QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

1 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

BACKGROUND

The Department of Housing and Urban Development (HUD), Office of Housing Voucher

Programs, Quality Assurance Division (QAD) selected the Little Rock Housing Authority

(LRHA), AR004, for an on-site Financial Management Review (FMR) of the LRHA Housing

Choice Voucher (HCV) program based on multiple factors, including, but not limited to, a

request from the Little Rock Field Office Director, the LRHA failure to submit audited financial

statements from 2019 forward, and as a follow up to the 2015 FMR (QAD-FMR-2015-AR004)

which revealed five (5) findings with eight (8) required corrective actions and three (3) concerns

with four (4) recommended corrective actions. Additionally considered factors for the scheduling

were the recurring audit findings related to internal control over financial reporting and recording

dating back to 2016.

Accordingly, we conducted the on-site FMR from March 27 – 30, 2023. However, due to the

conditions outlined later in this report additional on-site review time from June 20 – 29, 2023

was scheduled. The onsite review(s) were conducted utilizing records provided by LRHA staff.

The review was originally intended to include calculation of the Restricted Net Position (RNP)

and Unrestricted Net Position (UNP) account balances, verification of whether the LRHA HCV

program had sufficient cash and investments on-hand to cover the calculated RNP and UNP

account balances, and examination of the LRHA administrative expenses for determination if

appropriated funds were expended for the intended purposes. However, based on the condition of

the financial records and the overall record keeping of the LRHA the review was expanded for

the return on-site review to include a Management and Operation(s) Review (MOR).

The MOR was intended to review/assess the overall management and operation(s) of the HCV

program, including but not limited to:

• Review of Participant files for accuracy

• Enterprise Income Verification (EIV)

• PHA Management (Annual Plan)

• Project Based Voucher (PBV) administration.

• Review Family Self Sufficiency Escrow forfeitures

• Review Family Self-Sufficiency program administration

• Special Purpose Voucher Review

SUMMARY

The QAD conducted the on-site FMR/MOR for the review period of January 1, 2018, through

June 30, 2023, or the most recently closed period. It should be noted, and as is further detailed

later in this report the last closed accounting period was approximately October 2022; therefore,

given the individual facts and circumstances as outlined in this report and present within the

LRHA, the QAD FMR Team collected as much information as possible but could not specify a

specific ‘end’ date for the review. Source records provided by the LRHA including, but not

limited to, prior Independent Audit Reports, trial balances, general ledgers, bank statements,

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

2 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

credit card statements, invoices, payroll registers, and any/all additional data submitted by the

LRHA to the Financial Assessment Subsystem (FASS) were utilized.

Our review revealed not only what appears to be a continuation of the previous practices as

outlined in the above referenced report(s), but a further degradation of internal controls, financial

management and reporting practices. Substantive errors in the financial recording and reporting

discrepancies appear to be prevalent, pervasive, and systemic, based on the information provided by the

LRHA staff. Continued and substantial financial management weaknesses exist and are explained in the

body of this report. Based on the significance of the reporting and recording problems, coupled with the

poor condition of the financial records provided by LRHA, we were unable to calculate the Restricted Net

Position and/or Unrestricted Net Position balances.

Further, based on the information provided by the LRHA staff, and other information sources as outlined

above, the LRHA appears to be non-compliant with substantially all of 24 CFR 982, 24 CFR 983, and

HUD Policy Guidance as provided through Notice(s) PIH. Further, the LRHA appears to be in substantial

default of their Annual Contributions Contract (ACC) and will be referred for further review and potential

enforcement action(s).

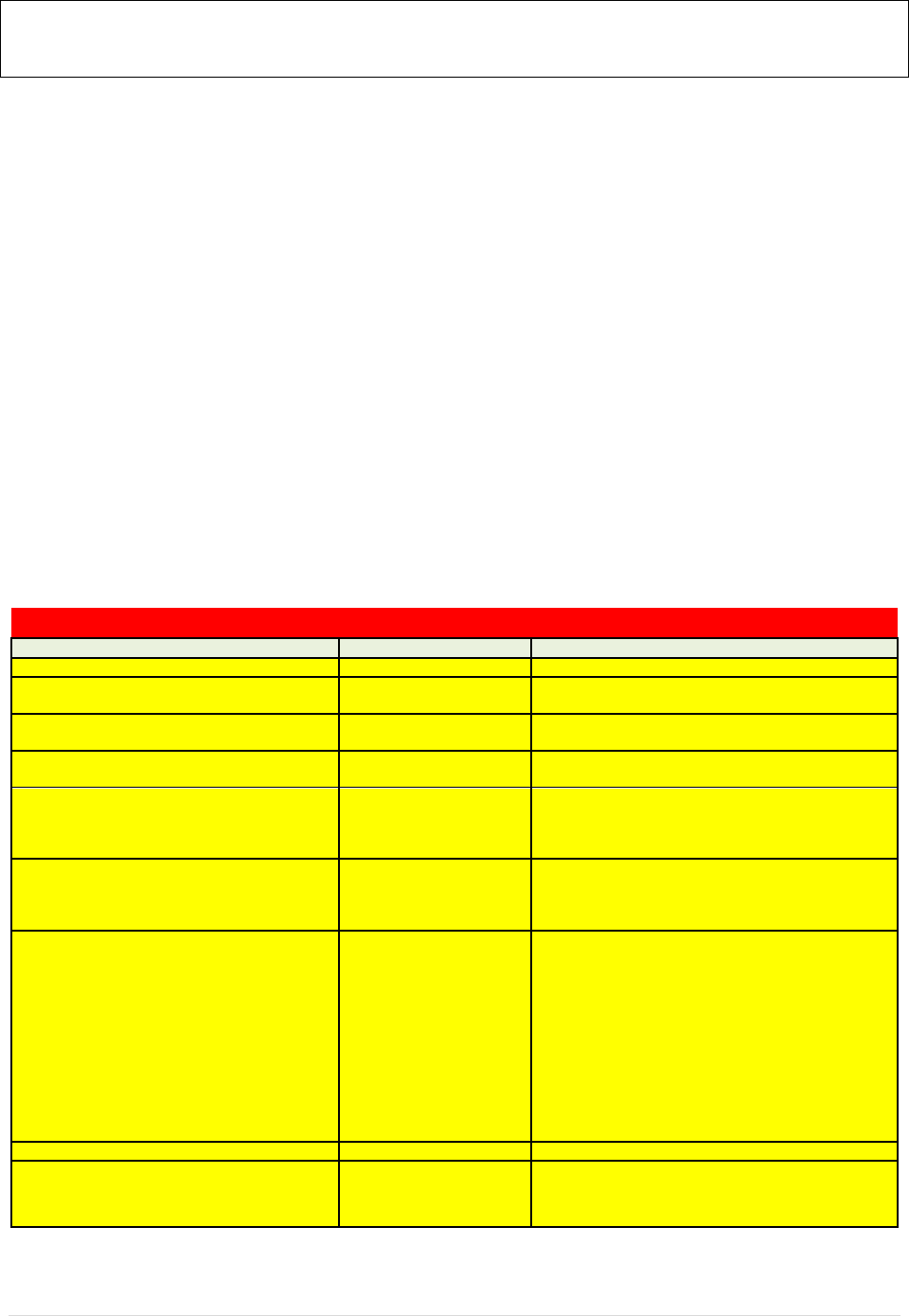

Table No. 1 details questioned and potentially disallowed costs. Below summarized potential debts owed by

the LRHA to the HCV program, along with the calculation method utilized detailed later in this report.

