1

Tsunami risk and information shocks: Evidence from the Oregon

housing market

Amila Hadziomerspahic

1

Oregon State University

September 2021

PRELIMINARY DRAFT – PLEASE DO NOT CITE WITHOUT PERMISSION

Abstract: Estimating risk perceptions related to natural disasters is critical to understanding behavioral

responses of individuals and adaptive capacity of communities. Developed coastlines experience hazard

risk from sources with different frequency and intensity, such as flooding, erosion, and sea-level rise. In the

Pacific Northwest, there is an additional high severity but very low frequency risk: the Cascadia Subduction

Zone earthquake and tsunami. This paper investigates the impact of tsunami risk information on coastal

residents’ risk perceptions, as capitalized into property prices, using difference-in-differences and triple

differences hedonic frameworks. I study the coastal Oregon housing market response to three sets of risk

signals: two exogenous events - the March 11, 2011 Tohoku earthquake and tsunami and the July 20, 2015

New Yorker article “The Really Big One”; a hazard planning change – the 2013 release of new official

tsunami evacuation maps; and visual cues of tsunami risk – blue lines indicating the spatial extent of the

hazard zone installed by Oregon’s Tsunami Blue Line project. For the first analysis, results suggest that a

property inside the primary tsunami inundation zone sells for 6.5-8.5% less than a property outside of the

zone after the Tohoku event, with a return to baseline levels within 2.5 years. For the second analysis, I find

evidence that the 2013 hazard planning change was capitalized into home values in only the most vulnerable

new inundation zone. For the third analysis, results suggest houses near blue lines may be selling for 8.0%

less compared to houses farther away. The potential risk discounts identified in these analyses suggest that

tsunami risk signals can be salient to coastal residents.

Keywords: Natural hazard risk, tsunamis, hedonic models, difference-in-differences, triple differences

JEL codes: Q51, Q54

This research was supported by Oregon Sea Grant under award no. NA18OAR170072 (CDFA no. 11.417)

from NOAA’s National Sea Grant College Program, US Department of Commerce, and by appropriations

made by the Oregon State Legislature. Housing data provided by Zillow through the Zillow Transaction

and Assessment Dataset (ZTRAX). More information on accessing the data can be found

at http://www.zillow.com/ztrax

. The results and opinions are those of the author and do not reflect the

position of Zillow Group.

1

Ph.D. candidate at Oregon State University, Department of Applied Economics, 322 Ballard Extension Hall, Corvallis, OR 97331.

E-mail: [email protected]

.

2

1 Introduction

Severe but low frequency events pose a unique challenge for hazard planning. The connection between risk

perception about catastrophic events and preparedness action is still much disputed (Wachinger et al.,

2013). The risk of a catastrophic natural disaster must be salient to the people it will impact to translate into

personal preparedness. If the risk is either not salient to individuals or does not translate into behavior

change, it may fall on policymakers to correct the market failure to internalize risk and increase resilience.

The Pacific Northwest of the United States (U.S.) is facing such a challenge. There is a 7 to 15

percent chance for a major earthquake (up to 9.2 in magnitude) to occur in the next 50 years along the

Cascadia Subduction Zone (CSZ) (OSSPAC, 2013). In Oregon, preparedness for such a large seismic event

is low. A recent study estimated that economic losses could be more than $30 billion – almost one-fifth of

Oregon’s gross state product – and fatalities due to the combined earthquake and tsunami could be more

than ten thousand (OSSPAC, 2013). Coastal communities in the tsunami zone are especially vulnerable

since they will experience the strongest earthquake motions due to their proximity to the fault, will be

subject to multiple tsunami inundations, and will account for the majority of expected fatalities (OSSPAC,

2013; Schulz, 2015b).

Individual Oregonians can increase their resilience by retrofitting their homes, purchasing

earthquake and flood insurance, or moving away from high-risk areas such as the tsunami inundation zone.

Whether individuals will take action to prepare themselves depends in part on their beliefs about the risk of

a Cascadia earthquake and tsunami occurring in their lifetimes. If Oregonians’ subjective risk perceptions

underestimate the objective probability of a Cascadia event – if the risk is not salient – then they will likely

underprepare themselves. This gap between subjective risk perceptions and objective risk is plausible given

that Oregon has not experienced a major earthquake and tsunami in recent history – the last CSZ earthquake

and tsunami occurred in 1700 – and has low resilience compared to countries, like Japan and Chile, that

regularly experience earthquakes (OSSPAC, 2013). The lack of recent earthquakes has led Oregon to also

be less prepared and more vulnerable than its neighboring states of California and Washington (Totten,

2019). This motivates an important question about tsunami risk perceptions: Can new information about

the risk of a Cascadia earthquake and tsunami change people’s risk perceptions and narrow the gap between

subjective and objective risk? Here, I investigate whether a risk discount is present in coastal Oregon

housing markets following exogenous information shocks about tsunami risk. I study the housing market’s

response to three sets of risk signals: 1) two exogenous events – the March 11, 2011 Tohoku (Japan)

earthquake and tsunami and the July 20, 2015 New Yorker article “The Really Big One”; 2) a hazard

planning change – the release of new official tsunami evacuation maps in 2013 by the Oregon Department

of Geology and Mineral Industries (DOGAMI); and 3) visual cues of tsunami risk – the Tsunami Blue Line

3

project, which installed signage denoting the upper limit of the tsunami inundation zone in communities

along the coast.

Using a dataset of residential property transactions for the Oregon coast (Zillow, 2020), I estimate

the treatment effects of these tsunami risk signals in a series of hedonic difference-in-differences (DID) and

triple differences (DDD) frameworks. First, I use information from the northern Oregon coast housing

market to estimate the impact of two exogenous events that represent “pure” or “distant” information shocks

in that there is no actual disaster event or that the disaster event is distant and there is little associated local

damage. An increased volume of Google searches suggest that these events were salient to Oregonians and

may be a mechanism by which individuals update perceptions of risk related to the potential for a major

Cascadia event. I test how these information shocks capitalize into home values in the three northernmost

coastal counties in Oregon (Clatsop, Tillamook, and Lincoln). I differentiate risk using a regulatory tsunami

hazard line as the treatment boundary since the entire coastline is likely to face similar impacts from an

earthquake. Results suggest that a property inside the regulatory tsunami inundation zone sells for 6.5 -

8.5% less than a property outside of the zone after the Tohoku event. This result is robust to a number of

alternative specifications, including the Oaxaca-Blinder estimator, four post-matching estimators, and an

event study specification. I find that the effect is short-lived as property prices inside the inundation zone

quickly return to baseline levels within 2.5 years of the Tohoku event.

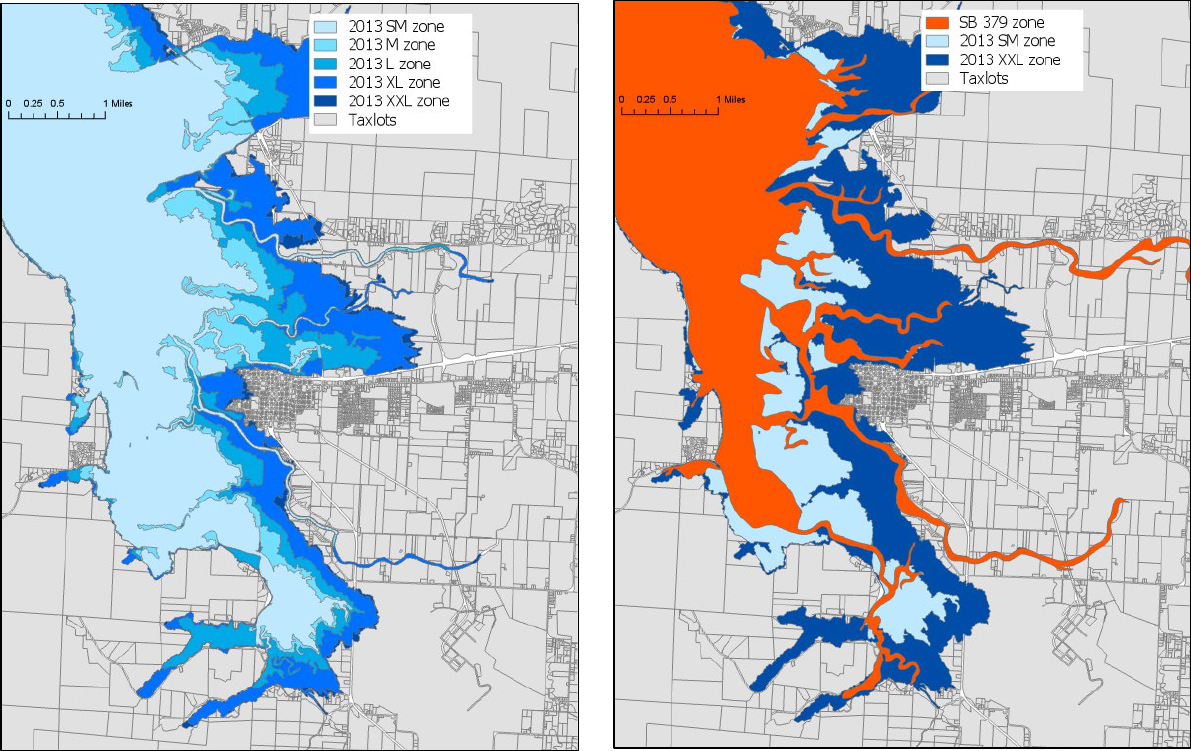

I then use housing information from the entire Oregon coast to estimate the impact of the 2013

update of official tsunami inundation and evacuation maps based on a new series of modeled inundation

maps for five CSZ scenarios (S, M, L, XL, XXL) (DOGAMI, n.d.-a). The largest of this series – the XXL

scenario – became the inundation line for official tsunami evacuation brochures and signage, supplanting

the original and more conservative inundation line that was established in 1995 through Senate Bill 379.

This hazard planning change represents a tsunami risk signal – and a “pure” information shock – about

houses that were not in the original 1995 SB 379 evacuation zone but found themselves inside one of the

new 2013 inundation zones. I find the estimates are not statistically significant for the XXL, XL, L or M

tsunami inundation zones. The DID and Oaxaca-Blinder estimators for the smallest inundation zone (SM)

suggest that homes that were not in the original tsunami inundation zone but are now in the most vulnerable

inundation zone sell for 17 - 27% less after the map update. This risk discount does not have a statistically

significant decay effect.

Lastly, the Tsunami Blue Line project has installed thermoplastic blue line signs on the 2013 XXL

tsunami inundation line on roads in several coastal communities since its launch in 2016 (Office of

Emergency Management, 2016). The blue lines are visual cues of tsunami risk and their installation

represents a tsunami risk signal and a “pure” information shock to properties near those blue lines. To

determine whether this project resulted in a risk discount for homes near the blue lines and inside the

4

tsunami evacuation zone, I estimate the effect of the blue lines on property prices, with properties

differentiated by proximity to the blue lines and – for a DDD approach – by the XXL tsunami inundation

zone. Results from my preferred standard two-way fixed effects (TWFE) DID model suggest there is an

8.0% risk discount for properties that are within 1000’ of a blue line. The DDD results for this model are

not statistically significant, suggesting homebuyers attend to the visual cue but not the risk signal given by

the tsunami inundation zone. However, since the blue lines were installed at different times, there is

variation in treatment timing. Several recent studies have pointed out problems with interpreting the results

of the standard TWFE DID regression when the treatment effect is heterogeneous over time (Borusyak &

Jaravel, 2017; de Chaisemartin & D’Haultfœuille, 2020; Goodman-Bacon, 2018; Sun & Abraham, 2020).

