This document is incorporated by reference into the

Fannie Mae Selling Guide.

© 2024 Fannie Mae. 1

February 07, 2024

The Eligibility Matrix provides the comprehensive LTV, CLTV, and HCLTV ratio

requirements for conventional first mortgage loans eligible for delivery to Fannie Mae. The

Eligibility Matrix also includes credit score, minimum reserve requirements (in months), and

maximum debt-to-income ratio requirements for manually underwritten loans. Other

eligibility criteria that are not covered in the Eligibility Matrix may be applicable for loans to

be eligible for purchase by Fannie Mae, e.g., allowable ARM plans. See the Selling Guide

for details. Refer to the last two pages of this document for exceptions to the requirements

shown in the matrices.

Acronyms and Abbreviations Used in this Document

ARM: Adjustable-rate mortgage, fully amortizing

DTI: Debt-to-income ratio

DU

®

: Desktop Underwriter

®

FRM: Fixed-rate mortgage, fully amortizing

LTV: Loan-to-value ratio

CLTV: Combined loan-to-value ratio

HCLTV: Home equity combined loan-to-value ratio

Credit Score/LTV: Credit score and highest of LTV, CLTV, and HCLTV ratios

Table of Contents

Standard Eligibility Requirements - Desktop Underwriter Page 2

HomeStyle® Renovation, Manufactured Housing, and HomeReady

®

-

Desktop Underwriter

Page 3

Standard Eligibility Requirements - Manual Underwriting Page 4

HomeStyle Renovation and HomeReady - Manual Underwriting Page 5

High LTV Refinance *Acquisition of high LTV refinance loans is

suspended

Page 6

Notes - Exceptions Applicable to ALL Matrices Other than High LTV

Refinance

Page 7-8

Notes - Specific to Certain Transactions Page 8-9

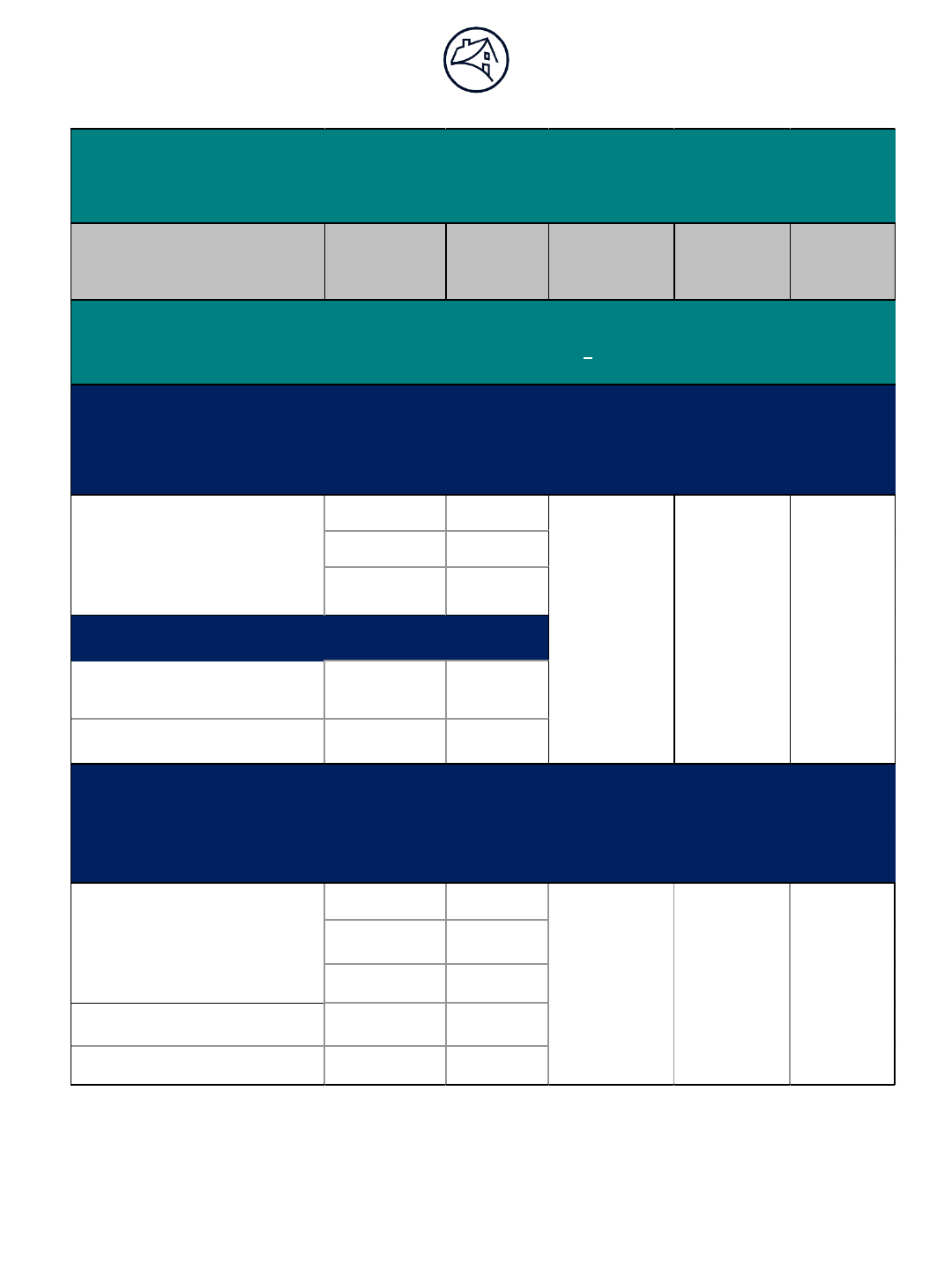

ELIGIBILITY MATRIX

© 2024 Fannie Mae. 2This document is incorporated by reference into the

Fannie Mae Selling Guide.

February 07, 2024

NOTE: THERE MAY BE EXCEPTIONS TO THE ABOVE REQUIREMENTS FOR CERTAIN TRANSACTIONS.

REFER TO THE NOTES SECTION ON PAGES 7-9 FOR THE EXCEPTIONS.