Table No. 1 – Potentially Identified Debt –

Source

Amount Due

Owed to/Resolution

Bank Transfers from LRHA to CAHC

$288,500

Currently Questioned potentially Disallowed

Public Housing Operating Fund(s) transferred to

CAHC

$5,877,074

Currently Questioned potentially Disallowed

Public Housing Capital Fund(s) transferred to

CAHC

$2,256,885

Currently Questioned potentially Disallowed

Loan extension paid by LRHA on behalf of

CAHC

$166,356

Currently Questioned potentially Disallowed

Housing Assistance Payments paid for households

with late reexamination(s) {late income eligibility

determinations}

$10,150,132

Currently Questioned potentially Disallowed *Please

note any associated administrative fees that may be

subject to repayment will be calculated upon final

review

Housing Assistance Payments paid for households

with late Housing Quality Standards Inspections

$10,395,827

Currently Questioned potentially Disallowed *Please

note any associated administrative fees that may be

subject to repayment will be calculated upon final

review

Amounts paid by LRHA on behalf of the CAHC,

but no reimbursements from CAHC could be

located/identified:

o American Express charges

o HD Supply charges

o Home Depot charges

o Payroll, workers

compensation, insurance,

etc.,

o Any other yet to be

identified item.

This amount is yet to be

determined as a Forensic

Audit/Reconstruction of the

financial records must be

completed to determine the

full amount.

Currently Questioned potentially Disallowed

CARES Act Administrative Funds

$770,086

Currently Questioned potentially Disallowed

Total Currently Questioned Potentially

Disallowed expenses

$29,904,860

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

3 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Please note that the above calculated debt is as of as of July 2023. It is entirely possible that

upon the completion of the required corrective action(s) these amounts may increase.

Additionally, it should be noted that continued failure to provide sufficient documentation as

required may/will result in the disallowance of the above-listed costs. If either of these events

take place, these amounts will be updated and addressed in a future review or by the Debt

Collection Team.

Additionally, as outlined later in this report currently known amount(s) of questioned and/or

disallowed costs/payments that are/will be required to be repaid due to the utilization of funds for

purposes other than the intended use and in a manner that does not appear, based on the

information received, to be consistent with and/or compliant with the intended use of funds as

allocated in appropriation(s) law. During the required Corrective Action(s) process, it is more

likely than not that additional debt(s) may be identified, and the above listed amounts will be

adjusted accordingly and any additionally identified items will be added.

Financial Management Review (FMR)

Financial Management system(s)

It is important to note the overall financial management process and software systems utilized by

the LRHA both for the programmatic requirement(s) and the financial management and record

keeping requirement(s). In short, the LRHA currently utilizes Yardi for applicant/participant

processing and for financial record keeping. However, it should be noted that as of the return on-

site visit the Yardi financial management module had not been set up and was not being utilized.

Additionally, it should be noted that the LRHA administers the following Voucher

Programming: Housing Choice Voucher (Section 8), Mainstream, Emergency Housing

Voucher(s), and the Veteran Affairs Supportive Housing Voucher (HUD VASH) program(s). In

addition to the previously listed Voucher Programming, the LRHA is comprised of Public

Housing facility(ies), properties that have undergone or are in the process of the Rental

Assistance Demonstration (RAD) conversion(s) and the Central Arkansas Housing Corporation

(CAHC) (a nonprofit corporation that appears to be an instrumentality of the LRHA and is

included as a component unit and/or a wholly owned subsidiary of the LRHA for their annual

audited financial statements).

As previously noted, the LRHA currently utilizes Yardi software for their activities related to

program participants, for example eligibility, housing quality standards and submission of

50058’s to HUD. Previously, the LRHA utilized Tenmast as their programmatic and financial

management software. During the initial QAD on-site visit LRHA staff stated that the financial

system(s) were being migrated to Yardi from Tenmast. However, during the subsequent on-site

visit it was observed that Yardi financial management module continued to not be completely set

up for financial management functions and there was no clear method of maintaining the

monthly and/or annual accounting functions.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

4 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Financial management and reporting

Review and analysis of the LRHA financial management and reporting system(s) that were

available, and/or available document(s) the following conditions were noted:

• The last bank reconciliation was completed in May 2022 or June 2022

o The Bank of America account contains all voucher programmatic funding

disbursed by the HUD Financial Management Center

o There are multiple bank accounts with Regions Bank for Public Housing, the

CAHC, The LRHA in general, and Family Self Sufficiency (FSS) Program

Escrow Funds

o There are multiple bank accounts with Bank of the Ozarks

▪ These appear to be for Public Housing and/or properties that were, or will

be, the subject of a Rental Assistance Demonstration (RAD) conversion(s)

o There are accounts listed with Simmons Bank; however, current LRHA staff does

not have access to these bank accounts and cannot provide information related to

amount(s) and/or funding purpose and/or funding restriction(s) we were

unsuccessful in locating any information regarding these accounts other than they

are listed as belonging to LRHA, but no one at LRHA knew what the accounts

were.

o There is/was no discernable differentiation between the programmatic sources of

funding,

▪ This appears to have led to the comingling of funds and funding usage that

may not be in compliance with the programmatic restrictions.

o The LRHA was unable to provide properly executed General Depository

Agreements as required and/or for all accounts containing HUD provided funds.

o It appears that the CAHC financial records are comingled with the LRHA

financial records.

▪ There are booked Inter-program due to/from accounts on the PHA

financial records between the LRHA and the CAHC

▪ The CAHC Finance Director appears to be listed on all LRHA bank

accounts as a signatory for all accounts except the Bank of America

account. There should be no one at the CAHC instrumentality with

authority to withdraw funds from any LRHA bank account.

• Bank transactions revealed the CAHC Finance Director has

initiated transfers from LRHA bank accounts to CAHC bank

account(s) with no valid reason for doing so.

▪ The CAHC staff was being paid through ADP along with the LRHA staff

until approximately January 2023. It is currently unknown when this

practice began, and there were no locatable reimbursements from the

CAHC to the LRHA for these expenses.

▪ LRHA finance staff were/are completing the monthly accounting and

other administrative functions for the CAHC. Review and analysis of

documents revealed that invoices were being sent directly to the LRHA

for the CAHC. It is currently unclear when the practice began, and there

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

5 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

▪ were no locatable reimbursements from the CAHC to the LRHA for this

work.

• The last ‘closed’ financial period in Tenmast appears to be October 2022

• The Emergency Housing Voucher Program was initially included with the Housing

Choice Voucher program.

o Based on staff statements Tenmast did not have the capacity to incorporate

another program.

o EHV participants have since been correctly coded in Yardi.

▪ Based on staff statements and a review of the available documentation

HCV funds were utilized for the Emergency Housing Voucher Program

▪ Corrected 50058’s appears to have been completed; however, no

corrections on the financial records have been made.

Based on the incomplete financial record keeping, and the inability to differentiate between

programmatic funding sources the QAD began reviewing all financial records entity wide that

were made available to ascertain the extent to which the comingling of funds is/was present

regardless of programmatic restriction(s).

Audited Financial Statements

The last audited financial statement submission was for 2018. Based on the information

provided, and an interview with a representative of the Independent Public Accountant (IPA)’s

office revealed that the 2019 audit continued to be a work in progress and that 2020 forward had

not been started. Additionally, when asked specifically why the audited financial statements had

not been completed the IPA’s representative stated that they had not received all requested

information related to the CAHC.

