2022 ANNUAL REPORT

Citi is proud of its

colleagues in Ukraine,

who are supporting

the country through

a devastating war.

A mission of enabling growth

and economic progress

What you can expect from us and what we expect from ourselves

Citi’s mission is to serve as a trusted partner to our clients by responsibly providing

financial services that enable growth and economic progress. Our core activities

are safeguarding assets, lending money, making payments and accessing the

capital markets on behalf of our clients. We have more than 200 years of experience

helping our clients meet the world’s toughest challenges and embrace its greatest

opportunities. We are Citi, the global bank — an institution connecting millions of

people across hundreds of countries and cities.

We protect people’s savings and help them make the purchases — from everyday

transactions to buying a home — that improve the quality of their lives. We advise

people on how to invest for future needs, such as their children’s education and

their own retirement, and help them buy securities such as stocks and bonds.

We work with companies to optimize their daily operations, whether they need

working capital, to make payroll or export their goods overseas. By lending to

companies large and small, we help them grow, creating jobs and real economic

value at home and in communities around the world. We provide financing and

support to governments at all levels, so they can build sustainable infrastructure,

such as housing, transportation, schools and other vital public works.

These capabilities create an obligation to act responsibly, do everything possible to

create the best outcomes and prudently manage risk. If we fall short, we will take

decisive action and learn from our experience.

We strive to earn and maintain the public’s trust by constantly adhering to the

highest ethical standards. We ask our colleagues to ensure that their decisions pass

three tests: they are in our clients’ interests, create economic value and are always

systemically responsible. When we do these things well, we make a positive financial

and social impact in the communities we serve and show what a global bank can do.

Citi’s Value Proposition

More than 20 years ago, I started at Citi as a market risk analyst in New York City. Since then, I have

benefited from the career opportunities that come with being at a global bank and have worked across

the world. In 2018, I took on the role of leading Citi’s franchise in Ukraine and have had the pleasure of

making my home with my family in the beautiful city of Kyiv.

At Citi, we like to think of ourselves as a “human bank,” and nowhere has that been more apparent than

in Ukraine. When Russia invaded our country last year, the entire firm moved swiftly to support our

colleagues and clients. Thanks to the courage and dedication of our Citi Ukraine team, our business

here has operated continuously throughout the war. That’s allowed us to support clients on the ground

who are overseeing essential services and the non-governmental organizations that are delivering aid.

On the cover of this report, you will find some images illustrating these heroic efforts.

I am also incredibly grateful to my Citi colleagues in Poland, Romania, Hungary and other neighboring

countries who have received displaced Ukrainians and mobilized volunteer efforts. On top of that,

so many members of the firm from around the world have found other ways to support us in Ukraine.

Simply put, I could not be prouder to work at Citi.

May 2023 bring peace to Ukraine.

Alex McWhorter

Citi Country Officer, Citi Ukraine

Hear more from Alex and

Citi Ukraine colleagues

on the impact of the war.

Europe, Middle East and Africa CEO David Livingstone (center left) and Alex McWhorter (center right) meet with Citi Ukraine

colleagues during a visit to Poland.

1

Jane Fraser

Chief Executive Officer

Dear shareholders,

Looking back at 2022, I don’t think any of us could have predicted the

twists and turns the year would take. Lingering disruptions to supply

chains, historic inflationary pressures, persistent lockdowns in China

and the largest war on European soil since World War II combined to

create a tumultuous environment for businesses and financial markets.

As a leading global bank with a more-than-210-year history, these

dynamics are not unfamiliar to us. And as we showed throughout the

pandemic, Citi is an important source of strength and stability during

times of immense change and challenge. This is an opportunity and a

responsibility we take very seriously.

So, for me, 2022 will be remembered most for two things:

The first is how we continued to support our clients. We helped them

navigate macro and geopolitical dynamics. We advised them in their digital

transformations and supported the shifts in their business models. We

guided them in their transitions toward a clean-energy economy. When war

broke out in Ukraine, we sprang to the aid of our employees and clients on

the ground, and helped our multinational clients unwind their operations in

Russia in response to Western sanctions aimed at the country.

The second is the important strides we are making to position Citi to win

in the decade ahead. In March 2022, at our first Investor Day in several

years, we set a vision and refreshed our strategy to change our business

mix and simplify our operating model. We have

absolute clarity on our future, and we are focused

on accelerating growth, gaining share and

increasing returns for shareholders over time.

By most measures, we ended the year in a stronger

position than we started.

A foundation for the future

Our vision for Citi is to be the preeminent banking

partner for institutions with cross-border needs,

a global leader in wealth management and a

valued personal bank in our home market.

To that end, we have laid the foundation

by focusing on five core interconnected

businesses: Services, Markets, Banking,

Global Wealth Management and U.S.

Personal Banking. We intentionally designed

our business mix to withstand different

macroeconomic conditions, and we have seen

that borne out over the past year. So whilst the

environment has changed, our strategy has

not, and we remain steadfast in executing and

delivering for our shareholders.

For the year, we delivered $14.8 billion in net income on

revenues of $75.3 billion. Our Return on Tangible Common

Equity (RoTCE

1

) was 8.9%, and we remain on track to achieve

an RoTCE of 11–12% in the medium term.

We increased our Common Equity Tier 1 Capital ratio by nearly

80 basis points to 13%, which includes a buffer of 100 basis

points above the regulatory requirement to help absorb the

impact of various macro and other factors. Finally, our tangible

book value per share

1

increased to $81.65, and we returned

more than $7 billion to our shareholders through common

dividends and share repurchases.

How our core businesses fared

Our Services business had an exceptional year with revenues

up 27% versus 2021. Treasury and Trade Solutions (TTS),

the crown jewel of our global network, experienced a 32%

increase in revenues as we continued to grow our wallet

share with existing clients whilst also adding new client

relationships. With the introduction of a seven-day sweeps

service, the industry’s first 24/7 USD clearing capabilities

and instant payments in 33 markets, we’re moving closer

to an always-on, near real-time cash management solution

for corporate clients. In Securities Services, we grew yearly

revenues by 15% and onboarded $1.2 trillion in assets under

custody and administration.

Our Markets business closed 2022 with revenues up 7%

from 2021, ending the year with one of the best fourth

quarters in recent memory. Our traders navigated the

volatility quite well, with notable performance amongst

corporate clients and strong gains in FX and rates. And

together with our Corporate Bank, our Markets team

continued to optimize its balance sheet.

Revenues in Banking fell 35% as we contended with a materially

slower deal environment. But Banking remains a key part of

our strategy, and we continued to play a leading role in the

year’s notable transactions. This included acting as one of the

lead advisors on Volkswagen’s €9.4 billion IPO of Porsche, the

largest public listing of the year, and serving as financial advisor

to Amgen on its proposed $27.8 billion acquisition of Horizon

Therapeutics. We hired exceptional bankers in healthcare, clean

energy and technology — all sectors critical to our growth —

and welcomed new talent into our Commercial Bank as it has

expanded into Canada, Germany and Switzerland.

In U.S. Personal Banking, revenues for the year rose 7% as we

bolstered our leadership in payments and lending. Branded

Cards grew revenues by 9%, whilst Retail Services revenues

were up 7%. We launched new credit cards with ExxonMobil

and AT&T and celebrated 35 years of our co-branded credit

“ We have absolute clarity

on our future, and we are

focused on accelerating

growth, gaining share

and increasing returns for

shareholders over time.”