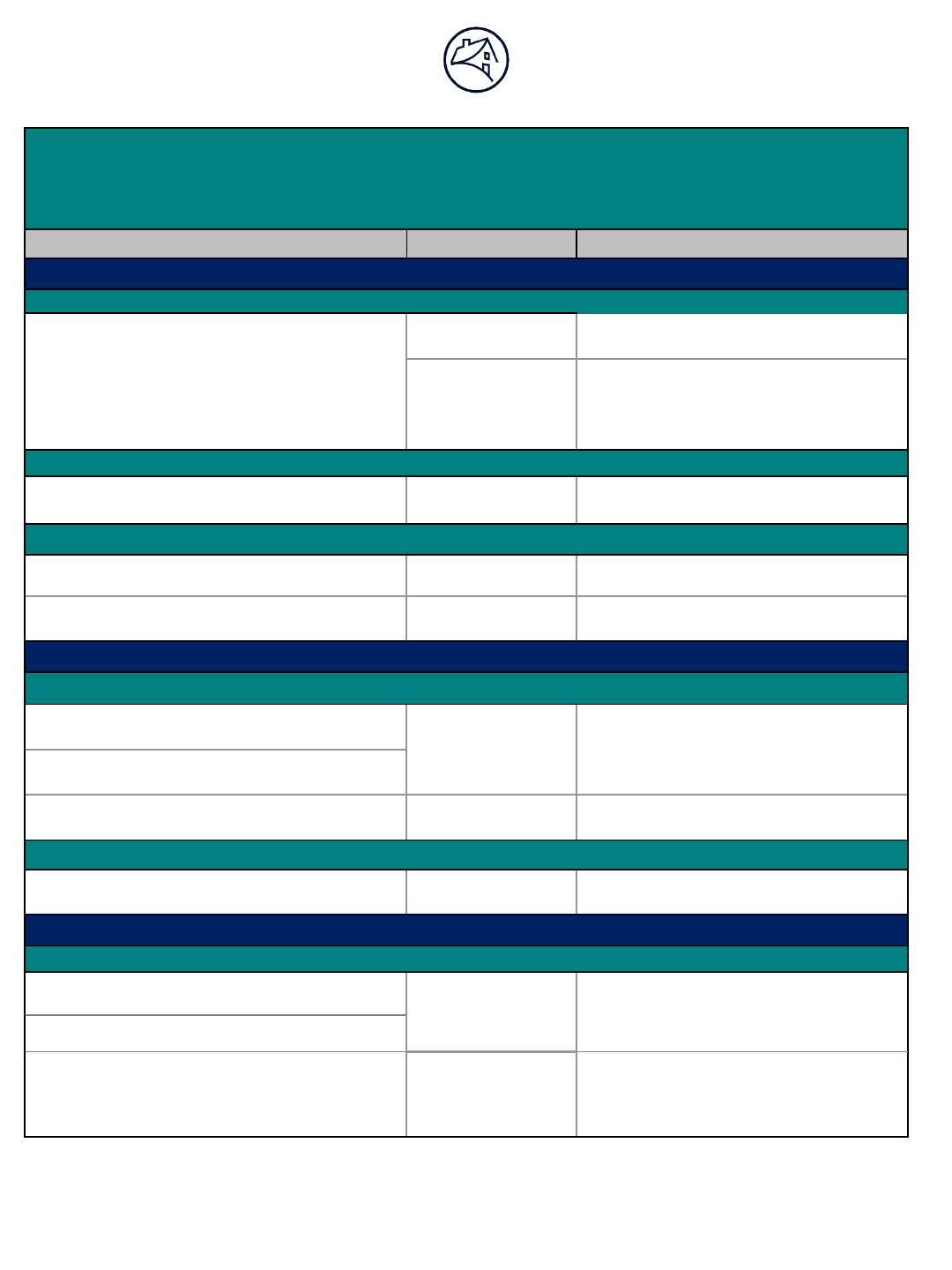

Transaction Type Number of Units Maximum LTV, CLTV, HCLTV

1 Unit

FRM: 97%

(1)

ARM: 95%

1 Unit FRM/ARM: 80%

2-4 Units FRM/ARM: 75%

Purchase

Limited Cash-Out Refinance

1 Unit FRM/ARM: 90%

Cash-Out Refinance 1 Unit FRM/ARM: 75%

1 Unit

FRM/ARM: 85%

2-4 Units FRM/ARM: 75%

1 Unit

2-4 Units FRM/ARM: 70%

Standard Eligibility Requirements - Desktop Underwriter Version 11.1

Excludes: High LTV Refinance, HomeReady, HomeStyle Renovation, and

Manufactured Housing

Principal Residence

Purchase

Limited Cash-Out Refinance

Cash-Out Refinance

Limited Cash-Out Refinance

Purchase

Cash-Out Refinance

Second Homes

Investment Property

1-4 Units

FRM/ARM: 75%

2- 4 Units

(2)

FRM/ARM: 95%

© 2024 Fannie Mae. 3This document is incorporated by reference into the

Fannie Mae Selling Guide.

February 07, 2024

NOTE: THERE MAY BE EXCEPTIONS TO THE ABOVE REQUIREMENTS FOR CERTAIN TRANSACTIONS.

REFER TO THE NOTES SECTION ON PAGES 7-9 FOR THE EXCEPTIONS.