The QAD requested that all audited financial statements from 2019 forward for all subsidiary

and/or component properties be provided. This would include, but not be limited to Granite

Mountain, Granite Mountain Senior Homes.

Based on discussions with the LRHA staff it is/was the understanding of the QAD that the

CAHC managed the operations of the subsidiary/component properties. As noted above, the

QAD requested all audited financial statements from 2019 forward for all component

units/properties and as of the writing of this report the LRHA and/or the CAHC have

failed/refused to provide the requested audited financial statements for any period beyond 2019.

Due to the financing and/or partnership agreement(s) typically associated with property

conversion(s) through RAD and/or development it would be unusual for lien holders and/or

investors to have concurred with not having audited financial statements from 2020 through and

including 2023. LRHA staff did not have copies of the requested audited financial statements

and stated they would be requesting this information from the CAHC.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

6 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Credit Card and/or Charge account usage

A generalized review of the American Express credit card statements, without supporting

documentation, revealed what appears to be regular and habitual utilization of the credit card(s)

for ineligible purposes. Based on the previously mentioned review of transactions there are at

least $33,248.29 in questionable and/or disallowed costs for the period between January 2022

and January 2023. Coupling what appears to be a disregard for credit card utilization policy with

the lacking support documentation and/or business use justification(s) it is reasonable to question

the validity of all costs billed to the credit card(s). Detailed review and analysis of credit card

transaction(s) is strongly recommended to confirm the validity of and eligibility of billed

expenditures not only within the restrictions of the funds utilized to pay the credit card bill(s),

but within the eligible uses of federal funds. Additionally, it should be noted that the CAHC

utilizes one of the American Express credit cards that is billed to the LRHA. There is no

identifiable reimbursement(s) from the CAHC to the LRHA for its utilization of the American

Express account.

A generalized review of the HD Supply account statements and/or invoices and/or purchase

orders revealed the following:

• The HD Supply invoice(s) are paid through the LRHA.

• The HD Supply invoice(s) appear to primarily contain material(s) for public housing

and/or converted properties managed by the CAHC.

• In May 2023 the statement(s) indicate that an individual no longer employed with the

LRHA was approving and/or ordering supplies from HD Supply

A generalized review of the Home Depot invoice(s)/statement(s) revealed the following:

• The Home Depot invoice(s) are paid through the LRHA.

• The Home Depot invoice(s) appear to primarily contain material(s) for public housing

and/or converted properties managed by the CAHC.

As is noted later in this report as part of Finding 2023 – 1b the LRHA will be required to review

all credit card and/or charge account activity and provide sufficiently detailed original

documentation to validate the eligibility of the expenditures and the reimbursement from the

CAHC for any/all its expenses that were paid through the LRHA.

Additional noteworthy information

Review and analysis of available information revealed:

• Immediately upon receipt from HUD, Public Housing Operating funds are being

transferred to the CAHC.

o At some point in 2018 or 2019 the LRHA began transferring its Public Housing

Operating Fund(s) and/or the Public Housing Capital Funds to the CAHC – this

was confirmed by a review of bank transaction activity.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

7 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

• The CAHC Finance Director not only has signatory access to the LRHA bank account(s)

but has also initiated cash transfers from LRHA bank account(s) into CAHC bank

account(s)

o Bank transactions revealed that between March and April 2023 $288,500 was

transferred from the LRHA Modernization bank account into a CAHC bank

account.

o Based on the available information it appears that these funds were originally a

result of a repayment requirement from the Departmental Enforcement Center

Report previously issued.

o The LRHA staff were unable to provide documentation related to the purpose of

these transfers, why a ‘non LRHA’ staff member was initiating these transactions,

o why a ‘non-LRHA’ staff member has signatory access to LRHA bank account(s),

and information related to the ultimate funding utilization.

o Due to the lack of documentation supporting these transactions the entire

$288,500 is currently determined to be a questioned cost and as further outlined in

The Findings section of this report related to Questioned and/or Disallowed costs

sufficient documentation must be provided to demonstrate the eligibility of the

funding utilization.

o Additionally, as part of the above referenced questioned cash transfers 3/27/23

$30,000, 3/28/23 $35,000, and 3/30/23 $40,000 was transferred from the

Modernization (Regions 5011) account were not transferred into any known bank

account for the LRHA and/or the CAHC. The LRHA and/or CAHC has, as of the

date of this document, failed to provide information related to where these funds

were transferred, the purpose of the funds being moved to unknown bank

accounts, and the ultimate funding utilization.

• As previously referenced in this report, the LRHA has been transferring the Public

Housing Operating and/or Capital Funds to the CAHC. Due to the lack of complete

financial records and no documentation supporting the transfers the below amounts are

currently determined to be Questioned and/or Disallowed costs. Sufficient documentation

must be provided to demonstrate the eligibility of the funding utilization. Further, the

below amounts represent a calculated total of all funds drawn during the period from

2018 forward, as there is not sufficient documentation to demonstrate the eligible uses the

entirety of the amounts must demonstrate eligibility regardless of any amounts that may

not have been transferred to the CAHC.

o A review of the draws from 2018 forward revealed that:

▪ $2,256,885 in Capital Funds have been drawn,

▪ $5,877,074 in Operating Funds have been drawn.

• A review of miscellaneous file documents revealed:

o A Loan extension of $277,260 was paid by LRHA and CAHC on January 13,

2023

▪ LRHA paid $166,356.03.

▪ As is more fully detailed later in this report, this amount was paid with

what appear to be restricted, HCV funds. This amount is a disallowed

cost as a loan extension for a converted Public Housing property. HCV

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

8 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

▪ restricted funds may only be used for HCV Housing Assistance

Payment(s).

o A Memorandum/Letter dated April 14, 2023, from the CAHC to the LRHA

requesting payment in the amount of $300,000 for “…reimbursements for the

receipts incurred from September 2021 through August 2022. This also includes

loans to MHA

1

from CAHC ($166,000 for extension with Walker Dunlap and

unauthorized payments made by financial staff with CAHC funds.) …”

It is unclear if this payment was made, additionally as previously outlined it appears that LRHA

was/had been transferring all Operating and/or Capital Funds to the CAHC therefore it is unclear

what additional reimbursements the CAHC would be seeking.

▪ As is more fully detailed later in this report, this amount (if paid) would

have been remitted with Housing Choice Voucher Program funds and

would not be an eligible utilization of said funds.

• A review of the bank statements and available financial records indicate that, as

previously outlined in this report, the LRHA was/has been transferring all Public Housing

Operating and/or Capital Fund(s) to the CAHC in addition to the cash transfers initiated

by the CAHC Finance Director. However, the LRHA has been paying (at least) the

below expenses for the CAHC:

o American Express charges

o HD Supply charges

o Home Depot charges

o Payroll, workers compensation, insurance, etc.

o Loan Extension(s)

• Provided that the LRHA’s only other funding stream is the Voucher program(s)

{Housing Choice Voucher/Section 8, Emergency Housing Voucher, Mainstream, and

Veterans Affairs Supportive Housing Vouchers} it is reasonable to conclude that the

voucher program(s) administrative and/or housing assistance payments fund(s) have been

utilized to pay the above listed charges along with the questioned costs previously

outlined in this report.

o As is outlined in the Findings section of this report, the LRHA will be required to

conduct a forensic reconstruction of their financial records from Fiscal Year 2018

to the current month. This reconstruction will be required to calculate and

document the total amount of voucher funds (by program) that were utilized to

pay ineligible public housing and/or Central Office Cost Center and/or CAHC

expenditures and determine the amount.

o of repayment required either to the administrative reserves of the voucher

program(s) and/or the amount of funds required to be repaid to HUD for the

ineligible utilization of Housing Assistance Payment(s).

