CCA.HAWAII.GOV/INS

@INSURANCEHI

MY INSURANCE DOESN’T COVER WHAT?

Avoid surprises by understanding your insurance policy

Department of Commerce & Consumer Affairs

Insurance Division

MY INSURANCE DOESN’T COVER WHAT?

Avoid surprises by understanding your homeowners insurance policy

Department of Commerce & Consumer Affairs

Insurance Division

TABLE OF CONTENTS

1 My Insurance Doesn’t Cover What? . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . .2

2 Home Inventory . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4

3 Theft . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 5

4 Fire . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6

5 Flooding . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 7

6 Natural Disasters . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 8

7 Preventative Measures and Actions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10

8 What Isn’t Typically Covered . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12

9 The Claims Process . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 13

The State of Hawaii Department of Commerce and Consumer Affairs (DCCA) is a regulatory agency that promotes

a strong and healthy business environment by upholding fairness and public condence in the marketplace. The

department also strives to increase knowledge and opportunity for businesses and individuals, and to protect

consumers against unfair and deceptive business practices.

The DCCA Insurance Division oversees the insurance industry in the State of Hawaii. Its regulatory functions include:

issuing licenses, examining the scal condition of Hawaii-based companies, reviewing rate and policy lings, and

investigating insurance-related complaints.

The National Association of Insurance Commissioners (NAIC) is the U.S. standard-setting and regulatory support

organization created and governed by the chief insurance regulators from the 50 states, the District of Columbia

and ve U.S. territories. The NAIC’s website is a great source of consumer information at www.naic.org.

This guide was created to equip you with information to better prepare for an emergency and understand what

may or may not be covered by their insurance policy or policies. Learn how to protect your biggest investments.

An insurance policy for your home or apartment is supposed to provide a sense of security. But before you get

too comfortable, take time to speak to your agent or insurer to understand what’s covered and what’s not in your

homeowners or renters policy. Don’t make any assumptions.

COMMON MISCONCEPTIONS

“Flood damage is covered by a standard homeowners insurance policy.”

Flood insurance is not covered as part of standard homeowners and renters insurance policies. If you want to be

covered for ood damage, you’ll have to purchase coverage specic to ooding.

Even if a car is parked in your home garage during a ood event, ood damage would only be covered with

comprehensive or other-than-collision coverage.

“Homeowners insurance only covers the structure.”

A typical homeowners policy pays claims for damage caused by certain events to your home, garage, other

structures on your property, as well as your personal property or contents. In contrast, renters insurance only

protects your personal property. Both homeowners and renters insurance offers protection against liability for

accidents that injure other people or damage their property.

“I’m covered under my landlord’s insurance.”

Never assume that the landlord’s insurance covers you or your belongings. Landlord’s insurance only protects the

building.

“Renters insurance is too expensive.”

The average renters insurance policy costs between $15 and $30 per month. Replacing your possessions, nding

another place to stay during repairs, or being liable for an accident on your premises could cost much more.

“Insurance is a waste of money, you should only purchase the minimum required.”

Homeowners or renters insurance is not mandatory but can help protect you from a nancial catastrophe if a

disaster were to occur. Without insurance, you could pay hundreds of thousands of dollars out of pocket to repair

or replace your home.

Always shop around and compare the costs of coverage from different insurers to get the best value.

2

1 MY INSURANCE DOESN’T COVER WHAT?

UNDERSTANDING YOUR POLICY

A standard homeowner or rental insurance policy contains four parts:

• declarations page

• insuring agreement

• exclusions section

• general conditions

A standard homeowners or renters policy generally provides coverage for either the actual cash value or

replacement value of your property with standard building materials. After a loss, you will have to pay your

deductible as outlined in your policy.

There are different types of coverages under a standard home or renters policy. Renters insurance is different from

homeowners insurance in that rental policies only insure the contents, not the structure. Policies vary from company to

company, so be sure you read and understand yours.

REVIEWING YOUR POLICY

Re-evaluate your risk prole at least once a year to ensure your existing homeowners policy provides the protection

you and your family need. Plan to review your policy at the same time each year. Ask yourself:

• Am I not at risk? Are earthquakes, oods, wildres or other disasters now a threat?

• What has changed in my home? Did the number of people (and belongings) increase or decrease? Have I

made any major purchases?

• Have I updated my home with a kitchen renovation, new security system or other improvements?

• Should I be looking at different coverage? Can I save money by bundling my home and auto insurance?

