Global Monitoring Report on

Non-Bank Financial Intermediation

2023

18 December 2023

The Financial Stability Board (FSB) coordinates at the international level the work of national

financial authorities and international standard-setting bodies in order to develop and promote

the implementation of effective regulatory, supervisory and other financial sector policies. Its

mandate is set out in the FSB Charter, which governs the policymaking and related activities of

the FSB. These activities, including any decisions reached in their context, shall not be binding

or give rise to any legal rights or obligations.

Contact the Financial Stability Board

Sign up for e-mail alerts: www.fsb.org/emailalert

Follow the FSB on Twitter: @FinStbBoard

E-mail the FSB at: [email protected]

Copyright © 2024 Financial Stability Board. Please refer to the terms and conditions

iii

Table of Contents

Executive summary ................................................................................................................. 1

Introduction .............................................................................................................................. 4

1. Financial intermediation in the global financial system ..................................................... 6

1.1. Developments in 2022 ........................................................................................... 6

1.2. Credit assets, wholesale funding, and financial leverage .................................... 15

1.3. Interconnectedness among financial sectors ....................................................... 22

2. The narrow measure of NBFI ......................................................................................... 28

2.1. Narrow measure trends ....................................................................................... 29

2.2. Collective investment vehicles with features that make them susceptible to runs

(EF1) .................................................................................................................... 34

2.3. Loan provision dependent on short-term funding (EF2) ...................................... 48

2.4. Intermediation of market activities dependent on short-term funding (EF3) ........ 52

2.5. Insurance or guarantees of financial products (EF4) ........................................... 57

2.6. Securitisation-based credit intermediation (EF5) ................................................. 59

3. Case study on private finance and non-bank financial intermediation ............................ 63

3.1. Introduction .......................................................................................................... 63

3.2. Private finance and the role of NBFI .................................................................... 63

3.3. Key market segments and developments in private finance ............................... 65

3.4. Private finance in the FSB global monitoring report ............................................ 66

3.5. Interconnectedness – across sectors and globally .............................................. 69

Annex 1: Jurisdiction-specific financial sectors ...................................................................... 72

Annex 2: Summary table ....................................................................................................... 74

Annex 3: Main developments per major NBFI sub-sectors ................................................... 75

Annex 4: Narrowing down and exclusion of NBFI entity types from the narrow measure ..... 79

Annex 5: Vulnerability metrics ............................................................................................... 84

Annex 6: Additional statistics ................................................................................................. 88

Annex 7: Sankey charts ......................................................................................................... 90

Abbreviations ......................................................................................................................... 94

iv

1

Executive summary

This report assesses global trends in the non-bank financial intermediation (NBFI) sector

for the year ending 31 December 2022. It presents the results of the 13th annual FSB global

monitoring exercise, covering 29 jurisdictions that account for around 85% of global GDP. It

describes broad trends in financial intermediation before narrowing its focus to the subset of

NBFI activities that may be more likely to give rise to vulnerabilities (narrow measure). The report

mainly covers developments in 2022, during which most economies experienced a rising interest

rate environment in response to inflationary pressures. The report also includes a case study

exploring the role of NBFI in private finance and providing examples in key selected jurisdictions.

The size of the NBFI sector decreased in 2022, which is the first notable decrease since

2009, and which can be largely attributed to the impact of higher interest rates

. Total

financial assets of the NBFI sector declined 5.5% compared to 2021, mainly reflecting valuation

losses in mark-to-market asset portfolios, particularly in investment funds. Total financial assets

held by banks increased 6.9% as bank portfolios, largely composed of loans, traditionally have

a lower sensitivity to interest rate changes. As a result, the relative share of total global financial

assets held by the NBFI sector decreased from 49.8% to 47.2%. In emerging market economies,

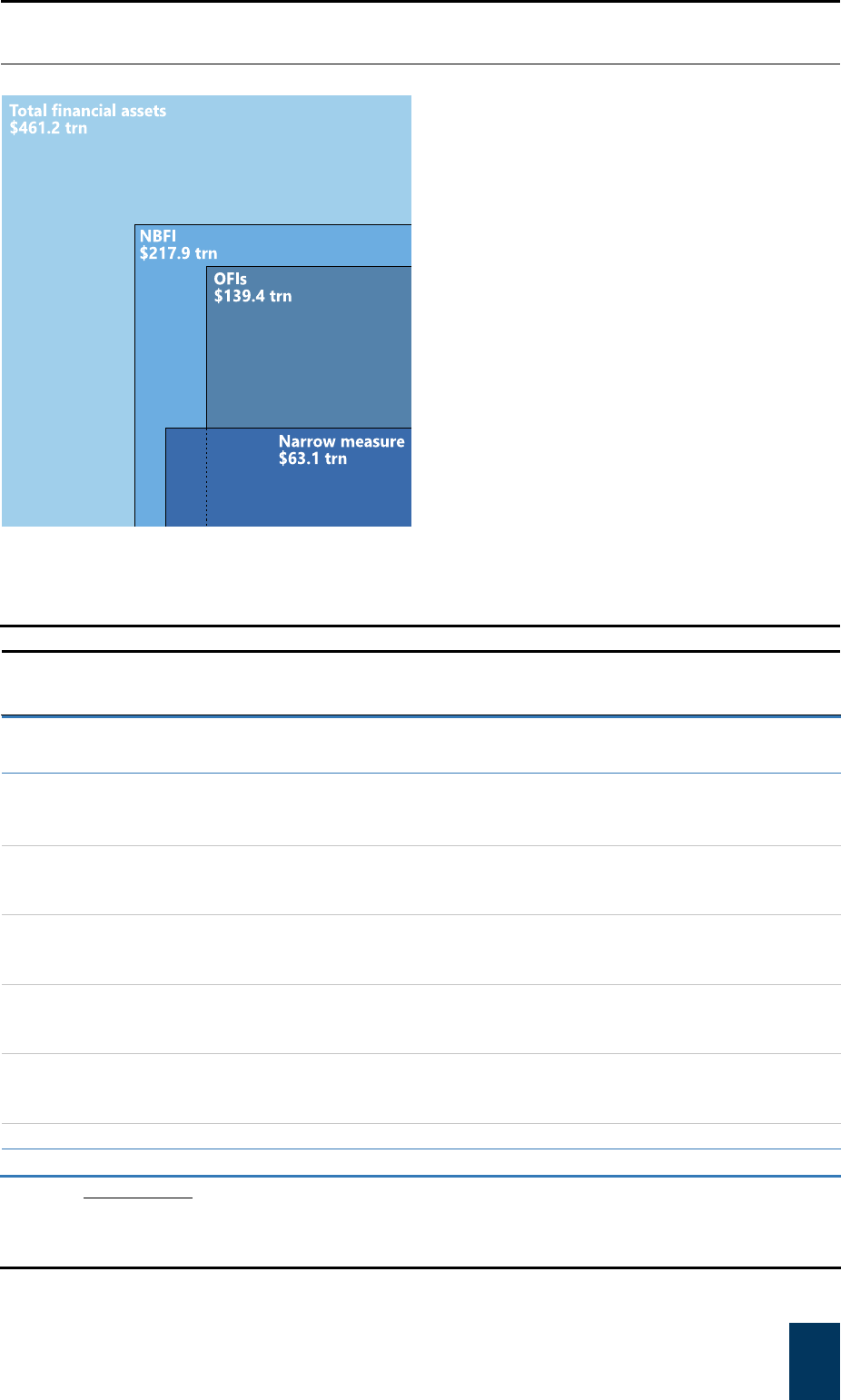

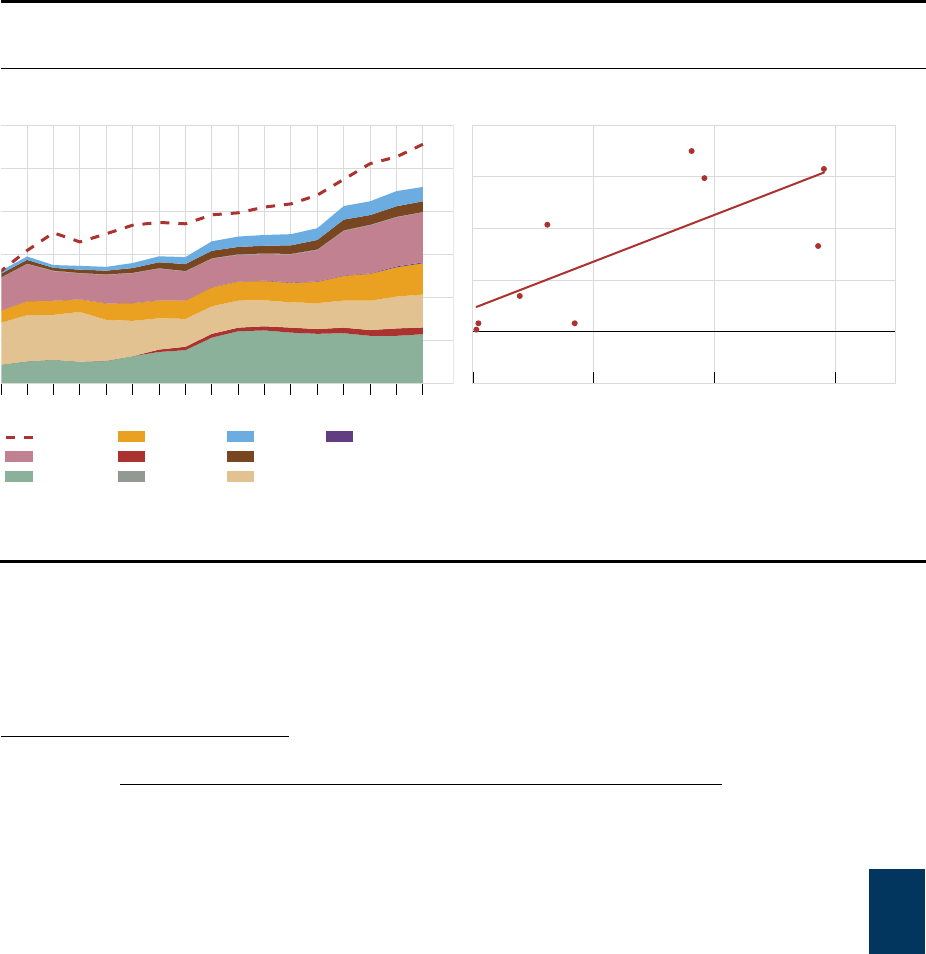

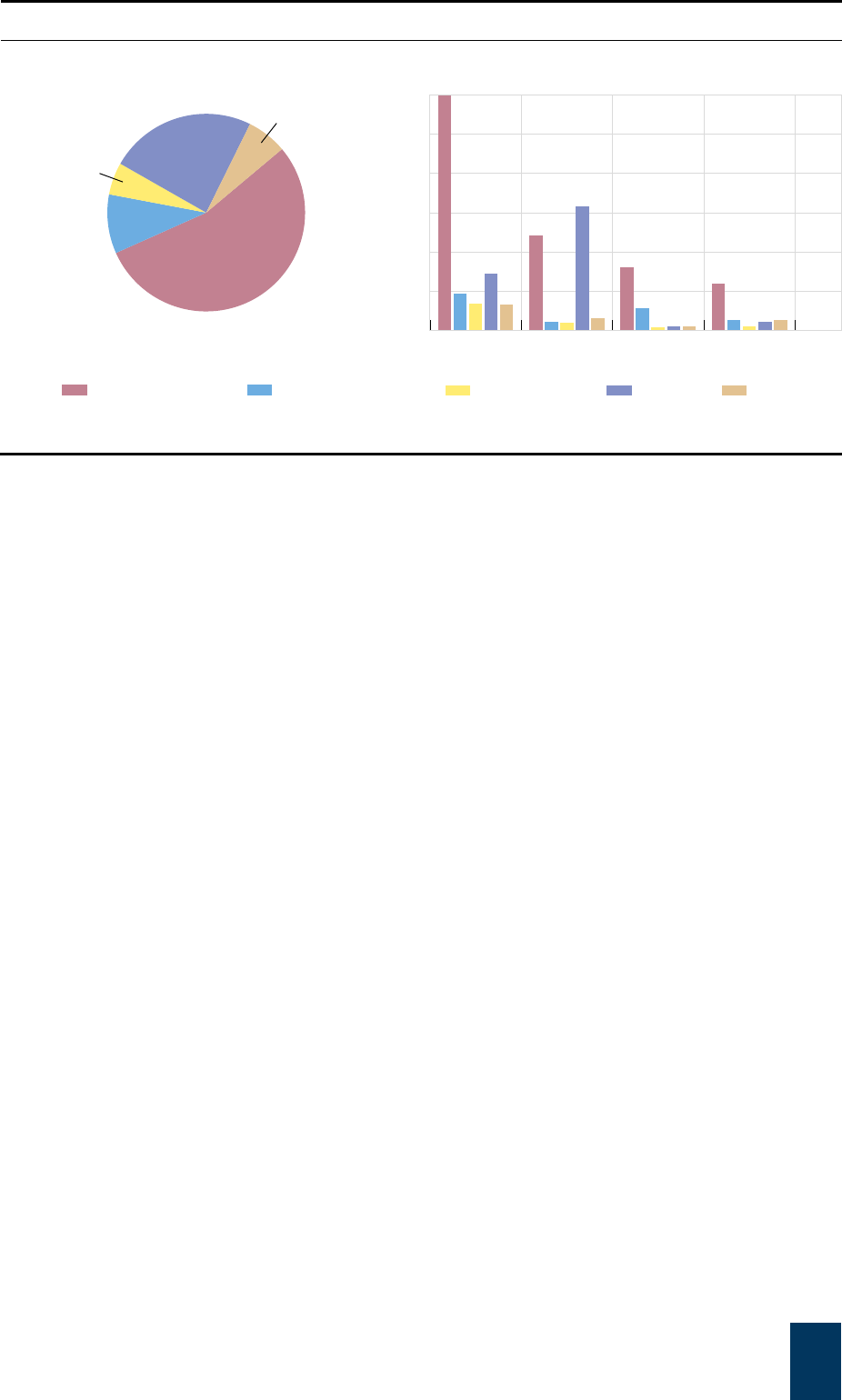

however, this share marginally increased. Graph 0-1 provides the size of the main monitoring

aggregates.

The financial assets of entities classified into the five economic functions of the narrow

measure set out in the FSB monitoring approach decreased 2.9%, approximately half of

the decrease observed in the NBFI sector. The narrow measure of NBFI declined to $63.1

trillion in 2022, representing 28.9% of total NBFI assets and 13.9% of total global financial

assets. This decline can be almost entirely attributed to collective investment vehicles

susceptible to runs (economic function 1), as the four other economic functions continued to

grow. Table 0-1 provides an overview of the size and growth of each economic function.

Fixed income funds remained the largest entity type within economic function 1, while

money market funds (MMFs) became the second largest entity type. Fixed income fund

assets accounted for 24.5% of total economic function 1 assets, having declined 14.3% year on

year. MMFs experienced different trends to other types of funds: inflows over the period Q2-Q4

2022 increased the assets under management (AUM) of non-government and longer-term

MMFs, as these funds’ yields were attractive to investors. On the other hand, outflows from

short-term government MMFs led to a slight reduction in their AUM in the first part of 2022, but

these outflows were reversed in Q4 2022. Similar to fixed income funds, mixed fund assets

decreased and became the third largest entity in economic function 1. Credit hedge funds

remained the fourth largest entity in economic function 1, though their AUM increased in 2022.

In contrast to economic function 1, assets of entities belonging to the four other

economic functions increased in 2022. The main entity types for economic functions 2 to 5

were finance companies (81.5% of total economic function 2), broker-dealers (97.8%), insurance

corporations and mortgage insurers (37.1% and 29.5%), and structured finance vehicles

(95.1%), respectively. The increase in assets ranged from 1.4% to 8.6% across entities in these

four economic functions, but their relatively smaller share compared to economic function 1 still

led to an overall decline in the size of the narrow measure.

2

Interconnectedness between the banking and NBFI sectors decreased for the banking

sector but increased for the NBFI sector, as measured as a proportion of the respective

sector assets. Data enhancements in this year’s report reduced unspecified linkages across all

non-bank entity types and were most notable in the case of pension funds, where identified

linkages increased 25–30 percentage points with regard to both claims and liabilities. Banks

continued to be net recipients of funding from NBFI entities, although this funding has been

gradually decreasing since 2013 when measured as a proportion of bank assets. In contrast,

interconnectedness between other financial intermediaries (OFIs) – a subset of the overall NBFI

sector that excludes insurance corporations, pension funds, and financial auxiliaries (see

Graph 0-1) – and banks, when measured as a proportion of OFI assets, increased in 2022. OFIs’

use of wholesale funding (in particular long-term funding) increased slightly in 2022, reversing

the trend observed over the previous four years. MMFs, trust companies, other investment funds

(OIFs) – defined as funds other than MMFs, hedge funds and real estate investment trusts and

funds – and structured finance vehicles tended to be cash providers through reverse repo

transactions. Meanwhile, hedge funds, finance companies, and broker-dealers reported an

almost net zero repo position.

Most vulnerability metrics remained stable over the past year, with some entity types

showing high degrees of liquidity and maturity transformation. For this report, jurisdictions

were asked for the first time to provide percentile data for the metrics for credit intermediation

and liquidity and maturity transformation for economic function 1 entities. The additional data

showed that metrics for maturity transformation in fixed income funds were high overall, while

those of mixed funds displayed dispersed levels. Metrics for liquidity transformation were also

high across most funds. Economic function 1 entity types continued to report low balance sheet

leverage both across and within jurisdictions. To complement the monitoring of these

vulnerabilities, which is conducted on a pre-mitigant basis, jurisdictions also provided information

on the availability of policy tools for economic function 1 entities (see Box 2-1). The vulnerability

metrics for economic function 2 remained largely stable year on year. For economic function 3,

metrics of maturity and liquidity transformation decreased in 2022, while credit intermediation

and leverage increased. Vulnerability metrics for economic function 5 increased slightly. The

importance of economic function 4 may be significantly understated because of the difficulty of

adequately capturing off-balance sheet exposures and the lack of vulnerability metrics.

Market prices have generally rebounded since the analysis presented in this report for

2022. In particular, data on the first quarter of 2023 showed increased AUM for all fund types,

which is mostly due to valuation effects for equity, fixed income, and mixed funds. The AUM of

both short-term government and non-government MMFs increased due to inflows, especially

following the banking sector turmoil in March 2023. These developments and potential

implications for vulnerabilities in the NBFI sector will be assessed in next year’s report.