1

The LRHA is also known as Metropolitan Housing Alliance (MHA). This is a direct quote, so we did not

chance to LRHA as we have used throughout this document.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

9 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Combining the previously described conditions coupled with the described financial

management weaknesses, questionable and/or disallowed costs, questioned bank transfers of

funds, and the extended period related to the incomplete accounting there are reasonable

concerns that t there is/has been a complete breakdown of internal control(s) and internal quality

control procedures are either non-existent or not followed.

Management and Operations Review

The MOR was intended to review and assess the overall management and operation(s) of the

HCV program, including but not limited to:

• Review of Participant files for accuracy

• Enterprise Income Verification (EIV)

• PHA Management (Annual Plan)

• Project Based Voucher (PBV) administration.

• Review Family Self Sufficiency Escrow forfeitures

• Review Family Self-Sufficiency program administration

• Special Purpose Voucher Review

The below summary, and subsequent analysis, indicates that there are systemic internal control

failure(s) which are not confined to the financial management of LRHA.

It should be noted that the LRHA staff provided requested applicant/participant files for review,

and informed QAD staff that participant files were primarily scanned into either the Tenmast or

the Yardi system(s) for document management. The LRHA was in possession of ‘paper’ files,

however, these are not/were not readily available as they had been ‘archived’ due to the file

scanning. Therefore, with the LRHA reliance upon the electronic documents the QAD utilized

electronic participant file(s) to conduct the file review(s).

PIH Information Center (PIC) reporting

Annual eligibility

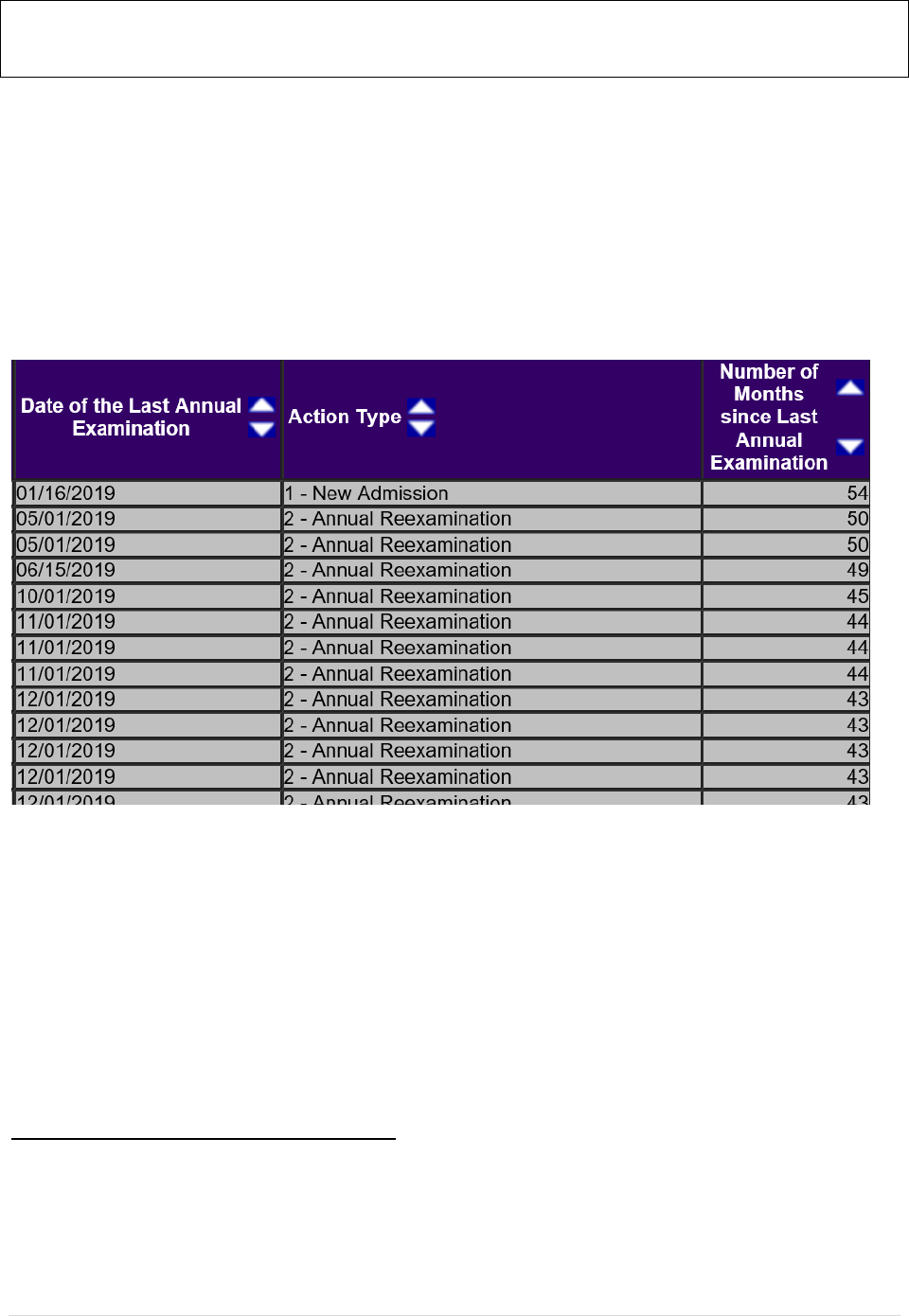

The below illustration is from the Reexamination Report and has been redacted to prevent the

distribution of Personally Identifiable Information. It should be noted that this information is

dependent upon the LRHA transmitting the information to the PIC system, but as the 50058’s

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

10 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

are required to be submitted within 60 days of the effective date of the action if the 50058 has

not been submitted then absent sufficient documentation to demonstrate an annual

reexamination.

was completed then any payment for these households would be considered a questioned cost

and/or disallowed cost. However, as illustrated there are participant households who have not

had an annual reexamination conducted in up to 54 months. As of July 31, 2024, report

generation date there are currently 1,226 participant households who have not had an annual

reexamination in 13 or more months.

As the provided Administrative Plan (Amended Nov. 18, 2021, by Resolution 6789) indicates

that program participants will have an annual reexamination with the above illustrated late

annual reexamination(s) any/all costs associated with housing assistance payments and/or utility

assistance payments are determined to be questioned costs. The amount of questioned costs is

calculated at 1,226 households x current per unit cost x the number of months past due =

currently calculated questioned costs. The currently calculated questioned, and potentially

disallowed costs due to late reexamination(s) is $10,150,132.95. As further detailed in the

Findings section of this report, the LRHA will be required to demonstrate that the annual

reexamination(s) are/were completed and that all households were in fact eligible for any

assistance that was remitted on their behalf.

