1

29 July 2022

Aston Martin Lagonda Global Holdings plc

Interim results for the six months to 30 June 2022

• Strong demand across the portfolio with GT/Sports sold out into 2023

• H1 revenues increased 9% year-on-year, driven by record core ASPs

• Supply chain and logistics disruptions affecting H1 volumes and working capital,

with impact expected to unwind in H2

• FY 2022 guidance reaffirmed, with positive free cash flow

2

expected in H2

• On track to deliver medium-term targets

• Previously announced transformational capital raise of £653m with strategic

investment by the Public Investment Fund

• Amendment to Strategic Cooperation Agreement with Mercedes-Benz AG extends

timeframe for tranche 2 share issuance into 2024

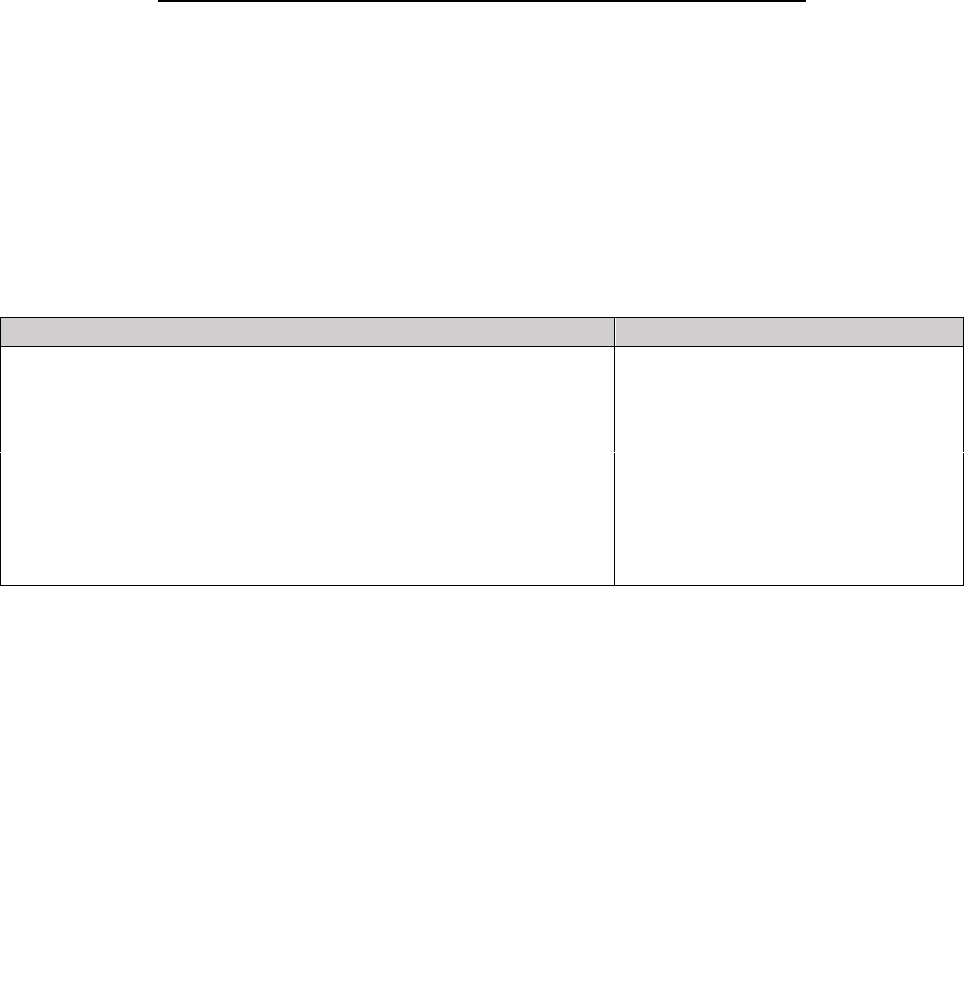

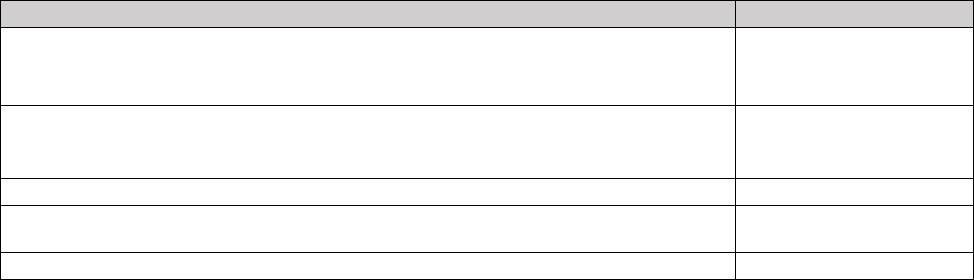

£m

H1 2022

H1 2021

% change

Q2 2022

Q2 2021

% change

Total wholesale volumes

1

2,676

2,901

(8%)

1,508

1,548

(3%)

Revenue

541.7

498.8

9%

309.0

274.4

13%

Adjusted EBITDA

2

58.6

48.8

20%

34.2

28.1

22%

Adjusted operating loss

2

(72.7)

(36.0)

(102%)

(38.4)

(20.7)

(86%)

Operating loss

(89.9)

(38.0)

(137%)

(42.2)

(22.7)

(86%)

Loss before tax

(285.4)

(90.7)

nm

(173.8)

(48.5)

nm

Net debt

2

(1,266.4)

(791.5)

(1,266.4)

(791.5)

1

Number of vehicles including specials;

2

For definition of alternative performance measures please see Appendix;

H1 2022 Financial highlights

• Strong demand across product lines with GT/Sports cars fully sold out into 2023 and DBX orders more

than 40% higher year-on-year

• Wholesale volumes decreased by 8% year-on-year to 2,676 (H1 2021: 2,901) due to supply chain and

logistics disruptions, most notably impacting DBX deliveries in Q2. GT/Sports wholesales of 1,561

increased by 22% year-on-year (H1 2021: 1,280)

• Revenue increased 9% year-on-year to £542m driven by:

- Strong pricing dynamics throughout the core portfolio, with record core ASP in Q2 2022

▪ ASP of £164k in H1 2022, up 9% vs £150k in H1 2021

▪ ASP of £174k in Q2 2022, up 15% vs £151K in Q2 2021

- Aston Martin Valkyrie programme deliveries (27 vehicles delivered, 38 assembled in H1 2022)

- Foreign exchange tailwinds

• Gross profit increased by 31% year-on-year to £188m (H1 2021: £143m) and gross margin increased

substantially year-on-year to 35% (H1 2021: 29%) reflecting improved pricing and mix, as well as

efficiency benefits, partially offset by higher manufacturing and logistics costs

• Adjusted EBITDA increased 20% year-on-year to £59m (11% margin) primarily driven by revenue

growth and higher gross profit, partially offset by higher operating expenses including reinvestments

into brand, marketing and new product launch activities, as well as inflationary impact on general costs

• Operating loss of £90m included a £47m year-on-year increase in depreciation and amortisation

• Loss before tax of £285m was driven by a £134m negative non-cash FX revaluation impact

• H1 2022 free cash outflow of £234m included:

2

- Capital expenditure of £138m, primarily related to new model development including the next-

generation of front-engine sports cars due to launch in 2023

- Net cash interest payments of £63m

- Working capital outflow of £67m driven by temporary supply chain and logistics disruptions,

most notably in Q2. These isolated but impactful issues pushed planned deliveries towards

the end of the period, resulting in elevated receivables and more than 350 ordered vehicles

awaiting final parts at the end of June, which in combination had a cash impact of more than

£80m

• Cash balance of £156m (December 2021: £419m) impacted by a combination of more than £125m of

short-term factors. This relates to the £46m repayment of the revolving credit facility, and more than

£80m from the elevated receivables and number of vehicles held in stock, which are expected to be

delivered in the second half of the year

• Net debt of £1,266m (December 2021: £892m) including £134m impact of non-cash FX revaluation of

US dollar-denominated debt as the GBP weakened against the US dollar during the period

• Positive cash flow performance expected in early Q3, driven by the partial unwind of the short-term

working capital dynamics referenced above

H1 2022 Operational Highlights: Taking off into a new era for Aston Martin:

• Retail customer demand continued to run ahead of wholesales in H1 2022

• DBX707, the world’s most powerful luxury SUV, launched to significant customer and media

excitement; DBX order intake more than 40% higher year-on-year

• New V12 Vantage announced, with all 333 units sold-out by launch in March following unprecedented

demand

• Racing.Green., new ESG strategy, reiterating electrification plans;

- First PHEV deliveries in 2024 and first BEV targeted for launch in 2025

- Fully electrified front-engine and SUV portfolio by 2030

• Strengthened leadership team with appointments of

- Chief Executive Officer, Amedeo Felisa appointed to the Board 4 May 2022

- Chief Financial Officer, Doug Lafferty appointed to the Board 1 May 2022

- Chief Technology Officer, Roberto Fedeli appointed 1 June 2022

- Chief People Officer, Simon Smith appointed 11 April 2022

3

Lawrence Stroll, Executive Chairman commented:

“We have continued to make strong progress in our vision to become the world’s most desirable, ultra-luxury

British performance brand during the first six months of 2022, despite supply chain challenges in Q2. The

underlying fundamentals of Aston Martin have never been stronger, with robust demand across our product

range, sports cars sold out into 2023 and DBX orders up by more than 40% compared to 2021. In addition, we

have aligned the business for its future by assembling a very experienced team, led by Amedeo Felisa, to fully

realise our potential and deliver on the targets we have set.