3

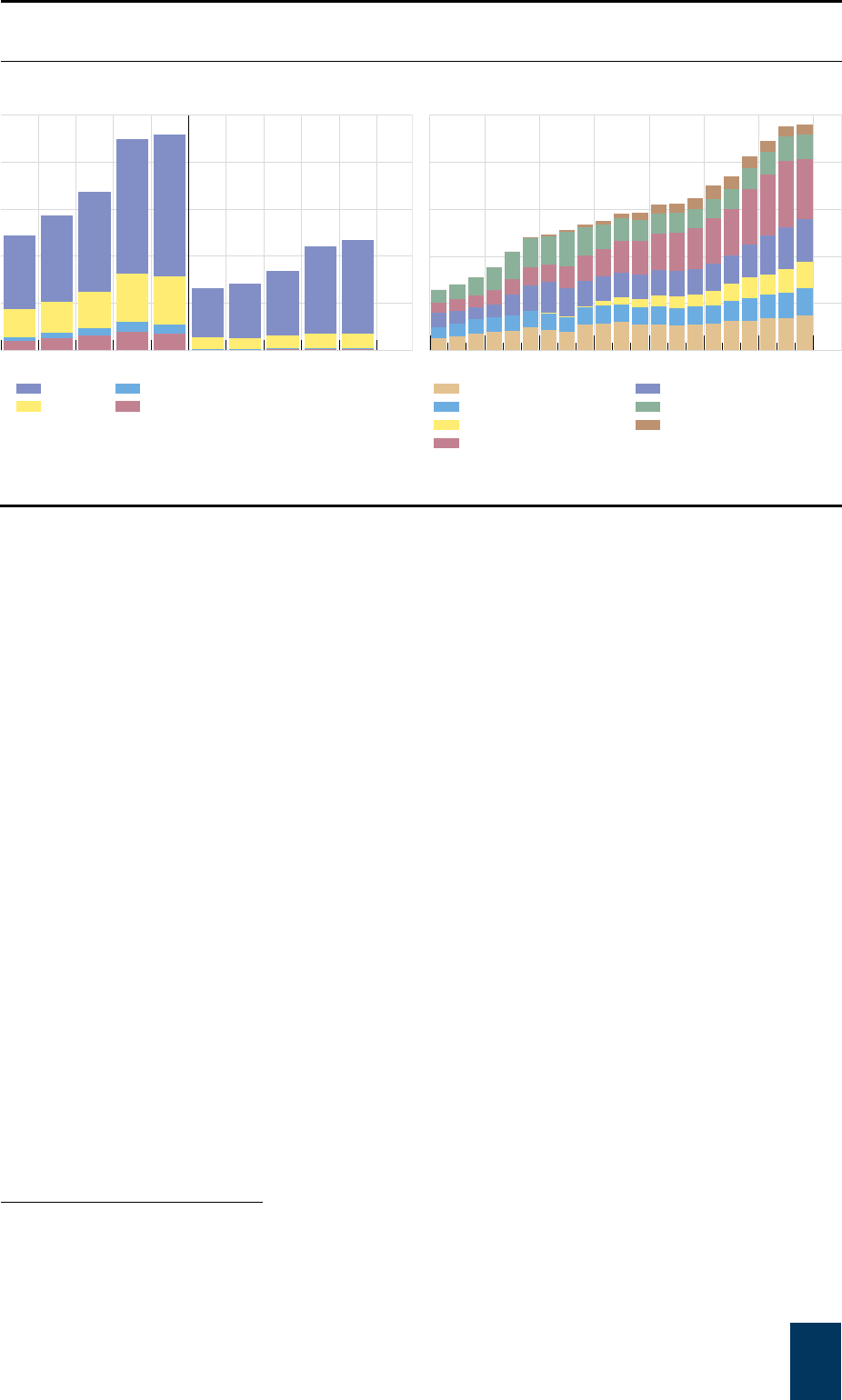

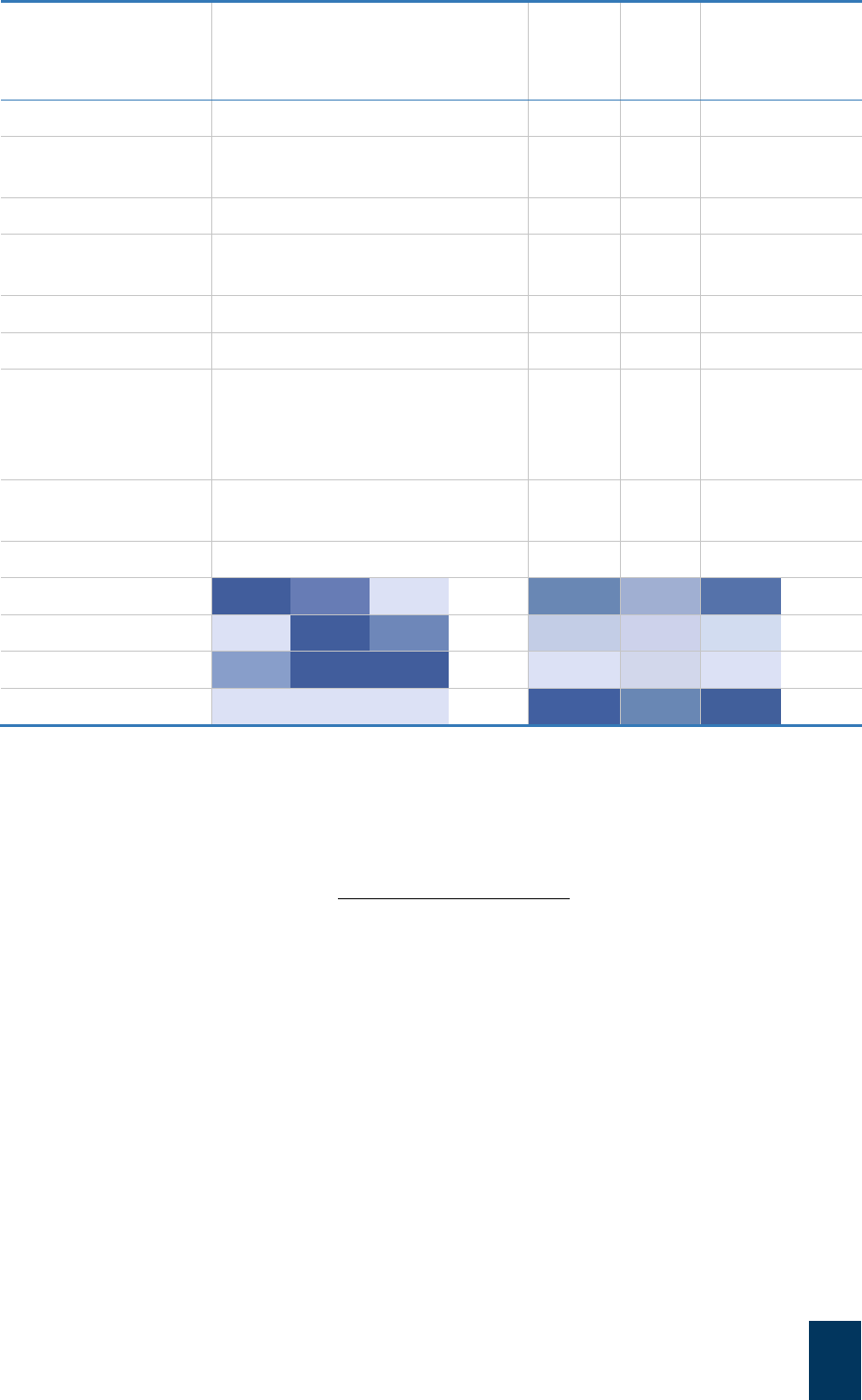

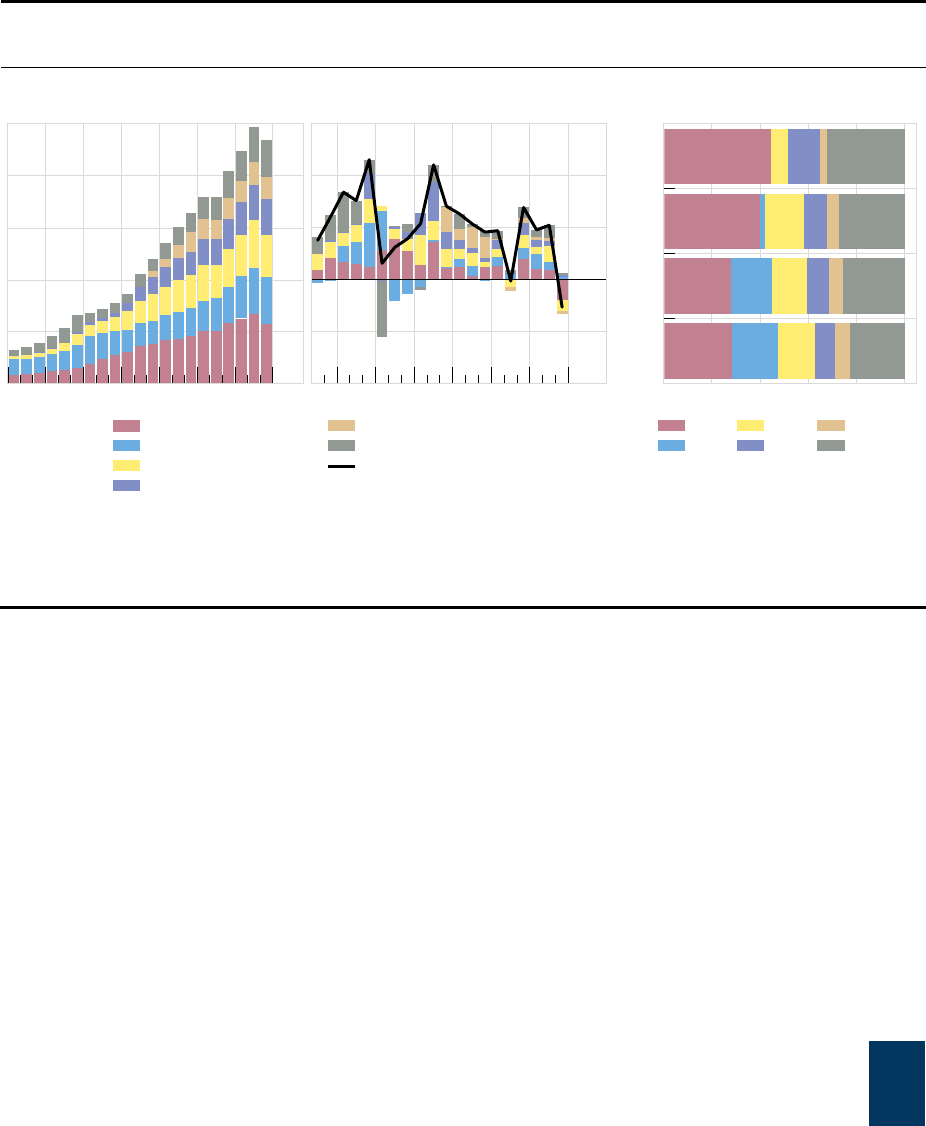

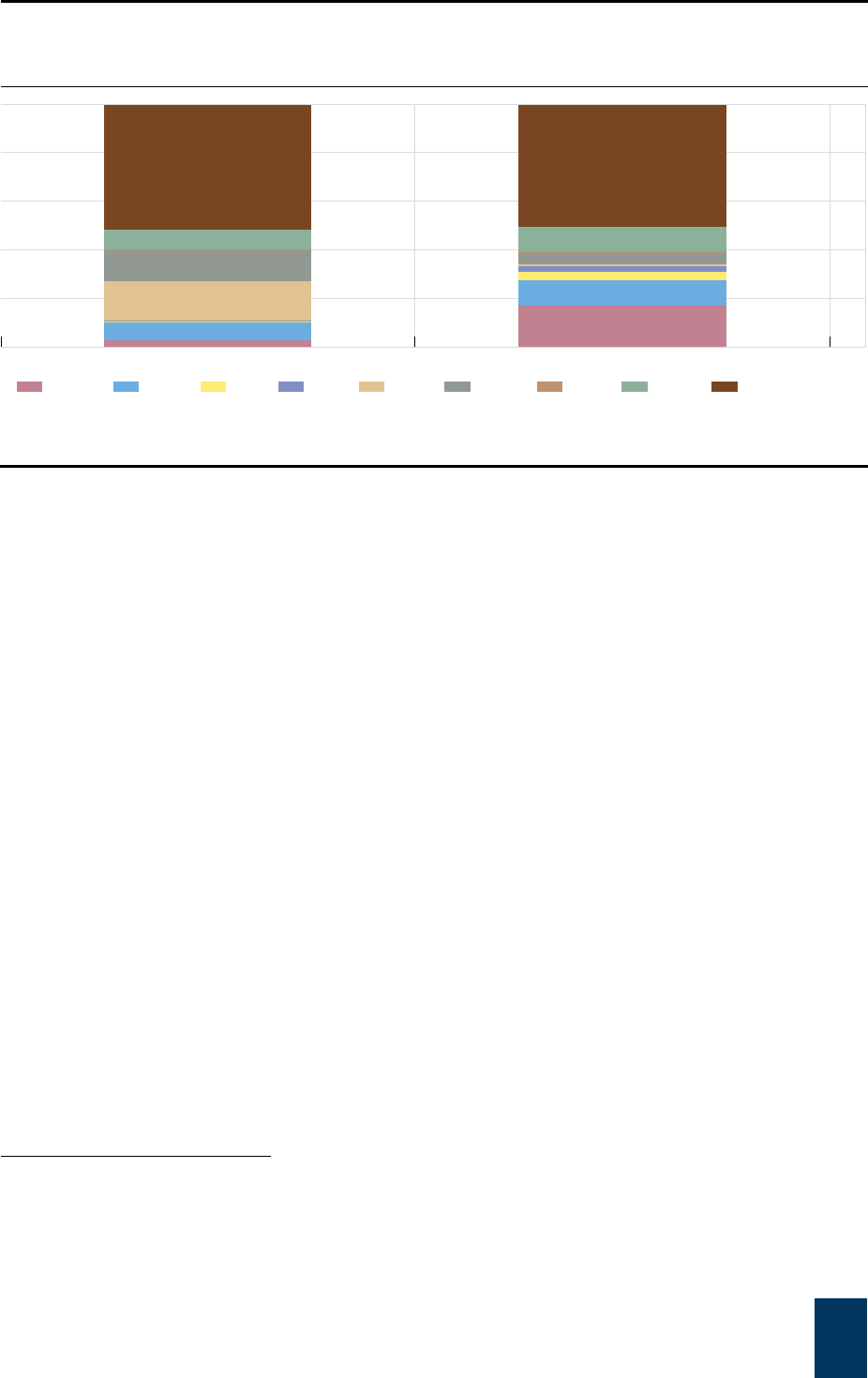

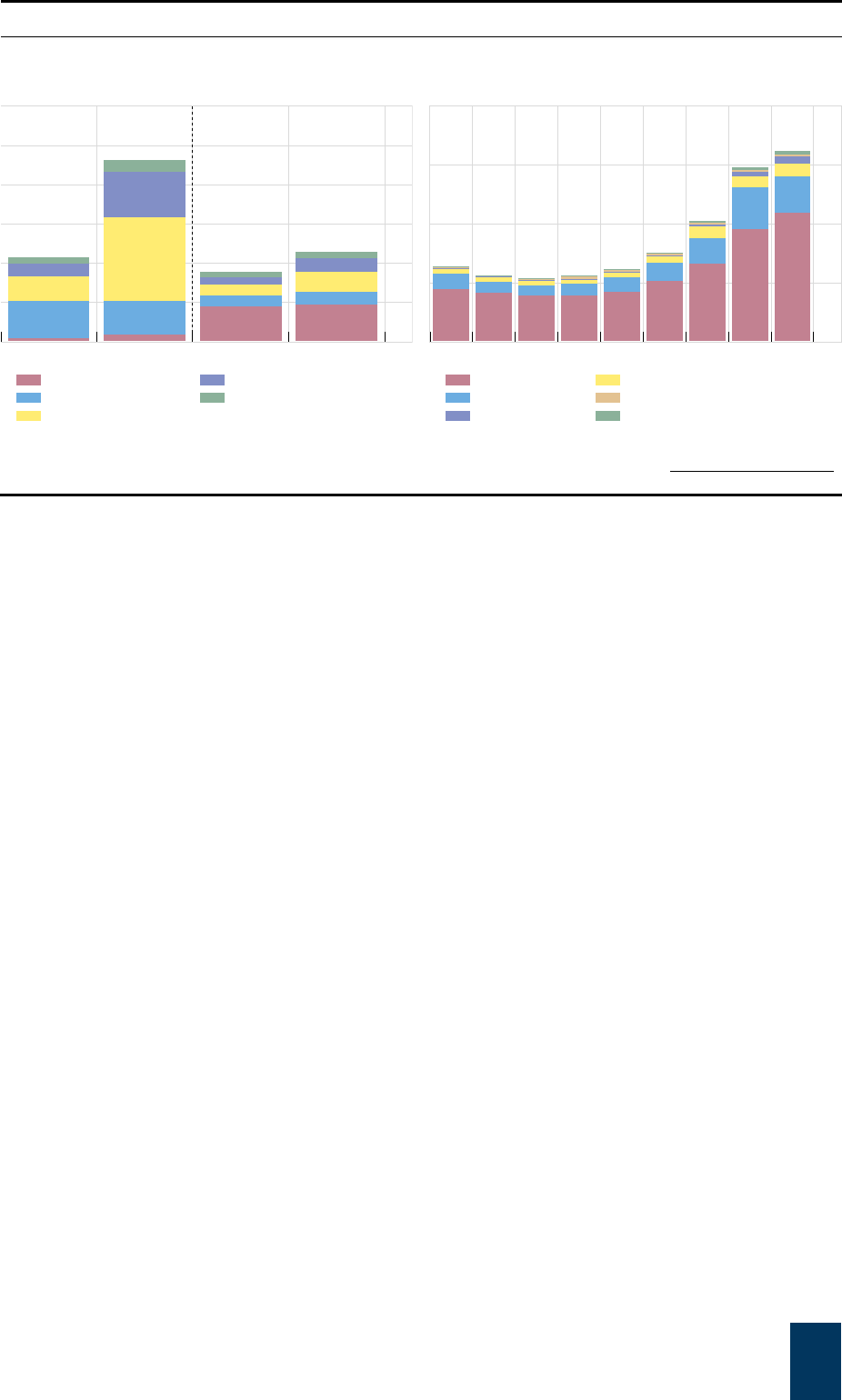

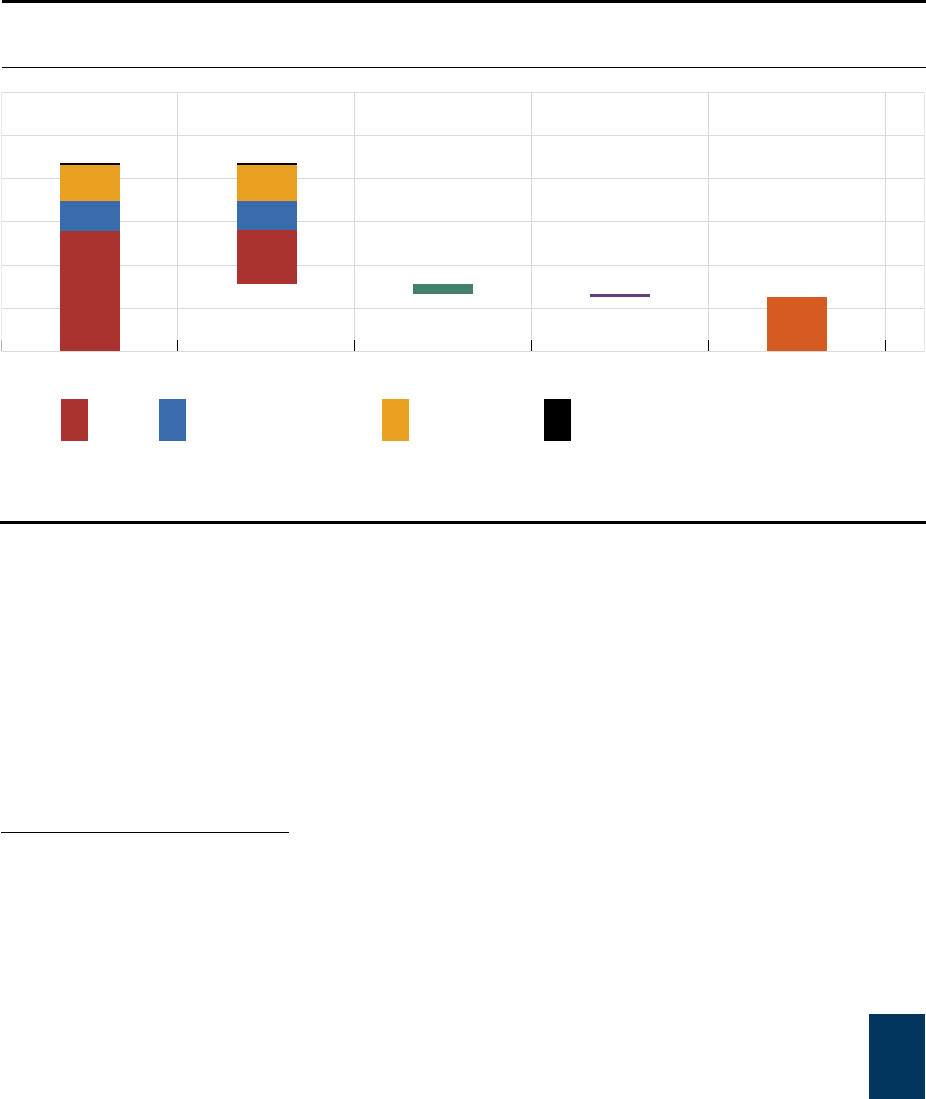

Size of monitoring aggregates and composition of the narrow measure

A

t end-2022 Graph 0-1

Narrowing down to the narrow measure

1

Monitoring aggregates

T

he following monitoring aggregates are referenced throughout

t

his report:

(

i) The NBFI sector is a broad measure of all non-bank financial

entities, composed of all financial institutions that are not

central banks, banks, or public financial institutions.

(

ii) Other financial intermediaries (OFIs) are a subset of the

NBFI sector, composed of all financial institutions that are

not central banks, banks, public financial institutions,

insurance corporations (ICs), pension funds (PFs), o

r

financial auxiliaries. OFIs include money market funds

(MMFs), hedge funds (HFs), other investment funds (OIFs),

captive financial institutions and money lenders, central

counterparties (CCPs), broker-dealers (BDs), finance

companies (FinCos), trust companies (TCs), and structured

finance vehicles (SFVs).

(

iii) The narrow measure of NBFI is composed of NBFI entities

that authorities have assessed as being involved in credit

intermediation activities that may pose bank-like financial

stability risks (i.e. credit intermediation that involves

maturity/liquidity transformation, leverage or imperfect credit

risk transfer) and/or regulatory arbitrage, according to the

methodology and classification guidance used in the FSB’s

annual NBFI monitoring exercise.

1

Total financial assets, NBFI and OFIs include participating jurisdictions and all of the euro area countries, whereas the narrow measure

includes only participating jurisdictions. The semi-dashed area in the LHS graph showing the narrow measure represents assets that were

not from OFIs and that correspond to ICs included in EF4 and to other financial auxiliaries unallocated to the five economic functions. This

graph does not include data for Russia.

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

Composition of the narrow measure

A

t end-2022 Table 0-1

Economic Functions Typical entity types

1

Size

2

(USD trn)

Share

(%)

Change in

2022 (%)

EF1 (collective investment

vehicles with features that make

them susceptible to runs)

MMFs, fixed income funds,

mixed funds, credit hedge funds

3

,

real estate funds

46.9 74.3 -5.2

EF2 (lending dependent on

short-term funding)

Finance companies,

leasing/factoring companies,

consumer credit companies

5.0 7.9 9.7

EF3 (market intermediation

dependent on short-term funding)

Broker-dealers, custodial

accounts, securities finance

companies

4.5 7.1 4.6

EF4 (facilitation of credit

intermediation)

Credit insurance companies,

financial guarantors, monoline

insurers

0.1 0.2 7.2

EF5 (securitisation-based credit

intermediation)

Securitisation vehicles,

structured finance vehicles,

asset-backed securities

5.0 7.8 2.0

Unallocated Other financial auxiliaries 1.6 2.6 -3.5

Total 63.1 100 -2.9

1

The FSB’s Policy Framework acknowledges that the narrow measure may take different forms across jurisdictions because of different

legal and regulatory settings, as well as the constant innovation and dynamic nature of the non-bank financial sector. It also enables

authorities to capture new structures or innovations that may introduce vulnerability, by examining underlying economic functions. Thus, the

entity types listed should be taken as typical examples.

2

Net of prudential consolidation into banking groups.

3

Credit hedge funds are

hedge funds that invest primarily in credit assets (e.g. bonds, loans). This table does not include data for Russia.

4

Introduction

The comprehensive monitoring of global trends, risks, and innovations of the NBFI sector

is a key part of the FSB’s ongoing efforts to enhance financial system resilience.

1

The

FSB’s annual global monitoring exercise uses sectoral balance sheet data from national financial

accounts statistics (“flow of funds”), complemented with supervisory and other publicly available

data.

2

This year’s edition mostly uses data as of end-2022 and primarily discusses developments

related to the NBFI sector up until that date.

The monitoring exercise adopts a two-step approach.

3

The first step takes a comprehensive

look at the NBFI sector to ensure that the collected data covers all areas where vulnerabilities

might arise within the financial system, including from recent NBFI related innovations (see Box

1-2). The second step of the monitoring approach focuses on vulnerabilities associated with the

NBFI sector that resemble those in the banking system or where regulatory arbitrage could

undermine the goals of regulatory reforms enacted after the global financial crisis. To arrive at

the narrow measure of the NBFI sector, the participating jurisdictions classify a subset of NBFI

entities on the basis of their economic functions (or activities) that may give rise to vulnerabilities

because they involve liquidity/maturity transformation, imperfect credit risk transfer, or use of

leverage (see Section 2).

4

To enhance consistency across jurisdictions, this classification is done

on a conservative and inclusive basis, reflecting the assumption that policy measures and/or risk

management tools have not been exercised (i.e. on a pre-mitigant basis). Consequently, the

narrow measure may overestimate the degree to which NBFI currently gives rise to post-mitigant

financial stability risks, given that existing policy measures, risk management tools, or structural

features may have significantly reduced or addressed financial stability risks.

Each year, the FSB aims to enhance the annual monitoring exercise by learning from the

experiences of previous exercises. This year’s monitoring exercise includes enhancements

in (i) the interconnectedness data; (ii) data on sources of funding to allow an assessment of

leverage trends per entity type; and (iii) the vulnerability metrics data to assess the distribution

of the metric values per jurisdiction. This report also provides information on the availability of

policy tools for collective investment vehicles with features making them susceptible to runs,

economic function (EF) 1 entities, and includes a case study on private finance and NBFI, with

a box providing an overview of private finance in key selected jurisdictions.

To maximise both the scope and granularity of available data, the monitoring results are

presented for two different samples of jurisdictions, which differ in terms of the treatment

1

The monitoring exercise is conducted by the FSB’s Non-bank Monitoring Experts Group, which was established in 2016 under

the Standing Committee on Assessment of Vulnerabilities (SCAV). The Experts Group includes experts from 29 participating

jurisdictions (see Table 0-2), as well as the Bank for International Settlements, European Commission, European Securities and

Markets Authority, European Systemic Risk Board, International Association of Insurance Supervisors, International Monetary

Fund, International Organization of Securities Commissions and the Organisation for Economic Co-operation and Development.

2

The FSB’s NBFI monitoring exercise uses sectoral balance sheet statistics, as these are widely available and provide generally

consistent financial sector data for mapping the global size and trends of NBFI. Some jurisdictions that currently lack sectoral

balance sheet statistics have used other data sources that may not be fully consistent with the data from other participating

jurisdictions.

3

The two-step approach in this report is based on the monitoring framework to assess bank-like financial stability risks from NBFI

as set out in FSB (2011), Shadow Banking: Strengthening Oversight and Regulation, October.

4

The focus on economic functions is based on an approach that was introduced in FSB (2013), Policy Framework for

Strengthening Oversight and Regulation of Shadow Banking Entities, August (the “FSB Policy Framework”).

5

of euro area (EA) jurisdictions (Table 0-2). The first sample, denoted as 29-Group, comprises

29 individual jurisdictions and includes more granular information for non-bank financial sectors.

The second sample, denoted as 21+EA-Group, is a more comprehensive sample in terms of

jurisdictional

coverage because it not only comprises 21 individual non-euro area jurisdictions,

but also includes the 19-member euro area as a whole, as opposed to only eight individual euro

area jurisdictions in the 29-Group sample.

5

The 21+EA-Group sample is used in parts of Section

1, where it provides wider jurisdictional coverage, though it is not as comprehensive in its

coverage of financial sectors. The 29-Group is used in Section 2 because of better coverage of

NBFI sub-sectors.

6

Table 0-2: Data sample composition

Belgium (BE)* Argentina (AR)** Hong Kong (HK)*

Saudi Arabia (SA)** Euro area (EA)*

France (FR)* Australia (AU)* India (IN)** Singapore (SG)*

Germany (DE)* Brazil (BR)** Indonesia (ID)** South Africa (ZA)**

Ireland (IE)* Canada (CA)* Japan (JP)* Switzerland (CH)*

Italy (IT)* Cayman Islands (KY)* Korea (KR)* Türkiye (TR)**

Luxembourg (LU)* Chile (CL)** Mexico (MX)** United Kingdom (UK)*

Netherlands (NL)* China (CN)** Russia (RU)**

1

United States (US)*

Spain (ES)*

= 29-Group = 21+EA-Group *= Advanced economy **= Emerging market economy (EME)

1

This report does not include data for Russia for 2021 and 2022, though data for previous years (based on the 2021

submission) are included in the analysis where appropriate. Where growth rates are calculated in this report, or comparison

with previous years is made, Russian data are not included in order to keep a consistent data sample. Graph footnotes in the

report specify if and how data on Russia were used.

Measures of growth and results throughout this report are mainly based on either annual

historical data covering end-2002 to end-2022 or cross-sectional data as of end-2022.

Some exchange rate effects have been corrected when presenting growth rates by applying a

constant end-2022 exchange rate across all past years to convert each jurisdiction’s local

currency data into U.S. dollars. Growth rates have not been otherwise adjusted (e.g. for the

appreciation or depreciation of asset prices). The results in this report are not strictly comparable

to those presented in previous reports because of jurisdictions’ revisions to historical data,

improvements in national statistics and more granular reporting. When material, these revisions

are noted in footnotes throughout this report.

5

The European Central Bank (ECB) provided the euro area aggregated data. The euro area data in this report covers the following

19 jurisdictions: Austria, Belgium, Cyprus, Estonia, Finland, France, Germany, Greece, Ireland, Italy, Latvia, Lithuania,

Luxembourg, Malta, the Netherlands, Portugal, Slovakia, Slovenia, and Spain.

6

Throughout the report, 29-Group and 21+EA-Group refer to the sample of jurisdictions used for analysis, although for some

analyses, data corresponding to a subset of jurisdictions are available.

6

1. Financial intermediation in the global financial system

Section 1.1 provides an overview of the growth and size of the global financial system, with

comparisons to the NBFI sector, which includes insurance corporations, pension funds, OFIs

and financial auxiliaries. Section 1.2 focuses on trends and the main drivers of growth in the

NBFI sector. Credit intermediation and wholesale funding trends of OFIs are analysed in Section

1.3. Section 1.4 discusses the direct domestic balance sheet interconnectedness between

banks, insurance corporations, pension funds and OFIs, as well as cross-border linkages.

1.1. Developments in 2022

1.1.1. Macro developments

The value of total global financial assets declined for the first time recorded in this

monitoring exercise against the backdrop of higher interest rates in response to

inflationary pressures (Graph 1-1, RHS). Since early 2022, heightened geopolitical and

economic uncertainty, as well as the rising interest rate environment in response to high

inflationary pressures, contributed to tighter financial conditions in most jurisdictions. The

combination of these factors contributed to lower asset prices, while market liquidity deteriorated

across key asset classes. Amid lower asset valuations, total global financial assets decreased

0.4% in 2022, following years of continued and rapid growth. Central bank balance sheets

decreased, amid lower asset valuations and quantitative tightening. Total financial assets of the

NBFI sector decreased 5.5% compared to 2021, mainly reflecting valuation losses in mark-to-

market asset portfolios. On the other hand, financial assets held by banks increased 6.9%,

supported by the fact that their asset portfolios, largely composed of loans, traditionally have a

lower sensitivity to interest rate changes. Consequently, the relative share of total global financial

assets held by the NBFI sector decreased to 47.2%.