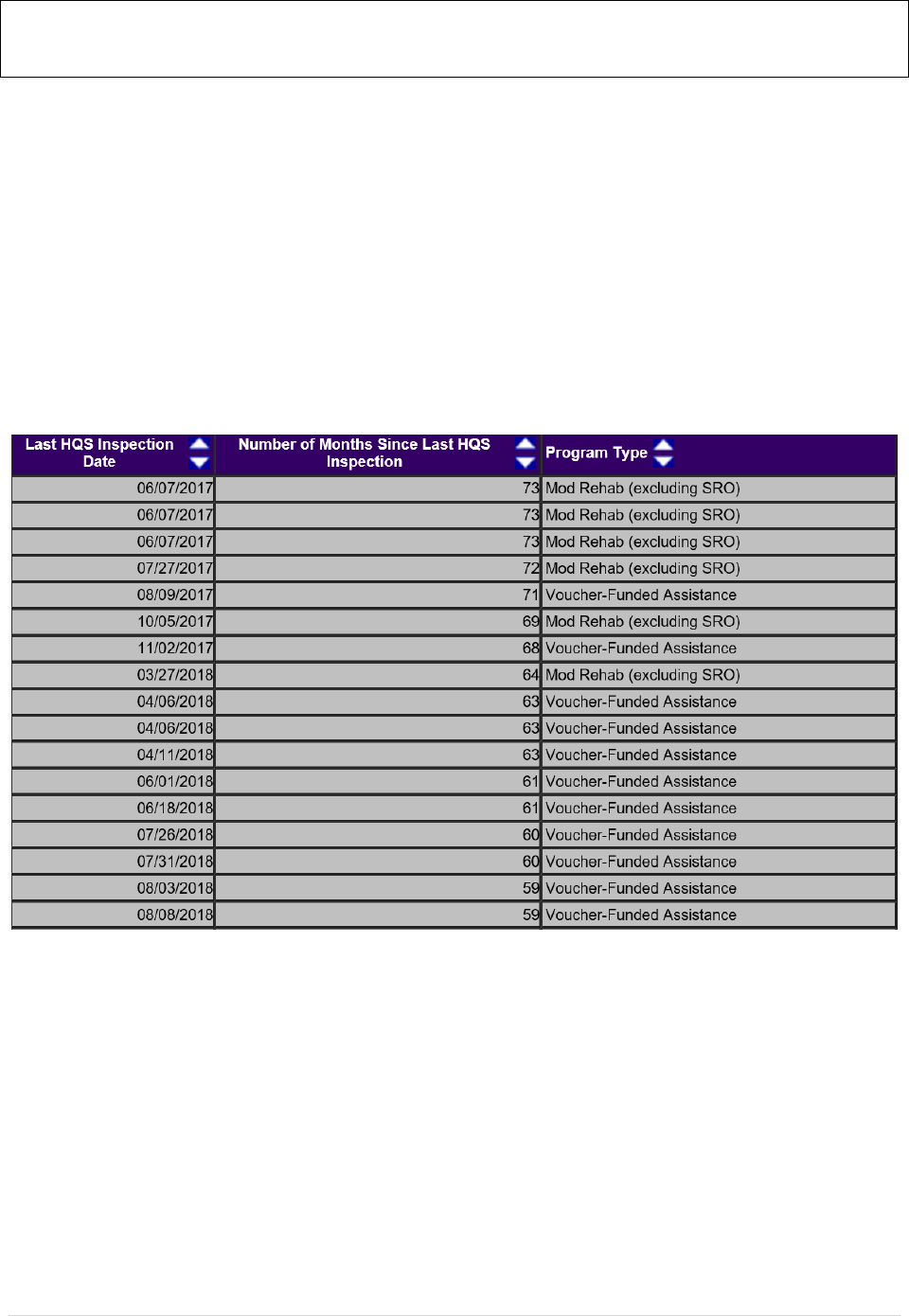

Housing Quality Standards Inspection(s)

The below illustration is from the Housing Quality Standard(s) Report and has been redacted to

prevent the distribution of Personally Identifiable Information. It should be noted that this

information is dependent upon the LRHA transmitting the information to the PIC system, but as

the 50058’s are required to be submitted within 60 days of the effective date of the action if the

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

11 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

50058 has not been submitted then absent sufficient documentation to demonstrate a Housing

Quality Standards Inspection was completed then any payment for these households would be

considered a questioned cost and/or disallowed cost. However, as illustrated there are participant

households who have not had a Housing Quality Standards Inspection conducted in up to 73

months. As of July 31, 2024, report generation date, there are currently 615 participant

households who have not a Housing Standards Inspection in 25 or more months.

Please note the Administrative Plan does indicate that Housing Quality Standards inspections

will be conducted at the Initial/Move-in, Biennial Inspections to occur within 24 months of the

last passed annual/bi-annual inspections, and for Special/Complaint Inspections, and Quality

Control.

As the Administrative Plan does indicate that inspections will be conducted within 24 months,

program participants for whom housing assistance payments were remitted to the landlord

outside of compliance with 24 CFR 982.405(a) and the administrative plan are considered

questioned and/or disallowed costs. The amount of questioned costs is calculated at 615

households x current per unit cost x the number of months past due = currently calculated

questioned costs. The currently calculated questioned, and potentially disallowed costs due to

late Housing Quality Standards Inspections is $10,395,827. As further detailed in the Findings

section of this report, the LRHA will be required to demonstrate that the Housing Quality

Standards Inspection(s) are/were completed and that all Housing Assistance Payments were

made for units in compliance with the Housing Quality Standards Inspection requirements as

outlined in the Administrative Plan and in compliance with the applicable Federal Regulation(s).

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

12 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

It should be noted that during the COVID pandemic HUD issued multiple notices allowing for

Public Housing Authorities to implement specified requirement waivers. However, as was

outlined in the notices there were documentation and reporting requirements to support and

substantiate the selected waivers. These waiver(s) were available to the LRHA and may have

been applicable to the above referenced questioned and potentially disallowed costs; however,

the LRHA either did not implement the waivers or did not maintain the required documentation

as it was not provided when requested. Therefore, as the record keeping requirements for the

waivers do not appear to have been complied with the LRHA is being reviewed based on non-

waiver (standard) requirements.

Results of Participant File Review(s)

The Management and Operation(s) Review additionally consisted of reviewing participant

file(s), it should be noted that the review of these randomly selected participant files yielded a

100% failure rate. This failure rate is defined as all required documentation not being present in

the participant file when reviewed. Below is a summary of the identified deficiencies.

Additionally, please note the below information is summarized to identify the specific

deficiencies, a detailed workbook has been prepared but due to the Personally Identifiable

Information contained is not presented in or attached to this report. The workbook can/will be

provided as requested and as appropriate should it be requested.

Below is a summary of the file deficiencies identified in the 56 participant files selected as a

representative sampling of the LRHA voucher program(s) as a whole:

• 54 files either did not contain a properly executed, or did not contain a HUD Form 9886 –

Authorization for the Release of information/Privacy Act Notice,

• 11 files did not contain documentation related to updated Utility Allowance

calculation(s),

• 49 files either did not contain any EIV information or did not contain properly executed

EIV information,

• 10 files did not contain documentation to substantiate the income determination(s)

o 1 file contained EIV information, but the EIV report clearly indicated reportable

income that was not included in the income determination,

• 43 files did not contain the required Tenancy Addendum,

• 48 files did not contain properly executed Declarations for S.A.V.E., specifically the ID #

and date of certification was not completed, or the document(s) were not present in the

file.

Please note for the purposes of the above listing, this is not an indication of, and should not be

interpreted as a complete listing of file deficiencies. It is simply a count of the most prevalent

incidents.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

13 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Family Self Sufficiency (FSS)

The LRHA operates a Family Self Sufficiency Program and does have participants with escrow

balances. However, due to the overall condition of the financial records and the participant file

deficiencies identified the QAD was unable to confirm/validate that participant families were

receiving accurate accrual(s). As later discussed in the Findings section of this report, the

LRHA will be required to review, validate, and provide sufficient documentation to

demonstrate that all households received the appropriate escrow deposit and associated interest

payment(s).