Letter to shareholders

32

Celebrated

35 years

of the American

Airlines co-branded

credit card, a leading

airline rewards

credit card

Hired exceptional

talent in Banking,

Capital Markets

and Advisory

to strengthen coverage

of growth sectors such as

healthcare, clean energy

and technology

Expanded the

Private Bank

to France and Germany,

opened the first Citi

Global Wealth Center

in Hong Kong and

established a Citi Global

Wealth at Work presence

in Luxembourg

Grew Citi

Commercial Bank

by expanding into

Canada, Germany and

Switzerland and

hiring talent

to execute on our

client-centric

coverage model

Served as one of

the lead advisors

on Porsche’s IPO and

as financial advisor

on Amgen’s proposed

acquisition of Horizon

Therapeutics

Onboarded

$1.2 trillion of

new assets under

custody and

administration

in Securities

Services

Enhanced risk

and controls

by improving stress

test capabilities and

our approval process

for new products

Debuted

a refreshed

strategy

for improving

returns at Citi’s

Investor Day

Built out digital

capabilities

in our market-leading

Treasury and Trade Solutions

business and launched

a 24/7 payments

clearing service

Simplified our

operating model

by closing the sale of five

consumer businesses

and announced plans

to end nearly all

operations in Russia

Strengthened

connections between

businesses

resulting in more

than 60,000 client

referrals from the U.S.

Personal Bank to

Citi Global Wealth

Implemented

new performance

management

framework

to drive excellence

and accountability

across the firm

A year of progress

54

1

RoTCE and tangible book value per share are non-GAAP financial measures. For more information, see page 40 of Citi’s 2022 Form 10-K.

2

Citi’s binding CET1 Capital ratio was derived under the Basel III Standardized Approach as of December 31, 2022.

3

Closed the sale of India and Vietnam consumer businesses in March 2023.

card partnership with American Airlines. Revenues in Retail

Banking were roughly flat for the full year, but we continued to

enhance our digital capabilities, growing digital users by 6%

for the year. And as part of our efforts to break down barriers to

banking, last year we became the first of the largest U.S. banks

to completely eliminate overdraft fees and returned item fees

for our customers.

We also made progress building out our Global Wealth

Management business despite the economic headwinds

that slowed activity amongst our Asia-based clients in

particular and reduced overall revenues by 2%. Having unified

our Wealth businesses under a single platform, we’ve been

acquiring new clients and investing in hiring advisors to make

sure we’re well-positioned for success as the markets recover.

In addition, we forged ahead with our global expansion,

opening Private Bank offices in Paris and Frankfurt, a new

Wealth center in Hong Kong and a Citi Global Wealth at Work

presence in Luxembourg.

Greater connectivity and focus

A centerpiece of our go-forward plan is increasing the linkages

between our businesses so we can more easily engage clients

in one part of our firm with products and services from another.

By delivering the full power of Citi to clients, we can deepen

existing relationships and win new mandates.

Our Markets and Banking businesses are now aligned more

closely than ever, and, as a result, we are supporting our

clients in a more integrated way. Our Wealth business is also

benefiting from closer connections and received more than

60,000 referrals from the Retail Bank last year. In addition,

we have established a new partnership agreement between

Wealth and our Commercial Bank, where 90% of our clients

are privately owned companies.

At the same time, we are making progress in simplifying our

firm, making us easier to manage and allowing us to focus on

the parts of our business where we know we can grow and

improve our competitiveness.

We announced our intention to exit 14 consumer businesses

in Asia, Europe, the Middle East and Mexico — businesses

that do not have clear synergies with our global network.

As a result of swift but disciplined execution, in 2022 we

successfully closed the sale of our consumer businesses in

Australia, Bahrain, Malaysia, the Philippines and Thailand.

In March 2023, we closed the sale of our consumer

businesses in India and Vietnam and are on track to close

two additional markets by the end of the year. We also

are progressing with the wind-down of our consumer

business in Korea. In addition to exiting our consumer and

local commercial banking businesses in Russia, we are

actively ending nearly all institutional banking services in

the country, and by the second quarter of 2023, our only

operations will be those necessary to fulfill any legal and

regulatory obligations. Apart from Russia, Citi will continue

to serve our clients and invest in these markets through our

institutional franchise and our Wealth business.

Citi’s Transformation

For our strategy to unlock the greatest possible value,

we know we need to modernize our infrastructure so that

we are scaled and agile and able to continue to deliver

for our clients. The consent orders issued in 2020 by the

Federal Reserve Board and Office of the Comptroller of

the Currency underscored how we had underinvested not

only in parts of our infrastructure but also in our risk and

controls environment and our data governance.

Last year, we made progress in accelerating our work to address

these gaps and simplify and modernize our operating model for

the digital age. This work is so consequential in nature that we

call it our “Transformation.” It remains my number one priority.

Whilst this is a multi-year journey, we are already seeing the

fruits of our labors. We have dramatically streamlined our

approval process for new products. And new stress testing

capabilities enable us to make faster, better-informed risk

decisions. This made a huge difference in how we have been

able to minimize the impact of Russia’s invasion of Ukraine

on all parts of our business.

Investments in our people and communities

Ensuring we have a culture characterized by excellence and

accountability underpins the success of our Transformation

and broader vision for the firm. Last year, we launched a

program, Citi’s New Way, to help our colleagues adopt the

everyday habits we need in order to operate with excellence.

We have also hardwired accountability into our firm by

strengthening our performance management process and

implementing a greater emphasis on financial returns rather

than on revenues.

The diversity of the nearly 240,000 people who work at Citi

is a distinguishing aspect of our firm, as is the diversity of our

Board, which is majority female. We remain committed to a

workplace that mirrors the communities we serve. In 2022,

we set new goals to increase the number of women and other

underrepresented groups working at Citi. These new goals

follow our success in exceeding the three-year goals we set in

2018 to increase the percentage of women in the firm globally

and of Black talent in the U.S.

In another sign of our progress, last year we celebrated the

promotion of one of the largest and most diverse Managing

Director classes in recent years. Maintaining a workplace

that is diverse, equitable and inclusive is not only true to our

values but key to our competitiveness.

Our commitment to advancing diversity, equity and inclusion

goes well beyond Citi’s walls as we continue to use our

resources as a global bank to take on some of society’s

toughest challenges. We expanded the Citi Impact Fund

to $500 million in support of diverse founders who are

driving both financial and social returns. And we delivered

on our commitment to transparency and accountability by

announcing the findings from an external review and audit of

our $1 billion Action for Racial Equity initiative to help close

the racial wealth gap.

We have also been a leader in reimagining the future of

work. Drawing on lessons learned during the pandemic, we

have institutionalized a hybrid work model for much of our

firm. This approach provides the flexibility that our people

want whilst also ensuring we benefit from the in-person

collaboration, real-time coaching and apprenticeship that

occurs only when we are physically together.

Everywhere you look around the firm, there is an undeniable

sense of momentum. We have never been clearer about the

bank we want to be, and we have made significant progress

over the past year in bringing this vision to life. Through our

relentless commitment to excellence, we are changing the

trajectory of Citi to close the gap with our competitors and

deliver a new era of success for all our stakeholders.

Sincerely,

Jane Fraser

Chief Executive Officer, Citigroup Inc.

Full year 2022 results and key metrics

Key financial metrics Businesses snapshot

REVENUES

$75.3B

NET INCOME

$14.8B

TOTAL SERVICES

REVENUES

27%

TOTAL MARKETS

REVENUES

7%

EPS

$7.00

ROCE

7.7%

TOTAL BANKING

REVENUES

35%

U.S. PERSONAL

BANKING REVENUES

7%

RoTCE

8.9%

1

SLR

5.8%

CET1 CAPITAL

RATIO

13.0%

2

GLOBAL WEALTH

MANAGEMENT

REVENUES

2%

LEGACY FRANCHISES

REVENUES

3%

Key highlights

TTS revenues

32% YoY

with further

wallet share gains

Fixed Income revenues

13% YoY

signaling our strengthened

leadership position

Returned

~$7.3B

in capital to shareholders in

the form of common dividends

and share repurchases

Securities Services

15% YoY

with

$1.2T

of new client assets under custody

and administration onboarded

Cards revenues

8% YoY

with double-digit growth in

revenues and interest-earning

balances in the second half

Closed the sale of

5

non-strategic consumer

exit markets

3

76

Became

the first

major U.S.

bank to

eliminate

overdraft

fees.

Expanded the

Citi Impact Fund

to $500 million

more than tripling our initial

commitment to invest in

private companies helping to

address societal challenges.

