LIST OF ABBREVIATIONS

NEKRTC : North East Karnataka Road Transport

Corporation

CPKM : Cost per Kilometer

EPKM : Earnings per Kilometer

MPKM : Margin per kilometer

CIRT : Central Institute of Road Transport

STU : State Transport Undertaking

BEP : Break Even Point

AC : Air Conditioner

AWATAR : Any Where Any Time Advance Reservation

ETMs : Electronic Ticketing Machines

MIS : Management Information System

DCS : Depot Computerization Software

IT : Information Technology

KMs : Kilometers

HSD : High Speed Diesel.

FINANCIAL PERFORMANCE EVALUATION OF STATE ROAD

TRANSPORT CORPORATIONS – A STUDY WITH A FOCUS ON

NEKRTC

Synopsis:

I. Introduction

II. Review of Literature

III. Statement of the problem

IV. Objectives of the studies

V. Prole of NEKRTC

VI. Financial indicators OF NEKRTC

Ÿ CPKM

Ÿ EPKM

Ÿ MPKM

Ÿ Gross Revenue

VII. Summary of Findings, Suggestions and Conclusions

I .INTRODUCTION:

It is usual to judge the performance of private sector units by the

yardstick of net prot or loss; hence in their case maximization of

the prot is the sole aim. This yardstick fails in the case of public

sector undertakings, since they give more preference to attain

other priorities which in the public interest. Due to this the

performance of the public sector should not be judged by what

they earn in the form of prots but by the total additions they

make to the ow of goods and services in the economy. Thus

instead of prots, the yardstick should be the total sales value of

the enterprises.

Though there is no dispute regarding the role of the public sector

undertaking in country's economic development, yet the feeling is

widely prevalent that, the rate of prot in these undertakings is

either too low or is negative. Accordingly their performance is not

up to the expected standard.

However it is not so easy to decide about the efciency of the

public sector undertakings. As noted earlier the rate of prot might

be a good criterion to judge the efciency of a private sector

enterprise but cannot be deemed so for public sector enterprise. It

Original Research Paper Commerce

FINANCIAL PERFORMANCE EVALUATION OF STATE

ROAD TRANSPORT CORPORATIONS – A STUDY

WITH A FOCUS ON NEKRTC

SUNITA RAMESH

KATKE

DEPARTMENT OF POST GRADUATE STUDIES & RESEARCH IN COMMERCE,

GULBARGA UNIVERSITY KALABURAGI, KARNATAKA

Dr. RAJNALKAR

LAXMAN

DEPARTMENT OF POST GRADUATE STUDIES & RESEARCH IN COMMERCE,

GULBARGA UNIVERSITY KALABURAGI, KARNATAKA

ISSN - 2250-1991 | IF : 5.761 | IC Value : 79.96

Volume : 6 | Issue : 3 | - 2017

March

KEYWORDS

ABSTRACT

North East Road Transort Corporation. NEKRTC was established on 1.10.2000 having been separated from KSRTC for providing

“adequate, efcient, economic and properly coordinated road transport services” in the North eastern part of the state of

Karnataka. As on 31.03.2015 NEKRTC is operating 3970 schedules covering 12.46 lakhs kms carrying 12.00 lakhs passengers

every day. NEKRTC is serving 92% of the villages in its area (3859 out of 4203) with transport facility. NEKRTC owns a wide

Infrastructure consisting one corporate ofce, 09-Divisional ofces, 48 Depots, 134 bus stands and 4369 buses. NEKRTC

provides the wide range of services to the commuters like AC sleeper , AC Semi Sleeper, AC Jumbo, AC Mofussil, Rajahansa and

Suhas (Executive services) Karnatak Sarige ( Branded and Regular services), Mofussil (Express and ordinary city /sub urban services).

The corporation is nancially not depended on the state government as state road transport should operate the schedules and

generate the revenue to meet its expenditures. Likewise NEKRTC is managing its expenditure by generating the revenue. Major

components of the expenditure is fuel and staff salary, here fuel contributes around 40% of the total cost and staff salary around

15% -20 % of total cost. Being major cost components these two are playing a vital role in the nance management. Public

transport corporation is directly linked to the common man hence can't avoid any cost due to losses and lower earnings. Paper

prepared on “Financial Performance Evaluation of State Road Transport Corporation-A case study with Focus on

NEKRTC, nancial parameters like CPKM, EPKM, Marginal revenue and Gross revenue are discussed in detail. A public transport

organization like NEKRTC is giving equal importance to both nancial and physical parameters for performance evaluation.

Financial parameters are given importance here because all the expenditures incurred by the corporation are borne by the revenue

earned by the corporation. The revenue may be trafc revenue or commercial revenue here. Any organization can survive if it is

nancially sound. Meanwhile the public transportation like NEKRTC has to provide services to commuters without expecting the

prots. Due to various reasons NEKRTC operates vehicles in those routes which are loss making in most of the time and some time

breakeven point. Very less routes generate prot for the schedule. CPKM of the corporation is increasing every year, EPKM is also

increasing every year, but the ratio between these two parameters is not similar. Growth rate Cost of production is higher than the

growth rate of earnings. Gross revenue of the corporation is showing a favorable growth rate. Margin per kilometer is always

shown a negative gure which affects the nancial strength of the corporation in long run if the same continues for a longer

period.

PARIPEX - INDIAN JOURNAL OF RESEARCH | 515

is preferred that to judge the efciency of the public sector

undertaking it is recommended the criterion of social marginal

productivity and the utility of investment in any project should be

judged by its impact on national income, balance of payments and

distribution of income. Further the evolution of investment in the

public sector should be done on the basis of marginal per capita

investment quotient. According to this criterion, we must examine

whether investment of capital in any project will lead to

maximization of national income at any point in the future or not.

Without entering into the controversy regarding determination of

investment in the public sector at this juncture, we would like

emphasize that evaluation of any state enterprise should be done

on the basis of social benet and social cost and not on the basis of

rate of prot.

The elds of engineering and management associate efciency

with how well a relevant action is performed, i.e. ''doing things

right'', and effectiveness with selecting the best action, i.e. ''doing

the right thing''. Thus, a rm is effective if identies appropriate

strategic goals, and efcient if it achieves them with minimal

resources. Operational efciency or the ability to deliver products

and services cost effectively without sacricing quality. Efciency

with both queuing models and productivity, and efciency analysis

methods that identify maximum productivity and measure

efciency as a ratio of observed productivity to maximum

productivity. The maximum productivity levels serves as a

benchmark for desired perform.

