ELECTRONIC TRANSMISSION DISCLAIMER

STRICTLY NOT TO BE FORWARDED TO ANY OTHER PERSONS

IMPORTANT: You must read the following disclaimer before continuing. This electronic transmission applies to the

attached document and you are therefore advised to read this disclaimer carefully before reading, accessing or

making any other use of the attached combined prospectus and circular (the “Prospectus”) relating to Aston Martin

Lagonda Global Holdings plc (the “Company”) dated 27 February 2020 received by means of electronic

communication. In accessing or making any other use of the attached document, you agree to be bound by the

following terms and conditions, including any modifications to them from time to time, each time you receive any

information from us as a result of such access.

You acknowledge that this electronic transmission and the delivery of the attached document is confidential and intended

for you only and you agree you will not forward, reproduce, copy, download or publish this electronic transmission or the

attached document to any other person. The Prospectus has been prepared solely in connection with the proposed placing

of ordinary shares (the “Placing Shares”) in the Company to the Yew Tree Consortium (the “Placing”) and the rights issue

(the “Rights Issue” which taken together with the Placing shall comprise the “Capital Raise”) of ordinary shares (the “New

Shares”) of the Company and the proposed admission of the Placing Shares and the New Shares (nil paid and fully paid) to

the premium listing segment of the Official List of the UK Financial Conduct Authority (the “FCA”) and to trading on the

London Stock Exchange plc’s main market for listed securities (“Admission”).

This Prospectus comprises (i) a circular prepared in accordance with the Listing Rules of the FCA made under section 73A of

the Financial Services and Markets Act 2000 (“FSMA”) and (ii) a prospectus relating to the Company prepared in

accordance with the Prospectus Regulation Rules of the FCA made under section 73A of the FSMA. This Prospectus has

been approved by the FCA (as competent authority under Regulation (EU) 2017/1129) (the “Prospectus Regulation”) in

accordance with section 85 of the FSMA. The FCA only approves this document as meeting the standards of completeness,

comprehensibility and consistency imposed by the Prospectus Regulation, and such approval should not be considered as

an endorsement of the issuer that is, or the quality of the securities that are, the subject of this document. Investors should

make their own assessment as to the suitability of investing in the New Shares.

This Prospectus has been filed with the FCA in accordance with the Prospectus Regulation Rules and will be made

available to the public in accordance with Prospectus Regulation Rule 3.2 by the same being made available, free of

charge, at www.astonmartinlagonda.com/investors and at the Company’s registered office at Banbury Road, Gaydon,

Warwick CV35 0DB, United Kingdom.

THIS ELECTRONIC TRANSMISSION AND THE ATTACHED DOCUMENT MAY ONLY BE DISTRIBUTED, OUTSIDE THE UNITED

STATES, IN “OFFSHORE TRANSACTIONS” IN ACCORDANCE WITH RULE 904 OF REGULATION S UNDER THE U.S. SECURITIES

ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”) OR, WITHIN THE UNITED STATES, TO CERTAIN PERSONS

REASONABLY BELIEVED TO BE QUALIFIED INSTITUTIONAL BUYERS (“QIBs”) AS DEFINED IN RULE 144A UNDER THE

SECURITIES ACT (“RULE 144A”) OR TO OTHER PERSONS, IN OFFERINGS EXEMPT FROM OR IN A TRANSACTION NOT

SUBJECT TO THE REGISTRATION REQUIREMENTS UNDER THE SECURITIES ACT, AND, IN EACH CASE, IN COMPLIANCE WITH

ANY APPLICABLE SECURITIES LAWS OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES. ANY FORWARDING,

DISTRIBUTION OR REPRODUCTION OF THE ATTACHED DOCUMENT IN WHOLE OR IN PART IS UNAUTHORISED. FAILURE TO

COMPLY WITH THIS NOTICE MAY RESULT IN A VIOLATION OF THE SECURITIES ACT OR THE APPLICABLE LAWS OF OTHER

JURISDICTIONS. NOTHING IN THIS ELECTRONIC TRANSMISSION AND THE ATTACHED DOCUMENT CONSTITUTES AN OFFER

OF SECURITIES FOR SALE IN ANY JURISDICTION WHERE IT IS UNLAWFUL TO DO SO.

THE NIL PAID RIGHTS, THE FULLY PAID RIGHTS, THE NEW SHARES, THE PROVISIONAL ALLOTMENT LETTERS AND THE

PLACING SHARES HAVE NOT BEEN AND WILL NOT BE REGISTERED UNDER THE SECURITIES ACT OR UNDER ANY

SECURITIES LAWS OF ANY STATE OR OTHER JURISDICTION OF THE UNITED STATES AND MAY NOT BE OFFERED, SOLD,

PLEDGED, TAKEN UP, EXERCISED, RESOLD, RENOUNCED, TRANSFERRED OR DELIVERED, DIRECTLY OR INDIRECTLY, EXCEPT

(1) WITHIN THE UNITED STATES TO A PERSON THAT THE HOLDER AND ANY PERSON ACTING ON ITS BEHALF REASONABLY

BELIEVES IS A QIB IN ACCORDANCE WITH RULE 144A, OR TO OTHER PERSONS PURSUANT TO AN APPLICABLE EXEMPTION

FROM OR IN A TRANSACTION NOT SUBJECT TO THE REGISTRATION REQUIREMENTS OF THE SECURITIES ACT, OR

(2) OUTSIDE THE UNITED STATES, IN AN OFFSHORE TRANSACTION IN RELIANCE ON REGULATION S UNDER THE SECURITIES

ACT, IN EACH CASE IN COMPLIANCE WITH ANY APPLICABLE SECURITIES LAWS OF ANY STATE OR OTHER JURISDICTION OF

THE UNITED STATES. THERE WILL BE NO PUBLIC OFFER OF THE NIL PAID RIGHTS, THE FULLY PAID RIGHTS, THE NEW

SHARES OR THE PLACING SHARES IN THE UNITED STATES. SUBJECT TO CERTAIN LIMITED EXCEPTIONS, PROVISIONAL

ALLOTMENT LETTERS HAVE NOT BEEN, AND WILL NOT BE, SENT TO, AND NIL PAID RIGHTS HAVE NOT BEEN AND WILL

NOT BE CREDITED TO THE CREST ACCOUNT OF, ANY QUALIFYING SHAREHOLDER WITH A REGISTERED ADDRESS IN OR

THAT IS LOCATED IN THE UNITED STATES.

The distribution of this document or the provisional allotment letters and the transfer of Nil Paid Rights, Fully Paid Rights,

New Shares or Placing Shares into jurisdictions other than the United Kingdom may be restricted by law and therefore

persons into whose possession this document comes should inform themselves about and observe any such restrictions.

Any failure to comply with any such restrictions may constitute a violation of the securities laws or regulations of such

jurisdictions. In particular, subject to certain exceptions, this document, the enclosures and any other such documents

should not be distributed, forwarded to or transmitted in, and the provisional allotment letters, the Nil Paid Rights, the

Fully Paid Rights, the New Shares and the Placing Shares may not be transferred or sold to, or renounced or delivered in or

into the United States, Australia, Canada, Japan, the People’s Republic of China and the Republic of South Africa or any

other jurisdictions where the extension and availability of the Capital Raise would breach any applicable law. No offer of

New Shares is being made by virtue of this document of the provisional allotment letters into the United States, Australia,

Canada, Japan, the People’s Republic of China and the Republic of South Africa.

This electronic transmission and the attached document and the Capital Raise when made are only addressed to and

directed at persons in member states of the European Economic Area, other than the United Kingdom, who are

“qualified investors” within the meaning of Article 2(e) of the Prospectus Regulation (“Qualified Investors”). This

electronic transmission and the attached document must not be acted on or relied on in any member state of the

European Economic Area other than the United Kingdom, by persons who are not Qualified Investors. Any investment

or investment activity to which this document relates is available only, in any member state of the European Economic

Area other than the United Kingdom, to Qualified Investors, and will be engaged in only with such persons.

The making or acceptance of the proposed offer of Nil Paid Rights, Fully Paid Rights and New Shares to persons who

have registered addresses outside the United Kingdom, or who are resident in, or citizens of, countries other than

the United Kingdom may be affected by the laws of the relevant jurisdiction. Those persons should consult their

professional advisers as to whether they require any governmental or other consents or need to observe any other

formalities to enable them to participate in the Capital Raise.

It is also the responsibility of any person (including, without limitation, custodians, nominees and trustees) outside the

UK wishing to take up rights under or otherwise participate in the Rights Issue to satisfy himself, herself or itself as to

the full observance of the laws of any relevant territory in connection therewith, including the obtaining of any

governmental or other consents which may be required, the compliance with other necessary formalities and the

payment of any issue, transfer or other taxes due in such territories.

