Economic Capital for Life Insurance

Companies

October 2016

2

© 2016 Society of Actuaries

Economic Capital for Life Insurance

Companies

Caveat and Disclaimer

The opinions expressed and conclusions reached by the authors are their own and do not represent any official position or opinion of the Society of Actuaries or its

members. The Society of Actuaries makes no representation or warranty to the accuracy of the information.

Copyright ©2016 All rights reserved by the Society of Actuaries

SPONSOR

Committee on Finance Research

AUTHORS

Ian Farr, FIA

Adam Koursaris, FIA

Mark Mennemeyer, FSA, MAAA

3

© 2016 Society of Actuaries

TABLE OF CONTENTS

Section 1: Acknowledgements .................................................................................................................................. 4

Section 2: Background and Scope .............................................................................................................................. 5

2.1 Background .............................................................................................................................................................. 5

2.2 Scope ........................................................................................................................................................................ 5

2.3 Fundamentals .......................................................................................................................................................... 5

Section 3: EC Methodology and Modeling ............................................................................................................... 12

3.1 Main Considerations .............................................................................................................................................. 12

3.2 The Liability Runoff Approach ............................................................................................................................... 17

3.3 The Finite Risk Horizon Approach ......................................................................................................................... 19

3.4 Contrasting runoff and finite horizon approaches............................................................................................... 21

3.5 Risk Aggregation .................................................................................................................................................... 22

3.6 Pros and Cons of EC Approaches .......................................................................................................................... 25

3.7 Prevalence of Approaches ..................................................................................................................................... 27

Section 4: Risk Calibration and Validation ............................................................................................................... 30

4.1 Risk Metrics ............................................................................................................................................................ 30

4.2 Risk Factors ............................................................................................................................................................ 32

Section 5: Influence of Market and Supervisory Developments ............................................................................... 39

5.1 Global Financial Crisis ............................................................................................................................................ 39

5.2 Solvency II............................................................................................................................................................... 39

5.3 Own Risk and Solvency Assessment ..................................................................................................................... 40

5.4 Global Capital Standards ....................................................................................................................................... 40

5.5 U.S. Federal Regulatory Activities ......................................................................................................................... 41

Section 6: Applications of Economic Capital ............................................................................................................ 42

6.1 Capital Adequacy ................................................................................................................................................... 42

6.2 Capital Allocation ................................................................................................................................................... 42

6.3 Risk Appetite .......................................................................................................................................................... 43

6.4 Performance Measurement .................................................................................................................................. 44

6.5 Strategic Planning .................................................................................................................................................. 45

6.6 Pricing ..................................................................................................................................................................... 45

6.7 Mergers & Acquisitions ......................................................................................................................................... 45

Section 7: Implementation and Communication ..................................................................................................... 46

7.1 Objectives ............................................................................................................................................................... 46

7.2 Constraints ............................................................................................................................................................. 47

7.3 Governance ............................................................................................................................................................ 48

7.4 Validation ............................................................................................................................................................... 48

7.5 Reporting ................................................................................................................................................................ 49

4

© 2016 Society of Actuaries

Economic Capital for Life Insurance

Companies

Section 1: Acknowledgements

The authors would like to thank the Society of Actuaries for commissioning this research report describing economic

capital practices and theory for life insurance companies. In particular, the practitioners composing the Project

Oversight Group (POG) provided structure and valuable feedback throughout the development of this report. Members

of the POG were:

Nate Deboer

James Berger

Steve Marco

Dennis Radliff

Bob Reitano, Chair

Steven Siegel

Several colleagues provided insightful discussions to support the development of this report, especially Graeme Lawson

and Frederic el Cherif.

The authors also wish to thank Barbara Scott for her assistance coordinating this project, as well as other members of

the Committee on Financial Research for their sponsorship.

5

© 2016 Society of Actuaries

Section 2: Background and Scope

2.1 Background

In recent years, EC has continued to grow in importance, and the insurance landscape has continued to evolve.

Influences from regulatory initiatives in many different countries and the 2008 financial crisis have given risk and

capital increased prominence, while improved computing capabilities have expanded the calculation techniques and

the applications of EC.

In 2008, the Society of Actuaries (SOA) commissioned Willis Towers Watson to develop a research paper on economic

capital (EC), examining the mechanics and implementation of EC methods employed by insurance companies. A

significant finding of that report was that no global consensus had yet emerged on the definition of EC or how to

calculate it. While significant progress has been made since 2008, this finding remains true today.

Consequently, the SOA has commissioned Willis Towers Watson to develop this research paper, designed as a

refreshed edition of the 2008 EC report for life insurance companies. However, this report is accessible as a standalone

document with no assumption that the reader is familiar with the previous edition.

2.2 Scope

This paper aims to address key questions on the calculation of economic capital for long-term life insurers. It discusses

the drivers of economic capital, the development of an internal EC framework and the uses of EC within an insurance

company. It concentrates on the features that make long term life insurance business unique within the financial

landscape.

2.3 Fundamentals

It is useful to introduce some terminology and ideas that will be used in this report to help frame the discussion.

2.3.1 What do we mean by capital?

For an EC calculation we distinguish between the available capital—i.e., the excess of assets over liabilities held by the

insurer—and the required capital – i.e., the amount of assets in excess of liabilities needed to withstand future adverse

outcomes. The capital ratio is the available divided by the required capital.

Because numerous accounting systems exist, the initial (time 0) valuation of assets and liabilities used on a company’s

balance sheet will not necessarily agree with the baseline valuation that is preferred for EC purposes. Differences arise

from accounting conventions (e.g., GAAP, statutory, fair value, economic), the inclusion of different subsets of the

assets and liabilities and different methodologies applied to value those assets and liabilities.

While time 0 accounting conventions may affect the quoted available, required and capital ratio, the most important

feature of EC results is that the correct total asset requirement (liabilities plus required capital) at time 0 is derived.

6

© 2016 Society of Actuaries

A more important aspect of the EC calculation is the set of assumptions used for future balance sheet evaluation (and

whether future balance sheets are considered or not). The choice of this valuation metric directly affects the total asset

requirement. For example total assets required at time 0 to cover a market-consistent value of liabilities in one years’

time may be higher than those required to cover a future GAAP value.

2.3.2 What makes capital “economic”?

The term “economic capital” is frequently used in different and contradictory ways. The debate often lies along

geographic lines but for many is rooted in strong philosophical views.

The common, basic element of EC is that it attempts to measure a capital requirement based on the most realistic

assessment of future economic risks that the company faces. These risks may be market-based, such as interest rates

and asset returns, or insurance-based such as mortality, morbidity or policyholder actions. To measure the capital

requirement, a joint, real-world, distribution of risks is projected into the future, and the effect of those risks on the

company’s financial condition is measured. The capital required to cover these outcomes with a specified degree of

security is then calculated.

This is typically the point where broad agreement ends. Some practitioners argue that a long term projection should be

used (typically for the life of the existing policyholders) and the risk to resulting net cash flows measured. Others

propose a measurement of assets and liabilities after a shorter projection time horizon (such as 1 year). Many hybrid

time horizons, measurement systems and adjustments are applied in practice.

