GDP compact

Grid Development Plan Electricity 2037 with

Outlook 2045, Version 2023, second draft

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 2

GDP compact

50Hertz Transmission GmbH

Heidestraße 2

10557 Berlin, Germany

www.50hertz.com

Amprion GmbH

Robert-Schuman-Straße 7

44263 Dortmund

www.amprion.net

TenneT TSO GmbH

Bernecker Straße 70

95448 Bayreuth, Germany

www.tennet.eu

TransnetBW GmbH

Pariser Platz

Osloer Straße 15–17

70173 Stuttgart, Germany

www.transnetbw.de

Editorial staff

Volker Gustedt (50Hertz Transmission GmbH),

Birte Greve (Amprion GmbH),

Christian Brehm (TenneT TSO GmbH),

Claudia Halici (TransnetBW GmbH)

Email: [email protected]

www.netzentwicklungsplan.de

Design

CBE DIGIDEN AG

www.cbe-digiden.de

Dated

26 June 2023

Imprint

All graphics, tables and texts from the second draft of the Grid Development Plan Electricity 2037 / 2045, Version 2023 are licensed under

Creative Commons licence CC BY 4.0. The text of the licence is available at creativecommons.org/licenses/by/4.0/legalcode

An example for proper referencing is: Grid Development Plan Electricity 2037 / 2045, (2023), second draft | Transmission system operator CC-BY-4.0

For adaptations / edits: Grid Development Plan Electricity 2037 / 2045, (2023), second draft | Transmission system operators (M) CC-BY-4.0

Excluded from this rule are graphics, tables and texts with a different or additional source. The overview maps and individual maps can be used with

reference to the source and licence indicated there.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 3

GDP compact

Summary

The transmission system operators (TSOs) with control

area responsibility plan, build and operate new grids for

new energies. In the Grid Development Plan Electricity

(GDP), they present the measures for optimising, rein-

forcing and expanding the German transmission grid. This

includes measures on land as well as the offshore grid

connection systems in the exclusive economic zone and in

the territorial sea in accordance with the legal requirements

of the Energy Industry Act (EnWG).

This GDP 2037 / 2045 (2023) looks at the years 2037 and

2045 and thus also at the statutory target year for achieving

climate neutrality in Germany. It analyses the grid develop-

ment demand for three different scenarios for these years.

This scenario framework is mainly based on the expansion

targets for renewable energy of the Renewable Energy

Act (EEG) 2023. The scenarios differ in their assumptions

regarding the use of hydrogen, the level of direct electri-

fication and the increase in efficiency. Consequently, they

represent a range of potential developments. Moreover,

ad-hoc measures for 2030 were analysed to make it easier

to respond to the stronger expansion of renewable energy

and the likewise increasing gross power consumption in the

short and medium term.

In Germany as well as in Europe, an accelerated ex-

pansion of renewable energy and a strongly rising and

increasingly flexible power demand will point the way

towards a decarbonised society in the coming years. It is

crucial that power is reliably available and can be used

as directly and efficiently as possible. The correspond-

ing expansion and conversion of the transmission grid is

therefore a vital prerequisite for a carbon-neutral future.

The GDP presents the necessary expansion measures in

the transmission grid towards a carbon-neutral grid.

Transport demand grows significantly with

the expansion of renewable energy

To achieve carbon-neutrality in Germany until 2045 and to get

more indepently in terms of energy supply are reflected in

the political targets. Therefore, these political targets are

assumend within the scenario framework for the GDP.

Compared to the last GDP with the observation periods

ending in 2035 and 2040, installed capacity of renewable en-

ergy and gross energy consumption in 2037 and 2045 have

increased significantly. According to Renewable Energy Act

(EEG), the major share of the expansion of renewable ener-

gies is supposed to be implemented by the mid-2030s. The

aim is to enable carbon-neutral power supply to decarbon-

ize other sectors. The development is accelerating by leaps

and bounds. Consequently, this increases the demands on

the transmission grid enormously. The demand for power

transport from northern to southern Germany is expected

to rise significantly to around 87.7 GW by 2037. Between 2037

and 2045 the increase in transport in the scenarios remains

at a similar level or increases only from northern to southern

Germany moderately. The further expansion of renewable

energy can largely be offset by the expansion of flexibilities.

Due to the increasing electrification of the building,

transport and industrial sectors, the total gross power

consumption increases from about 650 to 700 TWh in 2035

of the previous GDP to 899 to 1,053 TWh in 2037 of the cur-

rent GDP. Compared to the last GDP, this corresponds to

an increase of around 40 to 44%. After 2037, gross power

consumption increases further to 1,079 to 1,303 TWh in

2045 according to the scenario framework. To cover this

increase, the installed renewable energy capacity will

have to be expanded to 638 to 703 GW. This corresponds

to almost a fivefold increase in installed renewable energy

capacities by 2045 compared to today.

Expansion of renewable energy

Installed capacity

in GW

Reference

(2020 / 2021)

Target year 2035

(GDP 2021)

Target year 2037

(GDP 2023)

Target year 2045

(GDP 2023)

Photovoltaics 59 110 – 120 345 400 – 445

Offshore wind 8 28 – 34 51 – 59 70

Onshore wind 56 82 – 91 158 – 162 160 – 180

Source: Transmission system operators

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 4

GDP compact

In terms of regional distribution, this GDP reveals new

trends. As before, southern and now also increasingly

western federal states tend to experience a generation

deficit in the scenarios, while there is a generation surplus

in northern and north-eastern federal states. The demand

for transport within Germany is still largely determined by

a high feed-in of wind energy in the north and north-east

of Germany and the location of the consumption centres in

the west and south of Germany. Firstly, load flows occur in

the opposite direction – partly due to high generation from

photovoltaics in the south, while electrolyers are opera-

tional in the north.

The national development of the german energy system

are embedded in the European scenario ‘Distributed

Energy’ of the Ten Year Network Development Plan 2022.

This plan accounts for the reduction of EU-wide emissions

manifested at the European level with the target of climate

neutrality by 2050. The Europe-wide balancing of power

and consumption is of vital importance for the reliable and

demand-based design of a carbon-neutral energy system.

This will also reduce the need for flexibility and power

generation capacities in Germany.

Hydrogen gains in importance

Compared to earlier GDPs, the assumptions regarding

the extent of hydrogen utilisation and the expansion of

the hydrogen infrastructure have also increased signifi-

cantly. According to the approved scenario framework, a

comprehensive hydrogen infrastructure is assumed as

early as 2037. In 2045, up to 80 GW of electrolysis capacity

for domestic hydrogen production is supposed to be inte-

grated into the system. The future hydrogen infrastruc-

ture has a major impact on the development needs of the

transmission grid. An extended hydrogen infrastructure

is a prerequisite for grid-supporting allocation of hydro-

gen. This GDP adopts electrolysis locations that support

the grid – a procedure for which currently no regulatory

framework exist. This approach ensures that bottlenecks

in the transmission grid can be minimised and the cur-

tailment of renewable energy in times of high generation

can be reduced as far as possible. Since the corresponding

framework conditions are currently not in place, the ap-

proach is associated with high uncertainties from today’s

perspective. If other criteria are decisive for the allocation

in the future, additional bottlenecks in the transmission

grid are likely to occur.

Progressive interconnection

With the target of tackling the increasing transport de-

mands at the lowest possible investment and redispatch

costs, a higher-level controlling algorithm was used for

the first time in the grid analyses. This metaheuristic

method made it possible to compare several hundred

combinations of expansion options – far more than usual.

Combinations of measures were formed from the cate-

gories of grid connection points (GLP), corridors for High

Voltage Direct Current Transmission lines (HVDC), in-

terconnection of HVDC sites, grid-supporting location

of offsite power-to-gas plants (electrolysers) as well as

load flow control and AC projects in the vicinity of HVDC

and GLP.

The four German TSOs continue to rely on a range of

proven, innovative solutions and technologies and con-

sider potentials of future innovative technologies such as

modern system management concepts and grid boosters.

Transport-bottlenecks identified in the scenarios were not

completely removed by grid enhancement and expansion

measures, so that between 1.5 and 5.9 TWh of redispatch

volume are left. However, no peak capping was applied.

This procedure corresponds to the scenario framework

approval of the German Federal Network Agency (BNetzA).

In order to be able to react to the increasing demands

flexibly and reliably, the TSOs are interconnecting the

transmission grid even further. Since the first GDP in 2012,

the TSOs have focused on linking AC and DC measures.

This GDP now proposes additional measures on linked DC

structures onshore as well as offshore measures among

each other. Together with the European interconnection,

renewable energy can be comprehensively integrated

for flexible demand, and redispatch requirements can be

reduced. This limits congestion management costs and

contributes to a secure energy supply. Furthermore, the

flexibility in grid operations gained through DC linking

increases the security of supply.

Further expansion demand for a carbon-neutral grid

by 2037

The climate neutrality network resulting from this

GDP shows a considerable increase in necessary grid

enhancement and expansion measures. Considering the

increasing transport demand, the measures entrenched

in the current Federal Demand Plan are far from suffi-

cient for a demand-based grid.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 5

GDP compact

The scope and cost volume of the expansion grid will

therefore increase significantly compared to the previ-

ous GDP. Compared to the project portfolio proposed in

the GDP 2035 (2021), the present GDP 2037 / 2045 (2023)

identifies new onshore projects with a route length of

5,620 km and additional investments of EUR 52.3 billion.

This is particularly attributable to the designation of five

additional DC projects, which are necessary to secure

the required transport task and are not yet included

in the current Federal Demand Plan (BBP). Bundling

options with each other or with existing DC projects are

mostly possible or are being examined. The new DC

projects increase the north-south as well as the east-west

transport capacity. Other key drivers for the additional grid

development measures are the strong expansion of re-

newable energy in the north, the dismantling of conven-

tional power plants, the interconnected energy exchange

with foreign countries, and the increasing loads in the

course of achieving climate neutrality in all sectors.

Regarding to the results of the grid development target

grids for the years 2037 and 2045 are almost identical.

This is mainly due to the fact that onshore expansion of

renewable energy between 2037 and 2045 is almost com-

pleted. The moderate increase in onshore renewable en-

ergy capacities by 2045 may cause additional bottlenecks

in the onshore grid. However, it can be offset by the grid

structures in place at that time and correspondingly flex-

ible demand, especially from electrolysers, centralised

and decentralised battery storage as well as demand

side management. A majority of the carbon-neutral grid

must therefore already be implemented in 2037.

Considering these assumptions, the target grid consists

of a robust portfolio of grid enhancement and expansion

measures that are necessary for all scenarios. All projects

presented in GDP 2037 / 2045 (2023) should therefore be

considered to be ‘no-regret’. In the scenarios, the desig-

nated target grid only differs in terms of the remaining

redispatch demand. Currently, there are still high uncer-

tainties due to the not yet fully completed legal planning

for the expansion of renewable energy (including at the

federal states level), the decarbonisation strategies of the

industry or the planning for the future hydrogen economy.

It is important to clarified in the following GDP cycles to

which extent the remaining redispatch can be further

reduced, and especially whether it requires additional

moderate grid expansion or other technical measures.

The onshore initial grid comprises AC and DC measures

totalling around 6,950 km with an estimated investment

volume of EUR 50 billion. For the onshore grid expansion,

grid enhancements AC amount to 6,125 km. Furthermore,

there are about 180 km of DC enhancement measures.

Another 1,714 km are accounted for new AC construction

measures and 4,396 km new DC construction measures.

In total, the onshore expansion grid for all scenarios

includes 12,413 km. For scenarios A / B / C 2037, the in-

vestment costs amount to around EUR 106.1 billion. The

investment costs for the onshore expansion grid of the

A / B / C 2045 scenarios are EUR 0.1 billion higher.

The system stability analyses show considerable addi-

tional demand for reactive power compensation as well

as for the control of grid disconnections in the form of

instantaneous reserve, which already occur in the an-

alysed intermediate scenario 2030. As a consequence,

previously reported plants must be prioritised and made

available via grid-supporting contributions from third

parties (e.g. provision from the distribution grids, from

large consumers such as electrolysers, and other sys-

tem participants, possibly through market procurement).

The analyse on transient stability indicates that control-

lability could no longer be safely guaranteed in individual

hours after conceptual fault clearance in case of distur-

bances. Therefore, in order to maintain system stability,

additional solution concepts must be developed beyond

the suggested measures. The results are presented in

the accompanying document of the stability analyses, and

the necessary measures are indicated.

Compared to the first draft of the GDP 2037 / 2045 (2023),

the investment costs in the second draft of the GDP have

increased by EUR 12.5 billion. This is mainly attributable

to the consideration of additional projects based on addi-

tional demand for transformers and substations between

the distribution and transmission grid. Other contribut-

ing factors include an update of the scope and costs of

existing projects as well as the updated requirements

for plants for reactive power compensation and for the

provision of instantaneous reserve.

The drastic increase in investment costs compared to

the previous GDP is caused by the change in the scope

of projects and measures as well as the adjustment of

standard and project costs resulting from the overall

economic development.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 6

GDP compact

Tapping offshore potential comprehensively

The expansion of the installed capacity from offshore-wind

will continue even after 2037. Compared to today (7.8 GW),

the installed capacity from offshore wind assumed in the

scenarios increases by up to 7.5 times to 58.5 GW in 2037.

By 2045, it further increases to 70 GW of installed capacity.

To integrate offshore wind generation the TSOs have de-

termined offshore grid connection systems in the North

Sea and Baltic Sea with a length of about 6,600 km and a

transmission capacity of about 36 GW in scenario A 2037,

as well as a length of about 9,300 km with a transmission

capacity of about 44 GW in scenarios B 2037 and C 2037.

For long-term scenarios A 2045, B 2045 and C 2045, a

transmission capacity of about 60 GW results in grid con-

nection systems with a length of 13,310 km (excl. initial

grid). Even after 2037, eight more systems with a trans-

mission capacity of 16 GW will be connected.

For the first time, national offshore interconnection is

examined, its benefits are presented and a project with

two measures is identified. Overall, national offshore

interconnection is shown to be a grid-supporting and

cost-efficient expansion measure aimed at minimising

long-range grid bottlenecks.

The investment volume for the offshore grid expansion

until 2037 is about EUR 77 billion for scenario A 2037.