Confirmation of Your Representation: This electronic transmission and the attached document is delivered to you on

the basis that you are deemed to have represented to the Company and Morgan Stanley & Co. International plc, J.P.

Morgan Securities plc (which conducts its UK investment banking activities under the marketing name J.P. Morgan

Cazenove) and Deutsche Bank AG, London Branch (together, the “Banks”) that (i) you are (a), if located within the

United States, a QIB, in according with Rule 144A under the Securities Act, acquiring such securities for its own account

or for the account of another QIB, or are a person who the Company has otherwise specifically permitted to access the

attached document or (b), if located outside the United States, acquiring such securities in “offshore transactions”, in

accordance with Rule 904 of Regulation S under the Securities Act; (ii) if you are in the United Kingdom, you are a

relevant person and/or a relevant person who is acting on behalf of relevant persons in the United Kingdom and/or

Qualified Investors to the extent you are acting on behalf of persons or entities in the EEA other than the United

Kingdom; (iii) if you are in any member state of the European Economic Area other than the United Kingdom, you are

a Qualified Investor and/or a Qualified Investor acting on behalf of Qualified Investors to the extent you are acting on

behalf of persons or entities in the EEA other than the United Kingdom; (iv) you are an institutional investor that is

eligible to receive this document and you consent to delivery by electronic transmission and (v) you are not located in

Australia, Canada, Japan, the People’s Republic of China and the Republic of South Africa.

You are reminded that you have received this electronic transmission and the attached document on the basis that you

are a person into whose possession this document may be lawfully delivered in accordance with the laws of the

jurisdiction in which you are located and you may not nor are you authorised to deliver this document, electronically or

otherwise, to any other person. This document has been made available to you in an electronic form. You are reminded

that documents transmitted via this medium may be altered or changed during the process of electronic transmission

and consequently neither the Company, the Banks nor any of their respective affiliates, directors, officers, employees or

agents accepts any liability or responsibility whatsoever in respect of any difference between the document distributed

to you in electronic format and the hard copy version. By accessing the attached document, you consent to receiving it

in electronic form. Apart from the responsibilities and liabilities, if any, which may be imposed on the Banks by the

FSMA or the regulatory regime established thereunder, or under the regulatory regime of any jurisdiction where

exclusion of liability under the relevant regulatory regime would be illegal, void or unenforceable, none of the Banks,

nor any of their respective affiliates, directors, officers, employees or advisers accepts any responsibility or liability

whatsoever for the contents of the attached document, including its accuracy, completeness or verification and makes

no representation or warranty, express or implied, as to the contents of this document or for any statement made or

purported to be made by it, or on its behalf, in connection with the Company or the Nil Paid Rights, the Fully Paid

Rights, the New Shares or the Placing Shares. The Banks and each of their respective affiliates, each accordingly

disclaims to the fullest extent permitted by law all and any liability whether arising in tort, contract or otherwise which

they might otherwise have in respect of such document or any such statement. No representation or warranty express

or implied, is made by any of the Banks or any of their respective affiliates as to the accuracy, completeness or

sufficiency of the information set out in the attached document.

Restriction: Nothing in this electronic transmission constitutes, and may not be used in connection with, an offer of

securities for sale to persons other than the specified categories of institutional buyers described above and to whom

it is directed and access has been limited so that it shall not constitute a general solicitation. If you have gained access

to this transmission contrary to the foregoing restrictions, you will be unable to purchase any of the securities

described therein.

The Banks are acting exclusively for the Company and are acting for no one else in connection with the Capital Raise.

They will not regard any other person (whether or not a recipient of this document) as their client in relation to the

Capital Raise and will not be responsible to anyone other than the Company for providing the protections afforded to

their respective clients nor for giving advice in relation to the Capital Raise or any transaction or arrangement

referred to in this document.

You are responsible for protecting against viruses and other destructive items. Your receipt of this document via

electronic transmission is at your own risk and it is your responsibility to take precautions to ensure that it is free from

viruses and other items of a destructive nature.

THIS DOCUMENT AND ANY ACCOMPANYING DOCUMENTS ARE IMPORTANT AND REQUIRE YOUR IMMEDIATE

ATTENTION. If you are in any doubt as to what action you should take, you are recommended to seek immediately your

own financial advice from your stockbroker, bank manager, solicitor, accountant, fund manager or other appropriate

independent financial adviser, who is authorised under the Financial Services and Markets Act 2000 if you are resident in

the United Kingdom or, if not, from another appropriately authorised independent financial adviser.

This document comprises (i) a circular prepared in accordance with the Listing Rules of the FCA made under section 73A of

the FSMA and (ii) a prospectus relating to Aston Martin Lagonda Global Holdings plc prepared in accordance with the

Prospectus Regulation Rules of the FCA made under section 73A of the FSMA. This document has been approved by the

FCA (as competent authority under Regulation (EU) 2017/1129) in accordance with section 85 of the FSMA. The FCA only

approves this document as meeting the standards of completeness, comprehensibility and consistency imposed by

Regulation (EU) 2017/1129, and such approval should not be considered as an endorsement of the issuer that is, or the

quality of the securities that are, the subject of this document. Investors should make their own assessment as to the

suitability of investing in the Shares.

This document has been filed with the FCA in accordance with the Prospectus Regulation Rules and will be made available

to the public in accordance with Prospectus Regulation Rule 3.2 by the same being made available, free of charge, at

www.astonmartinlagonda.com/investors and at the Company’s registered office at Banbury Road, Gaydon, Warwick CV35

0DB, United Kingdom.

If you sell or have sold or have otherwise transferred all of your Shares (other than ex-rights) held in certificated form

before 8.00 a.m. (London time) on 18 March 2020 (the Ex-Rights Date) please send this document, together with any

Provisional Allotment Letter, if and when received, at once to the purchaser or transferee or to the bank, stockbroker or

other agent through whom the sale or transfer was effected for delivery to the purchaser or transferee except that such

documents should not be sent to any jurisdiction where to do so might constitute a violation of local securities laws or

regulations, including but not limited to the United States or Australia, Canada, Japan, the People’s Republic of China and

the Republic of South Africa (the Excluded Territories). If you sell or have sold or have otherwise transferred all or some of

your Existing Shares (other than ex-rights) held in uncertificated form before the Ex-Rights Date, a claim transaction will

automatically be generated by Euroclear which, on settlement, will transfer the appropriate number of Nil Paid Rights to

the purchaser or transferee. If you sell or have sold or otherwise transferred only part of your holding of Existing Shares

(other than ex-rights) held in certificated form before the Ex-Rights Date, you should refer to the instruction regarding

split applications in Part III - Terms and Conditions of the Rights Issue of this document and in the Provisional Allotment

Letter.

The directors of the Company (the Directors), whose names appear on page 47 of this document, Lawrence Stroll (the

Proposed Director) and the Company accept responsibility for the information contained in this document. To the best of

the knowledge of the Directors and the Company, the information contained in this document is in accordance with the

facts and this document contains no omission likely to affect its import.

The distribution of this document, the Provisional Allotment Letter and the transfer of Nil Paid Rights, Fully Paid Rights

and New Shares into jurisdictions other than the United Kingdom may be restricted by law and therefore persons into

whose possession this document comes should inform themselves about and observe any such restrictions. Any failure

to comply with any such restrictions may constitute a violation of the securities laws or regulations of such jurisdictions.

In particular, subject to certain exceptions, this document, the enclosures and the Provisional Allotment Letter and any

other such documents should not be distributed, forwarded to or transmitted in or into the United States, any of the

Excluded Territories or any other jurisdictions where the extension and availability of the Rights Issue would breach any

applicable law.

Aston Martin Lagonda Global Holdings plc

(incorporated in England and Wales under the Companies Act 2006 with registered number 11488166)

Proposed Placing of 45,600,577 Placing Shares at

400 pence per Placing Share to the Yew Tree Consortium

Proposed 14 for 25 Rights Issue of 153,217,942 New Shares at

207 pence per New Share

Notice of General Meeting

Sole Financial Adviser, Sponsor, Joint Global Co-ordinator and Joint Bookrunner

Morgan Stanley

Joint Global Co-ordinators and Joint Bookrunners

Deutsche Bank J.P. Morgan Cazenove

A Notice of General Meeting of the Company, to be held at 10.00 a.m. on 16 March 2020 at

Freshfields Bruckhaus Deringer LLP, 65 Fleet Street, London EC4Y 1HT, United Kingdom, is set out

at the end of this document. Whether or not you intend to be present at the General Meeting, if

you hold your shares directly you are asked to complete and return the enclosed Form of Proxy in

accordance with the instructions printed on it as soon as possible and, in any event, so as to be

received by the Registrar, Equiniti Limited (Equiniti) at Corporate Actions, Aspect House, Spencer

Road, Lancing, West Sussex, BN99 6DA, United Kingdom, by not later than 10.00 a.m. on

12 March 2020 (or, in the case of an adjournment, not later than 48 hours before the time fixed

for the holding of the adjourned meeting) and in the case of AML Nominee Service Shareholders

the enclosed Voting Instruction Form so as to be received by the Registrar, Equiniti at Corporate

Actions, Aspect House, Spencer Road, Lancing, West Sussex, BN99 6DA, United Kingdom, by not

later than 10.00 a.m. on 11 March 2020.