Became the first

major U.S. bank to set

a recruiting goal

for LGBTQ+

candidates

from colleges and

universities around

the globe.

Financed nearly

$6 billion in

affordable

housing

projects in

the U.S.

Provided more than

2.5 million households,

including nearly

1 million women,

access to essential

goods and services in

emerging markets.

Committed

$50 million through

the Citi Foundation

to nonprofits supporting

community finance

initiatives throughout

the U.S.

Volunteered

over 115,000 hours

across 84 countries

and territories as

part of Citi’s Global

Community Day.

Set 2030

emissions

reductions

targets

Signed onto the

Sustainable

Steel

Principles,

Created a first-of-its-kind

diverse financial

institutions group

to deepen our work with

minority-owned firms.

Became a founding

member of the Biden

administration’s

Economic

Opportunity

Coalition

focused on addressing

economic disparities in

underserved communities.

Advised the

Egyptian government,

in its role as COP27

president, on climate

finance in Egypt and other

developing countries.

Prioritized the safety of

Citi colleagues in Ukraine

while supporting clients and relief

organizations on the ground.

for energy and power lending

portfolios as part of Citi’s

net zero commitment.

the first framework for

lenders to measure steel

industry emissions.

Mobilized over $3 billion

in

emerging market

social finance

activity, including access to

finance, healthcare, digital

connectivity, smallholder

agriculture, reliable energy,

water and sanitation.

Confronting society’s toughest challenges

98

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

☒

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

For the fiscal year ended December 31, 2022

OR

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT

OF 1934

For the transition period from to

Commission file number 1-9924

Citigroup Inc.

(Exact name of registrant as specified in its charter)

Delaware 52-1568099

(State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.)

388 Greenwich Street, New York NY 10013

(Address of principal executive offices) (Zip code)

(212) 559-1000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934 formatted in Inline XBRL: See Exhibit 99.01

Securities registered pursuant to Section 12(g) of the Act: none

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during

the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of

Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an

emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company”

in Rule 12b-2 of the Exchange Act.

Large accelerated filer

☒

Accelerated filer

☐

Non-accelerated filer

☐

Smaller reporting company

☐

Emerging growth company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or

revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. Yes o

Indicate by check mark whether the Registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control

over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued

its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing

reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received

by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No x

The aggregate market value of Citigroup Inc. common stock held by non-affiliates of Citigroup Inc. on June 30, 2022 was approximately $88.9 billion.

Number of shares of Citigroup Inc. common stock outstanding on January 31, 2023: 1,943,712,436

Documents Incorporated by Reference: Portions of the registrant’s proxy statement for the annual meeting of stockholders scheduled to be held on April 25,

2023 are incorporated by reference in this Form 10-K in response to Items 10, 11, 12, 13 and 14 of Part III.

Available on the web at www.citigroup.com

FORM 10-K CROSS-REFERENCE INDEX

Item Number Page

Part I

1. Business 1–23, 122–128,

131, 163–164,

315–316

1A. Risk Factors 41–54

1B. Unresolved Staff Comments Not Applicable

2. Properties Not Applicable

3.

Legal Proceedings—See

Note 29 to the Consolidated

Financial Statements 298–304

4. Mine Safety Disclosures Not Applicable

Part II

5.

Market for Registrant’s

Common Equity, Related

Stockholder Matters and

Issuer Purchases of Equity

Securities

142–143, 170–172,

317–318

6. [Reserved]

7.

Management’s Discussion

and Analysis of Financial

Condition and Results of

Operations 3–23, 60–121

7A.

Quantitative and Qualitative

Disclosures About Market

Risk

60–121, 165–169,

189–232, 238–289

8.

Financial Statements and

Supplementary Data 138–314

9.

Changes in and

Disagreements with

Accountants on Accounting

and Financial Disclosure Not Applicable

9A. Controls and Procedures 129–130

9B. Other Information Not Applicable

9C. Disclosure Regarding

Foreign Jurisdictions that

Prevent Inspections

Not Applicable

Part III

10.

Directors, Executive Officers

and Corporate Governance 319–321*

11. Executive Compensation **

12.

Security Ownership of

Certain Beneficial Owners

and Management and

Related Stockholder Matters ***

13.

Certain Relationships and

Related Transactions, and

Director Independence ****

14.

Principal Accountant Fees

and Services *****

Part IV

15.

Exhibit and Financial

Statement Schedules

* For additional information regarding Citigroup’s Directors, see

“Corporate Governance” and “Proposal 1: Election of Directors” in

the definitive Proxy Statement for Citigroup’s Annual Meeting of

Stockholders scheduled to be held on April 25, 2023, to be filed

with the SEC (the Proxy Statement), incorporated herein by

reference.

** See “Compensation Discussion and Analysis,” “The Personnel and

Compensation Committee Report,” and “2022 Summary

Compensation Table and Compensation Information” and “CEO

Pay Ratio” in the Proxy Statement, incorporated herein by

reference, other than disclosure under the heading “Pay versus

Performance” information responsive to Item 402(v) of Regulation

S-K of SEC rules.

*** See “About the Annual Meeting,” “Stock Ownership,” and “Equity

Compensation Plan Information” in the Proxy Statement,

incorporated herein by reference.

**** See “Corporate Governance—Director Independence,” “—Certain

Transactions and Relationships, Compensation Committee

Interlocks and Insider Participation” and “—Indebtedness” in the

Proxy Statement, incorporated herein by reference.

***** See “Proposal 2: Ratification of Selection of Independent

Registered Public Accountants” in the Proxy Statement,

incorporated herein by reference.

CITIGROUP’S 2022 ANNUAL REPORT ON FORM 10-K

OVERVIEW 1

Citigroup Operating Segments 2

MANAGEMENT’S DISCUSSION AND

ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS 3

Executive Summary 3

Citi’s Consent Order Compliance 6

Summary of Selected Financial Data 8

Segment Revenues and Income (Loss) 10

Segment Balance Sheet 11

Institutional Clients Group 12

Personal Banking and Wealth Management 18

Legacy Franchises 20

Corporate/Other 23

CAPITAL RESOURCES 24

RISK FACTORS 41

SUSTAINABILITY AND OTHER ESG MATTERS 54

HUMAN CAPITAL RESOURCES AND

MANAGEMENT 57

Managing Global Risk Table of Contents 59

MANAGING GLOBAL RISK 60

SIGNIFICANT ACCOUNTING POLICIES AND

SIGNIFICANT ESTIMATES 122

DISCLOSURE CONTROLS AND

PROCEDURES 129

MANAGEMENT’S ANNUAL REPORT ON

INTERNAL CONTROL OVER FINANCIAL

REPORTING 130

FORWARD-LOOKING STATEMENTS 131

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM (PCAOB ID # 185) 132

FINANCIAL STATEMENTS AND NOTES

TABLE OF CONTENTS 137

CONSOLIDATED FINANCIAL STATEMENTS 138

NOTES TO CONSOLIDATED FINANCIAL

STATEMENTS 146

FINANCIAL DATA SUPPLEMENT 314

SUPERVISION, REGULATION AND OTHER 315

CORPORATE INFORMATION 319

Executive Officers 319

Citigroup Board of Directors 320

GLOSSARY OF TERMS AND ACRONYMS 322

OVERVIEW

Citigroup’s history dates back to the founding of the City

Bank of New York in 1812.

Citigroup is a global diversified financial services holding

company whose businesses provide consumers, corporations,

governments and institutions with a broad, yet focused, range

of financial products and services, including consumer

banking and credit, corporate and investment banking,

securities brokerage, trade and securities services and wealth

management. Citi has approximately 200 million customer

accounts and does business in nearly 160 countries and

jurisdictions.

At December 31, 2022, Citi had approximately 240,000

full-time employees, compared to approximately 223,400 full-

time employees at December 31, 2021. For additional

information, see “Human Capital Resources and

Management” below.