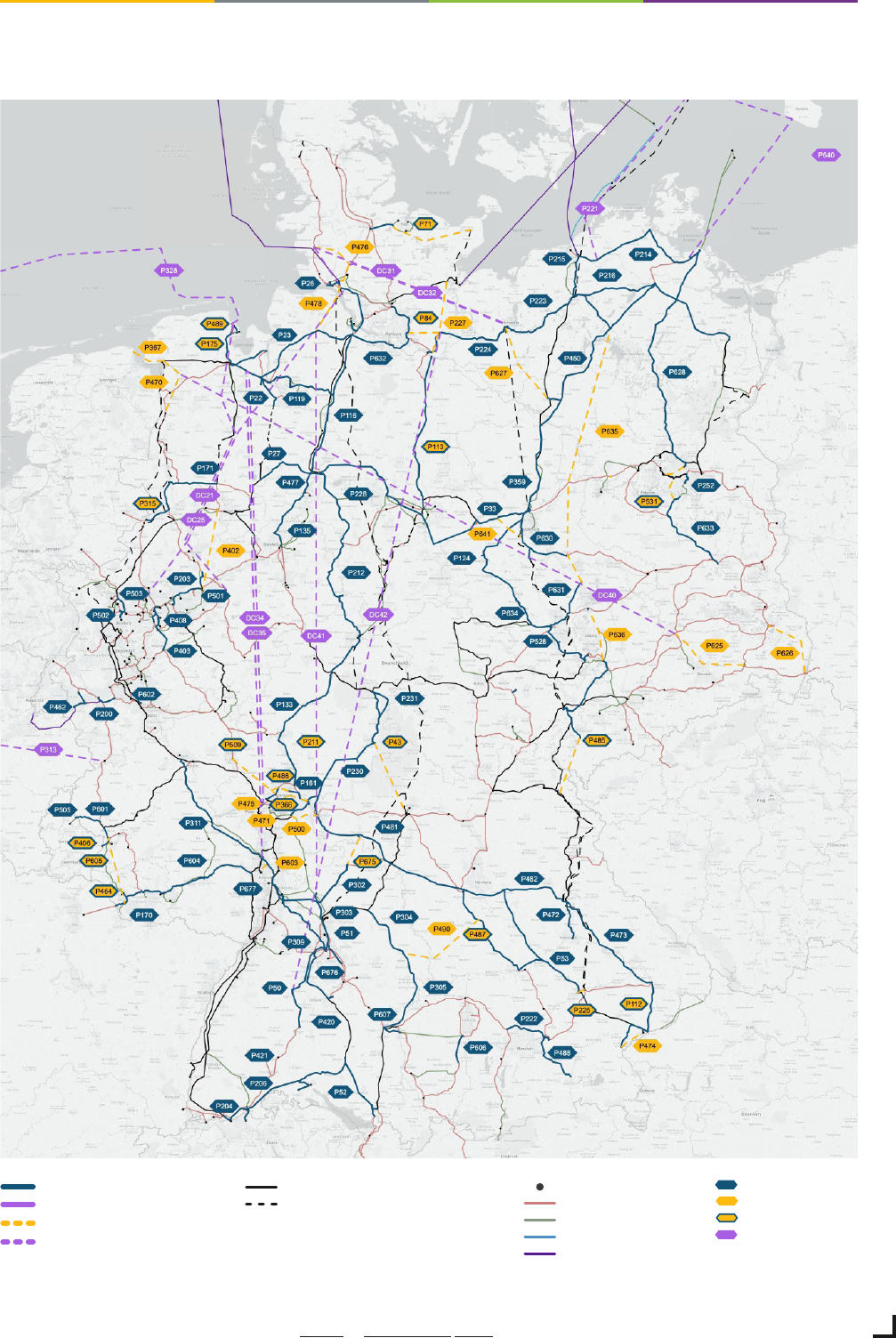

Route kilometres and investment costs of the expansion grid for B / C 2037 (A 2037) offshore and A / B / C 2037 onshore

Route length in km Investment volume in EUR billion

Offshore 9,250 (6,610) 103.5 (77)

Onshore 12,413 106.1

Total 21,663 (19,023) 209.6 (183.1)

Source: Transmission system operators

Scenarios B 2037 and C 2037 require investments of

about EUR 103.5 billion (incl. interconnection). For long-

term scenarios A 2045, B 2045 and C 2045, the estimated

investment costs are around EUR 145.1 billion (incl.

interconnection). Moreover, the investment costs for

the offshore grid expansion measures of the offshore

initial grid that are already being implemented amount

to around EUR 12.4 billion for all scenarios with a route

length of 1,580 km.

Based on the offshore grid connection systems confirmed

by BNetzA in the GDP 2035 (2021), the additional need

for 20 new Offshore grid connection systems with a route

length of approx. 8,455 km and an investment volume of

EUR 86.7 billion was identified in this GDP 2037 / 2045 (2023).

Energy corridors for lower spatial requirements

According to § 12b (3a) of the EnWG (German Energy Act),

the TSOs need to for the first time identify bundling options

for newly identified DC grid expansion measures and the

cross-border onshore part of the offshore connection

lines. It needs to be shown how these measures can be

realised with existing or at least firmly planned routes,

either entirely or to a large extent in one power line corri-

dor. Bundling makes it possible to align offshore connec-

tion systems and newly identified DC projects in the same

route and thus minimise the use of space. According to the

HVDC projects already confirmed in the GDP 2035 (2021)

or submitted for confirmation in the GDP 2037 / 2045 (2023),

there are three central energy corridors based on the

current planning status.

Route kilometres and investment costs for the expansions in scenarios A / B / C 2045

Route length in km Investment volume in EUR billion

Offshore 13,310 145.1

Onshore 12,413 106.2

Total 25,723 251.3

Source: Transmission system operators

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 7

GDP compact

The full report with descriptions of all projects for the onshore and offshore grid is available at www.netzentwicklungsplan.de

Shaping the future with determination

The transformation to climate neutrality by one of the

world’s largest industrial nations can only succeed as

a project involving society. It is up to politics, business,

science and citizens to successfully shape this trans-

formation together.

A secure, reliable and efficient transmission grid that keeps

pace with the expansion of renewable energy makes a sig-

nificant contribution to the success of the transformation.

The GDP clearly shows what this transformation means.

Numerous grid development projects throughout Germany,

on land as well as at sea, as enhancement of existing lines

and as new construction need to be explained, decided,

planned, built and operated. Dedicated skilled workers,

available materials at reasonable prices and stable supply

chains are a prerequisite for this.

The implementation of the carbon-neutral grid thus

requires decisive action and joint commitment – from

TSOs and approval authorities, from politicians at

federal, state and local level, as well as other stake-

holders in the energy transition.

Therefore, the follwing is needed:

Faster implementation of grid expansion. The first

important steps to accelerate planning and approval

processes have been taken. They must now be swiftly

put into practice. In order to integrate the very high

output of renewable energy into the power grid by

2037, this GDP presents the carbon-neutral grid that

must be implemented to the greatest possible extent

as early as 2037.

More innovations to reduce the need for grid expan-

sion. One example is the first-time utilisation of

potential through national offshore interconnection.

More flexibility. Appropriate regulatory framework

conditions and sufficient incentives must be created

so that the flexibility potential of new technologies

such as electrolysers can be optimised.This includes

system-supporting locations and utilisation methods.

The same applies to decentralised technologies such

as electric vehicles and heat pumps. In addition to the

provision of communication technologies for control,

suitable market and grid charging structures are

extremely necessary.

An integrated system planning for power, gas and

hydrogen. Even if separate grid planning processes

continue to make sense, they should be based on

jointly agreed scenario key figures in the future.

With its analyses, the GDP not only offers a specific out-

look for the power grid of the next decades, but also a

continuously updated and well-founded information base

for central energy and economic policy decisions. The

biennial rhythm ensures that the latest developments are

reflected, covering market design and price development

to the design of flexibilities or the speed of the expansion

of renewable energy sources. Accordingly, the climate

neutrality network presented in this GDP will also be

further developed in the following GDPs.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 8

GDP compact

Key statements of the chapters

The process of the grid development plan

The demands on the transmission grid are becoming

increasingly complex. Decarbonisation through electri-

fication ensures that ever greater amounts of power are

consumed and in some cases transported over longer

distances. Furthermore, it must be possible to react to

volatile renewable energy generation caused by weather

conditions and to operate the grid more and more flexible.

The continuous development of the power grid is therefore

an important component of a successful energy transition.

According to § 12b EnWG, the four german transmission

system operators with control area responsibility (50Hertz,

Amprion, TenneT and TransnetBW) are obligated to pre-

pare a joint ‘Grid Development Plan Electricity’ document

every two years and submit it to BNetzA for confirmation.

The GDP presents the measures for optimisation, en-

hancement and expansion in the German power transmis-

sion grid as well as the offshore connection systems in the

exclusive economic zone and in the territorial sea, includ-

ing the grid interconnection points on land, considering

the statutory requirements of the EnWG.

Based on the results of GDP, BNetzA determines which

measures are required so that the German transmission

grid can fulfil its future tasks. The calculations in the GDP

are based on the scenario framework previously prepared

by the TSOs and reviewed and approved by BNetzA.

The scenario framework on which this GDP is based con-

siders 2045 and 2037. Considering political targets, it is

assumed that Germany will be climate neutral

1

by 2045

at the leatest. The GDP presents a transmission grid for

a carbon-neutral energy system

1

in Germany for the first

time. It is based on the amendment to the Energy Industry

Act. § 12a of the EnWG was amended as follows: ‘Three

additional scenarios must consider the year 2045 and

present a range of probable developments, which are

aligned with the legally defined climate and energy policy

targets of the Federal Government.’

Therefore, three scenarios were created for each of the

two target years: A, B and C. The GDP 2037 / 2045 (2023)

calculates the grid developments necessary in six different

scenarios.

1

With the GDP, the transmission system operators balance the CO

2

emissions in the domestic power sector. The achievement of targets in other sectors

(such as industry, transport or heat) is outside the scope of our study. Moreover, imports or greenhouse gases used elsewhere are not included in the

CO

2

balance for Germany.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 9

GDP compact

Scenario Framework: Starting point for the

GDP 2037 / 2045 (2023)

The scenario framework for GDP 2037 / 2045 (2023) consid-

ers a carbon-neutral energy system for the first time and

thus forms the basis for a carbon-neutral grid in Germany.

It considers the expansion targets for renewable energy of

Renewable Energy Act 2023.

Scenario A (decarbonisation through higher

share of hydrogen):

This scenario is characterised by the comparatively

highest hydrogen demand in all scenarios. Hydrogen

is increasingly used in some industrial sectors, where

the uncertainty regarding potential electrification still

seems high today. To meet this demand, a high domestic

installed capacity is assumed in this scenario. Gross

power consumption increases to around 1,050 TWh

in 2045. The renewable capacities correspond to the

targets of the Renewable Energy Act (EEG) and the

Offshore Wind Power Act (WindSeeG).

Scenario B (decarbonisation through intensive

electrification):

Scenario B relies on increased direct electrification in all

final energy consumption sectors. Hydrogen is only used

in applications where such direct electrification seems

unlikely from today’s perspective. Efficiency counteracts

a strong increase in power consumption. The increase in

power consumption is thus limited to just under 1,100 TWh.

The renewable expansion path corresponds to the targets of

the Renewable Energy Act (EEG) and Offshore Wind Power

Act (WindSeeG).

Scenario C (decarbonisation despite lower efficiency):

Scenario C also assumes increased direct electrification

in all final energy consumption sectors. Lower efficiency

than in scenario B results in higher power consumption of

almost 1,300 TWh. This is also accompanied by the need

for stronger expansion of renewable energy.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 10