To explore this further I first assess the robustness of the TWFE estimator to heterogeneous treatment

effects using the measure proposed by de Chaisemartin and D’Haultfœuille (2020) and then I estimate two

new estimators that are valid in the presence of treatment effect heterogeneity (Callaway & Sant’Anna,

2020; de Chaisemartin & D’Haultfœuille, 2020). Using de Chaisemartin's and D’Haultfœuille's (2020)

approach, I find a large, negative, but not statistically significant effect. The data for this analysis is too

sparse to be able to estimate most of Callaway's and Sant’Anna's (2020) group-time average treatment

effects. Treatment effect heterogeneity could be a problem for this analysis, however, this dataset is

composed of small, rural communities so I do not have the power to precisely estimate treatment effects

that account for treatment effect heterogeneity.

This work contributes to the hedonic literature on catastrophic risk and the impacts of information

on subjective risk perceptions. This paper is one of few studies that attempts to measure the effects of “pure”

or “distant” information shocks in that either there is no actual disaster event, as in the case of the 2015

New Yorker article, 2013 evacuation map change, and the Tsunami Blue Line project, or that the disaster

event is distant and there is little associated local damage, as in the case of the 2011 Tohoku earthquake

and tsunami (Atreya & Ferreira, 2015; Brookshire et al., 1985; Gibson & Mullins, 2020; Gu et al., 2018;

Hallstrom & Smith, 2005; Nakanishi, 2017; Parton & Dundas, 2020). To my knowledge, this paper is also

the first to investigate the tsunami risk discount in property values disentangled from the earthquake risk

discount. Previous studies have explored either the combined earthquake and tsunami risk or the earthquake

risk alone (Beron et al., 1997; Brookshire et al., 1985; Gu et al., 2018; Nakanishi, 2017; Naoi et al., 2009).

This study’s results also contribute to the literature on risk salience (Kask & Maani, 1992; Nakanishi, 2017)

and the link between risk perception and preparedness action (Wachinger et al., 2013).

My results have important risk communication and policy implications for the Pacific Northwest.

Research shows that Oregon is chronically under-prepared for a Cascadia earthquake and tsunami

(OSSPAC, 2013). Policymakers and emergency managers will need to communicate risk more effectively

to increase risk salience and induce individual decision-makers to take appropriate preparedness actions.

5

Some recent policy changes have even done the opposite. House Bill 3309, passed and signed in June 2019

with nearly unanimous bipartisan support in both the Oregon House and Senate, overturns a nearly 25-year-

old law prohibiting new schools, hospitals, jails, police stations, and fire stations from being built in the

tsunami inundation zone (Oregonian, 2019). Efforts such as this run counter to Oregon’s dual policy

challenge of increasing risk salience and preparedness actions. The potential risk discounts identified here

suggest that at least three types of tsunami risk signals – exogenous events, hazard planning changes, and

visual cues – may be salient to coastal residents. These results suggest that “pure” or “distant” information

shocks can shift homebuyers’ subjective risk perceptions to better match the objective risks of the Cascadia

event. Thus, according to these findings, policies and other “pure” information shocks may be able to

successfully communicate the risk of a Cascadia event and induce individuals to take preparedness actions.

And given Oregon’s current and chronic under-preparedness for a Cascadia event, additional policies – or

risk signals – are needed to mitigate hazard risk.

This paper proceeds as follows. Section 2 reviews the hedonic literature on risk and hazards, along

with empirical strategies to investigate price differentials across hazard zones and the persistence of risk

premium changes. Section 3 describes the study areas and their policy and news backgrounds. Section 4

describes the data collected and some key data limitations. Section 5 defines my empirical approach and

discusses identification strategies for all three analyses. Section 6 presents results for all three analyses.

Section 7 concludes by providing a summary of my current findings, potential next steps to identify these

risk signals, and implications for resilience planning and policy.

2 Hazards and housing markets: previous research

The property attribute of interest in this paper is subjective tsunami risk and I use hedonic frameworks to

test whether three different types of tsunami risk signals capitalize into coastal Oregon property values.

Rosen's (1974) seminal paper was the first to show that regressing observed product prices on their

attributes can reveal buyers’ marginal willingness-to-pay (MWTP) for individual attributes of a

differentiated product.

2

Modern hedonic property models typically rely on the foundational assumptions

that the total supply of housing is fixed and implicit marginal prices represent market equilibria (Hanley et

2

Kuminoff and Pope (2014) point out that the parameters estimated by panel models such as difference-in-differences are not

necessarily theoretically equivalent to the parameters (MWTP) identified by the reduced-form (first-stage) hedonic model. Rosen’s

model considers market equilibrium, not the equilibrating process that would follow an exogenous change in product attributes. If

we are willing to make the assumption that the gradient of the price function is constant over the duration of the study period, then

we can interpret the panel model coefficients as MWTP values (Kuminoff & Pope, 2014). This is a strong assumption for study

periods that span potentially large changes in house and neighborhood attributes – such as the eight-year duration of the first

analysis (2009-2017). Therefore, I interpret the coefficient estimates from my hedonic approach as capitalization effects, not

MWTP, because they describe how the change in the attribute of interest was capitalized into housing prices over time.

6

al., 2007). Since Rosen (1974), many studies have used this method to estimate capitalization of risk factors

in housing prices.

Previous literature has used hazard events or regulatory hazard delineation to identify the impact

of risk on housing prices. In one of the first studies of its kind, Brookshire et al. (1985) found significant

discounting of housing prices in zones with high earthquake risk in California following the passing of an

earthquake risk disclosure law in 1974. The majority of hedonic earthquake risk studies have examined the

impacts of specific earthquake events (Beron et al., 1997; Gu et al., 2018; Naoi et al., 2009). Other hedonic

studies that investigate earthquake risk impacts without the occurrence of a local seismic event have

nonetheless focused on locations like California and Japan where earthquakes have occurred in recent

memory (Brookshire et al., 1985; Nakanishi, 2017). Hedonic models have also been used to measure risk

premiums for natural hazards like floods (Atreya et al., 2013; Kousky, 2010), hurricanes (Bakkensen et al.,

2019; Bin & Landry, 2013; Gibson & Mullins, 2020; Hallstrom & Smith, 2005), wildfires (McCoy &

Walsh, 2018), and coastal storm surge (Dundas, 2017; Qiu & Gopalakrishnan, 2018), as well as man-made

sources of risk like proximity to fuel pipelines (Hansen et al., 2006) and hazardous waste sites (McCluskey

& Rausser, 2001).

Recently, difference-in-differences (DID) approaches have been used to show that disaster events

can increase house price differentials across hazard zones (Atreya et al., 2013; Bakkensen et al., 2019; Bin

& Landry, 2013; Gibson & Mullins, 2020; McCoy & Walsh, 2018; Nakanishi, 2017; Naoi et al., 2009).

The quasi-experimental DID approach uses a recent disaster as an exogenous information change to

separate properties into a treatment group that experiences the disaster event and a control group that does

not. The idea behind this approach is that the disaster event provides new information that causes a change

in the level of subjective risk that may capitalize into house prices. Temporal variation in the attribute of

interest is used to difference out time-invariant omitted variables that would otherwise confound

identification. The DID approach allows us to isolate contemporaneous effects, such as macroeconomic

shocks or housing supply changes, and measure only the effect attributable to the exogenous risk signal.

Triple differences (DDD) has also been used to recover amenity and disamenity effects on property prices

(Bakkensen et al., 2019; Muehlenbachs et al., 2015; Qiu & Gopalakrishnan, 2018). In the hazard risk

literature, the DDD approach has typically exploited an additional treatment (control) group that is more

(less) sensitive to the treatment, i.e., the DDD estimator compares the DID estimator for observations

considered to be more sensitive to the treatment to the DID estimator for observations that are less sensitive

to the treatment.

Information available to housing market participants can change due to a catastrophic event, media

coverage, or new laws (Bakkensen et al., 2019; Bin & Landry, 2013; Brookshire et al., 1985; Gibson &

Mullins, 2020; Hallstrom & Smith, 2005; Kask & Maani, 1992; Kousky, 2010; McCluskey & Rausser,

7

2001; McCoy & Walsh, 2018; Parton & Dundas, 2020; Qiu & Gopalakrishnan, 2018). Kask and Maani

(1992) were the first to show that consumers’ subjective probabilities may under or overestimate objective

probabilities, biasing hedonic prices under conditions of uncertainty. Under the uncertainty of a hazardous

event occurring, hedonic prices are based on consumers’ subjective probability which they define as a

function of the objective probability, the consumer’s expenditures on self-protection (e.g., insurance) and

information level (an exogenous variable). The effect of increased information on behavior depends on the

gap between objective risk and the consumer’s initial subjective risk, e.g., above-average objective risk and

a lower initial subjective probability will lead to increasing subjective probability and hedonic price as

information increases (Kask & Maani, 1992).

New information can lead individuals to update their subjective perceptions of risk and, in turn,

risk premiums may be identified in a hedonic model. However, few studies have attempted to measure the

effects of a “pure” information shock – when there is no actual disaster event – on property prices (Atreya

& Ferreira, 2015; Brookshire et al., 1985; Gibson & Mullins, 2020; Nakanishi, 2017; Parton & Dundas,

2020). For example, Gibson and Mullins (2020) use DID to look at housing market responses to two “pure”

flood risk signals in New York – the passing of the Biggert-Waters Flood Insurance Reform Act (which

increased flood insurance premiums) and new floodplain maps produced by the Federal Emergency

Management Agency (FEMA) – as well as housing market responses to an actual disaster event – Hurricane

Sandy. The release of the new floodplain maps, which had not been updated in 30 years, was accompanied

by prominent press coverage and presented New Yorkers with three decades worth of updated information

about climate change in a single event. Hurricane Sandy and the Biggert-Waters Act, similarly, acted as

exogenous information shocks about flood risk. Gibson and Mullins (2020) find that all three flood risk

signals decreased the sales prices of impacted properties by 3% to 11% (depending on the risk signal).

Furthermore, salience of risk may capitalize into property prices only temporarily after a disaster

event. Other studies have found that the change in risk premium due to a disaster event may disappear

rapidly over the course of a couple of years if additional disaster events do not occur (Atreya et al., 2013;

Bin & Landry, 2013; Hansen et al., 2006; Kousky, 2010; McCluskey & Rausser, 2001; McCoy & Walsh,

2018). Leveraging multiple storm events in North Carolina, Bin and Landry (2013) find risk premiums

between 6.0% and 20.2% following major flooding events for properties inside the 100-year flood zone.

This risk premium decreases over time without new flood events and disappears 5-6 years after the last

recorded event. This decay of risk premium suggests that people’s risk perceptions change with the

prevalence of disaster events. Without new information, individuals’ subjective probabilities will diminish.

Hansen et al. (2006) investigate the effects of distance from a fuel pipeline on property prices in Bellingham,

WA before and after a major pipeline accident in 1999. They find a large risk discount following the

accident and that, for a given distance from the pipeline, the effect of the explosion decays over time.

8

Hansen et al. (2006) point out three reasons why the effect of an event on subjective risk perceptions may

decrease over time. First, the informational effect of the event will diminish as new people move into the

area. Second, individuals who were exposed to the event may experience decay of their active recall.

Finally, as media coverage decreases and people’s attention turns to more recent events, the attention-

focusing effect of the event will diminish over time.

Another potential explanation for the observed decay in risk premium over time is availability bias

– wherein individuals’ subjective probability of an event occurring depends on how recent or memorable

that event was (Atreya et al., 2013; Bin & Landry, 2013; Gallagher, 2014; Kousky, 2010; McCoy & Walsh,

2018). For example, Gallagher (2014) uses an event study framework to estimate the effect of large regional

floods on insurance uptake rates and finds strong evidence of an immediate increase in the fraction of

homeowners with flood insurance policies in communities hit by the flood. The insurance uptake rate

steadily declines until, after nine years, the effect of the flood is no longer statistically distinguishable in

uptake rates. Gallagher (2014) also finds that this insurance uptake spike-and-decay pattern repeats if a

community is hit by another flood, suggesting that the occurrence of new flood events is relatively important

in forming flood risk beliefs. Without new information, individuals’ subjective probabilities will diminish.