7

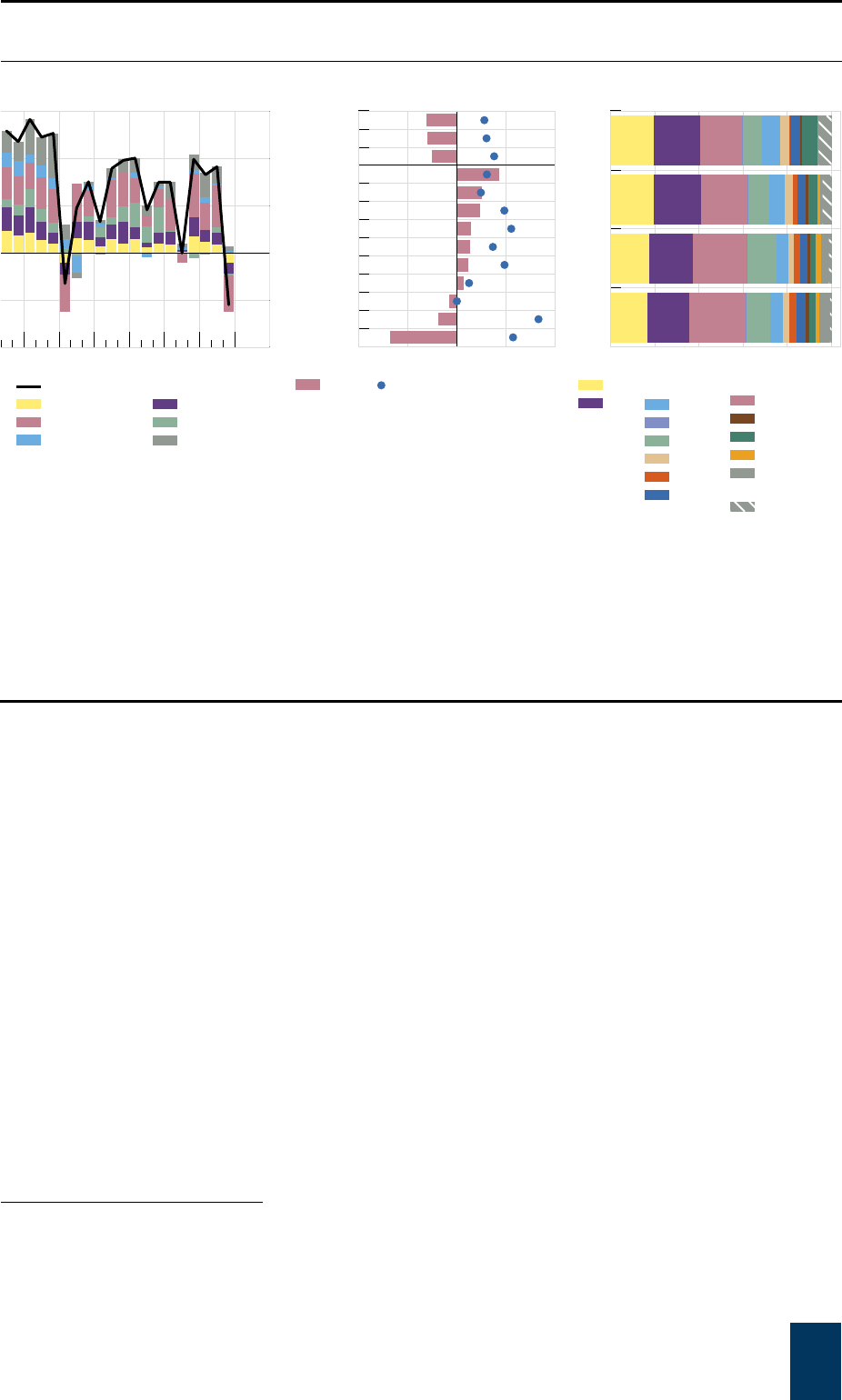

NBFI as a share of total global financial assets decreased in 2022

21+EA-Group Graph 1-1

Total global financial assets

1

Composition of the global financial system

4

Share of total financial assets USD trillion

Total

global

financial

assets

Central

banks

Banks

3

PFIs

5

NBFI

sector

Size at end-2022

(USD trillion)

461.2 39.0 183.2 21.0 217.9

Share of total

global financial

assets (%)

100.0 8.5 39.7 4.6 47.2

Growth in 2022

(year-over-year, %)

-0.4 -6.0 6.9 8.0 -5.5

Growth 2017–21

(annualised growth,

%)

6.5 11.0 5.3 4.6 6.9

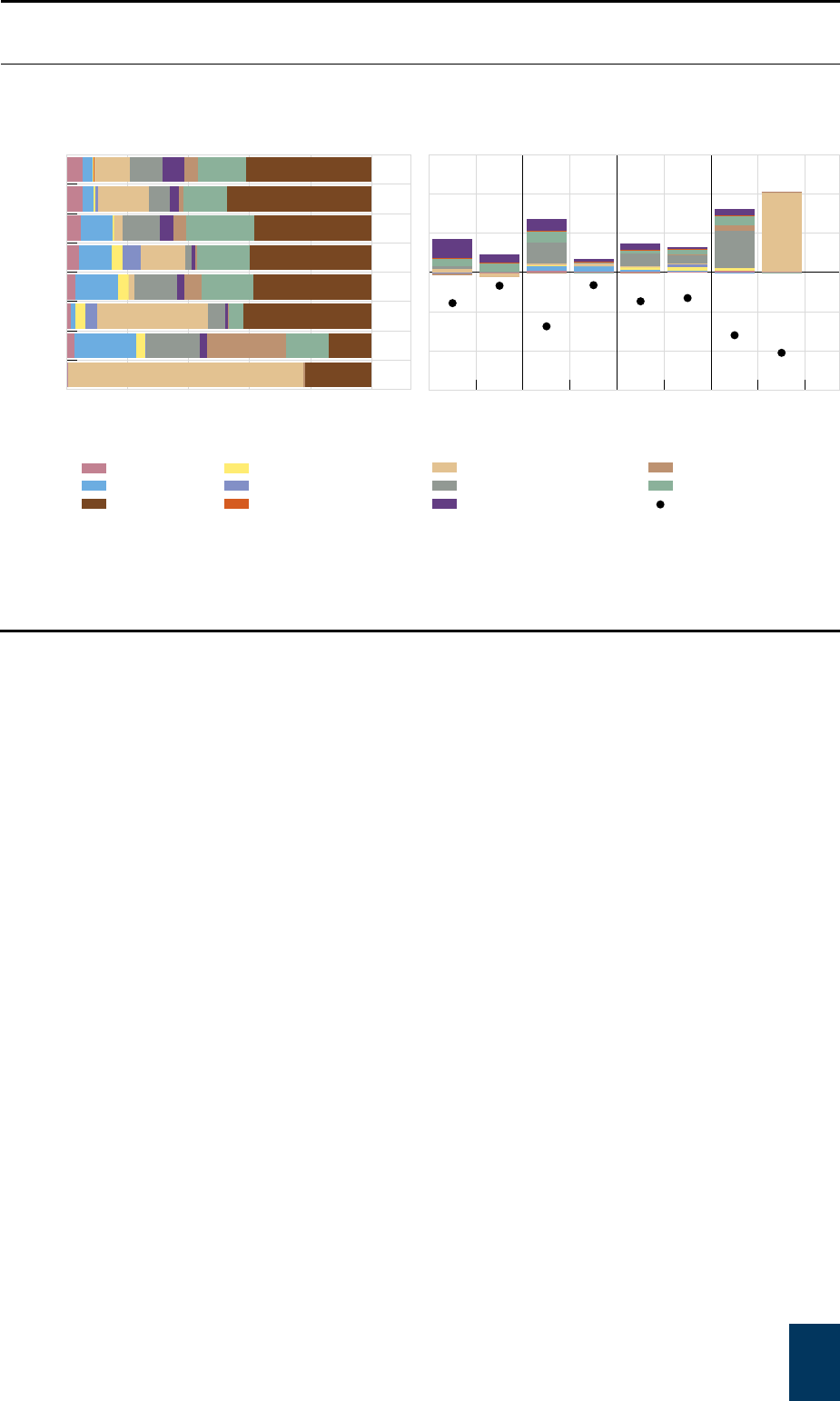

With the NBFI sector’s share of total global financial assets decreasing in many

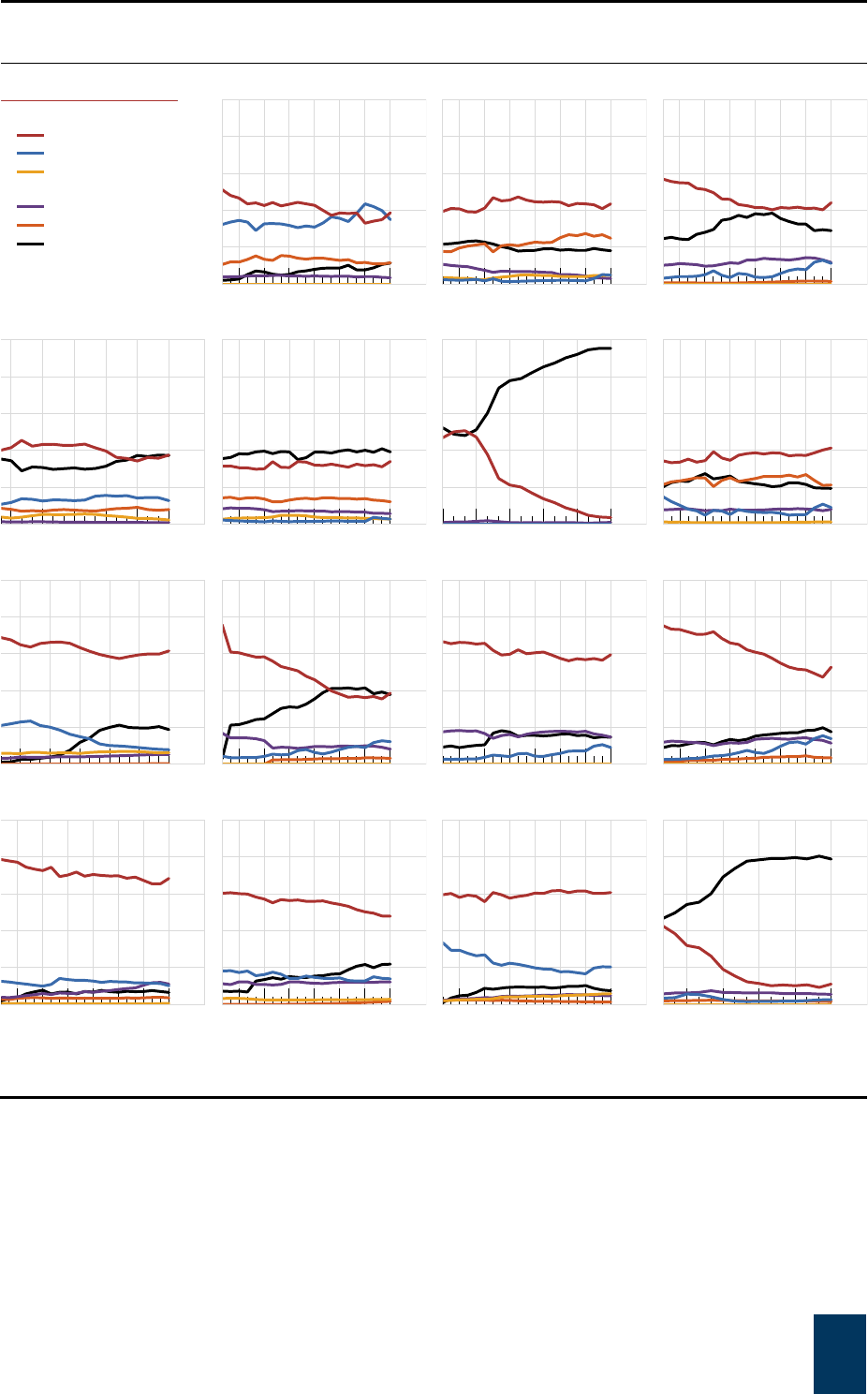

jurisdictions, banks continued to be the largest financial entity type (Graph 1-2). This was

particularly the case in emerging market economies, where banks represented 57.9% of total

financial assets, while they represented 34.5% in advanced economies. The OFI sector was the

largest sector in the Cayman Islands, Luxembourg, Ireland, the Netherlands, Canada, and the

United States. While pension funds’ size varied across jurisdictions, they constituted at least

10% of total financial assets in Australia, Chile, the United States, Mexico, the Netherlands,

South Africa, Switzerland, Canada, and Argentina.

50

48

46

44

42

400

300

200

100

0

22201816141210080604

NBFI

sector

2

Lhs: NBFI sector

Banks

3

Rhs: Central banks

institutions

Public financial

1

Includes data for Russia up until 2020.

2

NBFI includes ICs, PFs, OFIs and financial auxiliaries.

3

All deposit-taking

corporations.

4

Does not include data for Russia.

5

Public financial institutions.

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data) and 2021 submission for Russia; FSB calculations.

8

The structure of the financial system differed across jurisdictions, with

banks comprising the single largest entity type in most jurisdictions

29-Group at end-2022 Graph 1-2

Percenta

g

e of total domestic financial assets Percenta

g

e of GDP

1

Data for Russia as of 2020.

2

Russia not included in aggregates.

3

All deposit-taking corporations.

4

Jurisdictions with OFI assets

greater (lower) than their GDP will be above (below) the horizontal dashed line. The ratio of OFI assets to GDP for the Cayman Islands

(264,800), Luxembourg (19,349), Ireland (1,239) and the Netherlands (598) are not shown since they are particularly high compared to the

rest of the jurisdictions.

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data) and 2021 submission for Russia; FSB calculations.

1.1.2. NBFI sector developments

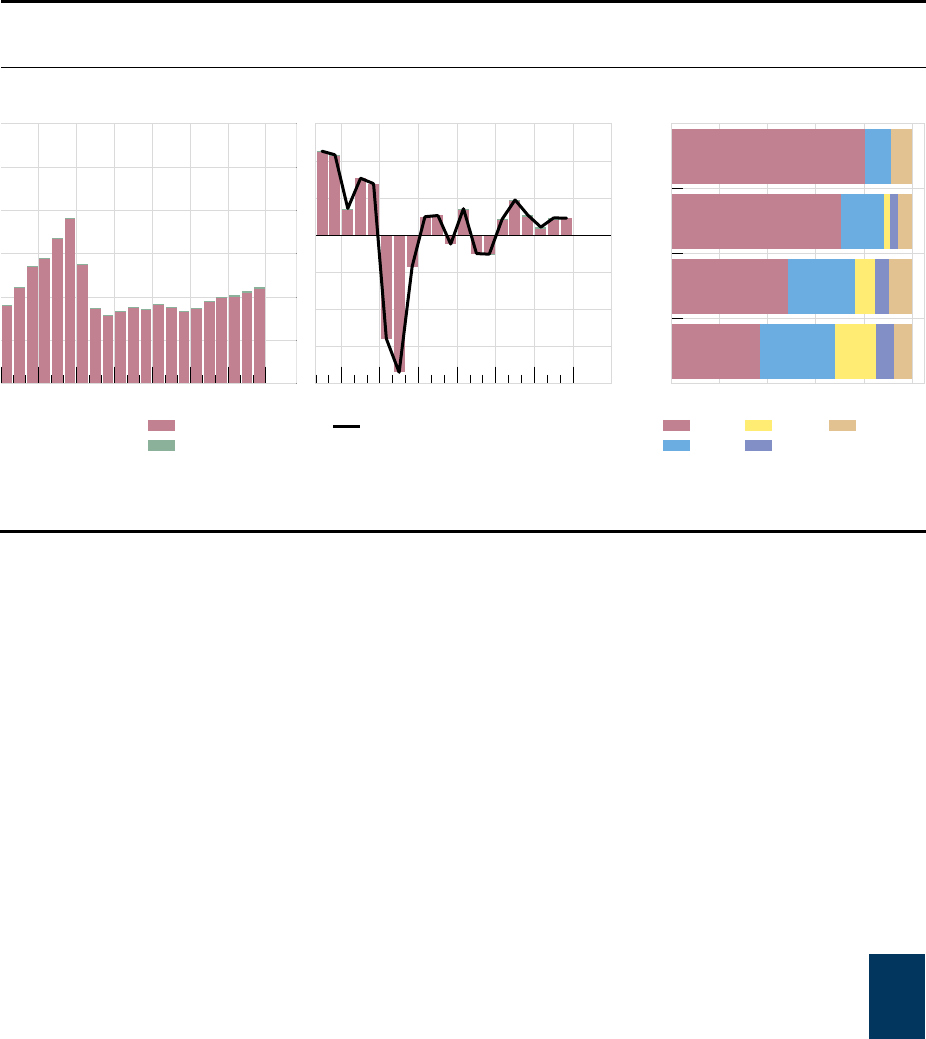

Since 2017 investment funds have driven changes in NBFI asset levels, and this

continued to be the case in 2022, as investment funds led the decline in NBFI assets.

Box 1-1 shows changes in the net asset value of investment funds and highlights that valuation

effects explain most of the decrease in funds' assets. More broadly, as discussed in Section 1.1,

there was a negative contribution to asset levels from sectors with large mark-to-market

portfolios (Graph 1-3). The decrease in the assets of OIFs accounted for approximately two-

thirds of the overall decline in NBFI sector assets in 2022, while insurance corporations and

pension funds collectively accounted for almost all of the rest of the decline (Graph 1-5, LHS).

This reflects the large investment portfolios that these entities have, which are sensitive to

valuation effects.

80

60

40

20

0

400

300

200

100

0

HK SG DE JP BE AU CA US LU TR CN RU

1

CL BR ZA AEs

FR ES UK KR IT CH NL IE KY SA ID IN AR MX All

2

EMEs

2

Advanced economies Emerging market economies Total

Banks

3

Central banks

Public financial institutions

Lhs:

Insurance corporations

Pension funds

Financial auxiliaries

OFIs

OFI as percentage of GDP

4

Rhs:

9

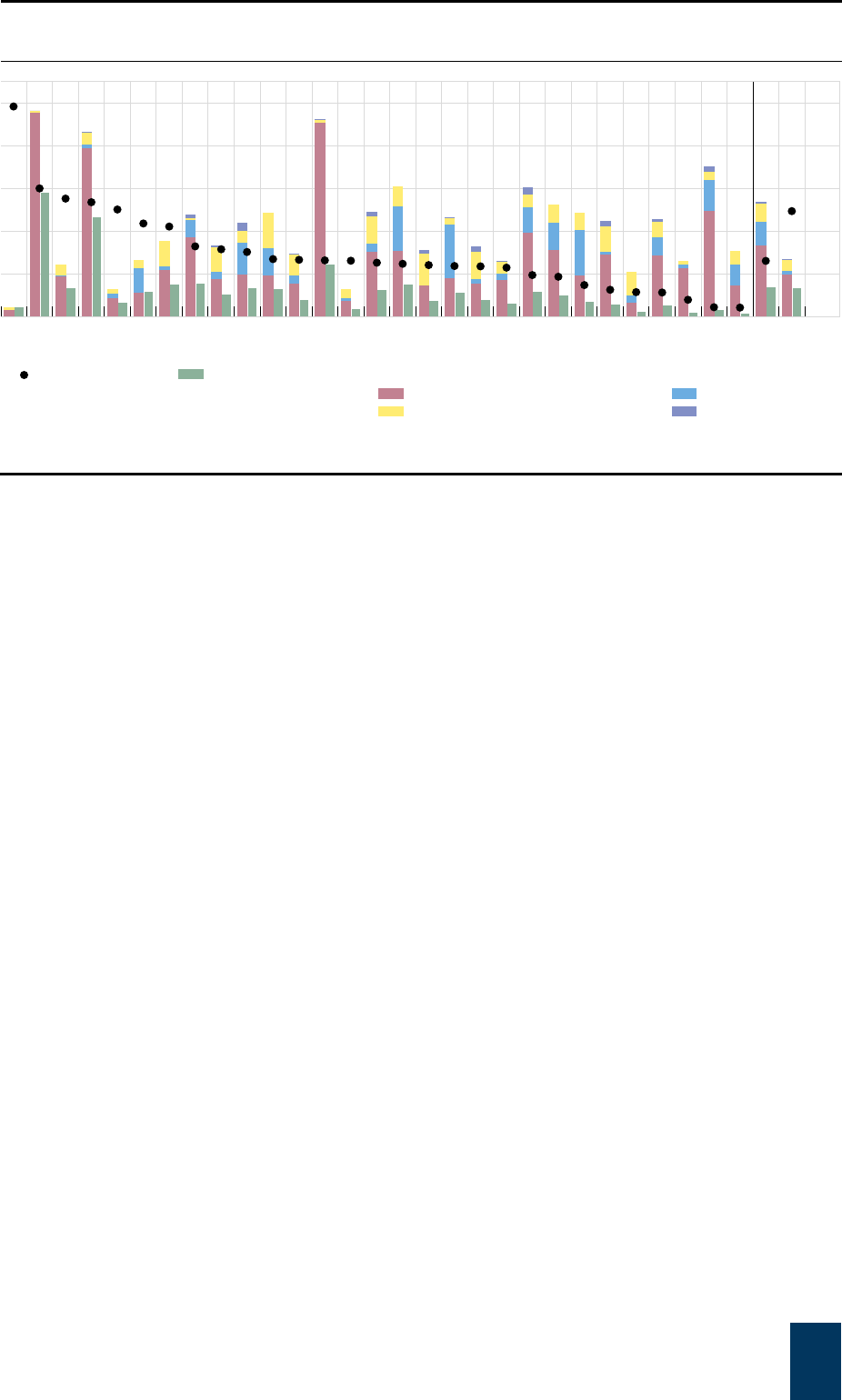

Size vs. growth in 2022 of major NBFI subsectors

Graph 1-3

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

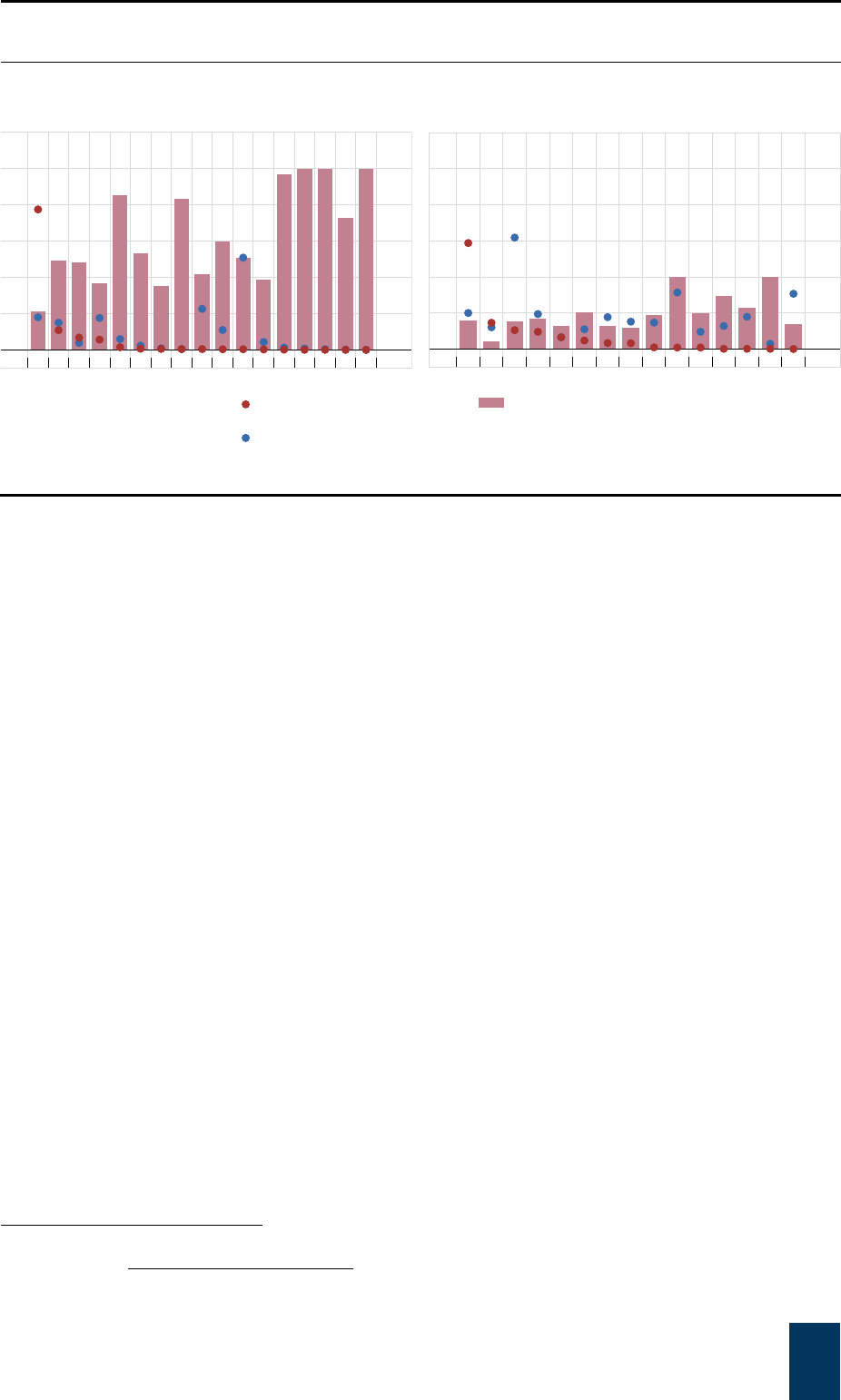

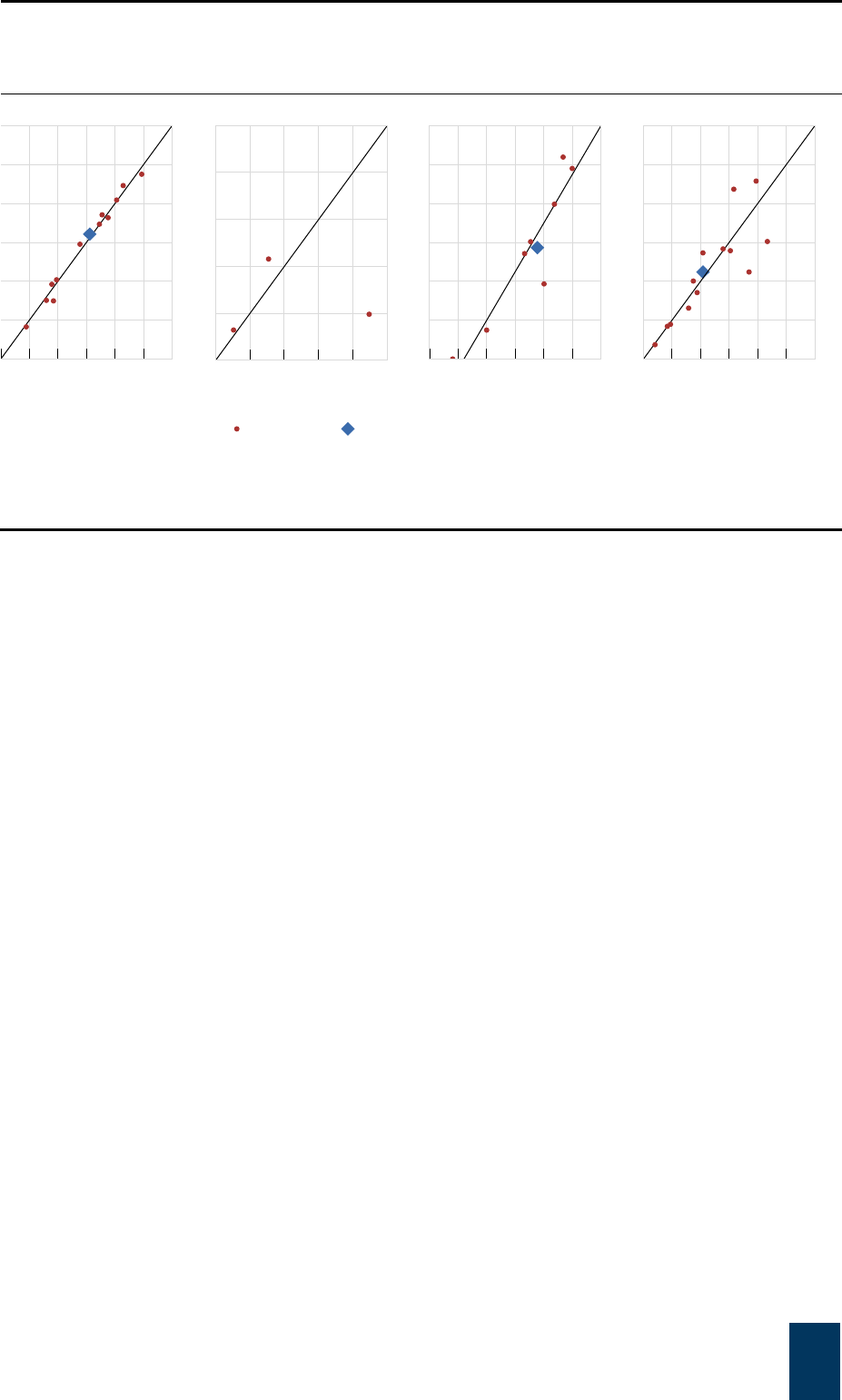

Box 1-1: Flow against valuation effects in investment funds

In 2022, central banks rapidly raised their policy rates from historically low levels, leading to

significant valuation losses in most regions for both fixed income and equity markets. Eighteen

jurisdictions reported data on the split between valuation and flows, though not for all fund types. Data

from these jurisdictions for these fund types represented 84% of total reported assets of equity funds,

89% of fixed income funds, 72% of mixed funds and 82% of MMFs (Graph B1, LHS and middle panel).

7

AUM declined in 2022 for most types of investment fund

In USD trillion Graph B1

Other investment fund asset

composition

1

MMF assets by type

1

Change in funds’ total assets split

between flows and valuation effects

3

7

Out of the 20 jurisdictions that reported quarterly AUM as part of the annual monitoring exercise, 18 were able to supply the

quarterly information about investor flows to separately identify flow and valuation effects.