Throughout this report, “Citigroup,” “Citi” and “the

Company” refer to Citigroup Inc. and its consolidated

subsidiaries. For a list of certain terms and acronyms used

herein, see “Glossary of Terms and Acronyms” at the end of

this report. All “Note” references correspond to the Notes to

the Consolidated Financial Statements.

Additional Information

Additional information about Citigroup is available on Citi’s

website at www.citigroup.com. Citigroup’s recent annual

reports on Form 10-K, quarterly reports on Form 10-Q, current

reports on Form 8-K and proxy statements, as well as other

filings with the U.S. Securities and Exchange Commission

(SEC) are available free of charge through Citi’s website by

clicking on the “Investors” tab and selecting “SEC Filings.”

The SEC’s website also contains these filings and other

information regarding Citi at www.sec.gov.

For a discussion of 2021 versus 2020 results of operations

of Institutional Clients Group (ICG), Personal Banking and

Wealth Management (PBWM), Legacy Franchises and

Corporate/Other, see each respective business’s results of

operations in Citigroup’s Annual Report on Form 10-K for the

year ended December 31, 2021 and its Current Report on

Form 8-K dated May 10, 2022 (as amended by a Current

Report on Form 8-K/A dated May 10, 2022) (collectively

referred to as Citigroup’s 2021 Annual Report on Form 10-K).

Certain reclassifications have been made to the prior

periods’ financial statements and disclosures to conform to the

current period’s presentation.

Please see “Risk Factors” below for a discussion of

material risks and uncertainties that could impact Citi’s

businesses, results of operations and financial condition.

Non-GAAP Financial Measures

Citi prepares its financial statements in accordance with U.S.

GAAP and also presents certain non-GAAP financial

measures (non-GAAP measures) that exclude certain items or

otherwise include components that differ from the most

directly comparable measures calculated in accordance with

U.S. GAAP. Non-GAAP measures are provided as additional

useful information to assess Citi’s financial condition and

results of operations (including period-to-period operating

performance). These non-GAAP measures are not intended as

a substitute for GAAP financial measures and may not be

defined or calculated the same way as non-GAAP measures

with similar names used by other companies. For more

information, including the reconciliation of these non-GAAP

financial measures to their corresponding GAAP financial

measures, see the respective sections where the measures are

presented and described and the “Glossary of Terms and

Acronyms” below.

1

Citigroup is managed pursuant to three operating segments: Institutional Clients Group, Personal Banking and Wealth Management

and Legacy Franchises. Activities not assigned to the operating segments are included in Corporate/Other.

Citigroup Operating Segments

Institutional

Clients Group

(ICG)

Personal Banking

and Wealth

Management

(PBWM)

Legacy

Franchises

• Services

– Treasury and trade solutions

(TTS)

– Securities services

• Markets

– Equity markets

– Fixed income markets

• Banking

– Investment banking

– Corporate lending

• U.S. Personal Banking

– Cards

◦ Branded cards

◦ Retail services

– Retail banking

• Global Wealth Management

(Global Wealth)

– Private bank

– Wealth at Work

– Citigold

• Asia Consumer Banking

(Asia Consumer)

– Retail banking and cards for the

remaining 8 exit markets (China,

India, Indonesia, Korea, Poland,

Russia, Taiwan and Vietnam)

• Mexico Consumer Banking

(Mexico Consumer) and Mexico

Small Business and Middle-

Market Banking (Mexico

SBMM)

– Retail banking and cards

• Legacy Holdings Assets

– Certain North America consumer

mortgage loans

– Other legacy assets

Corporate/Other

• Corporate Treasury managed portfolios

• Operations and technology

• Global staff functions and other corporate expenses

• Discontinued operations

The following are the four regions in which Citigroup operates. The regional results are fully reflected in the operating segments and

Corporate/Other above.

Citigroup Regions

(1)

North

America

Europe,

Middle East

and Africa

(EMEA)

Latin

America

Asia

(1) North America includes the U.S., Canada and Puerto Rico, Latin America includes Mexico and Asia includes Japan.

2

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION

AND RESULTS OF OPERATIONS

EXECUTIVE SUMMARY

As described further throughout this Executive Summary, Citi

demonstrated continued progress across the franchise during

2022:

• Citi’s revenues increased 5% versus the prior year,

including net gains on sales of Citi’s Philippines and

Thailand consumer banking businesses versus a loss on

sale of Citi’s Australia consumer banking business in the

prior year. Excluding these divestiture-related impacts

(see “2022 Results Summary” below), revenues increased

3%, driven by higher net interest income, partially offset

by lower non-interest revenues.

• Citi’s expenses increased 6% versus the prior year,

including divestiture-related impacts in both the current

and prior years. Excluding these divestiture-related

impacts (see “2022 Results Summary” below), expenses

increased 8%, driven by continued investments in Citi’s

transformation, business-led investments and volume-

related expenses, as well as other risk and control

investments and inflation, all partially offset by

productivity savings, the impact of foreign exchange

translation and the expense reduction from the closure of

five exit markets (see also “Expenses” below).

• Citi’s cost of credit was $5.2 billion, versus $(3.8) billion

in the prior year, largely reflecting a net build of $1.2

billion in the allowance for credit losses (ACL) for loans

and unfunded commitments, primarily due to consumer

loan growth and a deterioration in macroeconomic

assumptions, compared to a net ACL release of $8.8

billion in the prior year.

• Citi returned $7.3 billion to common shareholders in the

form of dividends and share repurchases.

• Citi’s Common Equity Tier 1 (CET1) Capital ratio

increased to 13.0% as of December 31, 2022, compared to

12.2% as of December 31, 2021 (for additional

information, see “Capital Resources” below). Citi’s

required regulatory CET1 Capital ratio was 12.0% as of

January 1, 2023, under the Basel III Standardized

Approach.

• Citi made substantial progress on its consumer banking

business divestitures in 2022, closing sales in five exit

markets and working toward closing four additional sale

transactions, as well as progressing with the ongoing

wind-downs of the Korea consumer banking business and

Russia consumer, local commercial and institutional

businesses.

2022 Results Summary

Citigroup

Citigroup reported net income of $14.8 billion, or $7.00 per

share, compared to net income of $22.0 billion, or $10.14 per

share in the prior year. The decrease in net income was

primarily driven by the higher cost of credit, resulting from

loan growth in Personal Banking and Wealth Management

(PBWM) and a deterioration in macroeconomic assumptions,

and the higher operating expenses, partially offset by the

higher revenues. Citigroup’s effective tax rate was 19.4% in

the current year versus 19.8% in the prior year. Earnings per

share (EPS) decreased 31%, reflecting the decrease in net

income, partially offset by a 4% decline in average diluted

shares outstanding.

As discussed above, results for 2022 included divestiture-

related impacts of approximately $(184) million in after-tax

earnings, substantially all of which were recorded in Legacy

Franchises (for additional information, see discussion below).

Collectively, divestiture-related impacts had a $0.09 negative

impact on EPS. This compares to divestiture-related negative

impacts on EPS of $0.80 in 2021. (As used throughout this

Form 10-K, Citi’s results of operations and financial condition

excluding the divestiture-related impacts are non-GAAP

financial measures. Citi believes the presentation of its results

of operations and financial condition excluding the divestiture-

related impacts described above provides a meaningful

depiction of the underlying fundamentals of its broader results

and Legacy Franchises’ results for investors, industry analysts

and others.)

