Your driving record. Insurers are not allowed to increase your rate based on

accidents or traffic violations that are more than three years old. Insurers may

consider traffic accidents and traffic violations that have happened in the past

three years in determining your risk. If your driving record is less than perfect,

then you will be considered a higher risk and will pay a higher premium.

Geographic area. The number of claims filed by policyholders in your

geographic area affects the rates charged by insurers. Counties or zip codes

are commonly used geographic areas.

Gender and age. Males and young adults are more likely to have accidents;

therefore, your gender and age will affect your rate. Rates generally decrease

at age 25 and may increase as you approach age 50 or 55.

Marital Status. Married individuals are less likely to have accidents and claims;

therefore, married individuals generally pay lower premiums than single

people.

When you apply for auto insurance, the insurer will ask for information about you to evaluate

your individual risk characteristics. These individual risk characteristics assist insurers in

determining whether you will be in an auto accident in the future or will file a claim for

damages. Insurers evaluate these characteristics to see whether their guidelines, known as

underwriting guidelines, permit them to write a policy for you.

If the insurer’s underwriting guidelines allow a policy to be written for you, the insurer will then

charge a rate based on your individual risk characteristics. Some risk characteristics that insurers

rely on to determine rates include:

AUTOMOBILE INSURANCE RATES:

WHAT IMPACTS MY COST &

WHAT I CAN I DO ABOUT IT

800-492-6116 Toll-free

insurance.maryland.gov

CONSUMER ADVISORY

Prior insurance coverage. Most insurers ask about your insurance history, including whether

or not you currently have coverage or whether or not you have ever been cancelled or

nonrenewed. Some insurers require individuals to pay higher premiums if there has been any

lapse in insurance coverage. However, insurers are prohibited by law from denying insurance

because an applicant was previously insured by the Maryland Automobile Insurance Fund.

Annual mileage. Insurers will also calculate your premium based on the average distance

you drive on an annual basis. If your annual mileage is high, then insurers will consider you a

greater risk and will charge you a higher premium.

Age, make and model of vehicle. Premiums are also based on your vehicle’s age, make,

model and value. Certain makes and models of vehicles – when involved in accidents – cause

or permit greater levels of bodily injury, sustain greater levels of damage, and are more

difficult and costly to repair. Insurers charge a higher premium to insure those makes and

models.

Credit history. Some insurers review an individual’s credit history when determining that

person’s premium. For instance, bankruptcies, late payments and the number of credit cards

you have may result in a higher premium. Insurers must follow specific laws when using a

consumer’s credit history to underwrite or rate an auto insurance policy.

Those laws state that an insurer may not:

Increase a renewal premium based on the credit history of the insured;

Apply a surcharge of more than 40% based on credit history; or

Use the following factors to rate a policy: the absence of or inability to obtain credit

history, the number of credit inquiries, or any factor that is more than 5 years old.

CONTINUED

800-492-6116 Toll-free

insurance.maryland.gov

Additionally, you have the right to request that your insurer recheck your credit history once per

policy period. If your credit history has improved, the renewal premium may be reduced.

However, if your credit history has deteriorated, this information cannot be used to increase

your premium.

You can review your credit report to become informed about your standing when you

apply for certain credit and certain types of insurance. You also may correct any errors you

discover in your report. You can review these reports at no charge every 12 months. For

questions, to make corrections to your credit report, or to access information about how to

obtain free copies of your credit reports, you should contact the Federal Trade Commission at

www.ftc.gov.

Compare the premium you are paying to what another company might charge you. Refer to our

“Automobile Insurance: A Comparison Guide to Insurance Rates” at

https://insurance.maryland.gov or call 410-468-2000 to obtain a copy. You can also use our

Interactive Auto Insurance Rate Guide at https://insurance.maryland.gov/Consumer/Pages/Auto-

Insurance-A-Comparison-Guide-To-Rates.aspx. Make sure you compare policies that have the

same coverage.