ICs

PFs

MMFs

OIFs

HFs

REITs

FCs

BDs

SFVs

TCs

CFIMLs

CCPs

5

0

–5

–10

–15

–20

30252015105

Share of total NBFI assets (%)

Growth in 2022 (%)

30

20

10

0

2221201918171615141312

Equity funds

Fixed income funds

Other funds

2

4

3

2

1

0

2221201918171615141312

Short-term government MMFs

longer maturity MMFs

Non-government/

NonGov/LTMMFs

STGovMMFs

MixFs

FIFs

EqFs

NonGov/LTMMFs

STGovMMFs

MixFs

FIFs

EqFs

43210–1–2–3–4–5

2021

2022

Net change

Flows

Valuation

Other

4

10

EqFs = equity funds; FIFs = fixed income funds; MixFs= mixed funds; MMFs = Total MMFs, STGovMMFs = Short-term government

MMFs, NonGov/LTMMFs = non-government/ longer-term maturity MMFs. Annual data (end of period) provided by 28 reporting

j

urisdictions.

1

In 2022 the breakdown of changes of total assets into flow and valuation effects of equity funds, fixed income funds and other funds,

was available for 84%, 89% and 72% of their total reported assets, respectively. For short-term government MMFs and non-government

/

longer-term maturity MMFs, the breakdown was available for 100% and 98% of their total reported assets, respectively.

2

Other funds

such as mixed funds, referenced investment funds, external debt investment funds, currency funds, asset allocation funds, etc. The

numerator includes only mixed funds.

3

Estimated based on the data reported by a sub-sample of jurisdictions.

4

“Other” represents

changes attributable to factors other than fund flows and valuation (e.g. changes in leverage and sample adjustments).

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

Lower valuations in equity, mixed, and fixed income funds led to a contraction in AUM in 2022.

Only MMFs’ AUM increased, differentiating them from other types of funds. Inflows during the last three

quarters of 2022 increased AUM of non-government and longer-term MMFs (Graph B1, RHS), while

outflows from short-term government MMFs slightly reduced their AUM. These outflows were then

reversed in Q4 2022 and turned into large inflows in early 2023, following the banking sector turmoil in

March of that year. Graph A6-1 provides times series for changes in AUM decomposed between

valuation and flows per entity type.

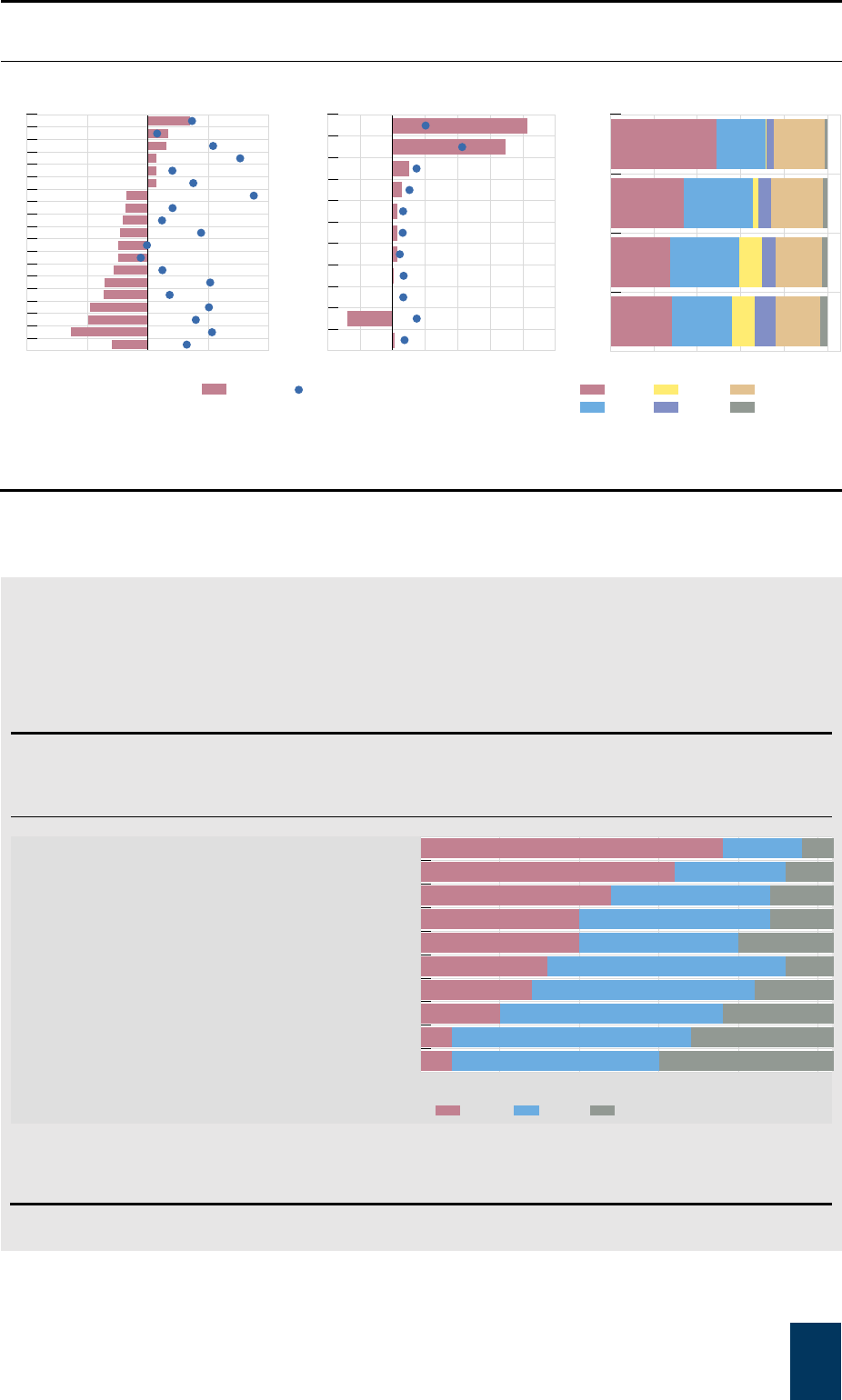

OIFs decreased in 23 jurisdictions (Graph 1-4, LHS and middle panel). Given the large size

of their respective OIF sectors, the United States and the euro area accounted for the largest

part of the decrease. The United States experienced a decrease in OIFs of 19.0% which was

primarily driven by equity funds, which fell $4.2 trillion – or 20.2% – accounting for 74.1% of the

year-on-year contraction in OIFs. Fixed income funds in the United States also decreased

significantly, by 16.1% to $5.9 trillion. The decline in aggregate euro area OIF assets in 2022

equalled 12.4% and was evenly spread across major regional fund domiciles (Luxembourg -

13.3%, Ireland -12.2% and Germany -13.4%). Whilst not significantly contributing to the euro

area’s decrease in OIF assets given the relatively small size of its fund sector, the Netherlands

experienced the largest percentage decline of any jurisdiction globally,

8

with OIFs’ assets

declining 30.1% in 2022.

9

8

In many cases, such as here for OIFs, year-on-year changes in Argentina and Türkiye are the largest; however, this is because

of their inflation rates and, therefore, this report does not comment specifically on those jurisdictions.

9

This decline was largely attributed to pension funds withdrawing from affiliated equity and fixed income funds, in order to invest

directly themselves.

11

OIFs’ size and growth by jurisdiction

1

In per cent Graph 1-4

A

nnual growth of OIFs in AEs and EMEs

2

Composition of the OIFs sector

3

1

Does not include data for Russia.

2

Growth rates in Argentina and Türkiye reflected high rates of inflation.

3

OIF assets by jurisdiction,

21+EA-Group.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

The composition of the NBFI sector remained broadly unchanged in 2022 compared with

2017, though the share of some sectors declined (Graph 1-5, RHS). Assets held by

insurance corporations contracted 6.2% in 2022, while for pension funds and OFIs they

contracted 6.1% and 5.0%, respectively (Graph 1-5, middle panel). For insurance corporations,

17 jurisdictions reported declines and total assets were $35.6 trillion at end-2022. For pension

funds, 16 jurisdictions reported declines, with total assets falling to $40.9 trillion at end 2022.

AEs

NL

US

SG

HK

BE

DE

LU

UK

CA

IE

IT

CH

ES

AU

KY

FR

KR

JP

100–10–20–30–40

2022

EMEs

SA

ID

CL

CN

ZA

MX

BR

IN

TR

AR

6040200–20–40

Compound annual growth 2016-21

2022

2017

2012

2007

100806040200

US

EA

CN

KY

Other AEs

EMEs ex CN

12

OIFs

1

were the largest contributor to the decline of NBFI assets in 2022

2

In per cent, 29-Group Graph 1-5

Contribution to NBFI sector growth

A

nnual growth, selected NBFI

subsectors

Composition of the NBFI sector

Within OFIs, declines were observed in OIFs, CCPs and captive financial institutions, and

money lenders (Graph 1-5, middle panel). These decreases outweighed the increases seen

in finance companies, broker dealers, REITs, structured finance vehicles, MMFs, hedge funds,

and trust companies. In terms of jurisdictions, Saudi Arabia experienced the largest decline in

OFIs’ assets, of 34.8% (Graph 1-6, middle panel) because of valuation effects on investment

funds; the United States, Hong Kong, and Germany experienced declines of 12.6% for the

former, and close to 10% for the latter two jurisdictions (Graph 1-6, LHS).

10

In contrast, India and

Brazil experienced increases in OFI assets of 12.3% and 7.2%, respectively (Graph 1-6, LHS

and middle panel).

11

Taken together, the composition of the OFI sector across jurisdictions in

2022 was only slightly changed from 2017, the most notable differences being the increase in

the Cayman Islands’ proportion of OFI assets and the decrease in the euro area’s share (Graph

1-6, RHS).

10

These declines were driven by the OIF sector; see above.

11

In Brazil, the increase was mainly driven by fixed income funds.

10

5

0

–5

–10

22191613100704

NBFI growth

ICs

OIFs

1

BDs

PFs

CFIMLs

Others

3

OIFs

CCPs

CFIMLs

TCs

HFs

SFVs

MMFs

REITs

BDs

FinCos

OFIs

PFs

ICs

100–10–20

2022

growth 2016-21

Compound annual

2022

2017

2012

2007

806040200

ICs

PFs

BDs

CCPs

CFIMLs

FinCos

HFs

MMFs

OFIs:

OIFs

REITs

SFVs

TCs

Others

identified

4

unidentified

Others

BDs = broker-dealers; CCPs = central counterparties; CFIMLs = captive financial institutions and money lenders; FinCos = finance

companies; HFs = hedge funds; MMFs = money market funds; OIFs = investment funds other than MMFs and hedge funds; REITs = real

estate investment trusts and real estate funds; SFVs = structured finance vehicles; TCs = trust companies, PFs = pension funds.

1

Investment funds other than hedge funds, real estate investments trusts and real estate funds (REITs), and MMFs. Other investment funds

include equity funds, fixed income funds and other funds such as mixed funds, referenced investment funds, external debt investment funds,

currency funds, asset allocation funds, etc.

2

Does not include data for Russia.

3

Others include MMFs, HFs, SFVs, TCs, REITs, and

CCPs.

4

Others identified comprise a variety of jurisdiction-specific entities that do not fit any of the explicit categories included in the

monitoring exercise.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations

13

OFIs’ size and growth by jurisdiction

1

In per cent Graph 1-6

A

nnual growth of OFIs in AEs and EMEs

2

Composition of the OFI sector

3

1

Does not include data for Russia.

2

Growth rates in Argentina and Türkiye reflected high rates of inflation.

3

OFI assets by jurisdiction,

21+EA-Group.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

Annex 3 provides an overview of the main developments in major NBFI sub-sectors, and

Box 1-2 includes an overview of the financial innovations in the NBFI sector.

Box 1-2: Financial innovations in NBFI

Participating jurisdictions responded to a survey in which they were asked to report whether

certain financial innovations, as well as innovative services and products, were present in their

jurisdictions. A total of 24 jurisdictions responded, and Graph B2 provides an overview of their

responses.

Fintech credit and peer-to-peer lending were the most commonly reported

financial innovation

A

t end-2022, 24 jurisdictions Graph B2

Number of

j

urisdictions

Responding jurisdictions were: Argentina, Australia, Belgium, Brazil, Canada, Switzerland, Spain, France, Hong Kong, Indonesia, India,

Italy, Japan, Korea, the Cayman Islands, Luxembourg, Mexico, the Netherlands, Saudi Arabia, Singapore, Türkiye, the United Kingdom,

the United States, and South Africa.

Source: Jurisdictions’ 2023 submissions; FSB calculations.

AEs

US

HK

DE

CH

IE

LU

NL

BE

CA

ES

FR

SG

AU

IT

KY

KR

UK

JP

100–10–20

2022

EMEs

SA

CN

ZA

ID

CL

MX

BR

IN

AR

TR

1007550250–25–50

Compound annual growth 2016-21

2022

2017

2012

2007

100806040200

US

EA

CN

KY

Other AEs

EMEs ex CN

Other

Fund innovation

NBFI (other than CLOs) involvement in leveraged loan markets

Crowd-funding to raise mortgage down payments

BigTech engagement in novel forms of credit intermediation

of crypto-assets to facilitate lending on DeFi trading platforms)

O

ther NBFI exposures to crypto-assets and stablecoins (e.g. use

Lending collateralised with crypto-assets

Crypto-based ETPs

App-based challenger or neobanks

Fintech credit and P2P lending

2520151050

Yes No No answer

14

Fintech credit, including peer-to-peer lending, was the most commonly reported innovation.

While overall this activity appears small in relation to the size of credit markets, some jurisdictions noted

a growing trend. In many cases, fintech credit is provided via electronic platforms that connect lenders

to borrowers – in which case the platform takes the role of a financial auxiliary. In some cases, however,

loans are taken on the balance sheet of these platforms (even if it is for a short period of time), in which

case the platforms are akin to new types of financial intermediaries. As part of the third phase of the

G20 Data Gaps Initiative, FSB jurisdictions plan to start reporting data on fintech credit in 2024 on a

best effort basis.

12

After fintech credit, app-based challenger or neobanks

13

have been identified in many

jurisdictions as an innovation. These entities are typically fintech firms that offer applications,

software, and other technologies to streamline mobile and online banking. In many jurisdictions, these

digital firms have a banking license and are therefore subject to the same prudential requirements as

incumbent banks.

Innovations linked to crypto-assets were reported by 12 jurisdictions. These innovations cover

crypto-based exchange-traded products, collateralised lending with crypto-assets usually done by

fintech firms, and other exposures to crypto-assets, including stablecoins. While this report does not

cover financial stability risks linked to the use of crypto-assets, the FSB and the IMF have published

policy recommendations covering a wide range of risks related to crypto-asset markets and activities

and global stablecoins.

14

1.1.3. Developments in emerging market economies

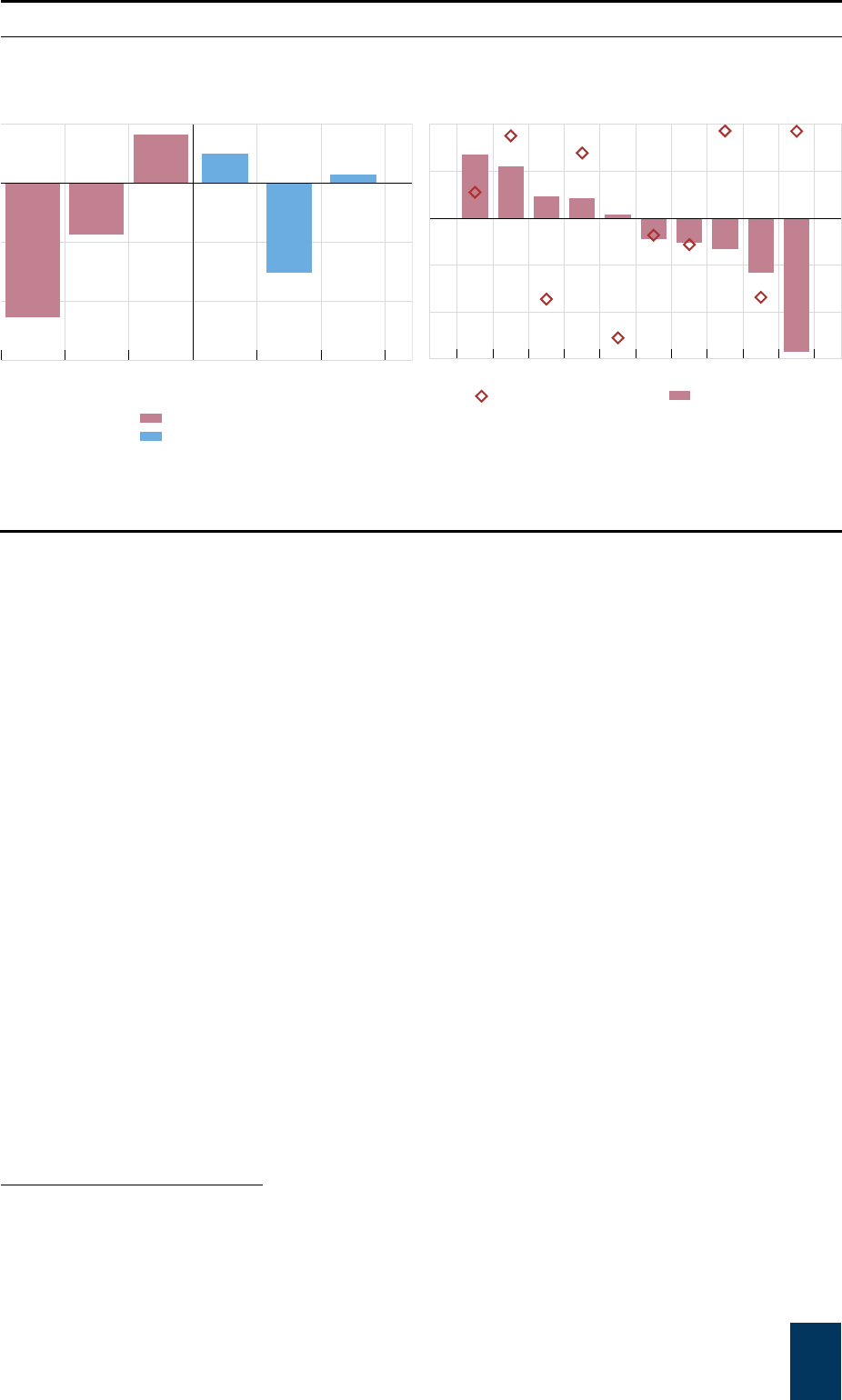

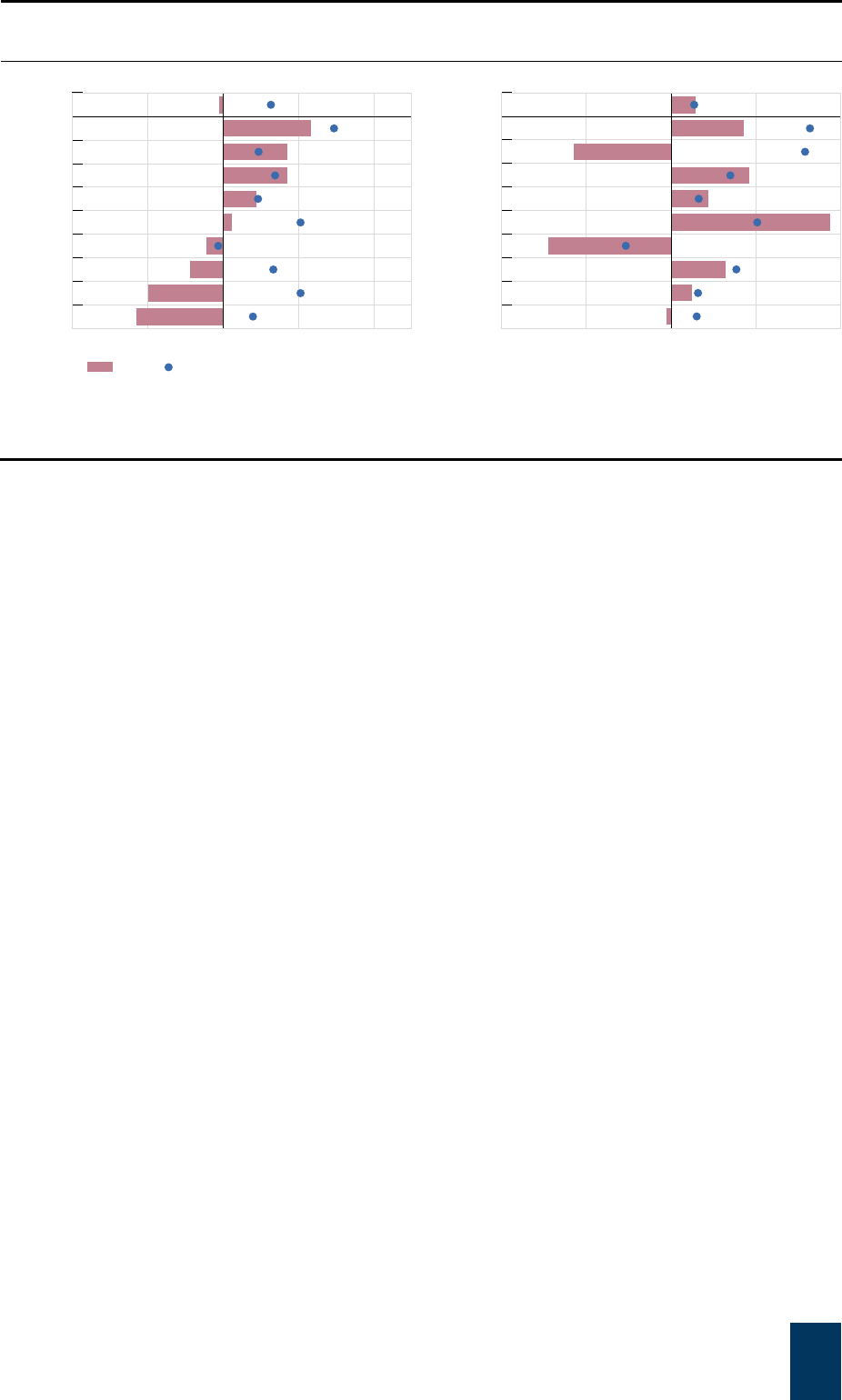

While the share of global NBFI sector assets held by emerging market economies (EMEs)

has increased over time, it remained small relative to global NBFI financial assets. The

share of global NBFI assets held by EMEs amounted to 12.0%, up from 10.9% in 2021, and this

included an 8.6% share held by China.

The relative importance of NBFI in EMEs has decreased over the last five years. As a

percentage of EME financial assets, the share of financial assets held by the NBFI sector

decreased 0.9% in EMEs between 2017 and 2022, albeit less so than in advanced economies

(AEs) (Graph 1-7, LHS). The narrow measure of NBFI as a share of financial assets has also

decreased in EMEs. However, when excluding China, these shares actually increased (Graph

1-7, LHS).

This fall in the relative importance of the NBFI sector was observed in half of EMEs. There

were large decreases between 2017 and 2022 in the share of total financial assets held by the

NBFI sector seen in Chile (-8.6pp), Indonesia (-3.5pp), South Africa (-2.0pp), China (-1.6pp),

and Argentina (-1.3pp). In most of these cases, the reduction in the relative size of the NBFI

sector was mainly due to an expansion in banks’ and central banks’ balance sheets since 2017

and the policy responses to the COVID-19 pandemic. In contrast, India (4.1pp), Brazil (3.3pp),

Türkiye (1.4pp), Mexico (1.3pp), and Saudi Arabia (0.3pp) showed an increase in the relative

importance of NBFI in the same period.

12

See Data Gaps Initiative 3 website.

13

These entities are FinTech firms that offer apps, software, and other technologies to streamline mobile and online banking.

14

See FSB (2023), IMF-FSB Synthesis Paper: Policies for Crypto-Assets, September.