Asset and liability measurement at time 0 for EC

Example 1: Some regimes may include some or all intangible assets, measure assets at book rather than

market value and include prudent margins in the assessment of liabilities.

Example 2: In Solvency II, assets and liabilities are notionally measured at market / market-consistent value (for

both base and stressed valuations) but on the company’s balance sheets IFRS values are used which can differ

significantly from these values.

Example 3: When using a run-off calculation of economic capital the modeler may derive the total market

value of assets required to meet future liability cash flows across a range of scenarios. A time 0 liability

valuation is often not necessary for this calculation. To calculate the available capital, required capital and

capital ratio, some base liability value must be subtracted from the total asset values. Because there is no

“natural” liability valuation as in a 1 year projection, an average or median present value of future cash flows is

often used as the liability valuation.

Example 4: Using differing base liability valuation metrics will affect the solvency ratio. In particular, increasing

the base liability value while keeping the total asset requirement the same will impact the company’s solvency

ratio by altering the split between assets backing liabilities and assets supporting capital requirements. This

measurement therefore requires careful specification and interpretation.

7

© 2016 Society of Actuaries

In this paper we propose that the litmus test for an economic capital model is the use of a realistic projection of

economic risk, coupled with a realistic assessment of the implications for the company. We intentionally use this broad

definition to encompass a number of varieties in this class.

2.3.3 What is an economic valuation?

The concept of “economic accounting” or “economic valuation principles” is often equated with fair-value, embedded

value or market-consistent valuation of liabilities to approximate the price that would be agreed by two independent

parties conducting an arm’s length transaction. These bases typically use risk-free market interest rates for discounting

promised liability cash flows and make allowance for the value of options and guarantees the insurer has sold with

reference to market option prices. Sets of principles have been published

1

for the embedded valuation of insurers and

their liabilities, promoting an “economic” assessment of assets and liabilities as one that is independent of any

regulatory or accounting framework, thereby enabling a consistent assessment of risks across different companies and

geographies.

1

CRO Forum. European Embedded Value Principles http://www.cfoforum.nl/letters/eev_principles.pdf

CRO Forum. Market Consistent Embedded Value Principles http://www.cfoforum.nl/downloads/MCEV_Principles_and_Guidance_October_2009.pdf

Realistic risk assessment

Example 1: Some systems of capital calculation apply simple factors to the quantity of assets or liabilities held

to calculate the capital that is required to be held. For example a fixed 10% of reserves factor is applied in

respect of interest rate risk. We do not classify this as a realistic risk assessment because it does not take

account of the specific risks faced by the company, is not based on current market data or historical analysis

and is not updated frequently.

Example 2: A projection of interest rate risks may be over a short or long time horizon. Either of these qualify

under our definition of economic capital, as long as the assessment of risks under these horizons is a realistic

best estimate of what interest rates are likely to do over the period. The risk model and calibration may come

from either an internal or external source.

Within each of these examples, additional factors for consideration include:

The way that risk is assessed over the projection horizon should be done in light of the asset and

liability profile. Complex, geared exposures need more sophisticated and granular risk assessment

methods.

Margins for prudence are usually minimized to promote a realistic assessment of risk, but

sensitivities for model and parameters uncertainties are useful and common.

Risk premia and term premia are important parts of run-off EC models, but their inclusion is often

challenged because of the difficulty in estimating long term average returns and mean reversion

effects.

8

© 2016 Society of Actuaries

Some practitioners, however, argue against the use of a fair value risk assessment for EC models, with arguments

following three lines: that these bases are inappropriate for the valuation of many types of life insurance liabilities;

that short-term market-value volatility is inappropriate for the measurement of long term economic risk; and that they

do not appropriately recognize the long term nature of their business and their ability to hold assets and liabilities for

the long term. These arguments and their implications are explored in detail in Section 3.

This report promotes a general definition, in which economic capital is measured consistently with the economics of

the company; taking into account the objectives, business plan, management actions, constraints, economic

circumstances and regulatory regime which the company faces. This means that the valuation basis should allow a

company to realistically assess its risks in a way that provides a meaningful perspective across a potentially diverse set

of exposures.

Along with this economic definition, the authors believe that two further questions are needed to develop an economic

capital framework – why is capital held, and who are the stakeholders?

2.3.4 Why is capital held?

Capital is held to allow the company to meet its objectives with a greater degree of certainty; therefore, an EC

framework should start with a detailed consideration of the objectives of the business. A basic and fundamental

objective is the protection of existing policyholders – ensuring their policy benefit payments are made with a high

degree of certainty is a moral imperative. There are also a number of objectives linked to other stakeholders.

Regulatory bodies act as policyholders’ agents in ensuring that payments are made; so as well as convincing

policyholders that capital levels are sufficient, it is equally necessary to satisfy regulators that this is true. Additionally,

to the extent that new and existing policyholders’ interests are represented by other agents such as financial advisors

or rating agencies, it is clear that capital is held to attract favorable assessments by these representatives.

Economics of the company

Example 1: A firm which uses a buy-and hold strategy for fixed interest investment and which closely matches

its assets and liabilities may consider a runoff EC model (defined further in Section 3) more appropriately

aligned with its long term focus, emphasizing risks such as defaults over the investment horizon.

Example 2: A firm which regularly hedges market exposure and undertakes a more active investment strategy

may have a greater concern with market fluctuations over a shorter-term risk horizon.

In reality, insurance firms exhibit elements of both examples. Even a buy-and-hold strategy is regularly

monitored and rebalanced, and even an insurer with an active trading department is still motivated by long-

term objectives. One guiding factor is how the firm behaves during adversity. While banks tend to trade out of

individual risk exposures (e.g., swap corporate bonds for treasuries), more common insurance approaches are

to run off the book as it is or to trade the book to a firm with greater financial security. The latter approach

suggests a strong focus on the tradeable value of the insurance portfolio, suggesting market-based values

cannot be ignored, even for buy-and-hold strategies.

9

© 2016 Society of Actuaries

Failure to meet these objectives ultimately results in significant costs to shareholders, so it is important to consider the

manner of failure and the consequences for the company. A model can then be built that reflects these dynamics

under the real-world distribution of risk.

Obviously having insufficient assets to meet policyholder benefit payments as they fall due would be a ruinous event,

but this is rarely the mechanism of life insurance company failure. Long before this happens, a forward looking

assessment should reveal that assets are expected to be insufficient to meet future liability payments. Both assets and

liabilities may then be transferred to an insolvency scheme or the company remediated through other means. Before

this event, it is likely that available capital would fall below minimum regulatory required capital levels, resulting in

removal of authorization to write new business, restrictions on management actions, forced liquidations, or capital

raising in unfavorable conditions. Even before this, it is likely that financial strength and credit ratings would be

downgraded, making it difficult to attract new business profitably or refinance debt. As well as the direct implications,

the associated drain on management resources and attention results in a significant financial drag.

Avoiding these frictional costs of distress is therefore important to profits and to this extent, shareholders’ profit

motive also encourages them to be well capitalized.