The first new models in the extraordinary pipeline of products developed since I became Executive Chairman

have also started to be delivered. Our combination of new ultra-luxury, high performance models commenced

with DBX707 – the premier ultra-luxury performance SUV on the market – and the highly-desirable V12

Vantage. They will be followed by an entirely new generation of sports cars from 2023. Importantly, all our new

vehicles are aligned with a minimum 40% contribution margin target, a significant increase from the past, and

a key driver of our medium-term targets. In addition, production of the Aston Martin Valkyrie has continued to

pick up pace, and we are on track to meet our targeted full year deliveries.

However, the first half of the year was not without its challenges. Isolated but impactful supply chain shortages,

particularly in Q2, resulted in lower wholesales and significant working capital headwinds. Specifically, we

ended June with more than 350 DBX707s that we had planned to deliver in Q2, still awaiting final parts,

consuming tens of millions in cash and temporarily limiting our ability to meet the strong demand we have.

We have now started to deliver these vehicles in July and expect further improvements in the supply chain as

we move through H2, supporting the delivery of our full year targets. As a result of the working capital build in

H1 and our expected second half performance, we now expect to generate positive free cashflow in H2,

resulting in a significantly higher cash balance at year end.

Earlier this month we announced a £653 million equity capital raise, which will also see the arrival of the Public

Investment Fund (PIF) as a new anchor shareholder with a 16.7 percent stake. This will transform our balance

sheet, significantly improve our liquidity and cashflow profile, provide greater clarity on our pathway to become

sustainably free cash flow positive from 2024, as well as creating significant shareholder value.

We continue to enjoy a long-term strategic relationship with Mercedes Benz, evidenced by their further

investment in the Company and our planned deployment of their technologies, accessed via tranche 1 of the

Strategic Cooperation Agreement (or SCA), to support all new product ranges in our medium-term plan.

Today, we are pleased to announce a mutually-agreed amendment to the SCA, which extends the timeframe

for the Company and Mercedes to agree additional technology requests by 12 months, with the corresponding

tranche 2 share issuance related to the second basket of Mercedes technologies to be accessed under the

SCA, including BEVs, to take place by July 2024. Importantly, the amendment does not impact our access to

the technologies, subject to reaching a commercial agreement, or change the timeline for our first BEV, which

we continue to target for launch in 2025.”

Amedeo Felisa, CEO, commented:

“Aston Martin is an iconic global brand in a unique position to transcend ultra-luxury and high performance.

The first phase of our journey is complete, building strong foundations for our future growth. Together with the

extraordinary talent and teams we have across the company, we must now ensure we execute on our targets.

With the supply chain challenges that impacted our first half performance expected to ease, we are now

focused on accelerating deliveries of the DBX707, continuing to ramp up Aston Martin Valkyrie production,

and transitioning to our next generation of sports cars.

Leveraging my experiences, I see great potential to build on the success of Project Horizon to optimise our

operational capabilities, reduce complexities and cost, which will drive sustained improvements in profitability

and cashflow generation. I am pleased with the initial progress we have made so far and am excited to lead

Aston Martin as we enter this next phase of our journey.”

Outlook

We remain on track to achieving our medium-term targets of c.10,000 wholesales, c.£2bn revenue and

c.£500m adjusted EBITDA by 2024/25.

For 2022, we continue to expect to deliver significant growth on 2021 with a c.8% increase in core volumes

expected to deliver a c.50% improvement in adjusted EBITDA from the core business. The global operating

environment remains uncertain, with the war in Ukraine, intermittent COVID-19 lockdowns in China, continued

supply chain and logistics disruptions, and raw material cost inflation. Our teams remain focused on minimising

any impact on the Company’s financial performance.

4

For the second half of 2022, we expect strong year-on-year wholesale volume growth, supported by easing

supply chain dynamics, robust demand, as well as the production ramp-up of the DBX707 and the V12

Vantage, which both bring improved profitability compared with prior models, aligned to our 40%+ contribution

margin target. In addition, price adjustments have been made across the portfolio, reflecting the strong pricing

power of the Aston Martin brand.

Aston Martin Valkyrie production continues to pick up pace. We continue to expect 75-90 Aston Martin Valkyrie

programme vehicles to be shipped in 2022, with 38 vehicles already assembled in the first half of the year.

In addition, we expect free cash flow to be positive in the second half of 2022 as higher profitability and cash

inflows from more normalised working capital dynamics are expected to offset cash interest payments and

planned capital expenditures. This is expected to support a year end cash balance in excess of £200m, before

the net proceeds from the proposed equity capital raise of £653m. With up to half of the net proceeds from the

proposed equity capital raise expected to be used to repay debt, we continue to expect a pro-forma cash

balance of £500-£600m.

2022 guidance unchanged – updated to reflect prevailing exchange rates:

• Wholesales: growth to > 6,600 units

• Adjusted EBITDA margin: c.350-450bps expansion

• Capex and R&D: c.£300m

• Depreciation and amortisation: c.£315m-£330m

Reflecting Aston Martin Valkyrie programme shipments and a full year of accelerated depreciation of

capitalised development costs ahead of next generation GT/Sports vehicles in 2023

• Interest costs

1

updated for FX movements (assuming £1:$1.21, versus previous assumption of

£1:$1.32):

• c.£290m (P&L), £95m higher than previous guidance of c.£195m largely driven by

non-cash FX revaluation of dollar-denominated debt in H1

• c.£130m (cash), unchanged from previous guidance

All metrics and commentary in this announcement exclude adjusting items unless stated otherwise and certain

financial data within this announcement have been rounded.

Enquiries

Investors and Analysts

Sherief Bakr Director of Investor Relations +44 (0) 7789 177547

Holly Grainger Deputy Head of Investor Relations +44 (0)7442 989551

Media

Kevin Watters Director of Communications +44 (0)7764 386683

Paul Garbett Head of Corporate & Brand Communications +44 (0)7501 380799

Grace Barnie Corporate Communications Manager +44 (0)7880 903490

Tulchan Communications

Harry Cameron and Simon Pilkington +44 (0)20 7353 4200

• Presentations from Amedeo Felisa, CEO and Doug Lafferty, CFO are available on the corporate website from

07.00am BST and there will be a call for investors and analysts today at 08:30am BST

• The conference call can be accessed live via the corporate website

https://www.astonmartinlagonda.com/investors/calendar

• A replay facility will be available on the website later in the day

• Interim Results for the nine months to 30 September 2022 will be announced on 2 November 2022

1

Assuming current exchange rates prevail for FY22. Note: interest payments are made in Q2 and Q4

5

No representations or warranties, express or implied, are made as to, and no reliance should be placed on, the accuracy, fairness

or completeness of the information presented or contained in this release. This release contains certain forward-looking

statements, which are based on current assumptions and estimates by the management of Aston Martin Lagonda Global Holdings

plc (“Aston Martin Lagonda”). Past performance cannot be relied upon as a guide to future performance and should not be taken

as a representation that trends or activities underlying past performance will continue in the future. Such statements are subject

to numerous risks and uncertainties that could cause actual results to differ materially from any expected future results in forward-

looking statements. These risks may include, for example, changes in the global economic situation, and changes affecting

individual markets and exchange rates.

Aston Martin Lagonda provides no guarantee that future development and future results achieved will correspond to the forward-

looking statements included here and accepts no liability if they should fail to do so. Aston Martin Lagonda undertakes no obligation

to update these forward-looking statements and will not publicly release any revisions that may be made to these forward-looking

statements, which may result from events or circumstances arising after the date of this release.

This release is for informational purposes only and does not constitute or form part of any invitation or inducement to engage in

investment activity, nor does it constitute an offer or invitation to buy any securities, in any jurisdiction including the United States,

or a recommendation in respect of buying, holding or selling any securities.

Nothing in this announcement should be interpreted as a term or condition of the Rights Issue or Capital Raise. Any decision to

purchase, subscribe for, otherwise acquire, sell or otherwise dispose of any nil paid rights, fully paid rights or new shares must be

made only on the basis of the information contained in the prospectus related to the rights issue once published. Copies of that

prospectus will, following publication, be available on the Company’s website at www.astonmartinlagonda.com.

This announcement does not contain or constitute an offer for sale or the solicitation of an offer to purchase securities in the

United States. The securities referred to herein have not been and will not be registered under the US Securities Act of 1933, as

amended (the “Securities Act”), or with any securities regulatory authority of any state or jurisdiction of the United States, and may

not be offered or sold in the United States absent registration under the Securities Act or an available exemption from, or

transaction not subject to, the registration requirements of the Securities Act. There will be no public offer of the securities in the

United States. None of the securities, this announcement or any other document connected with the Rights Issue or Capital Raise

has been or will be approved or disapproved by the United States Securities and Exchange Commission or by the securities

commissions of any state or other jurisdiction of the United States or any other regulatory authority, and none of the foregoing

authorities or any securities commission has passed upon or endorsed the merits of the offering of the securities or the accuracy

or adequacy of this announcement or any other document connected with the Rights Issue or Capital Raise. Any representation

to the contrary is a criminal offence in the United States.

This announcement is for information purposes only and is not intended to and does not constitute or form part of any offer or

invitation to purchase or subscribe for, or any solicitation to purchase or subscribe for, any securities or to take up any entitlements

to any securities in any jurisdiction. No offer or invitation to purchase or subscribe for, or any solicitation to purchase or subscribe

for, any securities or to take up any entitlements to any securities will be made in any jurisdiction in which such an offer or

solicitation is unlawful.

No securities have been nor will be registered under the Securities Act or under any securities laws of any state or other jurisdiction

of the United States and may not be offered, sold, taken up, exercised, resold, renounced, transferred or delivered, directly or

indirectly, within the United States except pursuant to an applicable exemption from or in a transaction not subject to the

registration requirements of the Securities Act and in compliance with any applicable securities laws of any state or other

jurisdiction of the United States. There will be no public offer of any securities in the United States.