• Do I have a home inventory?

3

PREMIUM COMPARISON GUIDES

Check out the Insurance Division’s annual Premium Comparison Guides available online at

cca.hawaii.gov/ins/resources/.

This is a free resource that helps to compare rates, explore coverage options and save money on your homeowners,

condominium unit owners, renters, and motor vehicle insurance.

2 HOME INVENTORY

ARE YOU PREPARED?

More than half of Americans don’t have a list of their possessions according to a National Association of Insurance

Commissioners (NAIC) survey.

Without an accurate inventory, you may not have the right home or rental insurance coverage. Because needs

change, you should create an inventory of your possessions every year. Without this checklist, you may forget to

claim items lost due to re or another covered event. Create one to catalog your personal property and include

photos or video of each room.

The NAIC offers the myHOME Scr.APP.book app to

help you capture images, descriptions, bar codes and

serial numbers of personal possessions and stores the

information electronically for safekeeping.

The app organizes information by room and creates

a back-up inventory for email sharing. This is a great

option to have an inventory that is in a safe, separate

and accessible location.

Be sure to share the inventory with your agent or in-

surer. Periodically update the list as you acquire new

things.

4

3 THEFT

I’M COVERED IF SOMEONE BREAKS IN AND STEALS MY STUFF, RIGHT?

Most standard homeowners and renters insurance policies cover items that have been stolen (up to your policy

limits). Most basic home insurance policies have standard limits for big ticket items like electronics or sporting

equipment.

Be aware that certain categories like jewelry, antiques,

art and other items often have limits as well. If valuable

items exceeding those limits are stolen or damaged and

you don’t have coverage for them, you may receive

payment far less than value. Talk to your agent or insurer

to discuss limits and special coverage.

If your children are college students, enrolled in classes

and living in on-campus housing, your homeowners policy

may extend to their belongings they take with them.

Personal property stolen from a dorm room or even while

studying, such as a laptop stolen while at the library, may

be covered.

5

4 FIRE

WHAT IF THERE’S A FIRE?

A typical policy will issue payment to replace or repair anything inside the home damaged by ames, smoke, soot,

and ash. While re and lightning are usually covered, don’t be surprised if your insurance company asks for an

inventory. The company is only required to pay for personal property you can prove you owned at the time of loss.

Make sure you’re prepared.

6

WILL MY HOMEOWNERS POLICY COVER DAMAGE FROM LAVA?

Each company’s policy is different and homeowners should contact their insurer to review their specic policy

coverage. If heat generated by a lava ow caused a re that damaged your home, then those damages may be

covered as a re peril under most standard market policies. If time permits, mitigate the amount of damage by

removing as much as possible from your home. Even if your home is not damaged, the lava ow may cut off access

to homes, businesses and belongings.

DOES INSURANCE COVER EXPLOSIONS?

Standard homeowners and rental policies will cover damage caused by explosions due to causes such as a gas

leak. However, if an act of terrorism causes an explosion, the damage will not be covered. Likewise, if your

neighbor is experimenting with unauthorized chemicals, damage to your home will be covered. However, if you are

doing such an act, damage to your home will not be covered.

5 FLOODING

MY PLACE FLOODED, NOW WHAT?

Homeowners and renters insurance generally do not offer protection against ood losses. Check your policy’s

exclusions; it will probably be listed under “water damage.”

Flooding includes any water or mud moving or accumulating on the outside of the home and nding its way inside.

You should consider ood insurance even if you don’t have waterfront property as ooding can happen anywhere.

Flood insurance is available under a separate policy through the National Flood Insurance Program (NFIP). Private

insurers may also provide primary and excess ood coverage in Hawaii.

Water damage inside your home caused by improper maintenance may not

be covered. You can mitigate your risk by regularly inspecting your home for

signs of leaks, musty odors, and dampness around pipes and appliances that

use water. You can also install a smart water sensor that alerts you to potential

leaks similar to a re alarm.

7

If you suffer from any damages after a ood event, contact your insurance agent or company rst. Inform them

of any damages and see what may be covered. Your policy might require that you make the notication to your

insurance agent or insurer’s claim hotline within a certain time frame.

Remediation efforts could help reduce the severity of damage to your property as well. Opening windows, utilizing

fans, and drying off as much as you can as soon as possible will help to reduce the chance of mold. Be cautious of

foundational damage, and if outside, stay away from moving water.