II .REVIEW OF LITERATURE:

Performance analysis on any organization facilitates to know its

functioning in key performance areas to suggest suitable steps,

where ever necessary for its improvement in efciency and

successful performance. Lau, (1997) suggests that evaluation of

public transport services can be divided into two aspects. The rst

one is to evaluate the public transport based on its efciency. The

second one is to evaluate the systems on its ability to meet the

basic objective like service to the public.

Shambhag (1972) examined the peculiar desires of the commuters

like “he (wants to) should get a bus within a reasonable period. He

should be able to reach his destination by a direct bus; he should be

able to travel to his destination by the shortest route”. He also

observed the losses on transport due to city transport, because its

very nature of operations is uneconomic, as a large number of eet

is required to be maintained and to take off peak hour trafc, etc.

He also discussed the facts of shortage of capital, absenteeism of

staff. (Efcient network with adequate frequency)

Venkaji Rao (1974) analyzed the managerial problem of state

transport undertaking with special reference to Mysore State. He

identied some administrative problem to improve the

performance of a state transport undertaking. They are: (i)

Balancing the transport requirements of the community as against

other facilities, requirements of the community as against other

facilities served, based on costs and income and nance, (ii) Peak-

load problems, (iii) the most efcient utilization of vehicles and

staff on the basis of moving of given loads of passengers. (iv)

Forecasting the picture of transport.(Optimal utilization of

resources)

Jakaria (1975) explained the need for the establishment of

adequate criteria for evaluating the performance of urban

transport systems.

Pereira, W.(1975) suggested that overcrowding, foot board travel

and indiscipline in the bus should be reduced. Special standee

buses should be introduced during peak hours, and checking

should be strengthened. Dishonesty and cheating should be

severely punished.(Comfort and Safety approach)

Purushotham, P.W., (1992) examined the organization and

management of the road transport corporation administered

under public sector in Andhra Pradesh with a view to promote

performance standards and organizational efciency.

Prasad, Srinivas, and Khan (1996) conducted a case study on

APSRTC and identied the operations of city services, with

negative margin and operation of obligatory services, concessional

passes to various categories of commuters, provision for passenger

amenities and operation of buses on bad roads with additional

cost of operation are for the social benet and hence cannot be

taken as wastage or ill utilization of funds.(Shouldering of Social

obligations)

Gundam Rajeswari (1998) examined the performance of Andhra

Pradesh Road Transport Corporation at the state and regional

levels. Both nancial and social performance were examined using

indicators like cost per kilometer, earnings, load factor etc. and

arrived at gross margins for the survey period.

Pradeep Singh Karola (2004) in his study explained the economy of

public transport system, factors affecting the cost of operation of

bus system, the manpower related parameters, the mechanized

parameters and the trafc related parameters relating to public

transport system.

Bhaskar, G. and N.V. Ramana Murthy (2004) analyzed the difcult

role played by Transport Undertakings in meeting the duel

objectives i.e. social objectives on one side and the commercial

objectives on the other side. (Social service with business

principles)

III. STATEMENT OF THE PROBLEM

Appraisal of operational performance of public transport service

can be divided in two aspects. The rst one is to evaluate the public

transport based on its efciency. The second one is to evaluate the

systems on its ability to meet the basic objective like service to the

public. The performance of the public transport can't be

determined on the nancial performance. performance of public

transportation is assessed more on nancial parameters rather

than physical parameters. A public transport corporation like

NEKRTC is giving equal importance to both nancial and physical

parameters for performance evaluation. The reason for giving

importance to nancial aspects here that all the expenditures are

borne by the corporation, it has to manage with the revenue

earned by the corporation (Self sustaining organization). Therefore

the survival of the organization is depended on the revenue

accumulated by way of trafc revenue as well as other commercial

revenue. It is a known fact that any organization may be private or

public can survive only if it is nancially sound in its business. In

case of public sector it may generate revenue on its own business

or government may give nancial assistance. On the other hand

performance of the public sector like NEKRTC is measured with

operational parameters which also play an important role for the

organization. People (public) and State Transport Undertakings

both are very much depended on each other for their survival. The

concept of the public sector is emerged only to facilitate people to

travel from one place to other. In earlier days the performance of

the public transport Undertakings is assessed depending on the

extent of reach of its vehicles to the commuters. Later on the

performance is assessed on the load factor, frequency, number of

schedules etc., though these are the physical parameters for

performance evaluation but considered as a major techniques to

assess the quality of the services delivered and for performance

improvements.

State Transport Undertaking constitutes an important part of

Indian public sector. CIRT, Pune regularly monitors the

performance of these undertakings. The parameters used by this

institute to evaluate the performance of these undertakings are i)

Vehicle productivity ii) Manpower productivity iii) Fuel productivity

iv) Protability. Thus to evaluate the performance of State

Transport Undertakings the CIRT uses both nancial and physical

performance indicators. Government of India, Planning

commission also conducts performance evaluation of these

undertakings from time to time. The Planning Commission also

uses both nancial and physical indicators for performance

analysis.

ISSN - 2250-1991 | IF : 5.761 | IC Value : 79.96

Volume : 6 | Issue : 3 | - 2017

March

516 | PARIPEX - INDIAN JOURNAL OF RESEARCH

IV. OBJECTIVES OF THE STUDY:

Ÿ To Study and analyze the Performance of NEKRTC, with

reference to the Financial Parameters

Ÿ To study and analyze total cost and cost per kilometer behavior

for a period of 10 years.

Ÿ To study and analyze total earnings and earnings per kilometer

for a period of 10 years

Ÿ To Analyze the Gross revenue

Ÿ To offer suggestions, alternative ways and means to improve

the operations of the organization in particular, Sector in

general.

V. PROFILE OF NEKRTC

NEKRTC was established on 1.10.2000 having been separated

from KSRTC for providing “adequate, efcient, economic and

properly coordinated road transport services” in the North eastern

part of the state of Karnataka. As on 31.03.2015 NEKRTC is

operating 3970 schedules covering 12.46 lakhs kms carrying

12.00 lakhs passengers every day. NEKRTC is serving 92% of the

villages in its area (3859 out of 4203) with transport facility.

NEKRTC owns a wide Infrastructure consisting one corporate

ofce, 09-Divisional ofces, 48 Depots, 134 bus stands and 4369

buses. NEKRTC provides the wide range of services to the

commuters like AC sleeper , AC Semi Sleeper, AC Jumbo, AC

Mofussil, Rajahansa and Suhas ( Executive services) Karnatak

Sarige ( Branded and Regular services) , Mofussil ( Express and

ordinary city /sub urban services).

The corporation is nancially not depended on the state

government as state road transport should operate the schedules

and generate the revenue to meet its expenditures. Likewise

NEKRTC is managing its expenditure by generating the revenue.