6

FINANCIAL REVIEW

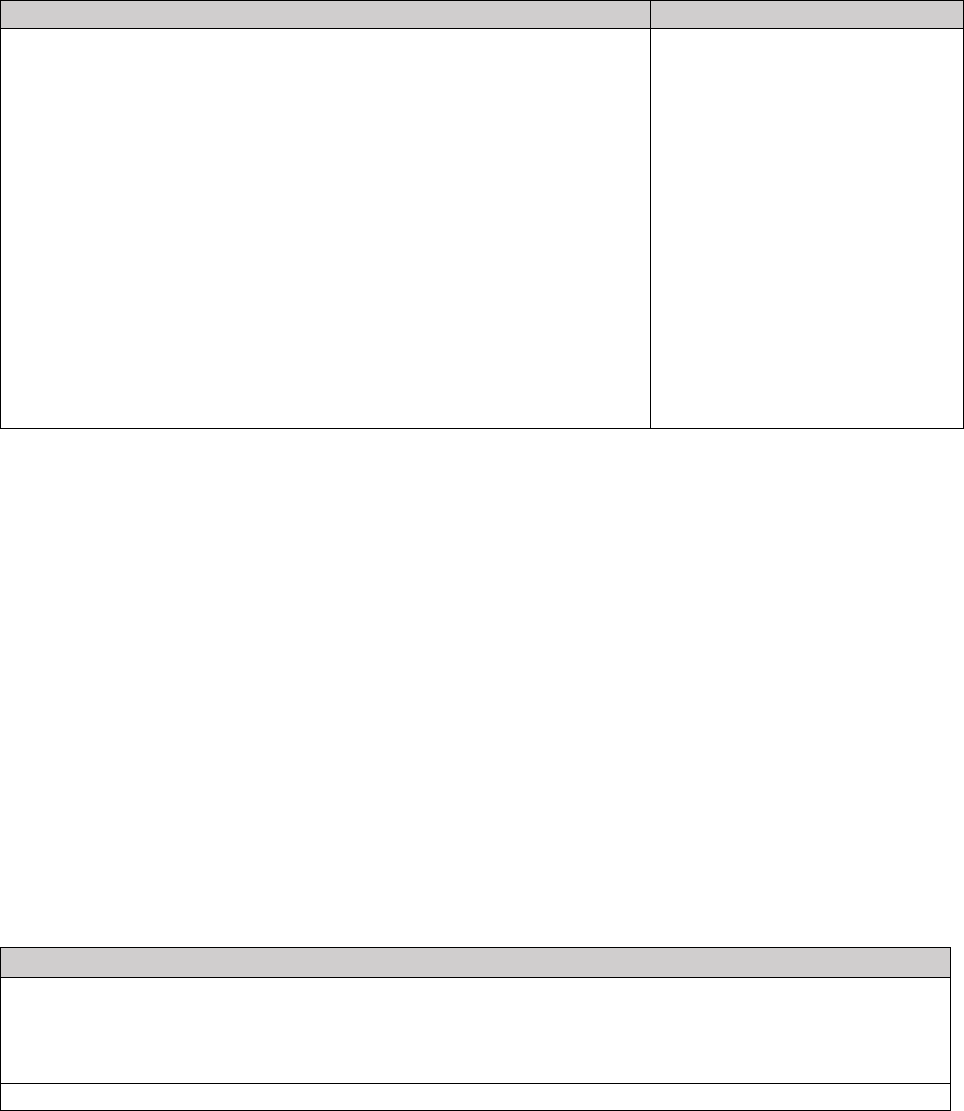

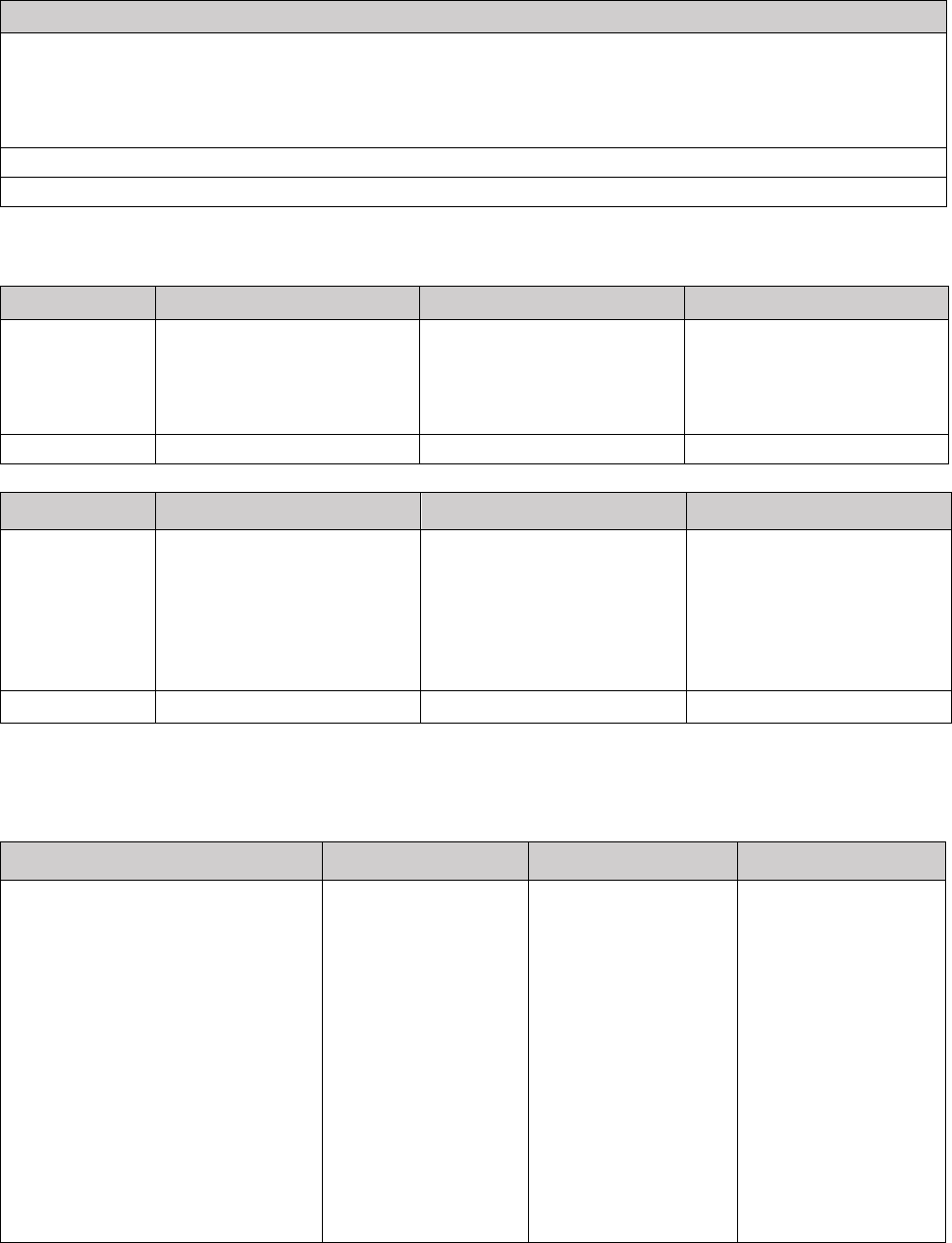

Sales and revenue analysis

Number of vehicles

H1 2022

H1 2021

Change

Q2 2022

Q2 2021

Change

Total wholesale

2,676

2,901

(8%)

1,508

1,548

(3%)

Core (excluding Specials)

2,644

2,881

(8%)

1,495

1,529

(2%)

By region:

UK

488

434

12%

224

162

38%

Americas

720

1,056

(32%)

359

625

(43%)

EMEA ex. UK

614

600

2%

343

316

9%

APAC

854

811

5%

582

445

31%

By model:

Sport

821

670

23%

440

358

23%

GT

740

610

21%

393

321

22%

SUV

1,083

1,595

(32%)

662

849

(22%)

Other

-

6

(100%)

-

1

(100%)

Specials

32

20

60%

13

19

(32%)

Note: Sport includes Vantage, GT includes DB11 and DBS, SUV includes DBX and Other includes prior generation models

Despite strong demand, total wholesales declined by 8% year-on-year in the first half of 2022 due to the

continued challenging operating environment, including disruptions to both supply chain and logistics.

Wholesales of 2,676 units included 32 Specials compared to 2,901 units and 20 Specials in the first half of

2021. The second quarter of 2022 showed a significant improvement over the prior quarter, with 29%

sequential volume growth, despite significant supply chain and logistics disruptions and a full quarter of

COVID-19 lockdowns in parts of China.

Our home market, the UK, saw the strongest year-on-year growth, up 12% in the half, accelerating by 38% in

the second quarter of 2022. The strong year-on-year growth, both in the first half and second quarter of 2022,

was primarily due to strong demand for GT/Sports. Year-on-year growth in the Americas was

disproportionately impacted by the supply chain and logistics disruptions experienced in the second quarter,

particularly for the DBX707. Year-on-year growth in APAC improved significantly in the second quarter,

following the transportation delays which affected first quarter volumes.

Revenue by Category

£m

H1 2022

H1 2021

Change

Sale of vehicles

499.6

458.5

9%

Sale of parts

32.9

32.2

2%

Servicing of vehicles

5.0

5.1

(2%)

Brand and motorsport

4.2

3.0

40%

Total

541.7

498.8

9%

First half revenues increased by 9% year-on-year to £542m (H1 2021: £499m), primarily driven by strong

pricing and mix dynamics, Aston Martin Valkyrie programme deliveries and foreign exchange tailwinds.