As an alternative to completing and returning the printed Form of Proxy, Shareholders can also

submit their proxy electronically by accessing the Registrar’s website at www.sharevote.co.uk. To

be valid, the electronic submission must be registered by not later than 10.00 a.m. on 12 March

2020 (or, in the case of an adjournment, not later than 48 hours before the time fixed for the

holding of the adjourned meeting). CREST members may also choose to utilise the CREST

electronic proxy appointment service in accordance with the procedures set out in the Notice of

General Meeting at the end of this document, as soon as possible and in any event no later than

10.00 a.m. on 12 March 2020 (or, in the case of an adjournment, not later than 48 hours before

the time fixed for the holding of the adjourned meeting).

Completion and return of a Form of Proxy (or the electronic appointment of a proxy) will not

preclude you from attending and voting in person at the General Meeting, should you so wish.

The Shares are listed on the premium listing segment of the Official List maintained by the FCA

and traded on the main market for listed securities of London Stock Exchange plc (the London

Stock Exchange). Application will be made to the FCA and to the London Stock Exchange for the

New Shares and the Placing Shares to be admitted to the premium listing segment of the Official

List of the FCA and to trading on the main market for listed securities of the London Stock

Exchange. It is expected that Admission of the New Shares (nil paid) will become effective and

that dealings on the London Stock Exchange in the New Shares (nil paid) will commence at 8.00

a.m. on 18 March 2020 and that Admission of the Placing Shares will become effective and that

dealings on the London Stock Exchange in the Placing Shares will commence at 8.00 a.m. on

17 March 2020.

Your attention is drawn to the letter of recommendation from the Chair which is set out in Part

I - Letter from the Chair of Aston Martin Lagonda Global Holdings plc. Your attention is also

drawn to the section headed “Risk Factors” at the beginning of this document which sets out

certain risks and other factors that should be considered by Shareholders when deciding on

what action to take in relation to the Rights Issue and the Placing (together, the Capital Raise),

and by others when deciding whether or not to purchase Nil Paid Rights, Fully Paid Rights or

New Shares.

Each of Morgan Stanley & Co. International plc (Morgan Stanley) and J.P. Morgan Securities plc

(which conducts its UK investment banking activities under the marketing name J.P. Morgan

Cazenove) (J.P. Morgan Cazenove) is authorised in the United Kingdom by the Prudential

Regulation Authority (PRA) and regulated in the United Kingdom by the FCA and the PRA.

Deutsche Bank AG, London Branch (Deutsche Bank, together with Morgan Stanley and J.P.

Morgan Cazenove, the Underwriters), which is authorised under German Banking Law

(competent authority: European Central Bank) and, in the United Kingdom, by the PRA, is subject

to supervision by the European Central Bank and by BaFin, Germany’s Federal Financial

Supervisory Authority, and is subject to limited regulation in the United Kingdom by the PRA and

the FCA. The Underwriters are acting exclusively for the Company and are acting for no one else

in connection with the Capital Raise and will not regard any other person as a client in relation

to the Capital Raise and will not be responsible to anyone other than the Company for providing

the protections afforded to their respective clients, nor for providing advice in connection with

the Capital Raise or any other matter, transaction or arrangement referred to in this document.

i

The Underwriters have given and not withdrawn their consent to the issue of this document with

the inclusion of the references to their respective names in the form and context in which they

are included.

Apart from the responsibilities and liabilities, if any, which may be imposed on the Underwriters

by the FSMA or the regulatory regime established thereunder, or under the regulatory regime of

any jurisdiction where exclusion of liability under the relevant regulatory regime would be

illegal, void or unenforceable, none of the Underwriters, nor any of their respective affiliates,

directors, officers, employees or advisers, accepts any responsibility whatsoever for, or makes any

representation or warranty, express or implied, as to the contents of this document, including its

accuracy, completeness or verification, or for any other statement made or purported to be made

by it, or on its behalf, in connection with the Company, the Nil Paid Rights, the Fully Paid Rights,

the New Shares, the Placing Shares, the Rights Issue or the Placing. The Underwriters and their

respective affiliates, directors, officers, employees and advisers accordingly disclaim to the fullest

extent permitted by law any and all liability whatsoever, whether arising in tort, contract or

otherwise, which they might otherwise have in respect of this document or any such statement.

The contents of this Prospectus are not to be construed as legal, business or tax advice. Each

prospective investor should consult their own legal, financial or tax adviser in connection with

the purchase of the New Shares. In making an investment decision, each investor must rely on

their own examination, analysis and enquiry of the Company and the terms of the Capital Raise,

including the merits and risks involved.

The investors also acknowledge that: (i) they have not relied on the Underwriters or any person

affiliated with the Underwriters in connection with any investigation of the accuracy of any

information contained in this document or their investment decision; and (ii) they have relied

only on the information contained in this document and that no person has been authorised to

give any information or to make any representation concerning the Company or its subsidiaries

or the Nil Paid Rights, the Fully Paid Rights, the New Shares or the Placing Shares (other than as

contained in this document) and, if given or made, any such other information or representation

should not be relied upon as having been authorised by the Company or the Underwriters.

Subject to, among other things, the passing of the Resolutions, it is expected that Provisional

Allotment Letters will be dispatched to Qualifying Non-CREST Shareholders and Forms of

Instruction will be dispatched to AML Nominee Service Shareholders (other than, subject to

certain exceptions, those with registered addresses in the United States or the Excluded

Territories) on 17 March 2020, and that Qualifying CREST Shareholders (other than, subject to

certain exceptions, those with registered addresses in the United States or the Excluded

Territories) will receive a credit to their appropriate stock accounts in CREST in respect of the Nil

Paid Rights to which they are entitled on 18 March 2020. The Nil Paid Rights so credited are

expected to be enabled for settlement by Euroclear as soon as practicable after Admission of the

New Shares (nil paid).

In connection with the Rights Issue, the Underwriters and any of their respective affiliates may, in

accordance with applicable legal and regulatory provisions, take up a portion of the Nil Paid

Rights, the Fully Paid Rights and the New Shares in the Rights Issue as a principal position and in

that capacity may retain, purchase, sell, offer to sell or otherwise deal for their own account in

securities of the Company and related or other securities and instruments (including Nil Paid

Rights, Fully Paid Rights and New Shares) and may offer or sell such securities otherwise than in

connection with the Rights Issue, provided that the Underwriters and their respective affiliates

may not engage in short selling for the purpose of hedging their commitments under the

Underwriting Agreement (subject to certain exceptions contained in the Underwriting

Agreement). Accordingly, references in this Prospectus to Nil Paid Rights, Fully Paid Rights and

New Shares being offered or placed should be read as including any offering or placement of Nil

Paid Rights, Fully Paid Rights and New Shares to any of the Underwriters or any of their

respective affiliates acting in such capacity. In addition, certain of the Underwriters or their

affiliates may enter into financing arrangements (including margin loans) with investors in

connection with which such Underwriters (or their affiliates) may from time to time acquire, hold

or dispose of Nil Paid Rights, Fully Paid Rights and New Shares. Except as required by applicable

law or regulation, the Underwriters do not propose to make any public disclosure in relation to

ii

such transactions. The latest time and date for acceptance and payment in full for the New

Shares by holders of the Nil Paid Rights is expected to be 11.00 a.m. on 1 April 2020. The

procedures for delivery of the Nil Paid Rights, acceptance and payment are set out in

Part III - Terms and Conditions of the Rights Issue and (other than, subject to certain exceptions,

those with registered addresses in the United States or the Excluded Territories), for Qualifying

Non-CREST Shareholders also in the Provisional Allotment Letter and, for Qualifying AML

Nominee Service Shareholders also in the Form of Instruction. Qualifying CREST Shareholders

should refer to paragraph 2.5 of Part III - Terms and Conditions of the Rights Issue.

