INTERNATIONAL MONETARY FUND

Modernizing the Framework for Fiscal Policy and Public Debt Sustainability Analysis

Prepared by the Fiscal Affairs Department and

the Strategy, Policy, and Review Department

Approved by Carlo Cottarelli and Reza Moghadam

August 5, 2011

Contents Page

Executive Summary...................................................................................................................3

I. Introduction ............................................................................................................................4

II. Conceptual Framework and Areas for Improvement ............................................................5

III. Realism of Baseline Projections ..........................................................................................7

A. Realistic Primary Fiscal Balance Paths .....................................................................8

B. Realism of Economic Growth and Interest Rate Assumptions ...............................10

IV. Role of the Debt Level in the DSA ....................................................................................11

V. Improving the Analysis of Fiscal Risks ..............................................................................15

A. Contingent Liabilities ..............................................................................................15

B. Identifying Country-Specific Shocks ......................................................................17

C. Assessing the Impact of Shocks ..............................................................................21

Bound tests .......................................................................................................21

Stochastic simulation methods .........................................................................22

VI. Vulnerabilities Associated with the Profile of Public Debt ...............................................25

VII. Coverage of Fiscal Balance and Public Debt ...................................................................28

A. Expanding the Coverage of the Fiscal Accounts ....................................................28

B. Integrating Long-Run Spending Pressures into DSA .............................................29

C. Assessing Gross and Net Debts ...............................................................................31

VIII. A Risk-Based Approach to DSAs - Implementation ......................................................33

IX. Issues for Discussion .........................................................................................................36

References................................................................................................................................54

2

Tables

1. Debt Ceilings for Selected Members ...................................................................................11

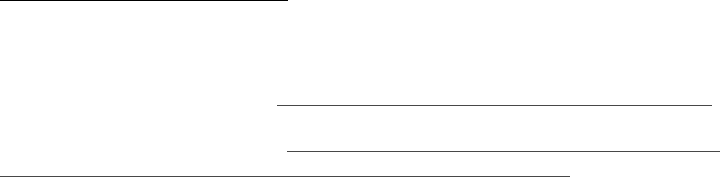

2. Summary of the Cost of Banking Crises..............................................................................16

Figures

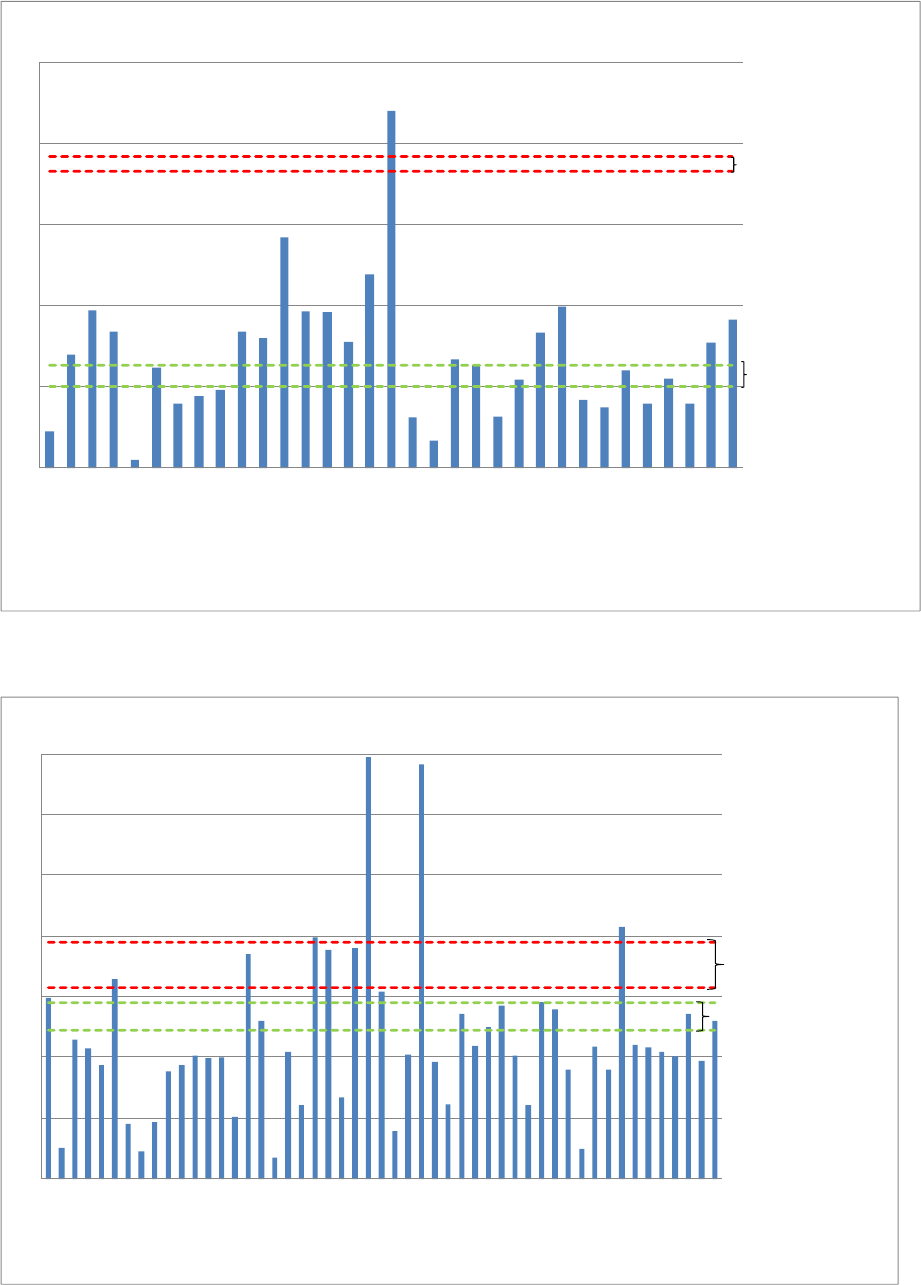

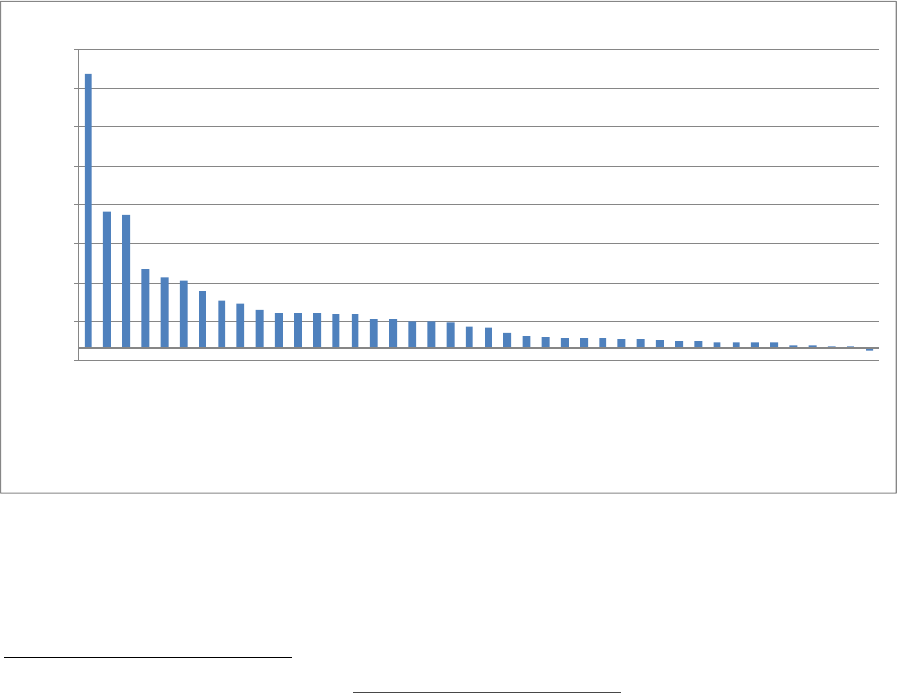

1. Frequency Plots of Maximum Primary Balance ....................................................................9

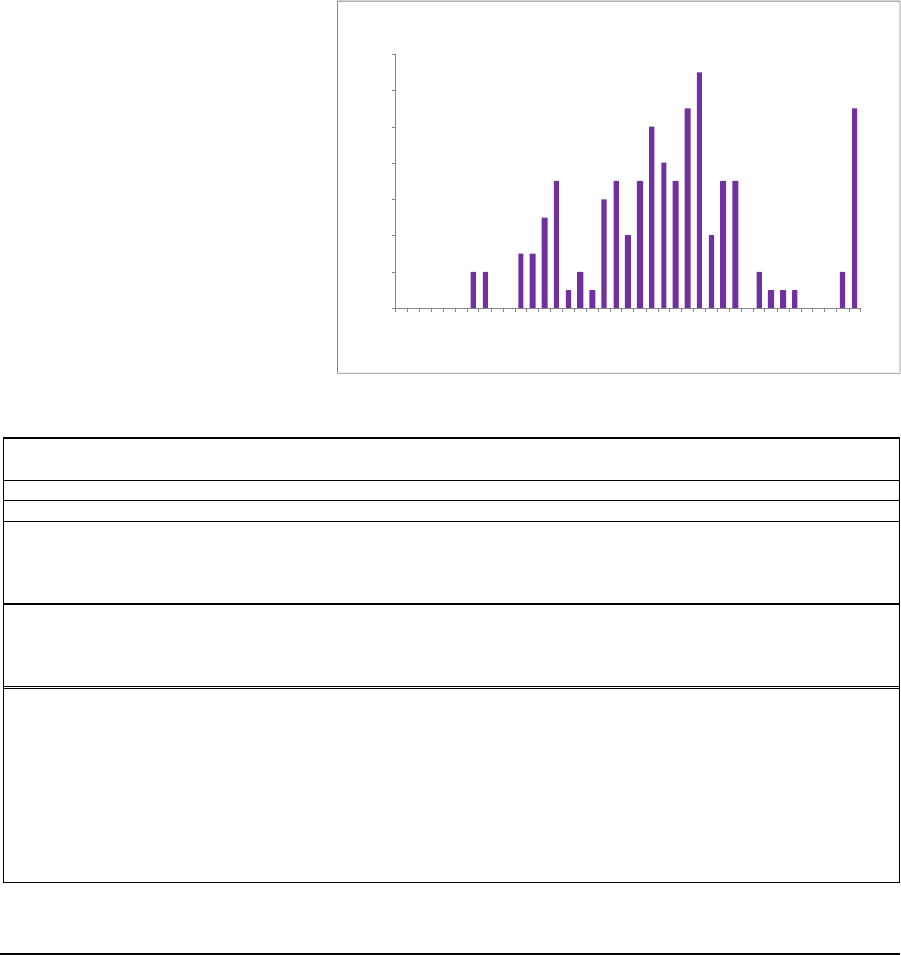

2. Largest Primary Balance Turnaround ..................................................................................10

3a. Long-run Debt and Maximum Sustainable Debt: Advanced Economies ..........................14

3b. Long-run Debt and Maximum Sustainable Debt: Emerging Market Economies ..............14

4. Incidence of Systemic Banking Crises, 1970–2008 ............................................................16

5. Banking Sector Credit to Private Sector Around Debt Distress Events ..............................18

6a. Debt Structure Indicators Around Debt Distress Events....................................................25

6b. Liquidity and Risk Pricing Inidcators Around Debt Distress Events ................................26

7. Country: Debt Profile Vulnerabilities ..................................................................................26

8a. Long-Term Spending Pressures: Advanced Economies ....................................................29

8b. Long-Term Spending Pressures: Emerging Markets .........................................................30

9. Gross Minus Net Debt for Selected Countries, 2010 ...........................................................31

10. Change in Gross vs. Net Debt ............................................................................................32

Boxes

1. Conceptual Framework for Fiscal Policy and Public Debt Sustainability .............................6

2. Using Confidence Intervals to Help Gauge Uncertainty .....................................................23

3. Defining Indicative Benchmarks for Debt Vulnerability Indicators ....................................27

4. Implementation of the Proposed Framework .......................................................................34

Annexes

I. Debt Sustainability Analysis in Selected Countries .............................................................37

II. Overview of Current Framework for Public DSA in Market-Access Countries ................41

III. Estimation of Indicative Public Debt Thresholds ..............................................................43

IV. Using Historical Episodes to Calibrate Tail Risks ............................................................49

V. Defining Gross and Net Debt ..............................................................................................53

3

Executive Summary

Modernizing the framework for fiscal policy and public debt sustainability analysis

(DSA) has become necessary, particularly in light of the recent crisis and rising

sustainability concerns in some advanced economies. While recognizing the inherently

challenging nature of such analysis, this paper highlights areas where improvements are

needed and makes both general and specific proposals on how this could be achieved. It also

proposes to move to a risk-based approach to DSAs for all market-access countries, where

the depth and extent of analysis would be commensurate with concerns regarding

sustainability, while a reasonable level of standardization would be maintained.