WHAT ABOUT FLOOD DAMAGE TO MY CAR?

Your homeowners or renters insurance wouldn’t cover any damages to your car regardless if it was parked on your

property or in your garage. Motor vehicle insurance may cover it if you have comprehensive or other-than-collision

coverage. This is separate from the required coverages you need to legally drive your car.

Comprehensive coverage pays, subject to your deductible, for losses to your car caused by theft, re, windstorm,

ood, falling objects, and vandalism. However, it does not cover personal property that is lost or damaged in

your vehicle. Comprehensive or other-than-collision coverage is limited to the value of your car at the time of the

accident or loss. Ask your agent or insurer if this coverage is right for you.

8

WHAT ABOUT NATURAL DISASTERS LIKE EARTHQUAKES, TORNADOES AND

HURRICANES?

Damage caused by earthquakes is not usually covered in a standard homeowners or renters policy. If you want

earthquake coverage, you need to purchase it separately. Earthquake insurance will only cover you for what is

stated in the policy. It will not replace everything you lost.

Hurricane insurance can supplement home insurance by covering wind-related damage associated with hurricanes,

which can bring heavy rains, strong winds, ying debris, and tidal surges. Just remember that homeowners and

hurricane insurance do not cover most instances of ooding even during a storm. Flood insurance applies when

water seeps or rushes into a home or structure during a storm.

Hawaii residents should consider ood and hurricane insurance. A ood insurance policy purchased through the NFIP

has a waiting period of 30 days before it takes effect, so act now.

6 NATURAL DISASTERS

WHAT TYPE OF DAMAGE IS COVERED UNDER MY HOMEOWNERS POLICY VERSUS

A POLICY THAT COVERS HURRICANES?

The language contained inside the policies outlines what triggers a hurricane policy to become effective.

Most companies have a “72-hour clause.” This means that once a hurricane “watch” or “warning” is issued by

Central Pacic Hurricane Center of the National Weather Service, damage sustained during the 72-hour period

following the issuance of the watch or warning should be covered under a policy that covers hurricanes. Even if the

hurricane did not make landfall, damages occurring within the 72-hour period would still most likely fall under a

hurricane policy. Similar to ood insurance, some policies that cover hurricanes may have waiting periods before

they take effect.

Policyholders should talk with their agent or insurer to nd out the specic language in their policy that references

when a hurricane policy will be triggered.

WHAT’S THE DIFFERENCE BETWEEN A HURRICANE WATCH AND

WARNING?

TROPICAL STORM OR HURRICANE

WATCH

The National Weather Service issues a tropical storm

or hurricane watch for an area

48 hours

prior to when it expects hurricane or tropical storm

conditions to materialize.

During a watch, tune into NOAA Weather Radio All

Hazards, local radio, or television for information and

conduct outside preparedness activities.

TROPICAL STORM OR HURRICANE

WARNING

The National Weather Service issues a tropical storm

or hurricane warning for an area

36 hours

prior to when weather conditions for a tropical storm

or hurricane are expected.

During a warning, complete storm preparations and

immediately leave the threatened area if directed by

local ofcials.