However, even when the natural hazard risk is salient, it may not translate into behavior. In their

review of prior research on natural hazard risk perception and behavior, Wachinger et al. (2013) find that

the link between risk perception and preparedness action can be weak even when individuals understand

the risk. Wachinger et al. (2013) also find that the main factors responsible for determining risk perception

are direct experience of a natural hazard, trust in scientific experts and authorities, and confidence in

protective measures. Secondary but significant factors include media coverage, a form of indirect

experience, and home ownership, which stimulates concern when the homeowner perceives a vulnerability

or has personal experience. They note that the indirect experience provided by mass media influences risk

perception but only when the respondents lack direct experience.

3 Study area and background

Oregon is a geologic mirror image of northern Japan, where the March 11, 2011 magnitude 9.0 Tohoku

earthquake caused widespread damage. The resulting tsunami surges also caused millions of dollars of

damages to parts of the Oregon coast (Jung, 2011). The majority of damage in Oregon was concentrated in

the port of Brookings where the waves destroyed docks, resulting in $7 million in damage (Tobias, 2012).

Longer-term effects of the tsunami included multiple cleanup efforts as debris from Japan slowly made its

way to Oregon shores.

Oregon is due to experience a major subduction zone earthquake of a similar magnitude to the

Tohoku event. The probability of a Cascadia Subduction Zone (CSZ) earthquake occurring in the next 50

9

years is 7-15% for a great earthquake between 8.7 and 9.2 magnitude and approximately 37% for a very

large earthquake between 8.0 and 8.6 magnitude (OSSPAC, 2013). Unlike Japan, Oregon’s resilience to a

magnitude 9.0 Cascadia earthquake is low. Coastal communities in the tsunami zone are especially

vulnerable since they will experience the strongest earthquake motions due to their proximity to the fault

and will then be subject to multiple tsunami inundations for up to 24 hours after the earthquake (OSSPAC,

2013). Residents who live within the tsunami inundation zone may be displaced instantly. It may take 3 to

6 months to restore electricity, 1 to 3 years to restore drinking water, and up to 3 years to restore healthcare

facilities on the coast (OSSPAC, 2013).

In their 2013 report, the Oregon Seismic Safety Policy Advisory Commission (OSSPAC) (2013)

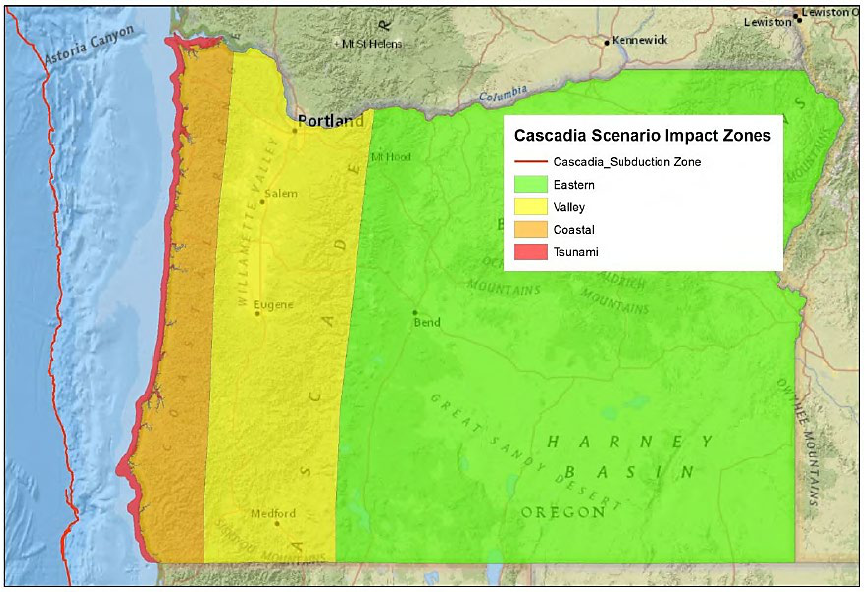

separated Oregon into four impact zones based on the expected pattern of damage for a 9.0 Cascadia

earthquake and tsunami scenario (Figure 1). They predict that damage will be the most extreme in the

tsunami (inundation) zone and heavy throughout the coastal zone. The coastal zone, which encompasses

most of the coastal county population centers, is expected to experience severe damages from shaking,

liquefaction, and landslides. Throughout the coastal zone, single-family homes and other wood frame

structures will shift off foundations if unsecured. In some areas of the coast, even well-built wooden

structures may be heavily damaged and in need of replacement. However, in the tsunami (inundation) zone,

the damage will be nearly complete. The tsunami will not only further damage buildings, roads, and utilities

but it will also “obliterate nearly all wood frame buildings” (OSSPAC, 2013, p. 49). This difference in

outcomes of residential buildings inside versus outside the tsunami inundation zone suggests that there is a

distinct difference between earthquake and tsunami risk for coastal residents. Similarly, the tsunami zone

will also experience a higher proportion of fatalities. Approximately 4% of permanent residents in the seven

coastal counties live in the tsunami inundation zone (as defined by the 1995 SB 379 regulatory tsunami

line) (Wood, 2007). However, half of the fatalities of a 9.0 magnitude Cascadia event are expected to be

due to the tsunami (OSSPAC, 2013).

Even though the entire coastline would experience similar impacts from an earthquake, coastal

homes outside of the tsunami inundation zone may survive the Cascadia earthquake but those inside of the

zone will likely not. In this paper, I differentiate risk using the tsunami inundation lines from maps produced

by the Oregon Department of Geology and Mineral Industries (DOGAMI) as the treatment boundaries.

Senate Bill 379 established the original tsunami inundation zone in Oregon in 1995. This line, also known

as “SB 379,” represents the best estimate of tsunami inundation from a typical or most likely Cascadia

earthquake in 1995 (DOGAMI, n.d.-b). The 1995 SB 379 line was the regulatory tsunami inundation line

for Oregon until 2019 and limited the construction of certain critical and essential facilities inside the

inundation line (DOGAMI, n.d.-b). House Bill 3309 overturned the regulatory power of the SB 379 line in

2019. Official tsunami evacuation brochures and signage used the SB 379 line until 2013 when DOGAMI

10

released a new series of tsunami inundation maps for a Cascadia earthquake. The 2013 tsunami inundation

map series TIM Plate 1 was derived using systematic, Oregon-coast-wide models of tsunami inundation for

five scenarios – XXL, XL, L, M, and SM – that represent the full range of severity of past and expected

tsunamis (DOGAMI, n.d.-a). The largest scenario of this series – the XXL scenario – became the one used

by DOGAMI to represent the “maximum local source” inundation level in their official tsunami evacuation

maps and signage (DOGAMI, n.d.-a). Thus, the XXL scenario has represented the tsunami evacuation line

for the public at large since 2013. The release of the evacuation maps in 2013 also confronted homeowners

who were outside of the 1995 SB 379 evacuation zone but inside the 2013 XXL evacuation zone with new

and up-to-date information about tsunami risk. Thus, this change in hazard planning also acts as a “pure”

information shock about those houses.

The July 20, 2015 New Yorker article “The Really Big One” by Kathryn Schulz (2015a) brought

national media attention to the predicted Cascadia event and to Oregon’s low level of resilience and

preparation for it. This article went viral in the summer of 2015 (Fletcher & Lovejoy, 2018; Lacitis, 2015;

Marum, 2016). It also prompted preparedness actions such as the selling out of emergency preparedness

kits (Lacitis, 2015; Lovejoy, 2018), earned its author a Pulitzer (Marum, 2016), and motivated a book

addressing risk perception, preparedness, and communication (Fletcher & Lovejoy, 2018). In a chapter of

Figure 1. Impact zones for the magnitude 9.0 Cascadia earthquake scenario. Damage will be extreme in the Tsunami zone,

heavy in the Coastal zone, moderate in the Valley zone, and light in the Eastern zone. From Figure 1.5 of the “Oregon Resilience

Plan” (OSSPAC, 2013).

11

this book, Crowe (2018) compares media coverage of the CSZ before and after Schulz’ article. She finds

that before Schulz’ article the 3 largest spikes in U.S. newspaper coverage occurred after the 2001 Nisqually

earthquake in WA, the 2004 Indian ocean earthquake and tsunami, and the 2011 Tohoku earthquake and

tsunami (Crowe, 2018). The Tohoku earthquake and tsunami had the most media coverage to date that

connects the CSZ to another natural disaster. Within 3 months of “The Really Big One”, 33 unique

newspaper articles were published that referenced both Schulz’ article and the CSZ. Journalists reported on

increased individual actions following the article, e.g., spikes in earthquake survival kit sales and home

earthquake retrofitting, and group actions including public forums, events, and roundtables on earthquake

preparedness. Essentially, “The Really Big One” both communicated the risk of the Cascadia earthquake

and tsunami and spurred the public to prepare for it (Lovejoy, 2018).

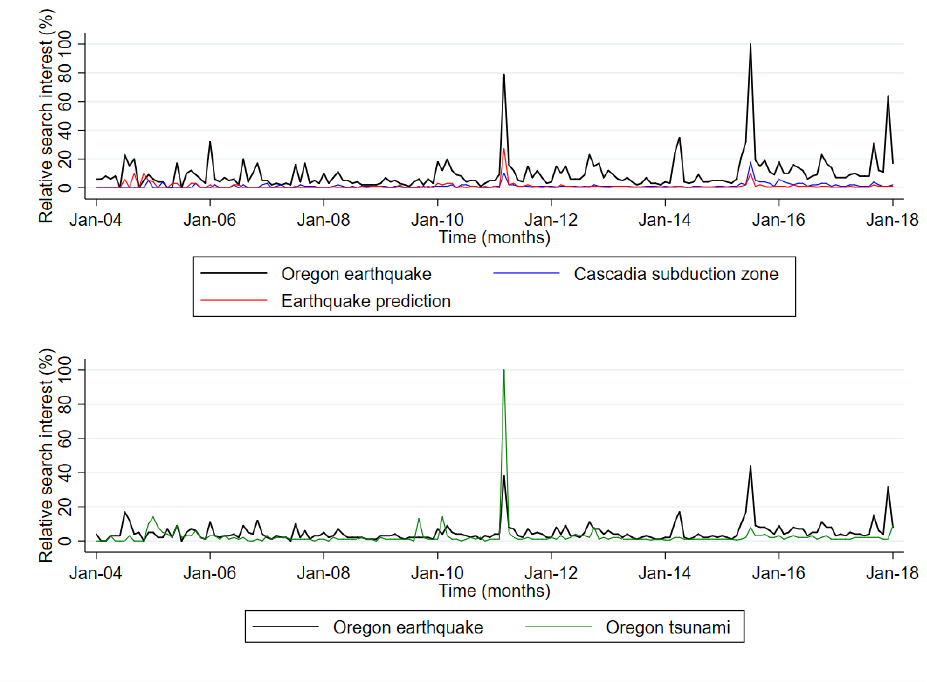

Google search intensity spikes are also in line with Crowe's (2018) findings of spikes in media

coverage following Schulz’ 2015 New Yorker article and the 2011 Tohoku earthquake and tsunami. Figure

Figure 2.

Google searches between 1/1/04 and 1/1/18 in Oregon as measured by search interest relative to the highest point

on the chart for the given region and time range. (a) For terms “Oregon earthquake”, “Cascadia subduction zone”, and

“Earthquake prediction”. (b) For terms “Oregon earthquake” and “Oregon tsunami”. The term “Oregon tsunami” is omitted

from (a) due to an order of magnitude spike in search intensity for “Oregon tsunami” during the Tohoku event relative to the

other three terms over the time range.

12

2(a) graphs the Google searches in Oregon for the terms “Oregon earthquake”, “Cascadia subduction zone”,

and “Earthquake prediction” between 2004 and 2017. Search popularity is measured as a percentage of

search interest relative to the highest point on the chart for Oregon web users (searches originating from

Oregon addresses) between 2004 and 2017 (Google Trends, n.d.). The number of searches peaked in July

2015 reflecting the viral popularity of the New Yorker article. The Tohoku earthquake and tsunami in

March 2011 represents the second highest peak in searches and was 75% as popular as the New Yorker

article. However, the search intensity for “Oregon earthquake” at its peak after the 2015 New Yorker article

is only 40% of the search intensity for “Oregon tsunami” at its peak during the 2011 Tohoku event (see

Figure 2(b)).