The Underwriters may arrange for the offer of New Shares in the United States not taken up in

the Rights Issue only to persons reasonably believed to be “qualified institutional buyers” (QIBs)

within the meaning of Rule 144A under the United States Securities Act of 1933, as amended (the

Securities Act)(Rule 144A) in reliance on an exemption from, or in a transaction not subject to,

the registration requirements of the Securities Act. The New Shares, the Nil Paid Rights and the

Fully Paid Rights offered outside the United States are being offered in reliance on Regulation S

under the Securities Act (Regulation S). Prospective investors are hereby notified that sellers of

the Nil Paid Rights, the Fully Paid Rights or the New Shares may be relying on the exemption

from registration provisions under Section 5 of the Securities Act, provided by Rule 144A

thereunder.

In addition, until 40 days after the commencement of the Rights Issue, an offer, sale or transfer

of the Nil Paid Rights, the Fully Paid Rights, the Provisional Allotment Letters, the New Shares or

the Placing Shares within the United States by a dealer (whether or not participating in the

Rights Issue) may violate the registration requirements of the Securities Act.

All Shareholders and any person (including, without limitation, a nominee or trustee) who has a

contractual or legal obligation to forward this document or any Provisional Allotment Letter, if

and when received, or other document to a jurisdiction outside the United Kingdom should read

the information set out in paragraph 2.5 of Part III - Terms and Conditions of the Rights Issue.

Notice to Overseas Shareholders

This document does not constitute an offer of Nil Paid Rights, Fully Paid Rights, New Shares or

Placing Shares to any person with a registered address, or who is located, in the United States or

the Excluded Territories or in any other jurisdiction in which such an offer or solicitation is

unlawful. The Nil Paid Rights, the Fully Paid Rights, the New Shares, the Placing Shares and the

Provisional Allotment Letters have not been and will not be registered or qualified for

distribution to the public under the relevant laws of any state, province or territory of the United

States or any Excluded Territory and may not be offered, sold, taken up, exercised, resold,

renounced, transferred or delivered, directly or indirectly, within the United States or any

Excluded Territory or in any other jurisdictions where the extension and availability of the Rights

Issue would breach any applicable law, except pursuant to an applicable exemption. See “Notice

to Investors in the United States of America” in the section titled “Important Information”.

The Nil Paid Rights, the Fully Paid Rights and the New Shares have not been and will not be

registered under the Securities Act or under any securities laws of any state or other jurisdiction

of the United States and may not be offered, sold, taken up, exercised, resold, renounced,

transferred or delivered, directly or indirectly, within the United States except pursuant to an

applicable exemption from or in a transaction not subject to the registration requirements of the

Securities Act and in compliance with any applicable securities laws of any state or other

jurisdiction of the United States. There will be no public offer of the Nil Paid Rights, the Fully

Paid Rights, the New Shares or the Placing Shares in the United States.

The Nil Paid Rights, the Fully Paid Rights, the New Shares, the Placing Shares and the Provisional

Allotment Letters have not been approved or disapproved by the United States Securities and

Exchange Commission, any state’s securities commission in the United States or any US

regulatory authority, nor have any of the foregoing authorities passed upon or endorsed the

merits of the offering of the Nil Paid Rights, the Fully Paid Rights, the New Shares or the Placing

Shares or the accuracy or adequacy of this document. Any representation to the contrary is a

criminal offence.

iii

The Nil Paid Rights, the Fully Paid Rights, the Provisional Allotment Letters, the New Shares and

the Placing Shares have not been and will not be registered or qualified for distribution to the

public under the securities laws of any Excluded Territory and may not be offered, sold, taken up,

exercised, resold, renounced, transferred or delivered, directly or indirectly, within any Excluded

Territory or in any other jurisdictions where the extension and availability of the Rights Issue

would breach any applicable law, except pursuant to an applicable exemption from, and in

compliance with, any applicable securities laws. There will be no public offer in any of the

Excluded Territories or in any other jurisdictions where the extension and availability of the

Rights Issue would breach any applicable law.

The Nil Paid Rights, Fully Paid Rights and New Shares may not be offered or sold in Hong Kong,

by means of any document, other than (i) to “professional investors” as defined in the Securities

and Futures Ordinance (Cap.571, Laws of Hong Kong) of Hong Kong (the SFO) and any rules

made under the SFO; or (ii) in other circumstances which do not constitute an offer to the public

within the meaning of the Companies (Winding up and Miscellaneous Provisions) Ordinance

(Cap.32, Laws of Hong Kong) of Hong Kong (the C(WUMP)O) or an invitation to induce an offer

by the public to subscribe for or purchase any shares and which do not result in this document or

the Provisional Allotment Letter being a “prospectus” as defined in the C(WUMP)O. No

advertisement, invitation or document relating to the Nil Paid Rights, Fully Paid Rights, New

Shares, the Provisional Allotment Letters or this document may be issued or may be in the

possession of any person for the purpose of issue, whether in Hong Kong or elsewhere, which is

directed at, or the contents of which are likely to be accessed or read by, the public of Hong

Kong (except if permitted to do so under the C(WUMP)O and the SFO) other than with respect to

the Nil Paid Rights, Fully Paid Rights and New Shares which are or are intended to be disposed of

only to persons outside Hong Kong or only to “professional investors” as defined in the SFO and

any rules made under the SFO or in other circumstances which do not constitute an offer or

invitation to the public within the meaning of the C(WUMP)O. The contents of this document

and the Provisional Allotment Letter have not been reviewed by any regulatory authority in

Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt

about any of the contents of this document or the Provisional Allotment Letter, you should

obtain independent professional advice.

This document is being communicated in or from Switzerland to a small number of selected

Shareholders only. Each copy of this document and/or the Provisional Allotment Letters is

addressed to a specifically named recipient and may not be copied, reproduced, distributed or

passed on to others without the Company’s prior written consent. The Nil Paid Rights, the Fully

Paid Rights and the New Shares may not be publicly offered, sold or advertised, directly or

indirectly, in or from Switzerland and will not be listed on the SIX Swiss Exchange (SIX) or on any

other stock exchange or regulated trading facility in Switzerland. This document has been

prepared without regard to the disclosure standards for issuance prospectuses under art. 652a or

art. 1156 of the Swiss Code of Obligations or the disclosure standards for listing prospectuses

under art. 27 ff. of the SIX Listing Rules or the listing rules of any other stock exchange or

regulated trading facility in Switzerland. Neither this document nor any other offering or

marketing material relating to the Nil Paid Rights, the Fully Paid Rights and the New Shares or

the offering may be publicly distributed or otherwise made publicly available in Switzerland.

Neither this document nor any other offering or marketing material relating to the Capital Raise,

the Company, the Nil Paid Rights, the Fully Paid Rights and the New Shares have been or will be

filed with or approved by any Swiss regulatory authority. In particular, this document will not be

filed with, and the offer of Nil Paid Rights, the Fully Paid Rights and the New Shares will not be

supervised by, the Swiss Financial Market Supervisory Authority FINMA.

Notice to all investors

Any reproduction or distribution of this document, in whole or in part, and any disclosure of its

contents or use of any information contained in this document for any purpose other than

considering an investment in the Nil Paid Rights, the Fully Paid Rights or the New Shares is

prohibited. By accepting delivery of this document, each offeree of the Nil Paid Rights, the Fully

Paid Rights and/or the New Shares agrees to the foregoing.

iv

The distribution of this document and/or the Provisional Allotment Letters and/or the transfer of

the Nil Paid Rights, the Fully Paid Rights and/or the New Shares into jurisdictions other than the

United Kingdom may be restricted by law. Persons into whose possession these documents come

should inform themselves about and observe any such restrictions. Any failure to comply with

these restrictions may constitute a violation of the securities laws of any such jurisdiction. In

particular, such documents should not be distributed, forwarded to or transmitted in or into the

United States, any of the Excluded Territories or in any other jurisdictions where the extension

and availability of the Rights Issue would breach any applicable law. The Nil Paid Rights, the Fully

Paid Rights, the New Shares and the Provisional Allotment Letters are not transferable, except in

accordance with, and the distribution of this document is subject to, the restrictions set out in

paragraph 2.5 of Part III - Terms and Conditions of the Rights Issue. No action has been taken by

the Company or by the Underwriters that would permit an offer of the New Shares or rights

thereto or possession or distribution of this document or any other offering or publicity material

or the Provisional Allotment Letters, the Nil Paid Rights, or the Fully Paid Rights in any

jurisdiction where action for that purpose is required, other than in the United Kingdom.

No person has been authorised to give any information or make any representations other than

those contained in this document and, if given or made, such information or representations

must not be relied upon as having been authorised by the Company or by the Underwriters.