Transaction Type Number of Units Maximum LTV, CLTV, HCLTV

1 Unit

FRM: 97%

(1)

ARM: 95%

Purchase

Limited Cash-Out Refinance

1 Unit FRM/ARM: 90%

Purchase 1 Unit

FRM/ARM: 85%

Limited Cash-Out Refinance 1 Unit FRM/ARM: 75%

Purchase

Limited Cash-Out Refinance

Cash-Out Refinance

1 Unit

FRM/ARM: 65%

Purchase

Limited Cash-Out Refinance

1 Unit FRM/ARM: 90%

Purchase

Limited Cash-Out Refinance

HomeReady Mortgage

Investment Property

Purchase

Limited Cash-Out Refinance

Principal Residence

Manufactured Housing

(4)

Principal Residence

Second Homes

HomeStyle Renovation, Manufactured Housing,

HomeReady

(3)

Desktop Underwriter Version

11.1

HomeStyle Renovation Mortgage

Second Homes

Principal Residence

Purchase

Limited Cash-Out Refinance

1 Unit

FRM: 97%

(1)

ARM: 95%

FRM: 97%

(1)

ARM: 95%

1 Unit

2 - 4 Units

(2)

FRM/ARM: 95%

(2)

FRM/ARM: 95%

2 - 4 Units

© 2024 Fannie Mae. 4This document is incorporated by reference into the

Fannie Mae Selling Guide.

February 07, 2024

NOTE: THERE MAY BE EXCEPTIONS TO THE ABOVE REQUIREMENTS FOR CERTAIN TRANSACTIONS.

REFER TO THE NOTES SECTION ON PAGES 7-9 FOR THE EXCEPTIONS.

