conclude the training module. Thank you and have a great day!

33