Major components of the expenditure is fuel and staff salary, here

fuel contributes around 40% of the total cost and staff salary

around 15 % of total cost. Being major cost components these

two are playing a vital role in the nance management. Public

transport corporation is directly linked to the common man hence

can't avoid any cost due to losses and lower earnings.

FACILITIES PROVIDED BY THE NEKRTC ITS TO COMMUTERS:

Ÿ Reservation of seats for lady passengers: Two seats have been

reserved in Rajahamsa and higher classes of services for lady

passengers travelling single. In Mofussil buses, nine seats and

fourteen seats in City/Suburban services are reserved for lady

passengers.

Ÿ Reservation of seats for physically handicapped persons: Two

seats (24 & 25) have been reserved in Mofussil and City/

Suburban services.

Ÿ Free / Concessional Passes: NEKRTC is extending free /

concessional travel facility to students, physically Challenged

persons, Visually Challenged persons, Freedom Fighters,

SHOURYA' Awardees, National Award Winners (Kannada &

Sanskrit Dept.), Freedom Fighters Wives/Widows, Free travel

facility to the Dependents of Soldiers who died for Country

and Journalists.

Ÿ Concession for senior citizens: NEKRTC provides Concession in

passengers fare for senior citizens about 25% of the Bus fare,

having the age 60 and above.

Ÿ Discount on Return Journey Tickets: A discount of 10% is

offered on return journey tickets, if both onward and return

journey tickets are booked simultaneously.

Ÿ Discount on Group bookings: A discount of 5% on the fare, if

four or more passengers book a single ticket. Further, discount

of 8% is given for a group of 10 or more passengers.

Ÿ Special services: Additional services to pilgrimage / tourist

places are operated during festivals, summer vacation, other

fairs/festivals, weekends and holidays.

Ÿ Casual Contract services: For special occasions like weddings,

excursions, pilgrimage or study tour etc, NEKRTC is providing

dedicated buses on hire basis at competitive rates.

Ÿ Monthly Season Tickets are available to the passengers

travelling between two selected destinations daily. These

passes are most suited for ofce / industry employees,

teachers, businessmen etc.

Ÿ Pass Issue counters are working at all bus stands for the

convenience of the travelling public in obtaining student

passes, Monthly Season Tickets and One Day Passes.

Ÿ Advance reservation booking network (AWATAR): NEKRTC

has implemented on-line advance reservation network called

AWATAR (Any Where Any Time Advance Reservation),

wherein tickets can be booked through Internet. Presently, 16

NEKRTC counters and 46 Franchisees are working on this

system. There are 03 on-line booking counters in Gulbarga,

13 Counters in Hospet, 4 Counters in Raichur,7 Counters in

Koppal, 3 Counters in Bijapur, 13 counters in Bellary, 1 Counter

at in Bidar and 2 Counters in Yadagiri, . Tickets can be booked

30 days in advance including return journey tickets from

selected destinations.

Ÿ Electronic Ticketing Machines: To enhance the usage of IT in

day-to-day operations ETMs have been deployed in all 48

Depots. ETMs are convenient, user-friendly, light in weight

apart from other benets like speedy issue of tickets, reduction

in manual entry of waybills, generation of MIS reports on the

no. of passengers travelled, distance of travel, integration with

DCS etc.

Ÿ Passenger Amenities at bus stands: Refreshment rooms,

drinking water facility, sitting arrangements, display of Time-

Tables, Enquiry counters, Pass issue counters, Advance

booking counters, Luggage booking counters, separate toilets

/ urinals for Gents/Ladies, cycle/ scooter/ car parking stands,

CCTV, book stall, fruit stall. STD/local telephone booths etc are

provided at bus stands. All the bus stands in NEKRTC

jurisdiction are taken up for up gradation.

Ÿ Advertisement media: NEKRTC has an extensive media for

advertisement like bus panels, hoardings, on the backside of

bus tickets, advance reservation tickets, various types of passes

wh ich can be utiliz ed for d isplay of commercia l

advertisements.

Ÿ Environment friendly initiatives: NEKRTC has undertaken

massive a forestation programmers in its premises in Depots,

Divisions, and Workshop etc. Modern vehicle testing

equipments are procured to adhere to vehicular emission

norms. Diesel particulate lters have been tted to reduce

particulate emission on trial basis. A forestation is taken up in

large scale.

VI FINANCIAL PERFORMANCE INDICATORS

Financial management to rather like maintenance is to a vehicle. If

we don't put in good quality fuel and oil and give it a regular

service, the functioning of the vehicle suffers and it will not run

efciently. If neglected, the vehicle will eventually break down and

fail to reach its intended destination. In practice, nancial

management is about taking action to look after the nancial

health of an organization, and not leaving things to chance. The

concept purely applicable to those organizations which do not run

to achieve prot, like public transport sector run by the state

corporations like NEKRTC.

Financial performance is a subjective measure of how well a rm

can use assets from its primary mode of business and generate

revenues. There are many different ways to measure nancial

performance, but all measures should be taken in aggregation.

Line items such as revenue from operations, operating income or

cash ow from operations can be used, as well as total unit sales.

ISSN - 2250-1991 | IF : 5.761 | IC Value : 79.96

Volume : 6 | Issue : 3 | - 2017

March

PARIPEX - INDIAN JOURNAL OF RESEARCH | 517

Therefore nancial performance refers to the act of performing

nancial activity. In broader sense, nancial performance refers to

the degree to which nancial objectives being or has been

accomplished. It is the process of measuring the results of a rm's

policies and operations in monetary terms. It is used to measure

rm's overall nancial health over a given period of time and can

also be used to compare similar rms across the same industry or to

compare industries or sectors in aggregation. However, nancial

indicators do not reveal all the information related to the nancial

operations of a rm, but they furnish some extremely useful

information, which highlights two important factors protability

and nancial soundness. Thus analysis of nancial indicators is an

important aid to nancial performance analysis. Financial

performance analysis includes analysis and interpretation of

nancial statements in such a way that it undertakes full diagnosis

of the protability and nancial soundness of the business.

An attempt is made in this paper to analyze the performance of

NEKRTC based on the major nancial indicators such as CPKM,

EPKM, MPKM and Gross revenue.

(I) COST PER KILOMETERS (CPKM)

For any Road Transport Corporation the main and utmost

important nancial performance indicator is cost per kilometer.

Because it, together with EPKM, sets the base for xing the fare.

The protability of an organization is a function of both costs and

prices, which are equally valid in case of the State Transport

Undertakings too. An organization incurs losses when the cost

goes up and the price remains constant or a cost remaining the

same the price/fare falls. The second phenomenon of fare coming

down does not ordinarily arise in the case of passenger road

transport industry for reasons of relative inelasticity of demand for

the service, monopoly rights conferred on the service and state

regulation of fares. The cost of operation in absolute terms does

not by itself indicate measure of cost. Cost has to be worked out to

compare the cost of providing the service with the rate of earnings.