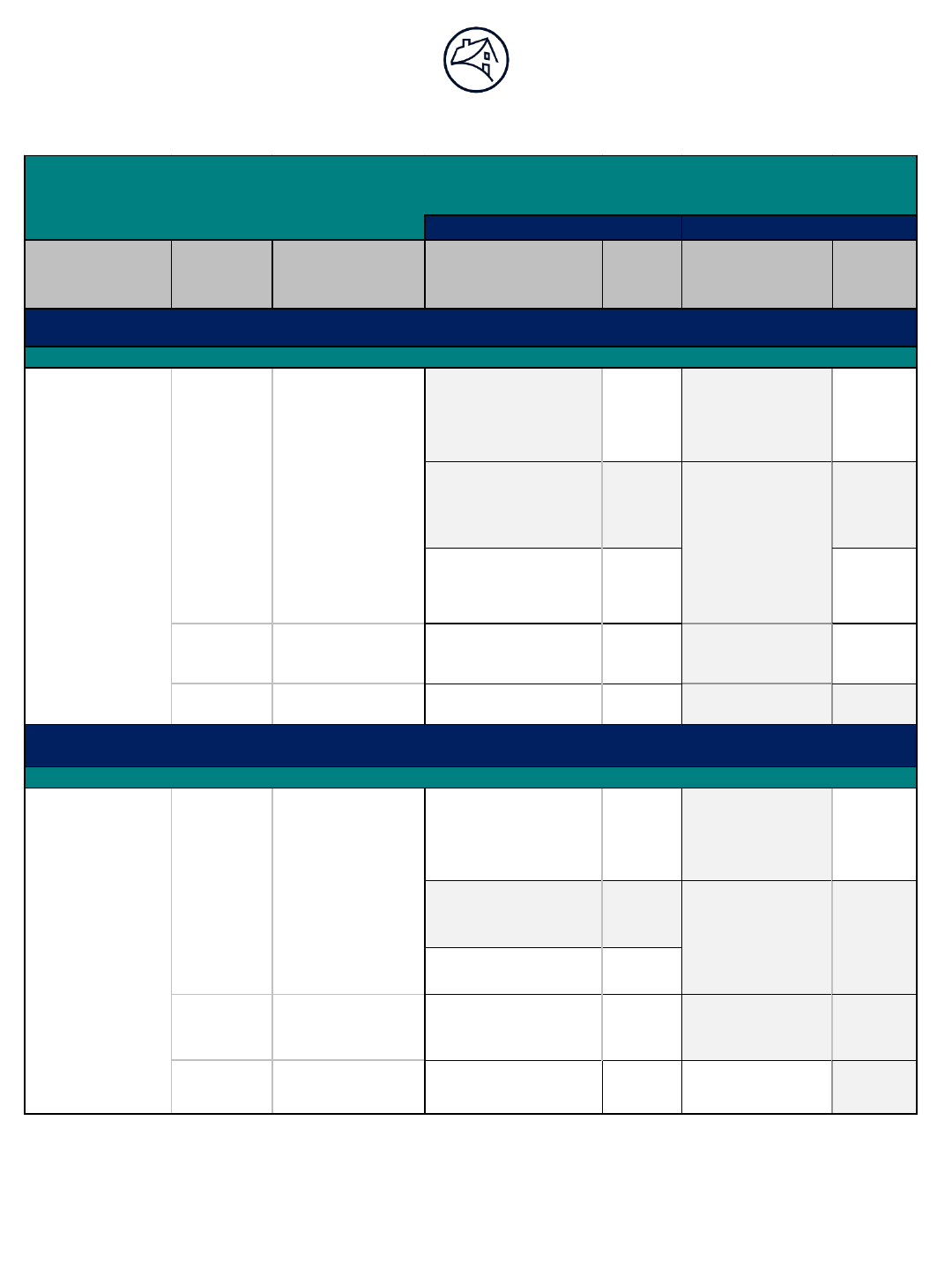

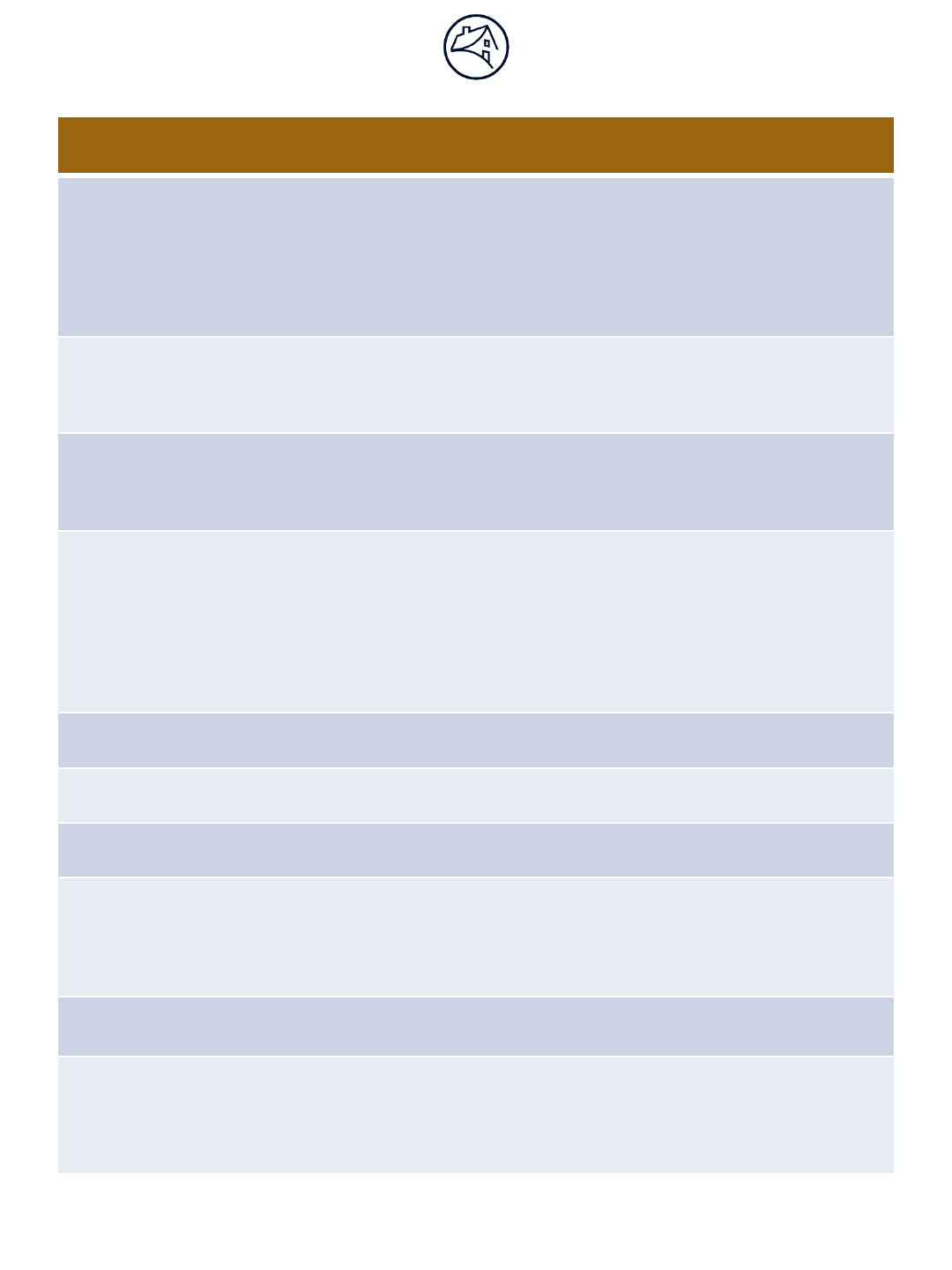

Transaction

Type

Number of

Units

Maximum

LTV, CLTV,

HCLTV

Credit Score/LTV

Minimum

Reserves

Credit Score/LTV

Minimum

Reserves

680 if > 75%

640 if ≤ 75%

0

FRM: 620 if ≤ 75% 2

660 if > 75% 6

700 if > 75%

660 if ≤ 75%

6

2 Units

FRM/ARM: 85%

680 if > 75%

640 if ≤ 75%

6

700 if > 75%

680 if ≤ 75%

6

680 if > 75%

660 if ≤ 75%

0

660 if > 75%

640 if ≤ 75%

6

700 6

680 12

Standard Eligibility Requirements - Manual Underwriting

Excludes: High LTV Refinance, HomeReady, HomeStyle Renovation

6

660

Maximum DTI ≤ 36%

Maximum DTI ≤ 45%

Cash-Out

Refinance

Principal Residence

720 if > 75%

680 if ≤ 75%

0

6

2

6

2-4 Units