EIV Reports

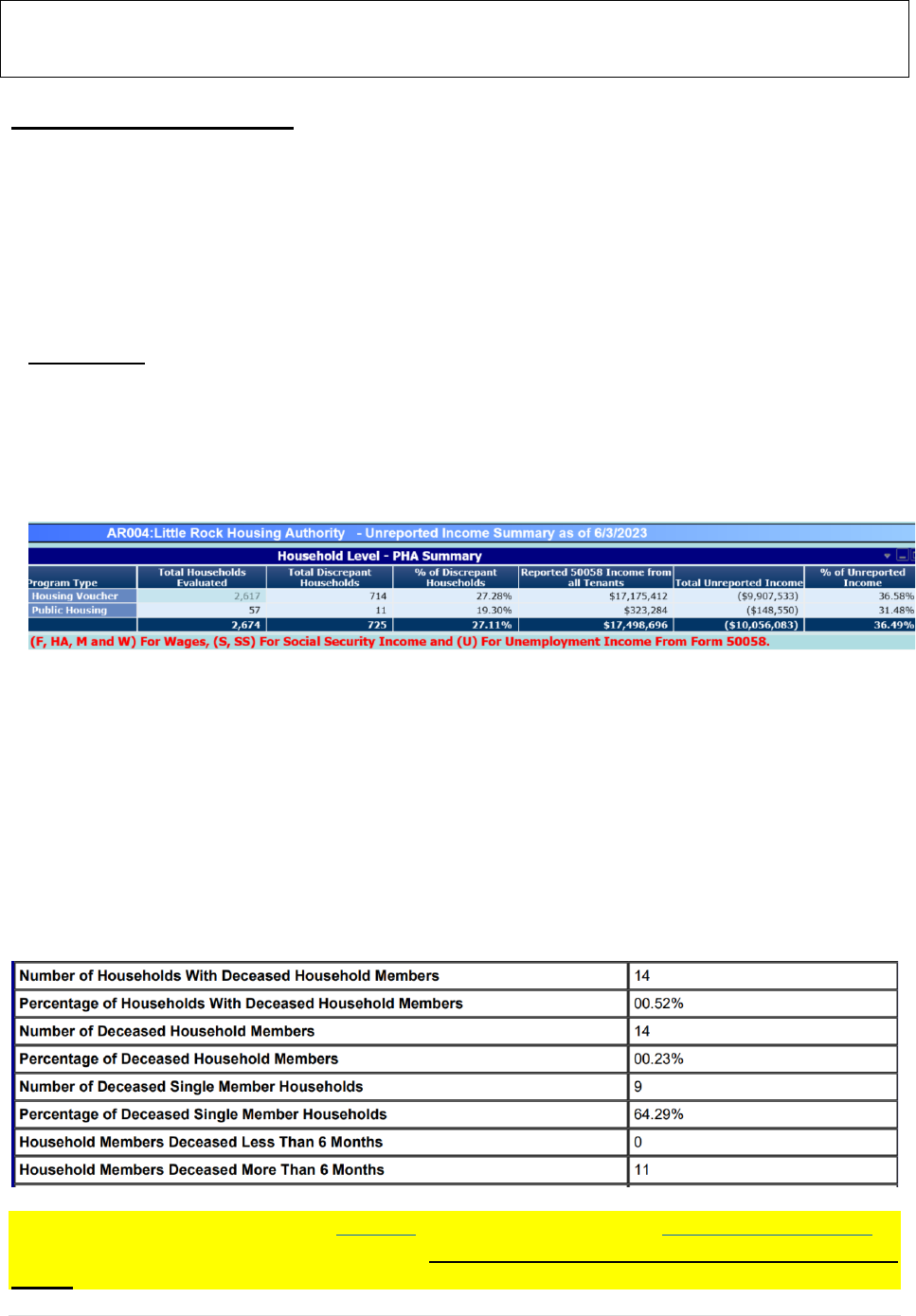

Unreported Income

A review of the Income Discrepancy report in the EIV system revealed, as illustrated below,

that there is almost $10M in underreporting income from participating households. This

strongly indicates that the calculated Tenant Portion is understated, and the associated Housing

Assistance Payment(s) are overstated and may be subject to a repayment requirement.

Deceased Tenants Report

A review of the Deceased Tenants report in the EIV system revealed, as illustrated below, that

there are (or appear to be) 14 households with deceased household members. Additionally, the

report indicates that 9 of the 14 households are/were single member households and 11 of the

14 have been deceased for 6 months or more. Upon the death of the participant, especially

single member, the subsidy assistance terminates. The LRHA was unable to provide sufficient

documentation to demonstrate that housing assistance payment(s) had been stopped for the

reflected households. Any HAP or utility allowance payments (UAP) after the month of death

would be subject to repayment.

The FMR/MOR revealed seven (7) Findings (listed below) for which a Corrective Action Plan

(CAP) must be prepared and submitted to the QAD not later than 30 days after the date of this

report.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

14 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

As outlined above, the LRHA is non-compliant with the requirements as outlined under 24 CFR

§ 982.158(a) as it relates to the FMR. When considering the MOR, the LRHA appears to be

non-compliant with substantially all of the requirements as outlined under 24 CFR §982.

In total, the LRHA appears to be in default on their Annual Contributions Contract (ACC) and

will be referred for further review and potential enforcement action(s).

SOLVENCY

SUMMARY OF CASH

Due to the significance of the financial management and recording issues, along with the

significance of expenditures lacking supporting documentation outlined in this report, overall

cash position is currently indeterminable. However, it is not unreasonable to conclude that the

LRHA is either insolvent or on the verge of insolvency. The LRHA should be monitored closely

during the Corrective Action Plan process to ensure the continued ability to meet all financial

obligations.

CALCULATED RNP AND UNP ACCOUNT BALANCES

Based on the significance of the previously outlined financial management and reporting issues,

and the fact that the required financial file reconstruction(s) and the validation of

applicant/participant file(s) RNP and UNP balances are currently undeterminable.

CARES ACT FUNDS

The LRHA received supplemental administrative fees in the amount of $770,086. Based on the

previously described conditions of the financial records it is currently indeterminable if these

funds were expended withing the applicable timeline(s) and/or for eligible purposes. These

funds are included in the currently questioned costs pending receipt of sufficient documentation

to demonstrate compliance with the programmatic restrictions of these funds.

RESULTS OF REVIEW

As indicated throughout this report, both the financial and applicant/participant records were

either unproduceable, nonexistent or were kept in a condition that did not allow for a speedy and

effective audit, nor were they in a condition that would allow for the unqualified calculation of

UNP, RNP or an accurate calculation of the cash available to cover the calculated balances.

The condition of the financial and applicant/participant records provided by the LRHA

contributes to a failure on part of the LRHA to fulfill its fiduciary duties as they pertain to the

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

15 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Annual Contribution Contract (ACC) and HUD regulations. The LRHA is in default of the

ACC and may be referred for further enforcement action.

FMR - FINDINGS

Finding No. FMR-2023-1: The LRHA HCV Financial records and Book of Accounts are

Non-Compliant with the Regulatory Requirement(s) and Require Significant

Improvement.

Condition: The HCV general ledgers financial recording and reporting could not be properly and

effectively tracked. There is no reliable audit trail the supporting documentation is either

missing or inadequate.