Cost per kilometer is one of such relative measure which is

computed by selecting effective kilometer as a unit of

measurement. In other words it is the Cost per Unit of the product

which in this case is passenger kms.

The cost per kilometer or CPKM is computed by dividing the total

cost of operation by the total effective kilometer. The CPKM is

expressed in terms of paisa/Rupees. The CPKM can be worked out

either in respect of the total cost of operation or in respect of each

components of the cost separately. The direct or operational or

variable cost reacts proportionately with the change in value of

operations and the cost per unit, i.e., CPKM is constituted with

value of operation. As indirect or total xed cost does not change

with volume of operation, the cost per unit, i.e., CPKM declines as

value rises or increases as volume falls.

In NEKRTC two types of cost are considered for assessing the

performance analysis, they are xed and variable cost. Here xed

cost consists of staff salary, general administrative expenditures,

interest and debt charges, welfare expenses, depreciation on other

assets, etc. whereas variable cost is consists of depreciation on

vehicle, HSD, lubricants, Tyres, Tubes, Flaps, spares and assembly,

batteries and electrical items, motor vehicle tax, Reconditioning

cost, Thus total cost comprises of xed costs which is independent

on vehicle utilization, but on its calculation on the basis of per

kilometer operated, it continuously declines as the vehicle

utilization increases, secondly , variable costs are dependent on

vehicle utilization but are constant on per kilometer basis. The sum

of these two costs per kilometers makes up the CPKM. Viewed

from the different angle, Total cost divided by seats kilometer gives

cost per kilometer. CPKM and cost per seat kilometer depends on

vehicle utilization which is depended on the seasons.

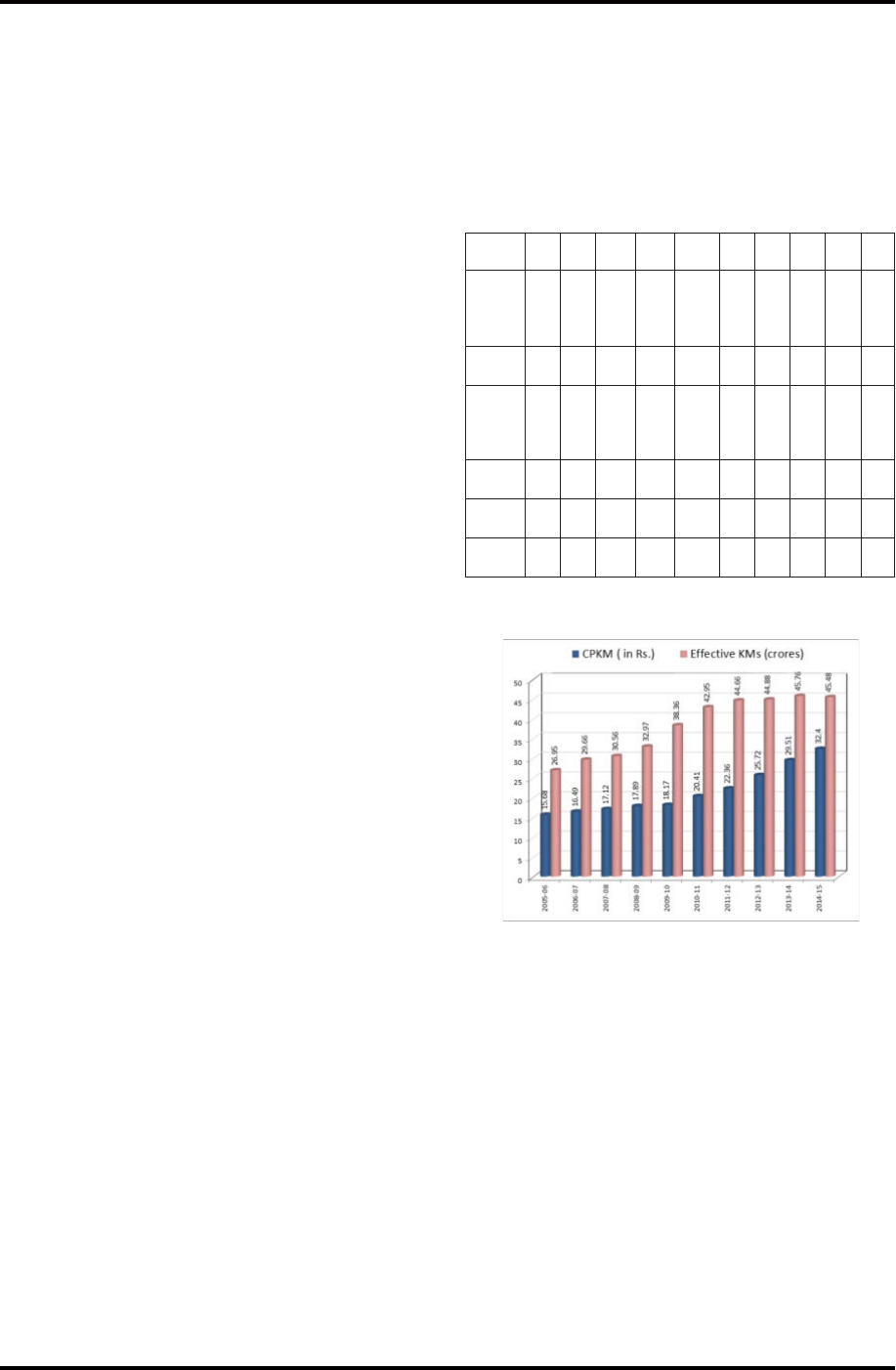

Data on CPKM for the reference period is given in Table.1. It could

be seen that in absolute terms CPKM increased continuously every

year. Further Table 1 reveals that, increasing trend in CPKM which

is purely due to increase in total cost, as the CPKM depends on the

total cost and effective KMs, both the gures are in increasing

trend from 2005-06 to 2014-15. Over a period of 10 years Cost of

operation is increased by 249% and effective Kms increased by

68%. Due to abnormal increase in the Cost of operation over and

above to effective Kms, the CPKM is increased by 106%. For any

other organization Cost per unit serves as a base to x the selling

price of the products with certain margin of prot. On the other

hand an organization can cut the costs according to its prot

making policy. In case of State Transport Undertakings like

NEKRTC, there are least options to cut down the costs or to avoid

the loss making schedules to reduce the increasing cost.