Combined, the increase in internet searches for information on an Oregon earthquake/tsunami and

media coverage on the CSZ immediately after these two events suggests that they acted as information

shocks to Oregon residents. The Tohoku 2011 earthquake and tsunami could have increased Oregonians’

information levels about the Cascadia event due to its similarity to the predicted Cascadia event and the

fact that its impacts were felt on the Oregon coast. The 2015 New Yorker article also likely impacted

Figure 3.

Tsunami blue line signage in (a) Newport, OR (courtesy of Mike Eastman) and (b) Seaside, OR (courtesy of Anne

McBride).

13

Oregonians’ information levels and risk perceptions about the Cascadia event through its viral status and

detailed explanation and illustration of the objective risk.

Oregon has implemented several policies designed to make the public more aware of and prepared

for the Cascadia earthquake and tsunami. The Tsunami Blue Line project launched in February 2016 and

provided communities along the Oregon coast with funds and materials to install thermoplastic blue lines

and signs marking the entrance to the tsunami evacuation zone (Office of Emergency Management, 2016).

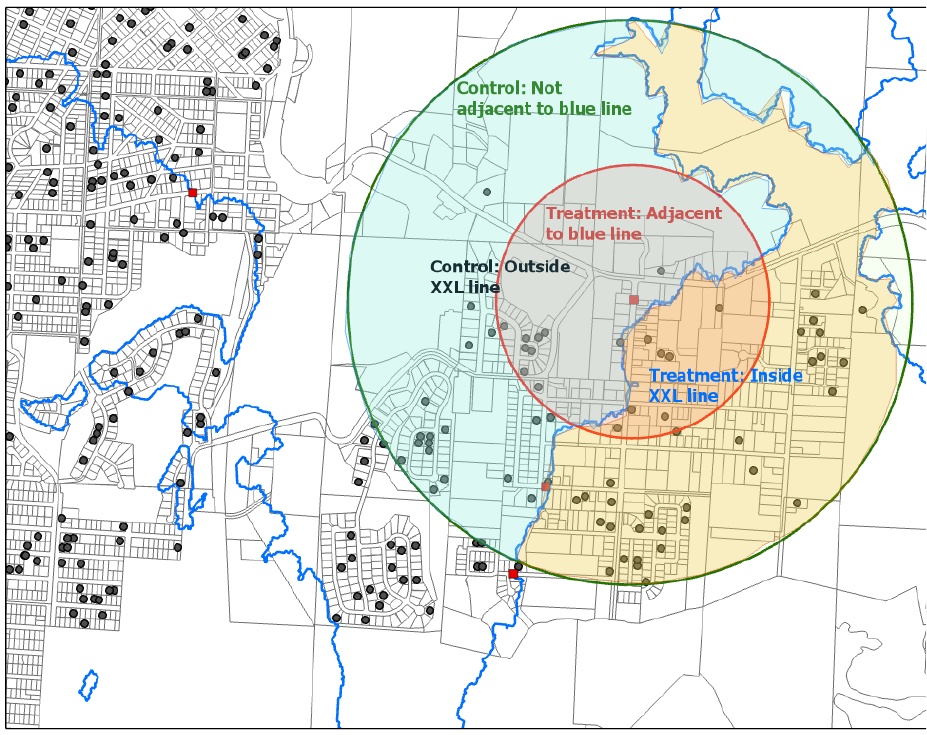

Figure 4.

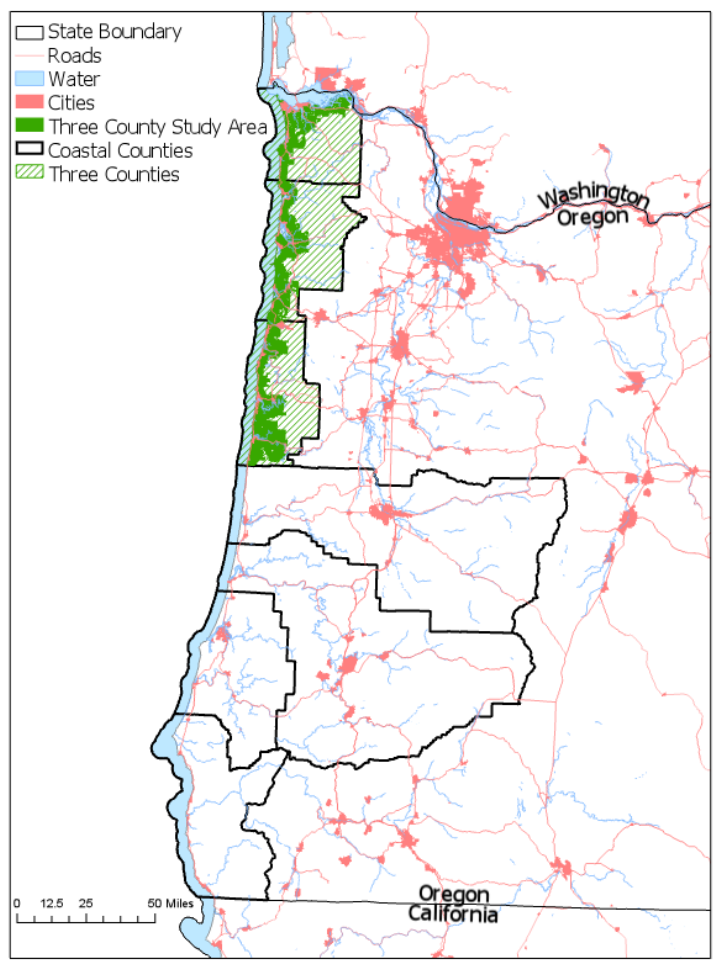

GIS data for three county study area (green hatching) and the seven coastal counties (black border). Coastal counties

from north to south (unlabeled): Clatsop, Tillamook, Lincoln, Lane, Douglas, Coos, and Curry. The study area for the first

analysis (solid green) is defined to be within 1 mile of the tsunami inundation zone given by the 1995 SB 379 line.

14

The blue lines and “Leaving Tsunami Zone” signs were installed on the 2013 XXL tsunami inundation and

evacuation line at various times since 2016 through the present day. Most blue lines are approximately 12”

wide and have “Leaving Tsunami Zone” signs next to them, as seen in Figure 3(a), though some only have

the “Leaving Tsunami Zone” sign without an accompanying blue line, as seen in Figure 3(b). Thus, the

blue lines present distinct visual markers of entry/exit into the tsunami inundation and evacuation zone. The

coastal communities that had blue lines installed were Bay City, Cannon Beach, Coos Bay, Florence, Gold

Beach, Lincoln City, Manzanita/Nehalem, Newport, Reedsport, Seaside, and Yachats as well as some

unincorporated areas of Lincoln County. Each of these communities managed the installation of their own

blue lines except for unincorporated communities whose blue lines were installed by their county’s public

works department. Most of the time the blue lines and signs were installed on roads on or near the 2013

XXL tsunami line though at times the community’s input changed the location of the blue line. In addition

to a statewide press release (Office of Emergency Management, 2016) and flyers announcing the new blue

lines, several community news agencies also reported on their local blue lines following installation

(Fontaine, 2016; Kustura, 2016; Sheeler, 2018).

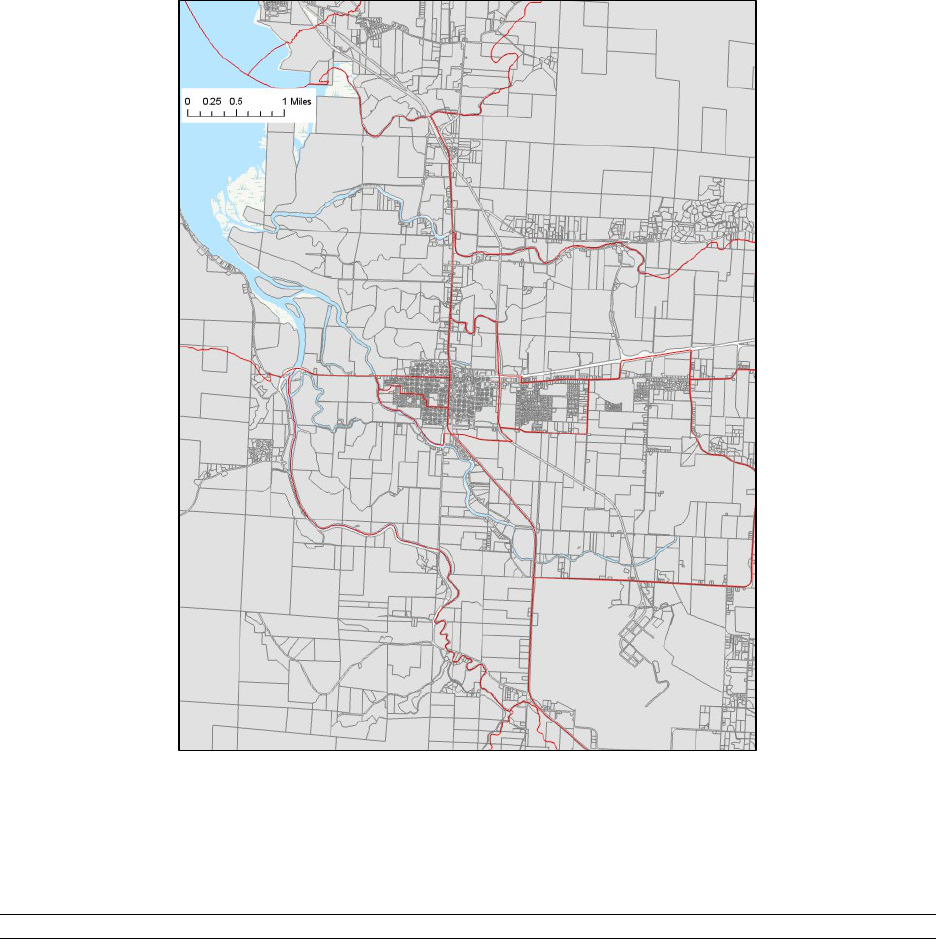

The first analysis in this paper focuses on the three northernmost counties of Clatsop, Tillamook,

and Lincoln because the North Oregon coast is expected to experience the most concentrated tsunami

exposure (OSSPAC, 2013).

3

Since the Tohoku earthquake/tsunami and New Yorker article are both “pure”

or “distant” information shocks, I chose to focus on the region of Oregon that is likely to be the most

sensitive to such shocks. The northern coast counties have the highest percentages of tsunami-prone land

that is zoned as urban (Wood, 2007). While 95% of the land in Oregon’s tsunami inundation zone is

classified as undeveloped, 48% of Clatsop County’s tsunami zone, 34% of Lincoln County’s tsunami zone,

and 21% of Tillamook County’s tsunami zone are zoned as urban (Wood, 2007). The northern coast cities

contain the highest number of public venues and dependent-population facilities like schools and hospitals

in the tsunami inundation zone. These cities also have the highest percentages of their employees in the

tsunami inundation zone (Wood, 2007). In 2018, the population of these counties was: 39,200 in Clatsop,

26,395 in Tillamook, and 48,210 in Lincoln (Secretary of State, n.d.-b). All three of these counties are rural

with the largest city – Newport, the county seat of Lincoln County – having a population of 10,125 in 2018

(Secretary of State, n.d.-a). Population and housing are concentrated primarily in the small incorporated

and unincorporated coastal towns of these counties. Clatsop County has five incorporated towns, Tillamook

County has seven, and Lincoln County has six. As of 2007, approximately 36% of residents in the tsunami

3

So as to measure only the “pure” information effect due to the Tohoku earthquake and tsunami and not the effect of damages

from the tsunami, Curry County (the southernmost county in Oregon) was intentionally excluded from the potential study area

because the port of Bookings experienced much higher damage than any other coastal community in Oregon. With this limitation,

the costs to the Oregon coast are then primarily the indirect cleanup costs of debris from Japan and not direct infrastructure damage.