DSA could be improved through a greater focus on:

Realism of baseline assumptions. Close scrutiny of assumptions underlying the

baseline scenario (primary fiscal balance, interest rate, and growth rate) would be

expected particularly if a large fiscal adjustment is required to ensure sustainability.

This analysis should be based on a combination of country-specific information and

cross-country experience.

Level of public debt as one of the triggers for further analysis. Although a DSA is a

multifaceted exercise, the paper emphasizes that not only the trend but also the level

of the debt-to-GDP ratio is a key indicator in this framework. The paper does not find

a sound basis for integrating specific sustainability thresholds into the DSA

framework. However, based on recent empirical evidence, it suggests that a reference

point for public debt of 60 percent of GDP be used flexibly to trigger deeper analysis

for market-access countries: the presence of other vulnerabilities (see below) would

call for in-depth analysis even for countries where debt is below the reference point.

Analysis of fiscal risks. Sensitivity analysis in DSAs should be primarily based on

country-specific risks and vulnerabilities. The assessment of the impact of shocks

could be improved by developing full-fledged alternative scenarios, allowing for

interaction among key variables, and more regular use of fan charts. Different tools

and analyses (e.g., FSAP and vulnerability exercises) could be used as inputs to

identify and quantify macroeconomic risks and contingent liabilities risks.

Vulnerabilities associated with the debt profile. The paper proposes to integrate the

assessment of debt structure and liquidity issues into the DSA. Indicative benchmarks

are proposed to facilitate staff analysis in this regard.

Coverage of fiscal balance and public debt. It should be as broad as possible, with

particular attention to entities that present significant fiscal risks, including state

owned enterprises, public-private partnerships, and pension and health care programs.

Based on Directors’ views, specific guidance would be developed in the coming months to

render these proposals fully operational, facilitate country team work, and ensure adequate

implementation. The public DSA template would be revised accordingly.

4

I. INTRODUCTION

1

1. Large increases in public debt in advanced economies (AEs) have brought the

sustainability of fiscal policy and public debt to the forefront of policy discussions. The

recent worsening of the debt outlook in AEs reflects a number of factors, including a sharp

deterioration of fiscal balances during the crisis and, in some cases, government intervention

in the banking sector. This deterioration is in addition to the long-term spending pressures

related to population aging.

2. Before the crisis, Fund analysis did not always pay sufficient attention to public

debt sustainability in market access countries (MACs), particularly in AEs. As

illustrated in Annex I, debt sustainability analysis (DSA) had often turned into a routine

exercise, with mechanical implementation of the DSA template, little discussion of DSA

results, and limited linkages between the DSA and discussion of macroeconomic and

financial policies. While problems with the implementation of the framework are not

universal, with hindsight, it is also clear that the framework has shortcomings that need to

be addressed: for instance, stress testing was not commensurate with the magnitude of the

crisis.

3. These developments make it timely to modernize the framework for public

DSA.

2

The objective of the paper is to highlight areas where improvements are needed and

to make both general and specific proposals on how this could be achieved.

3

This paper not

only suggests new tools to improve the analysis, but also draws attention to existing ones

that could be mobilized in light of interconnections across sectors. Based on Directors’

views on these proposals, more specific guidance would be developed in the coming months

to render them fully operational, facilitate country team work, and ensure adequate

implementation. The public DSA template would be revised accordingly.

4. The paper is organized as follows. Section II presents the conceptual framework

and outlines areas for improvement. Section III discusses issues related to the realism of

projections, particularly the fiscal path underlying baseline scenarios. Section IV analyzes

vulnerabilities associated with the level of public debt. Section V presents ideas to improve

1

This paper was prepared by a staff team led by Said Bakhache (SPR) and Ricardo Velloso (FAD) under the

broad guidance of Dominique Desruelle, Hervé Joly (both SPR), and Paolo Mauro (FAD). The team comprised

Santiago Acosta (FAD), Karina Garcia, Douglas Hostland, Mariusz Jarmuzek, Andrew Jewell, Kadima Kalonji

(all SPR), Andrea Lemgruber (FAD), Keiichi Nakatani, Francois Painchaud (both SPR), Christine Richmond

(FAD), Esteban Vesperoni (SPR), and Li Zeng (FAD).

2

The current DSA framework is briefly described in Annex II.

3

Some of these proposals were made in the past (see Sustainability Assessments – Review of Application and

Methodological Refinements, ) but were not satisfactorily implemented, possibly reflecting a number of issues

ranging from insufficiently specific guidance on implementation, difficulty to find relevant information,

significant resource implications, and a sense of complacency during the “great moderation.”

5

the analysis of fiscal risks. Section VI examines debt vulnerabilities associated with the

profile of public debt. Section VII discusses the appropriate coverage of fiscal balance and

public debt. Section VIII discusses the implementation of the proposed approach. Issues for

discussion are proposed in Section IX.

II. CONCEPTUAL FRAMEWORK AND AREAS FOR IMPROVEMENT

5. The fiscal policy stance can be regarded as unsustainable if, in the absence of

adjustment, sooner or later the government would not be able to service its debt

(Box 1). If no realistic fiscal adjustment can prevent this situation from arising, not only

fiscal policy, but also public debt would be unsustainable. To assess these issues, a DSA

begins with a baseline trajectory for public debt based on the assumptions underlying the

macroeconomic framework. It then tests these baseline assumptions and analyzes how

materialization of various risks would affect the public debt trajectory.

6. The paper proposes ways to improve the various elements that make up the

DSA. The objective is to improve the DSA framework and its use, while remaining realistic

about what can be achieved. Indeed, assessments of sustainability will remain inherently

challenging given the uncertainties associated with many aspects of the exercise. Staff has

identified the following areas where analysis could be improved.

Realism of baseline assumptions. Assumptions underlying the baseline scenario,

particularly the primary fiscal balance path, should be subjected to greater scrutiny,

especially for countries where significant fiscal adjustment is projected.

Level of public debt. Although a DSA is a multifaceted exercise, the paper

emphasizes that not only the trend but also the level of the debt-to-GDP ratio is a key

indicator in this framework. The paper does not propose adopting specific public debt

thresholds, but recommends a more stringent analysis of vulnerabilities when the debt

ratio exceeds a certain level.

Analysis of fiscal risks. Stress testing can be better tailored to country-specific

circumstances with improved identification of relevant risks, including those

associated with contingent liabilities arising from the financial sector, and greater

customization of bounds tests and alternative scenarios.

Vulnerabilities associated with the debt profile. Refinancing risks have typically

been analyzed outside of the DSA framework. The paper proposes to integrate the

analysis of this issue into the DSA, where relevant.

Coverage of fiscal balance and public debt. Off-budget public entities, partnerships

with the private sector, and long-term spending pressures associated with population

aging can have a sizable impact on the evolution of public debt. The paper reiterates

that coverage of public debt should be as broad as possible, with particular attention

to entities that present significant fiscal risks.

6

Box 1. Conceptual Framework for Fiscal Policy and Public Debt Sustainability

Fiscal policy sustainability and public debt sustainability are two inter-related concepts whose analysis is a

complex and multifaceted exercise. The analysis needs to consider: (i) the trajectory of the debt-to-GDP ratio,

both under a baseline scenario and alternative scenarios exploring key fiscal risks;

1

(ii) whether, at a minimum,

the debt ratio stabilizes at a level consistent with an acceptably low rollover risk and with preserving growth;

(iii) the realism of underlying assumptions; and (iv) debt composition, which also affects the likelihood of debt

distress.

The fiscal policy stance can be regarded as unsustainable if, in the absence of adjustment, sooner or later the

government would not be able to service its debt. Specifically, two cases should be distinguished:

The current level of the primary balance might not be sufficient to stabilize the debt-to-GDP ratio (which

therefore would be on an explosive path) but sufficient fiscal adjustment would be realistic (both

economically and politically) to bring the primary balance to a level that is necessary to service public debt.

In this case, while fiscal policy would be currently unsustainable (in the sense that an adjustment in the

primary balance is needed), public debt can be regarded as sustainable.

Alternatively, the primary balance needed to stabilize the debt ratio is politically and/or economically

infeasible. In this case, not only fiscal policy, but also public debt would be unsustainable (solvency problem)

and debt restructuring would be necessary.

2

The higher the level of public debt, the more likely it is that fiscal policy and public debt are unsustainable. This is

because—other things equal—a higher debt requires a higher primary surplus to sustain it. Moreover, higher debt

ratios are usually associated with higher interest rates (and possibly lower growth; see below), thus requiring an

even higher primary balance to service it.

A proper assessment of fiscal policy and public debt trajectory must be based on certain macroeconomic baseline

assumptions, notably economic growth and the interest rate on public debt,

3

as well as the likelihood that fiscal

risks (including those from contingent liabilities) might materialize. Thus, it is critical that the assessment of fiscal

policy and debt sustainability be based on realistic assumptions. It is equally important to stress test the underlying

assessment of both fiscal and debt sustainability with respect to deviations from baseline assumptions for all these

variables. Higher interest rates (possibly stemming from changes in market sentiment) or lower growth

assumptions could, for example, result in less favorable debt dynamics, requiring an increase in the primary

balance needed to stabilize the debt ratio, which could in turn change the assessment of debt sustainability.

Fiscal policy and public debt may be sustainable in the above sense, but the debt level may still be so high that

bringing it down would be recommended. This can occur for various reasons:

A high debt level exacerbates an economy’s vulnerability to shocks: the higher the initial debt level, the

greater the impact of a given increase in interest rates or of a decline in the growth rate on the primary surplus

needed to maintain debt stable. So, countries with a high debt level are more exposed to interest and growth

shocks.

The risk of a rollover crisis depends on the size of borrowing requirements and hence on the level of the fiscal

deficit (which depends in part on the level of the debt, through the size of the interest bill) and the

composition of the debt (e.g., short maturities) and investor base (e.g., a high share of externally-held debt).

Beyond certain levels, the higher the debt level the lower is long-term economic growth (see, for example,

Kumar and Woo, 2010).

4

________________________

1

Assuming that the interest rate on public debt exceeds the growth rate of the economy, the government’s intertemporal budget constraint is

met when the debt-to-GDP ratio is stable. For details see Bartolini and Cottarelli (1994).

2

In principle, assessing whether bringing down debt ratios through a primary adjustment is too costly requires looking at the alternative by

evaluating the costs of bringing down debt ratios through debt restructuring.

3

Potential growth is particularly important not only because it affects directly the evolution of debt-to-GDP ratios given a certain primary

balance, but also because sustaining a larger primary balance is likely to be easier when potential growth is higher.

4

At the same time, for countries with substantial infrastructure needs (e.g., low income countries), it is particularly important to assess whether

an increase in debt that finances public investment could have a positive impact on long-term growth.

7

7. In an environment marked by tight resource constraints, the paper also suggests

adopting a risk-based approach to DSA. While a minimum level of standardization would

be maintained to foster discipline, evenhandedness, and a degree of comparability across

countries, depth of analysis would be tailored to the magnitude of concerns about

sustainability (e.g., level of public debt; need for and size of fiscal adjustment; extent of

fiscal risks; and liquidity issues) or to operational requirements such as the need for “a

rigorous and systematic analysis” of debt sustainability in cases of exceptional access to

Fund resources.