GDP compact

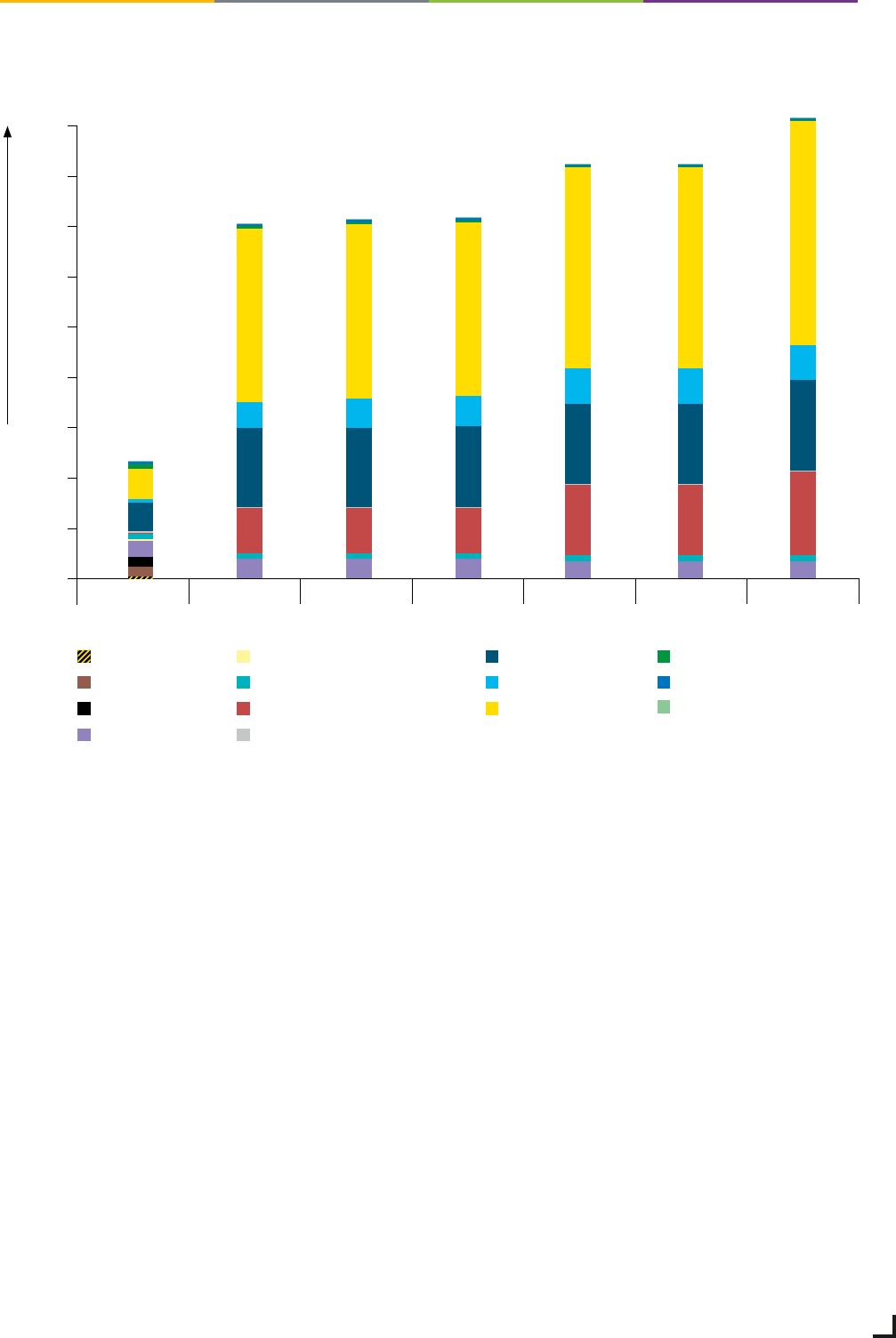

Overview of the distribution of installed capacities per energy source

0

300

400

500

600

200

100

700

800

900

Nuclear

Lignite

Coal

Natural gas/hydrogen

Oil

Pumped storage

Battery storage

other conventional generation*

Wind onshore

Wind offshore

Photovoltaics

Biomass

Hydropower

other renewable generation

* other conventional generation plus 50% waste

C 2045B 2045A 2045C 2037B 2037A 2037Reference

2020 / 2021

Installed capacity in GW

Figure 4: Overview of the distribution of installed capacities per energy source

Source: Transmission system operators

Source: Transmission system operators

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 11

GDP compact

Installed capacity in GW

Energy source

Reference

2020 / 2021

A 2037 B 2037 C 2037 A 2045 B 2045 C 2045

Nuclear 4.1 0.0 0.0 0.0 0.0 0.0 0.0

Lignite 18.9 0.0 0.0 0.0 0.0 0.0 0.0

Coal 19.0 0.0 0.0 0.0 0.0 0.0 0.0

Natural gas/hydrogen* 32.1 > 38.4 > 38.4 > 38.4 > 34.6 > 34.6 > 34.6

Oil 4.7 0.0 0.0 0.0 0.0 0.0 0.0

Pumped storage 9.8 12.2 12.2 12.2 12.2 12.2 12.2

other conventional generation** 4.3 1.0 1.0 1.0 1.0 1.0 1.0

Total conventional generation 92.9 > 51.6 > 51.6 > 51.6 > 47.8 > 47.8 > 47.8

Wind onshore 56.1 158.2 158.2 161.6 160.0 160.0 180.0

Wind offshore 7.8 50.5 58.5 58.5 70.0 70.0 70.0

Photovoltaics 59.3 345.4 345.4 345.4 400.0 400.0 445.0

Biomass 9.5 4.5 4.5 4.5 2.0 2.0 2.0

Hydropower*** 4.9 5.3 5.3 5.3 5.3 5.3 5.3

other renewable generation**** 1.1 1.0 1.0 1.0 1.0 1.0 1.0

Total renewable generation 138.7 564.9 572.9 576.3 638.3 638.3 703.3

Total generation 231.6 616.5 624.5 627.9 686.1 686.1 751.1

Power consumption in TWh

Net power consumption 478 828 891 982 999 1,025 1,222

Gross power consumption 533 899 961 1,053 1,079 1,106 1,303

Drivers of sector coupling

Heat pumps – household and commerce,

trade and services, quantity in millions.

1.2 14.3 14.3 14.3 16.3 16.3 16.3

Electromobility – quantity in millions. 1.2 25.2 31.7 31.7 34.8 37.3 37.3

Power-to-Heat – district heating/industry, in GW 0.8 12.6 16.1 22.0 14.9 20.4 27.0

Electrolysis in GW < 0.1 40.0 26.0 28.0 80.0 50.0 55.0

Further storage and demand-side flexibilities in GW

Photovoltaic battery storage 1.3 67.4 67.4 67.4 97.7 97.7 113.4

Large-scale battery storage 0.5 23.7 23.7 24.2 43.3 43.3 54.5

DSM – industry and commerce, trade and services 1.2 5.0 7.2 7.2 8.9 12.0 12.0

The presented values are from the approval document and a subsequently agreed increase in pumped storage capacity.

Deviations of these values arise in the course of modelling. Due to the large amount of flexible electrical loads and variables,

the exact power consumption will only result from the power market modelling.

* The stated capacities merely include the power plants explicitly allocated with the scenario framework approval, not the additional near-load reserves

reflected in the market simulation.

**

other conventional generation plus 50% waste

***

Storage water and run-of-river water

**** other renewable generation plus 50% waste

Source: Federal Network Agency

Overview of the scenario key figures

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 12

GDP compact

Central assumptions of the scenario framework are:

Power sector in pioneering role: The power sector is

highly important for achieving greenhouse gas neutrality

in Germany by 2045. In the context of sector coupling, the

power sector plays a pioneering role and can contribute

significantly to the decarbonisation of other sectors.

Direct electrification seems to be the most efficient

option to replace fossil fuels in many cases.

Developed hydrogen infrastructure: In cases where direct

electrification is associated with higher economic costs

or is not technologically feasible, the use of hydrogen or

synthetic fuels can be advantageous. The scenario frame-

work assumes a comprehensively developed hydrogen

infrastructure by 2037. In the scenarios for 2045, with an

installed capacity of between 50 and 80 GW, a significant

part of the hydrogen demand in Germany is covered by

domestic electrolysis. Bottlenecks in the transmission grid

can be minimised by allocating electrolysers to serve the

grid. Moreover, due to the proximity to renewable energy

plants and a market-oriented operation, the curtailment

of renewable energy in times of high generation can be

largely reduced.

Electrification of the sectors: Due to the increasing elec-

trification of the heating, transport and industrial sector,

gross power consumption is expected to double to 1,300

TWh by 2045 compared to today. The installed capacity

of renewable energy will be expanded to 640 to 700 GW

for this purpose. This corresponds to almost a fivefold

increase in installed capacities from renewable energy

compared to today. In this power system in 2045, which is

dominated by volatile generation, a high demand for flex-

ibility is needed in terms of generation and load capacity.

It is assumed that many power consumers can react flex-

ible to the supply and demand situation and adjust their

consumption accordingly. This ensures an integration with

an great extent of renewable energy and reduces variable

generation costs.

More storage technologies: Demand side management

and storage technologies support the balancing and inte-

gration of renewable power generation. 12 GW of pumped

storage power plants and up to 168 GW of large and small

battery storage are assumed. Hydrogen can be used as an

energy carrier for seasonal storage of renewable energy.

Phasing out coal and nuclear energy: A complete phase-

out of nuclear energy and an end to coal-fired power gen-

eration by 2037 is assumed in all scenarios. Conventional

power plants will still be needed in Germany to provide

secure power generation. To achieve climate neutrality,

these plants must be operated exclusively with hydrogen

or greenhouse gas-neutral fuels by 2045 at the leatest.

European integration: The Europe-wide balancing of

power generation and consumption is of vital importance

for an efficient and demand-based carbon-neutral energy

system. This will reduce the need for flexibility and power

generation capacities in Germany. The national develop-

ment for Germany is embedded in the European scenario

‘Distributed Energy’ of the Ten Year Network Development

Plan 2022.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 13

GDP compact

Market simulation: Focus on renewable

energy and flexible demand

The results of the market simulation highlight the domi-

nant role of renewable energy in Germany’s energy mix. In

all scenarios, power generation from renewable energy

rises to over 1,000 TWh in 2045. The use of conventional

power plant capacities, storage facilities and load-side

flexibilities is strongly aligned with the volatile generation

from renewable energy. Photovoltaics in particular domi-

nate the power system in the summer months and favour

the regular use of storage and electrolysers. Gas power

plants are used almost exclusively in the winter months.

The German power system is supported to a consider-

able extent by power generation from renewable energy,

especially in summer. The number of full load hours of

gas power plants in the scenarios is in some cases signifi-

cantly below 1,000 h/a.

In the various scenarios, Germany develops into a large

net power importer in Europe. This is primarily attrib-

utable to the relatively high domestic power demand and

the high installed capacity of renewable energy abroad.

The imported power increases significantly from 2037 to

2045, in C 2045 presenting the highest increase. Large

amounts of electricity are mainly imported from France,

Austria and Scandinavia in the scenarios.

A significant share of the German hydrogen demand can

be covered by domestic water electrolysis in the scenarios.

Because the hydrogen demand is subject to seasonal

fluctuations, long-term hydrogen storage or hydrogen

imports must be used to operate gas power plants in the

winter months.

The demand for power transport within Germany in-

creases significantly until 2037. By contrast, there is no

longer a significant increase in transport between 2037

and 2045 in the scenarios. Southern and western federal

states tend to experience a generation deficit in the scenar-

ios, while there is a generation surplus in northern and

eastern federal states. The demand for transport within

Germany is largely determined by a high generation of

wind energy in the north and the location of the consump-

tion centres in western and southern Germany. In addition,

load flows occur in the opposite direction due to situations

with high photovoltaic generation in the south.

Depending on the share of carbon-neutral hydrogen for

power generation in 2037, the remaining CO

2

emissions

are reduced. In all three scenarios, the power system

is still responsible for low residual emissions in 2045.

These emissions are attributable to waste incineration

in power plants and must be offset elsewhere to achieve

greenhouse gas neutrality.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 14

GDP compact

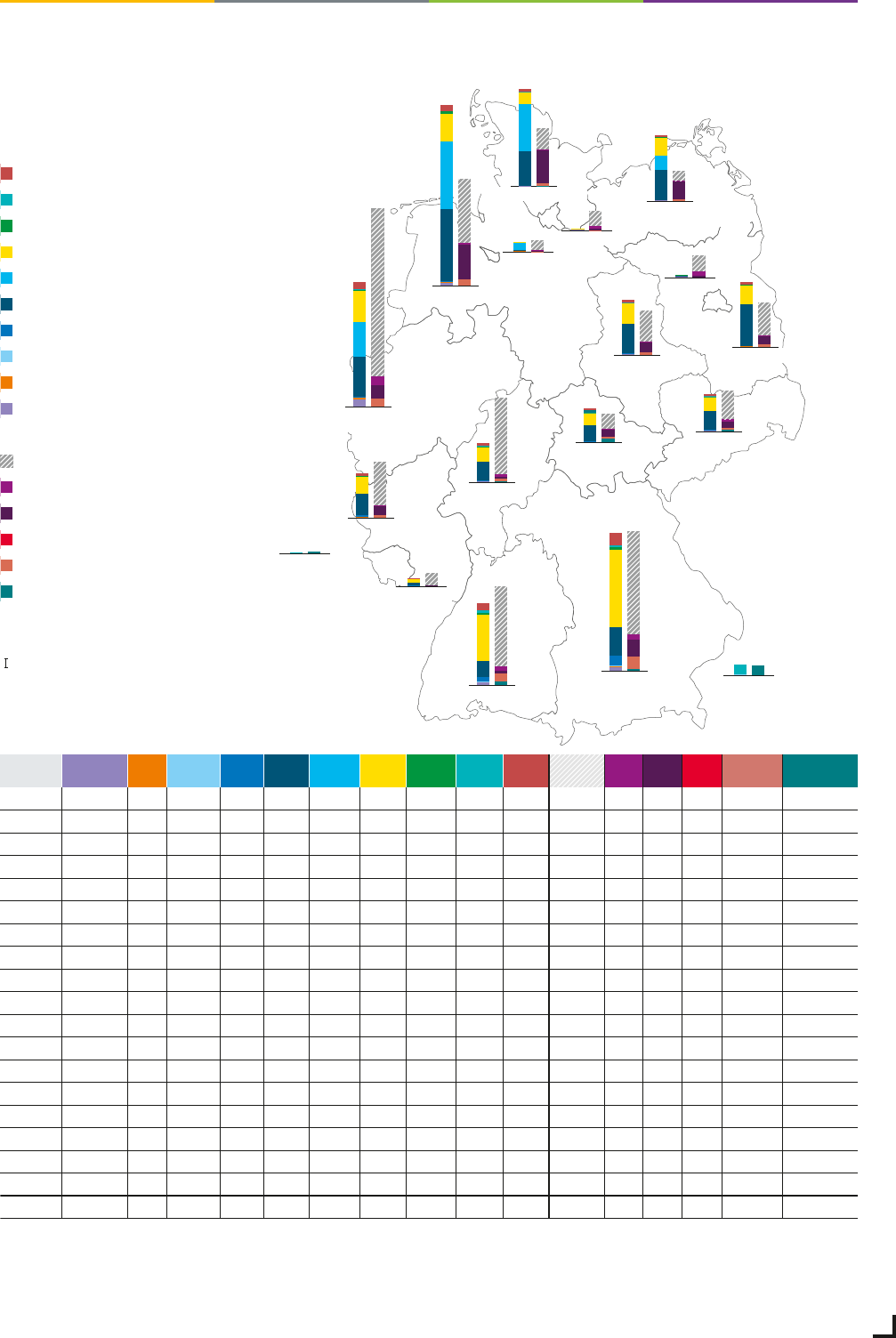

Schleswig-Holstein (SH)

Bremen (HB)

Hamburg (HH)

Berlin (BE)

Baden-Württemberg (BW)

Saarland (SL)

in TWh

Natural gas/

Hydrogen

Waste

Reservoir

water

Running

water

Wind

onshore

Wind

offshore

Photo-

voltaics

Biomass

Pumped

storage

Battery

storage

Power con-

sumption***

PtH PtG DSM

Battery

procurement

Pumped storage

procurement

BW

BY

BE

BB

HB

HH

HE

MV

NI

NW

RP

SL

SN

ST

SH

TH

LU (DE)*

AT (DE)*

Total**

Mecklenburg-

Western Pomerania (MV)

Bavaria (BY)

Baden-Württemberg (BW)

Rhineland-Palatinate (RP)

Saxony-Anhalt (ST)

Saxony (SN)

Brandenburg (BB)

Berlin (BE)

Luxembourg (DE)*

Austria (DE)*

Lower Saxony (NI)

*

Generation plants abroad with feed-in to the German transmission grid.

**

Rounding deviations may occur when the individual values are summed.

***

In this presentation, power consumption comprises net power consumption including all grid losses without considering the adjacent power

consumption by power-to-hydrogen and power-to-heat plants (district heating) as well as demand side management. Grid losses in the transmission

grid cannot be clearly allocated to the federal states.