Revenues in the second quarter of 2022 also showed a significant improvement over the prior quarter, with

33% sequential revenue growth.

7

The strong year-on-year pricing dynamics enjoyed in the first half of 2022 were supported by price increases

implemented across the range during late 2021 and early 2022, reflecting the strong pricing power of the Aston

Martin brand. In addition, lower customer and retail financing support as well as improved residual values in

market contributed to a sequential improvement in core ASP from £151k in Q1 to £174k in Q2 (H1 2022:

£164k; H1 2021: £150k) – a record level for Aston Martin. Total ASP of £186k in H1 reflected 32 Specials in

the half compared with 20 in the prior year period (H1 2021: £156k).

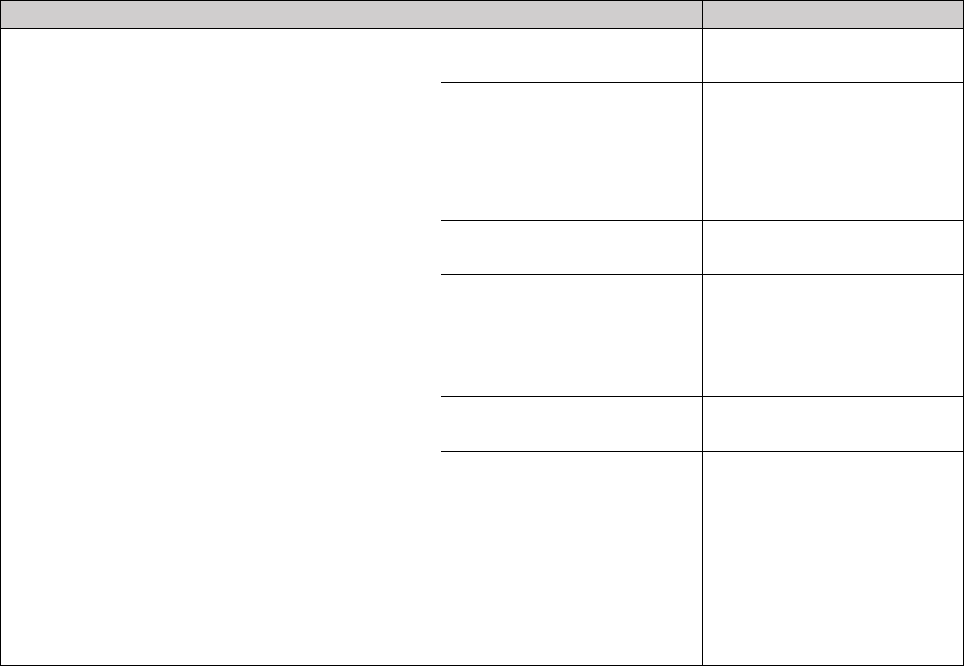

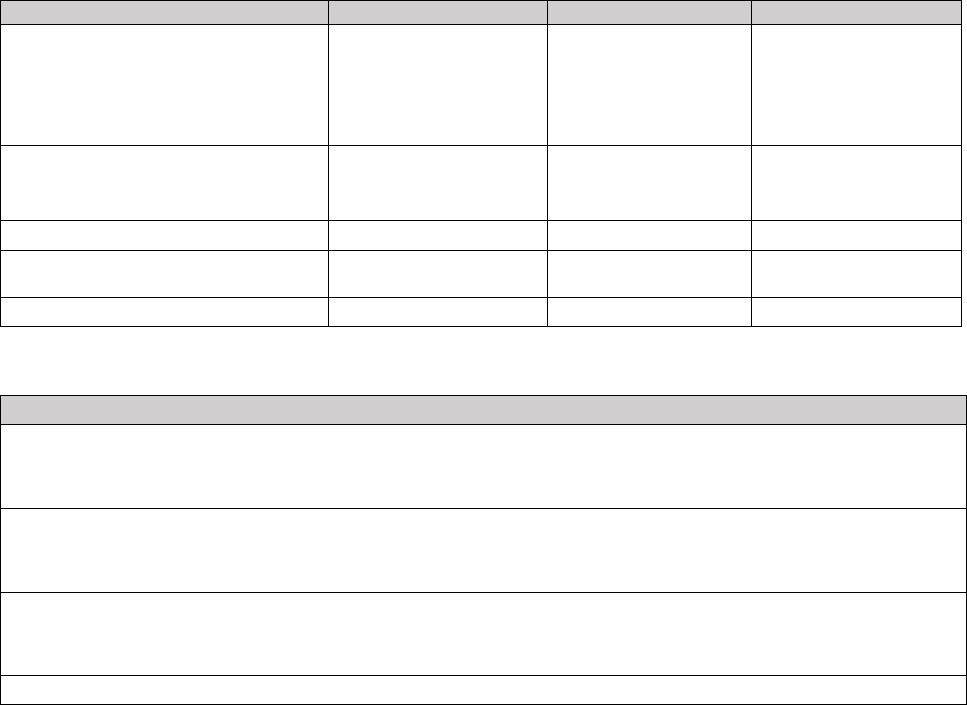

Summary income statement and analysis

£m

H1 2022

H1 2021

Q2 2022

Q2 2021

Revenue

541.7

498.8

309.0

274.4

Cost of sales

(353.6)

(355.5)

(204.9)

(194.4)

Gross profit

188.1

143.3

104.1

80.0

Gross margin %

34.7%

28.7%

33.7%

29.2%

Operating expenses

1

(260.8)

(179.3)

(142.5)

(100.7)

of which depreciation & amortisation

131.3

84.8

72.6

48.8

Adjusted operating loss

2

(72.7)

(36.0)

(38.4)

(20.7)

Adjusting operating items

(17.2)

(2.0)

(3.8)

(2.0)

Operating loss

(89.9)

(38.0)

(42.2)

(22.7)

Net financing expense

(195.5)

(52.7)

(131.6)

(25.8)

of which adjusting financing income

24.4

14.0

13.6

8.6

Loss before tax

(285.4)

(90.7)

(173.8)

(48.5)

Taxation

(4.4)

19.6

(4.0)

19.2

Loss for the period

(289.8)

(71.1)

(177.8)

(29.3)

Adjusted EBITDA

1,2

58.6

48.8

34.2

28.1

Adjusted EBITDA margin

10.8%

9.8%

11.1%

10.2%

Adjusted loss before tax

1

(292.6)

(102.7)

(183.6)

(55.1)

EPS (pence)

(249.0)

(63.3)

Adjusted EPS (pence)

2

(253.7)

(85.3)

1 Excludes adjusting items; 2 Alternative Performance Measures are defined in Appendix

In the first half of 2022, gross profit of £188m increased by £45m, or 31% year-on-year. This translated to a

gross margin of 35%, a year-on-year expansion of 600 basis points. The strong gross margin expansion was

primarily driven by favourable pricing and mix dynamics, and to a lesser extent, by FX benefits. The Company

continues to target a 40%+ contribution margin from its future products, starting with the V12 Vantage and

DBX707.

In the first half of 2022, adjusted EBITDA of £59m increased by £10m, or 20% year-on-year. This translated

to an adjusted EBITDA margin of 10.8%, a year-on-year expansion of 100 basis points.

Operating loss of £90m in the first half of 2022 compared to £38m loss in the prior year period. The £52m year-

on-year change was primarily driven by:

- a £47m increase in depreciation and amortisation charges, principally related to Aston Martin Valkyrie

deliveries and accelerated depreciation ahead of next generation GT/Sports vehicles in 2023, and

8

- increased brand and product launch investments such as the DBX707, V12 Vantage and Valhalla, as well

as marketing initiatives at events such as the Goodwood Festival of Speed

These factors were partially offset by:

- higher year-on-year gross margin as described above, and

- a £14m benefit to operating profit from exchange rate movements

Adjusting operating items of £17m in the first half of 2022 (H1 2021: £2m) predominantly related to the closure

to future accrual of the pension scheme disclosed at the Full Year 2021 results, as well as one-time expenses

related to the change of CEO and appointment of other new executives.

Net financing costs of £196m in the first half of 2022 increased significantly from £53m in the prior year period,

reflecting the revaluation of the US dollar-denominated Senior Secured Notes giving a non-cash FX charge of

£134m (H1 2021: £9m benefit). The £24m adjusting finance credit was due to movements in fair value of

outstanding warrants (H1 2021: £14m credit).

The loss before tax was £285m (H1 2021: £91m loss) and the loss for the period was £290m (H1 2021: £71m),

both impacted by the revaluation of the US dollar-denominated Senior Secured Notes.

The total effective tax rate for the period to 30 June 2022 was -1.5% which is lower than the prior period due

to no current period deferred tax asset movements being recognised (such that the tax charge related to the

financial performance of the overseas subsidiaries during the six month period, together with a small increase

in deferred tax liabilities attributable to distributable profits in China) (H1 2021: 22%).

The total share count at 30 June 2022 was 116 million, giving an adjusted EPS of (253.7)p (H1 2021: (85.3)p).

Cash flow and net debt

£m

H1 2022

H1 2021

Q2 2022

Q2 2021

Cash (used in)/generated from operating activities

(33.1)

103.8

(76.3)

31.6

Cash used in investing activities (excl. interest)

(138.2)

(91.0)

(71.5)

(43.4)

Net cash interest paid

(62.5)

(57.1)

(60.6)

(56.7)

Free cash outflow

(233.8)

(44.3)

(208.4)

(68.5)

Cash (outflow)/inflow from financing activities (excl.

interest)

(41.0)

62.4

(46.9)

(2.0)

(Decrease) / increase in net cash

(274.8)

18.1

(255.3)

(70.5)

Effect of exchange rates on cash and cash

equivalents

12.1

(1.9)

7.7

0.7

Cash balance

156.2

505.6

156.2

505.6

Cash flow from operating activities was an outflow of £33m in the first half of 2022 (H1 2021: £104m inflow).