4

8. While the main focus of this paper is on public DSA for MACs, many of the

issues also apply to low-income countries (LICs). The conceptual framework underpinning

the LIC DSA is essentially the same as that for the MAC DSA. However, its implementation

involves different data and operational issues and reflects the prevalence of concessional

financing from the official community. Furthermore, LICs face a number of unique

challenges such as overcoming large infrastructure gaps, which raises questions on how best

to capture the impact of public investment on growth and debt sustainability. LIC DSAs are

also conducted jointly with the World Bank and are more detailed than MAC DSAs,

particularly as regards external debt. In light of these differences with MACs, a review of the

LIC DSA framework will be undertaken separately in a forthcoming paper prepared jointly

with the World Bank. Given the general recognition that the analysis of total public debt in

LICs needs to be given more prominence (relative to the analysis of external public debt),

that review will draw on a number of the proposals made in this paper, with adaptation to

LICs’ specific circumstances when appropriate.

III. REALISM OF BASELINE PROJECTIONS

9. As the first step in the DSA is to derive the projected path of the debt-to-GDP

ratio, a crucial element of DSAs is the realism of the underlying assumptions regarding

the primary fiscal path as well as economic growth and interest rate projections. This

is particularly important in countries where sustainability is contingent upon large fiscal

adjustments. For example, the adjustment in primary balances required for AEs to bring

debt ratios to or below 60 percent of GDP is estimated, on average, at about 8 percentage

points of GDP between 2010 and 2020 (Abbas et al, 2010). Even though fiscal

consolidations of this magnitude were achieved in several cases in the past, they will pose

major challenges and their realism needs to be assessed in light of country-specific

4

Decision No. 14064–(08/18), February 22, 2008, as amended by Decision Nos. 14184–(08/93), October 29,

2008, 14284–(09/29), March 24, 2009, and 14716–(10/83), August 30, 2010.

8

circumstances. Moreover, the potential contractionary impact of fiscal consolidation on

growth needs to be taken into account.

5

A. Realistic Primary Fiscal Balance Paths

10. Cross-country experience provides useful insights about the prevalence of, and

circumstances underpinning, large and sustained primary surpluses.

Large primary surpluses have been frequent, but sustained large surpluses have

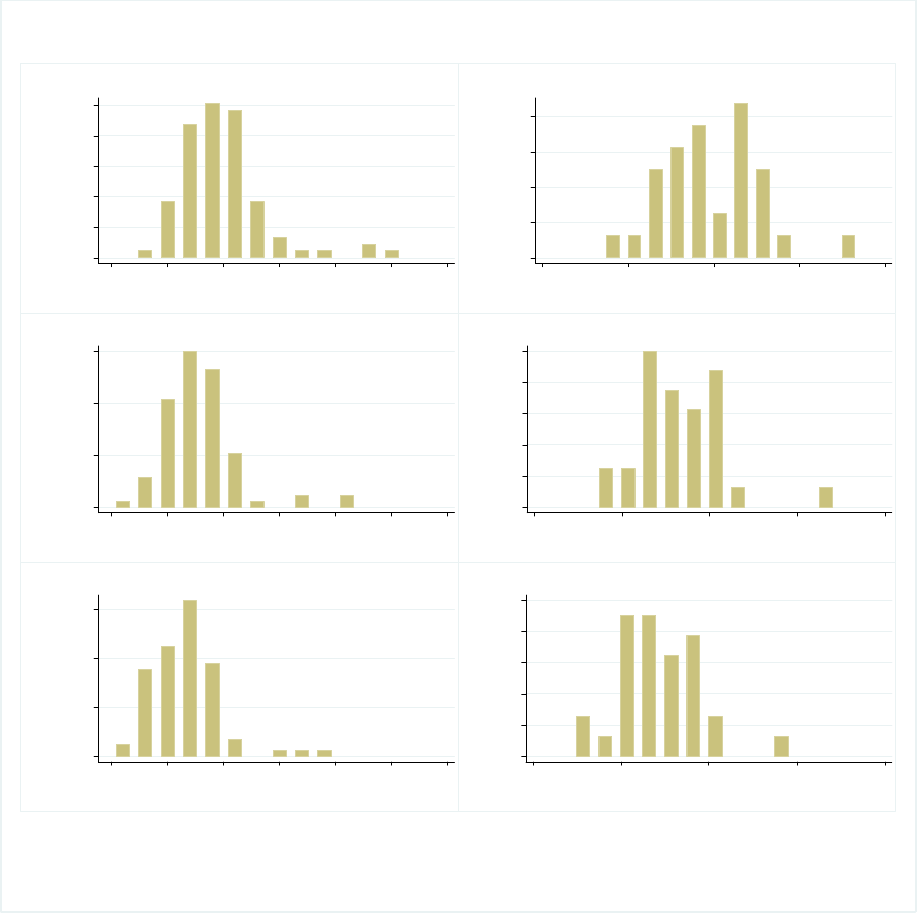

been less common (Figure 1). Out of 87 countries sampled, over 40 percent had a

maximum primary surplus exceeding 5 percent of GDP in at least one year. However,

only16 countries (less than 20 percent) sustained surpluses exceeding 5 percent of

GDP for five years or longer.

Some episodes of sustained large surpluses have been linked to specific conditions

that are not easily applicable to most countries. Out of the 16 countries that recorded

episodes of sustained surpluses, five had this performance in connection to exogenous

factors—large increase in revenue related to natural resources (Botswana, Chile,

Egypt, and Uzbekistan) or transfers arising from customs union membership

(Lesotho).

Episodes of sustained large surpluses in the absence of facilitating exogenous

factors have been limited to 11 countries (13 percent of the sample). A few of these

countries ran large primary surpluses in the absence of a large debt burden (Denmark,

New Zealand, Turkey), but the majority engaged in adjustment at times when they

were facing debt levels above 60 percent of GDP (Belgium, Canada, Dominica,

Israel, Jamaica, Panama, Seychelles, and Singapore).

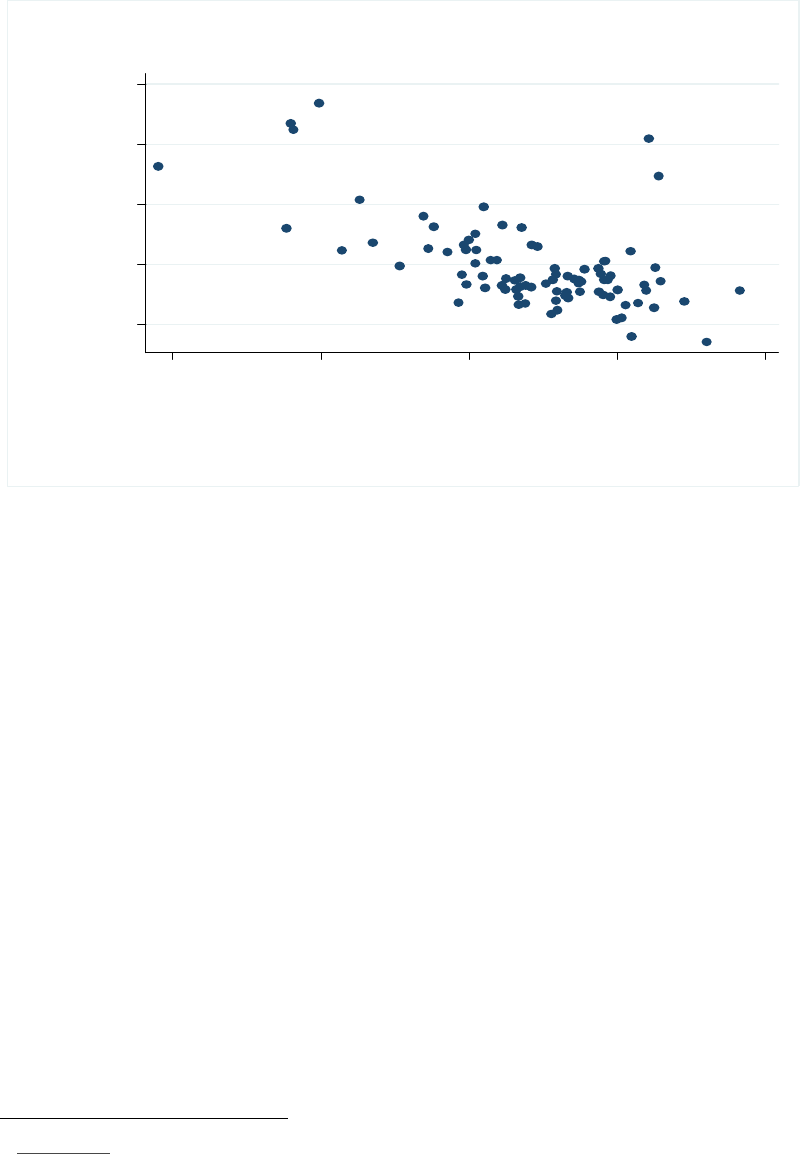

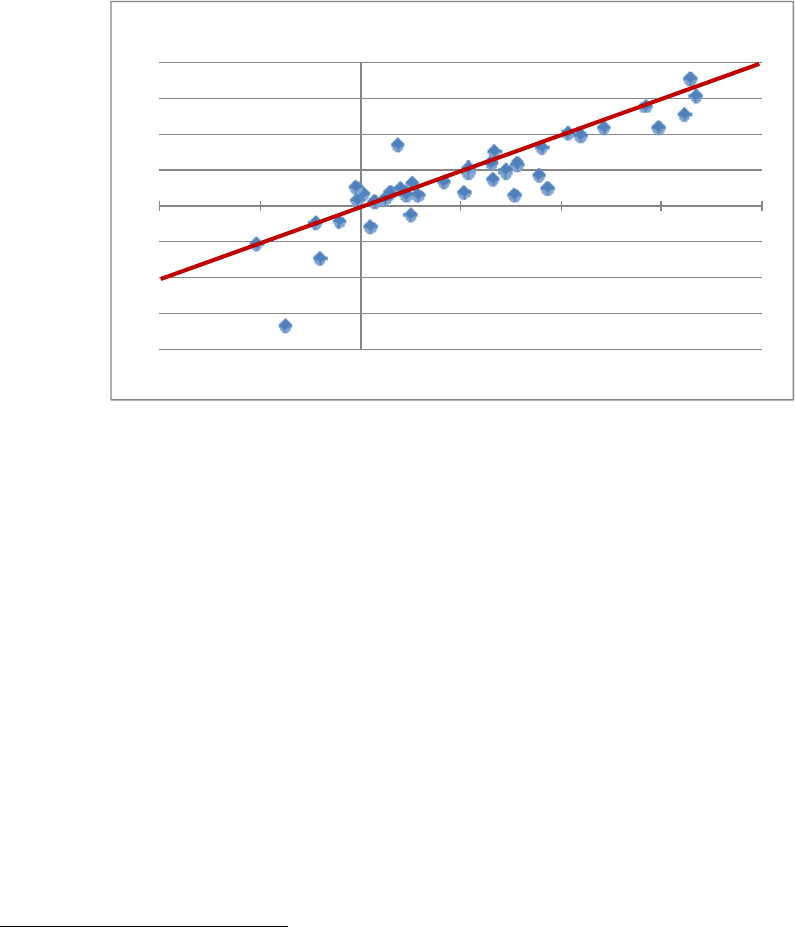

Episodes of significant fiscal correction have been numerous, and the correction

has generally been larger when the starting fiscal position was worse (Figure 2).

There were 30 instances in which countries were able to improve their five-year

average primary balance by at least 5 percentage points of GDP relative to the

average of the previous three years. Larger improvements in the primary balance

were positively correlated with weaker starting fiscal positions; in only 9 episodes,

the ensuing five-year primary balance was equal to or larger than 5 percent of GDP.

5

For example, the October 2010 World Economic Outlook, Chapter III

(https://www.imf.org/external/pubs/ft/weo/2010/02/index.htm

) found that a 1 percent of GDP fiscal

consolidation typically reduces GDP growth by ½ percent within two years.