Source: Transmission system operators

Battery storage

Pumped storage

Biomass

Photovoltaics

Wind offshore

Wind onshore

Running water

Reservoir water

Waste

Natural gas/hydrogen

Demand

***

Power-to-Heat

Power-to-Gas

DSM

Battery procurement

Pumped storage procurement

Scale

10 TWh

Thuringia (TH)

North Rhine-

Westphalia (NW)

Hesse (HE)

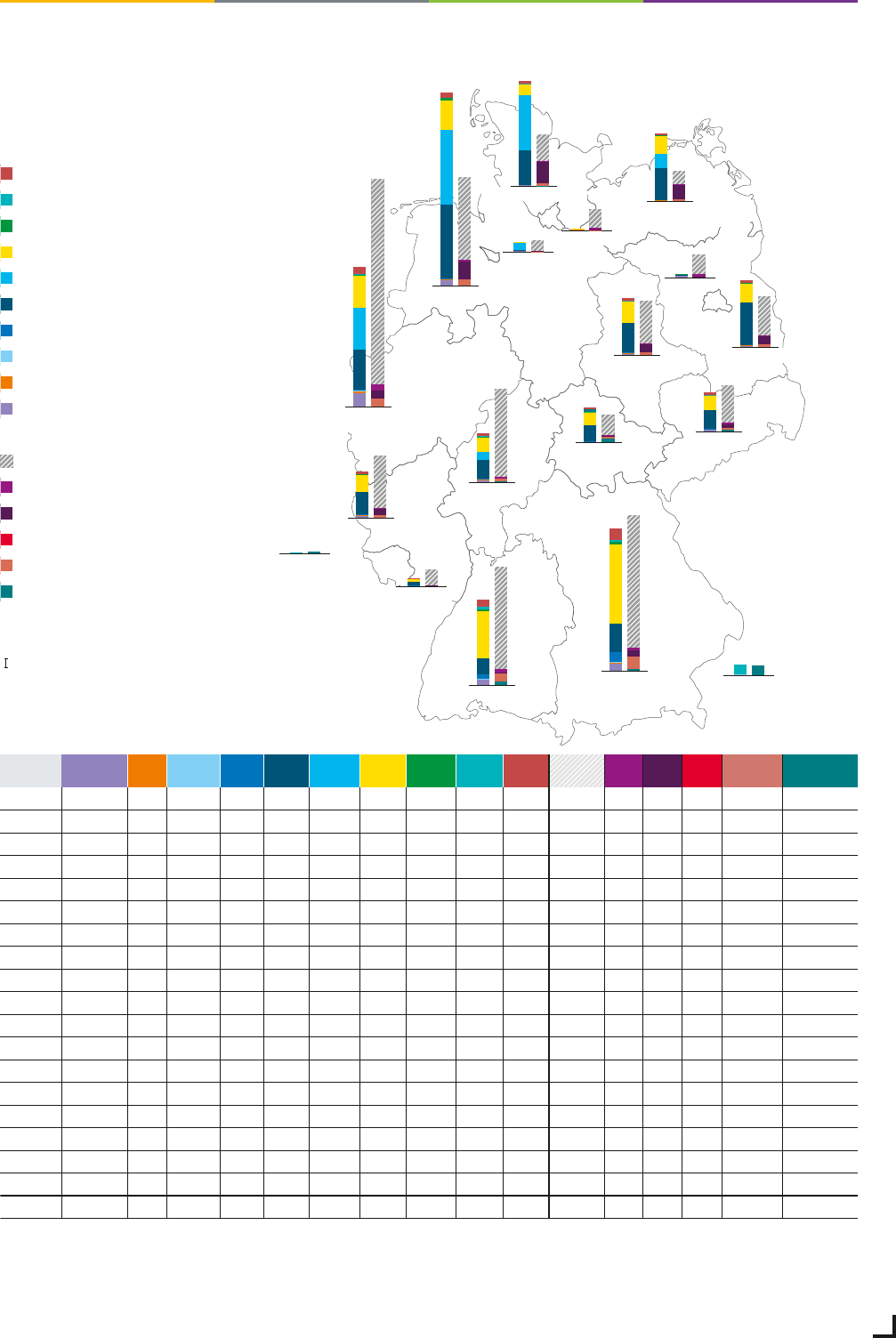

Figure 33: Energy balance in scenario A 2037

A 2037

3.2 0.5 0.1 4.2 15.9 0.0 46.0 1.6 2.8 7.3 79.3 4.8 2.6 -0.1 7.7 3.5

4.0 1.2 0.2 9.9 27.8 0.0 76.8 2.7 2.1 11.9 102.2 4.8 16.9 -0.1 12.5 1.9

1.4 0.2 0.0 0.0 0.3 0.0 0.7 0.1 0.0 0.2 16.1 4.1 1.7 0.0 0.2 0.0

0.6 0.7 0.0 0.0 41.9 0.0 18.0 0.7 0.0 2.8 32.1 0.7 8.7 0.0 2.9 0.0

0.5 0.6 0.0 0.0 0.6 7.6 0.3 0.0 0.0 0.1 9.6 0.6 1.0 0.0 0.1 0.0

0.4 0.1 0.0 0.0 0.3 0.0 0.3 0.1 0.0 0.1 15.3 2.5 1.2 0.0 0.1 0.0

1.0 1.0 0.0 0.3 18.1 0.0 14.7 0.5 0.6 2.7 76.0 2.6 2.0 0.0 2.8 0.7

0.2 0.1 0.0 0.0 31.2 13.9 17.6 0.6 0.0 2.2 10.0 0.5 17.6 0.0 2.3 0.0

3.1 0.6 0.4 0.3 71.6 66.5 28.0 2.8 0.0 5.8 63.2 1.9 34.6 -0.1 6.1 0.0

6.7 2.2 0.3 0.7 39.6 33.7 31.0 1.5 0.1 7.2 166.5 9.0 13.2 -0.1 7.6 0.2

1.1 0.5 0.0 1.0 21.9 0.0 17.0 0.3 0.0 2.8 43.1 1.0 8.9 0.0 2.9 0.0

0.4 0.2 0.0 0.1 3.2 0.0 3.1 0.0 0.0 0.6 12.3 0.4 0.2 0.0 0.6 0.0

1.0 0.1 0.0 0.4 18.3 0.0 13.3 0.5 0.9 2.2 28.6 2.3 6.2 0.0 2.3 1.1

0.8 1.0 0.0 0.1 28.7 0.0 20.7 0.9 0.1 2.7 30.9 0.9 9.8 0.0 2.9 0.1

0.4 0.3 0.0 0.0 34.2 46.9 10.9 0.9 0.1 2.4 20.8 1.1 32.9 0.0 2.6 0.1

0.5 0.1 0.0 0.1 15.5 0.0 12.5 0.4 2.7 1.7 14.9 0.7 7.4 0.0 1.8 3.3

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.8 0.0 0.0 0.0 0.0 0.0 1.2

0.0 0.0 0.9 0.0 0.0 0.0 0.0 0.0 9.3 0.0 0.0 0.0 0.0 0.0 9.5

25.3 9.2 2.0 17.3 368.9 168.5 310.6 13.5 19.4 52.6 746.0 37.7 164.9 -0.5 55.3 21.7

NEP 2037/2045, Version 2023, 2. Entwurf – Kapitel 2, Abb. 10–13 – CBE DIGIDEN Entwurf vom 22. Juni 2023, 11:54 AM

Energy balance in scenario A 2037

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 15

GDP compact

Schleswig-Holstein (SH)

Bremen (HB)

Hamburg (HH)

Berlin (BE)

Baden-Württemberg (BW)

Saarland (SL)

in TWh

Natural gas/

Hydrogen

Waste

Reservoir

water

Running

water

Wind

onshore

Wind

offshore

Photo-

voltaics

Biomass

Pumped

storage

Battery

storage

Power con-

sumption***

PtH PtG DSM

Battery

procurement

Pumped storage

procurement

BW

BY

BE

BB

HB

HH

HE

MV

NI

NW

RP

SL

SN

ST

SH

TH

LU (DE)*

AT (DE)*

Total**

Mecklenburg-

Western Pomerania (MV)

Bavaria (BY)

Baden-Württemberg (BW)

Rhineland-Palatinate (RP)

Saxony-Anhalt (ST)

Saxony (SN)

Brandenburg (BB)

Berlin (BE)

Luxembourg (DE)*

Austria (DE)*

Lower Saxony (NI)

*

Generation plants abroad with feed-in to the German transmission grid.

**

Rounding deviations may occur when the individual values are summed.

***

In this presentation, power consumption comprises net power consumption including all grid losses without considering the adjacent power

consumption by power-to-hydrogen and power-to-heat plants (district heating) as well as demand side management. Grid losses in the transmission

grid cannot be clearly allocated to the federal states.

Source: Transmission system operators

Thuringia (TH)

North Rhine-

Westphalia (NW)

Hesse (HE)