According to local newspapers, the majority of damage occurred in southern Oregon and northern California (Jung, 2011; Tobias,

2012).

15

inundation zone lived in rural, unincorporated areas of the seven coastal counties, primarily in the

unincorporated towns of the three northern counties (Wood, 2007).

Oregon’s Office of Economic Analysis (OEA) groups these three counties together as a regional

economy. It is reasonable to consider these counties as a single housing market given their separation from

Oregon’s population centers in the Willamette Valley, their connection via HWY 101, and their similar

economies and industries. These three counties span approximately 150 miles in the north-south direction.

While it is unlikely that someone would commute over three hours from Yachats (the southernmost town)

to Astoria (the northernmost town) for work, it is plausible that people would commute half that distance.

Figure 4 shows a map of the three northern counties (green hatching) and the boundaries of the seven coastal

counties (black). The map also illustrates the clustering of and connections between population centers on

the coast, the lack of population along the Oregon Coast Range, and the separation from the urban centers

in the adjacent Willamette Valley counties.

The second and third analyses have more narrowly defined sample spaces that contain a limited

number of treated observations, necessitating an expansion to include housing data from all seven coastal

counties. For example, only eleven coastal communities received blue lines and, of these, some

communities (e.g., Cannon Beach) received as few as three blue lines. These blue lines were installed at

times between 2016 and 2019, which results in a short post-installation time range and therefore few

property sales after installation for the DID model in the third analysis. This extension assumes that the

entire Oregon Coast can be treated as a single housing market, as in Dundas and Lewis (2020). Under this

assumption, the three northern coast counties comprise a sub-market of this larger housing market.

4 Data

Multiple data sources including property sales data, tsunami inundation maps, Census block group data,

and other GIS data are used for these analyses. Property sales data was aggregated from tax assessor records

in Zillow’s ZTRAX database and spans residential, agricultural, and commercial sales from 1995 through

2018 (Zillow, 2020). These data were cleaned to remove all non-residential transactions and transactions

missing key structural variables (age, etc.). In each year, transactions with prices in the bottom one percent

were removed because they may reflect non-arms-length transfers, e.g., intra-family transfers. Transactions

in the top one percent in each year were also removed. Houses that sold more than five times between 2009

and 2018 were dropped because of potential unobservables driving their frequent resale. Potential multi-

family dwellings – properties with more than eight bedrooms or six bathrooms – were dropped from the

sample. Finally, transactions that took place less than one year since the previous sale were removed since

they often reflected either the same transaction recorded at multiple points through the sale process or a

house purchased to be flipped and re-sold. The Zillow ZTRAX data does not have reliable second home

16

indicators, however, so identifying second home ownership is not possible at this time.

4

Following this

cleaning, the remaining transactions contain only arms-length, single-family residential sales that reflect

the valuations of potential homeowners. Some of the key structural covariates from the Zillow data include

the effective age of the house (2018 – remodel year), indoor square footage, total acreage, number of

bedrooms, number of bathrooms, and whether the house has a garage.

Neighborhood and location amenity data are collected from several state and federal sources. The

majority of the data comes from the Emergency Preparedness Data Collection, the public version of a

dataset compiled by Oregon’s Preparedness Framework Implementation Team (Prep-FIT) for the Oregon

Incident Response Information System (OR-IRIS). This dataset is a collection of existing and purpose-built

GIS datasets combined to help understand the setting of a potential emergency response incident

(Preparedness Framework Implementation Team (Prep-FIT), n.d.). Sources of the OR-IRIS data include

state agencies such as the Oregon Department of Transportation (ODOT) and federal agencies such as

USGS. This data includes location information for airports, fire stations, hospitals, wastewater treatment

plants, beach access points, highways and roads, railroads, rivers and other waterbodies, the ocean

shoreline, and cities. Distance to the nearest central business district is measured as the distance to the center

of the nearest town (incorporated or unincorporated). Coastal towns are small and likely have only one

central business district. Distances to the nearest hospital, law enforcement station, fire station, and

wastewater treatment plant were included since proximity to one of these facilities may serve as a proxy

for a “safety” amenity.

Location information on state and federal protected areas (public lands) primarily came from the

USGS Protected Areas Database of the United States (PAD-US). Federal public lands were trimmed to

include conservation areas, national forests, national historic sites, national monuments, national parks,

national recreation areas, national wildlife refuges, wilderness areas, and recreation or resource

management areas. State public lands were trimmed to include only state forests, state parks, and wildlife

management areas. Elevation data was collected in 10m-by-10m pixels from the Oregon Department of

Geology and Mineral Industries (DOGAMI). GIS software was used to calculate the elevation of each

property and the distance from each property to the nearest location amenity.

5

For oceanfront properties,

4

Second homes and vacation rentals constitute a large share of housing in the northern counties due to the dominance of the tourism

sector on the Oregon coast. According to the 2019 Clatsop County Housing Strategies Report (Appendix A, 2019) the estimated

vacancy rate of ownership housing is very high, especially in beachside communities. They also find that in several beachside

communities short-term rentals have outpaced the addition of new units; an estimated 58% of new houses built in the county since

2010 are used as short-term rentals (Clatsop County Housing Strategies Report, Appendix A, 2019). Second homeowners who do

not live on the Oregon coast and directly face the risk of a Cascadia tsunami may have different risk perceptions and preferences

than permanent residents of the Oregon coast. Accounting for second home ownership is therefore important for accurately

estimating residents’ risk perceptions.

5

All distances are Euclidian. Euclidian distances may underestimate true distances in these rural counties. Also, Euclidian and

travel distances may capture different amenities. For example, I would expect that as travel distance to the nearest beach access

17

additional data on shoreline armoring and armoring eligibility is included. Shoreline armoring is a private

option to protect oceanfront properties from erosion and storm surges by installing hardened shoreline

protection structures.

6

Armoring eligibility and the existence of shoreline protective structures represent

safety amenities for oceanfront properties. Oceanfront parcels were identified using the Oregon Department

of Land Conservation & Development’s inventory of oceanfront parcels and their armoring eligibility.

Several studies have used changes in the number of insurance policies following a disaster event

as a measure of changing subjective perceptions about the expectation of a future disaster (Atreya et al.,

2013; Gallagher, 2014). This study omits insurance information primarily due to a lack of parcel-level

earthquake and flood insurance data.

7

Finer-scale fixed effects, however, should be able to capture some of

the unobservable heterogeneity due in part to earthquake insurance uptake differences between

neighborhoods. 2010 Census information was collected at the Census block group level to be used for these

neighborhood-level spatial fixed effects. Block groups generally contain between 600 and 3,000 people,

with an optimum size of 1,500 people. The block group is the smallest geographical unit above the block

level that is uniquely identified and therefore represents the smallest neighborhood unit data available.

Earthquake insurance, however, only covers damage from strong shaking but not water damage

from a tsunami (OSSPAC, 2018). Tsunami damage is typically covered by flood insurance (OSSPAC,

2018). FEMA’s National Flood Insurance Program (NFIP) requires the purchase of flood insurance for

mortgages in the 100-year floodplain – also known as Special Flood Hazard Areas (SFHA) – that are

managed by federally regulated lenders. Mortgage lenders must also inform homebuyers if the property is

located in an SFHA. On the Oregon coast, the SFHA floodplain line is similar but not identical to the

tsunami inundation lines (OSSPAC, 2018). For example, for the first analysis, only 3% of properties outside

the SB 379 tsunami inundation zone are inside a SFHA; however, 36% of properties inside the SB 379

inundation zone are also inside a SFHA (Table 1). These homes in both the tsunami inundation zone and

in the SFHA likely have flood insurance. Therefore, even without fine-scale flood insurance policy data, it

may be possible to use presence in a SFHA to roughly proxy for flood insurance ownership inside the

tsunami inundation zone. This SFHA indicator will underestimate the amount of flood insurance policies

point increases, property values decrease since beach access is an amenity. However, Euclidian distance to a beach access point

may primarily capture the visual disamenity of congestion at popular beach access points.

6

Oregon’s Statewide Planning Goal 18 designates which parcels are eligible to install shoreline armoring (Department of Land

Conservation & Development, n.d., p. 18). To limit shoreline armoring and resulting beach erosion and loss of beach access Goal

18 limits shoreline armoring to parcels where development existed prior to 1977.

7

Most homeowner insurance policies in Oregon do not cover earthquake damage though many homeowners insurance providers

offer standalone earthquake coverage and earthquake insurance is widely available through the state of Oregon (Division of

Financial Regulation, n.d.). As of 2017 approximately 14.8% of Oregonians with residential homeowners insurance also have

earthquake insurance (Cheng, 2018). This is comparable to other Pacific Coast states with high earthquake risks, e.g., Washington’s

uptake rate of 11.3% and California’s uptake rate of 15.1%. Earthquake insurance data is only available at the county level and the

variation in insurance uptake between the coastal counties is too low for the county-level information to be useful.

18

because, while most homes inside the SFHA have flood insurance, some homes outside the SFHA may also

have flood insurance but will not be picked up by the SFHA indicator.

For the first analysis, the sample space of transactions was limited to those properties within 1 mile

of the original tsunami inundation zone (SB 379). This removes non-coastal properties on the eastern side

of the county from the sample. Non-coastal properties likely have different amenity sets than coastal

properties so their removal from the sample better controls for omitted neighborhood and location

amenities. A distance of 1 mile from the SB 379 line captures all of the towns in the three counties and does

not extend into large rural or forest parcels on the eastern sides of the counties.

8

The temporal extent of the

first analysis is 2009 to 2017 so that each event – the 2011 earthquake and the 2015 article – is bracketed

by two years of property sales data before and after the event. The Zillow data spans the years 2009 to 2017

and contains 15,627 transactions.

9

The tsunami inundation zones that define the treatment group in the first analysis include the 1995

SB 379 line and the largest of the 2013 TIM scenarios (XXL). Table 1 compares the descriptive statistics

of houses inside and outside the 1995 SB 379 tsunami inundation zone to illustrate differences between the

treatment and control groups for the sample used in the first analysis. Approximately 27% of the

transactions between 2009 and 2017 were inside the SB 379 inundation zone. The houses inside and outside

the SB 379 zone are similar in terms of effective age, total acreage, number of bedrooms and bathrooms,

and whether they have a fireplace or external structures (e.g., garage, patio, fencing). Houses inside the

inundation zone on average sell for $16,000 more which likely reflects the shorter distances to likely

amenities such as the ocean, rivers, public lands, and schools and the greater distances to likely disamenities

such as highways. Houses outside of the inundation zone have larger indoor square footage and total acreage

which may be due to the higher density of houses inside the inundation zone. Approximately 99% of the

houses inside the SB 379 inundation zone are also in the 2013 XXL scenario inundation zone. The XXL

scenario of the 2013 TIM series was in use for official tsunami evacuation maps during the 2015 New

Yorker article. Approximately 49% of the transactions between 2009 and 2017 were in this inundation

zone.

10

The change in tsunami inundation and evacuation maps between the two events of interest presents

a model specification problem that is addressed in section 5.1. See Appendix A.2 for figure comparisons of

the 2013 TIM and 1995 SB 379 tsunami inundation scenarios for the city of Tillamook.

8

Distance to the SB 379 tsunami inundation zone was chosen instead of distance to the shoreline only because the ocean shoreline

data does not extend into the Columbia River on the northern boundary of the three-county area and the SB 379 data does extend

into the Columbia.

9

Table A1 in Appendix A.3 presents summary statistics for the sample used in the first analysis, i.e., for 2009-2017 property sales

that occur within 1 mile of the 1995 SB 379 line in the three northern counties.

10

See Table A1 in Appendix A.3.