Neither the delivery of this document nor any subscription or sale made hereunder shall, under

any circumstances, create any implication that there has been no change in the affairs of the

Group since the date of this document or that the information in this document is correct as at

any time subsequent to its date.

Unless explicitly incorporated by reference herein, the contents of the websites of the Group do

not form part of this document. Capitalised terms have the meanings ascribed to them, and

certain technical terms are explained, in Part X – Definitions and Glossary.

WHERE TO FIND HELP

Part II - Some Questions and Answers about the Rights Issue and the Placing of this document

answers some of the questions most often asked by shareholders about rights issues. If you have

further questions, please call the Shareholder Helpline at Equiniti on 0333 207 6530 (+44 121 415

0915 if calling from outside the United Kingdom). Calls are charged at the standard geographic

rate and will vary by provider. Calls outside the United Kingdom will be charged at the applicable

international rate. The helpline is open between 8:30 a.m. – 5.30 p.m., Monday to Friday

excluding public holidays in England and Wales. Please note that Equiniti cannot provide any

financial, legal or tax advice and calls may be recorded and monitored for security and training

purposes. Please note that, for legal reasons, the Shareholder Helpline is only able to provide

information contained in this document and information relating to the Company’s register of

members and is unable to give advice on the merits of the Capital Raise.

This document is dated 27 February 2020.

v

CONTENTS

Page

SUMMARY ..................................................................... 1

RISK FACTORS .................................................................. 8

IMPORTANT INFORMATION ....................................................... 35

RIGHTS ISSUE AND PLACING STATISTICS ............................................ 44

EXPECTED TIMETABLE FOR THE RIGHTS ISSUE AND THE PLACING

(1) (2)

................... 45

DIRECTORS, COMPANY SECRETARY AND ADVISERS .................................. 47

PART I - LETTER FROM THE CHAIR OF ASTON MARTIN LAGONDA GLOBAL HOLDINGS

PLC ............................................................................ 49

PART II - SOME QUESTIONS AND ANSWERS ABOUT THE RIGHTS ISSUE AND THE

PLACING ....................................................................... 63

PART III - TERMS AND CONDITIONS OF THE RIGHTS ISSUE ............................. 72

PART IV - BUSINESS OVERVIEW OF THE GROUP ...................................... 103

PART V - OPERATING AND FINANCIAL REVIEW ...................................... 124

PART VI - FINANCIAL INFORMATION OF THE GROUP ................................. 153

PART VII – UNAUDITED PRO FORMA FINANCIAL INFORMATION ........................ 297

PART VIII – TAXATION ............................................................ 302

PART IX - ADDITIONAL INFORMATION ............................................. 310

PART X – DEFINITIONS AND GLOSSARY ............................................. 375

NOTICE OF GENERAL MEETING .................................................... 385

vi

SUMMARY

A. INTRODUCTION AND WARNINGS

A.1.1 Name and international securities identifier number (ISIN) of the securities

Ordinary shares: ISIN code GB00BFXZC448

Nil Paid Rights: ISIN code GB00BHNC9J35

Fully Paid Rights: ISIN code GB00BHNC9K40

A.1.2 Identity and contact details of the issuer, including its Legal Entity Identifier (LEI)

The Company’s legal name is Aston Martin Lagonda Global Holdings plc (the Company). The

commercial name is “Aston Martin Lagonda”. The Company’s registered address is Banbury Road,

Gaydon, Warwick CV35 0DB, United Kingdom, and its telephone number is +44 (0) 1926 644 644.

The Company’s legal entity identifier is 213800167WOVOK5ZC776.

A.1.3 Identity and contact details of the competent authority approving the prospectus

This document has been approved by the FCA, as competent authority, with its head office at 12

Endeavour Square, London, E20 1JN, and telephone number: +44 20 7066 1000, in accordance with

Regulation (EU) 2017/1129.

A.1.4 Date of approval of the prospectus

This document was approved by the FCA on 27 February 2020.

A.1.5 Warning

This summary has been prepared in accordance with Article 7 of Regulation (EU) 2017/1129 and

should be read as an introduction to this document (this document). Any decision to invest in the

Shares should be based on a consideration of this document as a whole by the investor. Any

investor could lose all or part of their invested capital and, where any investor’s liability is not

limited to the amount of the investment, it could lose more than the invested capital. Civil liability

attaches only to those persons who have tabled the summary, including any translation thereof, but

only where the summary is misleading, inaccurate or inconsistent when read together with the

other parts of this document or where it does not provide, when read together with the other parts

of this document, key information in order to aid investors when considering whether to invest in

the Shares.

B. KEY INFORMATION ON THE ISSUER

B.1 Who is the issuer of the securities?

B.1.1 Domicile, legal form, jurisdiction of incorporation, country of operation and legal entity identifier

The Company was incorporated and registered in England and Wales under the Companies Act

2006 as a private company limited by shares and under the name Aston Martin Lagonda Global

Holdings Limited on 27 July 2018 with registered number 11488166. On 7 September 2018, the

Company was re-registered as a public limited company as Aston Martin Lagonda Global Holdings

plc. Its legal entity identifier is 213800167WOVOK5ZC776.

B.1.2 Principal activities

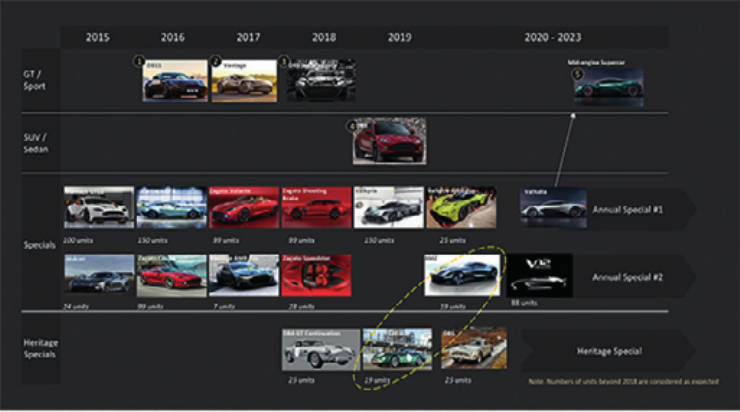

Aston Martin is a globally recognised luxury brand and a leader in the high-luxury sports car

market. For more than a century, the brand has symbolised exclusivity, elegance, power, beauty,

sophistication, innovation, performance and an exceptional standard of styling and design. Its cars

sit solely within the HLS car market segment and the Group’s market leadership position is

supported by award-winning design and engineering capabilities, world-class technology and

state-of-the-art facilities, creating distinctive model line-ups.

The Group sells cars worldwide, primarily from its main manufacturing facility and corporate

headquarters in Gaydon, England, and is currently ramping up pre-production in its second

manufacturing facility in St. Athan, Wales. The Group’s current core line-up comprises three models

of the new generation of products: the grand tourer – DB11; the sports car – Vantage; and the

super grand tourer – DBS Superleggera.

1

All of the Group’s models currently sit under the Aston Martin brand, and some models are

available with different options, including engine size and body type (such as coupe and convertible

models).

In November 2019, Aston Martin Lagonda unveiled its fourth new core model and first SUV, DBX.

Pre-production builds of DBX started as planned in the Group’s production facility located in St.

Athan, Wales and launch is planned for the second quarter of 2020. The DBX order book has built

rapidly, with approximately 1,800 orders from when it opened on 20 November 2019 to 7 January

2020, with approximately 1,200 of those orders being a combination of customer orders and

specifications in progress and approximately 600 dealer-specified to maintain the successful launch

of DBX including customer test cars, marketing cars and showroom cars. The order book has

continued to build, with total orders taken as at the date of this document in excess of the planned

DBX retail target for 2020.

The Group has also confirmed production of its new hypercars, the Aston Martin Valkyrie and Aston

Martin Valkyrie AMR Pro, which establishes a mid-engine platform for Aston Martin and which is

expected to continue with the unveiling of Valhalla in 2022 and of the Vanquish in 2023. The Group

also regularly develops and produces special limited edition models (which will continue to be a

focus), alongside a new range of heritage vehicles.

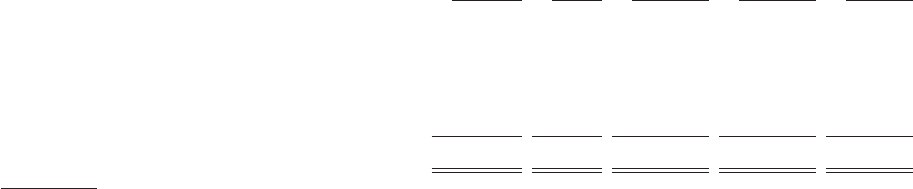

B.1.3 Major shareholders

Insofar as is known to the Company, the name of each person who, directly or indirectly, has an

interest in 3.0 per cent. or more of the Company’s issued share capital, and the amount of such

person’s interest, as at 21 February 2020 (being the latest practicable date prior to the publication

of this document) are as follows:

Shares

Name No. %

Prestige/SEIG Shareholder Group ....................