9

10

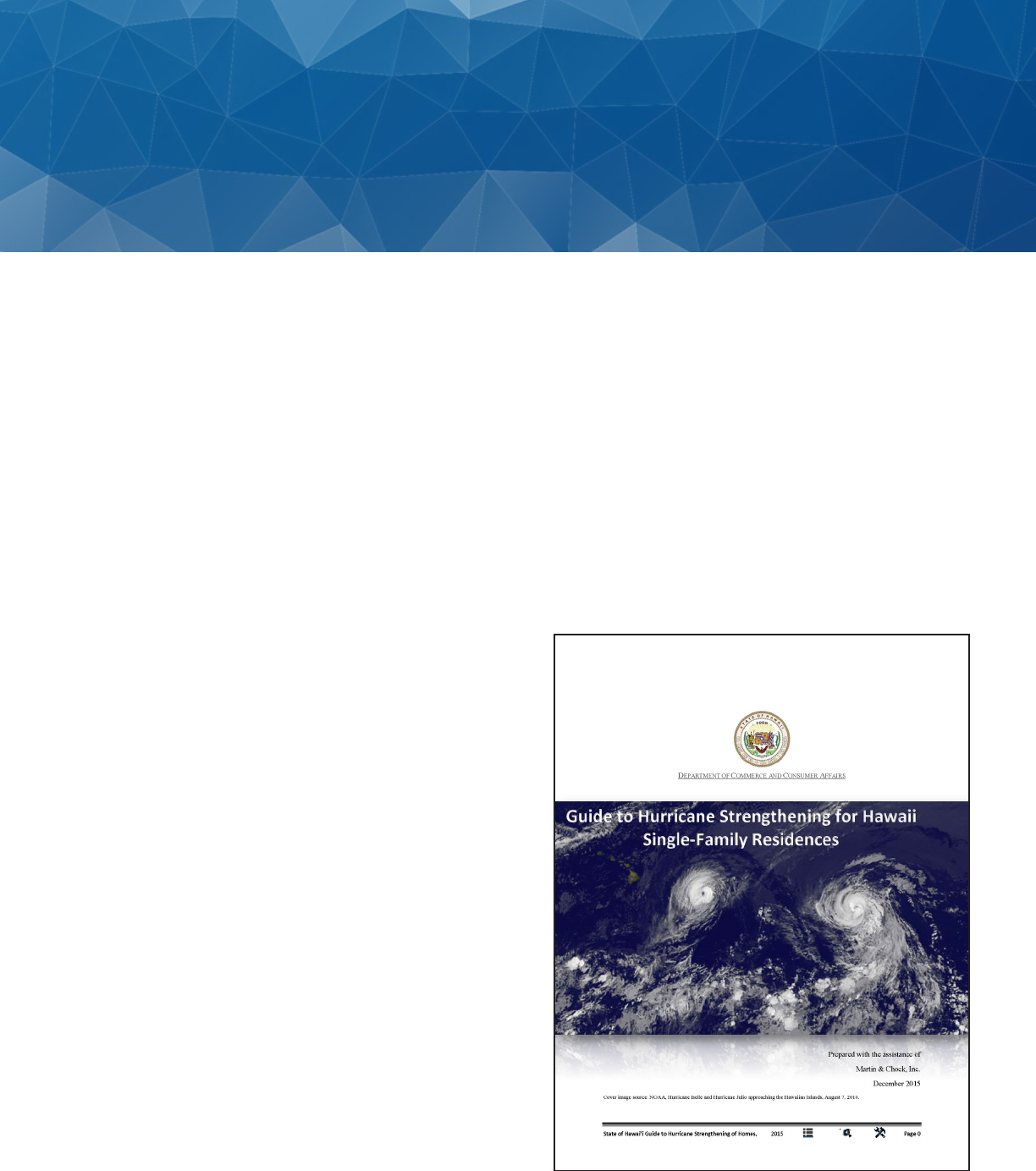

CAN HOMES BE BETTER PROTECTED AGAINST WIND DAMAGE?

Yes, there are hurricane clips for roof to wall connections, window opening protective shields, and roof to ground tie

down systems. Some insurers provide premium credits or discounts for these types of retrots.

Learn more on what you can do to protect your home before the next hurricane season. The Guide to Hurricane

Strengthening of Hawaii Single-Family Residences provides techniques with drawings and references for strengthening

existing homes. The guide was produced by engineers at Martin & Chock for the Hawaii Hurricane Relief Fund.

Learn about installing hurricane-resistant roong components, connectors to walls and foundations, and hurricane

safe rooms.

Find the guide online at

cca.hawaii.gov/ins/resources/.

Guide to Hurricane Strengthening of Hawaii

Single-Family Residences

7 PREVENTATIVE MEASURES AND ACTIONS

IS THERE ANYTHING I CAN DO TO FURTHER PROTECT MY FAMILY AND HOME?

Before a storm or incident takes place, consider the following tips:

□ Review your policy and coverages. Re-evaluate your risk prole at least once a year to ensure your existing

homeowners policy provides the protection you and your family need. Plan to review your policy at the same

time each year. Note additional coverage you may need including ood and hurricane.

□ Take steps to mitigate some of the potential damage to your home from natural disasters. Begin with

a survey of your home and the area around your home to identify objects like yard debris that could

compound damage to your home in high winds or under threat of wildre.

□ If you need to evacuate your home, turn off all utilities and disconnect appliances to reduce the chance of

additional damage and electrical shock when utilities are restored.

□ Keep a readily available list of 24-hour contact information for your insurance agent and insurance

company. Make a list that includes your policy numbers, your insurance company and insurance agent’s phone

numbers, website addresses and mailing addresses. Also, check to see if the company or your agent has set

up an emergency information hotline in case of storm damage. It is a good idea to store this information, and

a home inventory, in a waterproof/reproof safe or a safe deposit box. Also consider sending an electronic

copy to someone you trust. If you have to evacuate your home, you want this information to be easily

available to you.