Battery storage

Pumped storage

Biomass

Photovoltaics

Wind offshore

Wind onshore

Running water

Reservoir water

Waste

Natural gas/hydrogen ****

Demand

***

Power-to-Heat

Power-to-Gas

DSM

Battery procurement

Pumped storage procurement

Scale

10 TWh

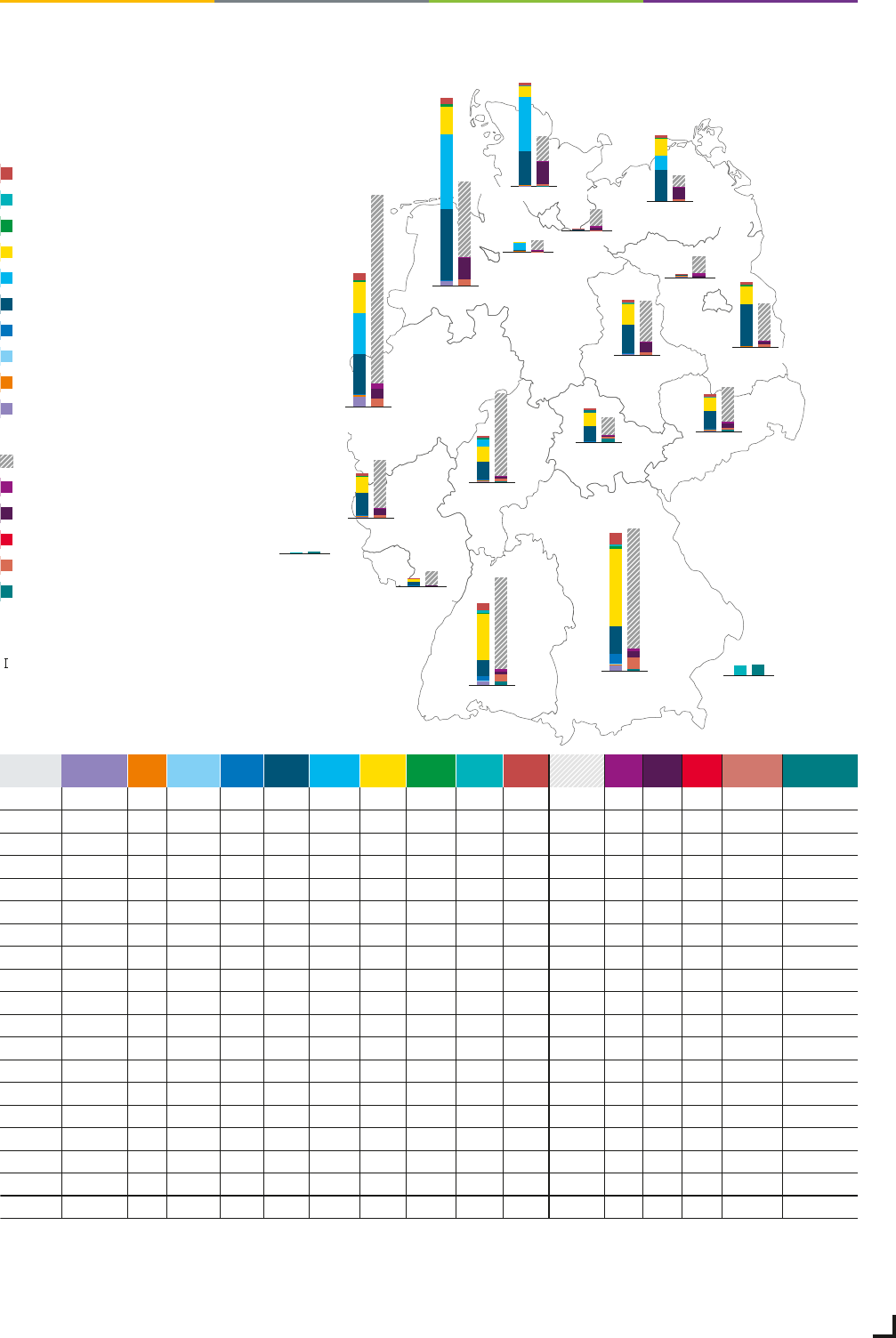

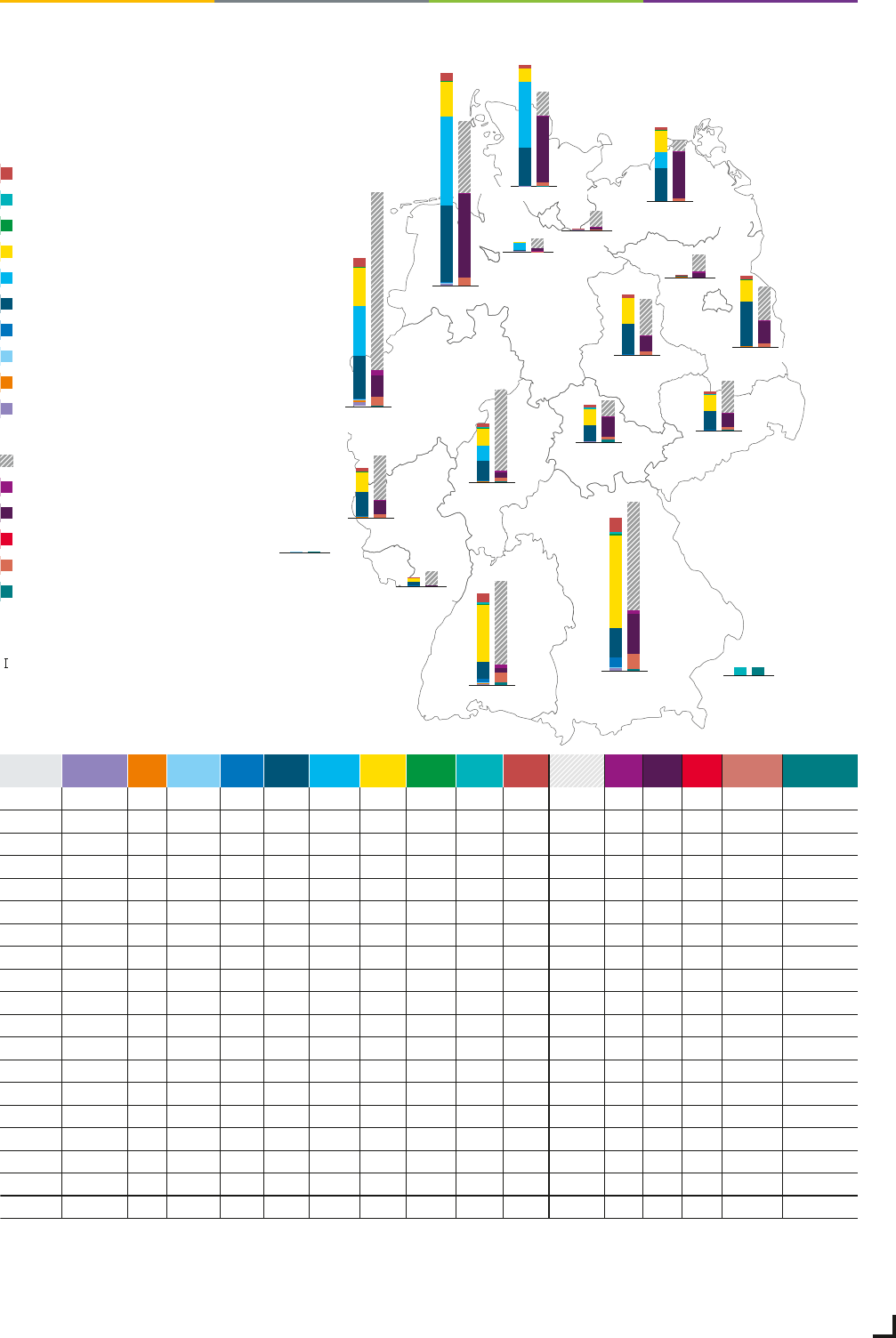

Figure 34: Energy balance in scenario B 2037

B 2037

Natural gas/

hydrogen****

4.0 0.5 0.1 4.2 15.7 0.0 45.7 1.6 2.7 6.9 91.2 2.8 2.2 -0.2 7.3 3.5

5.4 1.2 0.2 9.9 27.5 0.0 76.3 2.7 2.1 11.2 118.8 2.7 6.0 -0.2 11.8 1.9

1.8 0.2 0.0 0.0 0.3 0.0 0.7 0.1 0.0 0.1 16.9 2.1 1.9 0.0 0.2 0.0

0.8 0.8 0.0 0.0 41.5 0.0 17.9 0.7 0.0 2.6 36.8 0.4 3.5 0.0 2.8 0.0

0.6 0.6 0.0 0.0 0.6 7.5 0.3 0.0 0.0 0.1 9.9 0.3 1.0 0.0 0.1 0.0

0.5 0.1 0.0 0.0 0.3 0.0 0.3 0.1 0.0 0.1 16.9 1.4 2.7 0.0 0.1 0.0

1.4 1.0 0.0 0.3 17.9 7.6 14.6 0.5 0.6 2.5 81.7 1.5 1.6 -0.1 2.7 0.7

0.3 0.1 0.0 0.0 30.9 13.8 17.5 0.6 0.0 2.1 11.4 0.3 12.0 0.0 2.2 0.0

4.1 0.6 0.4 0.3 70.8 73.4 27.8 2.8 0.0 5.5 75.2 1.1 21.3 -0.1 5.8 0.0

9.1 2.3 0.3 0.7 39.2 40.9 30.9 1.5 0.1 6.8 187.4 5.1 10.0 -0.3 7.2 0.1

1.5 0.5 0.0 1.0 21.6 0.0 16.9 0.3 0.0 2.6 47.8 0.6 6.4 -0.1 2.8 0.0

0.5 0.2 0.0 0.1 3.2 0.0 3.0 0.0 0.0 0.5 14.2 0.2 0.2 0.0 0.6 0.0

1.3 0.1 0.0 0.4 18.1 0.0 13.2 0.5 0.8 2.0 34.1 1.3 4.7 0.0 2.1 1.1

1.1 1.0 0.0 0.1 28.4 0.0 20.5 0.9 0.1 2.6 40.3 0.5 10.5 0.0 2.7 0.1

0.6 0.3 0.0 0.0 33.9 53.5 10.8 0.9 0.1 2.3 24.7 0.6 22.3 0.0 2.4 0.1

0.6 0.1 0.0 0.1 15.3 0.0 12.4 0.4 2.5 1.6 18.1 0.4 1.4 0.0 1.7 3.1

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.8 0.0 0.0 0.0 0.0 0.0 0.0 1.1

0.0 0.0 0.9 0.0 0.0 0.0 0.0 0.0 9.5 0.0 0.0 0.0 0.0 0.0 0.0 9.9

33.7 9.4 2.0 17.3 365.2 196.6 308.7 13.5 19.4 49.8 854.4 21.4 108.0 -1.0 52.3 21.7

NEP 2037/2045, Version 2023, 2. Entwurf – Kapitel 2, Abb. 33–38 – CBE DIGIDEN Entwurf vom 22. Juni 2023, 11:54 AM

Energy balance in scenario B 2037

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 16

GDP compact

Schleswig-Holstein (SH)

Bremen (HB)

Hamburg (HH)

Berlin (BE)

Baden-Württemberg (BW)

Saarland (SL)

in TWh

Natural gas/

Hydrogen

Waste

Reservoir

water

Running

water

Wind

onshore

Wind

offshore

Photo-

voltaics

Biomass

Pumped

storage

Battery

storage

Power con-

sumption***

PtH PtG DSM

Battery

procurement

Pumped storage

procurement

BW

BY

BE

BB

HB

HH

HE

MV

NI

NW

RP

SL

SN

ST

SH

TH

LU (DE)*

AT (DE)*

Total**

Mecklenburg-

Western Pomerania (MV)

Bavaria (BY)

Baden-Württemberg (BW)

Rhineland-Palatinate (RP)

Saxony-Anhalt (ST)

Saxony (SN)

Brandenburg (BB)

Berlin (BE)

Luxembourg (DE)*

Austria (DE)*

Lower Saxony (NI)

Thuringia (TH)

North Rhine-

Westphalia (NW)

Hesse (HE)

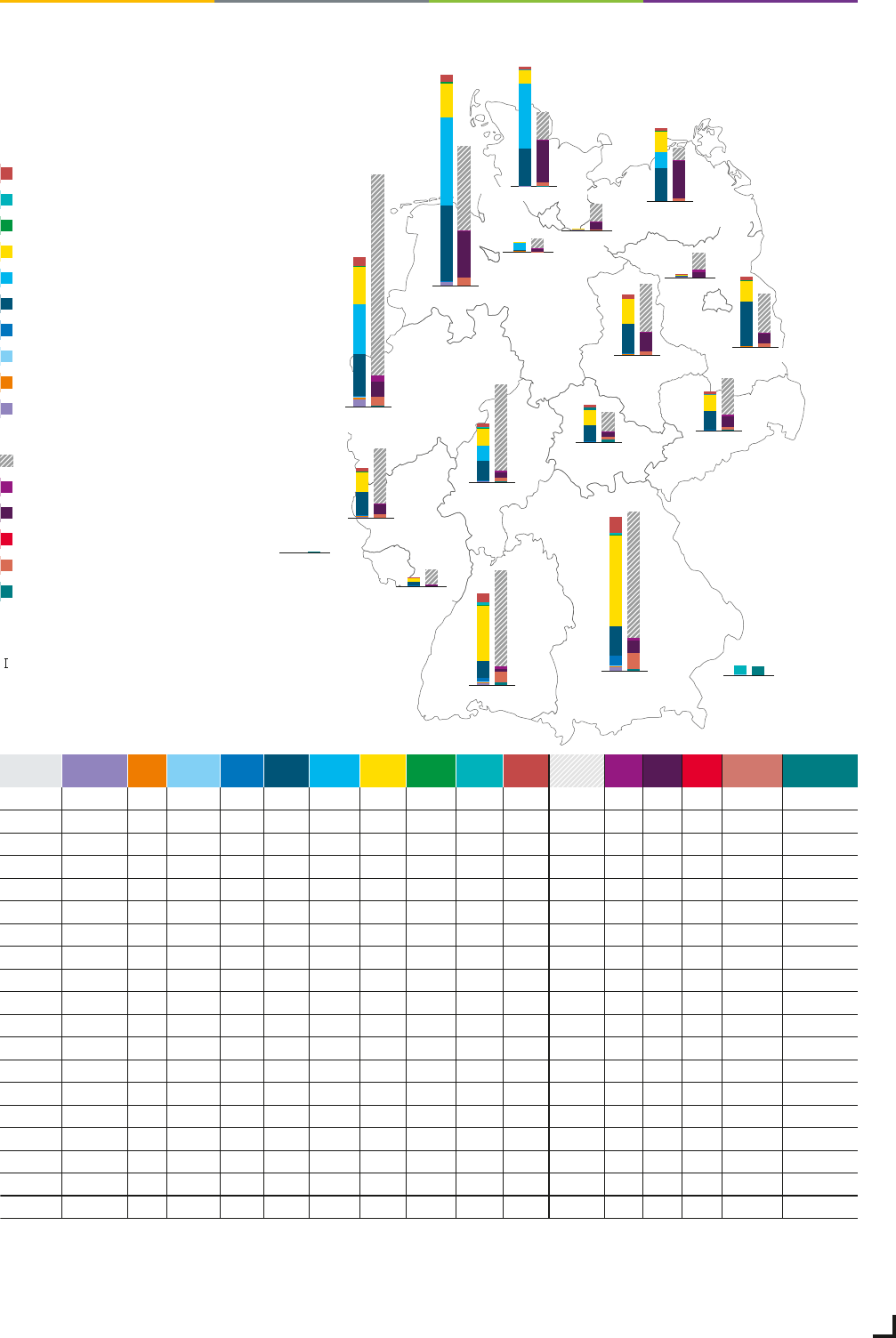

Figure 35: Energy balance in scenario C 2037

*

Generation plants abroad with feed-in to the German transmission grid.

**

Rounding deviations may occur when the individual values are summed.

***

In this presentation. power consumption comprises net power consumption including all grid losses without considering the adjacent power

consumption by power-to-hydrogen and power-to-heat plants (district heating) as well as demand side management. Grid losses in the transmission

grid cannot be clearly allocated to the federal states.

****

Includes utilisation of reserves near consumption areas.

Source: Transmission system operators

Battery storage

Pumped storage

Biomass

Photovoltaics

Wind offshore

Wind onshore

Running water

Reservoir water

Waste

Natural gas/hydrogen ****

Demand

***

Power-to-Heat

Power-to-Gas

DSM

Battery procurement

Pumped storage procurement

Scale

10 TWh

C 2037

Natural gas/

hydrogen****

5.5 0.5 0.1 4.2 16.4 0.0 46.6 1.6 2.8 7.1 101.2 3.4 1.60 -0.2 7.5 3.6

7.3 1.2 0.2 9.9 28.5 0.0 77.9 2.7 2.1 11.5 131.0 3.4 6.04 -0.3 12.1 1.9

2.4 0.2 0.0 0.0 0.3 0.0 0.7 0.1 0.0 0.2 18.8 2.7 0.97 0.0 0.2 0.0

1.2 0.8 0.0 0.0 42.6 0.0 18.3 0.7 0.0 2.7 38.8 0.5 8.38 0.0 2.8 0.0

0.8 0.6 0.0 0.0 0.6 7.6 0.3 0.0 0.0 0.1 10.5 0.4 0.43 0.0 0.1 0.0

0.7 0.1 0.0 0.0 0.3 0.0 0.3 0.1 0.0 0.1 18.1 1.8 0.74 0.0 0.1 0.0

2.1 1.0 0.0 0.3 18.7 7.6 14.9 0.5 0.6 2.6 87.0 1.9 0.53 -0.1 2.7 0.7

0.5 0.1 0.0 0.0 32.1 14.0 17.9 0.6 0.0 2.1 12.7 0.4 14.55 0.0 2.3 0.0

5.7 0.6 0.4 0.3 73.4 74.3 28.4 2.8 0.0 5.6 82.7 1.3 18.08 -0.1 5.9 0.0

12.8 2.3 0.3 0.7 40.4 41.4 31.5 1.5 0.1 7.0 203.4 6.3 8.43 -0.3 7.3 0.1

2.3 0.5 0.0 1.0 22.5 0.0 17.2 0.3 0.0 2.7 52.0 0.7 6.37 -0.1 2.8 0.0

0.7 0.2 0.0 0.1 3.3 0.0 3.1 0.0 0.0 0.5 15.3 0.3 0.19 0.0 0.6 0.0

1.7 0.1 0.0 0.4 18.9 0.0 13.5 0.5 0.8 2.1 37.2 1.6 3.72 -0.1 2.2 1.1

1.5 1.1 0.0 0.1 29.2 0.0 21.0 0.9 0.1 2.6 42.0 0.7 8.22 0.0 2.8 0.1

0.8 0.3 0.0 0.0 34.8 54.1 11.0 0.9 0.1 2.4 26.6 0.8 21.68 0.0 2.5 0.1

0.8 0.1 0.0 0.1 15.9 0.0 12.6 0.4 2.6 1.6 19.8 0.5 1.86 0.0 1.7 3.2

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.8 0.0 0.0 0.0 0.0 0.0 0.0 1.2

0.0 0.0 0.9 0.0 0.0 0.0 0.0 0.0 9.5 0.0 0.0 0.0 0.0 0.0 0.0 9.9

46.6 9.5 2.0 17.3 377.8 199.0 315.1 13.5 19.4 50.7 928.2 26.5 101.8 -1.3 53.4 21.8

NEP 2037/2045, Version 2023, 2. Entwurf – Kapitel 2, Abb. 33–38 – CBE DIGIDEN Entwurf vom 22. Juni 2023, 11:54 AM

Energy balance in scenario C 2037

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 17

GDP compact

Schleswig-Holstein (SH)

Bremen (HB)

Hamburg (HH)

Berlin (BE)

Baden-Württemberg (BW)

Saarland (SL)

in TWh

Natural gas/

Hydrogen

Waste

Reservoir

water

Running

water

Wind

onshore

Wind

offshore

Photo-

voltaics

Biomass

Pumped

storage

Battery

storage

Power con-

sumption***

PtH PtG DSM

Battery

procurement

Pumped storage

procurement

BW

BY

BE

BB

HB

HH

HE

MV

NI

NW

RP

SL

SN

ST

SH

TH

LU (DE)*

AT (DE)*

Total**

Mecklenburg-

Western Pomerania (MV)

Bavaria (BY)

Baden-Württemberg (BW)

Rhineland-Palatinate (RP)

Saxony-Anhalt (ST)

Saxony (SN)

Brandenburg (BB)

Berlin (BE)

Luxembourg (DE)*

Austria (DE)*

Lower Saxony (NI)

*

Generation plants abroad with feed-in to the German transmission grid.

**

Rounding deviations may occur when the individual values are summed.

***

In this presentation, power consumption comprises net power consumption including all grid losses without considering the adjacent power

consumption by power-to-hydrogen and power-to-heat plants (district heating) as well as demand side management. Grid losses in the transmission

grid cannot be clearly allocated to the federal states.