67,582,104 29.64

Adeem/PW Shareholder Group ......................

62,899,356 27.59

Invesco Limited ...................................

20,696,200 9.15

Mercedes-Benz AG ................................

9,529,739 4.18

Torreal Sociedad de Capital Resigo, S.A. ..............

7,151,411 3.14

Insofar as is known to the Company, immediately following the Capital Raise, the interests of those

persons with an interest in 3.0 per cent. or more of the Company’s issued share capital, including as

a percentage of the enlarged share capital (assuming 100 per cent. take up by such persons of their

entitlements under the Rights Issue (except in the case of the Adeem/PW Shareholder Group and

the Yew Tree Consortium) and no options granted under the Share-Based Incentive Plans are

exercised between 21 February 2020 (being the latest practicable date prior to the publication of

this document) and the completion of the Capital Raise), will be as follows:

Shares

Name No. %

Prestige/SEIG Shareholder Group

(1)

................... 105,428,082 24.7

Yew Tree Consortium

(2)

............................ 92,658,875 21.7

Adeem/PW Shareholder Group

(3)

.................... 76,601,021 17.9

Invesco Limited. ................................... 32,286,072 7.6

Mercedes-Benz AG

(4)

............................... 14,866,393 3.5

Torreal Sociedad de Capital Riesgo, S.A.

(5)

............ 11,156,201 2.6

Notes:

(1) The Prestige/SEIG Shareholder Group has irrevocably undertaken to take up 100 per cent. of its

entitlements under the Rights Issue.

(2) The expected shareholding of the Yew Tree Consortium assumes it takes up 100 per cent. of its

entitlements under the Rights Issue (which it has irrevocably undertaken to do), as well as the

entitlements in respect of the Nil Paid Rights that it has agreed to purchase from the Adeem/PW

Shareholder Group.

2

(3) The expected shareholding of the Adeem/PW Shareholder Group assumes it takes up 38.9 per

cent. of its entitlements under the Rights Issue. The Adeem/PW Shareholder Group has agreed to

sell such number of Nil Paid Rights to the Yew Tree Consortium which will result in (i) the Adeem/

PW Shareholder Group taking up 38.9 per cent. of its entitlements under the Rights Issue and (ii)

the Yew Tree Consortium taking up the remainder of the Adeem/PW Shareholder Group’s

entitlements.

(4) Mercedes-Benz AG has irrevocably undertaken to take up 100 per cent. of its entitlements under

the Rights Issue.

(5) Torreal Sociedad de Capital Riesgo, S.A. has irrevocably undertaken to take up 100 per cent. of

its entitlements under the Rights Issue.

B.1.4 Key managing directors

Dr. Andrew Palmer is the President and Group Chief Executive Officer of the Company and Mark

Wilson is the Chief Financial Officer and Executive Vice President of the Company.

B.1.5 Identity of the statutory auditors

Ernst & Young LLP, with its address at 1 Colmore Square, Birmingham B4 6HQ, United Kingdom, is

the statutory auditor to the Company. The financial information for the Group as of and for the

year ended 31 December 2019 included in this document was audited by Ernst & Young LLP.

The financial information for the Group as of and for the year ended 31 December 2018 contained

herein was audited by KPMG LLP.

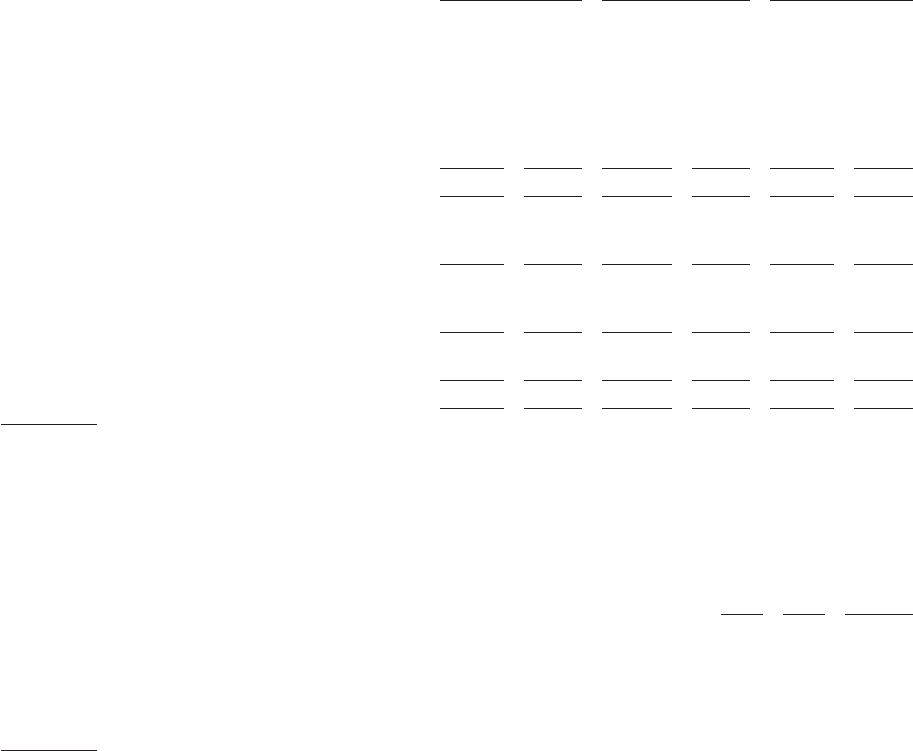

B.2 What is the key financial information regarding the issuer?

The tables below set out the Group’s summary financial information for the periods indicated.

The financial information set forth below is extracted or derived from, and should be read in

conjunction with, the audited consolidated financial statements of the Company as of and for the

year ended 31 December 2019 and the audited consolidated financial statements of the Company

as of and for the year ended 31 December 2018, each included in this document.

The following table sets forth the Group’s main operating results, extracted from the 2019 Financial

Statements and the 2018 Financial Statements, and shows these items as a percentage of total

revenue.

2017

(1)

2018 2019

(£

millions)

(% of

total

revenue)

(£

millions)

(% of

total

revenue)

(£

millions)

(% of

total

revenue)

(audited)

Consolidated Statement of Comprehensive

Income Data:

Revenue ................................. 876.0 100.0 1,096.5 100.0 997.3 100.0

Cost of sales .............................. (496.2) (56.6) (660.7) (60.3) (642.7) (64.4)

Gross profit .............................. 379.8 43.4 435.8 39.7 354.6 35.6

Selling and distribution expenses ............ (60.0) (6.8) (89.8) (8.2) (95.0) (9.5)

Administrative and other operating

expenses ............................... (171.0) (19.5) (293.2) (26.7) (277.3) (27.8)

Other income/(expense) .................... – – 20.0 1.8 (19.0) (1.9)

Operating profit/(loss) ..................... 148.8 17.0 72.8 6.6 (36.7) (3.7)

Finance income ........................... 35.6 4.1 4.2 0.4 16.3 1.6

Finance expense

(2)

......................... (99.9) (11.4) (145.2) (13.2) (83.9) (8.4)

Profit/(loss) before tax ..................... 84.5 9.6 (68.2) (6.2) (104.3) (10.5)

Income tax (charge)/credit .................. (7.7) (0.9) 11.1 1.0 (0.1) 0.0

Profit/(loss) for the year ................... 76.8 8.8 (57.1) (5.2) (104.4) (10.5)

Notes:

(1) Restated to reflect the adoption of IFRS 15.

3

(2) Finance expense includes interest expense with respect to the Preference Shares. The Preference Shares were converted into

ordinary shares as part of the AML IPO. Interest expense with respect to the Preference Shares was £37.9 million and

£93.9 million (including £32.0 million of interest expense and £61.9 million of costs in relation to the conversion of the

Preference Shares as part of the AML IPO) in 2017 and 2018, respectively. The following table presents the above line items

from finance expense through to profit/(loss) for the year, as adjusted to exclude the impact of the Preference Shares:

2017 2018 2019

(£ millions)

(unaudited) (audited)

Finance expense, excluding impact of the Preference Shares ....................... (62.0) (51.3) (83.9)

Profit/(loss) before tax, excluding impact of the Preference Shares .................. 122.4 25.7 (104.3)

Income tax (charge)/credit, excluding impact of the Preference Shares

(1)

............. (7.7) 8.2 (0.1)

Profit/(loss) for the year, excluding impact of the Preference Shares ................ 114.7 33.9 (104.4)

Note:

(1) The estimated reduction in the tax credit attributable to the impact of excluding the Preference Share interest for the

year ended 31 December 2018 would be £2.9 million.