□ Take inventory (photos or videos) of property and belongings. A home inventory can be invaluable when

deciding how much insurance your life situation requires to adequately insure your home in the path of a

natural disaster.

□ Ensure the safety of yourself and family. Identify what shelters may be available and prepare an evacuation

plan. Choose two meeting places: one right outside your home in case of a sudden emergency, such as a re;

and one outside your neighborhood in case you can’t return home.

11

WHAT ELSE ISN’T TYPICALLY COVERED BY HOMEOWNERS INSURANCE?

Other perils that are not usually covered include: war, nuclear accident, landslide, mudslide, sinkhole and any others

listed in your policy. The type of coverage varies based on the insurer.

12

Review your policy to see what is specically included and excluded in your coverage.

Speak with your agent or insurer before a storm hits or an incident occurs to get a better idea of what type of

coverage you have, the potential out-of-pocket expenses that might be incurred, and to purchase additional

coverage you may need such as earthquake, ood, sewer backup and other coverage additions. Don’t wait until it’s

too late.

war

nuclear

accident

landslide

mudslide

sinkhole

earthquake ood sewer backup

8 WHAT ISN’T TYPICALLY COVERED

Another loss not typically covered is damage due to normal wear and tear. Insurance is meant to protect against

unforeseen losses which means wear and tear is not commonly covered by standard homeowners, renters and motor

vehicle insurance.

However, replacement cost coverage may be available. Replacement cost is the amount it would take to replace

or rebuild your home or repair damages with materials of a similar kind and quality, without deducting for

depreciation. Note that sublimits may still apply, read your policy and talk with your agent or insurer to gauge the

additional cost and see if it’s right for you.

WHAT SHOULD I DO IF I HAVE A CLAIM?