FRM/ARM: 75%

680

Purchase

Limited Cash-

Out Refinance

3-4 Units

FRM/ARM: 75%

700 if > 75%

680 if ≤ 75%

FRM/ARM: 80%

1 Unit

FRM/ARM: 95%

1 Unit

680

© 2024 Fannie Mae. 5This document is incorporated by reference into the

Fannie Mae Selling Guide.

February 07, 2024

NOTE: THERE MAY BE EXCEPTIONS TO THE ABOVE REQUIREMENTS FOR CERTAIN TRANSACTIONS.

REFER TO THE NOTES SECTION ON PAGES 7-9 FOR THE EXCEPTIONS.

Transaction Type

Number of

Units

Maximum

LTV, CLTV, HCLTV

Credit Score/LTV

Minimum

Reserves

Credit Score/LTV

Minimum

Reserves

680 if > 75%

640 if ≤ 75%

0

720 if > 75%

680 if ≤ 75%

0

FRM: 620 if ≤ 75% 2 6

660 if > 75% 6 6

680 if > 75%

640 if ≤ 75%

0

720 if > 75%

680 if ≤ 75%

0

FRM: 620 if ≤ 75%

2

660 if > 75% 6

3-4 Units

FRM/ARM: 75%

660

6

Purchase

Limited Cash-Out

Refinance

6

FRM/ARM: 85%

FRM/ARM: 95%

2 Units

1 Unit

680 if > 75%

640 if ≤ 75%

700 if > 75%

680 if ≤ 75%

6

680

HomeStyle Renovation and HomeReady - Manual Underwriting

(3)

Maximum DTI ≤ 36%

Maximum DTI ≤ 45%

Purchase

Limited Cash-Out

Refinance

1 Unit

3-4 Units

FRM/ARM: 85%

6

700 if > 75%

660 if ≤ 75%

6

Principal Residence

HomeReady Mortgage

FRM/ARM: 75%

FRM/ARM: 95%

680 if > 75%

640 if ≤ 75%

HomeStyle Renovation Mortgage

Principal Residence

6

2 Units

6

660

680

6

700 if > 75%

680 if ≤ 75%

6

700 if > 75%

660 if ≤ 75%

© 2024 Fannie Mae. 6This document is incorporated by reference into the

Fannie Mae Selling Guide.