9

11. In countries where a large fiscal adjustment is planned, this cross-country

experience can be combined with country-specific information to assess the realism of

fiscal projections. If the planned fiscal adjustment is located close to the right-hand tail of

the cross-country distribution of fiscal adjustment (e.g., sustained surplus around 5 percent of

GDP or more), particularly close scrutiny of assumptions would be warranted. Country-

specific information includes past record of fiscal adjustment, extent of political commitment

to adjustment, and the implementation of supporting policy measures. These issues would be

expected to be taken into account in the development of the baseline scenario.

12. Comparisons of the baseline scenario with “no policy change” and historical

scenarios would be particularly helpful to inform the analysis of whether policy actions

and commitments are substantial enough to make a credible break from past or current

trends. This analysis would take account of the design of the authorities’ fiscal adjustment

0 5 10 15 20 25

Frequency

(% of sample countries)

-5 0 5 10 15 20 25

(% of GDP)

Single year, all countries, 87 obs.

0 5 10 15 20

Frequency

(% of sample countries)

-5 0 5 10 15

(% of GDP)

Single year, advanced economies, 32 obs.

0 10 20 30

Frequency

(% of sample countries)

-5 0 5 10 15 20 25

(% of GDP)

5-year moving average, all countries, 87 obs.

0 5 10 15 20 25

Frequency

(% of sample countries)

-5 0 5 10 15

(% of GDP)

5-year moving average, advanced economies, 32 obs.

0 10 20 30

Frequency

(% of sample countries)

-5 0 5 10 15 20 25

(% of GDP)

10-year moving average, all countries, 85 obs.

0 5 10 15 20 25

Frequency

(% of sample countries)

-5 0 5 10 15

(% of GDP)

10-year moving average, advanced economies, 31 obs.

Source: World Economic Outlook database, IMF

1/ Oil and primary product exporters, as defined by the WEO, and HIPC MDRI beneficiary countries are excluded from the sample.

Data are available beginning in 1956 for Japan, in the 1960s and 1970s for another 15 advanced economies, in the 1980s for

about 30 countries, and in the 1990s for the bulk of the sample. The total number of country-year observations is 2061.

(by country, annual data, 1956-2009 1/)

Figure 1. Frequency Plots of Maximum Primary Balance

10

plans, existing legal and institutional mechanisms to support a realistic implementation of

these plans, and experience regarding budget forecast errors.

B. Realism of Economic Growth and Interest Rate Assumptions

13. The interest rate-growth differential plays a critical role in DSA and its

underlying assumptions should be carefully assessed. A strongly negative differential has

been a key benign force for debt sustainability in emerging markets (EMs) and LICs, while

a generally positive differential in AEs has not been favorable for debt dynamics given the

need to run primary surpluses just to ensure debt stabilization.

6

In light of the sensitivity of

debt dynamics to the interest rate-growth differential, the latter deserves proper scrutiny. In

particular, a significant deviation vis-à-vis historical trends and market participants’

forecasts should be fully justified.

14. Experience suggests the need to scrutinize growth and interest rate

assumptions, especially when substantial fiscal adjustment is considered:

Timmermann (2006) found that World Economic Outlook real GDP growth forecasts

showed a tendency to systematically exceed outcomes. This phenomenon was

particularly prevalent in countries with an IMF-supported program. Such bias was

found to be most statistically significant in the next-year forecast.

6

IMF (2011) shows that the interest rate-growth differential in G-20 AEs has been on average 1 percent, while

this differential has been negative in EMs (-4 percent) and LICs (-8 percent).

0 5 10 15 20

Primary balance improvement

(5-year avg. - preceding 3-year avg.)

-15 -10 -5 0 5

(3-year avg. prior to adjustment period)

Source: World Economic Outlook database, IMF

Figure 2. Largest Primary Balance Turnaround

11

Bornhorst et al (2010) pointed out differences between growth forecasts estimated by

WEO and by country authorities in the (post-crisis) medium-term fiscal adjustment

plans prepared in 2010. In AEs with large adjustment needs, growth assumptions

underlying national plans were somewhat more optimistic than WEO or Consensus

Forecast projections. On the other hand, growth assumptions in EMs were largely in

line with WEO and Consensus Forecast projections.

IMF (2011) reported that shocks—especially to economic growth—often derailed

fiscal adjustment amongst 20 episodes of fiscal adjustment plans in G-7 countries.

Some of those plans were derailed almost immediately by unexpected downturns

(e.g., Germany in the 1970s, Japan), while success of some plans was facilitated by

higher-than-expected growth and asset prices (e.g., United States in the 1990s).

7

Differences between interest rate projections in WEO and those done by the

authorities tend to be higher in EMs, while projections are more aligned for AEs.

8

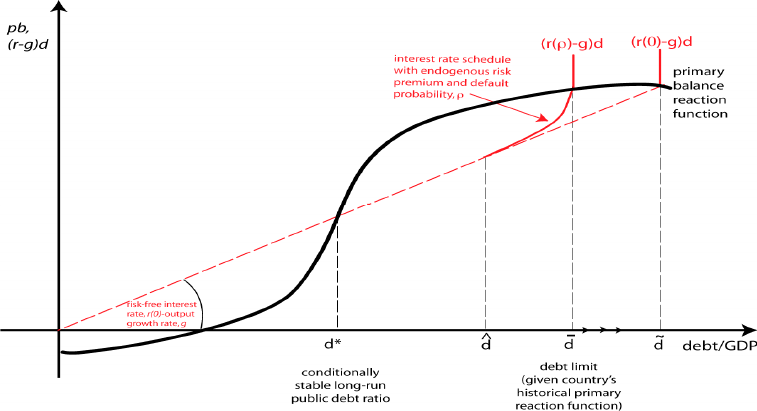

IV. ROLE OF THE DEBT LEVEL IN THE DSA

15. Having determined that the underlying assumptions are realistic, the analysis

turns to examining the projected path of the debt-to-GDP ratio. In this context, not only

the trend, but also the level of the debt-to-GDP ratio is highly relevant in the DSA. For

instance, a (modestly) increasing debt ratio from a “low” initial level may well entail less risk

than a stable but “high” debt ratio. The difficulty lies in defining “high” and “low”—a

definition that is likely to be country-specific. Some countries have indeed run into

difficulties at relatively low

levels of debt, while others have

been able to sustain high levels

of indebtedness for prolonged

periods without experiencing

debt distress. Many countries

have adopted debt ceilings in

their fiscal responsibility laws or

in the context of regional

integration agreements. A

commonly used ceiling is

60 percent of GDP (Table 1).

16. As discussed in Box 1, a high level of debt raises a number of challenges. First,

large primary fiscal surpluses are needed to service a high level of debt; such surpluses may

7

See Mauro (ed.) 2011.

8

See Bornhorst et al (2010).

Member Ceiling

Actual

1

Economic and Monetary Union of the EU 60 85

Eastern Caribbean Currency Union

2

60 103

Individual Countries

Pakistan 60 59

Panama 40 40

United Kingdom 60 77

Source: WEO

1

Actual for currency unions is based on aggregated debt and GDP data.

2

Actual level of debt is at end-2009.

Table 1. Debt Ceilings for Selected Members

(in percent of GDP at end-2010)

12

be difficult to sustain, both economically and politically. Second, a high level of debt

exacerbates an economy’s vulnerability to interest rate and growth shocks. Third, a high debt

level is generally associated with higher borrowing requirements, and therefore exposes a

country to a higher risk of a rollover crisis (i.e., being unable to fulfill borrowing

requirements from private sources or being able to do so only at very high interest rates).

Fourth, high levels of debt may be detrimental to economic growth; while lower growth is a

concern in itself, it also has a direct impact on debt dynamics and debt sustainability in the

long term.

17. Estimating robust thresholds for sustainable levels of public debt in MACs has

proven elusive in previous empirical studies.

9

This may reflect, among others, the many

channels through which high debt levels can lead to debt distress (see above). The empirical

literature on this issue can be summarized as follows. Two related concepts of sustainable

levels of debt have been studied and estimates vary significantly (Annex III):

The “long-run debt level” is the level to which the debt-to-GDP ratio converges over

the long run, as long as the actual debt-to-GDP ratio does not rise above the maximum

sustainable debt level (defined below). Estimates are derived using fiscal policy

track records and historical averages for growth and interest rates. Across

previously existing empirical studies, cross-country median estimates range from

50 to 75 percent of GDP for AEs, while the one available estimate for EM is

25 percent of GDP.

10

The “maximum sustainable debt level” is the level beyond which a debt distress event

is likely or inevitable. Estimates are based either on identification of defined debt

distress events, with statistical approaches used to estimate related debt thresholds, or

on evaluation of policy reaction functions to increasing levels of debt. For AEs,

median estimates range from 80 to 192 percent of GDP, while for EMs the range is

35 to 77 percent of GDP.

18. Staff analysis based on more recent data confirms the difficulty of defining

generally applicable debt thresholds, while pointing to an improved ability of EMs to

carry debt.

9

See Ghosh (2011); Ostry et. al. (2010); IMF, 2003, World Economic Outlook, Chapter III

(http://www.imf.org/external/pubs/ft/weo/2003/02/

); and Hemming et al (2003). Much work has been done on

the sustainable level of external debt – for example, Reinhart et al (2003) and Manasse et al (2003) –

particularly in light of the crises of the 1990s.

10

In this and subsequent bullets, estimates refer to average values of each individual study’s country sample.

Individual country estimates vary widely.

13

A re-estimation of public debt thresholds for a sample of EMs for the period 1993–

2009 gives a range of 49–58 percent for the long-run debt level and 63–78 percent for

the maximum sustainable debt level (Annex III).

11

These estimates, particularly those relating to long-run debt levels, are significantly

higher than earlier ones, which reflect the improved fiscal performance of EMs over

the past decade. Estimated long-run debt levels for EMs are also now closer to the

most recent estimates for AEs based on Ostry et al (2010).

19. The dispersion of empirical findings precludes introducing formal sustainability

thresholds in MAC DSAs, but they provide a useful reference to determine when to

conduct deeper analysis. As indicated above, many countries use a ceiling of 60 percent of

GDP as an anchor for fiscal policy. This ceiling is relatively close to the most recent

estimates of long-run debt levels for both AEs and EMs. As of end-2010, the public debt

level for 19 AEs and 9 EMs was close to or exceeded the 60 percent mark (Figures 3a and

3b). A possible way to use this reference in DSAs would be as follows. When public debt

exceeds or is projected to exceed 60 percent of GDP for a substantial part of the projection

horizon, particularly in the baseline scenario, a detailed discussion of potential risks to

sustainability arising from high debt levels would normally be expected. In this approach, the

reference to 60 percent of GDP should not be construed as a level beyond which debt distress

is likely or inevitable, nor should it be used to judge whether debt is sustainable or not.

Rather the reference point should be used as an indication that more analysis is needed.

While a single reference ratio would be applied to both AEs and EMs for simplicity, this

approach should recognize that potential risks are country specific and that debt below

60 percent of GDP may not be safe in some countries. As a result, a detailed analysis may be

needed where debt distress happened at lower debt levels (e.g. in some EMs), even if debt

were projected to remain below the reference point. Indeed, the presence of other

vulnerabilities (for example, stemming for fiscal risks or debt structure) would call for in-

depth analysis even for countries where public debt is below 60 percent of GDP.

11

The estimates for maximum sustainable debt level are broadly similar to those obtained by the application of

a probit regression model using a sample of 155 middle-income and low-income countries. This model has been

used to estimate external public debt thresholds for LICs, taking account of the impact of institutional and

policy implementation capacity. The forthcoming paper on reforming the LIC DSA framework will provide

further details.