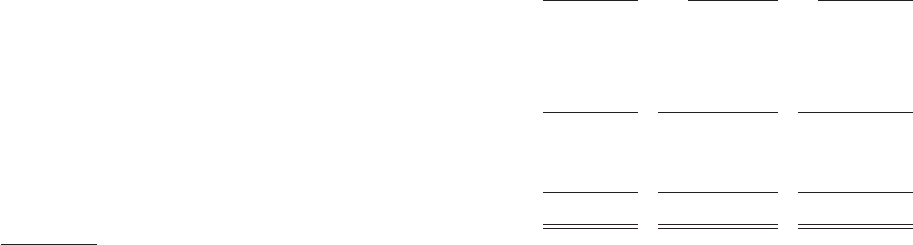

The following table sets out the condensed consolidated statement of financial position as at the

dates indicated:

As at 31 December

2017

(1)

2018 2019

(£ millions)

(audited, unless otherwise indicated)

Non-current assets ..................................... 1,213.8 1,418.6

(2)

1,663.6

Current assets ......................................... 418.3 551.6 567.5

Total assets .......................................... 1,632.1 1,970.2

(2)

2,231.1

Current liabilities ....................................... (529.5) (790.3)

(2)

(858.2)

Non-current liabilities ................................... (966.5) (730.5)

(2)

(1,014.0)

Total liabilities ......................................... (1,496.0) (1,520.8)

(2)

(1,872.2)

Net assets ............................................. 136.1 449.4 358.9

Equity attributable to owners of the group ................ 128.5 439.2 344.8

Non-controlling interests ................................ 7.6 10.2 14.1

Total shareholders equity ............................... 136.1 449.4 358.9

Note:

(1) Restated to reflect the adoption of IFRS 15.

(2) Certain reclassifications have been made in the statement of financial position in the 2019 Financial Statements regarding the

2018 comparative values. These restated items are unaudited.

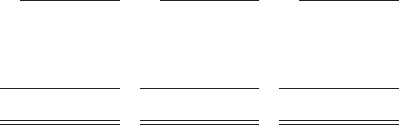

The following table sets out the condensed consolidated statement of cash flows for the periods

indicated:

2017

(1)

2018 2019

(£ millions)

(audited)

Net cash inflow from operating activities ......................... 344.0 222.6

(2)

19.4

Net cash used in investing activities .............................. (346.4) (306.3) (305.2)

Net cash inflow from financing activities .......................... 69.9 57.8 243.3

Net increase/(decrease) in cash and cash equivalents ................ 67.3 (25.9) (42.5)

Cash and cash equivalents at the beginning of the year ............. 101.7 167.8 144.6

Effect of exchange rates on cash and cash equivalents .............. (1.2) 2.7 5.8

Cash and cash equivalents at the end of the year .................. 167.8 144.6 107.9

Note:

(1) Restated to reflect the adoption of IFRS 15.

(2) A reclassification has been made in the statement of cash flows in the 2019 Financial Statements regarding

the 2018 comparative values of £7.2 million cash inflow from Movement in provisions to Decrease in trade and

other payables. This had no impact on the cash generated from operations.

4

There are no qualifications in the audit opinions on the historical financial information included in

this document.

B.3 What are the key risks that are specific to the issuer?

The Group is dependent on the proceeds of the Capital Raise for its liquidity, working capital and

the reset of the business plan and, absent such proceeds, the Group will have an immediate

working capital shortfall and therefore the Company and key trading companies in the Group could

enter into administration shortly thereafter, which could be as early as the next six months, and

which could result in the loss by Shareholders of all or part of their investment in the Company.

Aston Martin Lagonda currently has a significant amount of outstanding debt with substantial debt

service requirements which could have important consequences for its business and operations.

Aston Martin Lagonda’s business model assumes the Wholesale Finance Facility is available on an

ongoing basis, which involves certain liquidity risks, and the loss of the Group’s ability to draw

under this or a similar facility or its credit insurance backing could adversely affect its liquidity and

therefore have a material adverse effect on its business.

Aston Martin Lagonda’s future success depends on its continued ability to introduce its next

generation of cars, which will require significant capital expenditures and will depend in large part

on consumers’ acceptance of the new car offerings, as well as the Group’s ability to complete its car

launch schedule on the contemplated timeline.

Aston Martin Lagonda’s success depends on the continued popularity of its existing products and its

ability to provide its customers with new, attractive products tailored to their needs. These new

products may not achieve the level of consumer acceptance that the Company anticipates.

Aston Martin Lagonda is dependent on its primary manufacturing facility at Gaydon for the

production of its three current core models and it may incur unanticipated costs or delays in

ramping up its plant in St. Athan for full production of DBX.

Aston Martin Lagonda’s future success depends on its ability to continue to sell its cars to customers

at prices which reflect the cost of maintaining the high quality of its cars. Pricing pressure could

limit Aston Martin Lagonda’s ability to pass on production costs to its customers.

The Group’s profitability relies in part upon its ability to produce and deliver its special edition

models. If the Group is delayed or becomes unable to deliver these models in the applicable time

frames, this could lead to additional costs, reduced profitability, return of customer deposits and

damage to the Group’s reputation.

The strength of the Aston Martin brand could be diluted or weakened by a failure to continue to

produce cars of appropriate performance, aesthetics and quality, failure to keep up with new

technologies, quality issues or recalls, dealers promoting other manufacturers’ cars in priority to

Aston Martin Lagonda’s and counterfeit cars and parts affecting performance and quality

perceptions.

The Group may not be able to realise cost savings, reduce capital expenditure or balance supply and

demand effectively in line with its strategy. Aston Martin Lagonda’s ability to successfully

implement its strategy will depend on, at least in part, its ability to reduce costs without

diminishing the quality of its cars, as well as to reduce capital expenditures without limiting its

ability to introduce new cars in line with changes in trends and advances in technology. An inability

to achieve these goals could result in increased costs, damage to the Aston Martin brand, decreased

sales and/or liquidity constraints.

C. KEY INFORMATION ON THE SECURITIES

C.1 What are the main features of the securities?

C.1.1 Type, class and ISIN

Following the passing of the Resolutions at the General Meeting, the Company will issue and allot

to Yew Tree Overseas Limited (Yew Tree), an entity owned and controlled by Lawrence Stroll, as

well as entities owned and controlled by each of Michael de Picciotto, André Desmarais and his

family, Silas Chou (via Yew Tree), John Idol and Lord Anthony Bamford and John McCaw (together,

the Yew Tree Consortium), in aggregate 45,600,577 new ordinary shares of £0.009039687 each in

the capital of the Company (the Placing Shares) at an issue price of 400 pence per Placing Share.

This represents a discount of 0.67 per cent. to the closing price of 402.7 pence per ordinary share of

the Company (Shares) on 30 January 2020, the last Business Day before the Capital Raise was

announced to the market.

5

Pursuant to the Rights Issue, the Company will issue 153,217,942 new ordinary shares of

£0.009039687 each in the capital of the Company (the New Shares). The Rights Issue will be made

on the basis of 14 New Shares for every 25 existing ordinary share in the Company (the Existing

Shares).

When admitted to trading, the New Shares and the Placing Shares (all of which are ordinary shares)

will be registered with ISIN number GB00BFXZC448 and SEDOL number BFXZC44 and trade under

the symbol “AML”. The ISIN for the Nil Paid Rights will be GB00BHNC9J35 and the ISIN for the Fully

Paid Rights will be GB00BHNC9K40.

C.1.2 Currency, denomination, par value, number of securities issued and duration

The currency of the issue is United Kingdom pounds sterling.

Immediately prior to the publication of this document, the share capital of the Company was

£2,061,074.76, comprised of 228,002,890 Existing Shares of £0.009039687 each, all of which were

fully paid or credited as fully paid.

The issued and fully paid share capital of the Company immediately following completion of the

Placing and the Rights Issue (together, the Capital Raise), assuming that no Rights are issued as a

result of the exercise of any options between 21 February 2020 and the completion of the Rights

Issue, is expected to be £3,858,332, comprising 426,821,409 Shares of £0.009039687 each.

C.1.3 Rights attached to the Shares

The New Shares and the Placing Shares will, when issued and fully paid, rank equally in all respects

with the Existing Shares, including the right to receive all dividends and other distributions made,

paid or declared after the date of issue of the New Shares and the Placing Shares, as applicable.