Results for 2022 included pretax divestiture-related

impacts of approximately $82 million (approximately $(184)

million after-tax), substantially all of which were recorded in

Legacy Franchises, primarily consisting of the following:

• Approximately $618 million Philippines gain on sale

recorded in revenues

• Approximately $209 million Thailand gain on sale

recorded in revenues

• Approximately $(64) million incremental Australia

consumer business loss on sale recorded in revenues

• Approximately $535 million goodwill impairment

recorded in expenses due to re-segmentation and timing

of divestitures

• Approximately $161 million of aggregate divestiture-

related costs

Results for 2021 included pretax divestiture-related

impacts of $(1.9) billion (approximately $(1.6) billion after-

tax) in Legacy Franchises, which primarily consisted of the

following:

• Approximately $(694) million Australia loss on sale

recorded in revenues

• Approximately $1.1 billion related to charges incurred

from the voluntary early retirement program (VERP) in

connection with the wind-down of the Korea consumer

banking business recorded in expenses

• Contract modification costs related to the Asia

divestitures of $119 million

Citigroup revenues of $75.3 billion increased 5% versus

the prior year. Excluding the divestiture-related impacts,

revenues were up 3%, as the impact of higher interest rates

across businesses and strong loan growth in PBWM were

partially offset by declines in Banking in Institutional Clients

3

Group (ICG) and Asia investment product revenue in Global

Wealth Management (Global Wealth), as well as the reduction

in revenues from the closure of five exit markets and ongoing

wind-downs.

Citigroup’s end-of-period loans were $657 billion, down

2% versus the prior year, largely driven by Legacy Franchises

and the impact of foreign exchange translation. The decline in

Legacy Franchises primarily reflected the reclassification of

loans to Other assets to reflect held-for-sale (HFS) accounting,

as a result of the signing of sale agreements for consumer

banking businesses in Asia Consumer Banking (Asia

Consumer), as well as the impact of the ongoing Korea and

Russia wind-downs.

Citigroup’s end-of-period deposits were $1.4 trillion, up

4% versus the prior year, largely driven by Treasury and trade

solutions in ICG, partially offset by the impact of foreign

exchange translation.

Expenses

Citigroup’s operating expenses of $51.3 billion increased 6%

in 2022. Reported expenses included divestiture-related

impacts of approximately $696 million in the current year and

approximately $1.2 billion in the prior year, substantially all of

which were recorded in Legacy Franchises. Excluding these

divestiture-related impacts, expenses increased 8% versus the

prior year, largely driven by the following:

• Approximately 2% by transformation investments, with

about two-thirds related to the risk, controls, data and

finance programs (approximately 25% of the program

investments were related to technology).

• Approximately 1% by business-led investments, as Citi

continues to hire commercial and investment bankers, as

well as client advisors in Global Wealth, and continues to

invest in client experience, front-office platforms and

onboarding.

• Approximately 1% by higher volume-related expenses

across both PBWM and ICG.

• Approximately 3% by other risk and control investments

and inflation, partially offset by a Revlon-related wire

transfer recovery, productivity savings, the impact of

foreign exchange translation and the expense reduction

from the exit markets.

Citi expects to incur higher expenses in 2023, primarily

driven by transformation-related investments, volume-related

expenses and inflation-related impacts.

Cost of Credit

Citi’s total provisions for credit losses and for benefits and

claims was a cost of $5.2 billion, compared to a benefit of $3.8

billion in the prior year. Results in 2022 included net credit

losses of $3.8 billion versus $4.9 billion in the prior year. The

higher cost of credit was driven by the net build of $1.2 billion

in the ACL for loans and unfunded commitments, compared to

a net ACL release of $8.8 billion in the prior year, partially

offset by the lower net credit losses. The net ACL build was

primarily due to cards loan growth in PBWM and a

deterioration in macroeconomic assumptions. For additional

information on Citi’s ACL, see “Significant Accounting

Policies and Significant Estimates—Citi’s Allowance for

Credit Losses (ACL)” below.

Net credit losses of $3.8 billion decreased 23% from the

prior year, largely driven by lower consumer net credit losses.

Consumer net credit losses decreased 20% to $3.6 billion,

reflecting low loss rates in the first half of 2022, followed by

the ongoing normalization of losses toward pre-pandemic

levels, particularly in Retail services cards business in PBWM.

Corporate net credit losses decreased 54% to $178 million,

largely driven by improvements in portfolio credit quality.

Citi expects to incur higher net credit losses in 2023,

primarily driven by continued normalization toward pre-

pandemic levels, particularly in the cards business in PBWM.

For additional information on Citi’s consumer and

corporate credit costs, see each respective business’s results of

operations and “Credit Risk” below.

Capital

Citigroup’s CET1 Capital ratio was 13.0% as of December

31, 2022, compared to 12.2% as of December 31, 2021, based

on the Basel III Standardized Approach for determining risk-

weighted assets (RWA). The increase was primarily driven by

net income, impacts from the closing of the Australia,

Philippines and other Asia consumer banking business sales

and business actions to reduce RWA, partially offset by the

return of capital to common shareholders and interest rate

impacts on Citigroup’s investment portfolio. The increase in

Citi’s CET1 Capital ratio was also partially offset by the

impact of adopting the Standardized Approach for

Counterparty Credit Risk (SA-CCR) on January 1, 2022.

Citigroup’s Supplementary Leverage ratio as of

December 31, 2022 was 5.8%, compared to 5.7% as of

December 31, 2021. The increase was driven by a decrease in

Total Leverage Exposure, partly offset by lower Tier 1

Capital. For additional information on Citi’s capital ratios and

related components, see “Capital Resources” below.

Citi has continued to pause common share repurchases in

order to absorb any temporary capital impacts related to any

potential signing of a sale agreement for its Mexico Consumer

and Small Business and Middle-Market Banking (Mexico

Consumer/SBMM) business (for additional information, see

“Macroeconomic and Other Risks and Uncertainties” and the

capital return risk factor in “Risk Factors” below) and to

continue to have ample capital to serve its clients.

Institutional Clients Group

ICG net income of $10.7 billion decreased 25%, driven by a

net ACL release in the prior year, versus a net ACL build in

the current year, and higher expenses, partially offset by

higher revenues. ICG operating expenses of $26.3 billion

increased 10%, primarily driven by continued investment in

Citi’s transformation, business-led investments and volume-

related expenses, partially offset by a Revlon-related wire

transfer recovery, the impact of foreign exchange translation

and productivity savings.

ICG revenues of $41.2 billion increased 3% (including

losses on loan hedges), as revenue growth in Services and

Markets was partially offset by lower revenues in Banking.

Results included a gain on loan hedges of $307 million,

4

compared with a loss on loan hedges of $140 million in the

prior year.

Services revenues of $16.0 billion increased 27%.

Treasury and trade solutions (TTS) revenues of $12.2 billion

increased 32%, driven by 46% growth in net interest income

and 10% growth in non-interest revenue. The strong

performance in TTS was driven by the benefit of higher

interest rates, as well as business actions, including balance

sheet optimization and managing deposit pricing, deepening of

relationships with existing clients and an increase in new

clients across segments. Securities services revenues of $3.9

billion increased 15%, as net interest income increased 59%,

driven by higher interest rates across currencies, as well as the

impact of foreign exchange translation, partially offset by a

1% decrease in non-interest revenue due to the impact of

lower global financial markets.

Markets revenues of $19.1 billion increased 7% versus the

prior year, largely driven by Fixed income markets, partially

offset by lower client activity levels in Equity markets, as well

as business actions to reduce RWA. Fixed income markets

revenues of $14.6 billion increased 13%, driven by strength in

rates and currencies. Equity markets revenues of $4.6 billion

were down 9%, largely reflecting reduced client activity in

equity derivatives versus the prior year.

Banking revenues of $6.1 billion decreased 35%,

including the gain on loan hedges in the current year and loss

on loan hedges in the prior year. Excluding the gain and loss

on loan hedges, Banking revenues of $5.8 billion decreased

39%, driven by lower revenues in Investment banking and

Corporate lending. Investment banking revenues of $3.1

billion decreased 53%, as heightened macroeconomic

uncertainty and volatility continued to impact client activity.

Excluding the gain and loss on loan hedges, Corporate lending

revenues decreased 8% versus the prior year, driven by the

impact of foreign currency translation, higher cost of funds

and higher hedging costs.

For additional information on the results of operations of

ICG in 2022, see “Institutional Clients Group” below.