Good driving record. Insurers may consider traffic accidents and traffic violations that

have occurred in the past three years in determining what to charge you. If your driving

record is less than perfect, then you may be considered a higher risk and might pay a

higher premium.

Safety devices. Frequently discounts are offered for devices that limit bodily injury or

property damage caused by accidents. Such devices can include anti-lock brakes,

automatic safety belts or air bags.

Anti-theft devices. Car alarms and other theft-deterrent devices may also result in a

discount.

Multiple policies. Although an insurer cannot require you to buy a homeowners insurance

policy when you purchase an automobile insurance policy, some insurers offer discounts

to policyholders who purchase both automobile and homeowners policies. In addition,

insurers may offer discounts if you have more than one vehicle insured with the insurer.

Good student. Many insurers offer discounts to students who maintain at least a B

average.

Driver Education Courses. Many insurers offer discounts for the completion of a driver

education course.

Renewal Discount. Some insurers offer a discount to policyholders who have maintained

continuous coverage with the insurer for a specified number of years.

Memberships or employment discounts. Insurers may offer discounts to members of

certain organizations such as credit unions, shopper’s clubs or alumni associations. You

also may be eligible to receive a discount through your employer.

800-492-6116 Toll-free

insurance.maryland.gov

HOW CAN I SAVE MONEY ON MY

AUTOMOBILE INSURANCE POLICY?

Many insurers offer discounts. You should ask your insurance company or insurance producer

(agent or broker) about any available discounts before purchasing or renewing your auto

insurance policy. Not all insurers offer the same discounts but some of the most common

ones include:

Contact the Maryland Insurance Administration at:

200 St. Paul Place, Suite 2700

Baltimore, Maryland 21202

410-468-2000 | 800-492-6116 | 800-735-2258 TTY

https://insurance.maryland.gov/Consumer/Pages/FileAComplaint.aspx

ABOUT THE MARYLAND INSURANCE ADMINISTRATION

The Maryland Insurance Administration (MIA) is the state agency that

regulates the business of insurance in Maryland. If you feel that your insurer

or insurance producer acted improperly, you have the right to file a

complaint. The MIA can investigate complaints that an insurer or insurance

producer has:

Denied or delayed payment of all portions of a claim

Improperly terminated your insurance policy

Raised your insurance premiums without proper notice or in

excess of what the law allows

Made false statements to you in connection with the sale of

insurance or the processing of insurance claims

Overcharged you for services, including premium finance charges

This consumer guide should be used for educational purposes only. It is not intended to provide legal advice or opinions regarding coverage under a specific

insurance policy or contract; nor should it be construed as an endorsement of any product, service, person, or organization mentioned in this guide. Please

note that policy terms vary based on the particular insurer and you should contact your insurer or insurance producer (agent or broker) for more information.

This publication has been produced by the Maryland Insurance Administration (MIA) to provide consumers with general information about insurance-related

issues and/or state programs and services. This publication may contain copyrighted material which was used with permission of the copyright owner.

Publication herein does not authorize any use or appropriation of such copyrighted material without consent of the owner. All publications issued by the MIA

are available free of charge on the MIA's website or by request. The publication may be reproduced in its entirety without further permission of the MIA

provided the text and format are not altered or amended in any way, and no fee is assessed for the publication or duplication thereof. The MIA's name and

contact information must remain clearly visible, and no other name, including that of the insurer or insurance producer reproducing the publication, may

appear anywhere in the reproduction. Partial reproductions are not permitted without the prior written consent of the MIA. Persons with disabilities may

request this document in an alternative format. Requests should be submitted in writing to the Director of Communications at the address listed above.

CONTINUED

Consider whether you want to maintain comprehensive and/or collision coverage. If your

vehicle is older and has been paid off, you may want to consider dropping these coverages

to reduce your premium. However, if you drop these coverages and your vehicle is

damaged in an accident that you cause, or if it is stolen, vandalized or you collide with an

animal, you must pay for the repair.