The year-on-year change in cash flow from operating activities was primarily driven by a working capital outflow

of £67m (H1 2021: £62m inflow), impacted by supply chain and logistics disruptions. The largest driver was a

£105m increase in inventories (H1 2021: £9m decrease), reflecting a significant number of ordered vehicles

awaiting final parts at the end of June. In addition, there was a £41m increase in receivables (H1 2021: £40m

decrease) as supply chain and logistics disruptions pushed planned deliveries towards the end of the second

quarter.

Demand for Specials remains strong with a £10m increase in the deposit balance in the first half of 2022, as

new deposits more than offset the unwind from Specials delivered in the period.

9

Capital expenditure was £138m in the first half of 2022, an increase of £47m year-on-year, with investment

focused on the future product pipeline, particularly, the next generation GT/Sports vehicles, as well as

development of the mid-engine PHEV programme.

Free cash outflow of £234m in the first half of 2022 compared to a £44m outflow in the first half of 2021, or a

£190m year-on-year change. This was primarily due to the significant year-on-year movement in working

capital related cash flows detailed above, as well as the £47m year-on-year increase in capital expenditure.

£m

30-June-22

31-Dec-21

30-June-21

Loan notes

(1,221.5)

(1,074.9)

(1,041.6)

Inventory financing

(38.8)

(19.7)

(39.8)

Bank loans and overdrafts

(62.3)

(114.3)

(118.0)

Lease liabilities (IFRS 16)

(102.0)

(103.4)

(99.2)

Gross debt

(1,424.6)

(1,312.3)

(1,298.6)

Cash balance

156.2

418.9

505.6

Cash not available for short term use

2.0

1.8

1.5

Net debt

(1,266.4)

(891.6)

(791.5)

Cash at 30 June 2022 of £156m included a £46m repayment of the revolving credit facility. Net debt was

£1,266m, up from £892m at 31 December 2021, including £134m impact of non-cash FX revaluation of US

dollar-denominated debt as the pound weakened against the US dollar during the period.

Subsequent Events

Proposed New Equity Financing and Strategic Investment by the Public Investment Fund (“PIF”)

On 15 July 2022, the Company announced its intention to undertake a proposed equity capital raise of £653

million (the “Capital Raise”) to meaningfully deleverage the balance sheet, strengthen and accelerate its long-

term growth. The Company confirms the following plans for a linked primary issuance of shares, subject to

shareholder and regulatory approvals:

• a proposed placing of approximately 23.3 million new ordinary shares at a price of £3.35 per ordinary

share in the capital of the Company to PIF (the “Placing Shares”) to raise approximately £78.0 million,

representing approximately 16.7% of the post-placing share capital of the Company (the “Placing”);

and

• a subsequent underwritten rights issue to raise approximately £575 million (the “Rights Issue”),

including the irrevocable agreements from PIF, Yew Tree Overseas Limited and Mercedes-Benz AG

to fully take up in full their respective entitlement shares.

The Company intends to use the net proceeds from the Capital Raise for the following purposes:

• up to half to repay existing debt, strengthening financial resilience and improving the company’s cash

flow generation by reducing its interest costs;

• the balance to maintain a substantial liquidity cushion to underpin and accelerate future capital

expenditure, and to support execution of its targets in what remains a challenging operating

environment, impacted by the war in Ukraine, COVID-19 lockdowns in China, as well as continued

supply chain and logistics disruptions.

10

The Capital Raise has been in development for some time, and follows a comprehensive Board review of the

Company’s optimal capital structure and growth capital requirements over the medium-term and beyond, as

well as the debt reduction required in order to achieve a net debt leverage ratio of c.1-1.5x by 2024/25.

The specific terms and conditions of the Capital Raise will be announced by the Company in due course. The

Company expects to separately publish a circular in mid-August, which will contain notice of the General

Meeting of the Company required in connection with the Capital Raise, which it is expected will take place in

early September and at which the Company will seek approval from its shareholders. It is expected that a

Prospectus, containing further information on the Capital Raise will also be published in early September, and

in any event before the General Meeting, and that completion of the Capital Raise will take place by the end

of September.

Further information can be found in the announcement made on 15 July 2022:

https://otp.tools.investis.com/clients/uk/astonmartin/rns/regulatory-story.aspx?cid=2424&newsid=1606351

Amendment to Strategic Cooperation Agreement with Mercedes-Benz AG

On 28 July 2022, the Strategic Cooperation Agreement entered into between Mercedes-Benz AG (MBAG) and

the Company on 27 October 2020 (“SCA”) was amended to extend the timeframe for the Company and MBAG

to agree additional technology requests by 12 months to 31 December 2023, with the corresponding tranche

2 share issuance to take place by July of 2024.

11

APPENDICES

Dealerships

30 June-22

31 Dec-21

30 June-21

UK

21

22

22

Americas

44

44

44

EMEA ex. UK

52

53

53

APAC

49

49

50

Total

166

168

169

Number of countries

55

56

58

Units

Wholesale

Q1-22

Q1-21

Change

Q2-22

Q2-21

Change

H1-22

H1-21

Change

UK

264

272

(3%)

224

162

38%

488

434

12%

Americas

361

431

(16%)

359

625

(43%)

720

1,056

(32%)

EMEA ex. UK

271

284

(5%)

343

316

9%

614

600

2%

APAC

272

366

(26%)

582

445

31%

854

811

5%

Total

1,168

1,353

(14%)

1,508

1,548

(3%)

2,676

2,901

(8%)

Wholesale

Q1-22

Q1-21

Change

Q2-22

Q2-21

Change

H1-22

H1-21

Change

Sport

381

312

22%

440

358

23%

821

670

23%

GT

347

289

20%

393

321

22%

740

610

21%

SUV

421

746

(44%)

662

849

(22%)

1,083

1,595

(32%)

Other

0

5

(100%)

0

1

(100%)

0

6

(100%)

Specials

19

1

1,800%

13

19

(32%)

32

20

60%

Total

1,168

1,353

(14%)

1,508

1,548

(3%)

2,676

2,901

(8%)

Note: Sports includes Vantage, GT includes DB11 and DBS, Other includes prior generation models such as Rapide AMR

Summary financials

£m

Q1-22

Q1-21

Q2-22

Q2-21

H1-22

H1-21

Total wholesale volumes

1

1,168

1,353

1,508

1,548

2,676

2,901

Revenue

232.7

224.4

309.0

274.4

541.7

498.8

Gross profit

84.0

63.3

104.1

80.0

188.1

143.3

Gross margin

36.1%

28.2%

33.7%

29.2%

34.7%

28.7%

Adjusted EBITDA

24.4

20.7

34.2

28.1

58.6

48.8

Adjusted EBITDA margin

10.5%

9.2%

11.1%

10.2%

10.8%

9.8%

Adjusted operating loss

(34.3)

(15.3)

(38.4)

(20.7)

(72.7)

(36.0)

Adjusted operating margin

n.m.

n.m.

n.m.

n.m.

n.m.

n.m.

Adjusting operating items

(13.4)

-

(3.8)

(2.0)

(17.2)

(2.0)

Adjusting financing items

10.8

5.4

13.6

8.6

24.4

14.0

Operating loss

(47.7)

(15.3)

(42.2)

(22.7)

(89.9)

(38.0)

Loss before tax

(111.6)

(42.2)

(173.8)

(48.5)

(285.4)

(90.7)

Note: For definition of alternative performance measures please see the Appendices and note 17 of the Interim Financial Statements;

1

Number

of vehicles including specials

12

Summary cash flow statement

£m

Q1-22

Q1-21

Q2-22

Q2-21

H1-22

H1-21

Cash generated from/(used in)

operating activities

43.2

72.2

(76.3)

31.6

(33.1)

103.8

Cash used in investing activities

(excl. interest)

(66.7)

(47.6)

(71.5)

(43.4)

(138.2)

(91.0)

Net interest paid

(1.9)

(0.4)

(60.6)

(56.7)

(62.5)

(57.1)

Free cash (outflow)/inflow

(25.4)

24.2

(208.4)

(68.5)

(233.8)

(44.3)

Cash inflow/(outflow) from

financing activities (excl. interest)

5.9

64.4

(46.9)

(2.0)

(41.0)

62.4

(Decrease)/increase in net cash

(19.5)

88.6

(255.3)

(70.5)

(274.8)

18.1

Effect of exchange rates on cash

& cash equivalents

4.4

(2.6)

7.7

0.7

12.1

(1.9)

Cash balance

403.8

575.4

156.2

505.6

156.2

505.6

Alternative Performance Measure

£m

H1 2022

H1 2021

Loss before tax

(285.4)

(90.7)

Adjusting operating expense

17.2

2.0

Adjusting finance (income)

(24.4)

(14.0)

Adjusted EBT

(292.6)

(102.7)

Adjusted finance (income)

(1.2)

(10.7)

Adjusted finance expense

221.1

77.4

Adjusted operating loss

(72.7)

(36.0)

Reported depreciation

38.2

28.8

Reported amortisation

93.1

56.0

Adjusted EBITDA

58.6

48.8

Alternative performance measures

In the reporting of financial information, the Directors have adopted various Alternative Performance

Measures ("APMs"). APMs should be considered in addition to IFRS measurements. The Directors believe

that these APMs assist in providing useful information on the underlying performance of the Group, enhance

the comparability of information between reporting periods, and are used internally by the Directors to

measure the Group's performance.