Source: Transmission system operators

Battery storage

Pumped storage

Biomass

Photovoltaics

Wind offshore

Wind onshore

Running water

Reservoir water

Waste

Natural gas/hydrogen

Demand

***

Power-to-Heat

Power-to-Gas

DSM

Battery procurement

Pumped storage procurement

Scale

10 TWh

Thuringia (TH)

North Rhine-

Westphalia (NW)

Hesse (HE)

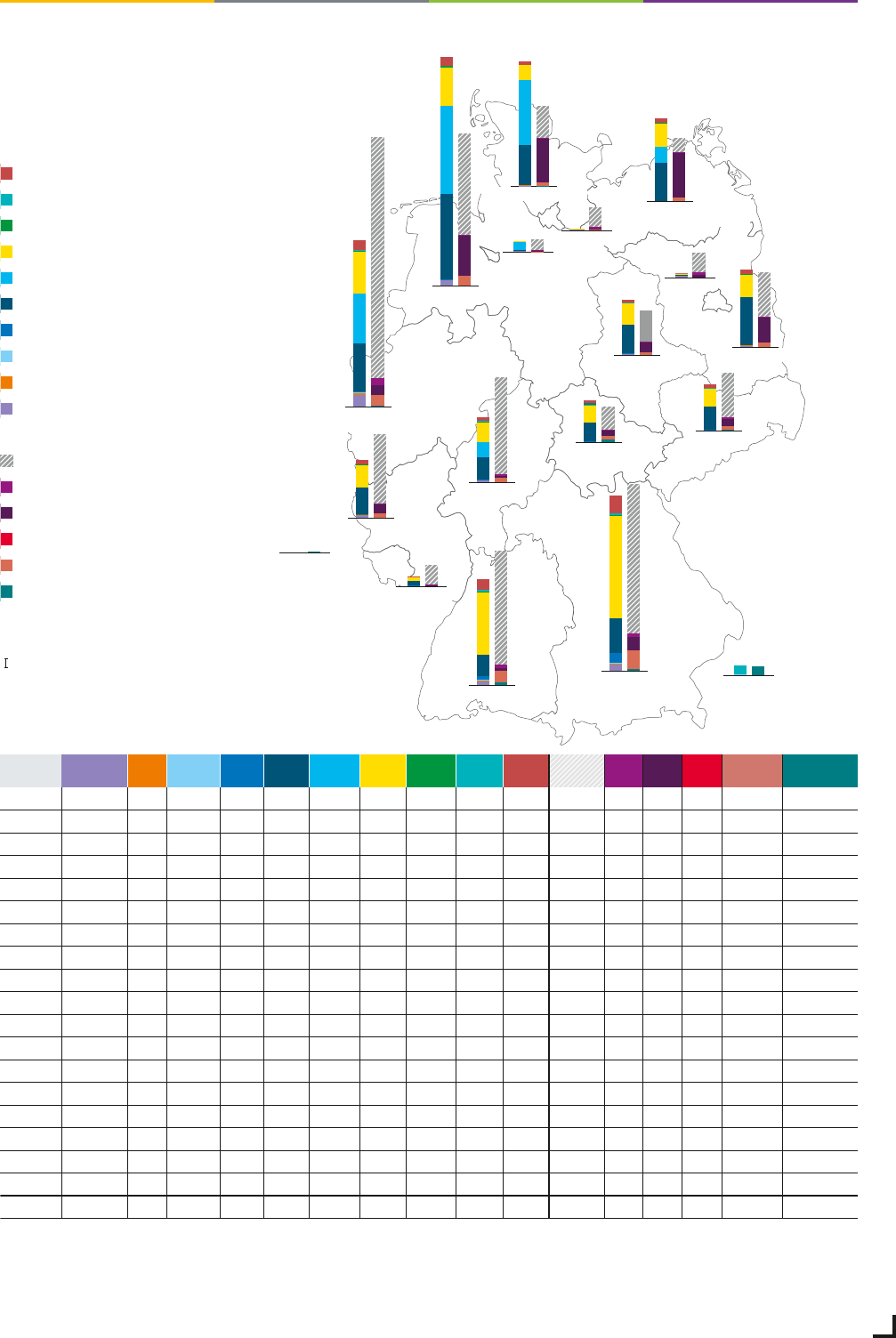

Figure 36: Energy balance in scenario A 2045

A 2045

1.6 0.4 0.1 4.2 16.9 0.0 55.9 0.7 2.1 9.0 83.7 3.0 4.7 -0.2 9.5 2.6

2.2 1.1 0.2 9.9 29.1 0.0 91.8 1.2 1.8 14.6 107.8 3.0 39.8 -0.2 15.4 1.5

0.9 0.2 0.0 0.0 0.3 0.0 0.8 0.0 0.0 0.2 16.3 2.5 3.7 0.0 0.2 0.0

0.3 0.7 0.0 0.0 44.4 0.0 21.2 0.3 0.0 3.6 33.9 0.4 22.4 0.0 3.8 0.0

0.3 0.5 0.0 0.0 0.7 7.7 0.4 0.0 0.0 0.1 9.7 0.4 2.5 0.0 0.1 0.0

0.1 0.1 0.0 0.0 0.3 0.0 0.3 0.0 0.0 0.1 15.6 1.6 1.8 0.0 0.1 0.0

0.3 0.9 0.0 0.3 19.3 15.0 18.1 0.2 0.5 3.4 80.5 1.7 5.4 -0.1 3.6 0.5

0.0 0.1 0.0 0.0 32.6 16.2 21.4 0.3 0.0 3.0 10.5 0.3 46.1 0.0 3.2 0.0

1.8 0.6 0.4 0.3 76.3 87.8 34.5 1.3 0.0 7.4 71.4 1.2 82.6 -0.1 7.8 0.0

4.0 2.2 0.3 0.7 42.2 50.0 37.6 0.7 0.1 8.6 176.1 5.6 20.9 -0.2 9.1 0.1

0.7 0.5 0.0 1.0 23.4 0.0 20.7 0.1 0.0 3.5 44.3 0.6 13.2 0.0 3.7 0.0

0.2 0.2 0.0 0.1 3.5 0.0 3.6 0.0 0.0 0.7 13.7 0.2 0.2 0.0 0.7 0.0

0.3 0.1 0.0 0.4 19.0 0.0 16.1 0.2 0.6 2.7 31.0 1.4 13.2 0.0 2.9 0.8

0.3 1.0 0.0 0.1 30.1 0.0 24.9 0.4 0.1 3.6 36.4 0.6 15.0 0.0 3.8 0.1

0.2 0.3 0.0 0.0 37.3 65.3 13.1 0.4 0.1 3.0 23.2 0.7 66.2 0.0 3.2 0.1

0.1 0.1 0.0 0.1 16.3 0.0 15.4 0.2 2.1 2.2 16.0 0.5 20.1 0.0 2.3 2.5

0.0 0.0 0.9 0.0 0.0 0.0 0.0 0.0 0.6 0.0 0.0 0.0 0.0 0.0 0.0 0.9

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 7.6 0.0 0.0 0.0 0.0 0.0 0.0 7.4

13.3 9.0 2.0 17.3 391.7 242.0 375.8 6.0 15.4 65.9 801.4 23.5 357.8 -1.0 69.3 16.4

NEP 2037/2045, Version 2023, 2. Entwurf – Kapitel 2, Abb. 33–38 – CBE DIGIDEN Entwurf vom 22. Juni 2023, 11:54 AM

Energy balance in scenario A 2045

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 18

GDP compact

Schleswig-Holstein (SH)

Bremen (HB)

Hamburg (HH)

Berlin (BE)

Baden-Württemberg (BW)

Saarland (SL)

in TWh

Natural gas/

Hydrogen

Waste

Reservoir

water

Running

water

Wind

onshore

Wind

offshore

Photo-

voltaics

Biomass

Pumped

storage

Battery

storage

Power con-

sumption***

PtH PtG DSM

Battery

procurement

Pumped storage

procurement

BW

BY

BE

BB

HB

HH

HE

MV

NI

NW

RP

SL

SN

ST

SH

TH

LU (DE)*

AT (DE)*

Total**

Mecklenburg-

Western Pomerania (MV)

Bavaria (BY)

Baden-Württemberg (BW)

Rhineland-Palatinate (RP)

Saxony-Anhalt (ST)

Saxony (SN)

Brandenburg (BB)

Berlin (BE)

Luxembourg (DE)*

Austria (DE)*

Lower Saxony (NI)

*

Generation plants abroad with feed-in to the German transmission grid.

**

Rounding deviations may occur when the individual values are summed.

***

In this presentation, power consumption comprises net power consumption including all grid losses without considering the adjacent power

consumption by power-to-hydrogen and power-to-heat plants (district heating) as well as demand side management. Grid losses in the transmission

grid cannot be clearly allocated to the federal states.

Source: Transmission system operators

Battery storage

Pumped storage

Biomass

Photovoltaics

Wind offshore

Wind onshore

Running water

Reservoir water

Waste

Natural gas/hydrogen

Demand

***

Power-to-Heat

Power-to-Gas

DSM

Battery procurement

Pumped storage procurement

Scale

10 TWh

Thuringia (TH)

North Rhine-

Westphalia (NW)

Hesse (HE)

Figure 37: Energy balance in scenario B 2045

B 2045

2.4 0.5 0.1 4.2 16.7 0.0 54.9 0.7 2.3 9.3 94.6 3.1 2.9 -0.2 9.8 2.9

3.9 1.2 0.2 9.9 28.7 0.0 90.1 1.2 1.9 15.1 125.1 3.0 12.4 -0.3 15.9 1.6

1.5 0.2 0.0 0.0 0.3 0.0 0.8 0.0 0.0 0.2 16.8 2.4 5.2 0.0 0.2 0.0

0.5 0.7 0.0 0.0 43.9 0.0 20.8 0.3 0.0 3.7 38.9 0.4 9.7 0.0 3.9 0.0

0.5 0.6 0.0 0.0 0.7 7.6 0.4 0.0 0.0 0.1 9.8 0.4 3.0 0.0 0.1 0.0

0.2 0.1 0.0 0.0 0.3 0.0 0.3 0.0 0.0 0.1 17.1 1.6 7.1 0.0 0.1 0.0

0.8 1.0 0.0 0.3 19.1 14.8 17.7 0.2 0.5 3.5 86.2 1.7 5.1 -0.1 3.7 0.6

0.1 0.1 0.0 0.0 32.2 16.1 21.0 0.3 0.0 3.1 11.9 0.3 37.2 0.0 3.3 0.0

3.1 0.6 0.4 0.3 75.3 86.7 33.8 1.3 0.0 7.6 83.8 1.2 45.5 -0.2 8.0 0.0

6.7 2.2 0.3 0.7 41.7 49.5 36.9 0.7 0.1 8.9 199.6 5.7 15.0 -0.4 9.4 0.1

1.1 0.5 0.0 1.0 23.1 0.0 20.3 0.1 0.0 3.6 54.3 0.6 9.9 -0.1 3.8 0.0

0.4 0.2 0.0 0.1 3.5 0.0 3.6 0.0 0.0 0.7 15.4 0.2 0.2 0.0 0.7 0.0

0.6 0.1 0.0 0.4 18.8 0.0 15.8 0.2 0.7 2.8 36.5 1.5 10.7 -0.1 2.9 0.9

0.5 1.0 0.0 0.1 29.7 0.0 24.4 0.4 0.1 3.7 47.1 0.6 18.8 0.0 3.9 0.1

0.3 0.3 0.0 0.0 36.8 64.6 12.8 0.4 0.1 3.1 26.9 0.7 42.0 0.0 3.3 0.1

0.2 0.1 0.0 0.1 16.1 0.0 15.1 0.2 2.2 2.3 19.5 0.5 4.6 0.0 2.4 2.7

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.7 0.0 0.0 0.0 0.0 0.0 0.0 0.9

0.0 0.0 0.9 0.0 0.0 0.0 0.0 0.0 8.5 0.0 0.0 0.0 0.0 0.0 0.0 8.5

22.7 9.1 2.0 17.3 386.9 239.2 368.7 6.0 17.0 67.8 914.8 23.7 229.7 -1.4 71.4 18.5

NEP 2037/2045, Version 2023, 2. Entwurf – Kapitel 2, Abb. 33–38 – CBE DIGIDEN Entwurf vom 22. Juni 2023, 11:54 AM

Energy balance in scenario B 2045

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 19

GDP compact

Schleswig-Holstein (SH)

Bremen (HB)

Hamburg (HH)

Berlin (BE)

Baden-Württemberg (BW)

Saarland (SL)

in TWh

Natural gas/

Hydrogen

Waste

Reservoir

water

Running

water

Wind

onshore

Wind

offshore

Photo-

voltaics

Biomass

Pumped

storage

Battery

storage

Power con-

sumption***

PtH PtG DSM

Battery

procurement

Pumped storage

procurement

BW

BY

BE

BB

HB

HH

HE

MV

NI

NW

RP

SL

SN

ST

SH

TH

LU (DE)*

AT (DE)*

Total**

Mecklenburg-

Western Pomerania (MV)

Bavaria (BY)

Baden-Württemberg (BW)

Rhineland-Palatinate (RP)

Saxony-Anhalt (ST)

Saxony (SN)

Brandenburg (BB)

Berlin (BE)

Luxembourg (DE)*

Austria (DE)*

Lower Saxony (NI)

Thuringia (TH)

North Rhine-

Westphalia (NW)

Hesse (HE)

Figure 38: Energy balance in scenario C 2045

*

Generation plants abroad with feed-in to the German transmission grid.

**

Rounding deviations may occur when the individual values are summed.

***

In this presentation. power consumption comprises net power consumption including all grid losses without considering the adjacent power

consumption by power-to-hydrogen and power-to-heat plants (district heating) as well as demand side management. Grid losses in the transmission

grid cannot be clearly allocated to the federal states.

****

Includes utilisation of reserves near consumption areas.

