1

Mortgage Products

Home Possible Mortgage

The Freddie Mac Home Possible

®

situations. With Home Possible, we’re all for helping you capitalize on opportunities to meet the home

mortgage offers outstanding flexible to fit a variety of borrower

sources of funds.

Origination and Underwriting Requirements

Eligible property

types

•

Owner-occupied primary residences.

• Planned unit development.

• Condominiums.

•

Co-ops.

• Manufactured homes with additional requirements; see Single-Family Seller-Servicer Guide

(Guide)

Section 5703

.

Occupancy

•

Primary residences only.

• Non-occupying borrowers are permitted in accordance with Guide Section 4501.7(b) provided at least

one borrower occupies the mortgaged premises as a primary residence.

Eligible

mortgages

•

•

First lien mortgages that are fully amortizing.

• Conventional mortgages.

• Conforming and super conforming loan amounts.

• Fixed-rate mortgages.

• 5/5 and 5/6-month, 7/6-month, 10/6-month ARMs.

•

7/6-month, or 10/6-month ARMs.

• Community Land Trust mortgages originated in accordance with Guide Chapter 4502

• CHOICEHome

®

mortgages originated in accordance with Guide Section 5703.9

• CHOICERenovation

®

mortgages originated in accordance with Guide Chapter 4607

• GreenCHOICE

®

Mortgages originated in accordance with Guide Chapter 3401.30

Minimum

borrower

contribution

and reserves

•

No minimum contribution is required from borrower personal funds on a purchase transaction for a

1-unit property, regardless of LTV/TLTV/HTLTV. This includes manufactured homes.

• Loan Product Advisor

®

determines minimum reserve requirements.

• For manually underwritten mortgages, there is no minimum reserve amount required on a 1-unit

property.

Acceptable

sources of

funds for down

payment and

closing costs

•

Eligible sources of funds for down payment and closing costs include gifts, grants, cash-on-hand,

Affordable Seconds

®

, proceeds from an unsecured loan, sweat equity and Employee Assisted Housing

(EAH). For additional detail, refer to Guide Section 4501.10(c).

GO ALL IN > SF.FreddieMac.com/HomePossible

financing needs of very low- to low-income borrowers looking for low down payment options and flexible

Mortgages secured by manufactored homes must be fully amortizing fixed-rate mortgages or

Purchase and no cash-out refinance transactions.

2

Mortgage Products

GO ALL IN > SF.FreddieMac.com/HomePossible

Without

Affordable

Seconds

•

TLTV/HTLTV ratio less than or equal to 97%.

With Affordable

Seconds

•

Primary residences only.

Eligible

mortgages

• Eligible Affordable Seconds can provide 100% of the borrower’s down payment and could be used for

both down payment and closing costs.

•

•

The Affordable Second must be p

rovided by an agency under an established, ongoing, documented

• Regional Federal Home Loan Bank under one of its affordable housing programs.

• An employer through an Employer Assisted Housing (EAH) program.

• The Affordable Second may not be funded by the property seller or any other interested party t

o the

transaction.

Seconds is available

here

Maximum Ratios For 1-Unit Properties

Loan Type Maximum LTV Maximum TLTV Maximum HTLTV

Conforming

Fixed-rate 97% 105%* 97%

Fixed-rate with non-

occupying borrowers**

95% 105%* 95%

Adjustable-rate (ARM) 95% 95% 95%

Manufactured homes 95% 95% 95%

Super Conforming

Fixed-rate 95% 105%* 95%

ARM 95% 95% 95%

* With Affordable Seconds

®

** Ratios in this row are for mortgages with a Loan Product Advisor

®

Accept risk class. For manually underwritten loans, ratios are 90% LTV and 105% TLTV.

Borrower Income Requirements

•

•

Total annual qualifying income limit is 80% of area median income (AMI). Eligible borrowers include:

Freddie Mac offers two tools that make it easy to determine if your borrower meets the income requirements: Loan Product

Advisor determines product eligibility and our map-based Home Possible

®

Income & Property Eligibility tool allows you to look up

Home Possible income limits and property eligibility.