• Adjusted operating loss is loss from operating activities before adjusting items

• Adjusted EBITDA removes depreciation, loss/(profit) on sale of fixed assets and amortisation from

adjusted operating loss

• Adjusted operating margin is adjusted operating (loss)/profit divided by revenue

• Adjusted EBITDA margin is adjusted EBITDA (as defined above) divided by revenue

• Adjusted Earnings Per Share is loss after income tax before adjusting items, divided by the weighted

average number of ordinary shares in issue during the reporting period

• Net Debt is current and non-current borrowings in addition to inventory financing arrangements,

lease liabilities recognised following the adoption of IFRS 16, less cash and cash equivalents and

cash held not available for short-term use

• Free cashflow is represented by cash (outflow)/inflow from operating activities plus the cash used in

investing activities (excluding interest received) plus interest paid in the year less interest received.

13

Principal risks and uncertainties

The principal risks and uncertainties that could substantially affect the Group’s business and results were

previously reported on pages 40 to 42 of the 2021 Annual Report and Accounts. Our Board and Management

team have reassessed the risk environment as at 30 June 2022 to consider any significant changes to the

Group’s risk assessment including any new and emerging risks and opportunities.

There have not been any significant changes to the principal risks previously disclosed within the 2021 Annual

Report and Accounts and the principal risks and uncertainties that the Group faces for the second half of the

year are consistent with those previously reported as summarised below.

Strategic risks

Macroeconomic uncertainty and political instability: The Group operates in the ultra-luxury segment (ULS)

vehicle market and accordingly its performance is linked to market conditions and consumer demand in that

market. Sales of ULS vehicles are affected by general economic conditions and can be materially affected by

the economic cycle. Demand for luxury goods, including ULS vehicles, is volatile and depends to a large extent

on the general economic, political, and social conditions in a given market. Furthermore, economic slowdowns

in the past have significantly affected the automotive and related markets. Periods of deteriorating general

economic conditions may result in a significant reduction in ULS vehicle sales, which may put downward

pressure on the Group’s product and service prices and volumes, and negatively affect profitability. These

effects may have a more pronounced effect on the Group’s business, due to the relatively small scale of its

operations and its limited product range.

Political change has the potential to directly affect the Group through the introduction of new laws (including

tax and environmental laws) or regulations or indirectly by altering customer sentiment. Government policy in

areas such as trade and the environment also have the opportunity to impact the business through the

introduction of new barriers, for example in relation to the trade between the United Kingdom and the European

Union or through changes in emissions legislation. Any future change in government in both the United

Kingdom and the Group’s key markets could have an impact on the Group due to changes in policy, legislation,

or regulatory interpretation.

In February 2022, Russia launched an invasion of Ukraine and in response to this invasion, a large number of

countries imposed severe sanctions on Russia (including certain Russian entities and individuals) and a large

number of private companies have also voluntarily ceased operating in, or doing business with, Russia.

Examples of such sanctions include a prohibition on doing business with certain Russian companies, large

financial institutions, officials and oligarchs and a commitment by certain countries and the European Union to

remove selected Russian banks from the Society for Worldwide Interbank Financial Telecommunications

(SWIFT), the electronic banking network that connects banks globally. Many companies have also announced

the cessation of their Russian businesses and/or their unwillingness to retain interests in Russian assets or to

continue dealings with Russian or related counterparties, even where such action is not required by current

sanction regimes. The scope and scale of such economic sanctions and voluntary actions by companies

remain subject to rapid and unpredictable change and may have considerable negative impacts on global

macroeconomic conditions and on European economies and counterparties. In particular, Russia’s invasion

of Ukraine has impacted and is expected to continue to impact energy prices and energy supply in Europe,

which has significant dependence on Russian natural gas and on crude oil. Moreover, existing concerns about

market volatility, rising commodity prices (such as metals), disruptions to supply chains, high rates of inflation

and the risk of regional or global recessions or “stagflation” (i.e., recession or reduced rates of economic growth

coupled with high rates of inflation) have been exacerbated by Russia’s invasion of Ukraine. As a result of

these sanctions and conditions, the Group has paused vehicle and parts shipments to Russia and the Ukraine,

which represented less than 1 per cent. of the Group’s total wholesales in the year ended 31 December 2021.

None of the Group’s Tier 1 suppliers are based in Russia or Ukraine. As at the date of this document, the war

in Ukraine continues. As the situation continues to evolve, the Group is unable to predict the ultimate impacts

that the war and the resulting sanctions will have on the global financial markets and economy more generally,

but such impacts could include those discussed in this risk. If the conflict is prolonged, escalates or expands

(including if additional countries become involved), or if additional economic sanctions or other measures are

imposed, or if volatility in commodity prices or disruptions to supply chains worsen, regional and global

macroeconomic conditions and financial markets could be impacted more severely, which in turn could have

a more severe effect on the Group’s business, financial condition, results and the value of its assets.

Damage to our brand image (luxury and exclusivity) or reputation: The Group’s success depends on the

preservation and enhancement of our brand and reputation with ultra-luxury consumers. Damage caused by

any reason (e.g. poor customer experience, poor design, quality issues, late delivery) could significantly impact

14

our ability to deliver planned volume growth. We promote brand awareness and identity through our marketing

activity, leveraging the global reach of the Aston Martin Aramco Cognizant Formula One

TM

Team. The

successful rebalance of GT/Sport supply to demand combined with our return to the ‘build to order’ strategy is

controlling supply to drive brand exclusivity. Investment in new technology combined with delivery of our three-

pillar strategy will further enhance the appeal of the brand and increase our customer base.

Technological advancement: To remain competitive the Group needs to incorporate the latest technologies

(e.g. electrification, active safety, connected car, autonomous driving) into its products and keep pace with the

transition to electrified and lower emission powertrains. Strategic agreements with key suppliers provide

access to technology that may otherwise be too costly to develop internally.

Operational risks

Talent acquisition and retention: The Group’s future success depends substantially on the continued service

and performance of the members of its senior management team for running its daily operations, as well as

planning and executing its strategy. The Group is also dependent on its ability to retain and replace its design,

engineering, and technical personnel so that the Group is able to continue to produce vehicles that are

competitive in terms of performance, quality, and aesthetics. There is strong competition worldwide for

experienced senior management and personnel with technical and industry expertise. If the Group loses the

services of its senior management or other key personnel, the Group may have difficulty and incur additional

costs in replacing them. If the Group is unable to find suitable replacements in a timely manner, its ability to

realise its strategic objectives could be impaired. In addition, the Group’s ability to realise its strategic

objectives could also be impaired if the Group is unable to recruit sufficient numbers of new personnel of the

right calibre and with the required skills and capabilities to support its strategic objectives.

Programme delivery: Failure to deliver major programmes on time, within budget and to the right technical

specification could jeopardise delivery of our strategy leading to adverse financial and reputational

consequences. The Group employs Project Management teams to deliver significant programmes using our

‘Mission’ programme delivery governance methodology. In 2021 we relocated production for all sports cars

(including Valkyrie and V12 Speedster) to the main production facility in Gaydon and assigned dedicated

project delivery teams to manage these programmes through to completion.

Achieving financial and cost-reduction targets: The Group’s ability to successfully implement its strategy will

depend on, at least in part, its ability to achieve its financial targets as well as to maintain capital expenditures

without limiting its ability to introduce new vehicles in line with changes in trends and advances in technology.

Market conditions and trends change over time and may be particularly affected by macroeconomic factors,

including high rates of inflation, increasing interest rates, rising commodity prices and the risk of regional or

global recessions or “stagflation” (i.e., recession or reduced rates of economic growth coupled with high rates

of inflation). In addition, the war in Ukraine and the COVID-19 pandemic may provide challenges to the Board’s

ability to implement its business plan or require it to re-consider it or adopt new strategies. Major events with

an impact on the Group’s business like the war in Ukraine and the COVID-19 pandemic, including further

variants or “waves,” may result in a diversion of management attention and require the Group to focus on

preserving liquidity rather than implementing its business plan. An inability to achieve these goals, or to achieve

them only in part or later than expected, could result in increased costs, damage to the Aston Martin brand,

decreased sales, elevated levels of Group or dealer stocks and/or liquidity constraints, any of which could have

a material adverse effect on the Group’s business, financial condition and results of operations.

Cyber security and IT resilience: The increasing threat of cyberattack presents risk to the availability,

confidentiality and integrity of information and IT-supported operating systems. A cybersecurity breach could

result in unplanned system outage, impacting core operations and/or result in a major data loss leading to

reputational damage and financial loss. A robust technology environment is critical to the Group’s success and

operational resilience. The Group is investing in tools and resources to enhance the control environment and

reduce the risk of core business operational disruption or major data loss. The phased implementation of a

new ERP system through 2022 will improve the operational resilience of our IT environment.

Supply chain disruption: The Group’s dependence on a limited number of suppliers exposes the Group to the

risk of increased material costs due to suppliers’ pricing power, limited availability and disrupted delivery

schedules, including as a result of the effects of the COVID-19 pandemic and ongoing global supply chain

issues, and the risk of the quality of the products produced by that supplier declining. If one or more of the

Group’s suppliers becomes unable or unwilling to fulfil its delivery obligations, or is unable to supply products

of the requisite quality for any reason (including favouring other purchasers due to better pricing or volume,

financial difficulties, damage to production, transportation difficulties, labour disruption, supply bottlenecks of

raw materials and pre-products, natural disasters, COVID-19 and other pandemics, the war in Ukraine and

15

other wars, terrorism or political unrest), there is a risk that the Group’s ability to produce vehicles or the quality

of its vehicles could be negatively affected, which could adversely affect demand for its vehicles.