Source: Transmission system operators

Battery storage

Pumped storage

Biomass

Photovoltaics

Wind offshore

Wind onshore

Running water

Reservoir water

Waste

Natural gas/hydrogen ****

Demand

***

Power-to-Heat

Power-to-Gas

DSM

Battery procurement

Pumped storage procurement

Scale

10 TWh

C 2045

Natural gas/

hydrogen****

4.2 0.5 0.1 4.2 20.6 0.0 61.9 0.7 2.2 10.8 112.9 3.5 2.6 -0.3 11.3 2.8

6.2 1.2 0.2 9.9 34.8 0.0 101.0 1.2 1.8 17.5 148.5 3.5 13.2 -0.4 18.4 1.5

2.2 0.2 0.0 0.0 0.4 0.0 0.9 0.0 0.0 0.2 19.7 2.7 2.1 0.0 0.2 0.0

0.9 0.8 0.0 0.0 47.7 0.0 23.1 0.3 0.0 4.4 43.8 0.5 25.3 -0.1 4.6 0.0

0.7 0.6 0.0 0.0 0.7 7.7 0.4 0.0 0.0 0.1 10.7 0.4 1.0 0.0 0.1 0.0

0.4 0.1 0.0 0.0 0.3 0.0 0.4 0.0 0.0 0.1 19.9 1.8 0.8 -0.1 0.1 0.0

1.7 1.0 0.0 0.3 22.1 14.9 20.0 0.2 0.5 4.1 95.7 1.9 1.7 -0.1 4.3 0.5

0.2 0.1 0.0 0.0 37.6 16.2 23.6 0.3 0.0 3.7 14.3 0.4 44.4 0.0 3.9 0.0

5.1 0.6 0.4 0.3 84.1 87.4 38.3 1.3 0.0 8.9 100.2 1.4 39.5 -0.2 9.4 0.0

11.5 2.3 0.3 0.7 47.2 49.8 41.8 0.7 0.1 10.2 239.2 6.5 10.3 -0.5 10.8 0.1

2.1 0.5 0.0 1.0 26.8 0.0 22.9 0.1 0.0 4.3 68.8 0.7 9.4 -0.1 4.5 0.0

0.7 0.2 0.0 0.1 3.9 0.0 4.0 0.0 0.0 0.8 19.2 0.3 0.2 0.0 0.8 0.0

1.1 0.1 0.0 0.4 22.8 0.0 17.7 0.2 0.7 3.3 43.6 1.7 7.8 -0.1 3.5 0.8

1.2 1.0 0.0 0.1 32.6 0.0 27.5 0.4 0.1 4.4 57.2 0.7 13.0 -0.1 4.6 0.1

0.6 0.3 0.0 0.0 39.4 65.0 14.5 0.4 0.1 3.6 32.2 0.8 42.8 0.0 3.7 0.1

0.4 0.1 0.0 0.1 18.6 0.0 17.0 0.2 2.2 2.7 23.0 0.5 6.0 -0.1 2.9 2.6

0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.0 0.7 0.0 0.0 0.0 0.0 0.0 0.0 0.91

0.0 0.0 0.9 0.0 0.0 0.0 0.0 0.0 8.4 0.0 0.0 0.0 0.0 0.0 0.0 8.3

39.2 9.3 2.0 17.3 439.5 241.0 414.9 6.0 16.6 78.9 1.080.2 27.2 220.1 -2.1 83.1 18.0

NEP 2037/2045, Version 2023, 2. Entwurf – Kapitel 2, Abb. 33–38 – CBE DIGIDEN Entwurf vom 22. Juni 2023, 11:54 AM

Energy balance in scenario C 2045

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 20

GDP compact

Offshore grid:

Comprehensive development and

progressive interconnection of potentials

The GDP and the Site Development Plan form a coherent

set of plans with the geographical planning of the coastal

states. The implementation of these statutory require-

ments frequently leads to (chronological) overlaps in the

process of preparing the GDP and Site Development Plan.

The process of updating the Site Development Plan was

completed on 20/01/2023. The TSOs considered the Site

Development Plan stipulation in the first draft of the GDP

2037 / 2045 (2023). However, the Site Development Plan

2023 lacks geographical and temporal stipulations that

are necessary for achieving the statutory expansion tar-

gets for offshore wind for the years 2035 and 2045 accord-

ing to the WindSeeG. Considering the fact that offshore

grid connection systems take a long time to be realised,

the necessary fundamentals for confirming the expansion

targets through specific projects in a timely manner is

therefore currently lacking. In agreement with the Fed-

eral Network Agency, the second draft of GDP 2037 / 2045

(2023) is therefore largely based on the draft of Site De-

velopment Plan 2023 dated 1 July 2022. This applies

especially to the geographical allocation of areas, border

corridors and the planned completion dates for offshore

grid connection systems after 2031.

Expansion volume of offshore grid connection systems

Based on the offshore grid connection systems confirmed

by Federal Network Agency, in the GDP 2035 (2021), the

additional need for 20 new offshore grid connection

systems with a route length of approx. 8,455 km and

investment costs of EUR 86.7 billion were identified in

this GDP 2037 / 2045 (2023).

For the offshore expansion grid in the North Sea and the

Baltic Sea, this results in a length of

about 6,600 km with a transmission capacity of about

36 GW in scenario A 2037,

about 9,300 km with a transmission capacity of about

44 GW in scenarios B 2037 and C 2037,

and a length of 13,300 km with a transmission

capacity of about 61.2 GW for long-term scenarios

A 2045, B 2045 and C 2045.

The corresponding grid connection points (GLP) on land

were identified. The investments for the offshore grid con-

nection systems in the offshore grid expansion are based

on specific cost rates and are of a preliminary nature.

For scenario A 2037, the estimated investment volume

for the offshore expansion grid amounts to around

EUR 77 billion by 2037.

Scenarios B 2037 and C 2037 require investment costs

of about EUR 103.5 billion.

For long-term scenarios A 2045, B 2045 and

C 2045, the estimated investment costs are around

EUR 145.1 billion.

Moreover, the investment costsfor the offshore grid

expansion measures of the offshore initial grid that

are already being implemented amounts to around

EUR 12.4 billion for all scenarios.

For the generation capacities to be installed for offshore

wind of the approved scenario framework, all required

transmission lines respectively offshore grid connection

systems were determined. As a result, the number and

thus the required investments for the 2037 and 2045

scenarios go beyond the expansion path for offshore wind

depicted in the 2023 Site Development Plan. Accordingly,

they represent a possible path to achieving the further

statutory expansion targets of at least 40 GW by 2035 and

at least 70 GW by 2045.

For the first time, the GDP 2037 / 2045 (2023) considers

national offshore interconnection. Additionally, it pres-

ents the corresponding benefits and identifies a project

with two measures. The offshore interconnection refers

to the offshore connections between offshore grid con-

nection systems. An offshore transmission capacity will

be created between two onshore GLPs of the offshore

grid connection systems. This additional transmission

capacity can be used as a flexible bypass to relieve the

onshore transmission grid, thus minimising redispatch

interventions. Overall, national offshore interconnection

is shown to be a grid-supporting and cost-efficient ex-

pansion measure aimed at minimising long-range grid

bottlenecks. Further core results of the study on national

offshore interconnection and the offshore interconnec-

tion study on international interconnection needs are

published in a separate report.

The implementation of a high number of offshore grid con-

nection systems in a short period poses a great challenge in

terms of the manufacturer’s market, logistics and approval

procedures. This applies especially to the long offshore and

onshore cable routes to be implemented as well as the cor-

responding planning, approval and construction times.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 21

GDP compact

Measures of the North Sea offshore expansion grid in scenario A 2037

DC grid expansion

AC grid expansion

Boundary of the territorial sea

Boundary of the exclusive

economic zone

Border corridor

Converter platform

Transformer platform

Grid link point

Offshore wind farm areaProject name

Source: Transmission system operator / map basis © Mapbox, © OpenStreetMap (ODbL), BSH (© GeoSeaPortal)

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 22

GDP compact

Measures of the North Sea offshore expansion grid in scenarios B / C 2037

DC grid expansion

AC grid expansion

Boundary of the territorial sea

Boundary of the exclusive

economic zone

Border corridor

Converter platform

Transformer platform

Grid link point

Offshore wind farm areaProject name

Source: Transmission system operator / map basis © Mapbox, © OpenStreetMap (ODbL), BSH (© GeoSeaPortal)

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 23

GDP compact

Measures of the North Sea offshore expansion grid in scenarios A / B / C 2045

DC grid expansion

AC grid expansion

Boundary of the territorial sea

Boundary of the exclusive

economic zone

Border corridor

Converter platform

Transformer platform

Grid link point

Offshore wind farm areaProject name

Source: Transmission system operator / map basis © Mapbox, © OpenStreetMap (ODbL), BSH (© GeoSeaPortal)

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 24

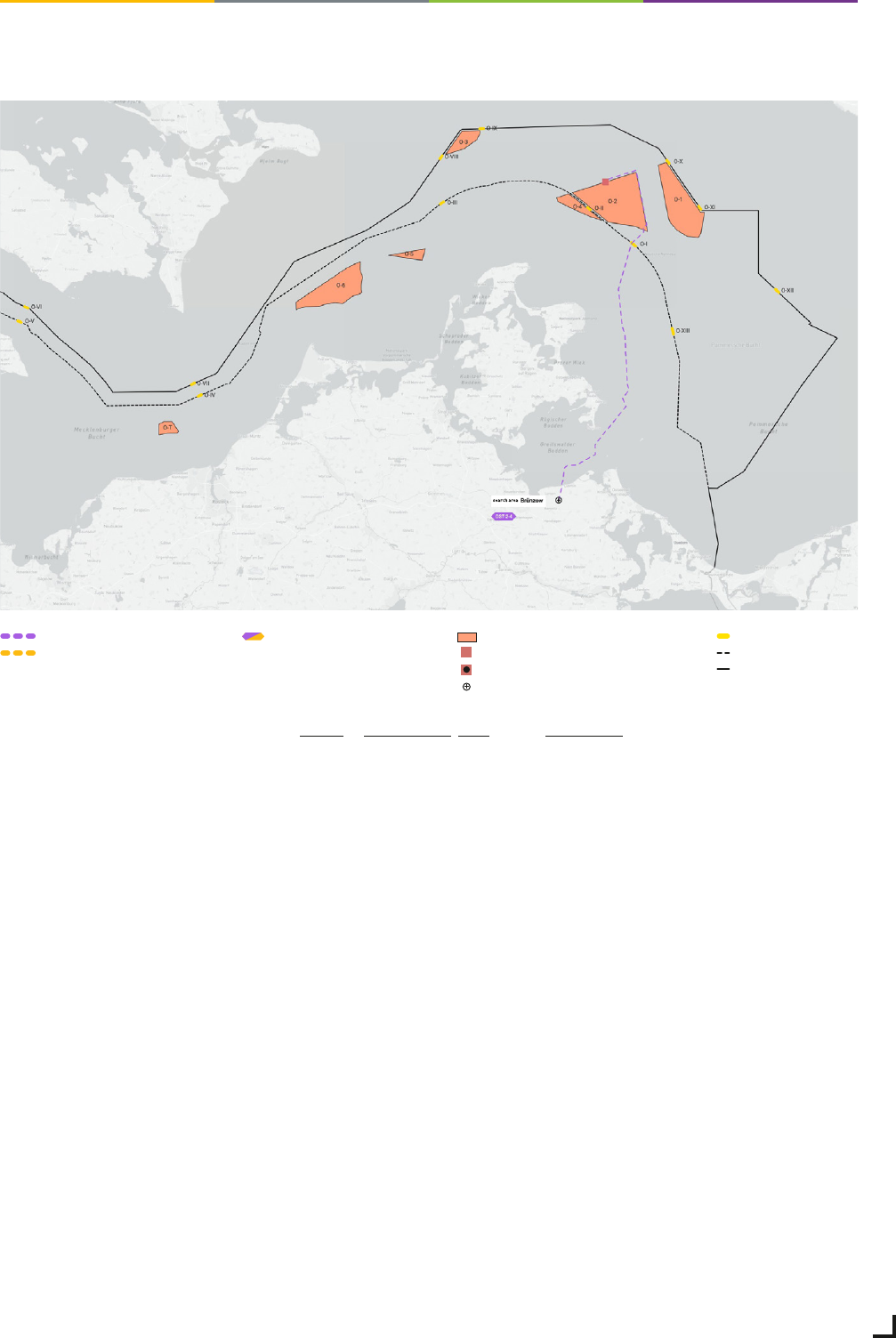

GDP compact

Measures of the Baltic Sea offshore expansion grid in scenarios A / B / C 2037

Source: Transmission system operator / map basis © Mapbox, © OpenStreetMap (ODbL), BSH (© GeoSeaPortal)

DC grid expansion

AC grid expansion

Boundary of the territorial sea

Boundary of the exclusive

economic zone

Border corridor

Converter platform

Transformer platform

Grid link point

Offshore wind farm areaProject name

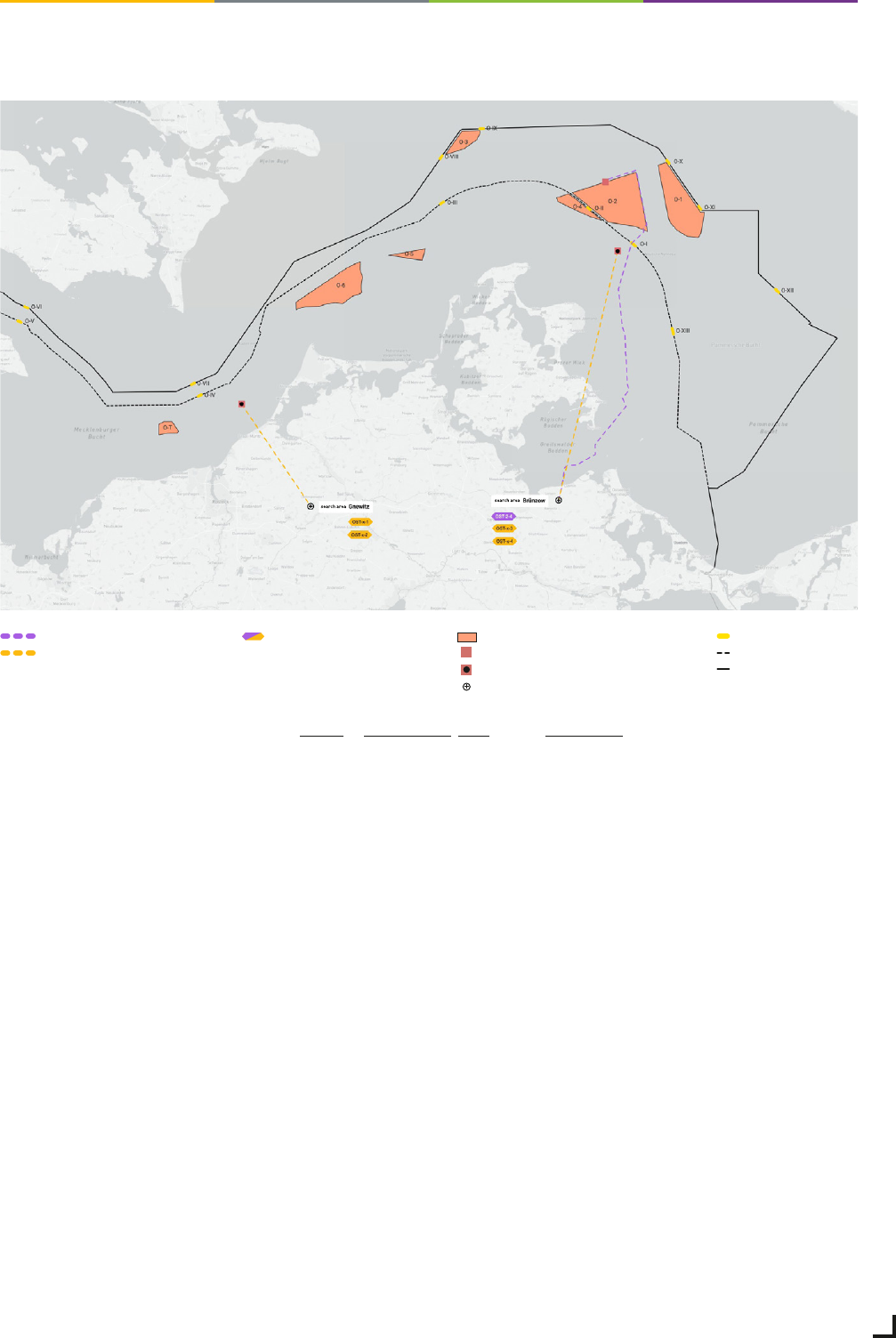

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 25

GDP compact

Measures of the Baltic Sea offshore expansion grid in scenarios A / B / C 2045

Source: Transmission system operator / map basis © Mapbox, © OpenStreetMap (ODbL), BSH (© GeoSeaPortal)

DC grid expansion

AC grid expansion

Boundary of the territorial sea

Boundary of the exclusive

economic zone

Border corridor

Converter platform

Transformer platform

Grid link point

Offshore wind farm areaProject name

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 27

GDP compact

Onshore grid: Considerable need

for expansion of a carbon-neutral

network by 2037

The statutory plans already foresee the majority of the

necessary expansion of renewable energy by the mid-

2030s. As a result of the substantial increase in domestic

German transport demand to around 87.7 GW by 2037,

a significant part of the onshore climate neutrality grid

needs also be implemented by then. Until 2045, the load

flow from northern to southern Germany almost remains

at a similar level. The further expansion of renewable

energy between 2037 and 2045 can be largely offset by

the expansion of flexibilities, especially electrolysers,

centralised and decentralised battery storage as well as

demand side management. Due to the massive expansion

of photovoltaic, significant load flows in opposite direction

will also occur for the first time. While they partly require

additional regional measures, the long-range transport

can be fulfilled by the transmission grid, which has so far

primarily been expanded for transport from northern to

sourthern Germany.