15

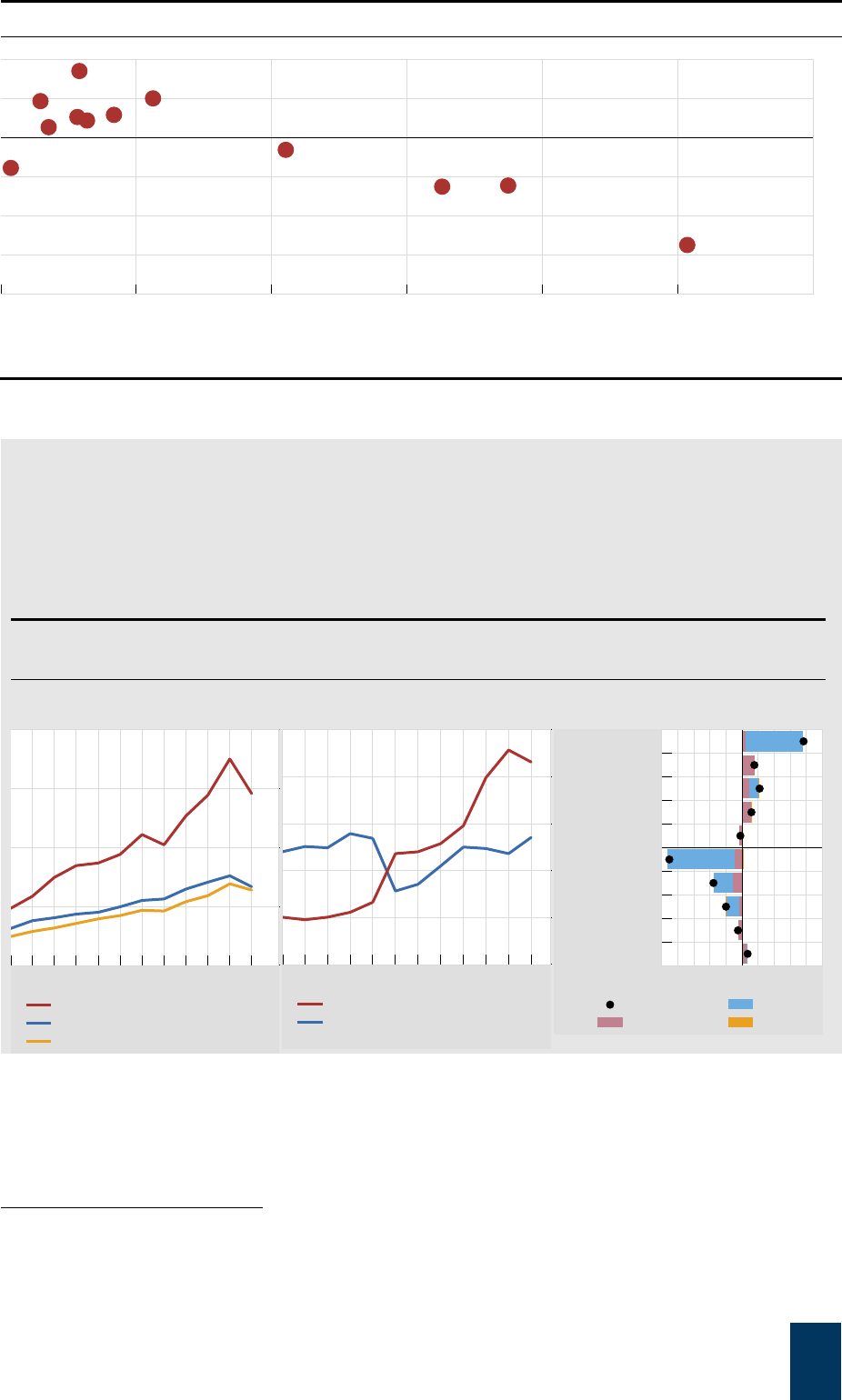

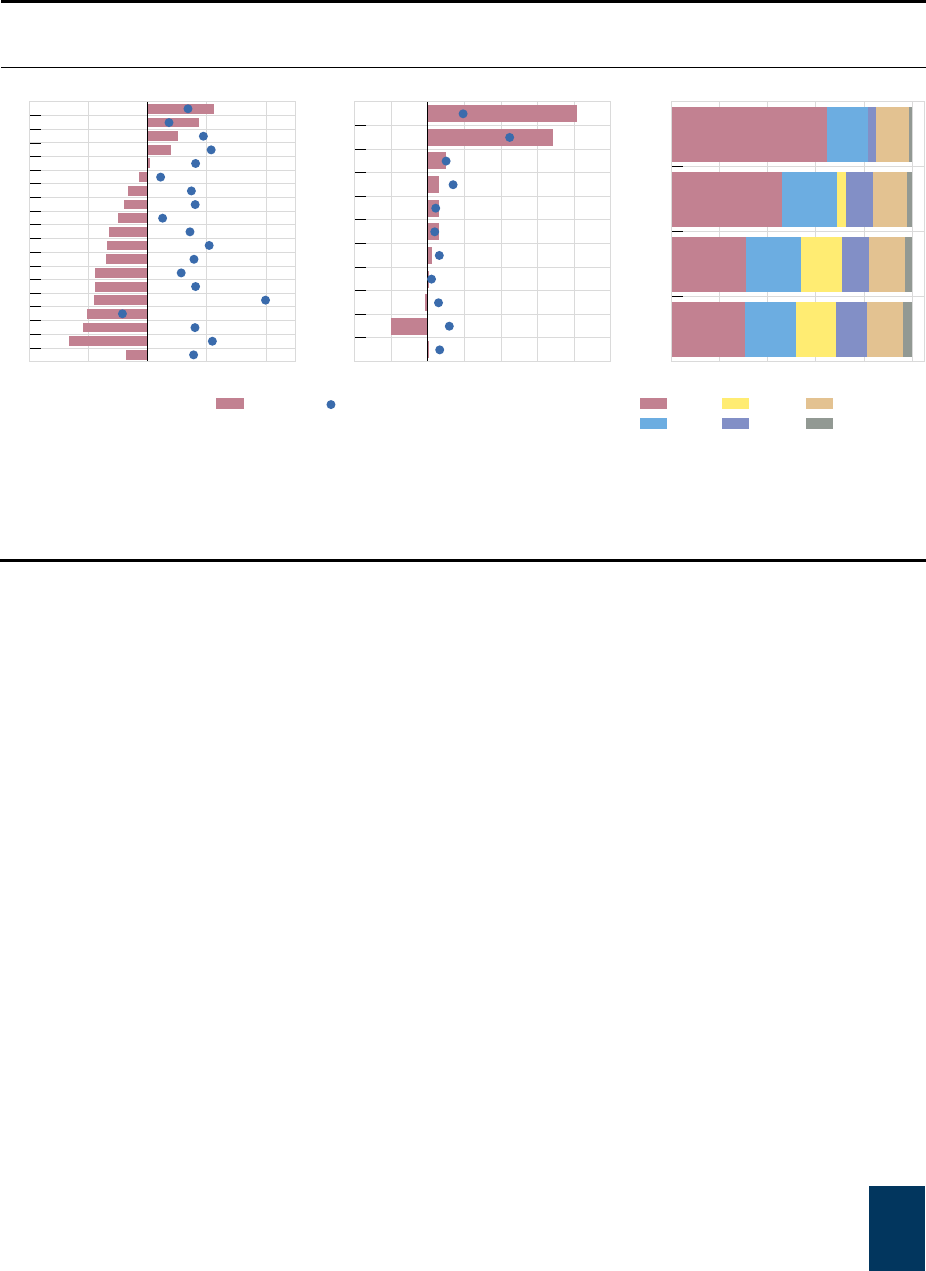

The relative importance of NBFI has decreased in EMEs

Graph 1-7

Changes in the share

1

of NBFI sector and narrow

measure as a percentage of total financial assets for

A

Es and EMEs over the last five years

Change in the share

2

of NBFI assets in each EME over

the last five years

Percenta

g

e points

Per cent Percenta

g

e points

1

Shares of the NBFI sector and narrow measure are calculated as aggregated financial assets of the NBFI sector and narrow measure o

f

each region divided by aggregated total financial assets of the region.

2

Shares of the NBFI sector for each jurisdiction are calculated as

financial assets of the NBFI sector of a jurisdiction divided by total financial assets of the jurisdiction.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

1.2. Credit assets, wholesale funding, and financial leverage

1.2.1. Credit and loan assets

The credit activities of NBFI entities are of particular importance to financial stability,

because maturity/liquidity transformation, leverage, and imperfect credit transfer can give rise to

vulnerabilities that may amplify or transmit shocks. Moreover, in jurisdictions where the NBFI

sector plays a more significant role in credit intermediation, NBFI entities that are not sufficiently

resilient to shocks could slow the flow of credit to the wider economy, especially during

downturns. Credit assets of financial intermediaries include loans,

15

debt securities,

16

and cash

on deposit, or “deposit assets”. Table 1-2 provides an overview of the credit assets in 2022 per

sector. A discussion of the deposit assets of financial intermediaries is included in Section 1.3.2.

15

These are also referred to as “loan assets,” which include overdrafts, instalment loans, hire-purchase credits, and loans to

finance trade credit.

16

Examples of debt securities include bills, bonds, and commercial paper.

0

–1

–2

–3

ex CNex CN

EMEsEMEsAEsEMEsEMEsAEs

NBFI sector

Narrow measure

Changes in share of:

40

30

20

10

0

3

0

–3

–6

–9

CLIDZACNARSAMXTRBRIN

in 2022

Share of NBFI sectorLhs:

Change since 2017Rhs:

16

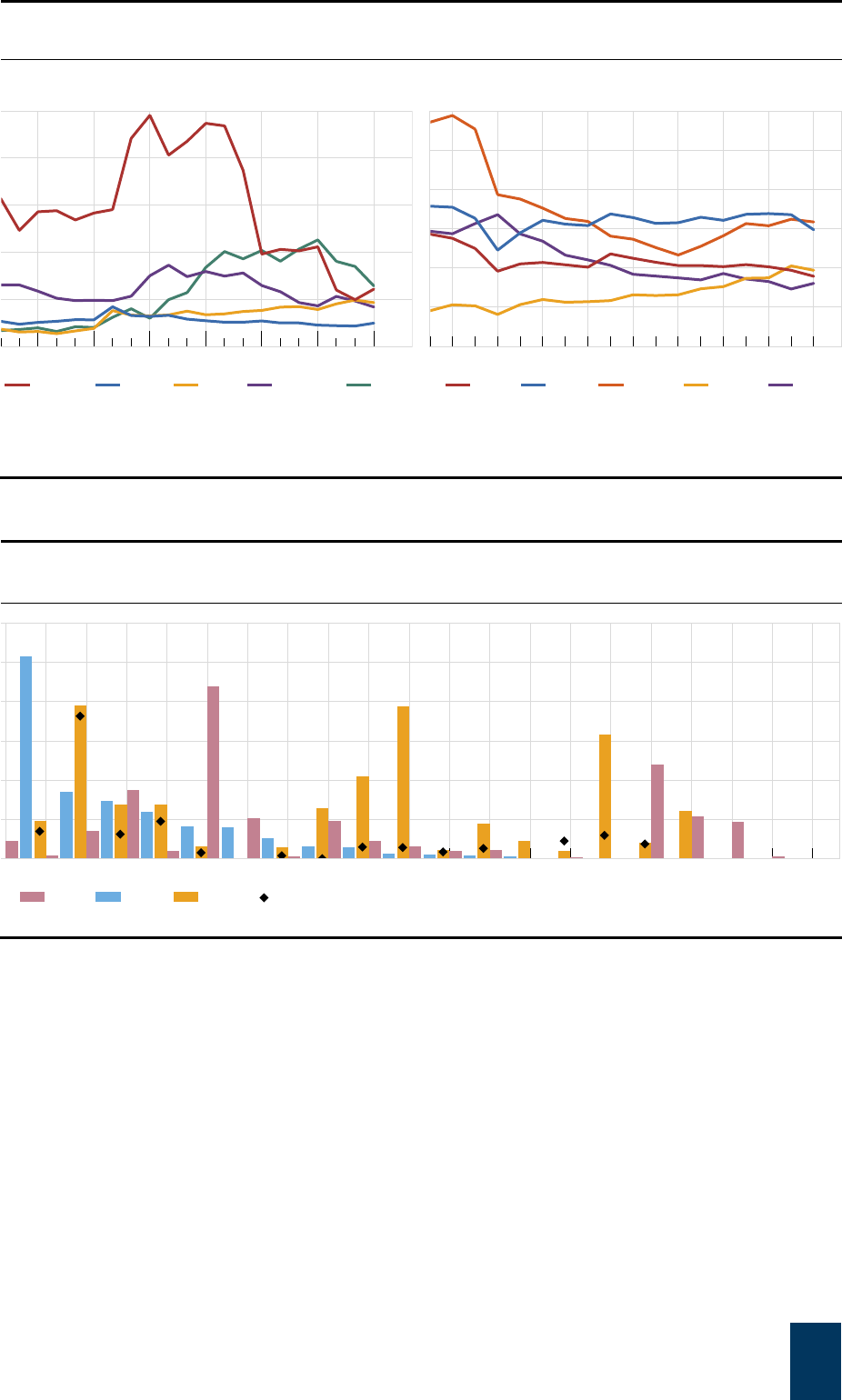

Table 1-2: Credit asset composition and growth in 2022, 21+EA-Group

Total Banks

1

ICs PFs OFIs

Credit assets

(USD trillion at end-2022)

228.8 149.9 17.3 10.1 51.5

Growth (% in 2022) 2.1 5.4 -11.5 -4.4 -0.6

Of which Loan assets

(USD trillion at end-2022)

117.5 99.5 2.4 0.3 15.4

Growth (% in 2022) 6.6 7.3 -0.6 6.4 2.8

Of which Deposit assets

(USD trillion at end-2022)

22.5 16.3 1.1 0.7 4.5

Growth (% in 2022) 0.4 -1.3 0.5 6.1 6.4

1

All deposit-taking corporations.

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

In 2022, credit assets held by banks

17

increased, while those of NBFI entities decreased

for the first time in several years. In 2022, banks’ credit assets grew 5.4% and within that loan

assets grew by 7.3%, lower than the pace observed in the previous two years. However, the

total amount of loan assets in the financial system continued to grow in 2022, largely due to the

growth in bank credit assets (Graph 1-8, LHS). Banks remained the single largest source of

loans, accounting for 84.7% of global loan assets at end-2022 (and the largest source of credit

assets overall with 65.5%). Credit assets held by insurance corporations, pension funds, and

OFIs fell from 2021 to 2022 by 11.5%, 4.4% and 0.6%, respectively (Table 1-2). These were, in

fact, the first falls in credit assets recorded for insurance corporations and pension funds.

17

The term “banks”, as used in the text, includes all deposit-taking corporations.

17

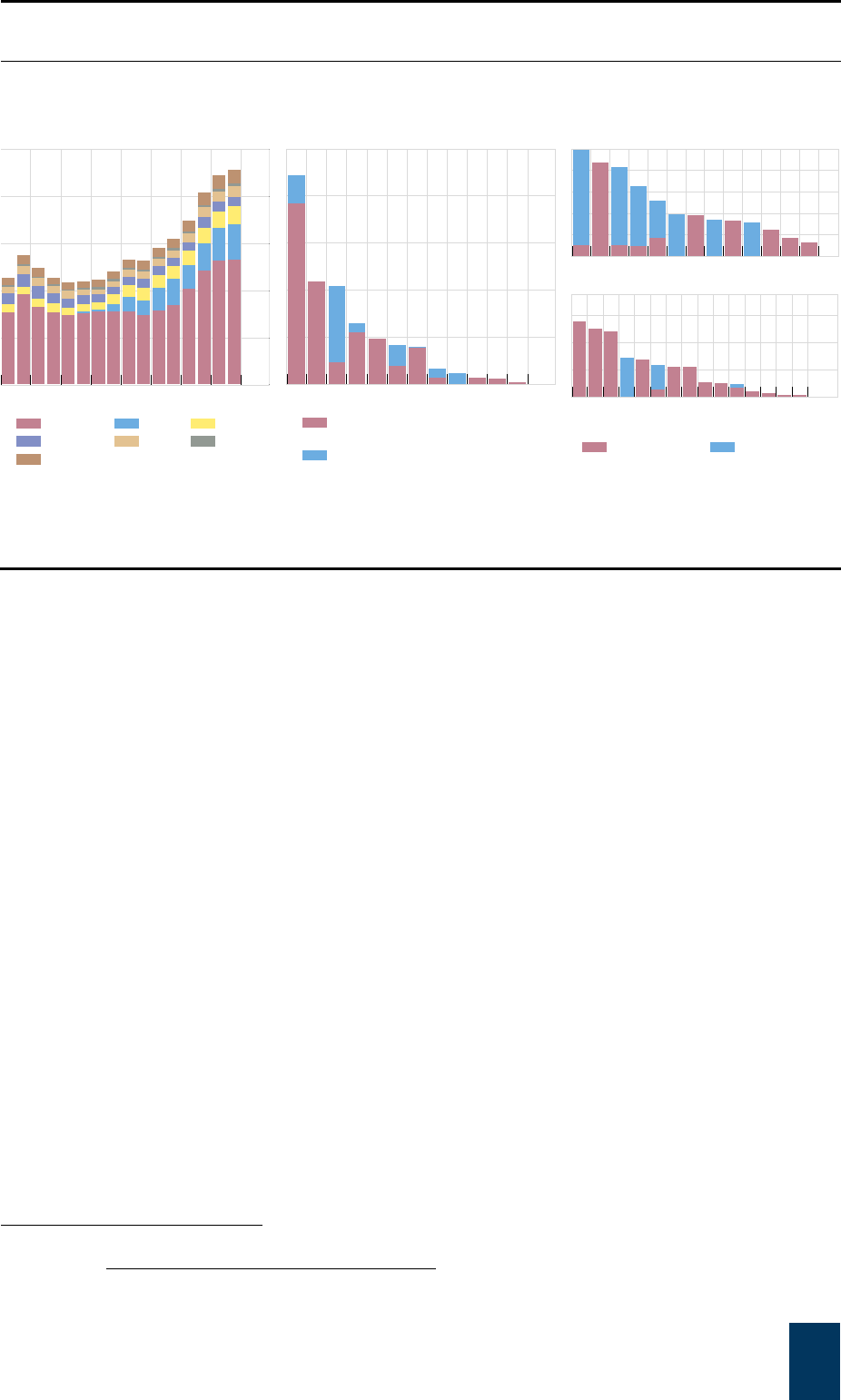

OFIs’ share of credit assets stalled in 2022

1

In USD trillions, 21+EA-Group Graph 1-8

Composition and evolution of credit assets since 2008

1

Credit assets held by selected OFIs

Among OFIs, credit assets of insurance corporations and other investment funds

decreased by the largest amount from 2021 (-11.5% and -9.9% respectively, Graph 1-8,

RHS and 1-9, LHS). Other investment funds continued to represent the largest share among

the OFIs (26.3%), followed by MMFs (18.8%) and broker-dealers (15.7%), (Graph 1-8, RHS).

18

The Netherlands experienced the greatest fall in OIF credit assets (-24.1%, see above), followed

by Ireland (-16.0%), Germany (-15.0%), and the United States (-14.9%). The United States

accounted for 57.4% of the OIF credit assets decline, given its size.

19

18

These shares refer to selected OFIs as shown in Graph 1-8, RHS

19

This contribution has been calculated with respect to the 29-Group sample for better data coverage.

200

150

100

50

0

22211612082221161208

of which: Loan assetsCredit assets

Banks

2

OFIs

Pension funds

Insurance corporations

32

24

16

8

0

22191613100704

Broker-dealers

Finance companies

Hedge funds

Other investment funds

Money market funds

Structured finance vehicles

Trust companies

1

Includes data for Russia up until 2020.

2

All deposit-taking corporations.

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data) and 2021 submission for Russia; FSB calculations.

18

Credit and lending assets of selected NBFI subsectors

In per cent; 21+EA-Group Graph 1-9

Growth of credit assets Growth of lending assets

OFIs = other financial intermediaries; PFs = pension funds; ICs = insurance corporations; BDs = broker-dealers; FinCos = finance companies;

HFs = hedge funds; MMFs = money market funds; OIFs = investment funds other than MMFs and hedge funds; SFVs = structured finance

vehicles; TCs = trust companies.

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

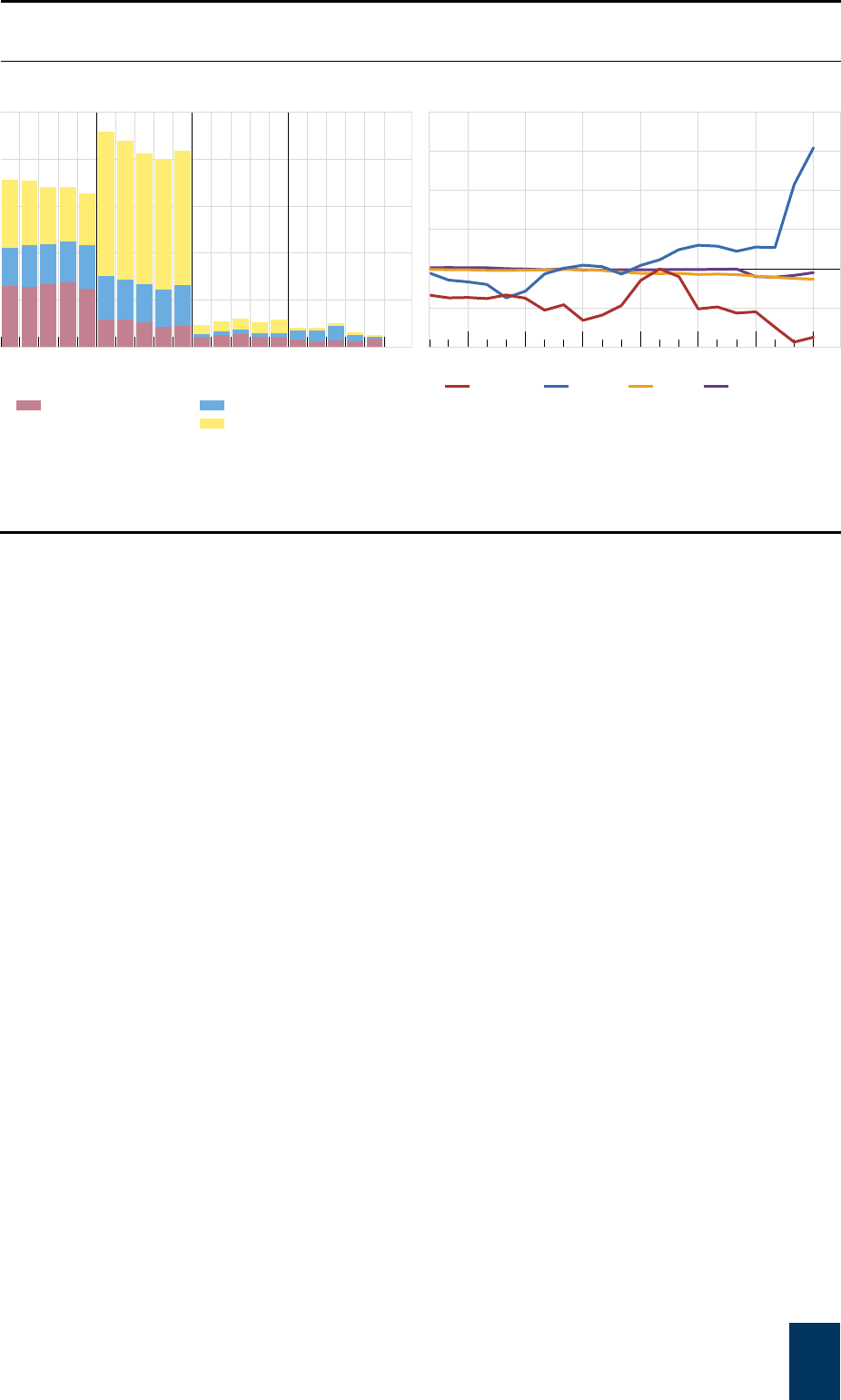

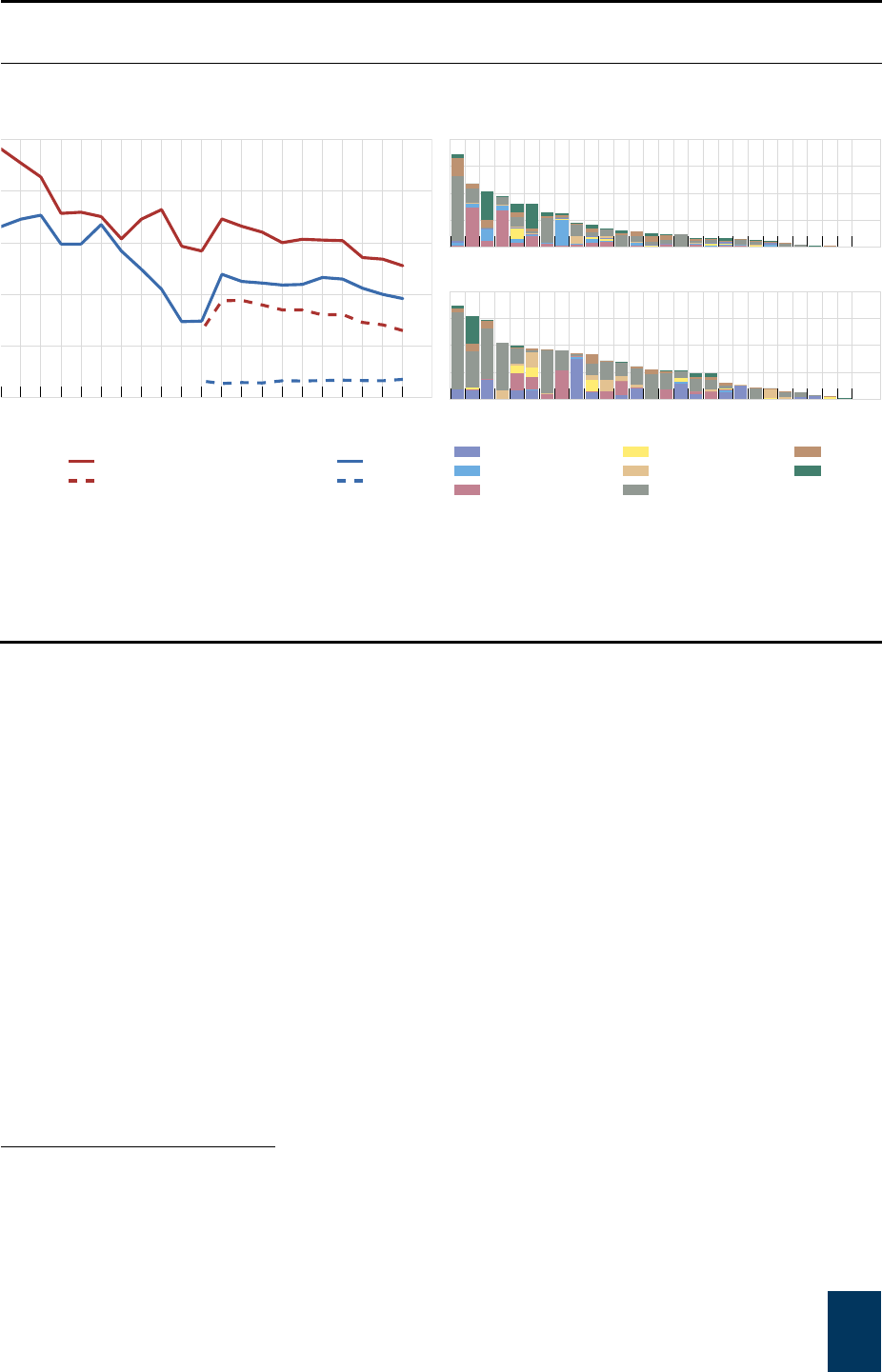

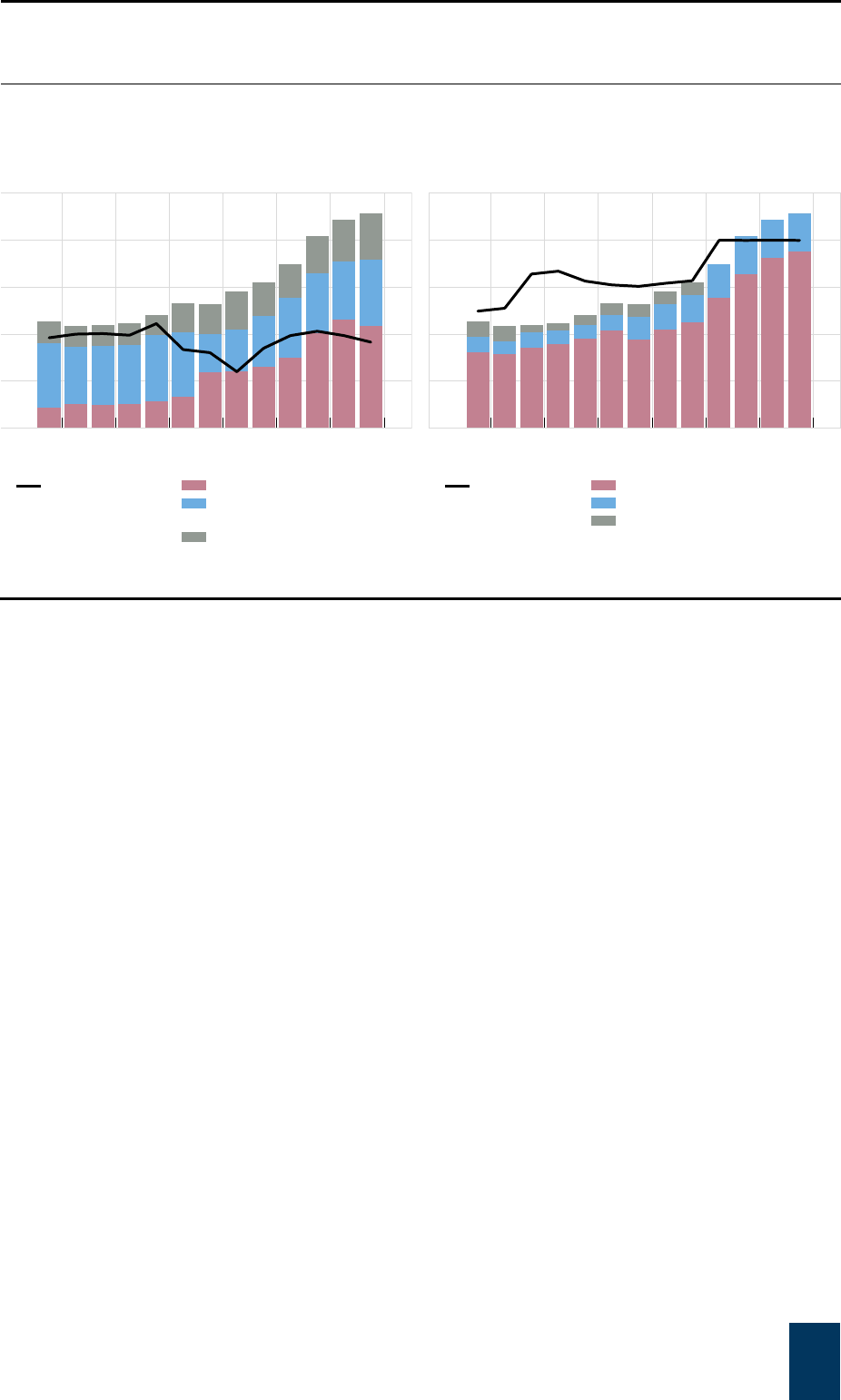

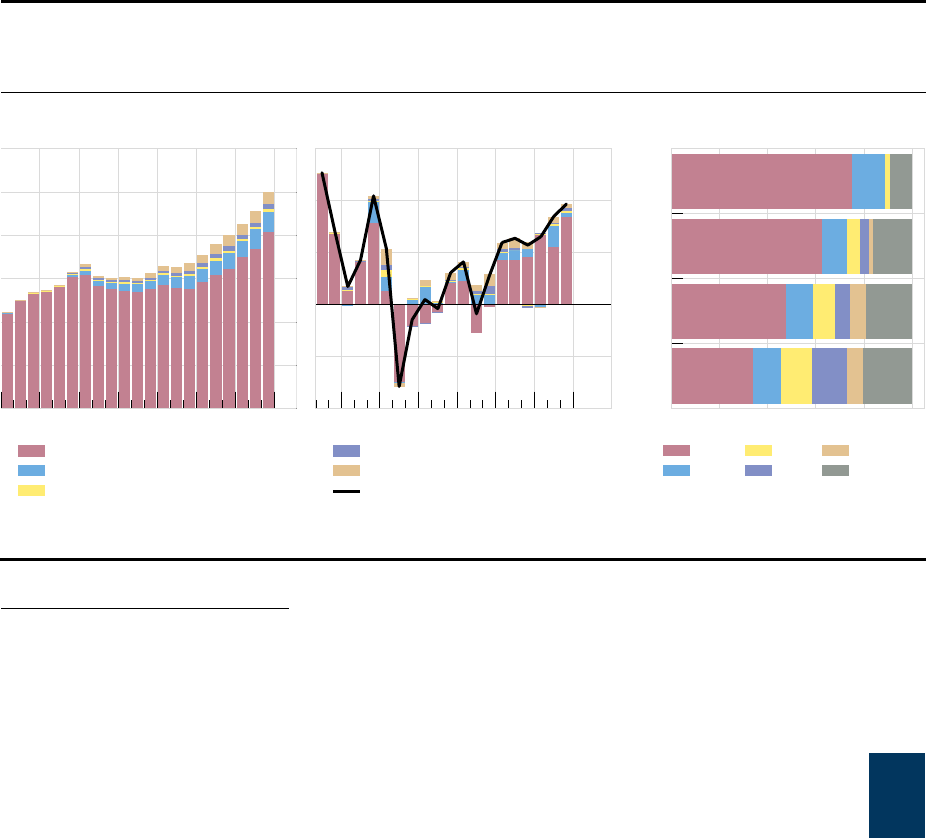

1.2.2. Wholesale funding and repos

Wholesale funding instruments – including repurchase agreements (or repos) – can be

used by NBFI entities to create short-term, money-like liabilities and increase leverage.