In addition, higher capital levels give added flexibility in the operation of the company and its ability to assume risk and

take advantage of opportunities as they arise. They may also give a competitive advantage of being well capitalized in

adverse market conditions when peers are under pressure. For example, a company which invests in safe treasuries

may hold more capital than needed so that they could change investment strategy later into corporate bonds at

favorable prevailing spreads, or launch a new, capital intensive line of business. Holding capital above the mathematical

optimal also allows a buffer for model risk or un-modelled outcomes such as changes in the regulatory regime, changes

in the views, and assumptions of management, parameter uncertainty etc.

10

© 2016 Society of Actuaries

The discussion above, and indeed much of the discussion in this report, is framed in the context of shareholder-owned

insurance companies. However, it should be noted that most of the discussion and conclusions being made are usually

as relevant for mutual insurers, albeit with a slightly different perspective.

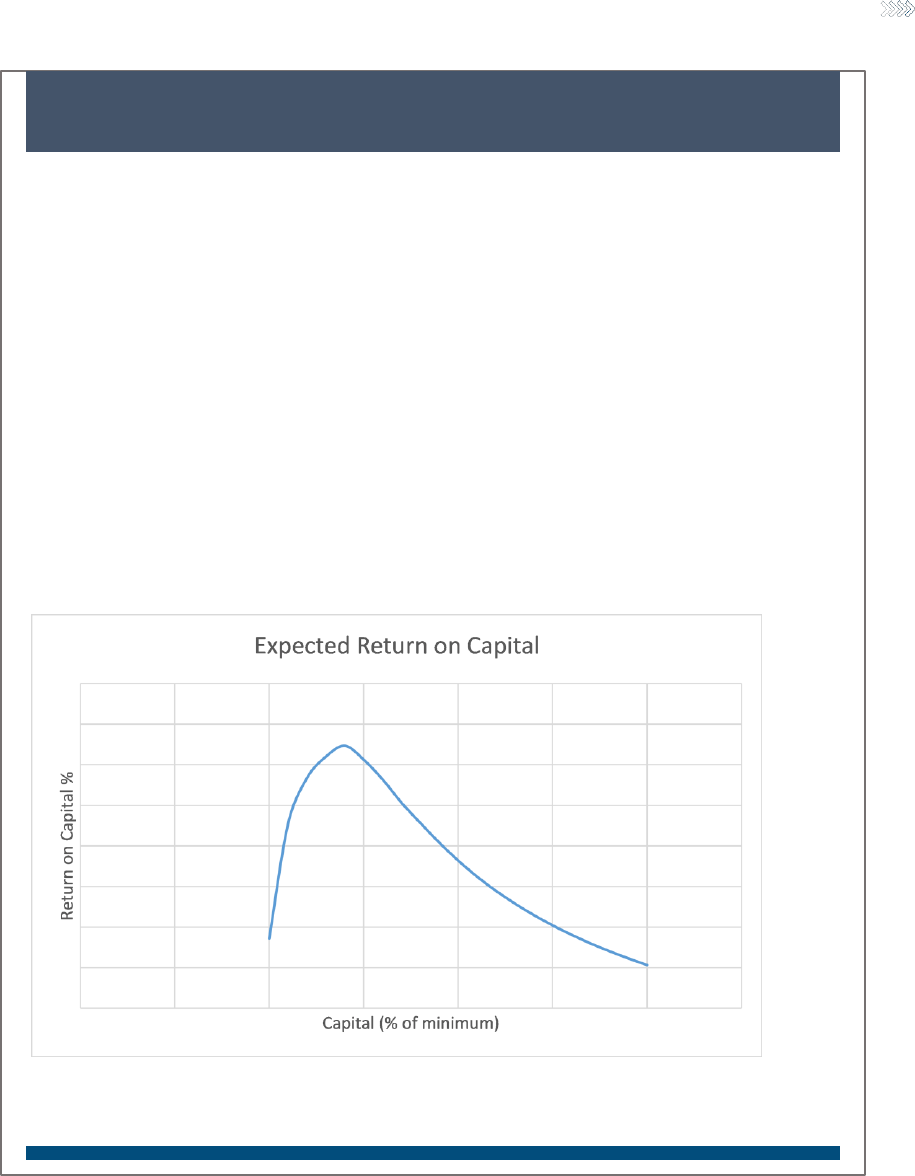

Optimizing the expected return on capital

A common belief is that holding less capital increases the return on capital by reducing the denominator of the

equation. However, if a company holds only the regulatory prescribed minimum, even mildly adverse

performance may cause them to breach this requirement over the next year and suffer the associated

frictional costs and loss to franchise value. These costs affect the numerator of the return on capital equation.

Many other cases of these costs arise in practice. Similarly, holding additional capital may increase the

franchise value by attracting a greater amount of profitable new business

Therefore the optimal return on capital is achieved by simultaneously limiting the probability and severity of

these costs while not holding excess levels of capital above those required for the smooth operation of the

business.

A stylized example is given below.

11

© 2016 Society of Actuaries

2.3.5 For whom is the EC calculation performed?

Economic capital is the amount of capital required by a company to ensure that certain goals are met with a high

degree of certainty, under a realistic assessment of future risk.

The specific goals, certainty and timeframe depend on the primary stakeholder of interest. This leads to various flavors

of economic capital: Internal economic capital is the type which we will concentrate on for the majority of this report.

This is the assessment of the capital required under the company’s own internal risk assessment, valuation

methodology, objectives, etc. The most important feature of this type of assessment is that the model reflects the

company’s own views business plan and planned management actions. In some publications, the terms “risk capital” or

“internal capital” would be used as an appropriate substitute.

Regulatory economic capital is calculated primarily for a regulator. These bodies’ have the objective of ensuring the

conformity, simplicity and prudence of the model used. They are therefore likely to be more prescriptive in the

application of rules and most interested in the implications to policyholders. Under a prescribed set of economic

assumptions and valuation / projection rules. We classify the Solvency II standard formula and the NAIC Risk Based

Capital regime as broadly falling under this category. We therefore consider a Solvency II internal model to be a mix of

regulatory and internal economic capital assessment since the rules for valuation and risk measurement are strictly

defined and the economic risk assessment, although nominally internal, is heavily guided by regulators.

12

© 2016 Society of Actuaries

Section 3: EC Methodology and Modeling

3.1 Main Considerations

At its core, economic capital is about projecting a future evolution of the world and the potential impact of adverse

events on business performance, including both the associated costs and the resulting actions taken. The fundamental

question to answer is then how much money would be required today to survive some adversity.

A number of challenges underlie this question, most notably the fact that the underlying variables are difficult to

observe and are altered by actions undertaken over time. This introduces subjective elements into the development of

economic capital models and raises questions about the ability to codify a single global framework, leading many

practitioners to embrace a variety of models that can be built to reflect varying views. Some important areas for

consideration in developing economic capital models are listed and discussed below:

The objectives of the company

The risk drivers that will be used

The risk evolutions that will be considered

Management and policyholder actions assumed

The time horizon for projection

The valuation metrics used

The statistical risk measure

The confidence level

The inclusion of new business

A number of these choices are significant both on their own and in the context of the other choices made. The

following sections discuss each in turn.