Table No. 1 : COST PER KILOMETER ( CPKM )

Source : Annual Administrative Reports

COST PER KILOMETER ( CPKM )

The table 1 reveals the growth rates of cost of operation in 2006-

07 is 16%, CPKM is raised by 7.08% and the Growth rate of

effective Kms is approximately 10% . In 2007-08 growth rate of

cost of operation is 7% where as effective kms hiked by 3% and

CPKM is increased by 2.03%. In 2008-09 nancial year growth

rate of cost of operation is 13%, on the other hand the rate of

effective KMs is increased by 8% and CPKM is increased by 4.4%

on its previous year gure. In 2009-10 cost of operation raised by

18% and effective kms by 16% and the growth rate CPKM

1.62%. But in 2010-11cost of operation is increased by 26%

,effective KMS and the growth rate of CPKM is same which shows

both 12% growth on its previous year gures. During 2011-12

cost of operation increased by 14%, effective Kms by 4% and

CPKM increased by 9.56%. In 2012-13 nancial year the cost of

operation increased by 16%, effective Kms increased by 1% and

CPKM is increased by 15.03%. During 2013-14 nancial year

Cost of oeration increased by 17%, Effective KMs by 2% and

CPKM increased by 14.74%. In 2014-15 nancial year Cost of

Operation increased by 9%, effective KMs showing a negative

gure with -1% growth and CPKM for the same period is 9.8%.

From the analysis of the above table it can be concluded the Cost

of Operation over a period of 10 years is increased by 249%,

CPKM is increased by 106% over a period of 10 years i.e. 2005-06

YEAR

200

5-06

200

6-07

2007

-08

2008

-09

2009-

10

201

0-11

201

1-12

201

2-13

2013

-14

201

4-15

Cost of

operatio

n (Rs.in

crores)

422.

49

489.

06

523.

34

589.

71

697.2

0

876.

43

998.

42

115

4.33

1350

.41

147

3.54

Changes

in %

-

16

7

13

18

26

14

16

17

9

Effective

KMs

( in

crores)

26.9

5

29.6

6

30.5

6

32.9

7

38.36

42.9

5

44.6

6

44.8

8

45.7

6

45.4

8

Changes

in %

-

10

3

8

16

12

4

1

2

-1

CPKM

( in Rs)

15.6

8

16.4

9

17.1

2

17.8

9

18.17

20.4

1

22.3

6

25.7

2

29.5

1

32.4

0

Changes

in %

-

7.08

2.03

4.44

1.62

12.2

7

9.56

15.0

3

14.7

4

9.80

ISSN - 2250-1991 | IF : 5.761 | IC Value : 79.96

Volume : 6 | Issue : 3 | - 2017

March

518 | PARIPEX - INDIAN JOURNAL OF RESEARCH

to 2014-15, and the effective kilometers increased only by 68%

over the same period.

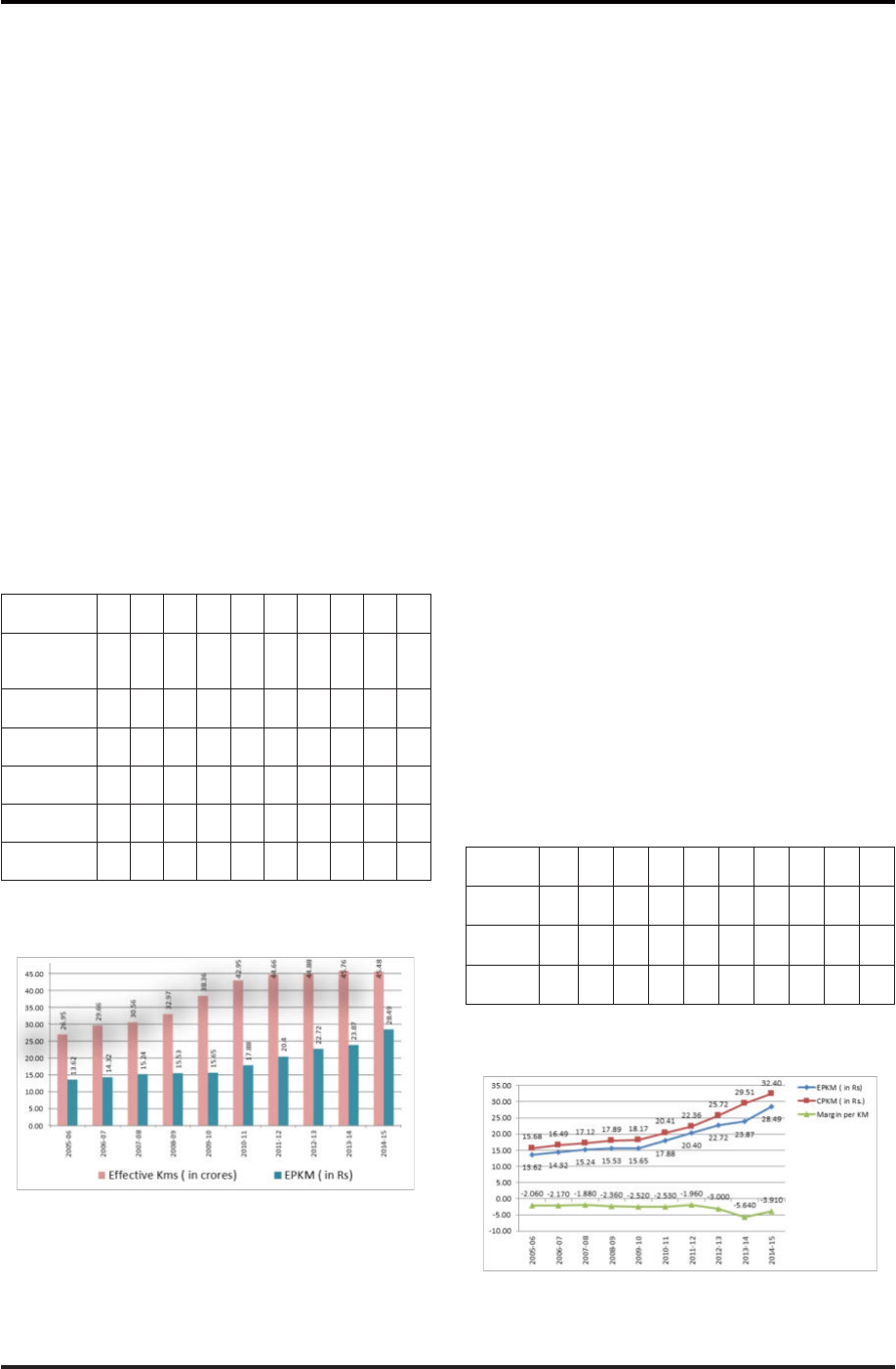

I) EARNINGS PER KILOMETER (EPKM)

Revenue in absolute term without reference to kilometer, hence it

does not correctly reect the Protability of the operation. EPKM is

one of the useful parameter to indicate the earning potential of a

route/depot/division/organization. The EPKM is related to the

carrying capacity of the buses, fare structure and the earning

potential of routes. The EPKM is calculated by dividing total

earnings by total effective kilometers. For any public transport

sector it is desirable to earn higher the EPKM for better nance

management. Making to increasing the revenue is not the easy

task for the corporation like NEKRTC, where revenue generation is

not done on protability factor. The organization has to operate

the schedules in spite of lower earnings and losses some times. But

the management can implement techniques to improve the

earnings per kilometers by rationalizing the schedules and routes.