14

Long-run debt range

(Ostry et al,2010)

Max sustainable debt range

(Ostry et al ,2010)

0

50

100

150

200

250

Australia

Austria

Belgium

Canada

Hong Kong SAR

Cyprus Republic

Czech Republic

Denmark

Finland

France

Germany

Greece

Iceland

Ireland

Israel

Italy

Japan

Korea

Luxembourg

Malta

Netherlands

New Zealand

Norway

Portugal

Singapore

Slovak Republic

Slovenia

Spain

Sweden

Switzerland

Taiwan Province of China

United Kingdom

United States

Figure 3a. Long-run Debt and Maximum Sustainable Debt: Advanced Economies

(percent of GDP, end-2010)

Source: WEO and Ostry et al (2010)

Long-run debt range

(staff estimates)

Max sustainable debt range

(staff estimates)

0

20

40

60

80

100

120

140

Albania

Algeria

Argentina

Armenia

Bosnia&Herzegovina

Brazil

Bulgaria

Chile

China

Colombia

Costa Rica

Croatia

Czech Republic

Dominican Republic

Ecuador

Egypt

El Salvador

Estonia

Georgia

Guatemala

Hungary

India

Indonesia

Israel

Jamaica

Jordan

Kazakhstan

Latvia

Lebanon

Lithuania

Macedonia

Malaysia

Mexico

Morocco

Pakistan

Panama

Peru

Philippines

Poland

Romania

Russia

Serbia

South Africa

Sri Lanka

Thailand

Tunisia

Turkey

Ukraine

Uruguay

Venezuela

Vietnam

Figure 3b. Long-run Debt and Maximum Sustainable Debt: Emerging Market

Economies, (percent of GDP, end-2010)

Source: WEO and Fund Staff estimates

15

V. IMPROVING THE ANALYSIS OF FISCAL RISKS

20. The current public DSA framework assesses risks around the baseline scenario

mainly through standardized sensitivity analysis. Stress tests are applied to the baseline

scenario to illustrate the potential impact of adverse shocks on the debt path. Macroeconomic

shocks are generally reported in a standardized way for all countries.

21. Risks, however, vary considerably across countries. Examples of risks that

materialized and resulted in a substantial rise in public debt range from large exchange rate

depreciations to systemic banking crises and include off-budget entities that were bailed out

by governments.

22. The analysis of contingent liabilities in DSAs has typically been too succinct and

uniform, which stands in sharp contrast to the actual impact of the materialization of

such liabilities on public debt. DSAs rarely discuss contingent liabilities in any significant

detail. The related stress test is not particularly informative as it assumes the same

10-percent-of-GDP shock for all countries regardless of the size and risk of materialization of

contingent liabilities in each country.

23. Thus, this section suggests placing greater emphasis on contingent liabilities and

proposes ways to improve the analysis of country-specific fiscal risks.

12

It points to

various tools that could be used to improve the identification of such risks. It also suggests

ways to enrich the analysis of the impact of shocks on the debt outlook.

A. Contingent Liabilities

24. Strengthening the analysis of contingent liabilities is critical given the scope and

magnitude of off-budget risk materialization. Both financial and non-financial sectors

have historically benefited from government financial interventions, including financial

support provided by the central bank.

13

These interventions arose out of explicit and implicit

guarantees to various public entities including sub-national governments and state-owned

enterprises (SOEs) and banks, explicit or implicit guarantees embedded in public-private

partnerships (PPPs), or support to private companies that were deemed too big to fail.

14

12

Fiscal risks are defined as “deviations of fiscal outcomes from what was expected at the time of the budget or

other forecast,” and may arise from macroeconomic shocks and the realization of contingent liabilities. See

Cebotari et al (2009).

13

Cebotari (2008) and chapter 4 of the Public Sector Debt Statistics Guide (http://www.tffs.org/PSDStoc.htm)

provide useful outlines of the typology of contingent liabilities.

14

It is particularly important to report properly on and assess carefully fiscal risks from public interventions

aimed at restoring confidence in the markets and stabilizing financial conditions. In the case of the recent global

financial crisis, these interventions have been carried out rapidly and by a wide range of institutions, with

different reporting and oversight mechanisms. They include liquidity injections; the resolution of financial

(continued)

16

25. Assistance to the financial sector has been particularly costly. Systemic banking

crises have not only been frequent, but they have often carried heavy fiscal costs (Figure 4

and Table 2). The estimated increase in public debt in the wake of a banking crisis often far

exceeds the size of the contingent liability shock in the current DSA template.

15

The median

overall increase in public debt,

which reflects both direct and

indirect effects of banking

crises, is close to 20 percent of

GDP. However, the large

variation across countries

suggests that a standardized

shock is not likely to

meaningfully capture the impact

of banking crises on public debt

(although it remains as a default

option when detailed

information on contingent

liabilities is not available).

institutions with public support through closure, nationalization, recapitalization, or mergers; the establishment

of funds to purchase troubled securities from financial institutions; and extensions of deposit and other

guarantees.

15

The cost of banking crises include the impact of government bailout, the shortfall in revenue due to the

resulting economic downturn, and the stimulus packages that often accompany some the banking crises.

Typically, the cost is partially covered by asset recovery.

Direct Fiscal Costs

1

Increase in Public Debt

2

Output Losses

3

Old crises (1970-2006)

Advanced economies 3.7 36.2 32.9

Emerging markets 11.5 12.7 29.4

All 10.0 16.3 19.5

New crises (2007-2009)

4

Advanced economies 5.9 25.1 24.8

Other economies 4.8 23.9 4.7

All 4.9 23.9 24.5

Source: Laeven and Valencia (2008 and 2010)

Medians (% of GDP)

1

Direct fiscal costs include fiscal outlays committed to the financial sector from the start of the crisis (t) up to t+5 (or up to end-2009 for the

recent crises), and capture the direct fiscal implications of intervention in the financial sector.

4

New crises include Austria, Belgium, Denmark, Germany, Iceland, Ireland, Latvia, Luxembourg, Mongolia, Netherlands, Ukraine, United

Kingdom, and the United States.

Table 2. Summary of the Cost of Banking Crises, 1970-2009

2

The increase in public debt is estimated by computing the difference between pre and post-crisis debt projections, measured in percent

of GDP over [T-1, T+3], where T is the starting year of the crisis. For the 2007-2009 crises, debt reflects fall WEO projections from the year

before the crisis year as pre-crisis debt figures (i.e., September 2006 WEO for the UK and US and October 2007 WEO for all other recent

crises) and the Spring WEO 2010 debt projections for the post-crisis debt figures. For past episodes, the actual change in debt is

reported.

3

Output losses are computed as deviations of actual GDP from its trend over a period of three years from the start of the crisis.

0

2

4

6

8

10

12

14

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

Number o f Countries

Figure 4. Incidence of Systemic Banking Crises, 1970–2008

Source: Laeven and Valencia (2008 and 2010)

17

26. Guarantees for SOEs and PPPs often pose sizable risks. For instance, in Chile,

revenue guarantees granted to airport and toll-road concessionaires were estimated to have

created government exposure of about 4 percent of GDP. In Portugal, guarantees of SOEs

debt amount to about 7 percent of GDP.

16

27. Demands on the government arising from natural disasters have been

substantial in some cases. In small economies, the cost of natural disasters relative to the

size of the economy can be very large. For instance, in 2004, hurricane Ivan inflicted damage

estimated at about twice the size of Grenada’s GDP. Even in larger countries, natural

disasters can have sizeable costs. For example, the recent earthquakes in New Zealand are

estimated to have cost the central government about 4 percent of GDP.

B. Identifying Country-Specific Shocks

28. Identification of relevant country-specific shocks can be based on a combination

of cross-country and individual experience. Different tools can be used to identify risks

stemming from macroeconomic imbalances, private sector liabilities, off-balance-sheet

public sector liabilities, and other shocks like natural disasters.

Sensitivity of public debt to economic shocks

29. Identification and calibration of risks arising from exchange rate depreciation

could be informed by exchange rate assessments done using CGER

17

(or other)

methodologies. For example, in cases where the exchange rate is found to be overvalued

(undervalued), an exchange rate shock of at least the maximum estimated magnitude of the

overvaluation (undervaluation) would be expected in the DSA, recognizing that exchange

rate adjustment may be accompanied by some overshooting.

30. More generally, the vulnerability exercises for emerging and advanced

economies as well as the spillover reports could be used to identify macroeconomic

risks.

18

The vulnerability exercises provide sectoral risk ratings (low, medium, and high risk)

for each country covered by the exercise. A medium or high risk rating in a certain sector

would warrant further investigation of the source of the vulnerability, which could suggest

relevant macro risks to include in the DSA.

16

See Cebotari et al (2009) for further evidence.

17

CGER refers the methodologies used by the IMF’s Consultative Group on Exchange Rate Issues (CGER).

For further information please see

http://www.imf.org/external/np/sec/pr/2006/pr06266.htm.

18

For more information, please see http://www.imf.org/external/pp/longres.aspx?id=4479, and

http://www.imf.org/external/pubs/ft/survey/so/2011/CAR090211B.htm

.

18

Risk of transformation of private debt into public debt

31. Rapid credit growth,

asset price bubbles, and

sustained surges in capital flows

have been shown to precede

banking crises.

19

Banking sector

credit to the private sector is

particularly relevant in this regard.

Staff analysis shows that the ratio

of domestic private sector credit to

GDP is an efficient predictor of

sovereign debt distress

(Figure 5).

20

32. Indicators of banking sector credit, in combination with other relevant financial

indicators, could thus inform decisions on the merit of running a “tail risk” scenario or

a bound test incorporating a financial crisis. Naturally, to avoid misunderstandings, it

would be important to clarify the rationale and goal of such exercises, which should not be

misconstrued as predicting a financial crisis or suggesting that the public sector should bail

out private firms. Rather, stress testing contingent liabilities that may arise from the financial

sector should be seen as an analytical exercise (similar to stress testing other shocks) to be

used to inform the authorities’ approach to dealing with macro-financial issues. Such an

exercise may well result in consideration of further regulatory and supervisory efforts to

minimize the risk of financial sector difficulties. In many cases, the authorities may be

already taking appropriate action to mitigate relevant risks or draw up contingency plans. In

others, stress tests may give further impetus to undertake risk-reducing actions. As with other

sensitive issues addressed in Fund surveillance, communication challenges stemming from

such stress testing would be handled in the framework set by existing policies on

transparency.

33. The financial stability assessment component of the FSAP sheds important light

on the extent of financial sector risks.

21

In particular, FSAPs include estimates of capital

19

See Laeven and Valancia (2010), Reinhart and Rogoff (2009), Mendoza and Terrones (2008), and Kaminsky

and Reinhart (1999) for further details.

20

This analysis suggests a domestic banking sector credit to the private sector-to-GDP ratio above 70 percent

provide an early warning signal of sovereign debt distress. Values around debt distress episodes (Figure 5) are

lower than the threshold because they are averages that do not reflect the optimization criteria used in the signal

approach. It should be noted also that an increase in this indicator may reflect financial deepening particularly in

countries undergoing structural reforms.

21

For more information on the Financial Sector Assessment Program (FSAP), please see

http://www.imf.org/external/np/exr/facts/fsap.htm

.

36

38

40

42

44

46

48

50

52

54

56

T

-5

T

-4

T

-3

T

-2

T

-1

T

T+1 T+2 T+3

T - year of debt distress

Source: World Economic Outlook

Figure 5. Banking Sector Credit to Private Sector around Debt Distress Events

(in percent of GDP)

19

shortfalls in the financial sector under a range of stress tests. While these capital shortfall

estimates should not, and hopefully would not, automatically become public liabilities in the

event financial stresses do arise, they provide valuable indications on the merit of reflecting

financial sector risks in DSAs. The size of the banking sector is also likely to have a bearing

on the impact of the financial sector contingent liability on the sustainability of public debt.

34. Various possibilities to reflect FSAP results in DSA exist, where relevant. One

approach would be to calibrate bound test(s) using stress test estimates of the capital

shortfalls of the systemic (or largest) banks.

22

Another approach would be to use results from

the FSSA’s risk assessment matrix (RAM). For instance, for risks that have a medium or

high impact on the banking sector, the public DSA could include a contingent liability shock

equivalent to half of the impact on the capital base. The size of the shock could be further

calibrated to take into account factors such as the nature of the banking sector (e.g., extent of

state ownership) and current market conditions (e.g., ability of private sector to raise capital).

In cases where risks stemming from the financial sector are high, a more ambitious step

would be to undertake a joint stress test of the financial sector and public debt. Joint stress

testing could focus first on simple feedbacks while understanding of the complex macro-

financial linkages is being developed. For example, where feasible, joint stress testing could

involve using the same underlying assumptions, and allowing contingent liabilities arising

from the financial sector to feed into the fiscal projections and vice versa.