3.1.1 Setting objectives

Developing a modelling framework involves asking the questions, “What objectives will define the capital calculation?”

and, “How to reflect these objectives in our capital model?”

These objectives and measures should reflect the real-world behaviors of the company, the mode of possible failure

and the business plan that they follow.

For example, many insurers with long term liabilities follow a buy-and-hold strategy for corporate bond investment

with cash flows used to meet liability payments. Under this strategy the risk to policyholders is that asset cash flows are

insufficient. This includes the impact of possible defaults, rebalancing of the portfolio, re-investment of net proceeds

and potential forced sales to meet policy liability payments or other liquidity requirements. A model that reflects these

risks realistically may choose a cash flow measure as the primary objective and therefore use a long-term, real world

runoff model to measure the primary capital requirement, motivated by the belief that policyholders are better

protected in this way.

Conversely, a company may have a similar set of liability payments but actively hedge market exposures or plan to sell

or hedge risky assets under stress to de-risk and maintain solvency. In this case market risk is of primary importance

and a market-consistent measure is of primary importance. For example the cost of matching risk-free cash flows in 1

year can be calculated, as well as the cost of re-insuring mortality risk etc. In any case some residual risk will remain –

for example, expenses and un-hedgeable policyholder risk. This risk will remain on the insurer’s balance sheet and the

capital available should cover these risks after the cost of de-risking is accounted for.

Other models propose a cost of transfer model. In this case the model tries to estimate the cost of transferring the

assets and liabilities to a willing third party. If this transfer happens then it is usually assumed that the transfer happens

at market- and market-consistent values plus a cost of capital to reflect the third party’s required return on the extra

capital they would need to hold for any remaining risks.

13

© 2016 Society of Actuaries

3.1.2 Risk drivers

Life insurance companies are subject to a large number of risks. On an individual basis, these risks could include the life

or death of each policy and the performance of each security invested in. As building a model is necessarily a

simplification of reality, the dimensionality of the problem must be reduced to create a representation of reality that is

tractable, understandable and useful in measuring and managing risks. There is some art involved in reducing a highly

complex system to the smallest number of risk factors without excluding features important to the current and future

risk exposures of the entity.

The process involves a combination of grouping and classifying risk families, identifying underlying processes, collapsing

highly correlated risks, grouping exposures into indices, and imposing a structural view of the risk’s dynamics based on

our understanding of its nature. Historical data analysis, expert judgement, academic research and peer benchmarking

all play a part in this process. A balance between model complexity, tractability and usefulness must govern the

selection of risk drivers.

For example, when determining the number of interest rate factors to be used in a 1 year stress model, a modeler will

typically analyze historical data by exploratory methods such as principal components analysis, determining the

number of underlying factors that explain a high percentage of the changes in market yield curves. Typically 2 or 3

factors are found to represent a suitably high percentage of the underlying market risk. They should then consider how

these factors relate to their underlying asset-liability position. For example, the third factor may explain only 2% of the

change in the overall curve but may drive most of the risk in the net value of assets position due to the complex cash

flow profile of assets and liabilities. In this case at least the first 3 factors should be retained as relevant for the EC

calculation. After this analysis, more complex models may be considered that integrate economic structure and logic

into the interest rate model, while retaining the required model complexity.

This simplification of the real world should represent the insurer’s views of how each risk behaves as well as the

underlying dynamics. Then, once these risks are combined into a larger model for measuring the effect that they have

on the solvency of the organization, the model should both mirror expectations and provide new insight into the

complex risk effects, enabling deeper investigations into the dynamics of the enterprise. As each organization is unique

in its business model, product exposure and risk management practices, it is therefore expected that each organization

may have its own unique set of risk factors – retaining the features that are important to the company and simplifying

or eliminating others.

3.1.3 Risk evolutions

After determining the risk factors to include in the EC model, the next step is to develop stresses of these risk factors

and test their effect on the company. This is done through various combinations of stress and scenario testing,

stochastic modelling or historic data analysis.

Stress and scenario testing is common in risk models. These are generally hand-crafted scenarios of the evolution of

risk, formulated by developing a narrative around the scenario – such as a global market crash, natural disasters or

historic periods of market turbulence. These are useful what-if analyses that give insight into the dynamics of the

business and aid our thinking, planning and decision making.

However the use of a small number of scenarios has many limitations. It is very difficult to assign probabilities to these

scenarios and therefore to give an overall confidence for any capital adequacy result derived from them. Further, it is

difficult to check whether the economic scenarios being considered are actually the most important ones for the

business. For example, a smaller equity shock, coupled with a larger interest rate move, may be both more likely and

more severe in relation to profits than a market crash scenario. The ability to test only a small number of scenarios is

especially limiting where exposures are highly geared, with large offsetting asset and liability positions, or in the

presence of complex hedging programs.

Using a stochastic set of scenarios overcomes this challenge. Assigning a joint distribution to the risk factors and then

simulating random outcomes from this distribution produces scenarios that display a wide range of characteristics and

combinations. Passing these scenarios through a model of the enterprise enables an assessment of the risks for the

14

© 2016 Society of Actuaries

business under many different future evolutions of the world, giving a more accurate view of which scenarios pose the

most risk.

In any method of developing scenarios, there are many human and data biases involved, such as a tendency to ignore

or discount scenarios that deviate from past experience and exclude data from “non-representative” economies. This

manifests clearly in hand-picked scenarios. Because a stochastic model includes more scenarios, more diverse events

and more extreme scenarios in its random outcomes some of these biases and blind-spots can be avoided. However,

another danger lies in the calibration of risk models related to limited imagination and understanding of the world. This

applies equally to deterministic, or stochastic models. Indeed, stochastic models may be seen as more dangerous in

this sense because the assumptions and limitations of the models are more difficult to communicate and require a

greater time commitment to fully understand.

3.1.4 Management and policyholder actions

Management actions may be important to include in the EC model, as they could significantly affect the level of capital

required. They should be as realistic as possible to reflect the actual actions that would be taken by management, both

in benign and extreme market conditions, as it is particularly these actions that will dictate the losses experienced by

the company in the scenarios that drive the required capital.

The management actions assumed in the model should, however be limited to those documented and approved at the

appropriate oversight level. It would be counter-productive, for example to assume in the model that management will

dispose of equity holdings after a market crash if this is not the intention. Such an assumption would lead the company

to underestimate the risk borne and the capital required to support the stated business plan.

Conversely, if risk mitigation strategies are in place which would lead to a reduction in required capital (e.g. dynamic

hedging strategies on VA business), these should not be omitted in the interest of simplicity or prudence. The presence

of these actions will affect the riskiness of each business unit and the diversification of risk between them. Extra

prudence in the measurement of risk or allocation of capital for these products will have the effect of reducing their

risk adjusted return and ultimately lead to sub-optimal decisions. The willingness to commit to management actions is

therefore related to the return on capital. Executing de-risking strategies as conditions deteriorate may involve selling

when markets are down and buying again as they rise, thus resulting in losses. Dynamic hedging is a prime example of

this, but taking out additional reinsurance as a pandemic event unfolds would have similar consequences. Thus, the

presence of management actions in the EC framework can lead to both lower capital and lower returns.