19

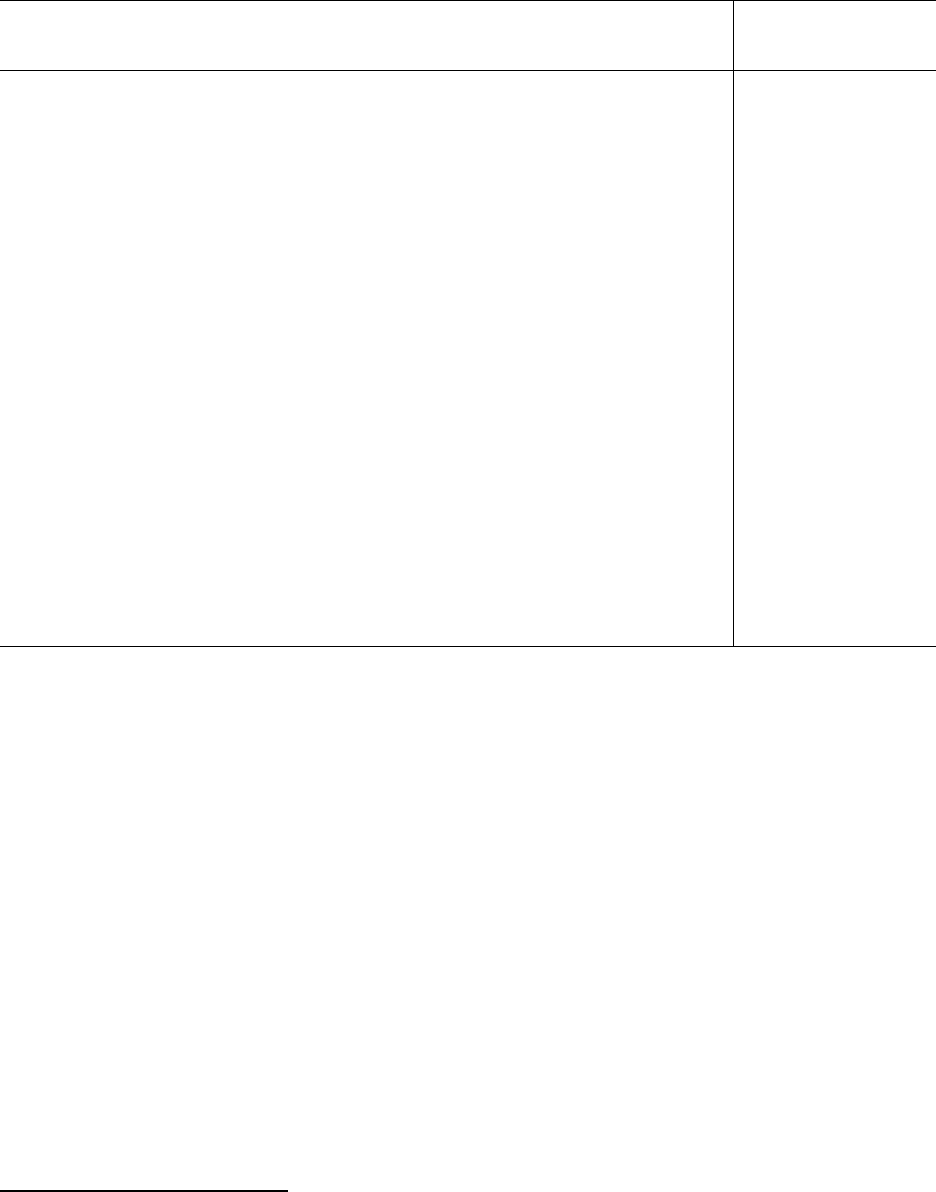

Table 1. Variable Definitions and Descriptive Statistics, by SB 379, First Analysis Sample, 2009-2017

Outside SB 379 zone

Inside SB 379 zone

Mean

Std dev

Mean

Std dev

Std diff in

means

Event

Sold after 2011 Tohoku EQ

(tohoku=1)

0.81

(0.39)

0.81

(0.39)

-

Sold after 2015 article (article=1)

0.33

(0.47)

0.32

(0.47)

-

Treatment

Inside 1995 SB 379 tsunami zone

(sb379=1)

0

(0)

1

(0)

-

Inside 2013 XXL tsunami zone

(xxl2013=1)

0.31

(0.46)

0.99

(0.09)

-

Inside 2013 XL tsunami zone

(xl2013=1)

0.28

(0.45)

0.99

(0.10)

-

Inside 2013 L tsunami zone (l2013=1)

0.12

(0.33)

0.96

(0.20)

-

Inside 2013 M tsunami zone

(m2013=1)

0.04

(0.20)

0.82

(0.38)

-

Inside 2013 SM tsunami zone

(sm2013=1)

0.01

(0.09)

0.47

(0.50)

-

Structural

Sale price (2019 constant dollars)

306,745.77

(163,480.12)

323,071.60

(186,908.93)

-0.09

Bedrooms

2.89

(0.92)

2.68

(0.93)

0.23

Bathrooms

2.06

(0.78)

1.90

(0.75)

0.22

Indoor square footage

1,744.24

(715.21)

1,505.16

(645.45)

0.35

Total acreage (equal to indoor area if

apartment)

0.42

(2.13)

0.33

(2.28)

0.04

Effective age of property (2018 -

remodel year)

35.97

(25.54)

36.43

(24.46)

-0.02

Heating (=1)

0.95

(0.22)

0.91

(0.29)

0.17

Fireplace (=1)

0.66

(0.47)

0.61

(0.49)

0.09

Garage (=1)

0.77

(0.42)

0.69

(0.46)

0.18

Carport (=1)

0.04

(0.20)

0.03

(0.18)

0.04

Deck (=1)

0.11

(0.31)

0.16

(0.36)

-0.14

Patio (=1)

0.17

(0.38)

0.20

(0.40)

-0.07

Fencing (=1)

0.14

(0.35)

0.18

(0.38)

-0.10

Goal 18 eligible (=1)

0.02

(0.13)

0.10

(0.30)

-0.35

Has shoreline armoring (=1)

0.00

(0.05)

0.04

(0.20)

-0.28

Location

Special Flood Hazard Area (SFHA)

(=1)

0.03

(0.16)

0.36

(0.48)

-0.94

Elevation (ft)

97.42

(70.54)

20.95

(11.02)

1.51

Slope (angular degrees of slope)

2.72

(4.82)

1.74

(2.38)

0.26

20

The last column of Table 1 presents the standardized difference in means for the structural and

location covariates. Several key explanatory variables such as elevation (1.51) and distance to the ocean

shoreline (0.55) have large absolute standardized differences (in parentheses). Some researchers have

suggested that an absolute standardized difference of 0.25 or more indicates that covariates are imbalanced

between groups (Stuart, 2010). This suggests that the treated and control groups are considerably

imbalanced and that covariate balancing, e.g., matching or weighting, may be useful or necessary for

identification.

For the second analysis, the sample space of transactions is limited to those properties that were

outside of the original 1995 SB 379 tsunami evacuation zone. The 2013 update of tsunami inundation and

evacuation maps represents an exogenous risk signal to houses that were outside of the original 1995 SB

379 inundation zone but with the hazard planning change found themselves inside one of the new 2013

inundation zones. As such, each of the five 2013 tsunami inundation zones is used as the treatment boundary

Distance to nearest beach access point

(ft)

4,348.03

(6,943.63)

2,075.03

(4,633.56)

0.39

Distance to ocean shoreline (ft)

16,402.69

(23,311.22)

5,926.15

(13,706.17)

0.55

Oceanfront (=1)

0.03

(0.16)

0.11

(0.32)

-0.35

Distance to nearest water body (lake,

pond, bay) (ft)

6,977.92

(7,673.00)

6,437.03

(9,694.99)

0.06

Distance to nearest river (ft)

8,155.13

(8,038.36)

4,987.01

(7,363.52)

0.41

Distance to nearest state park or public

land (ft)

25,889.50

(26,449.02)

21,853.60

(24,369.87)

0.16

Distance to nearest national park or

public land (ft)

17,547.64

(16,187.60)

20,618.42

(18,961.51)

-0.17

Distance to nearest highway or

interstate (ft)

2,735.67

(4,070.97)

4,346.39

(6,942.60)

-0.28

Distance to nearest major road (ft)

3,173.23

(5,045.23)

5,383.81

(8,321.11)

-0.32

Distance to nearest railroad (ft)

68,837.11

(60,557.73)

83,561.70

(51,105.73)

-0.26

Distance to nearest airport (ft)

32,312.90

(19,089.39)

26,215.34

(19,586.41)

0.32

Distance to nearest k-12 school (ft)

14,668.42

(15,629.87)

12,327.99

(10,823.89)

0.17

Distance to nearest central business

district (city) (ft)

11,027.20

(10,671.49)

9,171.75

(8,882.89)

0.19

Distance to nearest wastewater

treatment plant (ft)

15,651.49

(11,137.14)

11,604.52

(9,447.23)

0.39

Distance to nearest fire station (ft)

5,992.65

(4,597.47)

6,141.79

(5,116.56)

-0.03

Distance to nearest law enforcement

station (ft)

30,593.44

(35,657.69)

34,384.59

(44,793.06)

-0.09

Distance to nearest hospital (ft)

45,555.14

(42,443.18)

54,716.99

(45,225.25)

-0.21

Observations

11,467

4,160

21

for a separate sample where the sample is restricted to a narrow band of properties within 1 mile of the

treatment boundary given by the XXL, XL, L, M, or SM inundation line. Table 2 compares the samples of

the resulting five different sample spaces and lists the number of transactions inside and outside the given

inundation zone for each sample. This table illustrates the data limitations of this analysis even after

extending the sample space to all seven coastal counties, as can be seen by the small number of treated

observations (81) available for the SM inundation line treatment boundary sample. The time range for this

analysis is from 2011 to 2015 so that the 2013 evacuation map change is bracketed by two years of property

sales data before and after the event.

11

The third analysis restricts the sample space to a small neighborhood of properties around newly

installed blue lines and the 2013 XXL inundation line. The preferred model restricts treated observations

to be within 1000’ of the blue line and control observations to be within 2500’. The temporal extent of the

sample is 2014 and 2018 so that each blue line has at most two years of property sales before and after its

installation since the blue lines were installed at different times between 2016 and 2019.

12

Table A4 in

Appendix A.3 compares the descriptive statistics of houses inside and outside the blue line neighborhood

given by a 1000’ radius to illustrate differences between the treatment and control groups for the sample

used in the preferred model. This table shows that the standardized differences in means for this sample

space are small in comparison to the sample spaces of the first and second analyses. This suggests that the

11

Table A2 in Appendix A.3 presents summary statistics for the sample used in Model 1 of the second analysis, i.e., for 2011-2015

property sales that are outside the 1995 SB 379 line and are within 1 mile of the 2013 XXL line in the seven coastal counties. This

is the largest sample space in the second analysis and encompasses the other four sample spaces. Table A3 in Appendix A.3

compares the descriptive statistics of houses inside and outside the 2013 SM tsunami inundation zone to illustrate differences

between the treatment and control groups for the sample used in Model 5. This is the smallest sample space and has the largest

standardized differences in means. Descriptive statistics for the remaining samples used in this analysis are not presented here but

are available upon request.

12

For blue lines installed in 2018 less than one year of property sales is available post-installation. For blue lines installed in 2019,

there are no post-installation property sales. This is due to a lack of updates to ZTRAX housing transactions after 2018 for most

Oregon counties (as of June 2021).

Table 2. Second Analysis Samples, 2011-2015

Sample

Model

Total

observations

Outside inundation

zone

Inside inundation

zone

Within 1 mile of the XXL

inundation zone

1

8,010

5,855

2,155

Within 1 mile of the XL inundation

zone

2

7,790

5,829

1,961

Within 1 mile of the L inundation

zone

3

6,593

5,698

895

Within 1 mile of the M inundation

zone

4

5,842

5,527

315

Within 1 mile of the SM inundation

zone

5

5,429

5,348

81

22

narrow sample space definition successfully restricts neighborhoods to be more homogenous and thus may

help deal with time-invariant and time-varying unobservables that may be correlated with either proximity

to the blue lines or the 2013 XXL line.