The Earnings per kilometer is expressed in paisa per kilometer. The

Table No.2 exhibits the earnings per kilometer in Rs.

From the table.2it is observed that from 2005-06 to 2014-15 over

a period of 10 year EPKM increased from Rs.13.62 to Rs.28.49

which represents 109% increase. Trafc revenue over a period of

10 years increased from Rs.424.80 crores to Rs.1296.22 crores

which represents total growth rate of 205%, and effective kms

increased by 68% during the same period of 10 years. In this stage

of analysis it is difcult to analyze whether the % increase in EPKM

is due to operational efciency or due to fare hikes affected during

this period to offset the increase in the cost of operation.

Table No. 2: EARNINGS PER KILOMETERS (EPKM)

Source : Annual Administrative Reports.

EARNINGS PER KILOMETERS (EPKM)

Table 2 reveals that EPKM of the corporation has increased every

year. During the year 2006-2007 Total trafc revenue increased by

15.64%, effective Kms increased by 10% and EPKM increased by

5.07% to its previous year EPKM. During 2007-08 trafc revenue

increased by 9.65%, effective kms by 3% and EPKM increased by

6.41% compares to its previous year EPKM. During 2008-09 and

2009-10 nancial years growth rate trafc revenue is 9.97% and

17.23% respectively, effective kms increased by 8% and 16%

respectively and of EPKM is 1.94% and 0.75% which are the least

growth rate during the tenure of 10 years of study period of 2004-

05 to 2014-15. In 2010-11 trafc revenue increased by 27.89%,

effective kms by 12 % and EPKM hiked by 14.23%. In 2011-12 the

growth rate of trafc revenue increased by 18.67%, effective km

increased by 4 % and EPKM remains same almost 14%. During the

nancial year 2012-13 trafc revenue increased by 11.90%,

effective kms increased only by 1% and EPKM growth rate is

11.33%. In 2013-14 trafc revenue is increased by 16.11%,

effective kms are increased by 2% and EPKM is raised by 5.07% on

its previous year gure. During the nancial year 2014-15 trafc

revenue increased by 9.47% and effective kms showing a negative

gure of 1% on its previous gure and the highest growth rate of

EPKM in 10 years is observed in this year is 19%. By seeing the

above table it can be concluded that from 2005-06 to 2014-15

over a period of 10 year EPKM increased from Rs.13.62 to Rs.28.49

which represents 109% increase. Trace revenue over a period of

10 years increased from 424.80 crores to 1296.22 crores which

represents total growth rate of 205%, and effective kms increased

by 68% during the same period of 10 years. In this stage it is

difcult to analyze whether the % increase in EPKM is due to

operational efciency or due to fare hikes affected during this

period to offset the increase in the cost of operation.

(I) Margin per kilometer (MPKM)

Margin per kilometer refers to the difference between the EPKM

and CPKM for a particular period. In simple words it the prot or

loss margin after operating the shedues by the public transport

corporation. It is also stated as the difference between the total

earnings and total cost distributed by the total kilometers. It is one

of the most powerful technique for analyzing the nancial

performance in public sector like NEKRTC, which easily exhibits the

status of nancial condition. It is desirable to have higher EPKM

over to CPKM for better nancial conditions of the organization.

But being a state run public transportation it is difcult for NEKRTC

to have higher EPKM over to CPKM. Hence various routes and

schedules are operated in the interest of public to facilitate to

travel one place to other place. NEKRTC is public transport

corporation and it can't expect prot on every route/schedule. It is

difcult but also possible to earn the prot in each route provided

the routes are scientically established. In few cases it may not be

totally possible to get prot margin but lot of scope is there for

improvisation in the trafc management to get higher margin in

EPKM over to CPKM.

Table No. 3: MARGIN PER KILOMETR (MPKM)

Source : Annual Administrative Reports.

MARGIN PER KILOMETER. (MPKM)

In Table No. 1 and Table No.2 detailed analysis is done on most

important nancial parameters of NEKRTC, CPKM and EPKM. It is

necessary to understand the margin between these two factors

which is important to analyze the nancial sustainability in longer

YEAR

200

5-06

200

6-07

200

7-08

200

8-09

200

9-10

201

0-11

201

1-12

201

2-13

201

3-14

201

4-15

Trafc

Revenue (Rs.

In crores)

367.

35

424.

80

465.

80

512.

25

600.

49

767.

95

911.

33

101

9.75

118

4.04

129

6.22

Changes in

%

-

15.6

4

9.65

9.97

17.2

3

27.8

9

18.6

7

11.9

0

16.1

1

9.47

Effective Kms

(in crores)

26.9

5

29.6

6

30.5

6

32.9

7

38.3

6

42.9

5

44.6

6

44.8

8

45.7

6

45.4

8

Changes in

%

-

10

3

8

16

12

4

1

2

-1

EPKM ( in Rs.)

13.6

2

14.3

2

15.2

4

15.5

3

15.6

5

17.8

8

20.4

0

22.7

2

23.8

7

28.4

9

Changes in

%

-

5.07

6.41

1.94

0.75

14.2

3

14.1

2

11.3

3

5.07

19.3

6

YEAR

2005

-06

200

6-07

200

7-08

200

8-09

200

9-10

201

0-11

201

1-12

201

2-13

201

3-14

201

4-15

EPKM

(in Rs.)

13.6

2

14.3

2

15.2

4

15.5

3

15.6

5

17.8

8

20.0

4

22.7

2

23.8

7

28.4

9

CPKM

( in Rs.)

15.6

8

16.4

9

17.1

2

17.8

9

18.1

7

20.4

1

22.3

6

25.7

2

29.5

1

32.4

0

MPKM

( in Rs.)