Compliance risks

Compliance with laws and regulations: The Group is subject to a broad range of national and regional laws

and regulations which include vehicle emissions, fuel consumption, tariffs, safety and certification, competition,

health and safety, data protection, corporate governance, employment, and taxation. Changes to laws and

regulations or a major compliance breach could have a material impact on the business. As emissions

regulations become increasingly stringent the Group continues to invest in product portfolio expansion to

accelerate its transition towards electrified powertrains and reduced emissions. The Group also requires all

employees to complete annual re-certification training in its Standards of Corporate Conduct to promote good

business practice and compliance.

Climate Change risks

Climate change – There are a number of significant transition and physical risks associated with the impact of

climate change which could significantly impact demand for the Group’s vehicles, or the Group’s ability to sell

vehicles within certain markets or have financial consequences through potential increased carbon pricing and

taxes.

Transitioning to a lower-carbon economy poses the most significant climate related risk with the Group being

exposed to:

• Policy and legal risk: Capital and operating expenses required in order to comply with

environmental laws and regulations can be significant. New policy actions and/or legislation

changes relating to environmental matters, such as the implementation of carbon pricing

mechanisms to reduce green house gas (GHG) emissions or the imposition of more stringent

vehicle emissions regulations, could give rise to significant costs.

• Technology risk: New technologies that support the transition to a lower-carbon, energy-efficient

economic system, including the increasing demand for lower emission vehicles and electrified

powertrains, could have a significant impact on the Group. The Group many be unable to develop

lower capacity and fully electric vehicles successfully, as quickly as its competitors or at a

reasonable cost.

• Market risk: Customer preferences may change more quickly than anticipated away from

traditional internal combustion engines (ICEs) towards alternative non-ICE powertrains (e.g. plug-

in hybrid electric vehicle, battery electric vehicles, Hydrogen, Synthetic fuels). This could

significantly affect demand for the Group’s products. Increasing consumer awareness around

sustainability and the resultant desire to buy products which use sustainable materials may

adversely impact demand for the Group’s products.

• Reputation risk: Customers and communities are increasingly concerned with an organisation’s

contribution to or detraction from the transition to a lower-carbon economy. If the Group does not

deliver on its net-zero goals, sustainability targets, the production of hybrid and fully-electric

models or does not otherwise demonstrate its commitment to reducing its impact on climate

change, this could have a material adverse effect on the Group.

Physical risks resulting from climate change can be event driven (such as an extreme weather event) or longer-

term shifts in climate patterns (such as global warming). Increased frequency and severity of extreme weather

events could lead to damage to assets and/or facilities or lead to production or supply chain disruption. In each

case, this could have a material adverse effect on the Group’s business, financial condition, and results of

operations.

Financial risks

Liquidity: The Group’s significant leverage and existing levels of debt may make it difficult to obtain additional

debt financing should the need arise due to unforeseen economic shocks. Failure to collect planned deposits

could place additional stress on the Group’s liquidity. The Group's liquidity requirements arise primarily from

its need to fund capital expenditure for product development, including the electrification of its product portfolio,

and to service debt. The Group is also subject to foreign exchange risks and opportunities and manages its

exposure in accordance with the Group Hedging Policy.

16

Impairment of capitalised development costs: The Group's balance sheet and income statement may be

adversely impacted by an impairment in the carrying value of capitalised development costs. A significant

reduction in vehicle lifecycle profitability could result in the need to impair the capitalised development

intangible asset. Where potential impairment triggers are identified management perform assessments to

evaluate the recoverability of capitalised development costs.

The risks and opportunities summarised above, linkage to the Group's strategy, and additional mitigating

actions taken in respect of them, are explained and described in more detail on pages 40 to 42 of the 2021

Annual Report and Accounts.

CONSOLIDATED STATEMENT OF COMPREHENSIVE INCOME

6 months ended

30 June 2022

6 months ended

30 June 2021

12 months ended

31 December 2021

Notes

Adjusted

Adjusting

items*

Total

Adjusted

Adjusting

items*

Total

Adjusted

Adjusting

items*

Total

£m

£m

£m

£m

£m

£m

£m

£m

£m

Revenue

2

541.7

-

541.7

498.8

-

498.8

1,095.3

-

1,095.3

Cost of sales

(353.6)

-

(353.6)

(355.5)

-

(355.5)

(751.6)

-

(751.6)

Gross profit

188.1

-

188.1

143.3

-

143.3

343.7

-

343.7

Selling and distribution expenses

(51.9)

-

(51.9)

(35.1)

-

(35.1)

(84.8)

-

(84.8)

Administrative expenses

3

(208.9)

(17.2)

(226.1)

(144.2)

(2.0)

(146.2)

(333.2)

(2.2)

(335.4)

Operating loss

(72.7)

(17.2)

(89.9)

(36.0)

(2.0)

(38.0)

(74.3)

(2.2)

(76.5)

Finance income

3, 4

1.2

24.4

25.6

10.7

14.0

24.7

2.3

34.1

36.4

Finance expense

5

(221.1)

-

(221.1)

(77.4)

-

(77.4)

(173.7)

-

(173.7)

(Loss)/profit before tax

(292.6)

7.2

(285.4)

(102.7)

12.0

(90.7)

(245.7)

31.9

(213.8)

Income tax (charge)/credit

6

(2.6)

(1.8)

(4.4)

6.3

13.3

19.6

16.2

8.3

24.5

(Loss)/profit for the period

(295.2)

5.4

(289.8)

(96.4)

25.3

(71.1)

(229.5)

40.2

(189.3)

(Loss)/profit for the period attributable to:

Owners of the group

(290.0)

(72.7)

(191.6)

Non-controlling interests

0.2

1.6

2.3

(289.8)

(71.1)

(189.3)

Other comprehensive income

Items that will never be reclassified to the Income Statement

Remeasurement of defined benefit pension liability

6.1

2.4

3.8

Taxation on items that will never be reclassified to the Income Statement

(1.5)

(0.6)

(1.0)

Effect of change in rate of taxation

-

6.8

6.0

Items that are or may be reclassified to the Income Statement

Foreign exchange translation differences

4.3

-

2.3

Fair value adjustment on cash flow hedges

(4.2)

-

(0.3)

Amounts recycled to the Income Statement in respect of cash flow hedges

(0.8)

(2.1)

(4.3)

Taxation on items that may be reclassified to the Income Statement

1.3

0.5

1.2

Effect of change in rate of taxation

-

0.1

-

Other comprehensive income for the period, net of income tax

5.2

6.9

7.7

Total comprehensive loss for the period

(284.6)

(64.2)

(181.6)

Total comprehensive (loss)/income for the period attributable to:

Owners of the group

(284.8)

(65.8)

(183.9)

Non-controlling interests

0.2

1.6

2.3

(284.6)

(64.2)

(181.6)

Earnings per ordinary share

Basic

7

(249.0p)

(63.3p)

(165.9p)

Diluted

7

(249.0p)

(63.3p)

(165.9p)

* Adjusting items are detailed in note 3.

17

CONSOLIDATED STATEMENT OF CHANGES IN EQUITY

Share

Capital

Share

Premium

Capital

Redemption

Reserve

Merger

Reserve

Capital

Reserve

Translation

Reserve

Hedge

Reserve

Retained

Earnings

Non-

controlling

Interest

Total

Equity

£m

£m

£m

£m

£m

£m

£m

£m

£m

£m

At 1 January 2022

11.6

1,123.4

9.3

143.9

6.6

2.7

6.7

(662.4)

18.6

660.4

Total comprehensive loss for the

period

(Loss)/profit for the period

-

-

-

-

-

-

-

(290.0)

0.2

(289.8)

Other comprehensive income

Foreign currency translation

differences

-

-

-

-

-

4.3

-

-

-

4.3

Fair value movement - cash flow

hedges

-

-

-

-

-

-

(4.2)

-

-

(4.2)

Amounts recycled to the Income

Statement - cash flow hedges

-

-

-

-

-

-

(0.8)

-

-

(0.8)

Remeasurement of defined benefit

liability

-

-

-

-

-

-

-

6.1

-

6.1

Taxation on other comprehensive

income

-

-

-

-

-

-

1.3

(1.5)

-

(0.2)

Total other comprehensive

income/(loss)

-

-

-

-

-

4.3

(3.7)

4.6

-

5.2

Total comprehensive

income/(loss) for the period

-

-

-

-

-

4.3

(3.7)

(285.4)

0.2

(284.6)

Transactions with owners,

recorded directly in equity

Credit for the period under equity

settled share-based payments

-

-

-

-

-

-

-

2.1

-

2.1

Tax on items credited to equity

-

-

-

-

-

-

-

(0.1)

-

(0.1)

Total transactions with owners

-

-

-

-

-

-

-

2.0

-

2.0

At 30 June 2022

11.6

1,123.4

9.3

143.9

6.6

7.0

3.0

(945.8)

18.8

377.8

Share

Capital

Share

Premium

Capital

Redemption

Reserve

Merger

Reserve

Capital

Reserve

Translation

Reserve

Hedge

Reserve

Retained

Earnings

Non-

controlling

Interest

Total

Equity

£m

£m

£m

£m

£m

£m

£m

£m

£m

£m

At 1 January 2021

11.5

1,108.2

9.3

144.0

6.6

0.4

10.9

(503.1)

16.3

804.1

Total comprehensive loss for the

period

(Loss)/profit for the period

-

-

-

-

-

-

-

(72.7)

1.6

(71.1)

Other comprehensive income

Amounts recycled to the Income

Statement - cash flow hedges

-

-

-

-

-

-

(2.1)

-

-

(2.1)

Remeasurement of defined benefit

liability

-

-

-

-

-

-

-

2.4

-

2.4

Effect of change in rate of taxation

-

-

-

-

-

-

-

6.7

-

6.7

Taxation on other comprehensive

income

-

-

-

-

-

-

0.5

(0.6)

-

(0.1)