Personal Banking and Wealth Management

PBWM net income of $3.3 billion decreased 57% versus the

prior year, largely driven by a net ACL release in the prior

year versus a net ACL build in the current year, as well as

higher expenses. PBWM operating expenses of $16.3 billion

increased 11%, primarily driven by continued investments in

Citi’s transformation, other risk and control initiatives,

volume-related expenses and business-led investments,

partially offset by productivity savings.

PBWM revenues of $24.2 billion increased 4% versus the

prior year, as net interest income growth, driven by strong loan

growth across Branded cards and Retail services and higher

interest rates, was partially offset by a decline in non-interest

revenue, driven by lower investment product revenue in

Global Wealth and higher partner payments in Retail services.

U.S. Personal Banking revenues of $16.8 billion increased

7% versus the prior year. Branded cards revenues of $8.9

billion increased 9%, driven by higher net interest income. In

Branded cards, new account acquisitions increased 11%, card

spend volumes increased 16% and average loans increased

11%. Retail services revenues of $5.5 billion increased 7%,

driven by higher net interest income, partially offset by higher

partner payments. Retail banking revenues of $2.5 billion were

largely unchanged versus the prior year, as higher interest

income and modest deposit growth were offset by lower

mortgage revenues due to fewer mortgage originations.

Global Wealth revenues of $7.4 billion decreased 2%

versus the prior year, as investment product revenue

headwinds, particularly in Asia, more than offset net interest

income growth from higher interest rates and higher loan and

deposit volumes.

For additional information on the results of operations of

PBWM in 2022, see “Personal Banking and Wealth

Management” below.

Legacy Franchises

Legacy Franchises net loss of $12 million compared to net

income of $1 million in the prior year, primarily driven by

higher cost of credit, partially offset by lower expenses and

higher revenues, primarily reflecting the Philippines and

Thailand gains on sales in the current year and the Australia

loss on sale in the prior year. Legacy Franchises expenses of

$7.8 billion decreased 6%, largely driven by the absence of the

Korea VERP charge in the prior year and the benefit from

closing the five exit markets, partially offset by the $535

million goodwill impairment, an approximate $70 million

impairment of long-lived assets related to the Russia consumer

banking business and $156 million of other aggregate

divestiture-related costs.

Legacy Franchises revenues of $8.5 billion increased 3%

versus the prior year, primarily driven by the Philippines and

Thailand gains on sale versus the Australia loss on sale in the

prior year. Excluding these divestiture-related impacts,

revenues decreased 15%, primarily driven by the reduction in

revenues from the closings of the five exit markets, as well as

the impact of the ongoing Korea and Russia wind-downs.

For additional information on the results of operations of

Legacy Franchises in 2022, see “Legacy Franchises” below.

Corporate/Other

Corporate/Other net income was $879 million, compared to a

net loss of $8 million in the prior year, reflecting higher

revenue and lower expenses, partially offset by lower income

tax benefits, as well as the second quarter of 2022 release of a

CTA (cumulative translation adjustment) loss (net of hedges)

from Accumulated other comprehensive income (loss) (AOCI)

related to the substantial liquidation of a legacy U.K.

consumer operation, recorded in discontinued operations.

Corporate/Other operating expenses of $953 million

decreased 31%, primarily driven by lower consulting expenses

and the impact of certain legal settlements.

Corporate/Other revenues of $1.4 billion increased from

$0.5 billion in the prior year, driven by higher net interest

income, primarily from the investment portfolio, partially

offset by lower non-interest revenue, primarily due to the

absence of mark-to-market gains in the prior year as well as

higher hedging costs.

For additional information on the results of operations of

Corporate/Other in 2022, see “Corporate/Other” below.

5

Macroeconomic and Other Risks and Uncertainties

Various geopolitical and macroeconomic challenges and

uncertainties continue to adversely impact economic

conditions in the U.S. and globally. The U.S. and other

countries have continued to experience significantly elevated

levels of inflation, resulting in central banks implementing a

series of interest rates increases, with additional increases

expected in the near term. In addition to causing a

humanitarian crisis, the war in Ukraine continues to disrupt

energy and food markets. An economic rebound in China

remains uncertain, due to the ongoing impacts from

COVID-19, the amount of leverage in its economy and stress

in the property sector. These and other factors have adversely

affected financial markets, negatively impacted global

economic growth rates, contributed to lower consumer

confidence and increased the risk of recession in Europe, the

U.S. and other countries. These and other factors could

adversely affect Citi’s customers, clients, businesses, funding

costs, expenses and results during 2023.

In addition, Citi could incur a significant loss on sale in

2023, due to CTA losses (net of hedges) in AOCI, goodwill

write-offs and other AOCI loss components, related to the

potential signing of a sale agreement for any of its remaining

consumer banking divestitures. The majority of these losses

would be regulatory capital neutral at closing.

For a further discussion of trends, uncertainties and risks

that will or could impact Citi’s businesses, results of

operations, capital and other financial condition during 2023,

see “2022 Results Summary” above and “Risk Factors,” each

respective business’s results of operations and “Managing

Global Risk,” including “Managing Global Risk—Other Risks

—Country Risk—Russia,” below.

CITI’S CONSENT ORDER COMPLIANCE

Citi has embarked on a multiyear transformation, with the

target outcome to change Citi’s business and operating models

such that they simultaneously strengthen risk and controls and

improve Citi’s value to customers, clients and shareholders.

This includes efforts to effectively implement the October

2020 Federal Reserve Board (FRB) and Office of the

Comptroller of the Currency (OCC) consent orders issued to

Citigroup and Citibank, respectively. In the second quarter of

2021, Citi made an initial submission to the OCC, and

submitted its plans to address the consent orders to both

regulators during the third quarter of 2021. Citi continues to

work constructively with the regulators and provides to both

regulators on an ongoing basis additional information

regarding its plans and progress. Citi will continue to reflect

their feedback in its project plans and execution efforts.

As discussed above, Citi’s efforts include continued

investments in its transformation, including the remediation of

its consent orders. Citi’s CEO has made the strengthening of

Citi’s risk and control environment a strategic priority and has

established a Chief Administrative Officer organization to

centralize program management. In addition, the Citigroup

and Citibank Boards of Directors each formed a

Transformation Oversight Committee, an ad hoc committee of

each Board, to provide oversight of management’s

remediation efforts under the consent orders. The Citi Board

of Directors has determined that Citi’s plans are responsive to

the Company’s objectives and that progress continues to be

made on execution of the plans.

For additional information about the consent orders, see

“Risk Factors—Compliance Risks” below and Citi’s Current

Report on Form 8-K filed with the SEC on October 7, 2020.

6

This page intentionally left blank.

7

RESULTS OF OPERATIONS

SUMMARY OF SELECTED FINANCIAL DATA

Citigroup Inc. and Consolidated Subsidiaries

In millions of dollars, except per share amounts

2022 2021 2020 2019 2018

Net interest income $ 48,668 $ 42,494 $ 44,751 $ 48,128 $ 47,744

Non-interest revenue 26,670 29,390 30,750 26,939 26,292

Revenues, net of interest expense $ 75,338 $ 71,884 $ 75,501 $ 75,067 $ 74,036

Operating expenses 51,292 48,193 44,374 42,783 43,023

Provisions for credit losses and for benefits and claims 5,239 (3,778) 17,495 8,383 7,568

Income from continuing operations before income taxes $ 18,807 $ 27,469 $ 13,632 $ 23,901 $ 23,445

Income taxes 3,642 5,451 2,525 4,430 5,357

Income from continuing operations $ 15,165 $ 22,018 $ 11,107 $ 19,471 $ 18,088

Income (loss) from discontinued operations, net of taxes (231) 7 (20) (4) (8)

Net income before attribution of noncontrolling interests $ 14,934 $ 22,025 $ 11,087 $ 19,467 $ 18,080

Net income attributable to noncontrolling interests 89 73 40 66 35

Citigroup’s net income $ 14,845 $ 21,952 $ 11,047 $ 19,401 $ 18,045

Earnings per share

Basic

Income from continuing operations $ 7.16 $ 10.21 $ 4.75 $ 8.08 $ 6.69

Net income 7.04 10.21 4.74 8.08 6.69

Diluted

Income from continuing operations $ 7.11 $ 10.14 $ 4.73 $ 8.04 $ 6.69

Net income 7.00 10.14 4.72 8.04 6.68

Dividends declared per common share 2.04 2.04 2.04 1.92 1.54

Common dividends $ 4,028 $ 4,196 $ 4,299 $ 4,403 $ 3,865

Preferred dividends

(1)

1,032 1,040 1,095 1,109 1,174

Common share repurchases 3,250 7,600 2,925 17,875 14,545

Table continues on the next page, including footnotes.