-2.06

-2.1

7

-1.8

8

-2.3

6

-2.5

2

-2.5

3

-1.9

6

-3

-5.6

4

-3.9

1

ISSN - 2250-1991 | IF : 5.761 | IC Value : 79.96

Volume : 6 | Issue : 3 | - 2017

March

PARIPEX - INDIAN JOURNAL OF RESEARCH | 519

period. In 2005-06 and 2006-07 margin per kilometer is -2.06 and

-2.17 respectively. During the nancial year 2007-08 MPKM is -

1.88, which shows improved gure compared to 2005-06 and

2006-07. In the nancial year 2008-09 the gap between EPKM

and CPKM is further increased which represents -2.36. During the

nancial year 2009-10 and 2010-11 MPKM represents -2.52 and

-2.53 respectively. In the nancial year 2011-12 and 2012-13

MPKM represents -1.96 and -3 respectively. Again in 2013-14 and

2014-15 also MPKM is showing negative gures representing -

5.64 and -3.91. During a period of 10 years margin per kilometer

is showing negative gures, from the table it can be analyzed that

always cost per kilometer is higher than the earnings per kilometer,

which indirectly leads to accumulate the loss every year.

(I) GROSS REVENUE:-

Gross revenue of the corporation is the total revenue generated by

the corporation which includes total trafc revenue and total non

trafc revenue. Trafc revenue is the revenue generated by the

corporation from the commuters by operating its schedules/buses

. Non trafc revenue is the revenue generated by the corporation

other than operating the vehicles/buses, such as scrap revenue,

Bus stand shops rent, nes and penalties, advertisements etc.

Further the Gross revenue is the revenue where the various costs

incurred by the corporation are not yet deducted. In other words it

can be said that the Gross revenue is the total revenue receipt

excluding the expenditures.

Gross revenue in NEKRTC is the composition of trafc revenue and

other revenue, which are showing a increasing trend in all the 10

years, excluding 2011-12 where the other revenue represents with

negative growth %. Table 4 shows the increasing trend of trafc

revenue, other revenue and gross revenue put together of trafc

and other revenue. In 2005-06 trafc revenue is Rs 367.35 crores

and in 2014-15 trafc revenue is Rs 1296.22 crores , over a period

of 10 years trafc revenue increased by 252%. Other revenue for

the year 2005-06 and 2014-15 is Rs.27.35 Crores and Rs162.21

crores respectively. The growth rate for the same period is 493%.

The gross revenue in 2005-06 is Rs.394.71 crores and in 2014-15

Rs.1458.43 crores which shows a growth rate of 270% in 10

years. It is seen that growth rate of other revenue is considerably

higher than trafc revenue but, quantum of revenue in terms Rs in

crores is higher in trafc revenue compared to other revenue. It is

good to have increasing growth rate of other revenue but the main

business of the organization is revenue generation trafc which is

very important in NEKRTC for longer survival and nancial stability.

Table No. 4 : GROSS REVENUE

Source : Annual Administrative Reports.

Table 4 exhibits the Gross revenue earned by NEKRTC during the

period from 2005-06 to 2014-15. During the nancial year 2006-

07 trafc revenue increased by 15.64%, other revenue by 26.98%

and Gross revenue by 16.43%. In 2007-08 trafc revenue

increased by 9.65%, other revenue increased by 19.72% and

gross revenue increased by 10.41%. During the nancial year

2008-09 trafc revenue increased by 9.97%, other revenue

increased by 17.39% and Gross revenue increased by 10.58%. In

2009-10 trafc revenue increased by 17.23%, other revenue

increased by 28.76% and gross revenue increased by 18.23%. In

2010-11 trafc revenue increased by 27.89% ,other revenue

increased by 53.41% and Gross revenue increased by 30.31%.

During the nancial year 2011-12 trafc revenue increased by

18.67% but the other revenue showing a negative growth rate of -

28.43%. and growth rate of gross revenue increased by 13.42%.

in the nancial year 2012-13 the trafc revenue increased by

11.90%, other revenue increased by 64.69% and growth rate of

gross revenue is 15.61%. During the nancial year 2013-14 trafc

revenue increased by 16.11%, other revenue increased by

11.45% and Gross revenue increased by 15.64%. In 2014-15

trafc revenue increased by 9.47%, other revenue increased by

28.07% and 11.27 growth rate observed in gross revenue.

Among the 4 nancial factors discussed in this paper the gross

revenue is the factor which is showing a highest growth rate in

tenure of 10 years i.e. from 2005-06 to 2014-15. Gross revenue in

2005-2006 is Rs.394.71 (crores) and 2014-15 it is 1458.43

(crores), it shows total growth rate of 270% of Gross revenue.

Gross revenue is the total income of the corporation before

distributing the expenditures; hence the cost increased every year

as shown in the Table-1, it is necessary for the corporation to make

efforts to increase the Gross revenue. Otherwise gap between the

income and expenditures leads to create a nancial crisis, which is

difcult for the public sector corporation like the NEKRTC.

VII. SUMMARY OF FINDINGS, SUGGESTIONS AND

CONCLUSIONS:

FINDINGS

The present study executed wholly on the secondary data; the

following inferences were drawn on the basis of above data

Ÿ There is considerable gap between the two vital parameters

CPKM and EPKM on which the health of STUs is assessed.

Ÿ The corporation even not operating its schedules in BEP, i.e.,

Break Even Point, therefore if it operates in BEP, the

corporation can manage its cost and revenue with no prot

and no loss business.

Ÿ For the period of the study, the corporation has incurred losses

in every nancial year, due to higher CPKM over to EPKM.

Ÿ CPKM can be controlled by the effective cost control

techniques and EPKM can be increased by effective trafc

management.

Ÿ The corporation is operating its schedule in all the areas

demanded by the passengers without expecting to earn prot

on every schedule.

Ÿ There is no funding from the State Government to any of the

state road transportation corporation for its expenditures;

YEAR

2005

-06

2006

-07

2007

-08

2008

-09

2009

-10

2010

-11

2011

-12

2012

-13

2013

-14

2014

-15

Trafc

Reven

ue

367.

35

424.

81

465.

8

512.

25

600.

49

767.

96

911.

34

1019

.80

1184

.04

1296

.22

Chang

es in

%

-

15.6

4

9.65

9.97

17.2

3

27.8

9

18.6

7

11.9

0

16.1

1

9.47

Other

Reven

ue

27.3

5

34.7

3

41.5

8

48.8

1

62.8

5

96.4

2

69.0

1

113.

65

126.

66

162.

21

Chang

es in

%

-

26.9

8

19.7

2

17.3

9

28.7

6

53.4

1

-28.4

3

64.6

9

11.4

5

28.0

7

Gross

Reven

ue (Rs.

In

cores)

394.

71

459.

57

507.

38

561.

06

663.

35

864.

38

980.