The transmission grid must be reconstructed in such a way

that it can already integrate an installed capacity of between

565 and 576 GW of renewable energy by 2037. Compared

to today, it must also cover almost double the gross power

consumption of around 900 to 1,050 TWh.

The result shows:

All the projects of the Federal Demand Plan 2022

are necessary for scenarios A / B / C 2037 as well as

all scenarios with the target year 2045. The neces-

sity of these measures is thus confirmed in the GDP

2037 / 2045 (2023). However, in light of the increasing

transport task, they are far from sufficient for a de-

mand-based grid.

Compared to the confirmed grid from the GDP 2035

(2021), the need for grid enhancement and expansion

in GDP 2037 / 2045 (2023) increases by about 7,400 km

of additional measures in the A / B / C 2037 and A / B / C

2045 scenarios (see Chapter 5.2.5).

Of these measures, approx. 2,800 km are accounted

for by new DC construction and enhancement mea-

sures (five additional DC projects), 1,300 km for new

AC construction measures (approx. 20 additional AC

projects) and 3,300 km for grid enhancement mea-

sures. The ratio of DC to AC new construction is 1.6.

The onshore initial grid comprises AC and DC mea-

sures totalling around 6,950 km with estimated in-

vestment costs of EUR 50 billion. For the onshore

grid expansion, grid enhancements in the AC seg-

ment amount to 6,125 km. Furthermore, there are

about 180 km of DC enhancement measures. An-

other 1,714 km are accounted for new AC construc-

tion measures and 4,396 km for new DC construction

measures. In total, the onshore expansion grid for all

scenarios considers a total lentgh of about 12,413 km.

For scenarios A / B / C 2037, the investment costs

amount to around EUR 106.1 billion. The investment

costs for the onshore expansion grid of the A / B / C

2045 scenarios are EUR 0.1 billion higher. Compared

to the first draft of the GDP 2037 / 2045 (2023), the

investment costs have increased by approx. EUR 12.5

billion. This is mainly attributable to the consider-

ation of additional projects based on additional de-

mand for transformers and substations between the

distribution and transmission grid. Other contribut-

ing factors include an update of the scope and costs

of existing projects as well as the updated require-

ments for plants for reactive power compensation

and for the provision of instantaneous reserve.

Compared to the project portfolio proposed in

the GDP 2035 (2021), the present GDP 2037 / 2045

(2023) identifies new onshore projects with a route

length of 5,620 km and additional investments of

EUR 52.3 billion.

The results of the grid analyses show an identical

carbon-neutral grid for all scenarios. This grid only

differs in terms of the remaining redispatch demand.

The climate neutrality grid consists of a robust portfolio

of grid enhancement and expansion measures under

the proposed assumptions. The TSOs assume that these

measures are necessary in the sense of a ‘no-regret’

approach in the GDP 2037 / 2045 (2023) scenarios.

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 28

GDP compact

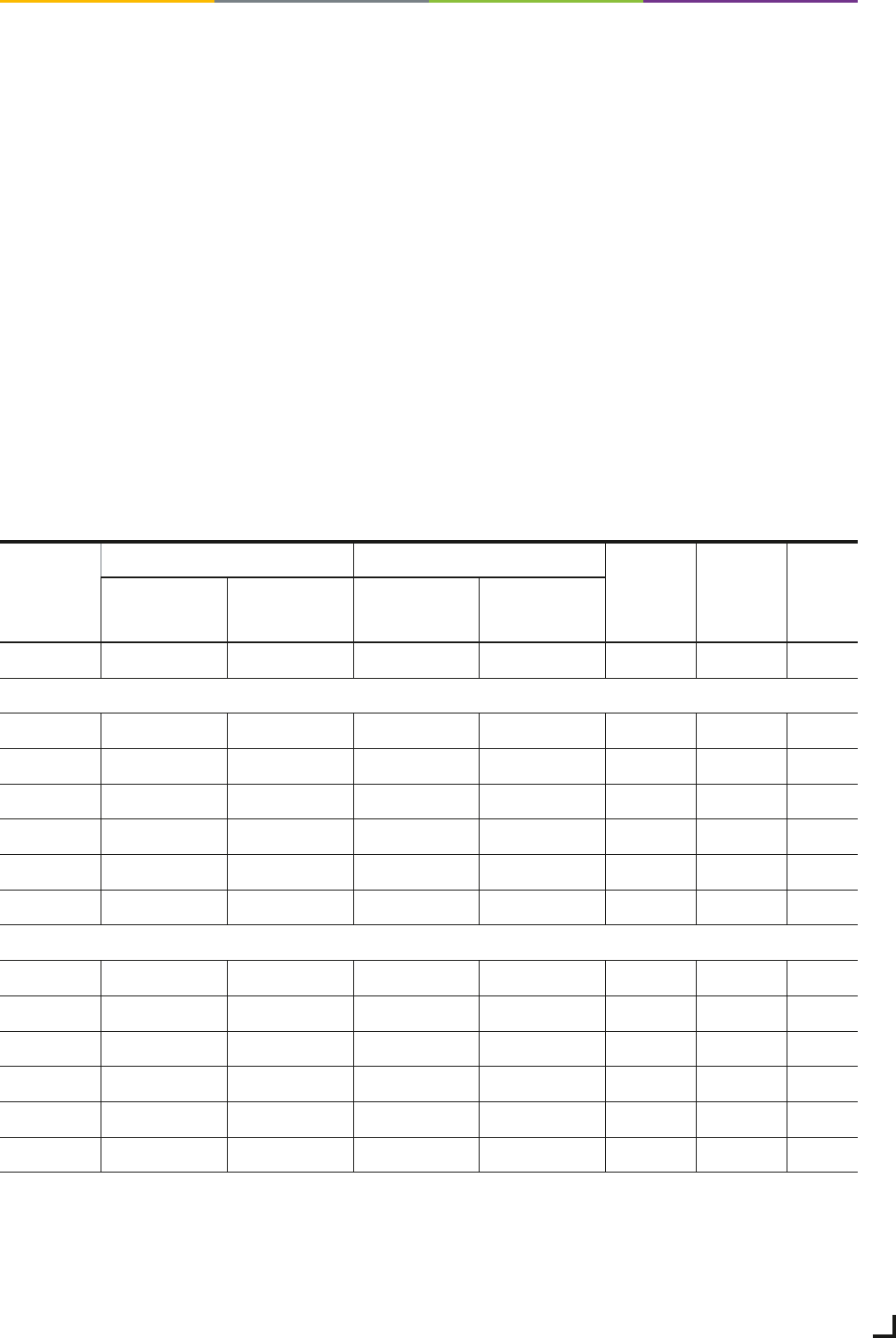

Lengths of initial and expansion grid in the GDP 2037 / 2045 (2023)

Figures

in km

AC enhancement DC enhancement

AC new

construction

DC new

construction

Total

Connection/

rewiring

Replacement/

parallel new

construction

Connection/

rewiring

Replacement/

parallel new

construction

Initial grid 919 2,081 321 560 599 2,466

6,945

Expansion grid

A 2037 2,279 3,846 0 179 1,714 4,396 12,413

B 2037 2,279 3,846 0 179 1,714 4,396 12,413

C 2037 2,279 3,846 0 179 1,714 4,396 12,413

A 2045 2,279 3,846 0 179 1,714 4,396 12,413

B 2045 2,279 3,846 0 179 1,714 4,396 12,413

C 2045 2,279 3,846 0 179 1,714 4,396 12,413

Initial and expansion grid

A 2037 3,198 5,927 321 739 2,312 6,861 19,358

B 2037 3,198 5,927 321 739 2,312 6,861 19,358

C 2037 3,198 5,927 321 739 2,312 6,861 19,358

A 2045 3,198 5,927 321 739 2,312 6,861 19,358

B 2045 3,198 5,927 321 739 2,312 6,861 19,358

C 2045 3,198 5,927 321 739 2,312 6,861 19,358

Due to the long timeframe until 2045 and the cor-

responding uncertainties, identified congestion was

not completely eliminated by grid enhancement and

expansion measures. Therefore, a redispatch volume

of 1.5 to 5.9 TWh remains in the scenarios. A further

reduction in congestion is conceivable by exploiting

the potential of future innovative technologies. Thus,

the curative redispatch potential for scenario B 2037

was explicitly investigated in this GDP.

To evaluate suitable grid topologies, the TSOs have refined

their simulation tools, for example by using heuristic tools.

It ensures more efficient and comprehensive investigation

of the potential solutions and facilitates the comparison

and evaluation of a large number of grid expansion com-

binations.

Considering a potentially significant increase in the ex-

pansion of renewable energy as early as 2030 and the

correspondingly increased short to medium-term load

on the transmission grid, the German transmission sys-

tem operators have identified additional suitable measures

(ad hoc measures) that can already be implemented in the

short to medium term to mitigate the expected situation.

These measures were assessed and identified based on

the scenario and grid model of the long-term analysis

according to § 34 of the Coal-fired Power Generation

Termination Act (KVBG) for the year 2030.

Source: Transmission system operators

Grid Development Plan Electricity 2037 / 2045, Version 2023, second draft 29

GDP compact

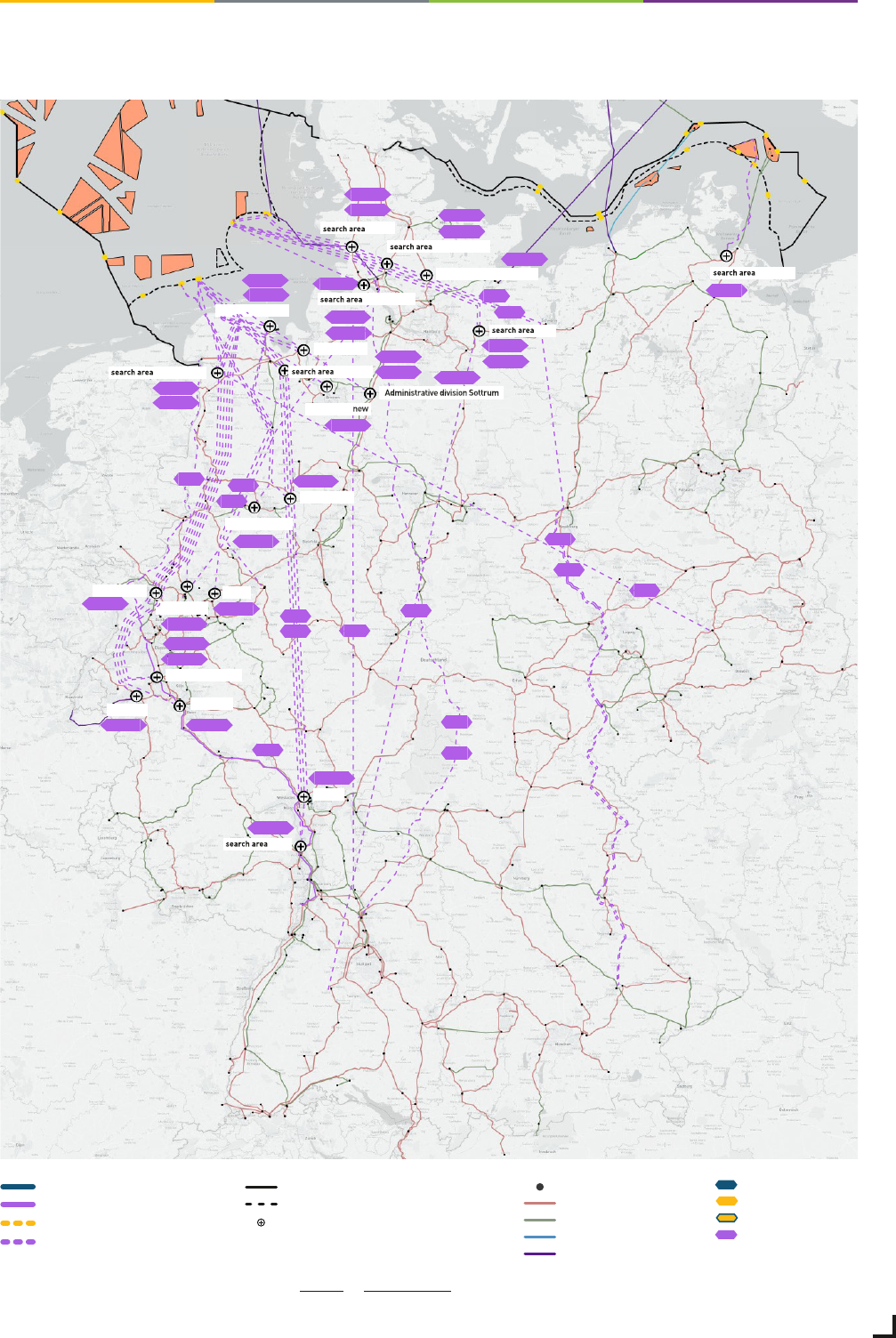

Potential bundling options of new onshore

DC projects and offshore grid connection systems

Regarding to § 12b (3a) of the EnWG (German Energy Act),

the TSOs are obligated for the first time to specify bundling

options for newly identified DC grid expansion measures

and the cross-border onshore part of the offshore connec-

tion lines. It needs to be shown how these measures can

be realised with existing or at least firmly planned routes,

either entirely or to a large extent in one power line corridor.

Bundling makes it possible to align offshore connection

systems and newly identified DC projects in the same