Secondary Financing

Ownership Of Other Properties

Any secondary financing that meets Freddie Mac requirements is allowed, including HELOCs, with a

TLTV allowed up to 105% with eligible Affordable Seconds when the first lien is a fixed-rate mortgage.

secondary financing or financial assistance program. Eligible providers include: federal agencies

municipal, state, county or local housing finance nonprofit organization.

For specific information on Affordable Seconds, refer to Guide Section 4204.1. A checklist for Affordable

secondary financing when the first lien is a fixed-rate mortgage.

The occupying borrowers must not have an ownership interest in more than two financed residential properties, including the subject

property, as of the note date, or for construction conversion and renovation mortgages, the effective date of permanent financing.

Very Low-Income Purchase (VLIP): borrower(s) whose qualifying income is less than or equal to 50% of AMI.

• Low-Income Purchase (LIP): borrower(s) whose qualifying income is greater than 50% and less than or equal to 80% of AMI.

•

®

Possible mortgage based on the property location and the borrowers' qualifying income.

Home Possible Income and Property Eligibility Tool

The Home Possible Income and Property Eligibility Tool can be used to verify if a borrower can qualify for a Freddie Mac Home

®

3

Mortgage Products

GO ALL IN > SF.FreddieMac.com/HomePossible

Mortgage Type for 1-Unit Properties Minimum Indicator Score

Fixed-rate mortgage that is a purchase transaction

1-unit ARM or a 1-unit no cash-out refinance mortgage

660

680

Manufactured home 680

See Guide Section 4501.8 (b) for additional underwriting requirements for manually underwritten mortgages.

2- to 4-Unit Properties

Loan Type Maximum LTV Maximum TLTV Maximum HTLTV

Conforming

and 2-unit ARM

95%

105%*

95%

3 and 4-unit ARMs 75%

105%*

75%

Super Conforming

85% 85% 85%

80% 80% 80%

75% 75% 75%

Credit Underwriting

• A borrower’s credit reputation is accept able if the Home Possible mortgage receives a risk class of Accept.

• Borrowers without credit scores may be underwritten for up to 95% LTV.

• A Home Possible mortgage that is a super conforming mortgage must receive a risk class of Accept.

• A Home Possible mortgage secured by a manufactured home must have a risk class of Accept if its term is greater than 20 years

and LTV/TLTV/HTLTV ratios are greater than 90% but less than 95%.

Credit Underwriting—Manually Underwritten Mortgages

• Rental income from a 1-2 unit primary residence can account for up to 30% of qualifying income.

• The person providing the rental income must have resided with the borrower for at least one year and will continue residing with

them in the new property.

• Rental income from a 1-unit primary residence must be provided by a person who:

• Is not obligated on the mortgage and does not have an ownership interest in the mortgaged premises.

• Is not the borrower’s spouse or domestic partner.

•

•

Evidence of residency.

• Documentation of receipt of rental income for at least nine of the past 12 months.

•

past year and intends to continue residing at the new residence for the foreseeable future.

• Rental income that meets the above requirements may be generated from an accessory unit. For more information see

Borrower statement affirming the source of rental income and the fact the renter has resided with the borrower for the

Guide Section 4501.9.

Requirements for 2- to 4-Unit Properties

Maximum Ratios For 2- To 4-Unit Properties

Affordable Second.

Must include in the loan file:

*A TLTV ratio up to 105% is permitted when secondary financing is an

2- to 4-unit fixed-rate

2-unit fixed-rate and ARM

3 abd 4-unit fixed-rate

3 to 4-unit ARM

Requirements For Rental Income From The Subject 1-Unit Property

4

Mortgage Products

LTV Ratio, 1-Unit Properties

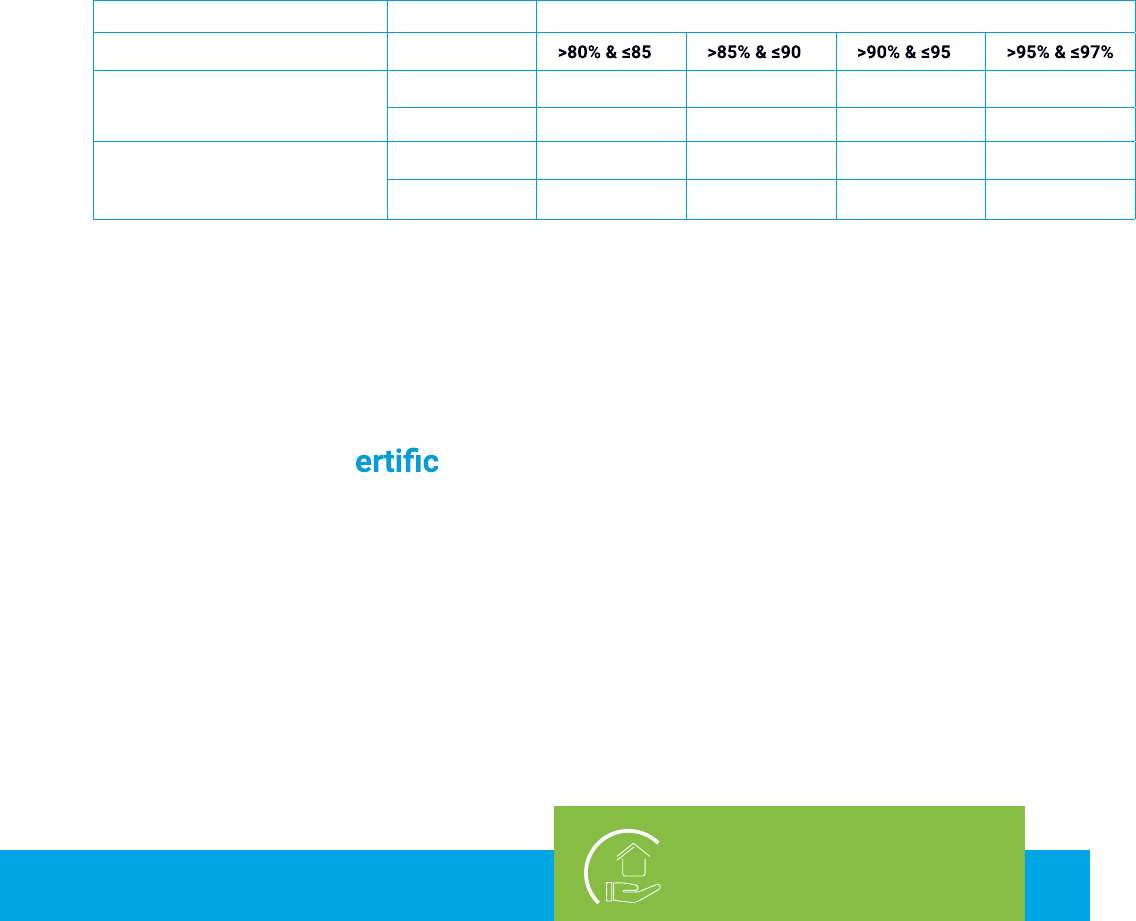

Transaction Type MI Coverage % % %

< 20 years

Standard 6% 12% 25% 25%

Custom n/a n/a 16% 18%

term > 20 years; ARMs; and

manufactured homes

Standard 12% 25% 25% 25%

Custom

6%

12% 16% 18%

Seller must obtain Freddie Mac’s approval to sell mortgages with annual or monthly premium lender-paid mortgage insurance to Freddie Mac. If custom MI is chosen, the custom MI fee applies

regardless of any cap on credit fees in price. See Guide Section 4701.1 for additional MI requirements and options including custom MI.

GO ALL IN > SF.FreddieMac.com/HomePossible

Additional Requirements For 2- To 4-Unit Properties

• Minimum contribution from borrower personal funds for LTV/TLTV and HTLTV ratios:

• <= 80% – none

• >80% <= 95% – 3% of value

• >95% – not applicable

• Minimum borrower reserves required will be determined by Loan Product Advisor. If the mortgage is manually underwritten, two

months of reserves are required.