This facilitates credit growth and maturity/liquidity transformation outside the banking system.

Wholesale funding increases interconnectedness among financial institutions. Although

increasing interconnectedness may support efficient risk sharing in the financial system, in

periods of stress it may also spread shocks and contribute to procyclicality.

OFIs’ use of wholesale funding, in particular long-term funding, increased slightly in 2022

(Graph 1-10, LHS). OFIs continued to rely more on long-term wholesale funding (14.3% of total

OFI assets) than on short-term wholesale funding (4.3% of total OFI assets) and repo (2.2% of

total OFI assets). This has led to a slight reversal of the decline in OFIs’ overall use of wholesale

and repo funding observed over the previous four consecutive years.

ICs

OIFs

PFs

TCs

MMFs

SFVs

FinCos

BDs

HFs

OFIs

20100–10–20

2022 Compound annual growth 2016-21

ICs

OIFs

PFs

TCs

MMFs

SFVs

FinCos

BDs

HFs

OFIs

100–10–20

19

OFIs’ net level of repo assets continued to increase in 2022

21+EA-Group Graph 1-10

Funding of entities by source

1

Net repo position

3

Percenta

g

e of balance sheet

USD trillion

1

Short-term funding is defined as wholesale funding whose residual maturity is less than 12 months. Includes data for Russia up until

2020.

2

All deposit-taking corporations.

3

Repo assets less repo liabilities. Assets related to repo transactions on the buyer’s (collateral-

taker, cash-provider) balance sheet. Liabilities related to repo transactions on the seller’s (collateral-provider, cash-taker) balance sheet.

Does not include data for Russia.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data) and 2021 submission for Russia; FSB calculations.

Across banks, pension funds, insurance corporations, and OFIs, the latter were the

largest net cash providers in the repo market (Graph 1-10, RHS). OFIs’ net level of repo

assets continued to increase significantly in 2022, with net positive repo positions at end-2022

six times higher than two years before. They accounted for the largest share of repo assets.

Amongst the 18 jurisdictions that reported OFI repo activity, MMFs, other investment funds,

structured finance vehicles, and trust companies tended to be net cash providers through

reverse repo transactions, while broker-dealers, hedge funds and finance companies achieved

an almost net zero repo position (Graph 1-11). For more detail on broker dealers’ expansion of

their repo assets, see also section 2.4.

20

15

10

5

0

2221201918222120191822212019182221201918

Banks

2

OFIs

Wholesale:

ICs PFs

Repo Short-term (ex repos)

Long-term

3

2

1

0

–1

–2

22191613100704

Banks

2

OFIs ICs PFs

20

OIFs’ repo liabilities decreased sharply in 2022

21+EA-Group Graph 1-11

A

ssets

1

Liabilities

1

Net position

2

Percenta

g

e of balance sheet

Percenta

g

e of balance sheet

USD trn

1

Assets related to repo transactions on the buyer’s (collateral-taker, cash-provider) balance sheet. Liabilities related to repo transactions on

the seller’s (collateral-provider, cash-taker) balance sheet. Does not include data for Russia. MMF repo liabilities were slightly above zero

and therefore not visible in the upper-middle panel.

2

Repo assets less repo liabilities. Does not include data for Russia.

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

As was the case in 2021, the increase in OFIs’ net level of repo assets was primarily driven

by MMFs in the United States. Indeed, MMFs continued to increase their (cash) investments

in the Federal Reserve’s overnight reverse repo facility, which provided attractive risk-free

returns.

20

The Federal Reserve introduced an overnight reverse repo facility in 2013, which

serves as a monetary policy tool intended to improve control over short-term interest rates, and

added MMFs as eligible counterparties. This facility provides an opportunity to invest cash on a

collateralised basis at a rate set by the Federal Reserve and does not pose the same type of

risks present in a repo transaction with a private counterparty. The facility already saw strong

uptake in 2021, which further increased in 2022, reaching record inflows of $2.6 trillion at the

end of 2022.

20

See SEC Staff document (2021), Primer: Money Market Funds and the Repo Market, February.

40

30

20

10

0

2220181614121008

40

30

20

10

0

2220181614121008

BDs MMFs

2.50

1.25

0.00

–1.25

–2.50

2220181614121008

4.5

3.0

1.5

0.0

2220181614121008

FinCos OIFs

4.5

3.0

1.5

0.0

2220181614121008

HFs TCs

0.15

0.10

0.05

0.00

–0.05

–0.10

2220181614121008

SFVs

21

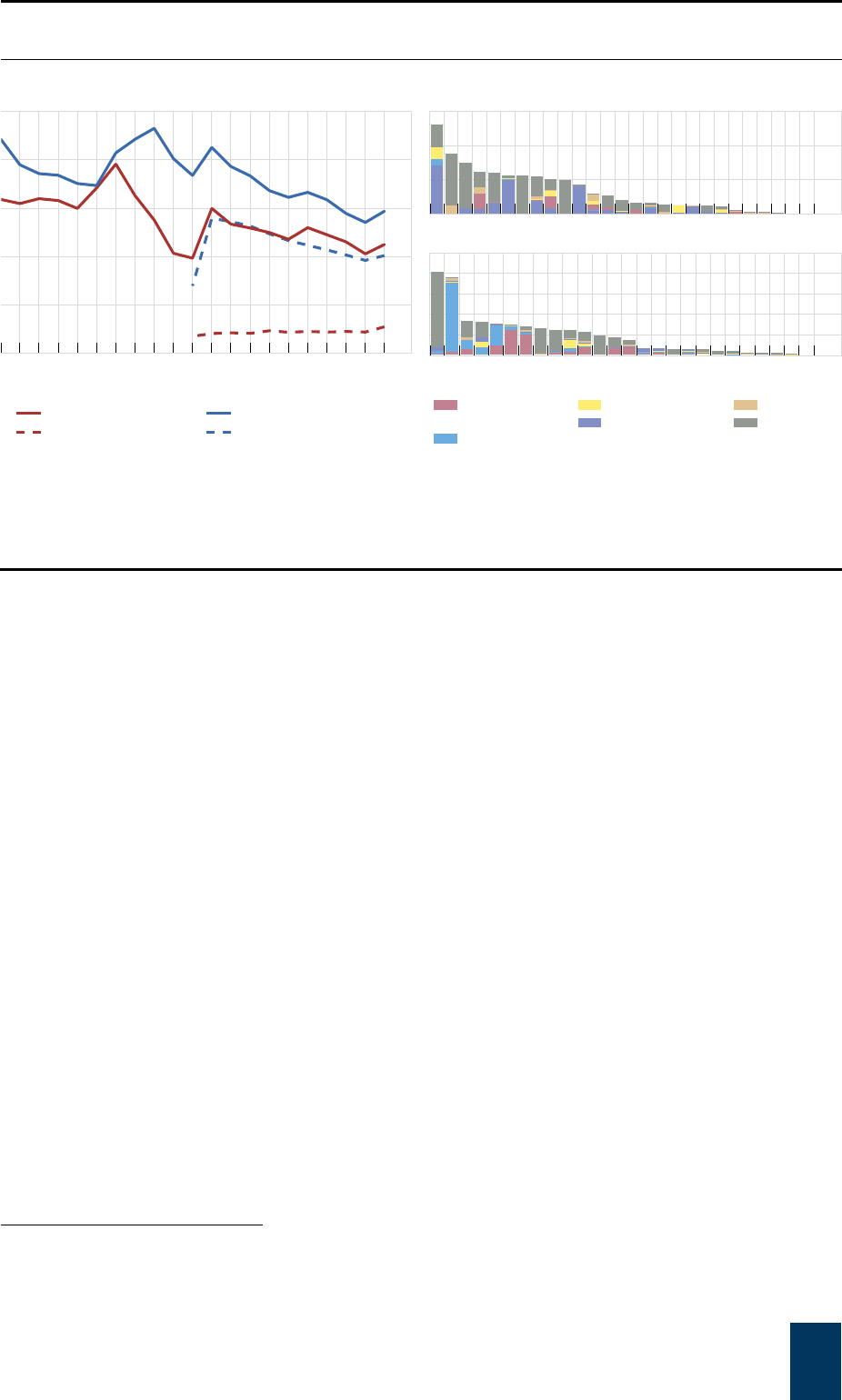

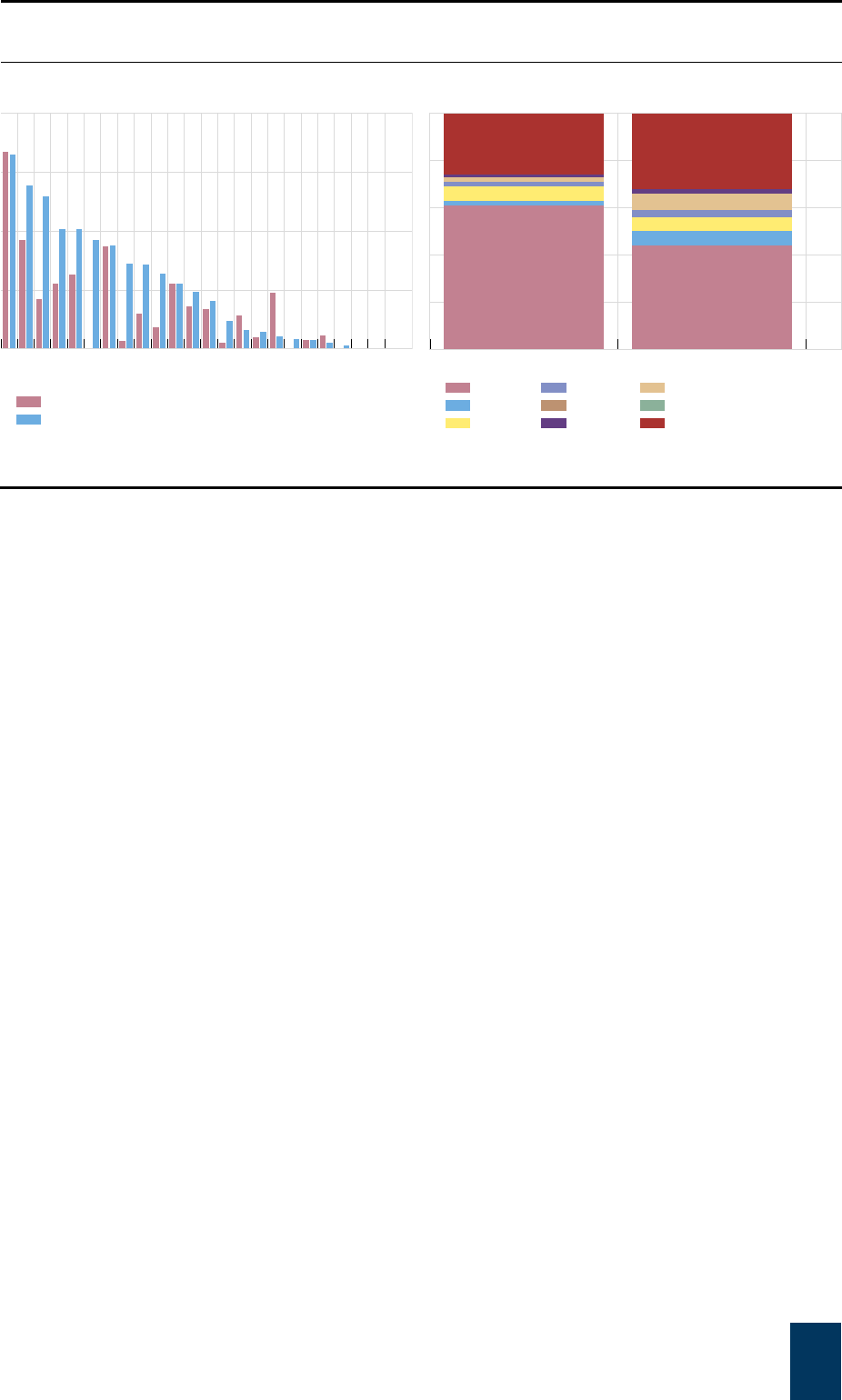

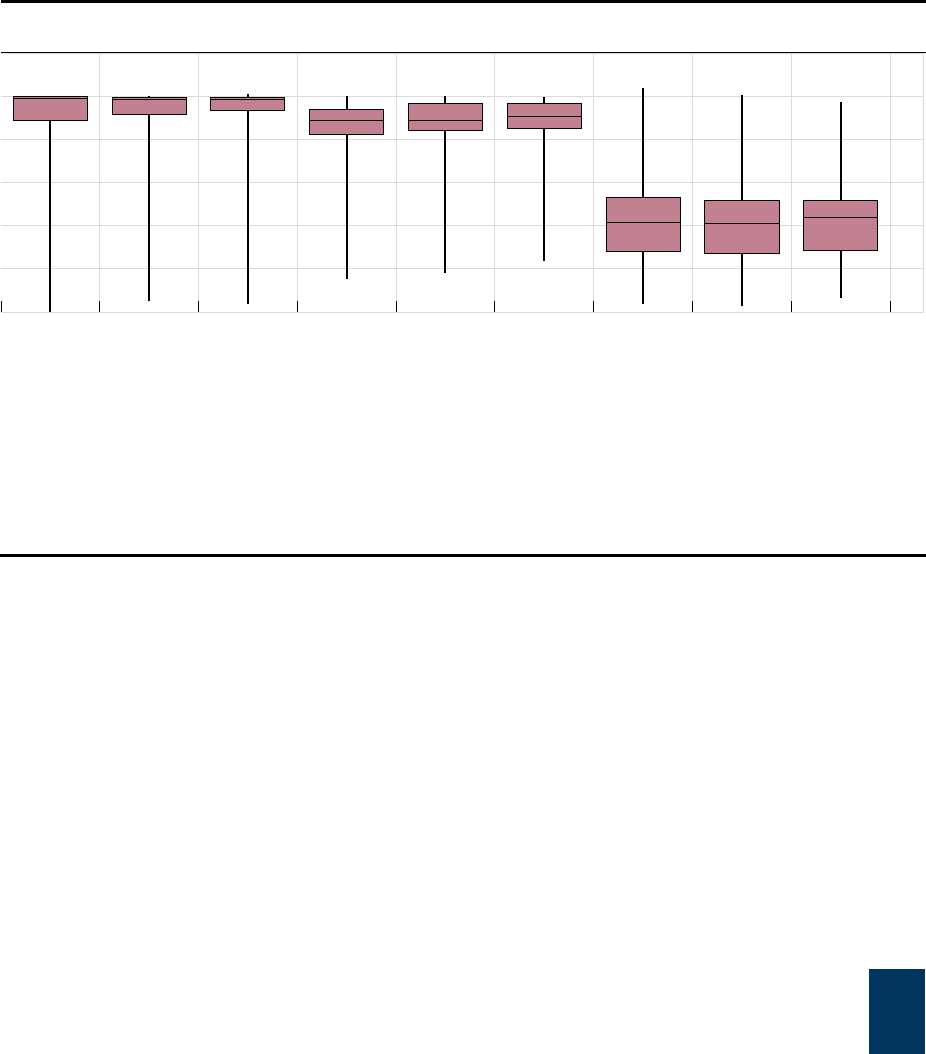

1.2.3. Financial leverage

As an enhancement to this year’s report, the FSB collected data on borrowings per entity

types outside of the narrow measure. Section 2 of the report features a number of vulnerability

metrics to measure (financial) leverage for the entities within the narrow measure. However,

entities outside the narrow measure – for example because they do not engage in credit

intermediation – can also take on leverage. In certain cases, this can have negative

consequences on financial stability.

21

After a small decrease following the Global Financial Crisis, OFI entities have increased

their borrowings, possibly leading to high levels of leverage (Graph 1-12, LHS). Total

borrowings measure how much debt financial intermediaries have taken on through various

means – issuing debt securities, taking on loans, or engaging in repo transactions (repo

liabilities). In aggregate, OFI total borrowings were smaller than that of banks (Graph 1-12, LHS).

Amongst OFIs, hedge funds and OIFs stood out as they decreased their borrowings 9.6% and

3.2% respectively, from 2021. In addition to debt levels, the debt-to-assets ratio was used

throughout to measure the extent to which financial intermediaries were levered in 2022 (Graph

1-12, RHS).

22

Finance companies, broker-dealers, structured finance vehicles and REITs

exhibited higher leverage ratios than other OFIs. Hedge funds’ financial leverage appeared

small, but data collected did not measure synthetic leverage.

OFI borrowings and leverage

29-Group

Graph 1-12

Total borrowings

1

Borrowings vs leverage in 2022

USD trillion

Ratio

1

Borrowings include debt securities, loans, and repos on the liability side of the balance sheet.

2

All deposit-taking corporations. For these

entities, borrowings do not include deposits on the liability side of the balance sheet.

Source: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

21

FSB (2023), The Financial Stability Implications of Leverage in Non-Bank Financial Intermediation, September.

22

This ratio was preferred to others (e.g. using equity) given data availability.

25

20

15

10

5

0

2220181614121008

Banks

2

BDs

CFIMLs

FinCos

HFs

MMFs

OIFs

REITs

SFVs

TCs

FinCos

BDs

SFVs

REITs

CFIMLs

HFs

TCs

OIFs

MMFs

45

30

15

0

–15

642

Total borrowings (USD trn)

Debt-to-assets (%)

22

1.3. Interconnectedness among financial sectors

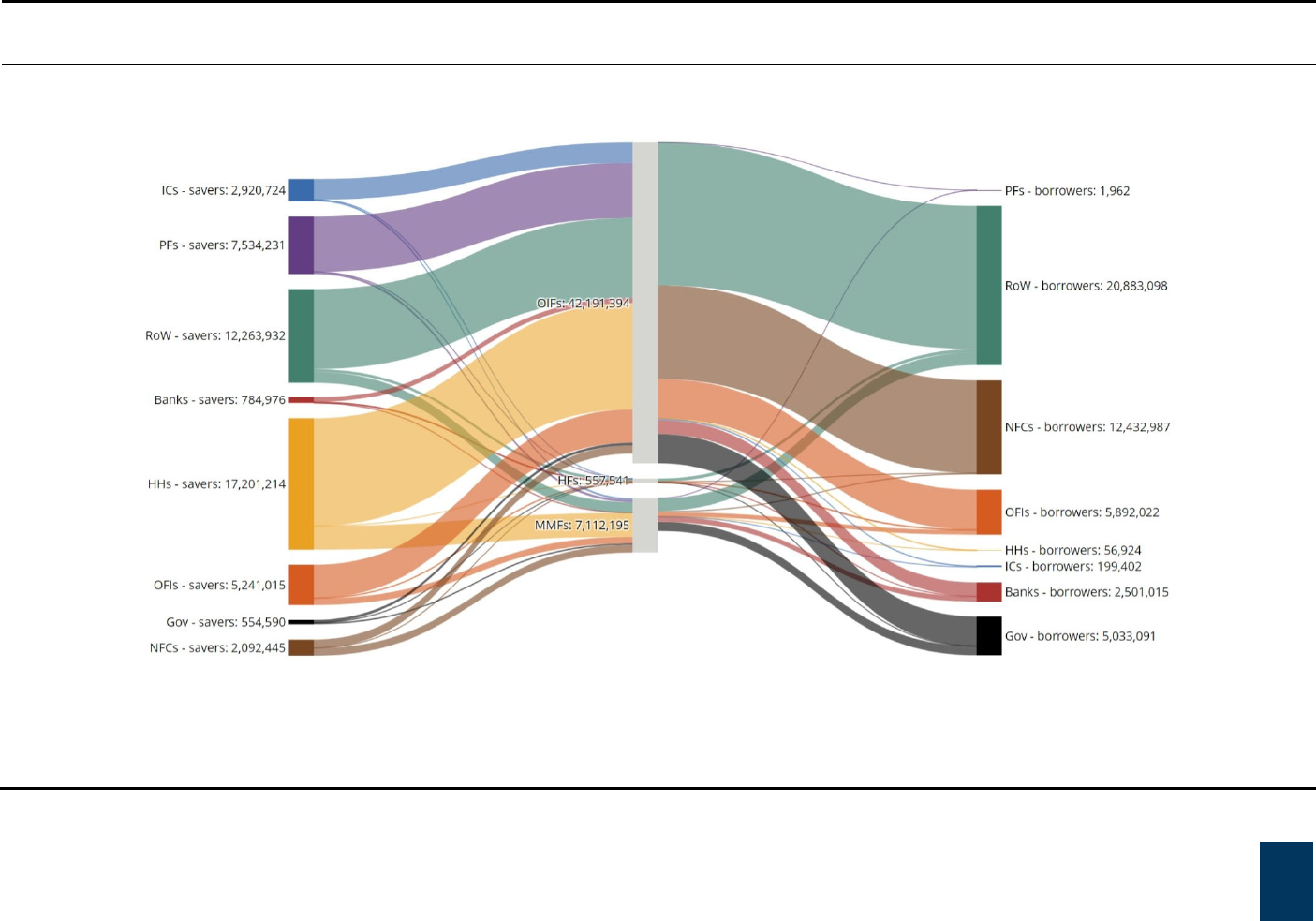

Financial interconnectedness is a feature of an open and integrated global financial

system. It may help share risk across financial sectors but may also serve as a channel for risk

transmission, particularly when entities along intermediation chains employ a high degree of

leverage or engage in maturity and/or liquidity transformation. Therefore, measures of

interconnectedness among banks, OFIs, and other NBFI entities can serve as important

indicators of potential contagion, within and across sectors and borders. This section focuses on

direct domestic and cross-border balance sheet interconnectedness between banks, insurance

corporations, pension funds, and OFIs. Interconnectedness is further discussed in each EF

section. To measure direct interconnectedness, such as direct borrowing and lending, or

investment exposures between two counterparties, the FSB compiled aggregated balance sheet

data to identify balance sheet asset and liability exposures between financial sectors that arose

from credit provision and/or investment in a counterparty.

23

These aggregated data were used

to calculate measures of interconnectedness between sectors, including exposures and funding

dependence.

Data enhancement for this year’s report reduced the data gaps relating to

interconnectedness, thus providing a more comprehensive picture of linkages between

entities and across borders. This work, which has sought to consider differences in reporting

approaches across jurisdictions, has been successful in reducing unidentified linkages as

highlighted in this section.