36

1133

.41

1310

.70

1458

.43

Chang

es in

%

-

16.4

3

10.4

1

10.5

8

18.2

3

30.3

1

13.4

2

15.6

1

15.6

4

11.2

7

ISSN - 2250-1991 | IF : 5.761 | IC Value : 79.96

Volume : 6 | Issue : 3 | - 2017

March

520 | PARIPEX - INDIAN JOURNAL OF RESEARCH

therefore, the survival of the corporation is completely

depended on the trafc revenue and other miscellaneous

revenue from its operations.

Ÿ Gross revenue of the corporation is showing an increasing

trend, which has grown up by 5 times of its value in between

2005-06 to 2015-16.

SUGGETIONS

As already discussed above the North East Karnataka Road

Transportation corporation is independent unit among the various

Karnataka state public sectors. Public Transport Undertakings in

Karnataka are nancially independent and have to manage all its

expenditures by way of trafc revenue. Therefore for the longer

survival and continuity of the corporation is completely depended

on its management decision to increase the revenue to meet

breakeven point. From the above analysis and ndings the

following are some of the major suggestions offered for

betterment of the corporation.

Ÿ Cost cut down policy has to be implemented strictly , for those

factors which contributes major part of CPKM, such as staff

cost controlling by avoiding unnecessary overtime schedules,

operating complete schedule without cancellation,

rationalization of schedules, cost control technique in HSD

management, Fuel Management and Tyres management etc

to be implemented by the management.

Ÿ Identifying the potential market of the passengers and

operating the schedules in a single goal to carry each needy

passenger from one place to another place, avoiding

overlapping of timings from bus stands,.

Ÿ The corporation need to convert the loss making schedules to

break even schedules to avoid nancial crises.

Ÿ Optimum utilization of vehicles makes the corporation to

accumulate trafc revenue.

CONCLUSION:

From the above data the study, it can be concluded with the

remarks that NEKRTC is making its efforts to generating trafc

revenue, further it has to emphasize more on route cancellation

and cost control. It is seen in the history of the corporation that

identication of new routes is always protable if the same is done

on the proper analysis and justication. Political interference in

recommending of implementation of routes/schedule is

unavoidable in the state road public sector, but it is always better to

be done with proper analysis of routes and passenger strength.

Though the revenue generation is not the primary objective of the

state transport unit, but the corporation like NEKRTC, it cannot be

run only with the social objectives of service providing to the

commuters, especially when the corporation has to meet its

expenditures on its own business.

References:

01. Prasad, Srinivas, T, and Khan, M.A.A., (1966), “Impact of Social Obligations on the

Financial Performance of SRTUS: A case study of APSRTC”, Indian Journal of

Transport Management, 20(6), pp. 406-418

02. Shambhag, A.R., (1972), “Problems of B.E.S.T. Bus Service”, Transport, vol.22,

pp.17-18.

03. Venkaji Rao, L.C., (1974), “Management of State Transport Undertakings” in D.M.

Nanjundappa (Ed), Transport Planning and Finance, pp. 379-392.

04. Jakaria, (1975), “Analysis of Urban Transportation Criteria”, Transportation

Engineering, Journal (17), pp.114-96

05. Pereira, W., (1975), “Leakage of Revenue in Metropolitan Transport Organization”,

Mobile, pp. 7-9.

06. Sankaraiah, V.V., Subramanya Sarma, (1985), “Urban Transportation by Andhra

Pradesh State Road Transport Corporation – A Depot level performance”. D.

Panduranga Rao (Ed) Problems of Transport in India, Inter India Publications, New

Delhi

07. . Govinda Rajan, (1988), “A study of Development and Performance of SLPES in

Andhra Pradesh”, Institute Public Enterprise Journal, p.78.

08. Lau, Joseph Cho-yam, (1997), “The performance of Public Transport Operations,

Land use and Urban Transport Plans in Hong Kong, Cities, Vol.14, No.3, pp.145-

153

09. Gore, M.L., (1997), “Strategy for Minimizing Vehicle Breakdowns in Transport

Undertakings” Indian Journal of Transport Management, volume 29, Number 9,

p.545

10. Gunadam Rajeswari : “ Public Sector Performance of State Road Transport

Corporation, A case study of Andrapradesh,1998

Cleaner Air and Better Transport in Cities - Making Informed Choices

11. by Tata Energy Research Institute (TERI) (2000)

12. Public Sector Bus Transport in India in the New Millennium A Historical Perspective

by M K Thomas, (2000)

Design and Appraisal of Rural Transport Infrastructure - Ensuring Basic Access for

Rural Communities

13. by Jerry Lebo & Dieter Schelling, for the WORLD BANK (2001)

14. Kharola, P.S. : Reducing the cost of Revenue Collection: an option available to the

STUs.Indian Journal of Transport Management. 2001

15. Transport Concepts in European Cities by Tim Pharoah, Dieter Ape (2002)

16. Kharola, P.S. : “Reforms in the public transport – a systems approach”, Proceedings

of CODATU X Conference, Lomé (Togo), 12-15 November 2002,

17. . Pradeep Singh Kharola, (2004), “The High Capacity Urban Bus: Pre-requisites and

Advantages”, Indian Journal of Transport Management, Vol.28, p.206.Bhasker, G.

& N. V Ramana Murthy, (2004), “Articial Neural Net work: An Efcient to simulate

the protability of State Transport Undertakings. Indian Journal of Transport

Management

18. The Best Transport System in the World by M.H Rose , B.E. Seely, P.F Barrett – The

Ohio State University Press(2006)

19. Transit Villages in the 21st Century by Michael Bernick, Robert Cervero (2007)

20. Kharola, P.S. : "Financing Urban Public Transport". Urban Transport Journal 2008

21. The Geography of Urban Transportation by Susan Hanson (2010)

22. Towards Coordinated Urban Transport Planning In India By Om Praksh Agarwal and

Ishita Chauhan (2010)

23. Prashant Kakade, (2010), “Impact Assessment of the withdrawal of the Daily Pass

System: A Case Study of Bangalore Metropolitan Corporation”, Indian Journal of

Transport Management,

24. Transport Policy and the Environment by David Banister (2010)

25. Prabhu D.B. & Satish Hegde, (2011), “Management Control System in Public

Transport: An Objective Study of Karnataka State Road Transport Corporation”,

Indian Journal of Transport Management

26. Singh, S.K.(2012) Urbanization and Urban Transport in India: The sketch for a

policy.

27. K.Kockelman, D.Chen, K Larsen, B Nichols – The University of Texas (2013)The

Economics of Transportation System : A reference for practitioners .

28. Annual Financial Reports and Annual Administrative Reports of NEKRTC, for the

period of 2004-05 to 2015-2016

ISSN - 2250-1991 | IF : 5.761 | IC Value : 79.96

Volume : 6 | Issue : 3 | - 2017

March

PARIPEX - INDIAN JOURNAL OF RESEARCH | 521