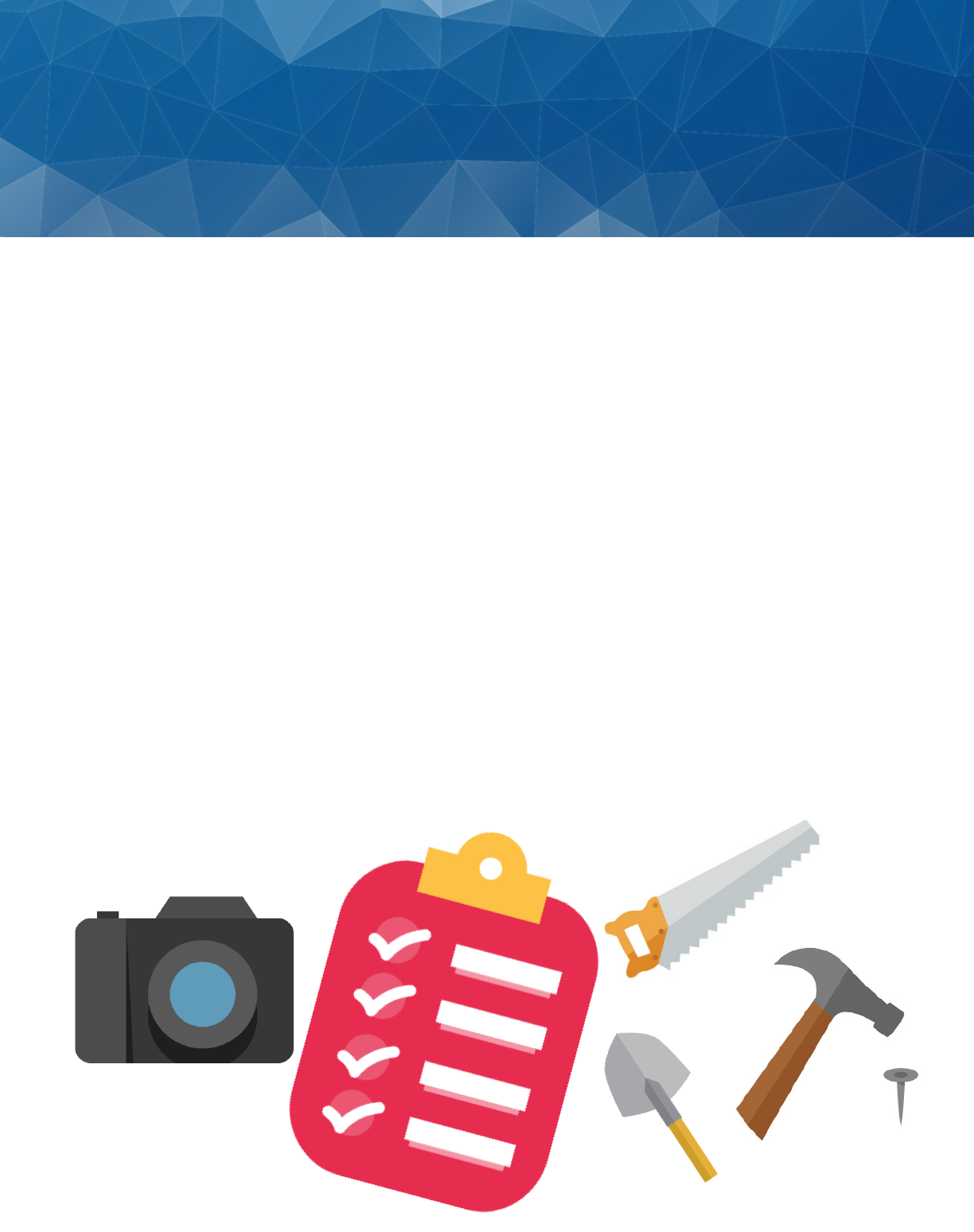

Residents that need to le a claim should:

• Check for damage. If possible, take photographs or video of the damage.

• Secure your property to prevent further damage (keep receipts for any materials used).

• Report your damage to your insurance company or agent (make a claim).

• If your home or condominium is uninhabitable, ask if your policy covers the cost of temporary/alternative

housing.

• Submit proof of loss form or other claim forms if requested by your insurance company.

• Set damaged items aside for later review/inspection by your adjuster.

• Don’t begin permanent repairs until damage is inspected by your adjuster or told to do so by your insurer.

• Work with your adjuster and contractor to estimate the cost of repairs.

• Receive settlement check and begin repairs.

There may be supplemental payments issued by your insurance company if additional damage is uncovered in the

course of repairs.

Be careful of scams. Do not sign your entire claims check over to a contractor.

If the damage to your home is extensive and you have a mortgage, your claim check may list you and your

lienholder as payees.

9 THE CLAIMS PROCESS

13

14

WHAT HAPPENS IF MY DEDUCTIBLE EXCEEDS THE AMOUNT OF DAMAGE TO MY

PROPERTY AND BELONGINGS?

If the damage is estimated to be less than the deductible, the policyholder won’t receive a check from the insurer

and must pay for the repairs and/or replaced items out-of-pocket.

If the amount of damage exceeds the deductible, the insurance company will issue a check for the amount less the

deductible. Policyholders do not need to come up with the money for the deductible to receive a payment from the

insurance company.

It is important to review the deductible amount when a policy is purchased to ensure that this amount can be paid in

the event of a disaster.

HOW DOES THE CLAIMS PROCESS WORK?

Don’t let bills or receipts pile up. Call your agent or insurance company’s claims hotline as soon as possible. Your

policy may require you to make the notication within a certain time frame. Be certain to give your insurance

company all the information they need when ling a claim. Incorrect or incomplete information will only cause a

delay in processing your claim.

Once a claim is led, the insurance company will assign a claims adjuster to assess the damage and determine the

payment. We encourage homeowners to jot down notes and keep track of the dates of any conversations between

the insurance agent and/or adjuster including the date, name and title of the person you spoke with, and what was

said. Also keep a record of your time and expenses.

WHAT IF THERE IS A DISAGREEMENT ABOUT THE CLAIM SETTLEMENT?

If there are disagreements, ask the company for the specic language in the policy that is in question. Find out if the

disagreement is because you and the insurance company interpret your policy differently. Don’t be afraid to ask

questions.

If this disagreement results in a claim denial, make sure you obtain a written letter explaining the reason for the

denial and the specic policy language under which the claim is being denied. If an agreement isn’t reached,

consumers can contact the Hawaii Insurance Division.

STATE OF HAWAII

DEPARTMENT OF COMMERCE AND CONSUMER AFFAIRS

INSURANCE DIVISION

335 Merchant Street, Room 213

Honolulu, HI 96813

cca.hawaii.gov/ins

Additional information available at,

naic.org and insureuonline.org.

SEPTEMBER 2018