February 07, 2024

NOTE: THERE MAY BE EXCEPTIONS TO THE ABOVE REQUIREMENTS FOR CERTAIN TRANSACTIONS.

REFER TO THE NOTES SECTION ON PAGES 7-9 FOR THE EXCEPTIONS.

Transaction Type Number of Units

Minimum LTV Maximum LTV

Minimum Credit

Score

Maximum DTI

Ratio

1 Unit 97.01

2 Units

85.01

3-4 Units 75.01

Desktop Underwriter

Second Home 1 Unit 90.01

Investment Property 1-4 Units 75.01

1 Unit 97.01

2 Units 85.01

3-4 Units 75.01

Second Home 1 Unit 90.01

Investment Property 1-4 Units 75.01

Principal Residence

FRM: No Limit

ARM: 105%

620

45%

FRM: No Limit

ARM: 105%

No Minimum

No Maximum

Limited Cash-Out Refinance, Fixed Rate, ARMs with Initial Fixed Periods > 5 Years

Desktop Underwriter and Manual Underwriting

High LTV Refinance

(5)

Acquisition of high LTV refinance loans is suspended*

Manual Underwriting

Principal Residence

Standard Eligibility

Alternative Qualification Path

© 2024 Fannie Mae. 7This document is incorporated by reference into the

Fannie Mae Selling Guide.

February 07, 2024

Notes – Exceptions Applicable to ALL Matrices

Other than High LTV Refinance

105% CLTV Ratio/Community Seconds

®

: The CLTV ratio may exceed the limits stated in the matrices

up to 105% only if the loan is part of a Community Seconds transaction. A loan securing a manufactured

home that is not MH Advantage that has a Community Seconds is limited to the LTV, CLTV, and HCLTV

ratios stated in the matrices.

The following are not permitted with Community Seconds: second homes, investment properties, cash-

out refinances, ARMs with initial adjustment periods less than 5 years, and co-op share loans.

Cash-out refinances: Minimum reserves apply to DU loan casefiles with DTI ratios exceeding 45%.

See B2-1.3-03, Cash-Out Refinance Transactions.

Condos: Lower LTV,CLTV, and HCLTV ratios may be required for certain loans depending on the type

of project review the lender performs for properties in condo projects. See B4-2.1-01, General

Information on Project Standards, B4-2.2-01, Limited Review Process, and B4-2.2-04, Geographic-

Specific Condo Project Considerations.

Construction-to-permanent: These transactions are subject to the applicable eligibility requirements

based on the loan purpose. Single-closing transactions are processed as purchases or limited cash-out

refinances, and two-closing transactions are processed as limited cash-out or cash-out refinances.

Exceptions: loans secured by units in a co-op project or attached units in a condo project are not eligible

for construction-to-permanent financing. If the transaction is a single-closing construction-to-permanent

loan, and the age of the credit or appraisal documents exceed standard guidelines, there are exceptions

to the eligibility requirements. See B5-3.1-02, Conversion of Construction-to-Permanent Financing:

Single-Closing Transactions.

Co-op properties: The following are not permitted with co-op share loans - subordinate financing,

investment properties, and cash-out refinances on second home properties.

Employment-related assets: Exceptions to the eligibility requirements apply if this type of asset is used

as qualifying income. See B3-3.1-09, Other Sources of Income.

High-balance loans: High-balance loans must be underwritten with DU. All borrowers on the loan must

have a credit score.

HomeStyle

®

Energy: For manually underwritten loans, the criteria that applies to DTI ratios of 36% may

apply up to 38% for HomeStyle Energy loans. (DTI ratios up to 45% are also permitted in accordance

with this matrix.) See B5-3.3-01, HomeStyle Energy for Improvements on Existing Properties. Loans with

energy-related improvements are subject to the applicable LTV, CLTV, and HCLTV ratios for purchase

and limited cash-out refinance transactions.