Total other comprehensive

(loss)/income

-

-

-

-

-

-

(1.6)

8.5

-

6.9

Total comprehensive income/(loss)

for the period

-

-

-

-

-

-

(1.6)

(64.2)

1.6

(64.2)

Transactions with owners,

recorded directly in equity

Reclassification

-

0.1

-

(0.1)

-

-

-

-

-

-

Credit for the period under equity

settled share-based payments

-

-

-

-

-

-

-

1.5

-

1.5

Effect of change in rate of taxation

-

-

-

-

-

-

-

4.7

-

4.7

Tax on items credited to equity

-

-

-

-

-

-

-

0.1

-

0.1

Total transactions with owners

-

0.1

-

(0.1)

-

-

-

6.3

-

6.3

At 30 June 2021

11.5

1,108.3

9.3

143.9

6.6

0.4

9.3

(561.0)

17.9

746.2

18

Share

Capital

Share

Premium

Capital

Redemption

Reserve

Merger

Reserve

Capital

Reserve

Translation

Reserve

Hedge

Reserve

Retained

Earnings

Non-

controlling

Interest

Total

Equity

£m

£m

£m

£m

£m

£m

£m

£m

£m

£m

At 1 January 2021

11.5

1,108.2

9.3

144.0

6.6

0.4

10.9

(503.1)

16.3

804.1

Total comprehensive loss for the

year

(Loss)/profit for the year

-

-

-

-

-

-

-

(191.6)

2.3

(189.3)

Other comprehensive income

Foreign currency translation

differences

-

-

-

-

-

2.3

-

-

-

2.3

Fair value movement - cash flow

hedges

-

-

-

-

-

-

(0.3)

-

-

(0.3)

Amounts recycled to the Income

Statement - cash flow hedges

-

-

-

-

-

-

(4.3)

-

-

(4.3)

Remeasurement of defined benefit

liability

-

-

-

-

-

-

-

3.8

-

3.8

Effect of change in rate of taxation

-

-

-

-

-

-

(0.8)

6.8

-

6.0

Tax on other comprehensive income

-

-

-

-

-

-

1.2

(1.0)

-

0.2

Total other comprehensive

income/(loss)

-

-

-

-

-

2.3

(4.2)

9.6

-

7.7

Total comprehensive income/(loss)

for the year

-

-

-

-

-

2.3

(4.2)

(182.0)

2.3

(181.6)

Transactions with owners,

recorded directly in equity

Warrant options exercised

0.1

15.1

-

-

-

-

-

14.8

-

30.0

Reclassification

-

0.1

-

(0.1)

-

-

-

-

-

-

Credit for the year under equity settled

share-based payments

-

-

-

-

-

-

-

3.1

-

3.1

Effect of change in rate of taxation

-

-

-

-

-

-

-

4.7

-

4.7

Tax on items credited to equity

-

-

-

-

-

-

-

0.1

-

0.1

Total transactions with owners

0.1

15.2

-

(0.1)

-

-

-

22.7

-

37.9

At 31 December 2021

11.6

1,123.4

9.3

143.9

6.6

2.7

6.7

(662.4)

18.6

660.4

CONSOLIDATED STATEMENT OF FINANCIAL POSITION

Notes

As at

30 June

2022

As at

30 June

2021

As at

31 December

2021

£m

£m

£m

Non-current assets

Intangible assets

1,392.6

1,362.0

1,384.1

Property, plant and equipment

352.6

381.3

355.5

Right-of-use assets

76.6

69.4

76.0

Trade and other receivables

2.3

0.7

2.1

Other financial assets

-

-

0.5

Deferred tax asset

6

157.3

143.7

156.4

1,981.4

1,957.1

1,974.6

Current assets

Inventories

307.6

202.4

196.8

Trade and other receivables

288.1

142.9

243.4

Income tax receivable

1.2

1.0

1.5

Other financial assets

11

9.2

8.1

7.3

Cash and cash equivalents

9, 10

156.2

505.6

418.9

762.3

860.0

867.9

Total assets

2,743.7

2,817.1

2,842.5

Current liabilities

Borrowings

62.3

118.0

114.3

Trade and other payables

842.8

609.1

721.0

Income tax payable

4.0

4.8

5.5

Other financial liabilities

15.4

69.9

34.8

Lease liabilities

7.4

10.8

9.7

Provisions

12

17.9

17.4

19.9

949.8

830.0

905.2

Non-current liabilities

19

Borrowings

11

1,221.5

1,041.6

1,074.9

Trade and other payables

9.2

6.0

9.8

Lease liabilities

94.6

88.4

93.7

Provisions

12

20.6

19.3

19.0

Employee benefits

13

68.8

85.4

78.7

Deferred tax liabilities

1.4

0.2

0.8

1,416.1

1,240.9

1,276.9

Total liabilities

2,365.9

2,070.9

2,182.1

Net assets

377.8

746.2

660.4

Capital and reserves

Share capital

14

11.6

11.5

11.6

Share premium

1,123.4

1,108.3

1,123.4

Merger reserve

143.9

143.9

143.9

Capital redemption reserve

9.3

9.3

9.3

Capital reserve

6.6

6.6

6.6

Translation reserve

7.0

0.4

2.7

Hedge reserve

3.0

9.3

6.7

Retained earnings

(945.8)

(561.0)

(662.4)

Equity attributable to owners of the group

359.0

728.3

641.8

Non-controlling interests

18.8

17.9

18.6

Total shareholders' equity

377.8

746.2

660.4

CONSOLIDATED STATEMENT OF CASH FLOWS

Notes

6 months

ended

30 June

2022

6 months

ended

30 June

2021

12 months

ended

31 December

2021

£m

£m

£m

Operating activities

Loss for the period

(289.8)

(71.1)

(189.3)

Adjustments to reconcile loss for the period to net cash inflow from operating activities

Tax charge/(credit)

6

4.4

(19.6)

(24.5)

Net finance costs

195.5

52.7

137.3

Other non-cash movements

4.2

(3.1)

(0.1)

Depreciation of property, plant and equipment

33.8

24.9

65.3

Depreciation of right-of-use assets

4.4

3.9

9.3

Amortisation of intangible assets

93.1

56.0

137.6

Difference between pension contributions paid and amounts recognised in Income Statement

(4.6)

(5.4)

(11.4)

(Increase)/decrease in inventories

(104.6)

8.7

7.7

(Increase)/decrease in trade and other receivables

(41.0)

40.1

(75.4)

Increase in trade and other payables

68.3

6.3

52.8

Increase in advances and customer deposits

10.4

7.0

70.7

Movement in provisions

(1.8)

(2.1)

(0.2)

Cash (outflow)/inflow from operations

(27.7)

98.3

179.8

(Increase)/decrease in cash held not available for short-term use

(0.2)

8.4

8.1

Income taxes paid

(5.2)

(2.9)

(9.0)

Net cash (outflow)/inflow from operating activities

(33.1)

103.8

178.9

Cash flows from investing activities

Interest received

0.7

1.4

1.1

Increase in loan assets

-

(1.5)

(1.4)

Decrease in loan assets

-

-

0.9

Payments to acquire property, plant and equipment

(29.1)

(24.7)

(40.7)

Payments to acquire intangible assets

(109.1)

(64.8)

(144.0)

Net cash used in investing activities

(137.5)

(89.6)

(184.1)

Cash flows from financing activities

Interest paid

(63.2)

(58.5)

(118.0)

Proceeds from issue of equity warrants

-

-

15.3

Principal element of lease payments

10

(6.4)

(5.0)

(9.9)

Repayment of existing borrowings

10

(52.3)

(2.1)

(37,3)

Proceeds from inventory repurchase arrangement

10

37.7

-

19.0

Repayment of inventory repurchase arrangement

10

(20.0)

-

(40.0)

New borrowings

10

-

77.0

108.5

Transaction fees on issuance of shares

-

(1.2)

(1.3)

20

Transaction fees on financing activities

-

(6.3)

(2.8)

Net cash (outflow)/inflow from financing activities

(104.2)

3.9

(66.5)

Net (decrease)/increase in cash and cash equivalents

(274.8)

18.1

71.7

Cash and cash equivalents at the beginning of the period

418.9

489.4

489.4

Effect of exchange rates on cash and cash equivalents

12.1

(1.9)

1.2

Cash and cash equivalents at the end of the period

156.2

505.6

418.9

Notes to the Interim Condensed Financial Statements

1. Basis of preparation

The results for the 6 month period ended 30 June 2022 have been reviewed by Ernst & Young LLP, the Group's auditor, and a copy of their review report

appears at the end of this interim report. The financial information for the year ended 31 December 2021 does not constitute statutory accounts as defined

in section 435 of the Companies Act 2006. The auditor’s report on the statutory accounts for the year ended 31 December 2021 was not qualified and did

not draw attention to any matters by way of emphasis and did not contain a statement under section 498(2) or (3) of the Companies Act 2006. A copy of the

statutory accounts for the year ended 31 December 2021 prepared in accordance with UK adopted international accounting standards have been delivered

to the Registrar of Companies. The annual report for the year ended 31 December 2022 will be prepared in accordance with UK adopted international

accounting standards.

Aston Martin Lagonda Global Holdings plc (the "Company") is a company incorporated and domiciled in the UK. The Consolidated Interim Condensed

Financial Statements of the Company as at the end of the period ended 30 June 2022 comprise the Company and its subsidiaries (together referred to as

the 'Group').

Going Concern

The Group meets its day-to-day working capital requirements and medium-term funding requirements through a mixture of $1,184.0m of 1st Lien notes at

10.5% which mature in November 2025, $335m of 2nd Lien split coupon notes at 15% per annum (8.89% cash and 6.11% PIK) which mature in November