8

SUMMARY OF SELECTED FINANCIAL DATA

(Continued)

Citigroup Inc. and Consolidated Subsidiaries

In millions of dollars, except per share amounts, ratios and direct staff

2022 2021 2020 2019 2018

At December 31:

Total assets $ 2,416,676 $ 2,291,413 $ 2,260,090 $ 1,951,158 $ 1,917,383

Total deposits 1,365,954 1,317,230 1,280,671 1,070,590 1,013,170

Long-term debt 271,606 254,374 271,686 248,760 231,999

Citigroup common stockholders’ equity 182,194 182,977 179,962 175,262 177,760

Total Citigroup stockholders’ equity 201,189 201,972 199,442 193,242 196,220

Average assets 2,396,023 2,347,709 2,226,454 1,978,805 1,920,242

Direct staff (in thousands) 240 223 210 200 204

Performance metrics

Return on average assets 0.62 % 0.94 % 0.50 % 0.98 % 0.94 %

Return on average common stockholders’ equity

(2)

7.7 11.5 5.7 10.3 9.4

Return on average total stockholders’ equity

(2)

7.5 10.9 5.7 9.9 9.1

Return on tangible common equity (RoTCE)

(3)

8.9 13.4 6.6 12.1 11.0

Efficiency ratio (total operating expenses/total revenues, net) 68.1 67.0 58.8 57.0 58.1

Basel III ratios

CET1 Capital

(4)

13.03 % 12.25 % 11.51 % 11.79 % 11.86 %

Tier 1 Capital

(4)

14.80 13.91 13.06 13.33 13.43

Total Capital

(4)

15.46 16.04 15.33 15.87 16.14

Supplementary Leverage ratio 5.82 5.73 6.99 6.20 6.40

Citigroup common stockholders’ equity to assets 7.54 % 7.99 % 7.96 % 8.98 % 9.27 %

Total Citigroup stockholders’ equity to assets 8.33 8.81 8.82 9.90 10.23

Dividend payout ratio

(5)

29 20 43 24 23

Total payout ratio

(6)

53 56 73 122 109

Book value per common share $ 94.06 $ 92.21 $ 86.43 $ 82.90 $ 75.05

Tangible book value (TBV) per share

(3)

81.65 79.16 73.67 70.39 63.79

(1) Certain series of preferred stock have semiannual payment dates. See Note 21.

(2) The return on average common stockholders’ equity is calculated using net income less preferred stock dividends divided by average common stockholders’

equity. The return on average total Citigroup stockholders’ equity is calculated using net income divided by average Citigroup stockholders’ equity.

(3) RoTCE and TBV are non-GAAP financial measures. For information on RoTCE and TBV, see “Capital Resources—Tangible Common Equity, Book Value Per

Share, Tangible Book Value Per Share and Returns on Equity” below.

(4) Citi’s binding CET1 Capital and Tier 1 Capital ratios were derived under the Basel III Standardized Approach as of December 31, 2022, 2021, 2019 and 2018, and

were derived under the Basel III Advanced Approaches framework as of December 31, 2020. Citi’s binding Total Capital ratio was derived under the Basel III

Advanced Approaches framework for all periods presented.

(5) Dividends declared per common share as a percentage of net income per diluted share.

(6) Total common dividends declared plus common share repurchases as a percentage of net income available to common shareholders (Net income less preferred

dividends). See “Consolidated Statement of Changes in Stockholders’ Equity,” Note 10 and “Equity Security Repurchases” below for the component details.

9

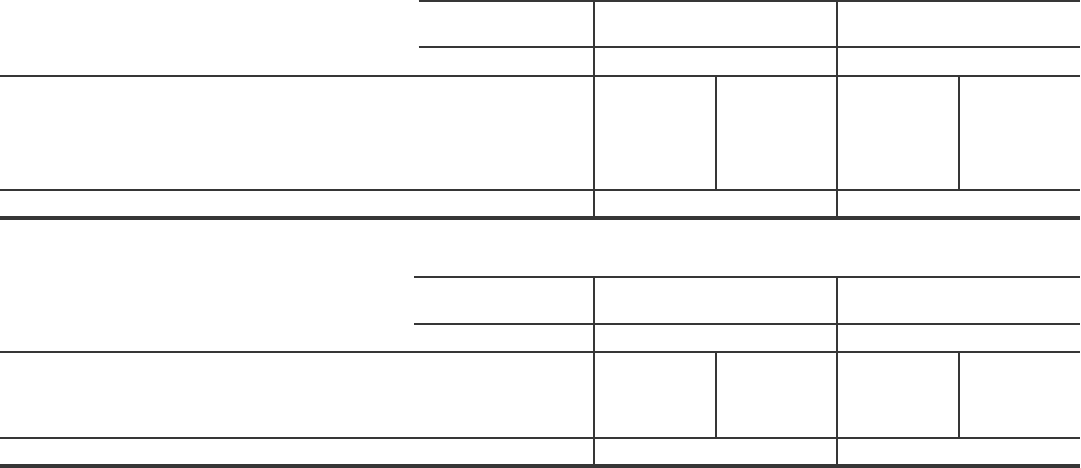

SEGMENT REVENUES AND INCOME (LOSS)

REVENUES

In millions of dollars

2022 2021 2020

% Change

2022 vs. 2021

% Change

2021 vs. 2020

Institutional Clients Group $ 41,206 $ 39,836 $ 41,093 3 % (3) %

Personal Banking and Wealth Management 24,217 23,327 25,140 4 (7)

Legacy Franchises 8,472 8,251 9,454 3 (13)

Corporate/Other 1,443 470 (186) NM NM

Total Citigroup net revenues $ 75,338 $ 71,884 $ 75,501 5 % (5) %

NM Not meaningful

INCOME

In millions of dollars

2022 2021 2020

% Change

2022 vs. 2021

% Change

2021 vs. 2020

Income (loss) from continuing operations

Institutional Clients Group $ 10,738 $ 14,308 $ 10,811 (25) % 32 %

Personal Banking and Wealth Management 3,319 7,734 1,322 (57) NM

Legacy Franchises (9) (9) (142) — 94

Corporate/Other 1,117 (15) (884) NM 98

Income from continuing operations $ 15,165 $ 22,018 $ 11,107 (31) % 98 %

Discontinued operations $ (231) $ 7 $ (20) NM NM

Less: Net income attributable to noncontrolling interests 89 73 40 22 % 83 %

Citigroup’s net income $ 14,845 $ 21,952 $ 11,047 (32) % 99 %

NM Not meaningful

10

SEGMENT BALANCE SHEET

(1)

—DECEMBER 31, 2022

In millions of dollars

Institutional

Clients

Group

Personal

Banking

and Wealth

Management

Legacy

Franchises

Corporate/Other

and

consolidating

eliminations

(2)

Citigroup

parent company-

issued long-term

debt and

stockholders’

equity

(3)

Total

Citigroup

consolidated

Assets

Cash and deposits with banks, net of

allowance $ 108,289 $ 6,411 $ 3,251 $ 224,074 $ — $ 342,025

Securities borrowed and purchased under

agreements to resell, net of allowance 364,673 425 303 — — 365,401

Trading account assets 319,376 2,250 639 11,849 — 334,114

Investments, net of allowance 140,613 73 1,516 384,380 — 526,582

Loans, net of unearned income and

allowance for credit losses on loans 279,337 324,260 36,650 — — 640,247

Other assets, net of allowance 111,477 25,559 27,764 43,507 — 208,307

Net intersegment liquid assets

(4)