Manufactured housing: Loans secured by manufactured homes (including MH Advantage) must be

underwritten with DU.

Multiple financed properties: Borrowers of second homes or investment properties with multiple

financed properties are subject to additional reserves requirements. Borrowers with seven to ten

financed properties are subject to a minimum credit score requirement (only permitted in DU). See B3-

4.1-01, Minimum Reserves Requirements.

© 2024 Fannie Mae. 8This document is incorporated by reference into the

Fannie Mae Selling Guide.

February 07, 2024

Notes – Exceptions Applicable to ALL Matrices

Other than High LTV Refinance

Non-occupant borrowers: If the income of a non-occupant borrower is used for qualifying purposes,

lower LTV, CLTV, or HCLTV ratios are required, and exceptions apply if there is a subordinate lien that

is a Community Second. See B2-2-04, Guarantors, Co-Signers, or Non-Occupant Borrowers on the

Subject Transaction. See also Note (1) below.

Nontraditional credit: Exceptions to the eligibility requirements apply to all transactions when no

borrowers have a credit score, or one or more borrowers are relying on nontraditional credit to qualify.

See B3-5.4-01, Eligibility Requirements for Loans with Nontraditional Credit.

RefiNow™ loans: These loans must be secured by fixed-rate, one-unit principal residences, with a

limited cash-out refinance transaction that has specific requirements. High-balance loans are not

permitted. A RefiNow loan may not be combined with a HomeReady refinance transaction. See LL-

2021-10 for additional information and exceptions to this Matrix.

Notes - Specific to Certain Transactions

(1) LTV, CLTV, or HCLTV Ratios Greater than 95%: These transactions are not permitted for

high-balance loans, manufactured homes that are not MH Advantage, or HomeReady loans

with sweat equity. At least one borrower on the loan must have a credit score. For non-

HomeReady purchase transactions without a Community Seconds, at least one borrower must

be a first-time home buyer. For limited cash-out refinances, Fannie Mae must be the owner of

the existing mortgage. See B2-1.3-01, Purchase Transactions and B5-6-01, HomeReady

Mortgage Loan and Borrower Eligibility.

If there is a non-occupant borrower on the transaction:

• Manually underwritten loans: LTV/CLTV/HCLTV ratio <

90%*

• DU loan casefiles: LTV/CLTV/HCLTV ratio <

95%

• Both: CLTV ratio <

105% with a Community Seconds

*For RefiNow loans, LTV/CLTV/HCLTV ratio <

95% is permitted.

(2) LTV, CLTV, or HCLTV Ratios for High-Balance 2-4 Unit Properties:

• 2 unit: <

85%

• 3-4 unit: <

75%

(3) Combination of HomeStyle Renovation, HomeReady, and Manufactured Housing: If a

transaction includes a combination of HomeStyle Renovation, HomeReady, and manufactured

housing, the more restrictive eligibility requirements of each of those transactions apply. DU will

apply the applicable eligibility requirements, but the lender must determine eligibility for

manually underwritten loans.

Examples:

1. A HomeReady mortgage that is also a HomeStyle Renovation mortgage must be a

principal residence (per HomeReady). The lender must meet the HomeStyle Renovation

lender approved requirements, as applicable.

2. A HomeReady mortgage for a manufactured home (that is not MH Advantage) must be a

one-unit property that is underwritten through DU with a maximum LTV ratio of 95% (per

manufactured housing), and a purchase or limited cash-out refinance of a principal

residence (per HomeReady).

© 2024 Fannie Mae. 9This document is incorporated by reference into the

Fannie Mae Selling Guide.

February 07, 2024

Notes - Specific to Certain Transactions

(4) Single-width Manufactured Homes: Loans are limited to principal residence purchase and

limited cash-out refinance transactions only.

(5) High LTV Refinance: Loans are subject to a unique limited cash-out refinance definition, and

other unique requirements. There is no maximum CLTV or HCLTV ratio limit. See Chapter B5-

7, High Loan-to-Value Refinance Option for additional eligibility requirements.

Acquisition of high LTV refinance loans is suspended*