A database of blue line locations and installation dates does not exist at the state or county levels.

Thus, information about when and where the blue lines were installed was gathered by contacting individual

city and county emergency managers, public works departments, and planning departments along the

Oregon coast. Emails and phone conversations were used to compile a list of approximate blue line

locations and installation times. Some locations were given as being in the vicinity of street intersections

or nearby landmarks so I approximate the location of the blue line based on the location of the 2013 XXL

tsunami inundation line and this firsthand information. Timing information was provided as the month and

year of installation. However, sometimes no timing information other than the year of installation was

available. This ambiguity of installation dates further reduces the post-installation time range for the DID

and DDD models. Timing and location information is currently incomplete for several towns that are known

to have blue lines installed, usually due to multiple blue line installation periods or uncertainty about

whether some blue lines were installed. Due to the potential non-randomness of this missing data, these

towns were not included in the dataset analyzed in this paper.

5 Methodology

5.1 First analysis: 2011 Tohoku earthquake and tsunami and 2015 New Yorker article

In the first analysis, I use two exogenous information shocks to distinguish between the effect of coastal

amenities and the increased subjective risk of tsunami inundation. I use a difference-in-differences (DID)

model to difference out time-invariant omitted variables and contemporaneous effects such as

macroeconomic shocks. There is a complication with defining the treatment group (inside the tsunami

inundation zone) and control group (outside of the inundation zone) because the DOGAMI tsunami

inundation maps changed in 2013 from the SB 379 line to the new TIM Plate 1 series. This motivates three

model specifications. For the first specification (Model I), I consider only the Tohoku earthquake event and

the 1995 SB 379 tsunami line as the boundary between the treatment and control groups. The time range

for this specification is from 2009 to 2013 (before the DOGAMI tsunami inundation maps change). The

model specification is:

(

)

=

+

379

+

+

379

+

+

+

,

(

1

)

where

is the sale price (in constant 2019 dollars) of house with structural and location

characteristics in Census block group at time . The log transformation of

was chosen as the

23

dependent variable in all models because taking the log of narrows its range and can make estimates

less sensitive to extreme values. The treatment variable 379

indicates whether the house is in the tsunami

inundation zone given by the 1995 SB 379 scenario. The event variable

indicates that the sale

happened after 3/11/2011 (the post-Tohoku period).

13

The parameter of interest is

, the marginal effect

of the Tohoku 2011 earthquake and tsunami on property values inside the tsunami inundation zone given

by the 1995 SB 379 scenario. The structural characteristics in

include quadratic terms for the non-binary

variables to better account for their expected diminishing effect on property prices (e.g., Atreya et al., 2013;

Bin & Landry, 2013). I also follow previous hedonic studies and take log transformations of the distance

variables (originally in feet) in

to abstract from unit issues (Atreya et al., 2013; Bin & Landry, 2013).

The temporal fixed effects

were included to capture any seasonal (90-day) heterogeneity or

shocks that affect all property sales. The Census block group spatial fixed effects

are interacted

with the annual fixed effects

in

to capture how these neighborhoods are changing

over time. These spatial-temporal fixed effects soak up annual changes at the neighborhood level such as

storm surges and allow neighborhoods to flexibly differ in their recoveries from the subprime mortgage

crisis and Great Recession.

14

Model II considers the New Yorker event and the largest scenario (XXL) of the new 2013 tsunami

zones as the boundary between treatment and control groups. The time range for this specification is 2013

– 2017. While the SB 379 is most comparable to the M and L scenarios by area, the XXL scenario was

chosen as the treatment for Model II because it is the most extreme scenario. I expect that households

willing to pay a risk premium to avoid tsunami inundation will likely choose to locate outside the entire

region of potential tsunami inundation. The XXL scenario is also the scenario used by DOGAMI to create

their tsunami evacuation maps, making it the most salient scenario for the public at large. The model

specification for Model II is:

(

)

=

+

2013

+

+

2013

+

+

+

(

2

)

The treatment variable 2013

indicates whether the house is in the tsunami inundation zone given by

the 2013 XXL scenario. The event variable

indicates the sale happened after 7/20/2015 (the post-

13

The

event variable is defined as between 3/11/2011 and 7/20/2015 (the post-Tohoku period and pre-New Yorker article

period). Since the time range for Model I is from 2009 to 2013, the

variable equals 1 for all sales during this time that

occur after the Tohoku earthquake and tsunami on 3/11/2011. The

variable definition is discussed further in the Model

III specification section.

14

The appropriate scale at which Great Recession recovery is capitalized may be at shorter time scales, i.e., at the

scale. This fixed effect is tested as a robustness check.

24

New Yorker article period). The parameter of interest is

, the marginal effect of the 2015 New Yorker

article on property values inside the tsunami inundation zone given by the 2013 XXL scenario.

Model III incorporates the New Yorker article event into Model I and keeps the 1995 SB 379

tsunami line as the treatment boundary. Since the 2013 tsunami inundation maps are only two years old and

the 1995 map had been in circulation for 20 years by the New Yorker article’s publication, there could be

a lag in the public’s knowledge and acceptance of the new tsunami boundaries. This specification assumes

an information lag and that homebuyers place more importance on the long-standing SB 379 line when

choosing where to locate. The time range for this specification is 2009 to 2017. The DID model

specification for Model III is:

(

)

=

+

379

+

+

+

379

+

379

+

+

+

(

3

)

The implicit assumption in the definition of the

variable here is that the impact of the 2011 Tohoku

earthquake/tsunami on property values decreases over time and disappears by the New Yorker article in

2015. This assumption follows previous findings that risk premiums decay over time and may disappear if

additional disaster events do not occur (Atreya et al., 2013; Bin & Landry, 2013; Hansen et al., 2006;

Kousky, 2010; McCluskey & Rausser, 2001; McCoy & Walsh, 2018). The parameters of interest are

and

, the marginal effects of the 2011 earthquake/tsunami and 2015 article on property values inside the

tsunami inundation zone given by the 1995 SB 379 scenario.

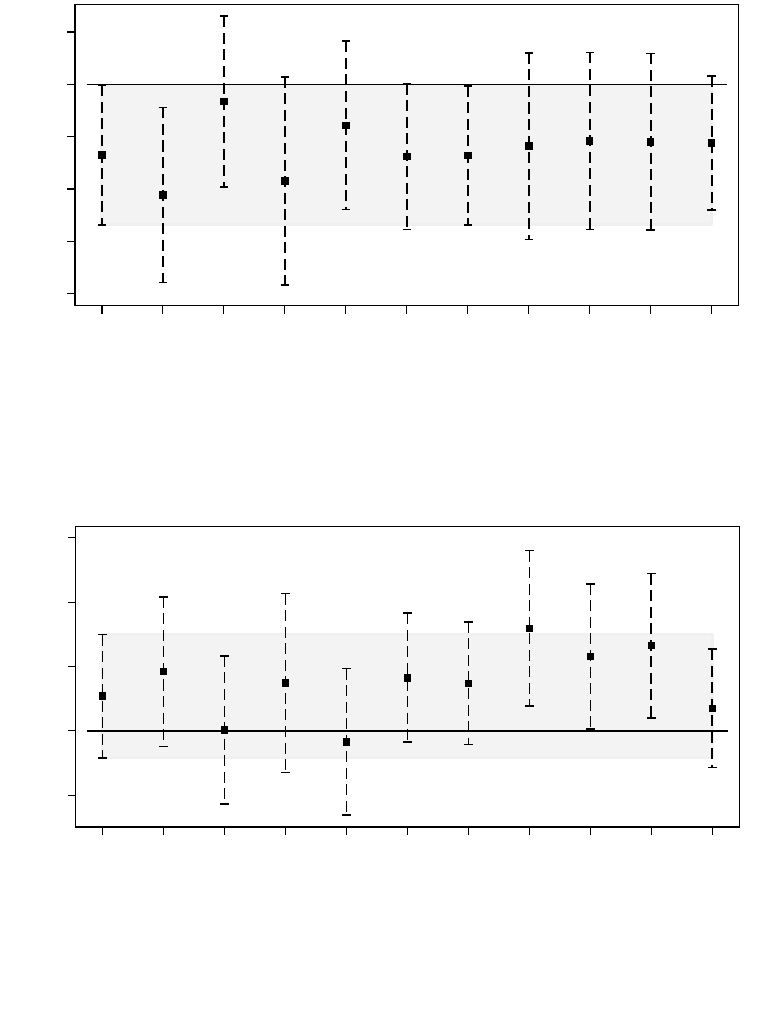

Consistent estimation of these treatment effects requires the parallel trends assumption. The parallel

trends assumption requires that absent the two information shocks, the difference in unobserved property

price drivers between properties inside the tsunami inundation zone and outside the tsunami inundation