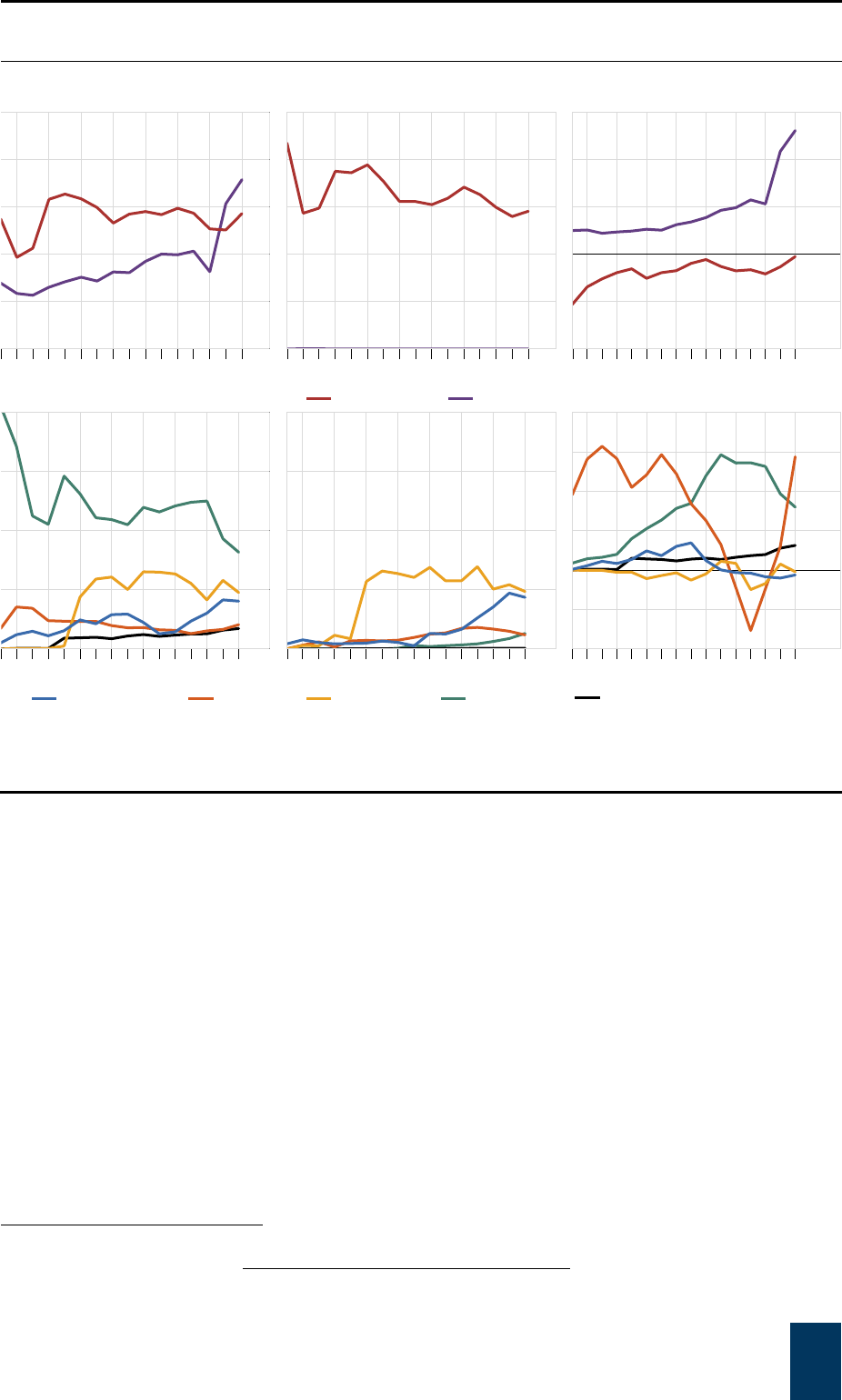

1.3.1. Aggregate linkages

Households had the largest claims on pension funds, insurance corporations, and banks.

OFIs had the largest cross-border linkages across entity types expressed as a percentage of

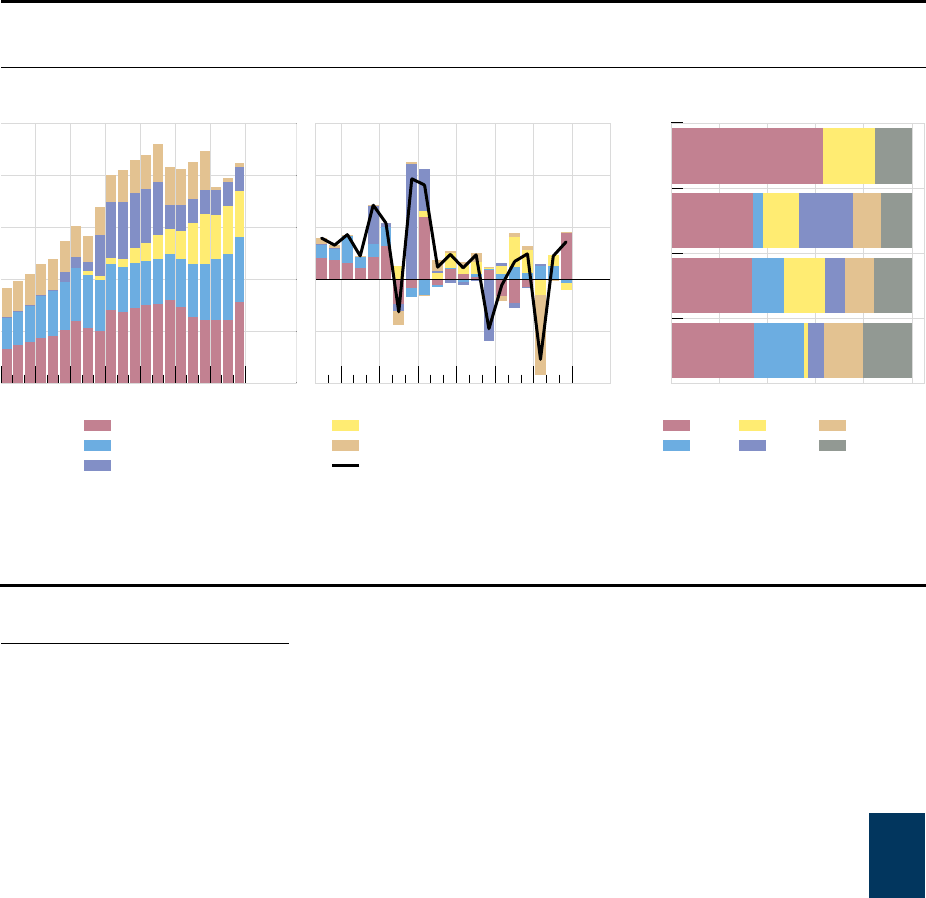

both total claims and liabilities, and these formed the largest proportion of OFIs’ identified

linkages, though a significant share remained unknown (Graph 1-13, LHS). Banks’ claims were

also mostly on the rest of the world (RoW). Pension funds and insurance corporations continued

to have large claims on OFIs, reflecting the use of investment funds to manage some of their

assets. The claims of central banks, public financial institutions, and non-bank deposit-taking

corporations are largest on banks, followed by OFIs (Graph 1-13, RHS).

While unspecified linkages are a gap in global data reporting, for 2022, jurisdictions

significantly reduced the share of unspecified financial linkages. This improvement was

observed across all entity types and was most notable in the case of pension funds, where

identified linkages increased by approximately 25 – 30 percentage points with regard to both

claims and liabilities (Graph 1-13, RHS). Thus, unspecified linkages accounted for only 21.8%,

at most, for pension funds (Graph 1-13, LHS).

23

Equity data was included in both “claims on” and “liabilities to”.

23

Aggregate linkages, measured as a percentage of financial assets

29-Group Graph 1-13

A

ggregate linkages

1

Change in identified linkages 2023 vs. 2022

Percenta

g

e of total financial assets

Percenta

g

e points

1

The total reported linkages of all participating jurisdictions as a percentage of total claims and liabilities of each sector. The computed

measures do not capture risks from indirect interconnectedness and do not take into account important qualitative aspects, such as the

difference between secured and unsecured liabilities.

2

“Unspecified” indicates linkages to other sectors not identified by jurisdiction or not

covered in this report.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

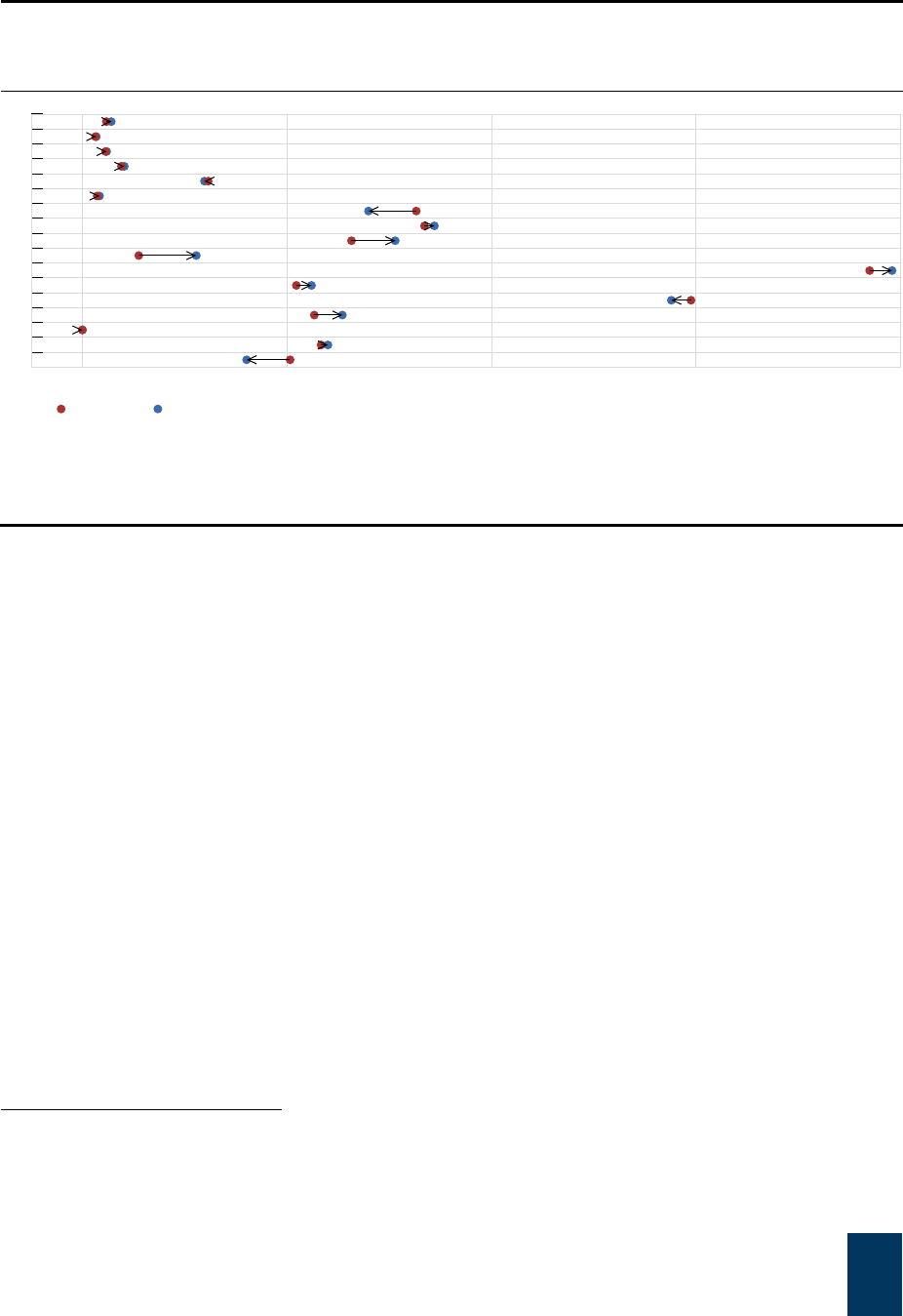

1.3.2. Linkages between the banking and NBFI sectors

Banks and NBFI entities are directly connected, with funding channels operating in both

directions. For instance, banks often extend credit to (or invest in) insurance corporations,

pension funds, or OFIs, while these entities provide funding to banks or deposit the non-invested

part of customer assets with custodian banks.

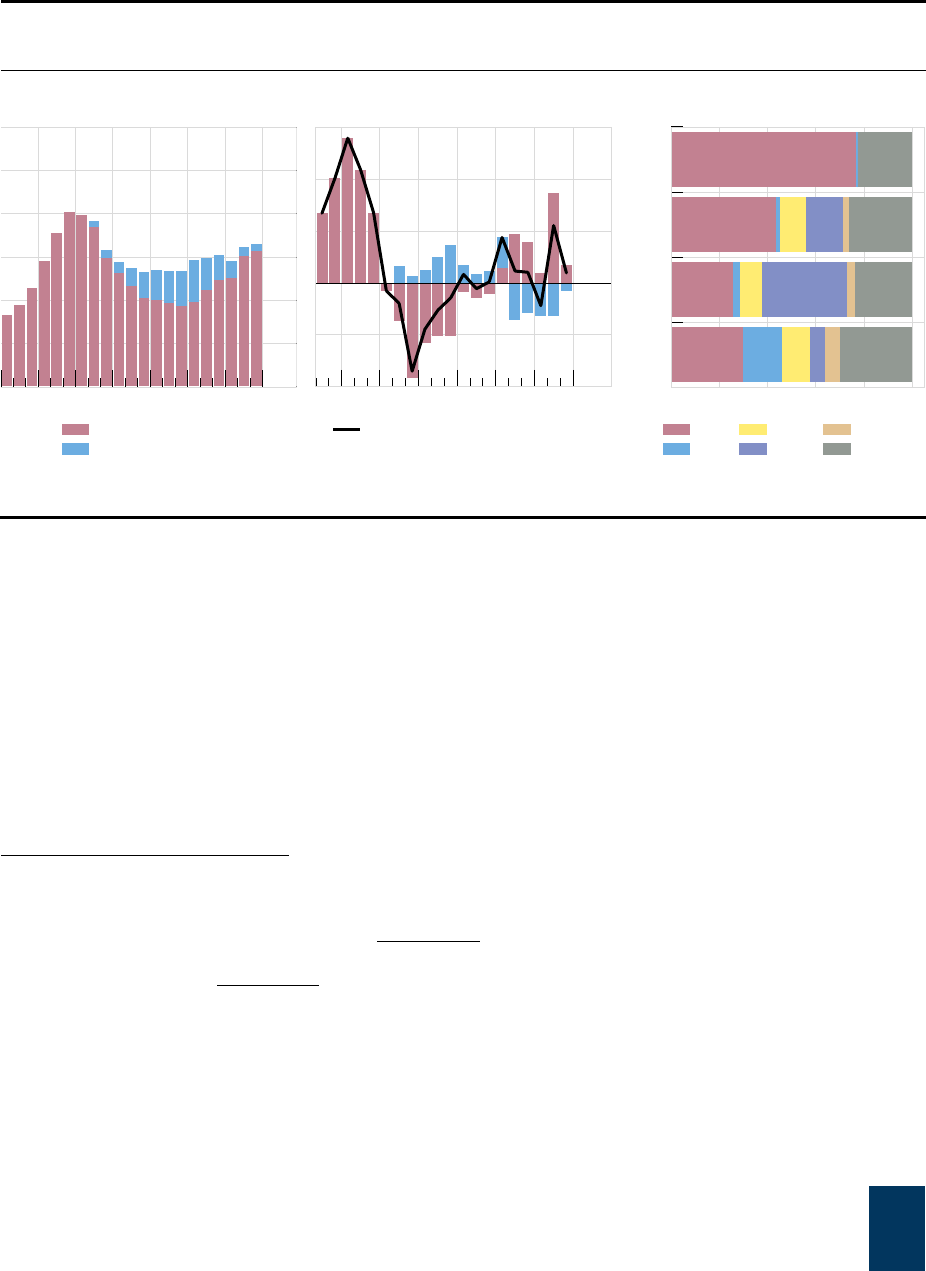

Interconnectedness between the banking and NBFI sectors decreased for the banking

sector, but increased for the NBFI sector, as measured by the size of links as a proportion

of the respective sector assets. Banks continued to be net recipients of funding from NBFI

entities, although this funding has been gradually decreasing since 2013 in proportion to banks’

assets (Graph 1-14, LHS). In contrast, OFIs’ use of funding from banks, when measured as a

proportion of OFI assets, increased in 2022 from 4.1% to 4.5% (Graph 1-15, LHS). While OFIs’

liabilities to banks increased year-on-year, the increase in the measure of interconnectedness is

largely attributed to OFIs’ assets having decreased in 2022, with the United States (-12.6%),

Ireland (-7.1%) and Luxembourg (-5.6%) contributing significantly to this fall in OFIs’ assets. In

nominal terms, OFIs’ use of funding from banks increased by approximately $180 billion.

Banks’ overall use of funding from NBFI entities has not changed significantly across

jurisdictions. As in 2021, in South Africa, funding from NBFI entities was larger than 30% of

Liabilities

Claims

Liabilities

Claims

Liabilities

Claims

Liabilities

Claims

100806040200

Banks

ICs

OFIs

PFs

Banks

OFIs

Unspecified

2

Insurance corporations

Pension funds

Financial auxiliaries

30

15

0

–15

–30

–45

Claims

Liabilities

Claims

Liabilities

Claims

Liabilities

Claims

Liabilities

Banks OFIs

corporations

Insurance

funds

Pension

Households

Non-financial companies

non-bank DTCs

CBs, PFIs and

Government

RoW

Change of "Unspecified"

24

total banks’ assets. In Luxembourg

24

and Chile, banks’ use of funding from NBFI entities was

over 20% of total banks’ assets, and for Brazil,

25

Korea, Australia, Switzerland, and Argentina it

was over 10% (Graph 1-14, RHS).

Banks’ interconnectedness with NBFI continued to decrease relative to

bank assets

Graph 1-14

Banks’ interconnectedness with OFIs and ICPFs

1

By jurisdiction, at end-2022

2

Percenta

g

e of

g

lobal banks’ assets

Percenta

g

e of banks’ assets

The left-hand panel includes data for the 21+EA-Group, while the right-hand panels include data for the 29-Group.

1

The sharp rise in OFI linkages in 2013 partly reflects availability of euro area aggregate data from 2013 onwards. Includes data for Russia

up until 2020.

2

For upper (lower) panel, banks’ use of funding from (exposure to) the corresponding NBFI sub-sector, net of prudential

consolidation (where data permits), as a share of bank assets. Neither includes data for Russia.

3

”Other OFIs” includes CCPs, hedge

funds, trust companies, and unidentified OFIs.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data) and 2021 submission for Russia; FSB calculations.

Within NBFI entities, OFIs’ interconnectedness with banks continues to be higher than

that of insurance corporations and pension funds taken together (Graph 1-15). OFIs’

funding from banks exceeded 15% of OFI assets in two jurisdictions. For most jurisdictions, the

OFIs entities most commonly using bank funding were CCPs, hedge funds, trust companies,

and unidentified OFIs, with the exception of India, Indonesia, and Saudi Arabia – where they

were finance companies. OFIs’ exposures to banks were very large in South Africa and

Argentina (more than 30% of OFI assets), with South African OFIs being CCPs, hedge funds,

trust companies, and other unidentified OFIs, while Argentinian OFIs were predominantly MMFs.

24

In Luxembourg, these linkages arise mainly because investment funds deposit part of their cash at local custodian banks.

25

In Brazil, these linkages mainly arise because investment funds channel their liquidity to banks via reverse repo operations

backed by government debt; the Central Bank drains this liquidity through repos with banks.

8

6

4

2

0

2221201918171615141312111009080706050403

OFIs

ICPFs

Banks' use of funding from:

Banks' exposures to:

30

20

10

0

SACNINKYCAITIDNLUSARAUBRLU

SGHKTRBEMXESDEFRUKIECHKRCLZA

Banks' use of funding from NBFI entities

9

6

3

0

HKCNNLMXBRIDFRDEUSKYKRITCA

SGSAARTRCLAUCHESIEINLUUKBEZA

Banks' exposures to NBFI entities

Finance companies

MMFs

funds

Other investment

Broker-dealers

SFVs

Other OFIs

3

ICs

PFs

25

NBFI’s interconnectedness with the banking sector increased relative to

NBFI assets

Graph 1-15

Interconnectedness of NBFI sector with banks

1

By jurisdiction, at end-2022

2

Percenta

g

e of OFI or ICPF assets

Percenta

g

e of OFI assets

The left-hand panel includes data for the 21+EA-Group, while the right-hand panels include data for the 29-Group.

1

Includes data from 19 jurisdictions and EA Group. The sharp rise in OFI linkages in 2013 partly reflects availability of euro area aggregate

data from 2013 onwards. Includes data for Russia up until 2020.

2

For upper (lower) panel, banks’ claims on (liabilities to) the corresponding

OFI sub-sector, net of prudential consolidation (where data permits), as a share of OFI assets. Neither includes data for Russia.

3

‘Othe

r

OFIs’ includes CCPs, hedge funds, trust companies, and unidentified OFIs.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data) and 2021 submission for Russia; FSB calculations.

OFI subsectors’ deposit exposures to banks largely continued to decrease, with the

exception of MMFs (Graph 1-16, LHS), while OIF’s use of funding from the NBFI sector

decreased (Graph 1-16, RHS). OFI funding sources varied across jurisdictions: pension fund

linkages were highest in Australia, insurance corporations in South Africa, and other financial

intermediaries in Brazil.

26

(Graph 1-17).

26

In Brazil, OFI linkages were predominantly with OIFs and mainly due to funds of funds.

8

6

4

2

0

2221201918171615141312111009080706050403

OFIs'

ICPFs'

Use of funding from banks:

Exposures to banks:

20

10

0

KYIEBRCNHKCLCAKRTRESINDEIT

SGLUNLUSMXARCHAUSAUKFRBEZAID

OFIs' use of funding from banks

40

30

20

10

0

KYIELUNLUSMXESTRKRITBRIDAR

SGSACABECNINDEUKCHAUCLFRZA

OFIs' exposures to banks

funds

Other investment

MMFs

Broker-dealers

Finance companies

SFVs

Other OFIs

3

26

Recent trends in OFIs’ deposit exposures to banks largely continued, with

the exception of MMFs, while OFIs’ use of funding from NBFIs decreased

Graph 1-16

OFI deposits – selected entities

1

OFIs’ use of funding

2

Per cent of total assets from each subsecto

r

Per cent of OFI assets

1

Includes data from 16 jurisdictions.

2

OFIs use of funding from ICs = OFIs’ liabilities to ICs as a share of OFI assets. OFIs use of funding

from PFs = OFIs’ liabilities to PFs as a share of OFI assets. OFIs’ use of funding from OIFs is based on data reported on a consolidated

basis by jurisdictions, net of entities prudentially consolidated into banking groups.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