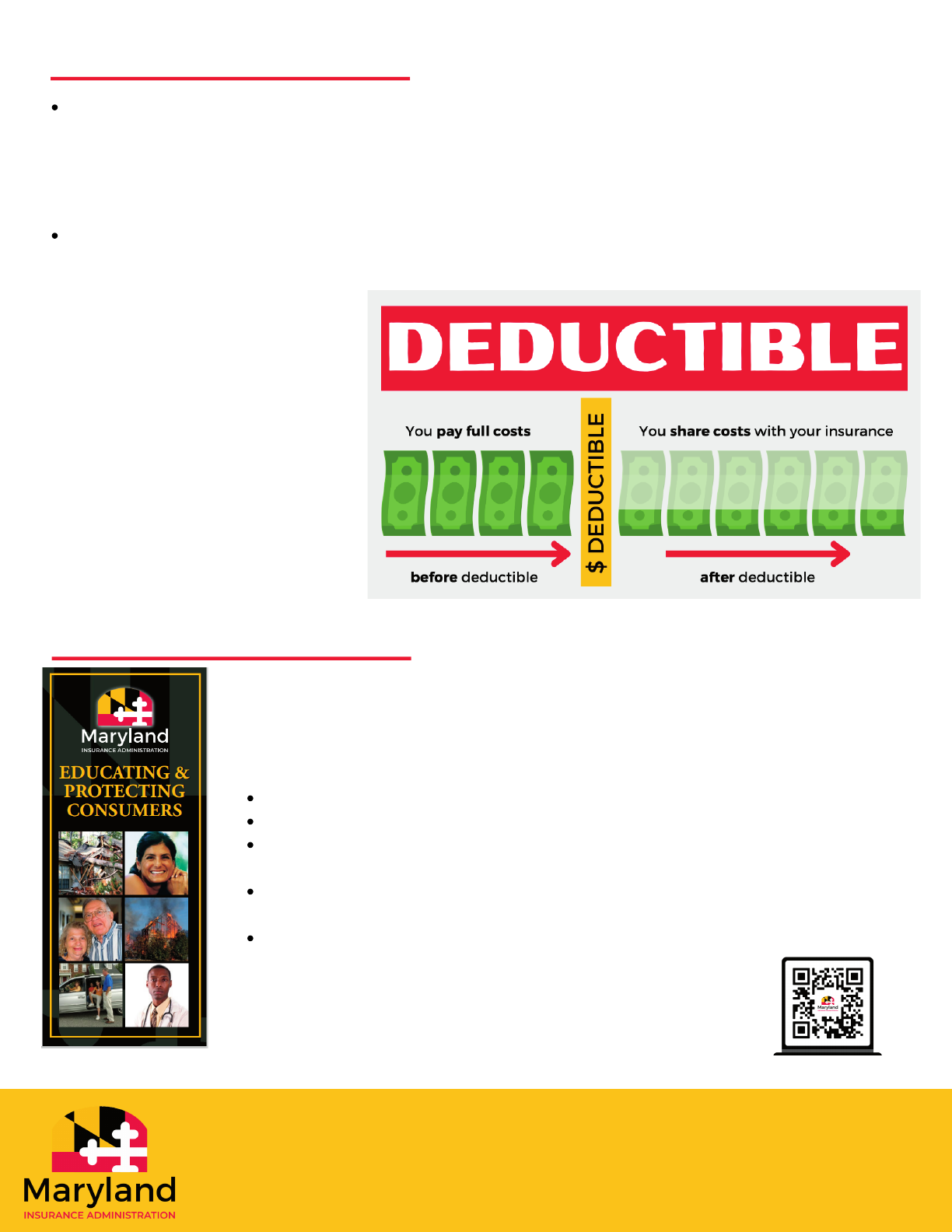

Review your deductible. The deductible is the amount you agree to pay in the event your

vehicle is damaged. Raising the deductible on your policy generally will decrease your

premium. If you select a high

deductible, you will pay more

money out of pocket for any

damage; however, your

insurance premium generally

will be lower.