Criteria: The 24 CFR § 982.158(a) requires the PHA to maintain complete and accurate

accounts and other records for the program in accordance with HUD requirements.

Cause: The LRHA financial records do not accurately reflect the financial position. The

Financial Management Review (FMR) section of this report (above) outlines the deficiencies.

Corrective Action No. FMR-2023-1a: The LRHA must engage a financial management

consultant to assist with bringing the financial record keeping current. Additionally, the

consultant should also be engaged to ensure that Yardi input is accurate and ensure corrections

are made where warranted, along with a reconciliation of the financial data between Yardi and

Tenmast. Any variances must be researched, reconciled, corrected and prior period adjustments

prepared for correction of the UNP and/or RNP balances. Additionally, the LRHA will provide

the QAD with all procurement information related to the financial management consultant

including, but not limited to the solicitation, bids received, selection and draft of the proposed

engagement contract.

Corrective Action No. FMR- 2023-1b: After the financial management consultant has brought

the LRHA up to date on all possible financial record keeping and any associated corrections to

financial records and data input to bring Yardi online as the financial management system for the

full conversion from the Tenmast system. Once this is complete the LRHA must engage a

properly licensed/certified forensic auditor to reconstruct/review all (entity wide) financial

transactions. The full forensic review of the LRHA must ensure that a reconstruction of the full

financial records to determine the true and accurate financial position; looking specifically at

those items trending toward possible misuse of funds and other possible misrepresentation of the

financial status that may not be revealed through the consultant’s effort, in addition to all areas of

questioned costs outlined in this report. This rereview and reconstruction must begin at least

January 1, 2018, moving forward to the most current closed accounting period. The LRHA

Executive Director must work with the QAD and Little Rock Field Office to develop and review

the plan of action for reviewing/reconstructing the financial records as needed based on the

outcome of the forensic reconstruction. Additionally, the LRHA will provide the QAD with all

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

16 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

procurement information related to the financial management consultant including, but not

limited to the solicitation, bids received, selection and draft of the proposed engagement contract.

Corrective Action No. FMR-2023-1c: The Board, executive, and financial staff must be

provided with extensive approved training on HUD financial recording and reporting. In

addition, the financial staff must be provided with training on the current PHA financial and

program management software.

Corrective Action No. FMR-2023-1d: The LRHA must ensure that the Yardi software is

properly installed and/or set up to allow for the proper programmatic separation and tracking of

the various programs administered. The LRHA must provide sufficient documentation to QAD

to demonstrate the software is set up and usable as designed.

Corrective Action No. FMR-2023-1e: The LRHA must provide the documented business

needs for all signatories to the bank accounts. Additionally, the LRHA must provide sufficient

documentation/business need for the CAHC Finance Director to be a signatory on any LRHA

Public Housing Authority bank account.

Corrective Action No. FMR-2023-1f: The LRHA must ensure that, upon completion of the

financial reconstruction, the VMS is updated, and the appropriate prior period adjustments are

entered into FDS. LRHA must provide QAD with sufficient documentation to demonstrate how

the balances were calculated, what the required adjustments are and validation that these

adjustments have been submitted to the respective reporting system.

Finding No. FMR-2023-2: There are Material Potential Disallowed and Questionable

Expenses.

Condition: During our review of financial records and programmatic files we found multiple

instances of HCV funds being used for purposes outside of the statutory, regulatory and HUD

Policy guidance. Of note are the transactions outlined in this report. Additionally, the ‘blanket’

transferring of Public Housing Operating and/or Capital Fund(s) is creating an environment in

which the LRHA is utilizing Housing Choice Voucher funding for ineligible purposes.

Criteria: 24 CFR § 982.152; Notice PIH-2015-17; Notice PIH-2022-14 among others; A PHA

HCV administrative fees may only be used to cover costs incurred to perform PHA HCV

administrative responsibilities for the program in accordance with HUD regulations and

requirements. Additionally, HCV Housing Assistance funds may only be utilized for Housing

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

17 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Assistance Payments and other associated expenses (FSS Escrow deposits, Utility Allowance(s),

etc.)

Cause: In most instances the disallowed costs were a result of the LRHA executive and/or

financial staff not understanding the program or understanding fiscal and appropriation law.

Effect: Due to the condition of the financial records, and because we were not provided with

reliable financial records, we were unable to determine with 100% accuracy a total for the

disallowed and questionable expenses and/or if any additional misappropriation of funds may

have occurred. The misuse of HCV funds is a violation of the Agency’s ACC agreement. In

addition, it inhibits the Agency from being able to meet their HCV administrative obligations or

to assist as many families as possible with the funds provided.

Corrective Action No. FMR-2023-2a: The LRHA must, provide sufficient documentation to

demonstrate the business need, validity and expenditure eligibility of all questioned costs

outlined in Table 1 except for the Questioned Housing Assistance Payments due to late

reexaminations and Housing Quality Inspections within 30 days of the date of this report.

Failure/refusal to provide sufficient documentation to fully demonstrate compliance and

eligibility will result in the disallowance of these costs.

Corrective Action No. 2023-2b: The LRHA Executive Director must work with the Little Rock

Field Office and the QAD to develop a mutually agreed upon timeline to review and validate the

eligibility of the questioned costs related to Housing Assistance Payments due to late

reexaminations and Housing Quality Inspections within 30 days of the date of this report.

Finding No. FMR- 2023-3: LRHA does not appear to be properly tracking FSS Escrow

accounts.

Condition: As described in this report, there is insufficient documentation to demonstrate

compliance with the applicable regulatory and policy requirements for the determination of FSS

Escrow deposits.

Criteria: 24 CFR § 984.303 – Contract of Participation, 24 CFR § 984.305 – FSS Escrow

Account, Notice PIH-2016-08 “Accurate Reporting of FSS Escrow Balances”, PIH-REAC

Accounting Brief #26 – “Financial Reporting for the Family Self-Sufficiency Program”

Cause: The LRHA was unable to provide documentation supporting, or reconciling, the FSS

Escrow balances to the bank account(s) and/or tenant ledger(s).

Effect: The QAD cannot independently confirm the actual amount of FSS escrow funds that the

LRHA should be holding for FSS participants.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

18 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Corrective Action No.FMR-2023-3a: The LRHA must provide the QAD with adequate

documentation to demonstrate that the FSS escrow accounts are fully funded.

Corrective Action No. FMR-2023-3b: The LRHA must reconcile the FSS program escrow

report, the FSS bank balance and the general ledger. Reconciliation documents must be provided

to the QAD.

Corrective Action No. FMR- 2023-3c: The LRHA must develop and implement a policy that

ensures the correct recording and reporting of FSS escrow balances in all systems. The

developed and implemented policy must be compliant with HUD PIH 2022-20, Family Self-

Sufficiency (FSS) Program: Establishment of the Escrow Account and Use of Forfeited FSS

Escrow and must be provided to the QAD through the CAP process.

Finding No. FMR-2023-4: The RNP and UNP Account Balances Were Incorrectly

Calculated and Incorrectly Reported in the VMS and FDS.

Condition: The LRHA miscalculated and misreported RNP and UNP in its FDS and VMS

submissions.

Criteria: Notice PIH-2015-17; VMS User’s Manual; 24 CFR § 982.151; 24 CFR § 982.158

Cause: As discussed previously in this report, due to the condition of the financial records and

the extended period that the monthly accounting has remained incomplete the balances reported

are, by default, incomplete.