The requirement for only fully approved and documented risk mitigation strategies to be included in the EC model is

often at odds with the need for flexibility and the exercise of context-specific professional judgement – having an

approved rule in place and included within a regulatory EC model could limit the ability of management to exercise

their best discretion when those circumstances appear. In the right environment, this discussion of economic

circumstances and resulting actions can lead to fruitful results – producing a view of EC under a variety of assumptions,

including a minimum set of management actions and an optimal quantitative, efficient-markets view would promote

valuable discussion and should ultimately lead to both enhanced strategic decisions and capital efficiency. In this

process, scenario specific rules chosen to reduce or optimize the level of capital required can be a valuable input to

managements risk contingency planning and improve the speed and quality of reactions to extreme events as they

unfold.

Where extensive reliance on management actions is made, the economic model and assumptions should be realistic

enough to allow the complexity of the management actions to be faithfully modelled, including their possible pitfalls

and limitations.

15

© 2016 Society of Actuaries

3.1.5 The time horizon

After determining what to project, the next question is how long to project it. Other things being equal, a longer

projection horizon should lead to a more conservative assessment of capital (using the same percentiles, accounting

convention and including intermediate assessments).

Often the time horizon chosen says less about how long the company will remain well capitalized and more about the

valuation metrics used, management actions assumed and business planning horizon.

One approach is to project forward for the lifetime of all business on the books. This is theoretically appealing, as it

matches the long term nature of typical life insurance policies. The risk profile of certain types of business may change

significantly in the future too. For example as rider benefits are taken up or returns locked in, an existing block of

business may naturally become riskier without any change to risk management policy or practice. Using a longer time

horizon can help ensure that the capital held is appropriate to cover the business through this evolution.

In reality, however, the choice of a time horizon is usually driven by the type of accounting measures used, the

business planning horizon and the risk mitigation strategies undertaken or planned. Some considerations for choosing

the time horizon are:

Where only cash flows are used without intermediate or terminal valuation, is a full runoff of the business

required?

Alignment of the business planning period and the EC projection period allows the projection to have a basis in

more formalized business plans, which helps management with the alignment of risk appetite to the levels of

economic capital required. This alignment would be difficult over a longer time horizon.

Considerations of the time horizon over which risk mitigation actions would or could be taken should influence the

choice of time horizon. For example, if all risks are fully hedgeable in capital markets in a short time horizon and a

market consistent liability measure is used, then a short projection period maybe sufficient to describe the risks

faced. In contrast, if a valuation measure is used that does not recognize losses for a number of years (like some

book value accounting systems), then a longer projection period which allows the full evolution of risks to unfold

may be needed.

3.1.6 Valuation metric for intermediate valuations

Where EC models use a valuation metric for assessment of intermediate value of assets required, there are a number

of alternatives that are possible. For example, a market consistent measure may be used to value assets and liabilities

consistently with the market prices of assets and derivatives. Many insurers use a “market based” measure of value in

addition to or instead of this stricter market consistent measure. This type of valuation typically attempts to account

for the company’s own view of the economic value of the value of assets and liabilities by making adjustments to

market discount rates, implied volatilities etc. to reflect the unique features and business plans of the company. For

example, where the assets backing a particular liability portfolio are very actively traded or hedged in the market, it is

usual to use pure market consistent techniques to value both. However where liabilities are long term and the assets

are considered to be hold-to-maturity, it is common to adjust either asset or liability valuations to diverge from strict

market-consistent pricing.

Other valuation measures may be used. For example accounting measures which take assets at book value and try to

discount liabilities on a consistent basis are also sometimes used as intermediate measures in practice. The precise

valuation metric used should be linked to the objectives of the economic capital model. Rather than being dogmatic

about the exact definition of value or capital, we believe that the size of, and change in the capital measures over time,

are often the most useful outputs from an EC model.

Other intermediate metrics that may be measured in the economic capital projection include statutory reporting

requirements like regulatory capital or insurance reserves. More complex capital models may integrate multiple

16

© 2016 Society of Actuaries

objectives into the calculation. Section 6.3 introduces this idea in the context of multiple valuation measures within a

risk appetite framework.

3.1.7 The statistical risk measure

The choice of statistical risk measure is an important choice for the model design. While a line-up of statistical risk

measures are available, the two most common in use are value-at-risk (VaR) and conditional tail expectation (CTE). CTE

is also known as tail value-at-risk (TVaR).

The VaR measure is a straightforward percentile of the loss that an insurance company may experience. It prescribed in

the Solvency II standard formula and almost universally adopted in companies using internal models. Alternative

approaches are permitted within internal models but only if offering greater security than the VaR metric. While VaR

has a number of advantages (see end of this section), it does have some shortfalls. Technically speaking, it is not a

coherent

2

risk measure – which is to say that it does not satisfy a number of desirable properties of risk measures. Most

important among these is that it does not consider the size of losses in excess of the measured percentile. This means

that a company may be exposed to low probability events that would cause losses only slightly more than their

available assets or at a scale that could devastate a national or global financial system - without any difference in their

capital requirement. This feature is a clear incentive to take on low probability, high severity risks which give a higher

return on capital profile in a VaR based EC model. These are in many ways the most dangerous risks because of the

difficulty in estimating their probability of occurrence.

More mathematically, the VaR measure in general lacks the property of sub-additivity, meaning that in some cases this

measure can fail to reward diversification of risks, particularly in the presence of events with low probability and high

severity

3

. This is problematic both in theory and in practice, limiting the ability to allocate risk to the business units,

products and sources from which it arises.

These limitations are solved by using a CTE metric, measured as the probability weighted average of possible losses in

excess of a given percentile. This corrects the failure of VaR to consider and allocate capital to extreme risks. It also

allows better recognition and allocation of diversification benefits.

This improvement in theoretical coherence comes at a cost for practical implementation. There is greater difficulty in

explaining the measure to a non-technical audience, or sometimes even to a technical audience. In addition, a CTE is

more difficult to handle numerically – for accurate assessment it is required to measure the whole tail of the risk

distribution and the effect on the company in all extreme circumstances. Any model limitations or quick

approximations which could be acceptable in a VaR model could end up unintentionally driving the capital result under

a CTE measure.

3.1.8 The confidence level

The aim of insurance regulation and capital is not to have a zero failure system, as the only way to ensure this would be

to avoid all risk entirely. Instead, the objective is to reduce the likelihood of failures up to the point where the marginal

cost of additional failure prevention exceeds the additional benefit of safety. Some compromises may be necessary in

this decision, as different stakeholders may have different tolerances for failure.

Risk appetite statements and fundamental corporate philosophies should ultimately drive the decision of selecting a

confidence level by contemplating the vision for what the company aims to achieve and the implications of succeeding

or failing in this mission. Translating this from an abstract exercise into a tangible decision requires an understanding of

2

Artzner, “Coherent Measures of Risk” https://people.math.ethz.ch/~delbaen/ftp/preprints/CoherentMF.pdf

17

© 2016 Society of Actuaries

the likelihood and severity of risks; therefore, EC models play an important, and often iterative, role in informing this

decision.