• Minimum indicator score for manually underwritten mortgages: 700.

• Collateral evaluation for 4-unit primary residences: Use Form 72, Small Residential Income Property Appraisal Report.

• Landlord education: For purchase transactions, at least one qualifying borrower must participate in a landlord education program

• Rental income from a 2- to 4-unit primary residence that meets requirements in Guide Chapter 5306 may be used as

qualifying income.

• Refer to the Guide for additional requirements.

Mortgage Insurance Requirements

The standard required or custom mortgage insurance (MI) coverage levels for Home Possible mortgages are as follows:

Temporary Subsidy Buydowns

• Allowed for mortgages secured by 1-2 unit properties that are not manufactured homes (See Guide Section 4204.4).

• If a mortgage with a temporary subsidy buydown plan is subject to secondary financing, including an Affordable Second, the

secondary financing must have a fixed interest rate.

Mortgage Credit C ates

•

5301.1 and 5305.2 are met.

• The amount used as qualifying income must be calculated as follows: (mortgage amount) x (note rate) x (MCC rate %) divided by 12

Homeownership Education

•

home ownership education.

• Homeownership education is also required for any transaction when the credit reputation for all borrowers is established using

only non credit payment references.

• Homeownership education must be completed prior to the note date.

before the note date. For refinances, landlord education is not required but is recommended. It must not be provided by an

interested party to the transaction, the originating lender or the mortgage seller. A certificate of completion must be retained in the

mortgage file.

Mortgage Credit Certificates (MCCs) may be considered as qualifying income, provided the requirements in Guide Sections

For a purchase transaction, if all occupying borrowers are first-time homebuyers, at least one occupying borrower must receive

Home Possible, fixed-rate, term

Home Possible, fixed-rate,

Eligible

Executions

•

Fixed-rate Guarantor

• WAC ARM Guarantor

• ARM Cash

• Servicing-Retained Cash

• Cash-Released XChange

SM

• MultiLender Swap

There are no special pooling requirements for the Home Possible mortgage. Mortgages may be pooled with

non-Home Possible mortgages. Refer to Guide Chapter 6202 for pooling requirements.

Delivery

Requirements

See Guide Section 6302.14(b) for special delivery instructions for the Home Possible mortgage and Guide

Section 6304.34 for applicable secondary financing delivery requirements. In additional Sellers must provide the

applicable information, as outlined in Guide Section 6302.14(b), for down payment, closing costs, automated

underwriting system and borrower counseling. Sellers must deliver the following ULDD Data Points:

• Loan Affordable Indicator: “true”.

• Loan Program Identifier: “Home Possible Mortgage” .

• If applicable, Sellers must deliver the following Investor Feature Identifiers (IFI) in ULDD Data Point IFI 532,

if mortgage satisfies the minimum number of payment reference requirements using noncredit payment

references.

5

Contact your Freddie Mac representative or 800-FREDDIE

SF.FreddieMac.com | Publication Number 1077 | May 2023

927912261

Mortgage Products

Collateral Evaluation

• 1-unit primary residences: Use Form 70, Uniform Residential Appraisal Report.

• Condominiums: Use Form 465, Individual Condominium Unit Appraisal Report.

• Manufactured housing: Use Form 70B, Manufactured Home Appraisal Report.

Credit Fees In Price

• Standard risk-based credit fees in price are waived. Custom MI credit fee in price will apply.

• See Guide Exhibit 19 for details on credit fees in price applicable to the Home Possible mortgage.

Delivery Requirements

Homeownership Education (cont.)

• Eligible homeownership education must meet the National Industry Standards for Homeownership Education and Counseling or

or Community Development Financial Institutions (CDFIs).

• Homeownership education must not be provided by an in terested party to the transaction, the originating lender or the

mortgage seller.

Certificate of completion must be retained in the loan file.

•

be provided by an eligible source, such as a HUD-approved counseling agency, mortgage insurer, housing finance agency (HFA)