23

It should be

recognized that full-fledged general equilibrium stress tests may not be feasible even for

AEs, and the extent to which this ideal can be approached will vary from country to country.

35. Where available, the balance sheet approach (BSA) can also play a useful

complementary role in identifying risks to public debt. The BSA focuses on the structure

of assets and liabilities of the main sectors of the economy and on key linkages across

sectors. The BSA can help identify vulnerabilities in different sectors, including the non-

financial corporate and household sectors, by providing information on different sectors’ net

financial position, net foreign currency position, and net short-term position. The BSA could

therefore help point to potential sources of contingent claims under adverse macroeconomic

scenarios.

24

25

Consideration could be given to encouraging the conduct of BSA in cases

22

Important issues related to the conduct of the FSAP may affect how and the extent to which the results of the

FSAP can be used in public DSAs. For example, in addition to the size of shocks being ad hoc, reporting of the

results of stress testing is not standardized with quantification often absent from the main report. It is intended

that the use of FSAP results in the DSA be done in the context of existing policies on confidentiality of

information.

23

Work in this area would involve close collaboration between various departments, including MCM.

24

Existing methodologies, such as the contingent claims approach (CCA), could be used where data is available

to inform this judgment. The CCA uses information based on the financial sector balance sheet, in addition to

market prices and measures of uncertainty, to derive forward-looking indicators of potential fiscal costs. See

Gapen et al (2005) for further information.

20

where, for example, the external debt sustainability analysis points to high and potentially

unsustainable levels of private sector external debt.

Transformation of off-balance-sheet public liabilities into on-balance-sheet public

liabilities

36. Obligations arising from PPPs and SOEs can be reflected in DSA in a number of

ways that depend on the extent of available information.

26

PPP contracts give rise to

obligations on the government to purchase services from a private operator and to honor calls

on guarantees. These obligations can influence debt sustainability in much the same way as if

the government had incurred debt to finance public investment and provided services itself.

Country teams could present information on the present value of liabilities under PPPs or

other concession arrangements. There are two ways to take non-debt obligations into account

when undertaking debt sustainability analysis. First, the net present value of future

payments—such as under PPP contracts—could be added to public debt. Debt sustainability

would then be judged by reference to public debt plus non-debt obligations. Second, an

analytically equivalent approach is to count known and potential costs of non-debt

obligations as primary spending.

27

More generally, the emphasis should be placed on

conducting scenario analyses that correspond to alternative degrees of risk exposure to test

debt projections under different assumptions about the materialization of contingent

liabilities.

37. The impact of natural disasters should be reflected in DSAs for countries prone

to recurrent floods, earthquakes, and other disasters (e.g., Caribbean islands). Baseline

scenarios do not take into account such disasters, even though they affect regularly many

countries that are not fully insured against such disasters. Alternative scenarios could be

developed using historical evidence on the frequency and cost of natural disasters.

28

25

Insights based on BSA concepts have been used in Fund surveillance for some time to inform the buildup of debt-

related vulnerabilities. Rosenberg et al

(2005) details the benefits of the BSA in Argentina (2001), Turkey (2001),

and Uruguay (2002). Iceland Selected Issues (http://www.imf.org/external/pubs/cat/longres.aspx?sk=24255.0

) is a

recent application of the BSA and that is used to inform the public debt sustainability analysis. Improvements in the

availability of data necessary for the application of the BSA have facilitated the conduct of the exercise, although it

remains resource intensive.

26

Guidance on the identification and quantification of fiscal risks due to contingent liabilities may be found in

Cebotari (2008), Cebotari et al (2009), Everaert et al (2009), Hemming (2006), and Irwin (2007).

27

While this approach could be applied to other legal obligations, extending it to implicit contingent liabilities

could be difficult to implement because the government may be able to constrain spending that it is not legally

bound to undertake.

28

A useful resource in this regard is the comprehensive database on natural disasters compiled and maintained

by Centre for Research on the Epidemiology of Disasters (CRED) at the Catholic University of Louvain

(http://www.emdat.be

/).

21

C. Assessing the Impact of Shocks

38. Bound tests, alternative scenarios, and stochastic simulations are different

methods to examine the impact of shocks on the debt trajectory.

29

The first two are used

to assess the impact of specific shocks, while stochastic simulations typically capture the

uncertainty surrounding the baseline scenario by examining the impact of a series of shocks

drawn from historical experience. Bound tests currently used in the DSA template are

relatively mechanistic, with generally only one variable shocked at a time, while history

suggests that shocks tend to be correlated. Another issue is whether existing bound tests are

always relevant, and conversely whether they capture all relevant shocks. This section

proposes improvements to the way bound tests are set up in the current framework and

suggests that fan charts from stochastic simulations could be used more widely.

Bound tests

39. An examination of historical episodes of large public debt increases suggests that

there is room to enhance the assessment of shocks, in particular “tail risks,” using the

current bound test approach. The current framework includes one macroeconomic stress

test—a 30 percent exchange rate depreciation—that is in the realm of tail risks compared to

the other less extreme, but more likely, stress tests. Looking back at the historical record

across a wide spectrum of countries, there have been several episodes where public debt

burdens have increased significantly over the space of just a few years (Annex IV). Although

the circumstances surrounding such episodes vary greatly, there are a few empirical

regularities that could be reflected in the analysis of macroeconomic shocks.

Growth collapses and large terms of trade shocks appear to have played a

prominent role in episodes of large public debt increases, which is not reflected in

the current stress tests. For example, in one half of episodes where real GDP growth

was negative over a five-year period, public debt increased by more than 14 percent

of GDP.

30

Similarly, in one half of episodes where the terms of trade deteriorated by

more than 25 percent in one year, public debt increased by more than 11 percent of

GDP.

The assessment of risks can be enhanced by taking into account linkages observed

between some key macro variables after certain shocks. For example, in episodes

29

Bound tests refer to the stress-testing used in the DSA templates to assess the impact of specific shocks to

certain key variables. Alternative scenarios refer to more elaborated scenarios, either standardized (e.g., no

policy change) or tailor made.

30

The frequency and size of growth “down-breaks” (statistically significant permanent reduction in growth) are

relatively large. Fifteen percent of a sample of 88 middle-income and advanced economies experienced at least

one such growth down-break with an average size of 4.7 percent, which is much higher than the negative shocks

implied by the bound test approach for the same period. See Berg et al (2008) for further details.

22

where the nominal exchange rate depreciated by more than 30 percent in one year

against the U.S. dollar, the inflation rate increased significantly, and real GDP growth

declined sharply relative to its historical trend. Banking crises, growth collapses, and

large terms of trade shocks tend to coincide with large output losses, exchange rate

depreciations, and higher inflation, all of which affect the public debt outlook. The

impact of such shocks can be made more realistic by taking into account how output,

inflation, and the exchange rate evolved over the course of the historical episodes.

Alternatively, country teams could develop full-fledged scenarios to capture country

specific linkages among key variables (such as endogenous increases in cost of

borrowing) not reflected in stress tests.

Stochastic simulation methods

40. Stochastic simulation methods could be applied to improve estimates of

uncertainty surrounding baseline debt projections and enhance assessments of fiscal

risks. The current configuration of stress tests provides a rough estimate of uncertainty

surrounding debt projections, and the persistence of shocks is calibrated in an ad-hoc

manner.

31

The individual shocks do not allow for feedback between key macroeconomic and

fiscal variables. Box 2 illustrates the usefulness of confidence intervals generated on a

country-specific basis, based on empirical models that take into account interaction between

key variables. The dynamics of the underlying empirical models determine the persistence of

shocks, which can vary greatly across countries, providing an additional dimension of

realism.

41. Stochastic simulations could be encouraged for countries where data are

available. The coming on line of new data and tools since the issue of stochastic simulations

was last discussed by the Board (see Sustainability Assessments – Review of Application and

methodological Refinements) suggests that they could be used more widely, and indeed they

have been more prevalent in staff analysis.

32

Confidence intervals however are sensitive to

model specification and the sample period used for estimation (Box 2). They may also not be

particularly useful in cases where there have been structural shifts, for example in the

conduct of policy (such as change in exchange rate regime and fiscal/monetary policy

objectives/tools). Consideration could be given to developing guidelines to ensure that the

31

The most extreme stress test is estimated to occur with a likelihood of 15 to 30 percent for MACs and around

25 percent for LICs. The duration of shocks is five years for MACs and two years for LICs.

32

Most applications to date have been based on vector autoregressive models using quarterly data, which are

available for around 40 countries, the majority of which are AEs. Examples include fan charts for public debt

projections for Greece, the UK, Germany, and the US reported in the November 2010 Fiscal Monitor and for

Greece, Ireland, Italy, Portugal and Spain reported in the Fall 2010 Vulnerability Exercise for Advanced

Economies. Recent examples of cases where DSAs in staff reports have included fan charts include Morocco

,

Mauritius

, El Salvador, Indonesia, Israel, and Costa Rica.

23

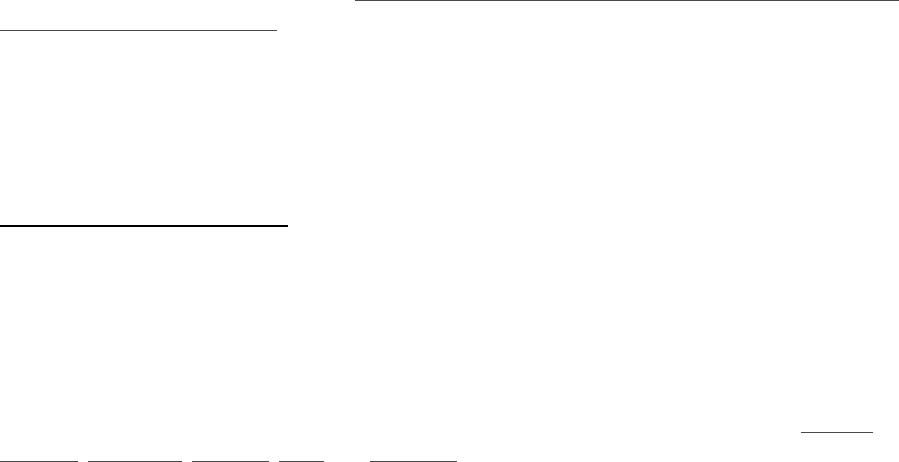

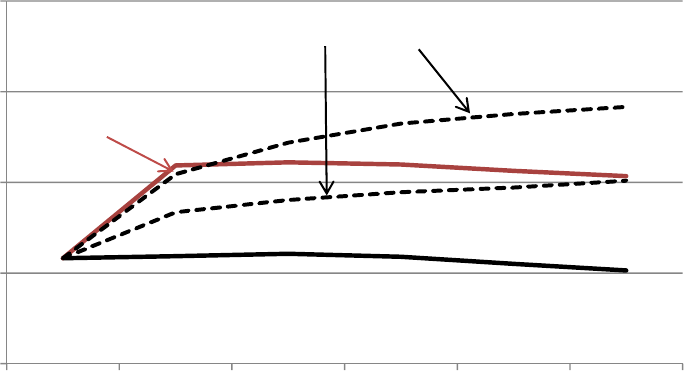

Box 2. Using Confidence Intervals to Help Gauge Uncertainty

Confidence intervals generated using stochastic simulation methods provide a well-defined measure of

uncertainty surrounding debt projections. This is illustrated using data for a market access country. Stochastic

simulation methods are applied to a vector autoregressive (VAR) model, estimated using annual data over the

period 1995–2010, to generate a probability distribution for the public debt-to-GDP ratio over a five-year

projection period (2011–2015). Public debt is projected to decline in the baseline projection scenario, reaching

75 percent by 2015 (Figure a). Under the most extreme shock reported in the current public DSA framework,

public debt increases to 92 percent of GDP by 2015, 17 percentage points above the baseline projection.

Stochastic simulations indicate that the there is a 25 percent probability that public debt would exceed

80 percent of GDP by 2015 (the 75

th

percentile) and a 10 percent probability that it would exceed 85 percent

(the 90

th

percentile), implying that the growth shock is not a likely outcome based on recent historical

experience.