Where a multi-year measure is used, the confidence used should (other things being equal) reasonably be lower

because it relates to a probability of ruin over a longer horizon. To put it another way, providing the same level of

protection against company failure over a longer horizon requires more resources than providing against company

failure over a shorter horizon. This further highlights the important relationship between modeling assumptions and

modeling implementation.

3.1.9 New business

Including new business in the projection may be important, especially for longer term models and companies writing

significant volumes. The reason relates to the tendency of management to write new business up to their comfortable

capitalization levels. For example, in good times the business may generate a high level of surplus capital. It would then

be natural to write new business or make extra distributions to policyholders or shareholders to enhance the return on

capital. If these features are not included in the long term projection these scenarios would tend to never see ruin,

whereas if a more realistic path were incorporated, they would be as likely as other scenarios to ruin because risk

would be increased to the point where they were as risky as average paths. This feature may have the effect of

significantly understating risk in a runoff model. Over time, however, new business should also increase available

capital in scenarios where it is written profitably. Achieving a sufficiently realistic representation within a runoff EC

model is needed.

A 1 year or intermediate term model aligned with the business planning horizon is more tractable in this context

because it can point to an explicit business plan and agreed actions for the management of the business. There is less

uncertainty about future management plans, insurance regulations, market regimes etc.

3.1.10 Putting it all together

Once all the above factors are considered, constructing an economic capital model is a task of representing the views

and needs of the company in a coherent, realistic and parsimonious way.

In practice, two broad methodologies have emerged as the most common: a liability runoff approach and a finite risk

horizon approach. Most insurers calculating EC today do so following one (or sometimes both) of these approaches.

While specific definitions and calculation approaches can vary widely, the two approaches can broadly be defined as

follows:

The liability runoff approach, where EC represents the current market value of assets required to pay all future

policyholder benefits, and associated expenses, at the chosen security level (expressed on a VaR or CTE basis), less

the current value of the liabilities (typically defined on a mean or best estimate basis).

The finite risk horizon approach, where EC represents the current market value of assets required to ensure that

the value of liabilities (typically market consistent), can be covered at a finite point in the future (typically one

year), at the chosen security level, less the current value of the liabilities.

3.2 The Liability Runoff Approach

While there are a number of approaches to implementation, the liability runoff approach is typically performed using a

stochastic simulation method as follows:

A set of (typically 1,000 or more) future scenarios for the runoff of the business is defined. The scenarios include

specifications for economic and demographic conditions, including risk drivers such as interest rate scenarios and

18

© 2016 Society of Actuaries

asset default rates. Mortality levels and other insurance risk drivers may also be included in the stochastic

scenario generation process.

The scenario distribution is a realistic assessment of the future risks and returns expected on each asset class or

risk driver.

Projected asset and liability cash flows are developed for each scenario, including realistic management actions,

product rules and policyholder behavior.

Intermediate valuations or required reserves for each time period and scenario are calculated (as required by the

capital definition)

Under each scenario, the level of assets required at the beginning of the scenario to satisfy all obligations through

to the end of the projection is determined.

These obligations may include paying policyholder cash flows, debt payments and dividends; having sufficient

funds available to meet regulatory reserve or capital requirements; having sufficient funds available to maintain a

minimum credit rating or other management objectives.

Assessing many of these intermediate objectives implies a nested stochastic calculation within the EC model. For

example, assessing a reserve which is calculated as a runoff CTE within the runoff EC model may require 1,000

scenarios repeated at each projection year.

The level of required assets includes consideration of the investment returns earned on those assets (including

investment strategy and re-investment considerations). This is equivalent to discounting future excess obligations

at the return earned on the excess capital assets.

The level of “required assets” for all scenarios is then ranked to form a distribution.

EC is defined by applying the chosen risk metric (e.g., VaR or CTE) to this distribution of total required asset levels

and deducting the current value of the liabilities, measured on the selected basis (typically mean or best

estimate).

Insurers using a runoff approach are increasingly pursuing the development of fully integrated stochastic models, in

which demographic and economic assumptions vary stochastically within the same model. This has distinct advantages

for capturing risk interactions within the EC model. For example, scenarios with high longevity and low interest or

investment returns will lead to a capital requirement in excess of the sum of the requirements should either of these

events occur in the scenario individually. This interaction drives the capital result. This level of integration makes use of

relatively new models of the stochastic evolution of insurance risks such as stochastic mortality and morbidity models

or predictive models for policyholder behavior

4

. These stochastic models of insurance risk are a significant

improvement on older approaches for including insurance risk in runoff models. Under these approaches, a stress

would generally be conducted for mortality rates (for example) at time 0 and the effect on insurers’ liability value

determined. This static, T0 stress would then need to be combined with the runoff risk calculation in a necessarily

approximate way.

The liability valuation basis used to define EC under the runoff approach can vary, with a different valuation basis

resulting in a different split between liabilities and EC (but the same level of total “required assets”). In practice, mean

or best estimate liability valuation bases are popular choices of liability valuation basis. Note that the most important

measure for the purpose of policyholder protection is the required assets; the split of required assets between

liabilities and EC is unimportant from this perspective, although will be relevant if EC is to be used in other contexts.

A few different variations of the liability runoff approach are observed in practice, in particular the inclusion of

requirements to meet interim solvency measures during the runoff. In its basic form, the liability runoff approach

considers the asset level currently required to pay all claims and expenses throughout the runoff period, and does not

explicitly take into account solvency levels at interim dates. Without any checks of interim solvency, there is an implicit

assumption that adverse experience in earlier time periods can be offset against positive experience in later time

periods. Put another way, the methodology allows the insurer to become technically insolvent in interim years

providing it rebounds before the end of the runoff. This ignores the potential impact of regulatory intervention or

reputational damage at times of technical insolvency.

4

Cainrs, Blake, Dowd Modelling and Management of Mortality Risk: A Review

19

© 2016 Society of Actuaries

Alternatively, the liability runoff approach can incorporate a check on solvency at interim points during the runoff. This

raises the additional questions as to what measure of interim solvency should be used and how frequently it should be

assessed. If the economic principles underlying the methodology are to be maintained, an economic basis of interim

solvency would be required, which can be computationally intensive.

3.3 The Finite Risk Horizon Approach

The finite risk horizon approach is typically performed as follows:

An economic balance sheet is developed as of the valuation date. The difference between the value of assets and

value of liabilities gives the economic value of net assets, i.e., the available capital at the valuation date measured

on an economic basis.

For a number of real world scenarios, assets and liabilities are projected forward over the length of the risk

horizon (e.g., one year), at which point a projected economic balance sheet is developed. The resulting projected

economic value of net assets (positive or negative) is then discounted to the valuation date using the projected

earned investment return over the year in that scenario.