C.1.4 Rank of securities in the issuer’s capital structure in the event of insolvency

The Shares do not carry any rights to participate in a distribution (including on a winding-up) other

than those that exist under the Companies Act 2006. The New Shares, the Placing Shares and the

Existing Shares will rank pari passu in all respects.

C.1.5 Restrictions on the free transferability of the securities

There are no restrictions on the free transferability of the Shares.

C.1.6 Dividend or payout policy

The Group is focused on improving its liquidity position, strengthening its balance sheet and

successfully executing the reset of the business plan. It is therefore the Directors’ intention during

the current phase of the Group’s development to retain the Group’s cash flow to achieve these

objectives. The Directors intend to review, on an ongoing basis, the Company’s dividend policy and

will consider the payment of dividends as the Group’s strategy matures, depending upon the

Group’s free cash flow, financial condition, future prospects and any other factors deemed by the

Directors to be relevant at the time.

C.2 Where will the securities be traded?

Application will be made to the FCA for the New Shares (nil paid and fully paid) and the Placing

Shares to be admitted to the premium listing segment of the Official List of the FCA and to the

London Stock Exchange for such Shares to be admitted to trading on the London Stock Exchange’s

main market for listed securities.

C.3 What are the key risks that are specific to the securities?

Risks relating to the Shares

The Major Shareholders and the Yew Tree Consortium will have significant interests in the

Company following the Capital Raise, and their interests may differ from those of other

Shareholders.

If the Major Shareholders, the Yew Tree Consortium, the Directors and/or certain other

Shareholders purchase additional Nil Paid Rights and/or Fully Paid Rights during the Rights Issue

offer period, the Company may cease to comply with the free float requirement under Listing Rule

6.14, and therefore, absent a modification from the FCA, the Shares may be suspended or cancelled

from the premium listing segment of the Official List in order to maintain the smooth operation of

the market or to protect investors.

6

The market price of the Nil Paid Rights, the Fully Paid Rights and/or the Shares could be subject to

significant fluctuations due to a change in sentiment in the market regarding the Nil Paid Rights,

the Fully Paid Rights and/or the Shares (or securities similar to them), including, in particular, in

response to various facts and events, including any regulatory changes affecting the Group’s

operations, variations in the Group’s operating results and/or business developments of the Group

and/or its competitors.

Shareholders who do not acquire New Shares in the Rights Issue will experience dilution in their

ownership of the Company, and all Shareholders will experience dilution as a result of the Placing.

D. KEY INFORMATION ON THE ADMISSION TO TRADING ON A REGULATED MARKET

D.1 Under which conditions and timetable can I invest in this security?

It is expected that Admission of the New Shares (nil paid) will become effective on 18 March 2020

and that dealings in New Shares will commence, nil paid, as soon as practicable after 8.00 a.m. on

that date.

It is expected that Admission of the Placing Shares will become effective on 17 March 2020 and that

dealings in Placing Shares will commence as soon as practicable after 8.00 a.m. on that date.

The Company proposes to issue 153,217,942 New Shares in connection with the Rights Issue.

Pursuant to the Rights Issue, New Shares will be offered by way of rights to Qualifying Shareholders

on the terms and conditions set out in this document and, in the case of Qualifying Non-CREST

Shareholders only, the Provisional Allotment Letter. The offer is to be made at 207 pence per New

Share, payable in full on acceptance by no later than 11.00 a.m. on 1 April 2020. The Issue Price

represents a discount of 47 per cent. to the closing price of 391 pence per Share on 26 February

2020 (the last Business Day before the publication of this document), and a discount of 36 per cent.

to the theoretical ex-rights price of 325 pence per Share by reference to the closing price on the

same basis.

The Rights Issue will be made on the basis of 14 New Shares at 207 pence per New Share for every

25 Existing Shares held on the Record Date (and so in proportion for any other number of Existing

Shares then held) and otherwise on the terms and conditions as set out in this document and, in the

case of Qualifying Non-CREST Shareholders also in the Provisional Allotment Letters and, for

Qualifying AML Nominee Service Shareholders also in the Forms of Instruction.

Following the passing of the Resolutions at the General Meeting, the Yew Tree Consortium will

subscribe for, and the Company will issue and allot to the Yew Tree Consortium, 45,600,577 Placing

Shares at an issue price of 400 pence per Placing Share. This represents a discount of 0.67 per cent.

to the closing price of 402.7 pence per Share on 30 January 2020, the last Business Day before the

Capital Raise was announced to the market. The Placing is conditional on the Resolutions being

duly passed at the General Meeting, Admission of the Placing Shares occurring at or before 8.00

a.m. on 17 March 2020, none of the warranties or undertakings in the Placing Agreement being

breached and none of the warranties becoming untrue, inaccurate or misleading.

Shareholders will experience a dilution of their shareholding in the Company of 16.67 per cent. as a

result of the Placing.

D.2 Why is this document being produced?

The Company proposes to issue 153,217,942 New Shares in connection with the Rights Issue and

45,600,577 Placing Shares in connection with the Placing.

Through the issue of the New Shares and the Placing Shares, the Company expects to raise gross

proceeds of £500 million. The aggregate expenses of, or incidental to, the Capital Raise to be borne

by the Company are estimated to be approximately £15 million, which the Company intends to pay

out of the proceeds of the Capital Raise.

The Company intends to use the net proceeds from the Capital Raise to improve liquidity, finance

the ramp-up in production of DBX and deliver the turnaround of the Company’s performance. The

Group will use a portion of the net proceeds of the Placing to refund the £55.5 million of short-

term working capital support provided by Yew Tree to the Group in early February 2020 and

between £70 million and £100 million to fund the working capital needs of the business in the first

half of 2020 to facilitate the delivery of DBX, Valkyrie and other special editions in 2020. The

remaining approximately £329.5 million to £359.5 million will be used for general corporate

purposes in support of the reset of the business plan.

7

RISK FACTORS

The Capital Raise and any investment in the New Shares, the Nil Paid Rights and/or the Fully Paid

Rights are subject to a number of risks. Accordingly, Shareholders and prospective investors

should carefully consider the factors and risks associated with any investment in the New Shares,

the Nil Paid Rights and/or the Fully Paid Rights, the Group’s business and the industry in which it

operates, together with all other information contained in this document and all of the

information incorporated by reference into this document, including, in particular, the risk

factors described below, and their personal circumstances prior to making any investment

decision. Some of the following factors relate principally to the Group’s businesses. Other factors

relate principally to the Capital Raise and an investment in the New Shares, the Nil Paid Rights

and/or the Fully Paid Rights. The Group’s businesses, operating results, financial condition and

prospects could be materially and adversely affected by any of the risks described below. In such

case, the market price of the Nil Paid Rights, the Fully Paid Rights and/or the New Shares may

decline and investors may lose all or part of their investment.

Prospective investors should note that the risks relating to the Group, its industry and the New

Shares, the Nil Paid Rights and/or the Fully Paid Rights summarised in the section of this

document headed “Summary” are the risks that the Directors believe to be the most essential to

an assessment by a prospective investor of whether to consider an investment in the New Shares,

the Nil Paid Rights and/or the Fully Paid Rights. However, as the risks which the Group faces

relate to events and depend on circumstances that may or may not occur in the future,

prospective investors should consider not only the information on the key risks summarised in the

section of this document headed “Summary” but also, among other things, the risks and

uncertainties described below.

The following is not an exhaustive list or explanation of all risks which investors may face when

making an investment in the New Shares, the Nil Paid Rights and/or the Fully Paid Rights and

should be used as guidance only. Additional risks and uncertainties relating to the Group that are

not currently known to the Group, or that it currently deems immaterial, may individually or

cumulatively also have a material adverse effect on the Group’s business, prospects, operating

results and financial condition and, if any such risk should occur, the price of the New Shares, the

Nil Paid Rights and/or the Fully Paid Rights may decline and investors could lose all or part of

their investment. Investors should consider carefully whether an investment in the New Shares,

the Nil Paid Rights and/or the Fully Paid Rights is suitable for them in the light of the information

in this document and their personal circumstances.

Risks relating to the business and industry of the Group

The Group is dependent on the proceeds of the Capital Raise for its liquidity, working capital

and the reset of the business plan and, absent such proceeds, the Group will have an immediate

working capital shortfall and therefore the Company and key trading companies in the Group

could enter into administration shortly thereafter, which could be as early as the next six

months. Even if near-term liquidity challenges can be alleviated, without the proceeds of the

Capital Raise the Group faces further liquidity risks over the medium and long terms.

Without the proceeds of the Capital Raise, the Company will have an immediate liquidity