Effect: At certain times, HUD must make use of RNP, UNP, and cash reporting to calculate

funding, offsets, or cash management disbursements. As such, the reporting of these balances in

the VMS must be accurate. By failing to maintain complete and accurate accounts and other

records for the HCV Program, the LRHA failed to provide HUD with information useful in

determining the RNP and UNP balances. The LRHA actual financial position was not clearly

presented to the Department.

Corrective Action No. FMR-2023-4a: The LRHA must immediately, for previously reported

totals, determine which of the totals was accurate and make the appropriate reporting

correction(s). Full documentation supporting the LRHA calculated balances must be provided to

the QAD.

Corrective Action No. 2023-4b: The LRHA must, upon completion of recalculation as

outlined in the previous findings and corrective actions, immediately prepare the appropriate

prior period adjustment to be reported in FDS and internal financial records.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

19 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Finding No. FMR 2023-5: The LRHA does not have a Properly Executed General

Depository Agreement.

Condition: The LRHA failed to properly complete the General Depository Agreement (GDA),

form HUD-51999. PHAs must have a fully executed GDA, which includes the account numbers

for all financial accounts where HUD funds are maintained.

Criteria: 24 CFR § 982.156 Depositary for Program Funds; Section 13 of the ACC; Notice

PIH-2015-17

Cause: LRHA was unable to provide executed GDA’s for bank accounts containing HUD

funding.

Effect: Without a properly executed GDA, HUD will not be able to control program funds in the

event of a default by the LRHA. HUD will not be able to prohibit the LRHA from withdrawing

funds held with the depositary or permitting the depositary from denying withdrawals of such

funds.

Corrective Action No. FMR 2023-5: The LRHA must immediately execute a new General

Depository Agreement that includes the account numbers of all financial accounts that contain

HUD funds.

(This space left intentionally blank)

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

20 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

MOR - FINDINGS

Finding No. MOR-2023-6: The Form HUD-9886 in the Majority of the

Participant Files Was Not Properly Completed.

Condition: The form HUD-9886, Authorization for Release of Information/Privacy Act

was not properly completed in 54 of the tenant files.

Criteria: The Authorization for Release of Information/Privacy Act Notice is required per

Section 904 of the Stewart B. McKinney Homeless Assistance Amendments Act of 1988, as

amended by Section 903 of the Housing and Community Development Act of 1992 and

Section 3003 of the Omnibus Budget Reconciliation Act of 1993. This law is found at 42

U.S.C. 3544.

The regulations at 24 CFR § 982.153 state, “the PHA must comply with the consolidated.

ACC, the application, HUD regulations and other requirements, and the PHA administrative

plan.”

Cause: As outlined in the MOR section of this report, substantially all files were missing

complete HUD-9886 forms.

Effect: The lack of a properly executed form HUD-9886 could negatively impact

program participants. Should files not be properly secured, an unauthorized third party

could potentially use the form to inappropriately obtain client documentation.

Corrective Action No. MOR-2023-6: This finding may be resolved as part of the file

review required by Corrective Action No.MOR-2023-7d. When responding to Finding

No. MOR-2023-7, Corrective Action No. MOR-2023-7d, please provide the Little Rock

Field Office with copies of the form HUD-9886 for the affected families.

Finding No. MOR-2023-7: The LRHA Does Not Properly Calculate and/or

Document its Calculation of HAP/Participant Rent and the Participant Files Do

Not Allow for a Speedy and Effective Audit.

Condition: As outlined in the MOR section of this report, substantially all

supporting documentation was incomplete, incorrect and/or missing. Additionally,

the organization of the participant files did not allow for a speedy and effective

audit.

Criteria: 24 CFR § 982.158

Cause: We requested a random sample of 56 participant files for review selected by the QAD

from the LRHA PIC submissions. It should be noted that 100% of the files reviewed were

noncompliant.

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

21 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

Effect: We were unable to validate the LRHA calculations of HAP and participant rent or

guarantee proper expenditure of program funds given the error rate. An error rate of 100% is

considered significantly material and constitutes a breach of the Annual Contributions

Contract. The HAP funding provided by HUD to the LRHA is at major risk of inappropriate

expenditure.

Corrective Action No. MOR-2023-7a: No later than 90 days from the date of this report, the

LRHA must obtain HUD or HUD approved contractor training for all HCV-related staff,

including finance and executive staff, that is appropriate for their job classification and roles in

administering the HCV program. For management-level staff, courses taken must include

training regarding quality control. Certifications of training must be provided to the QAD and

the Little Rock Field Office.

Corrective Action No. MOR-2023-7b: The LRHA must develop and implement quality

control procedures to ensure the accuracy of HAP/Participant rent calculations. These

procedures must ensure that LRHA management reviews a significant statistical sample of

each portion of every staff person’s complete portfolio annually. A copy of these procedures

must be provided to the Little Rock Field Office and the QAD as part of this CAP.

Additionally, documentation demonstrating that the LRHA is carrying out quality control

processes must be provided to the Little Rock Field Office and the QAD not less than

quarterly until no longer required. This documentation must include a listing of all files

reviewed for that quarter, the results of the review, and any subsequent actions taken to

correct errors and omissions discovered.

Corrective Action No. MOR-2023-7c: The LRHA must develop processes and procedures

(such as checklists) that ensure similar participant file formats between staff. These processes

must allow for a speedy and effective audit of the LRHA participant files at any time.

Corrective Action No. MOR-2023-7d: The LRHA must conduct a full re-examination of all

participants, converting files to the new, the LRHA-approved format within 365 days of the

date of this letter. The LRHA must provide a certification to the Little Rock Field Office and

the QAD monthly regarding the number of re-examinations completed and the number of files

converted. Please note that this corrective action is intended to ensure that the files are updated

at the annual re-exam. It may not be cost effective or efficient for the LRHA to undertake this

action at any other re-examination type.

Corrective Action No. MOR-2023-7e: The LRHA must incorporate into its HCV

Administrative Plan the quality control processes developed as part of correcting this finding.

A copy of the approved board resolution must be provided to the QAD and the Little Rock

Field Officed.

Corrective Action No. MOR-2023-7f: The LRHA must adopt policies and procedures to

ensure the accurate calculation of asset income. While we recognize that HUD allows self-

certification of assets under $5,000, the LRHA does not appear to have any way of

documenting self-certification. In several files, families appeared to have wage income and

bank accounts, but there was no documentation of verification attempts or even a self-

QAD-FMR-MOR-2023-AR004 REPORT

HOUSING AUTHORITY OF THE CITY OF LITTLE ROCK

ATTACHMENT

22 | QAD- FMR - M O R - 2023 - A R 0 0 4 0 9 / 0 1 / 2 0 2 3

certification. These policies and procedures must be adopted into the LRHA HCV

Administrative Plan.

For both the FMR and MOR Corrective Actions required, the LRHA must provide detailed

supporting documentation that shows corrective action has been taken.

RESOURCES

VMS guidance on RNP and UNP calculation

VMS User’s Manual (Voucher Management System (VMS) Release 17.0.0.0)

Notice PIH-2015-17, Use and Reporting of Administrative Fee Reserves

Office of Housing Choice Vouchers

Documents and Guidance

HUD website that includes Financial Reporting and FASS PH Systems and IMS/PIC. Some of

the information (provided through links) include the following:

- Accounting Briefs

- Financial Data Schedule Line Definition Guide (updated July 2020)

- PIH Notices

CARES Act for Public Housing Agencies

(End of the Report)