A negative discounted value quantifies the additional initial asset value the insurer needs to hold to ensure it

remains solvent on an economic basis at the end of the year under that scenario. A positive discounted value

quantifies the excess initial asset value over the amount needed to ensure solvency on an economic basis at the

end of the year. The discounted value (of the projected economic value of net assets) is therefore subtracted from

the value of assets at the valuation date to give the required assets for that scenario.

As with the runoff approach, the finite risk horizon approach can be implemented using stochastic simulation. The

steps described above are performed for a large number of real world scenariosperhaps 100,000 or more given the

higher security levels that would typically be used under shorter risk horizons. This gives a distribution of required

assets by scenario, from which the overall level of required assets can be determined (i.e., by calculating the chosen

risk measure at the target confidence level). The EC requirement is then determined by deducting the initial value of

the liabilities from the required assets.

It is also common to implement the finite risk horizon approach using stress tests as an approximation to stochastic

simulation. This has tended to be more common for business with significant financial options and guarantees where

the market-consistent value of liabilities requires the use of a risk neutral stochastic valuation. To implement a

stochastic risk horizon approach to EC would therefore lead to computationally challenging “stochastic on stochastic”

calculations (although proxy modeling techniques have now been developed to overcome this, as discussed in Section

7).

With a stress testing approach to implementation, the full, accurate multi-dimensional distribution of required capital

described is not developed. Rather a limited number of stress scenarios are run, where the scenarios have each been

calibrated to the chosen security level. Scenarios are chosen to explore each of the key risks, and the capital results for

each risk are typically combined using a correlation matrix.

It is important to note that even under the finite risk horizon approach, a runoff projection is still required, since a

terminal value of liabilities at the end of the risk horizon is needed. Future uncertainty surrounding the risk beyond the

risk horizon is captured within the value of the liabilities at the end of the year. This may consist of both the time value

of options and guarantees as well as the cost of capital required to support that uncertainty.

While the finite risk horizon approach originated with the banking industry’s use of short term market consistent

calculations, it has also been adopted by many European multinational insurers and their global subsidiaries, which

include many significant North American insurers. It is now being adopted as the basis for insurer solvency regulation

across Europe under Solvency II. A number of large North American insurers are also adopting this approach to EC

calculations.

20

© 2016 Society of Actuaries

Due to the common use of a mark-to-market balance sheet, the finite risk horizon approach can be sensitive to market

conditions and prices. Some consider that this results in market movements, particularly those driven by changes in

market sentiment, having undue influence in setting capital requirements, given the long-term nature of a life

insurance business. Others see the link to market prices as an advantage, both because they reveal the true market

volatility of the balance sheet and because these prices may be very relevant when assessing risk management options

available in adverse scenarios.

3.3.1 Market consistent approach for terminal valuation

Market consistent or similar valuation methodologies have become the most common method of allowing for terminal

balance sheet valuation globally. This adoption has been largely driven by European regulators who have mandated its

use in Solvency II capital calculations (although adjustments are allowed that make the result closer to market-based

than market consistent).

The use of a terminal valuation methodology in an EC perspective implies it can be used as the basis for securing the

payment of benefits to policyholders or capturing a view of the liability. Any measure that does not realistically relate

to these objectives is of little practical use. This does not prevent the use of multiple valuation metrics for different

other purposes in the model, for example, statutory reserves may serve as intermediate tests within a projection that

could trigger certain regulatory or management actions or require balance sheet strengthening. However, the ultimate

valuation metric that drives the capital requirement must relate to the ability to pay claims.

A market-consistent measure has many theoretical virtues and addresses many of the issues with a runoff approach,

but some substantial questions and issues remain. For background, a brief summary of market consistent valuation

practices is included below for the purpose of highlighting elements important to the EC calculation.

5

In a market consistent valuation, the insurer aims to value liabilities in a way that is consistent with market prices. This

means that:

Future cash flows that are certain or guaranteed are discounted at market risk-free interest rates. While there is

some debate between whether treasury or swap rates should form the basis of this risk free discount rate, this

debate is beyond the scope of this paper.

Where liabilities have contingent cash flows such as embedded options or variable guarantee features, their value

is included in the liability valuation in a way that is consistent with the market prices of similar options or using

similar valuation methods.

Assets are accounted for at market observed prices (or using a mark-to-model basis where prices are not readily

observable).

There is an allowance for the cost of capital, for non-hedgeable risks, that a willing buyer would need to hold to

take on the liabilities.

In theory this valuation basis gives a valuation of an insurer that is consistent with market prices and therefore gives a

value close to that which a willing buyer and seller in the market would transfer the assets and liabilities of the

company in an arms-length transaction. This should also give a valuation for assets and liabilities which can be “locked-

in” through risk transfer or capital markets transactions. For example, bonds or swaps should be able to be purchased

to exactly match guaranteed cash flows; derivatives traded that exactly pay for options offered to policyholders;

reinsurance purchased that removes the risk of adverse mortality and morbidity experience etc. Some risks however

remain, such as policyholder behavior, for which there are a very limited set of willing buyers.

The benefit of this argument for EC purposes is that, when considering risk to the market consistent balance sheet over

some time period (e.g. 1 year), the insurer should be able to completely de-risk the balance sheet at that point. This

means there would be no need to consider future economic risk (because there would be none, and any risk would be

5

Wilson, Value and Capital Management: A Handbook for the Finance and Risk Functions of Financial Institutions

21

© 2016 Society of Actuaries

assumed voluntarily or at the discretion of the regulator who would be in control at that point). This also means that

the terminal value measure is aligned with actions that can or would be taken in the market to mitigate risk and protect

the company in adverse circumstances.

There are, however, issues with this approach. When looking at market based rates and prices, it is usual to analyze

frequently traded assets and liquid derivatives. While these are more standardized, traded and compared, they are

fundamentally different from insurance liabilities. This has led to concern from many insurance companies who argue

that this valuation measure does not take account of the economics of long term insurance contracts. In particular, the

insurance company has use of the policyholder funds for long periods of time with no obligation to return it without

penalty (or very low likelihood of significant outflows due to policyholder behavior). Over this time the shareholders

benefit from the investment returns earned on the backing assets. This long term funding and the option to change

investment strategy have value to the company. However, a formal, consistent and broadly agreed framework for its

measurement has not been developed – some argue for an addition of a liquidity premium to reflect asset or liability

illiquidity; others for a recognition of the excess returns that are expected to be earned by holding the assets over the

long term. Whatever the underlying theory, the mechanism of the adjustment is typically represented by an addition to

the risk free rate for discounting liability cash flows.

Conversely, holding life insurance liabilities attracts a regulatory (and economic) capital requirement. The cost of

holding this capital against risks that cannot be perfectly hedged is often included in valuations (both base and

stressed) for economic capital purposes. In this way, both the benefit and cost of the specific business environment can

be reflected in the valuation measure.

In addition to identifying the rate at which cash flows should be discounted, there are issues related to the

completeness of markets for benchmarking liabilities. For example, life insurers typically have liabilities that go out for

many years longer than the assets available for benchmarking. Even where swap rates are quoted for the full term of

the liabilities, there are questions by many of the validity of these quoted rates or the willingness of banks to transact

at these prices in sizeable volumes. Some models address this through the liquidity premium or comparable

adjustments to risk-free rates.