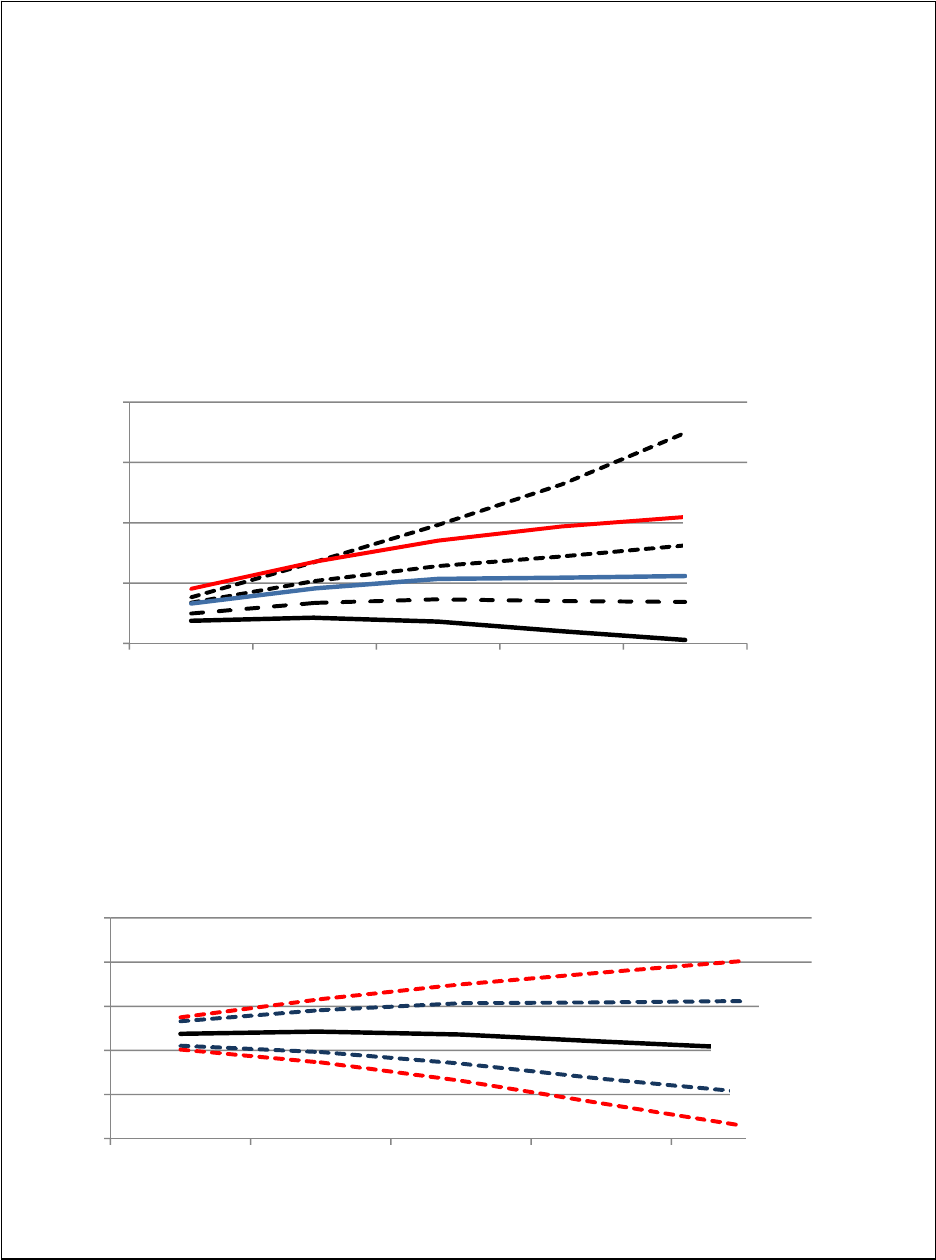

Confidence intervals can be sensitive to model specification issues and the sample period used for estimation.

For example, confidence intervals generated using an autoregressive (AR) model are significantly wider than

those generated using a VAR (Figure b), indicating the underlying dynamic specification and covariance of

shocks play a prominent role in deriving measures of uncertainty surrounding debt projections.

75

80

85

90

95

2011 2012 2013 2014 2015

Public Debt / GDP (percent)

Source: IMF Staff calculations.

Figure a. Percentiles Generated using a VAR model

75th percentile

Real interest rate shock

Growth shock

Baseline projection

Combination shock

90th percentile

65

70

75

80

85

90

2011 2012 2013 2014 2015

Public Debt / GDP (percent)

Source: IMF Staff calculations.

Figure b. Confidence Intervals Generated using a VAR versus AR Model

AR model

Baseline

projection

AR model

VAR model

24

statistical foundations of the analysis are sound and comparability across countries is

maintained to the greatest extent possible, while realizing that the DSA is a tool best used for

single country analysis.

33

A possible approach that recognizes the resource intensity of this

exercise and ensure more cross country comparability would be to generate confidence

intervals centrally for countries where data are available. This however would not preclude

country teams from tailoring stochastic simulation models to country-specific circumstances.

In cases where stochastic simulations are not considered useful or cannot be conducted,

country teams would be expected instead to develop well-specified and full-fledged

alternative scenarios to analyze risks.

42. Methodologies could be developed to generate confidence intervals for countries

where data remain inadequate, although care should be taken in this regard. One

approach would be to exploit cross-country experiences by estimating models using panel

data for broadly similar countries. A number of issues would need to be addressed to assess

the technical and procedural feasibility of this approach, including the classification of

countries with similar attributes (such as reliance on concessional resources, exchange rate

regime, and dependence on commodity exports). Such an approach could allow for some

33

One possible approach to address this issue would be to ensure that confidence intervals are broadly

consistent with the historical record of forecast errors based on the WEO projection database. This would

alleviate the risk of over-fitting empirical models (data mining), leading to a bias toward understating the risks.

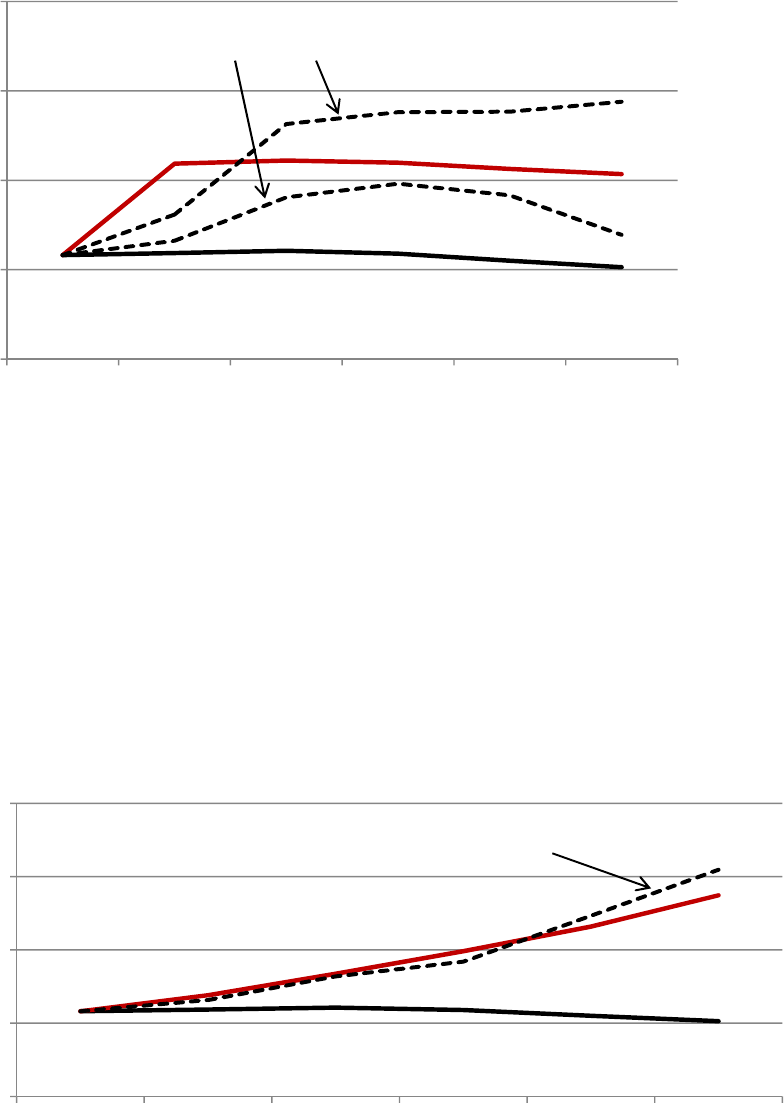

Box 2. Using Confidence Intervals to Help Gauge Uncertainty (continued)

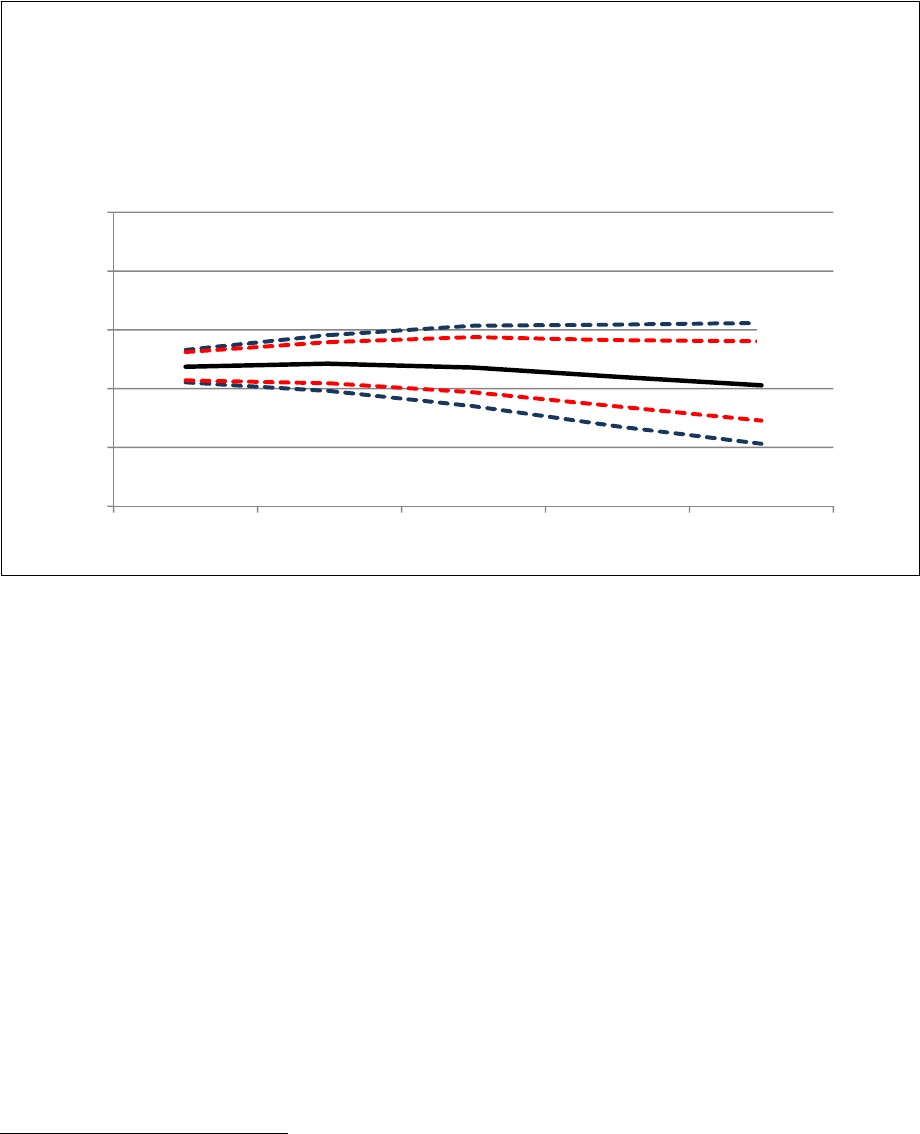

Similarly, estimating the VAR over a shorter sample period (1999–2010 versus 1995–2010) results, in this

particular case, in narrower confidence intervals (Figure c).

65

70

75

80

85

90

2011 2012 2013 2014 2015

Public Debt / GDP (percent)

Source: IMF Staff calculations.