406,143 134,852 26,592 (567,587) — —

Total assets $ 1,729,908 $ 493,830 $ 96,715 $ 96,223 $ — $ 2,416,676

Liabilities and equity

Total deposits $ 845,364 $ 437,813 $ 50,994 $ 31,783 $ — $ 1,365,954

Securities loaned and sold under

agreements to repurchase 199,895 80 2,469 — — 202,444

Trading account liabilities 168,550 1,636 258 203 — 170,647

Short-term borrowings 34,785 2 4 12,305 — 47,096

Long-term debt

(3)

93,219 189 75 11,866 166,257 271,606

Other liabilities 99,353 14,514 27,868 15,356 — 157,091

Net intersegment funding (lending)

(3)

288,742 39,596 15,047 24,061 (367,446) —

Total liabilities $ 1,729,908 $ 493,830 $ 96,715 $ 95,574 $ (201,189) $ 2,214,838

Total stockholders’ equity

(5)

— — — 649 201,189 201,838

Total liabilities and equity $ 1,729,908 $ 493,830 $ 96,715 $ 96,223 $ — $ 2,416,676

(1) The supplemental information presented in the table above reflects Citigroup’s consolidated GAAP balance sheet by reportable segment and component. The

respective segment information depicts the assets and liabilities managed by each segment.

(2) Consolidating eliminations for total Citigroup and Citigroup parent company assets and liabilities are recorded within Corporate/Other.

(3) Total stockholders’ equity and the majority of long-term debt of Citigroup are reflected on the Citigroup parent company balance sheet (see Notes 18 and 30).

Citigroup allocates stockholders’ equity and long-term debt to its businesses through intersegment allocations as shown above.

(4) Represents the attribution of Citigroup’s liquid assets (primarily consisting of cash, marketable equity securities and available-for-sale debt securities) to the

various businesses based on Liquidity Coverage ratio (LCR) assumptions.

(5) Corporate/Other equity represents noncontrolling interests.

11

INSTITUTIONAL CLIENTS GROUP

Institutional Clients Group (ICG) includes Services, Markets and Banking (for additional information on these businesses, see

“Citigroup Operating Segments” above). ICG provides corporate, institutional and public sector clients around the world with a full

range of wholesale banking products and services, including fixed income and equity sales and trading, foreign exchange, prime

brokerage, derivative services, equity and fixed income research, corporate lending, investment banking and advisory services, cash

management, trade finance and securities services. ICG transacts with clients in both cash instruments and derivatives, including fixed

income, foreign currency, equity and commodity products.

ICG’s revenue is generated primarily from fees and spreads associated with these activities. ICG earns fee income for assisting

clients with transactional services and clearing and providing brokerage and investment banking services and other such activities.

Such fees are recognized at the point in time when Citigroup’s performance under the terms of a contractual arrangement is

completed, which is typically at the trade/execution date or closing of a transaction. Revenue generated from these activities is

recorded in Commissions and fees and Investment banking fees. Revenue is also generated from assets under custody and

administration, which is recognized as/when the associated promised service is satisfied, which normally occurs at the point in time

the service is requested by the customer and provided by Citi. Revenue generated from these activities is primarily recorded in

Administration and other fiduciary fees. For additional information on these various types of revenues, see Note 5.

In addition, as a market maker, ICG facilitates transactions, including holding product inventory to meet client demand, and earns

the differential between the price at which it buys and sells the products. These price differentials and the unrealized gains and losses

on the inventory are recorded in Principal transactions. Mark-to-market gains and losses on certain credit derivatives (used to

economically hedge the corporate loan portfolio) are also recorded in Principal transactions (for additional information on Principal

transactions revenue, see Note 6). Other primarily includes realized gains and losses on available-for-sale (AFS) debt securities, gains

and losses on equity securities not held in trading accounts and other non-recurring gains and losses. Interest income earned on assets

held, less interest paid on long- and short-term debt, secured funding transactions and customers deposits, is recorded as Net interest

income.

The amount and types of Markets revenues are impacted by a variety of interrelated factors, including market liquidity; changes in

market variables such as interest rates, foreign exchange rates, equity prices, commodity prices and credit spreads, as well as their

implied volatilities; investor confidence and other macroeconomic conditions. Assuming all other market conditions do not change,

increases in client activity levels or bid/offer spreads generally result in increases in revenues. However, changes in market conditions

can significantly impact client activity levels, bid/offer spreads and the fair value of product inventory. For example, a decrease in

market liquidity may increase bid/offer spreads, decrease client activity levels and widen credit spreads on product inventory

positions. ICG’s management of the Markets businesses involves daily monitoring and evaluation of the above factors at the trading

desk as well as the country level.

In the Markets businesses, client revenues are those revenues directly attributable to client transactions at the time of inception,

including commissions, interest or fees earned. Client revenues do not include the results of client facilitation activities (e.g., holding

product inventory in anticipation of client demand) or the results of certain economic hedging activities.

ICG’s international presence is supported by trading floors in approximately 80 countries and a proprietary network in 95

countries and jurisdictions. As previously disclosed, Citi intends to end nearly all of the institutional banking services it offers in

Russia by the end of the first quarter of 2023. Going forward, Citi’s only operations in Russia will be those necessary to fulfill its

remaining legal and regulatory obligations. At this time, the estimated cost to be incurred in relation to this action is approximately

$80 million (excluding the impact from any portfolio sales), primarily through 2024. For additional information about Citi’s continued

efforts to reduce its operations and exposure in Russia, see “Legacy Franchises” and “Managing Global Risk—Other Risks—Country

Risk—Russia” below.

At December 31, 2022, ICG had $1.7 trillion in assets and $845 billion in deposits. Securities services managed $22.2 trillion in

assets under custody and administration at December 31, 2022, of which Citi provided both custody and administrative services to

certain clients related to $1.9 trillion of such assets. Managed assets under trust were $4.0 trillion at December 31, 2022. For additional

information on these operations, see “Administration and Other Fiduciary Fees” in Note 5.

In millions of dollars, except as otherwise noted

2022 2021 2020

% Change

2022 vs. 2021

% Change

2021 vs. 2020

Commissions and fees $ 4,404 $ 4,300 $ 3,961 2 % 9 %

Administration and other fiduciary fees 2,684 2,693 2,348 — 15

Investment banking fees

(1)

3,573 6,709 4,982 (47) 35

Principal transactions 13,633 9,763 12,916 40 (24)

Other (999) 1,372 1,136 NM 21

Total non-interest revenue $ 23,295 $ 24,837 $ 25,343 (6) % (2) %

Net interest income (including dividends) 17,911 14,999 15,750 19 (5)

Total revenues, net of interest expense $ 41,206 $ 39,836 $ 41,093 3 % (3) %

Total operating expenses

(2)

$ 26,299 $ 23,949 $ 22,336 10 % 7 %

12

Net credit losses on loans $ 152 $ 356 $ 877 (57) % (59) %

Credit reserve build (release) for loans 478 (2,093) 2,582 NM NM

Provision (release) for credit losses on unfunded lending

commitments 187 (753) 1,390 NM NM

Provisions for credit losses on HTM debt securities and other

assets 94 — 20 — 100

Provisions (releases) for credit losses $ 911 $ (2,490) $ 4,869 NM NM

Income from continuing operations before taxes $ 13,996 $ 18,377 $ 13,888 (24) % 32 %

Income taxes 3,258 4,069 3,077 (20) 32

Income from continuing operations $ 10,738 $ 14,308 $ 10,811 (25) % 32 %

Noncontrolling interests 79 83 50 (5) 66

Net income $ 10,659 $ 14,225 $ 10,761 (25) % 32 %

Balance Sheet data (in billions of dollars)

EOP assets $ 1,730 $ 1,613 $ 1,592 7 % 1 %

Average assets 1,716 1,669 1,566 3 7