3.4 Contrasting runoff and finite horizon approaches

A runoff calculation answers the same fundamental question as a one-year model—identifying the level of assets

required to cover policyholder benefits with some degree of security. The first investigates a runoff of the business,

while the second looks at transfers to a third party. These each have strengths and weaknesses from an EC perspective.

A runoff approach, taking into account the realistic evolution of the business, can give a pure view of the dynamics of

the risks and is consistent with the long term nature of the insurance operations in question. It is not complicated by

market movements in assets and prices which may fluctuate without much impact on the actual ability to pay claims. In

this sense it cuts to the heart of the problem.

On the other hand, a runoff approach with no intermediate valuation metrics may become disconnected from financial

market conditions. For example, in times of stressed market credit spreads, a runoff model may not show any increase

in risk to policyholders because defaults are assumed to remain relatively low and reinvestment at higher future

spreads increases returns. However, in this case it would not be possible to sell the bonds and move to a safer

investment position because this would realize the investment loss which may be bigger than the required capital level.

Similar arguments hold where reinsurance against non-market risks or derivatives used to hedge market risks are

considered. This means that a pure runoff approach is only appropriate where the management action model used is

realistic and explicitly tied to a formal business strategy. For example, a model where assets are assumed to be held till

maturity will not accurately reflect the risks inherent in an actively traded bond portfolio. Some may argue that this is

not the intent of the EC model, but to the extent that the company can become distressed and unable to trade or de-

risk or re-finance their way out of difficulty at market prices, these short term dislocations can affect the long term

health of the company and their ability to ultimately pay claims.

22

© 2016 Society of Actuaries

A one-year model, at least when implemented using market consistent valuations, is inherently more aligned with

financial markets and therefore with market-based risk mitigation strategies that can be or are being undertaken. This

may include financial derivatives, reinsurance or securitization transactions. This alignment is also beneficial from a

transparency and comparability point of view. The disadvantage being that this strict adherence to market principles

may come at the cost of consistency with long term insurance-specific features or the actual business model of the

insurer.

To bridge the gap between one year and run-off views, adjustments have been made in both directions. Market-based

valuation approaches (particularly in Solvency II) have employed an addition to the risk-free discount rate that varies

with the economic environment. For example, when credit spreads are high, the spread adjustment increases. These

adjustments are applicable only for certain classes of business.

This spread adjustment attempts to correct the market-consistent regime in a way that is cognizant of the particular

type of insurance portfolio under consideration. The effect is to assume that the insurer is only exposed to changes in

default or downgrade expectations (measured cumulatively over the life of the portfolio) on credit-risky bonds and that

changes in bond prices or spreads from other sources (like changes in actual or perceived liquidity; changes in risk

premium demanded by investors; changes in markets’ default expectations etc.) are offset by the adjustment made on

the liability discounting side. The end results is a set of assumptions (and an effect) very similar to the starting point of

a runoff cash flow model – that the company is exposed to the risk of cumulative defaults but that changes in the

market prices of assets or spreads are not important for the company’s ability to pay claims.

Under either regime, the company’s expectation of future (average and worst case) defaults can be dependent on

market observed values – to the extent that the company believes that market prices reliably embed expectations of

future performance. Viewed another way, both the adjusted market-based and runoff cash flow methodologies embed

strong assumptions about the mean reversion of asset returns after extreme market events.

This mean reversion theme is present in other senses too. A runoff model will typically make an assumption about the

expected level of yield curves based on historic experience that is different from the future level implied by the long

end of the initial market yield curve. Whereas the Solvency II adjusted market-based model incorporates these effects

by ignoring parts of the initial yield curve and extrapolating quickly to real world expectations. The effects of both are

to introduce a type of mean reversion into the measurement of capital that diverge strict short term market pricing or

market implied risk levels.

The nature of this mean reversion assumption is highly subjective and difficult to reliably estimate. The evidence for

these effects is also mixed and dependent on the particular time periods, asset types and economies included.

Other than these important effects, the models behave in different ways. A runoff model looks at the tail of the

outcomes over time whereas a one-year model looks at the average after a big stress and change in expectations.

These approaches naturally vary in the levels of capital they output and in the sensitivity of the capital result to changes

in economic conditions. From a consistency sense, where companies have a strong view about long term investment

and mean reversion of returns, the runoff model is a more natural model choice, allowing the user to directly input

their assumptions and observe the result based on the full dynamics of the projection, whereas the market based

adjustments are more difficult to estimate and often derived by equating to the result of a runoff projection with

limiting assumptions about future actions.

An additional consideration is the degree to which the capital estimates produced by these two types of models vary

with changes in market conditions and therefore promote or defend against cyclicality in global capital markets. Pure

market consistent one-year regimes may promote more cyclical investment markets if companies exposed to these

regimes and therefore larger swings in capital ratios are encouraged to sell risky assets more quickly in times of

distress. When one-year or runoff cash flow regimes are compared, the degree of cyclicality varies and is inherently

controlled by the degree of mean reversion or equivalent market adjustments assumed.

3.5 Risk Aggregation

23

© 2016 Society of Actuaries

3.5.1 Overview

Risk aggregation refers to the process by which risk exposures or capital requirements at lower levels (e.g., individual

risks, business units, or geographic regions) are consolidated to higher levels (e.g., the enterprise total or various

subtotals). Typically the required EC result for the total enterprise is less than the sum of the individual risk exposures

due to diversification benefits, which arise from imperfect correlation between risks—loosely speaking, the likelihood

of two extreme events occurring simultaneously is generally lower than the likelihood of each one occurring

individually. A special case of this is offsetting risks, when risks are negatively correlated. For example, an insurer who

writes both life insurance (negatively impacted by an increase in mortality) and payout annuities (positively impacted

by an increase in mortality) to similar classes of individuals will generally experience a reduction in overall mortality risk

exposure.

Diversification across distinct business portfolios is influenced by the relative shapes of the loss functions with respect

to risks. If loss functions are nonlinear—meaning the impact of a stress scenario grows at an increasing rate as the size

of the stress increases—then diversification ratios are generally lower under more extreme risk metrics because the

increasing contribution of the nonlinear variable has a greater influence on the total capital result. This impact on

aggregation generally becomes more pronounced as the loss function becomes steeper.

Although a range of aggregation techniques are used in practice, they can broadly be classified into two approaches.

3.5.2 The Flat Correlation Matrix Approach

Under the correlation matrix approach, standalone capital is calculated for individual risk factors—often by

deterministic stress testing at a targeted confidence level—and then aggregated by multiplying the capital results

through a correlation matrix using a formula similar to the following:

(3.1)

This can be generalized to multiple risks using standard matrix algebra:

(3.2)

Where C is a column vector of standalone capital amounts by risk, and M is a correlation matrix for those risks. Due to

the formulas involved, this approach is also referred to as “sum of squares aggregation” or the “variance-covariance

approach.”

The advantage of the correlation matrix approach is its ease of calculation; however, it has some limitations.

Correlation assumptions are often set by some combination of historical data or expert forecasts that analyze the