Figure c. Confidence Intervals Generated using Different Sample Periods

Sub-sample

Baseline

projection

Sub-sample

Full sample

Full sample

25

country-specific attributes (notably volatility), while constraining other attributes that are

more difficult to estimate robustly at the country level (correlation between the shocks, for

example).

VI. VULNERABILITIES ASSOCIATED WITH THE PROFILE OF PUBLIC DEBT

43. Debt vulnerabilities are associated not only with the level of debt, but also with

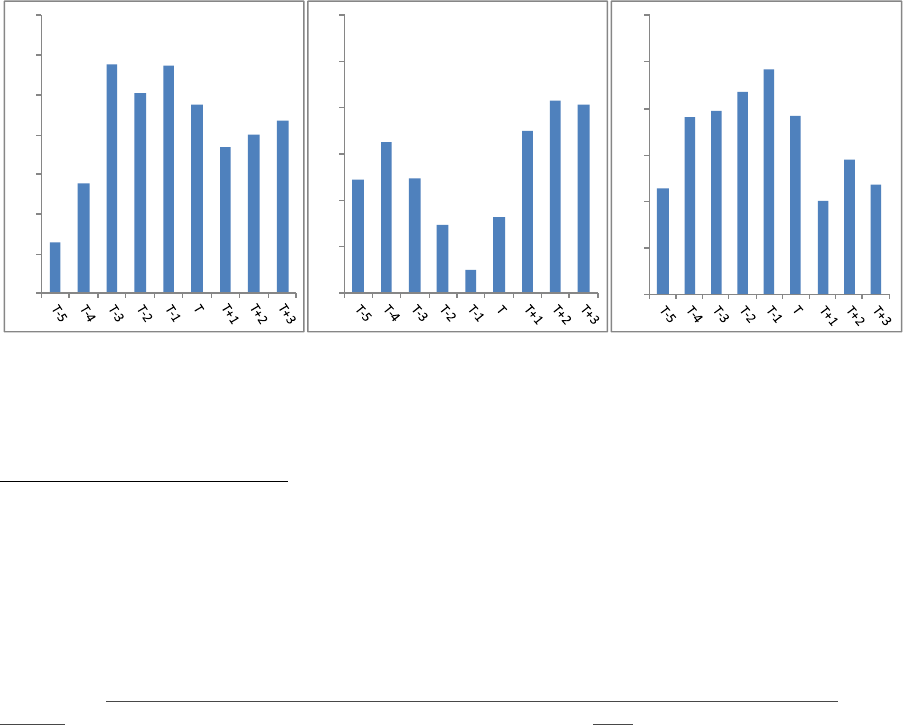

its profile. Debt structure characteristics—maturity, currency composition, and the creditor

base—have received much attention in the analysis of debt distress.

34

A high share of short-

term debt at original maturity, which may reflect the inability of certain sovereigns to issue

long-term debt, increases vulnerability to rollover and interest rate risks. A high share of

foreign currency-denominated debt increases vulnerability to exchange rate risk and can put

pressure on foreign exchange reserves. Debt distress events have typically been preceded

by an increase in the shares of short-term debt and foreign-currency denominated debt

(Figure 6a).

35

The nature of the creditor base―for example, whether it is diversified, reliable,

captive, domestic, or foreign― also matters for rollover risk.

36

34

See for example Deutsche Bank (2011), IADB (2007), Eichengreen and Hausman (2005).

35

Short-term debt at remaining maturity highlights the bunching of refinancing needs, and thus captures

different risks than short-term debt at original maturity. Indeed, the latter could be seen as an early warning of

liquidity problems.

36

The absence of comparable cross country data on the creditor base does not allow for an examination of its

behavior around debt distress episodes. However, its importance has been amply recognized and discussed. See

for example, Managing Sovereign Debt and Debt Markets through a Crisis- Practical Insights and Policy

Lessons ), Das et al (2010), JPMorgan (2011), and IMF and World Bank (2001).

Figure 6a. Debt Structure Indicators around Debt Distress Events

T - Year of debt distress event.

Source: IMF staff calculations, based on annual data.

5

6

7

8

9

10

11

12

Short-Term Public Debt at Original

Maturity (Percent of Total Public Debt)

8

9

10

11

12

13

14

Average Maturity on New Debt to

Private Sector (Years)

58

60

62

64

66

68

70

Foreign Currency Public Debt (Percent

of Total Public Debt)

26

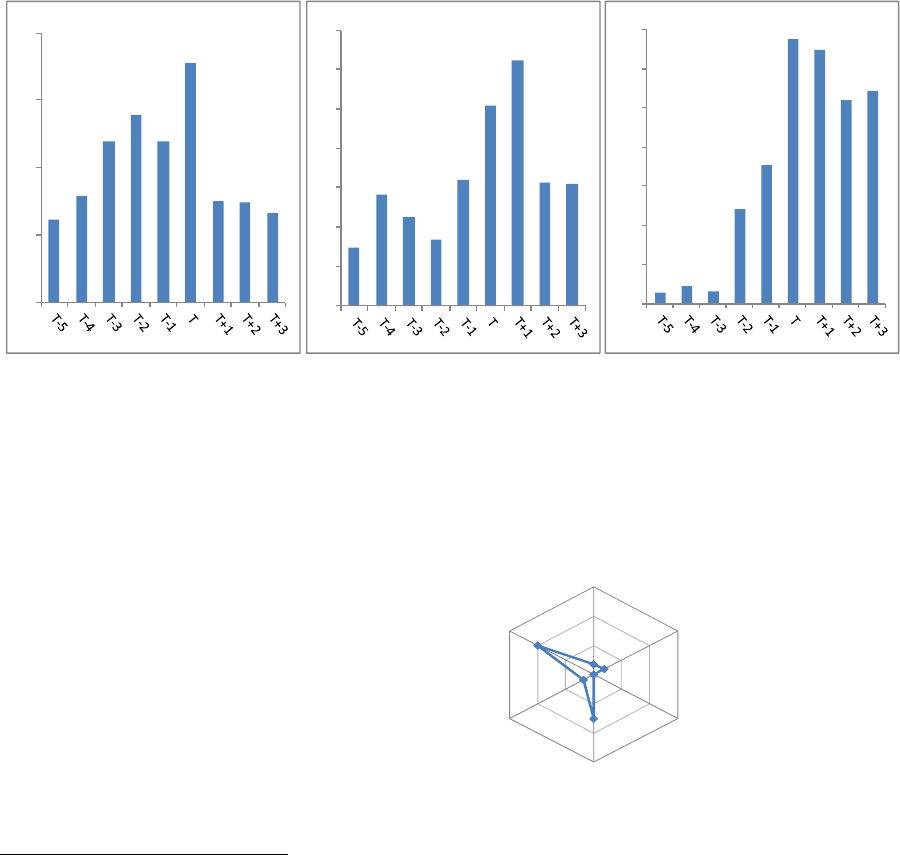

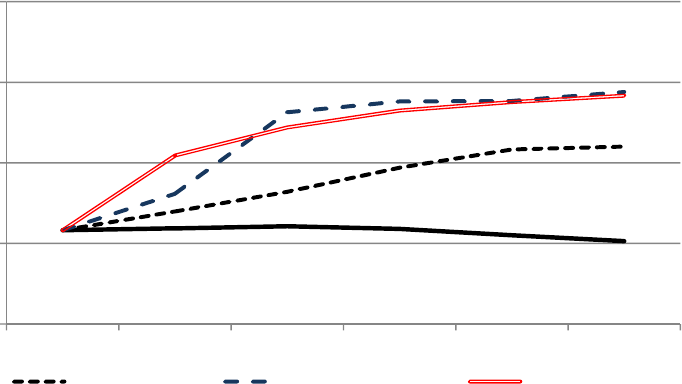

44. Additional indicators associated with the debt profile, such as external financing

needs and risk pricing, may also provide useful information on the risk of debt distress

(Figure 6b). External financing needs, which increase pressure on existing foreign exchange

reserves, tend to rise before episodes of sovereign debt distress. Similarly, bond and CDS

spreads tend to increase before debt distress episodes. Fluctuations in spreads may be related

to a number of underlying factors associated with country-specific macroeconomic

fundamentals and political risk, as well as other factors related to international financial

conditions and investors’ preferences. Given the significant noise in spreads, only sustained

increases in spreads, which is likely to be difficult to ascertain a priori, may be relevant for

assessing vulnerabilities.

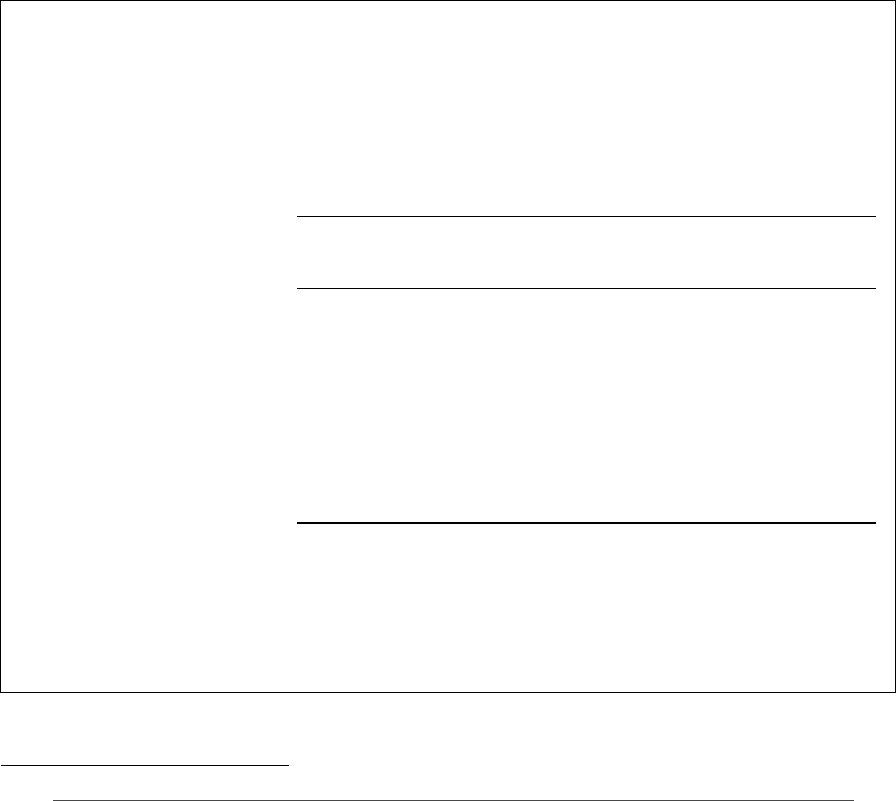

45. This suggests that the analysis of debt vulnerabilities can be improved by a

greater focus on debt structure and liquidity indicators. Staff proposes to add to the

public DSA framework the six

indicators shown in the previous

figures, together with an associated

benchmark level for each of them

based on its ability to signal debt

distress events (Figure 7 and

Box 3).

37

The purpose of the

benchmarks would be to facilitate

staff analysis rather than rate

countries in terms of likelihood of

debt distress or provide an early

37

A value of one means that an indicator is at the threshold level. The closer the indicator is to the center, the

lesser the vulnerability along this dimension.

Figure 6b. Liquidity and Risk Pricing Indicators around Debt Distress Events

T - Year of debt distress event.

Source: IMF staff calculations, based on annual data.

10

15

20

25

30

Total External Financing Requirement

(In percent of GDP)

4

5

6

7

8

9

10

11

EMBI Global Spreads (Percent)

0

100

200

300

400

500

600

700

5-Year CDS Spreads (Basis Points)

EMBIG spreads

(Percent)

Tot al ex ter n a l

financing

requirement

(percent of

GDP)

Short-term debt

(percent of

public debt)

Foreign

currency debt

(percent of

public debt)

Five-year CDS

spreads (basis

points)

Average

maturity (years)

1

Figure 7. Country: Debt Profile Vulnerabilities

27

warning regarding access to market financing. This assessment would be undertaken in a

flexible manner for MACs where data are available; in certain countries, some of the

indicators may not be relevant or applicable. With regard to the creditor base, the lack of