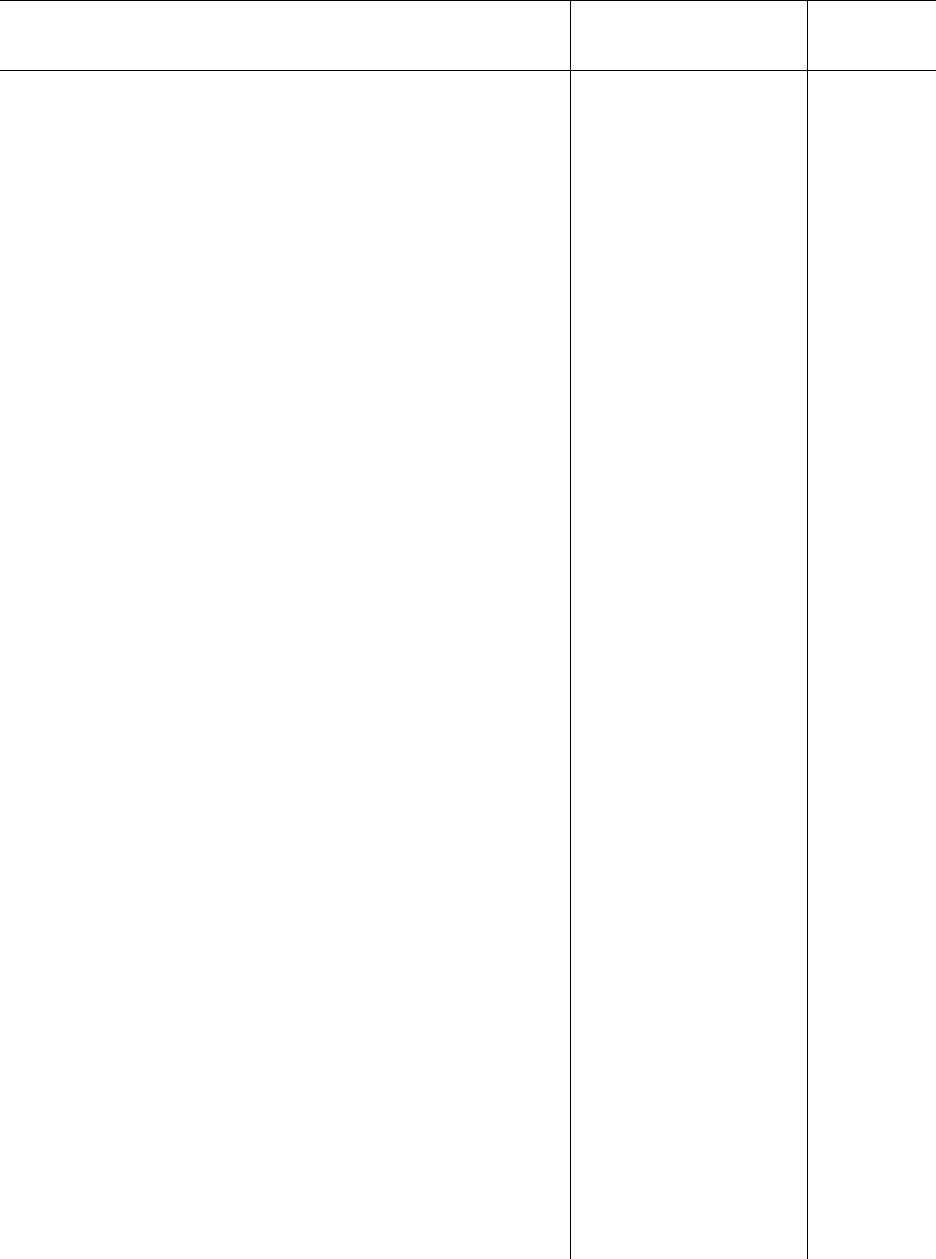

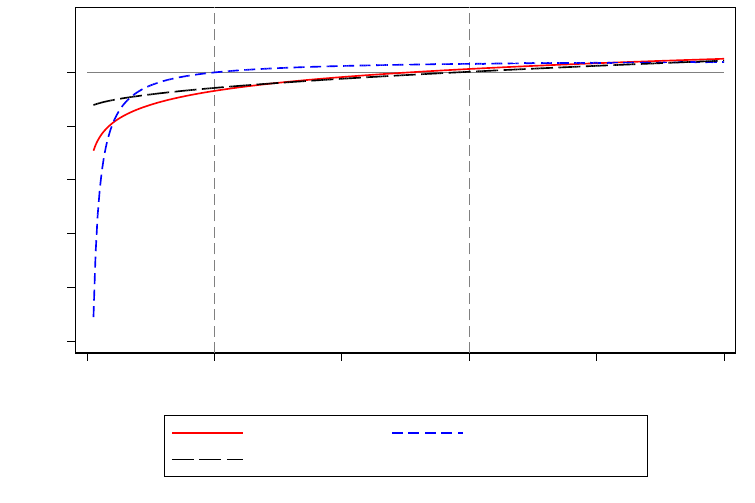

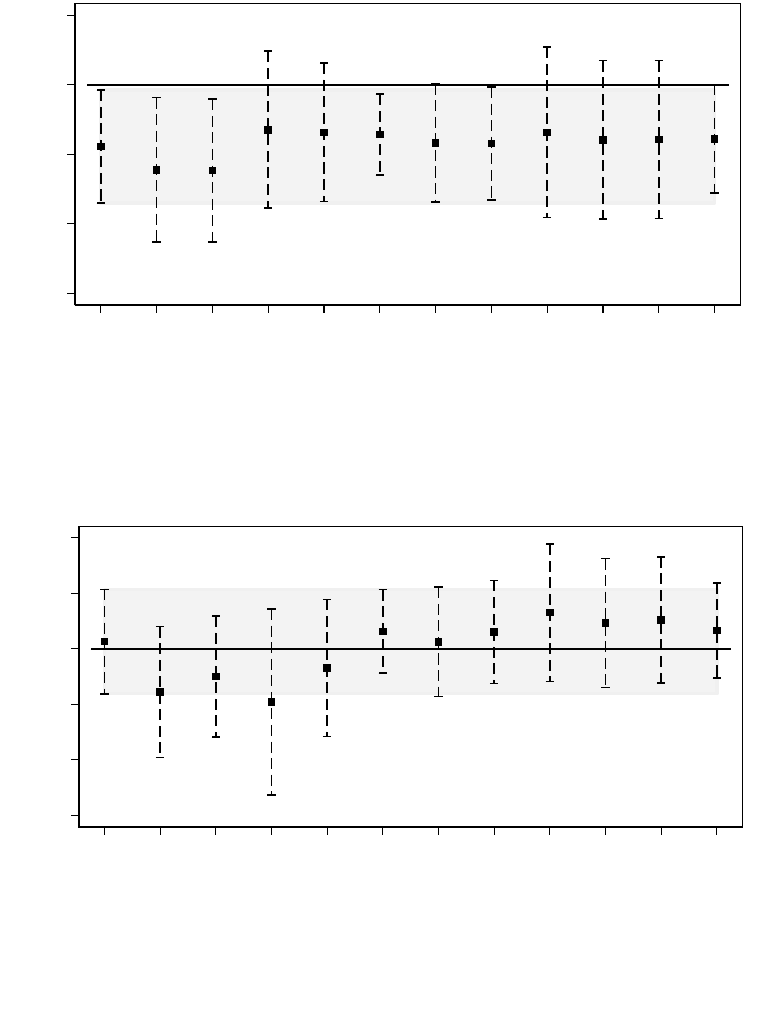

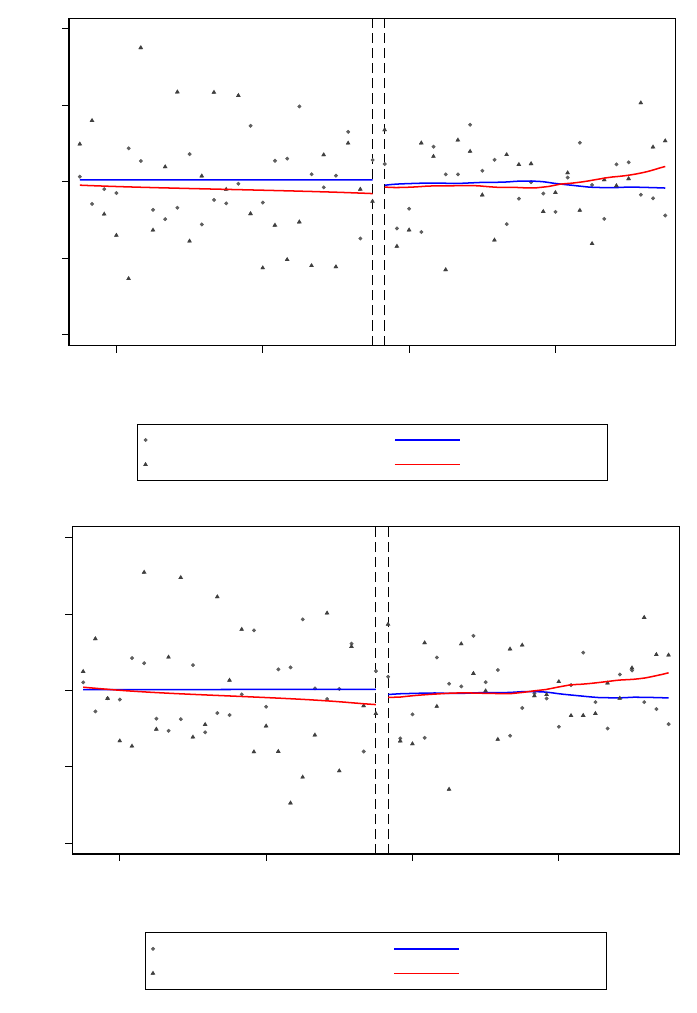

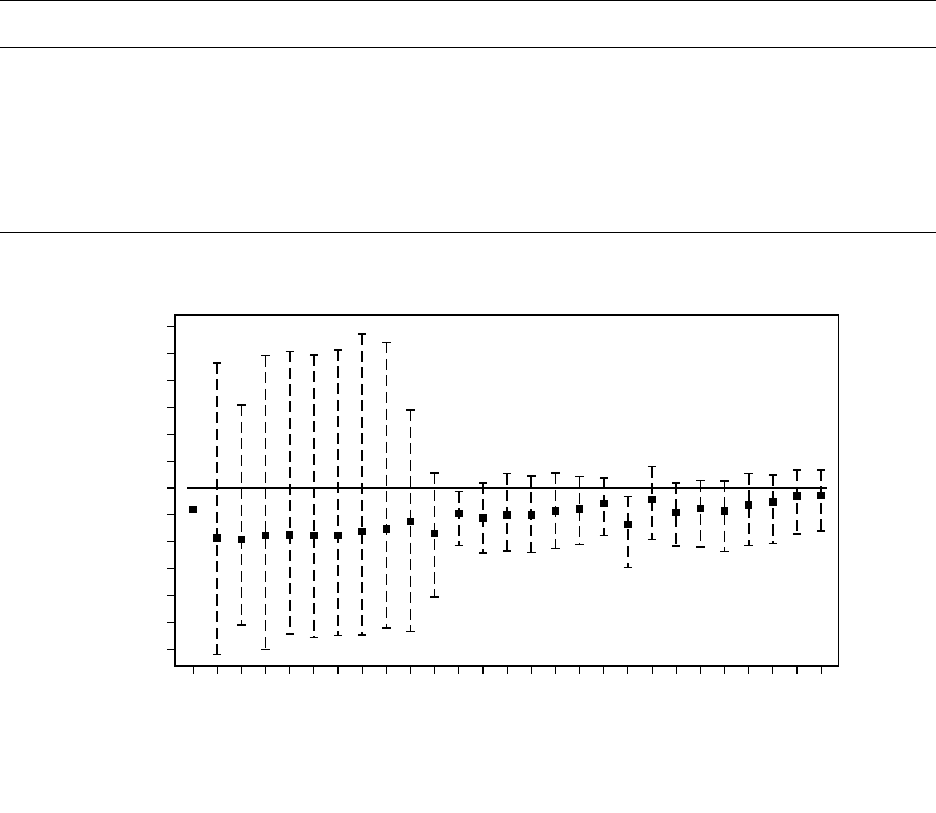

zone would have remained constant. I assess the validity of this assumption in Figure 5, which plots residual

housing prices inside and outside of the treatment inundation line – SB 379 or 2013 XXL, depending on

the model – for the three northern counties. To account for observable differences across houses, I first

regress log sale prices on structural attributes, location covariates, and fixed effects for quarter and Census

block group by year. I then aggregate the residuals to the group (treated or control) and month level and

plot these residuals over time using local polynomial regressions. Figure 5(a) plots the housing price trends

inside and outside of the 1995 SB 379 tsunami inundation zone for Model I’s time range – March 2011 to

March 2013. Adjusted prices of the treated group before the 2011 Tohoku earthquake and tsunami exhibit

a similar trend as those of the control group. Following the 2011 Tohoku event, residual prices for the

treated group initially drop but then recover to nearly pre-treatment levels by 2013. Figure 5(b) plots the

housing price trends inside and outside of the 2013 XXL tsunami inundation zone for Model II’s time range

– July 2013 to July 2017. Before the 2015 New Yorker article, the treated group exhibits a similar trend as

25

the control group. However, residual prices for the treated group appear to increase following the 2015

article event, a counterintuitive result.

Following the estimation of the DID regressions, I test whether the resulting risk discounts decay

over time. However, the literature on how to measure these decay effects is not standardized and a variety

(a)

(b)

Figure 5.

Housing price trends inside and outside of the treatment inundation line – SB 379 or 2013 XXL – for the three

counties. Plot of residual (log) sale prices net of structural attributes, location covariates, and fixed effects aggregated by month

with local polynomial trend lines. (a) For Model I’s time range. (b) For Model II’s time range.

2011 Tohoku EQ

-.2 -.1

0 .1 .2

Residual log sale prices

2010

2011

2012

2013

Year

Control (outside SB 379) Control trend

Treatment (inside SB 379) Treatment trend

2015 Article

-.2 -.1 0 .1

Residual log sale prices

2014

2015

2016

2017

Year

Control (outside 2013 XXL) Control trend

Treatment (inside 2013 XXL) Treatment trend

26

of methods exist that attempt to measure the decay effect. I use a method similar to the one used by Bin and

Landry (2013). This method uses only data after the event and regresses log sale prices on the treatment

variable, a count of months between the event and the month of sale

(

)

, and the interaction

between the two. For example, the specification for the SB 379 tsunami inundation zone is:

(

)

=

+

379

+

+

379

(

)

+

+

+

(

4

)

Different specifications are used for

(

)

transformation including linear, log, square root, and

ratio specifications, i.e.,

, ln

(

)

,

,

. The parameter of

interest is

, the coefficient on the interaction between the

(

)

transformation and the

treatment variable. A positive and statistically significant coefficient suggests that the risk premium is

decaying over time (Bin & Landry, 2013).

An important identification concern is the covariate imbalance found for several key explanatory

variables. Estimating average treatment effects using ordinary linear regression methods becomes more

challenging when there is considerable imbalance in covariates between the treatment and control groups.