OFIs’ use of funding from NBFI per jurisdiction

End-2022, as a percentage of OFI assets

Graph 1-17

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

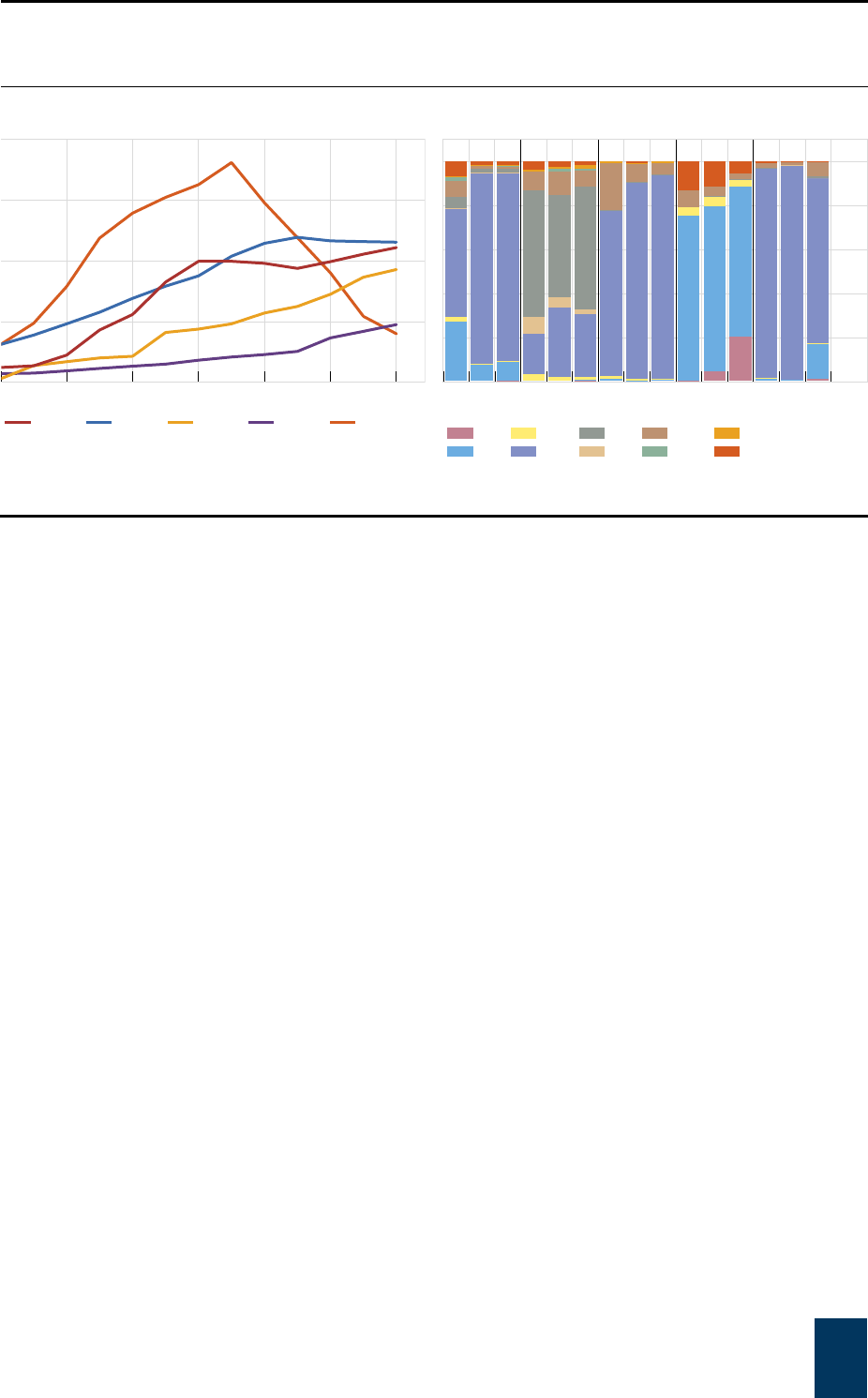

1.3.3. Cross-border interconnectedness

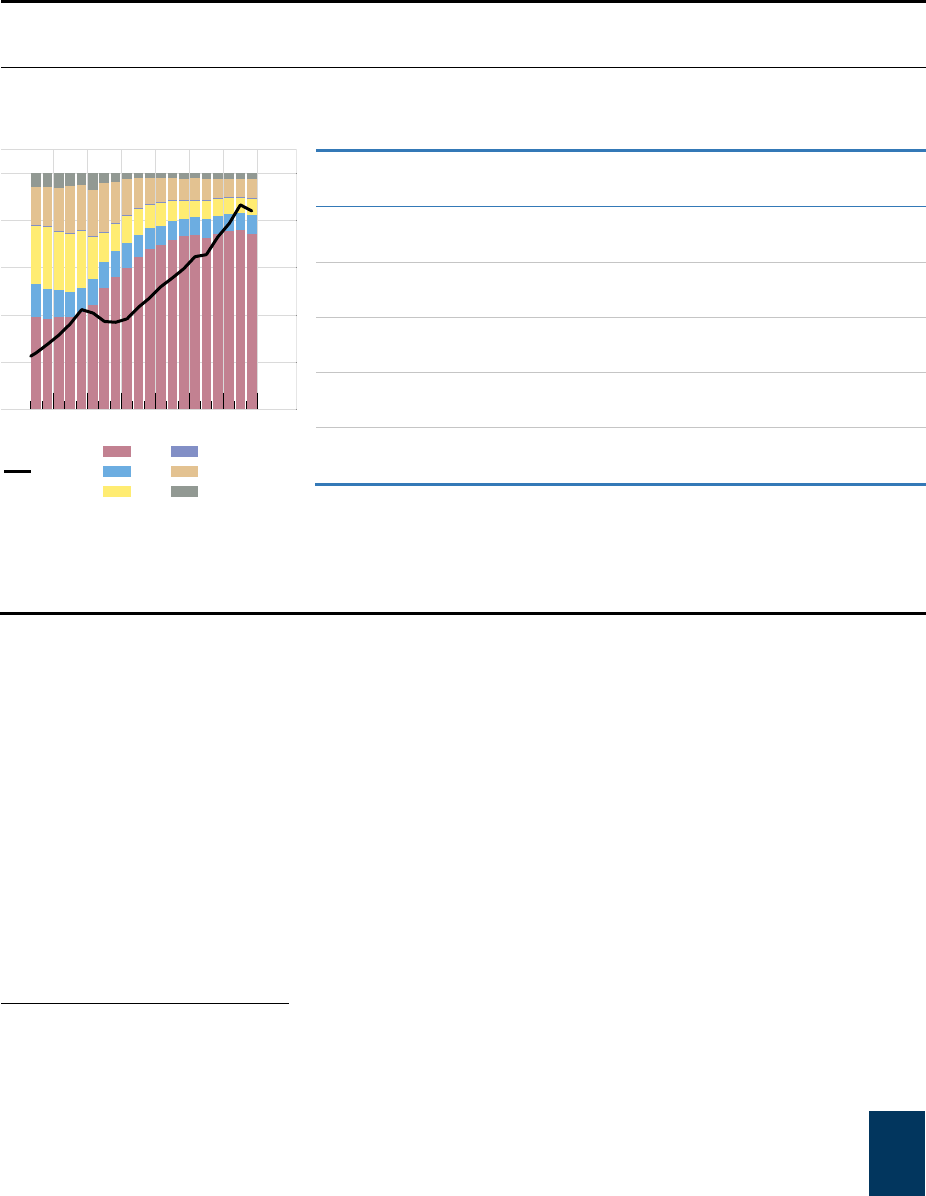

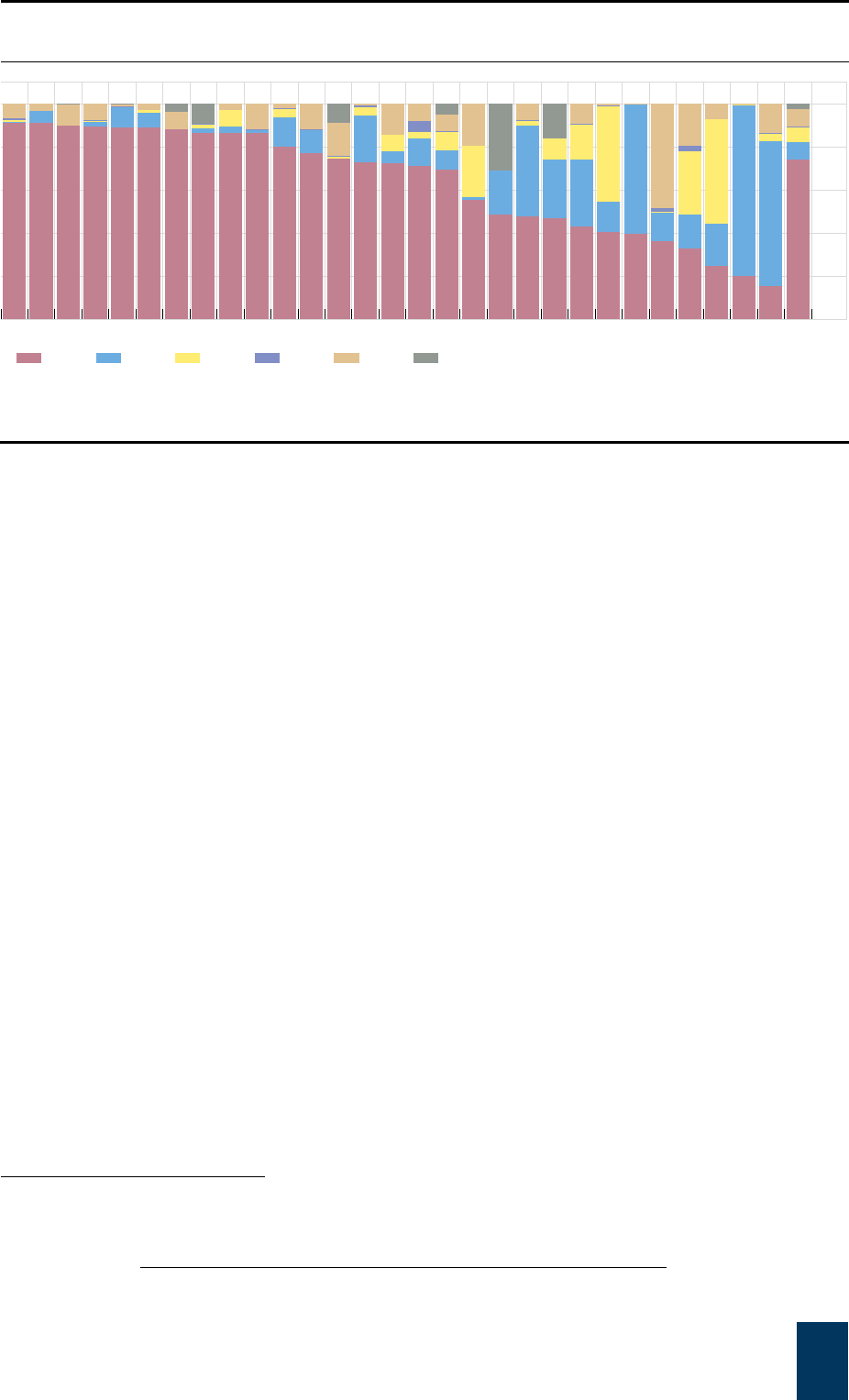

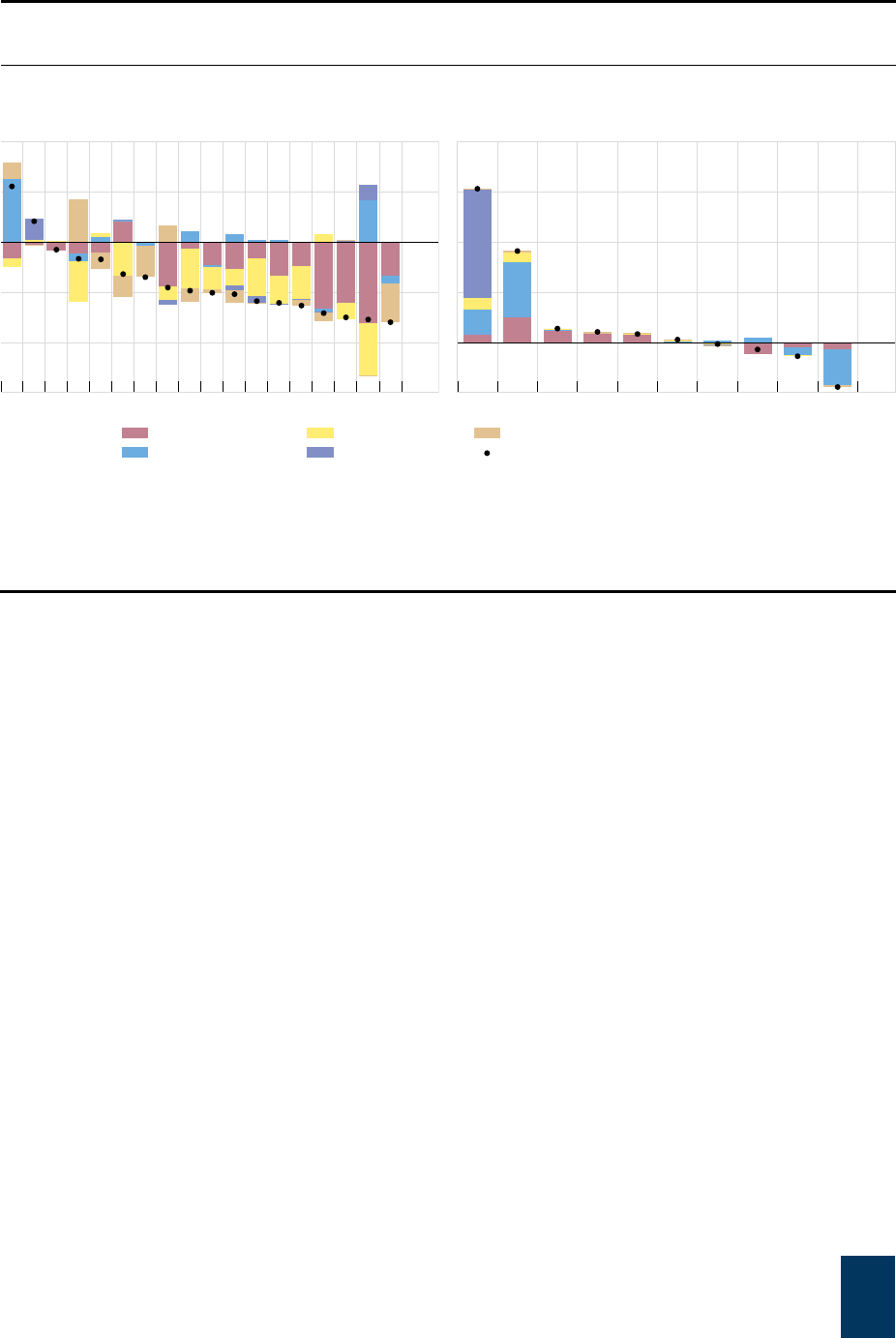

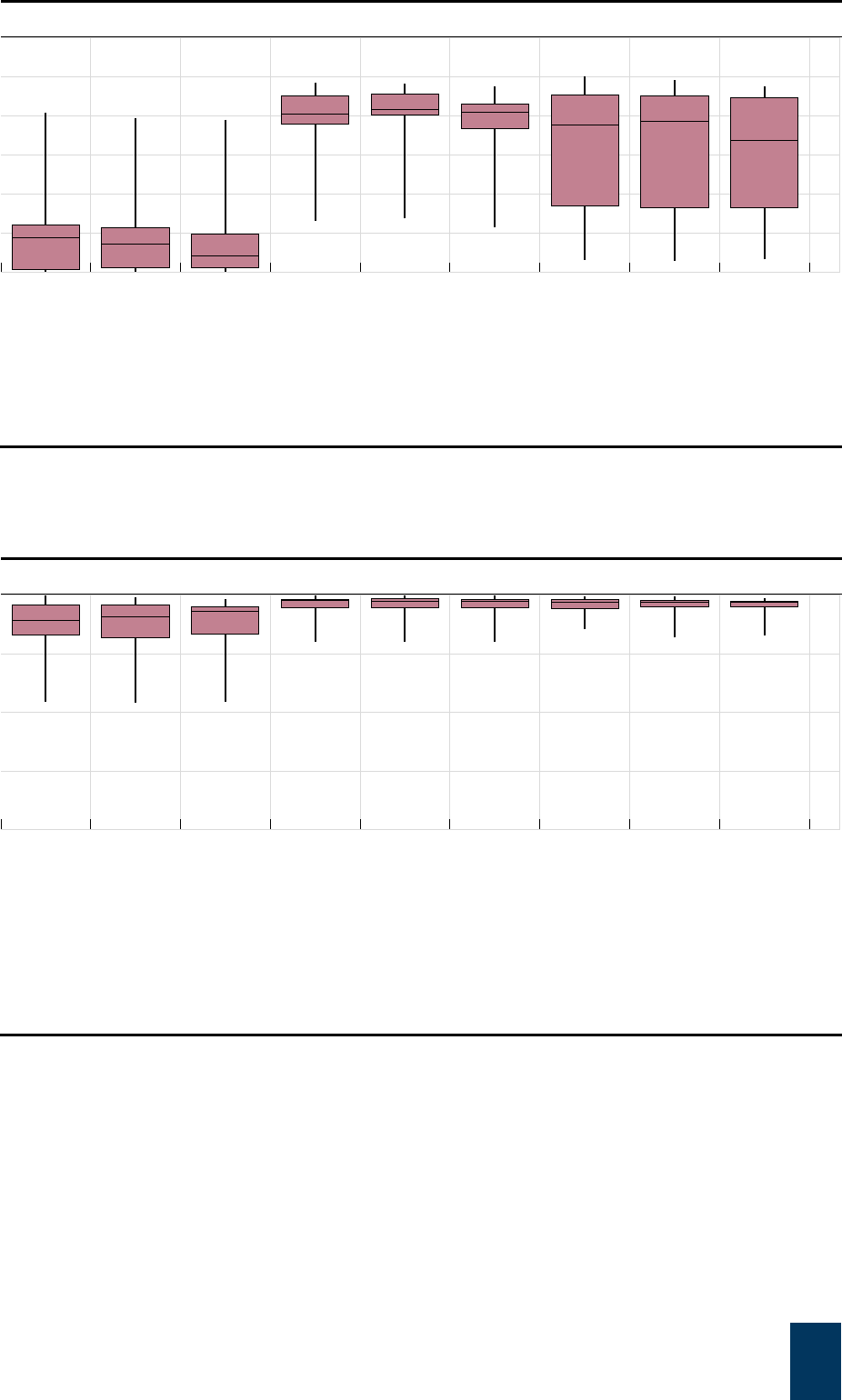

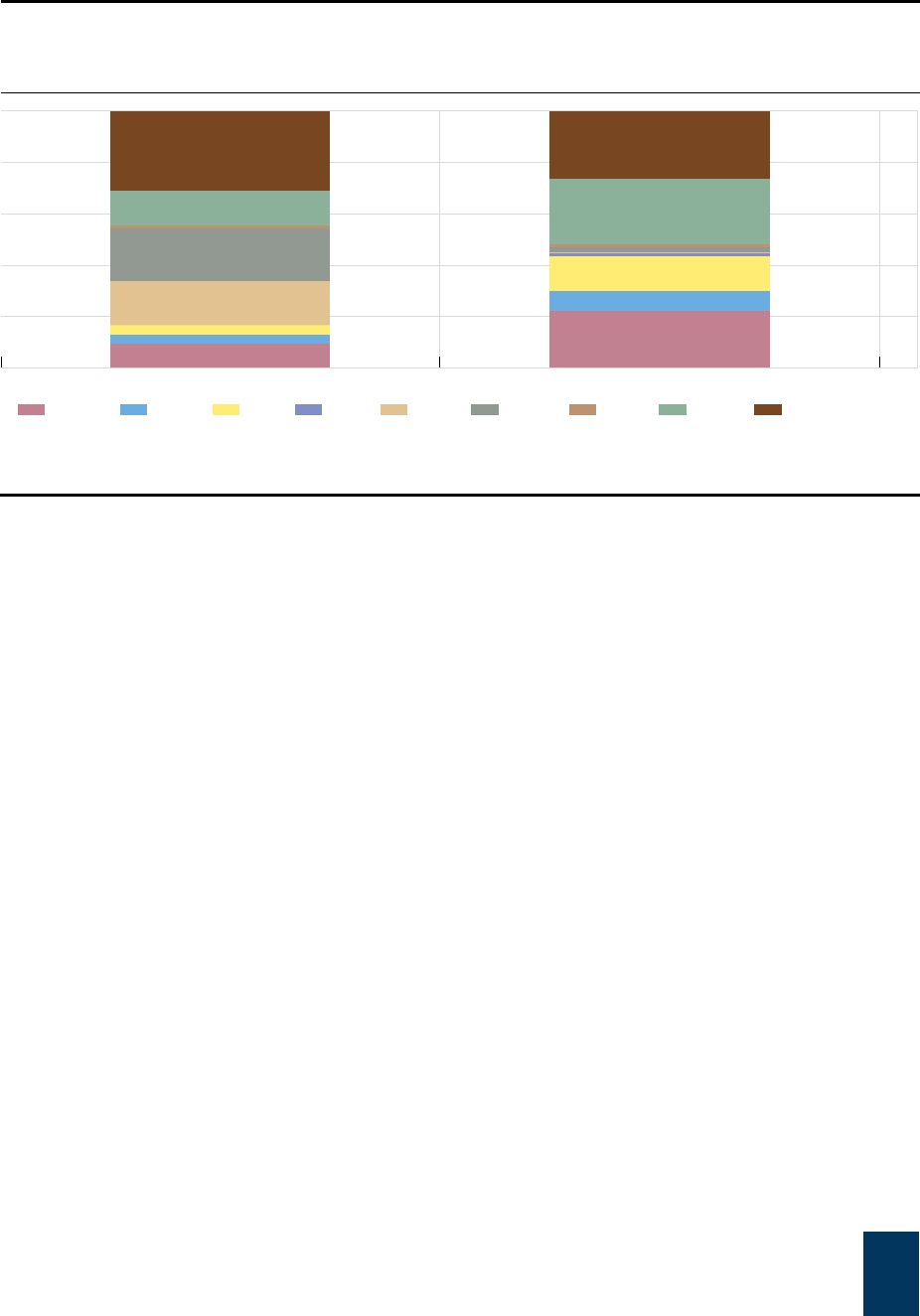

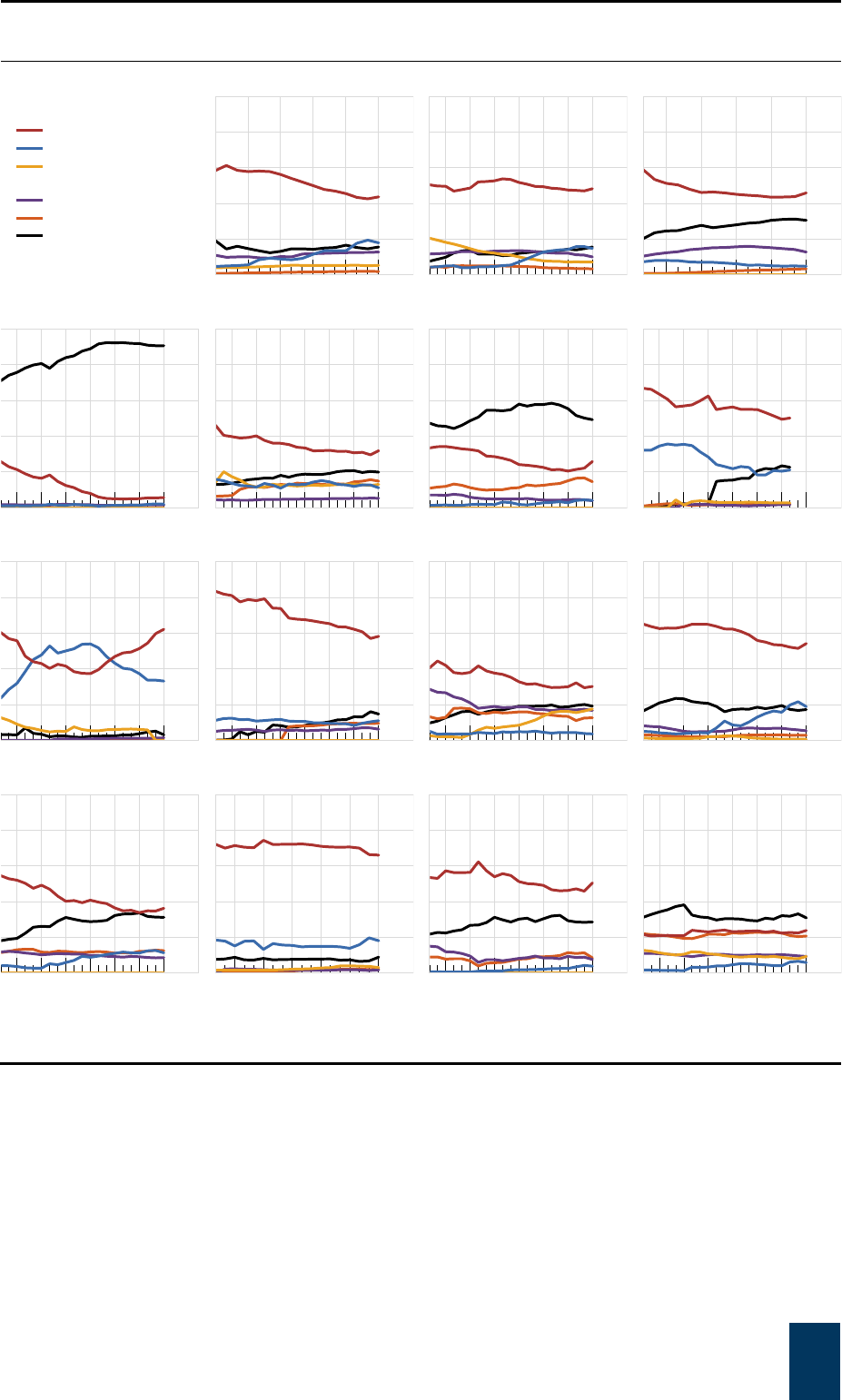

In some jurisdictions, cross-border linkages continued to represent a large share of OFI

assets (Graph 1-18, LHS). Funding from and exposures to the rest of the world were larger

than 20% of OFI assets in Luxembourg, Belgium, Spain, France, the Netherlands, and Ireland.

South Africa stood out as the only jurisdiction where OFIs’ use of funding from the rest of the

world was much larger than the claims. OIFs accounted for more than 40% of OFIs’ linkages

with the rest of the world (Graph 1-18, RHS). In some jurisdictions, cross-border linkages may

also be due to ownership structures and/or operational and distributional agreements involving

entities domiciled in different jurisdictions. This was particularly relevant for investment funds

where cross-border activities tend to play an important role.

18.0

13.5

9.0

4.5

0.0

22191613100704

MMFs OIFs BDs FinCos SFVs

10

8

6

4

2

0

222018161412100806

ICs PFs OFIs OIFs Banks

50

40

30

20

10

0

SGSAHKFRCLLUIEESBEMXINKRCAARZANLDEUSBRAU

ICs PFs OFIs OFIs, of which OIFs

27

Cross-border interconnectedness

29-Group

Graph 1-18

A

ggregate exposures between OFIs and RoW OFIs’ cross-border interconnectedness, at end-2022

Percenta

g

e of OFI assets

Per cent of total OFIs’ identified linka

g

es with RoW

60

40

20

0

TRBRARMXKRAUCASGCHFRBE

INJPCLZAITUSIEUKNLESDELU

OFIs' use of funding from RoW

1

OFIs' exposures to RoW

2

80

60

40

20

0

LiabilitiesClaims

OIFs

SFVs

MMFs

FinCos

TCs

HFs

BDs

CCPs

Other OFIs

1

OFIs’ liabilities to the RoW as a share of OFI assets.

2

OFIs’ claims to the RoW as a share of OFI assets.

Sources: Jurisdictions’ 2023 submissions (national sector balance sheet and other data); FSB calculations.

28

2. The narrow measure of NBFI

This section explores the narrow measure of NBFI in greater detail. It first provides an

overview of global trends for the overall narrow measure across all EFs.

27,28

It then presents

trends and vulnerability metrics

29

for each of the five EFs (see Annex 4 for a discussion of the

metrics used to describe them).

30

Each EF contains multiple entity types. Different entity types,

and business lines within entity types, may give rise to different types of vulnerabilities (Table 2-

1); this report provides an overview of the main vulnerabilities.

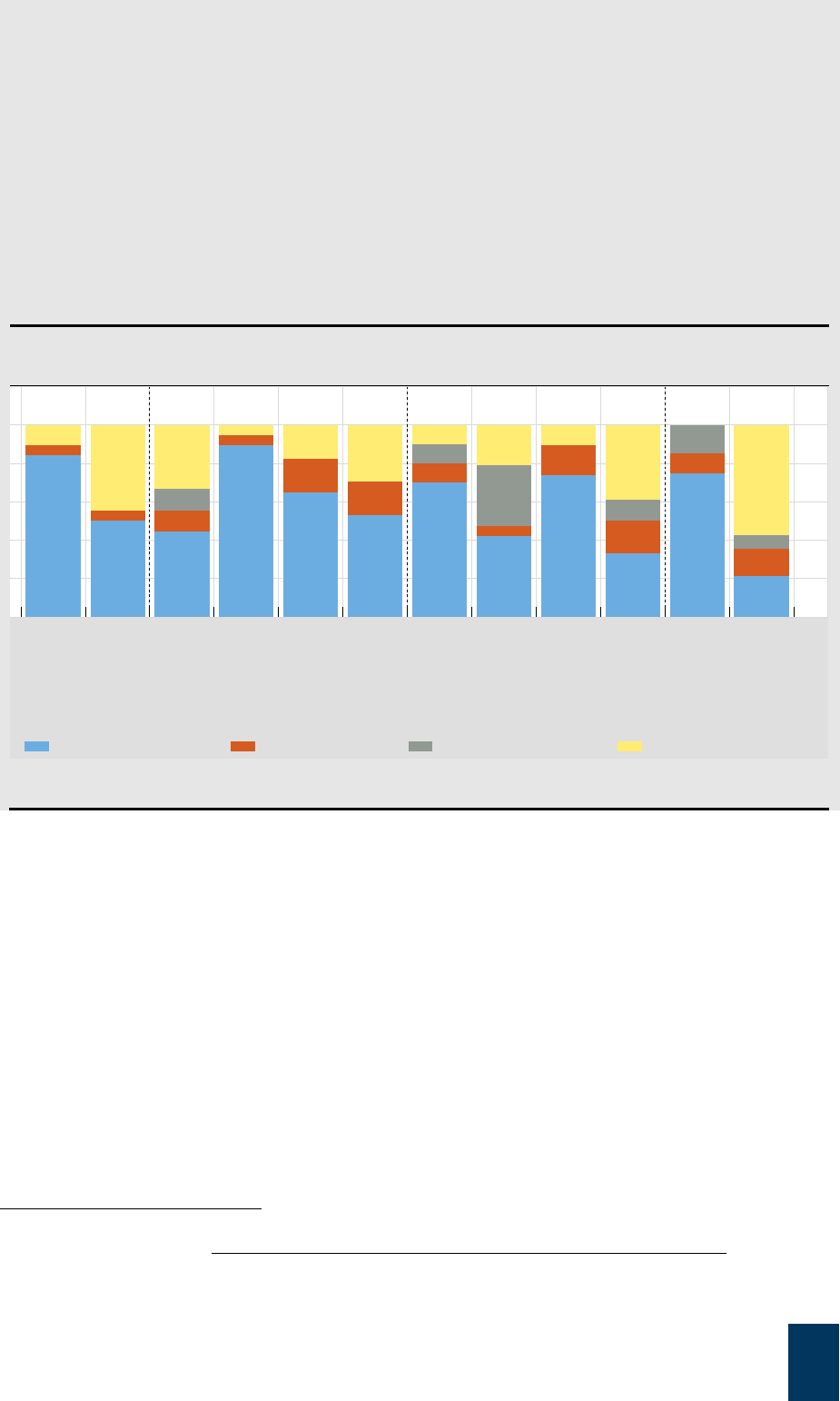

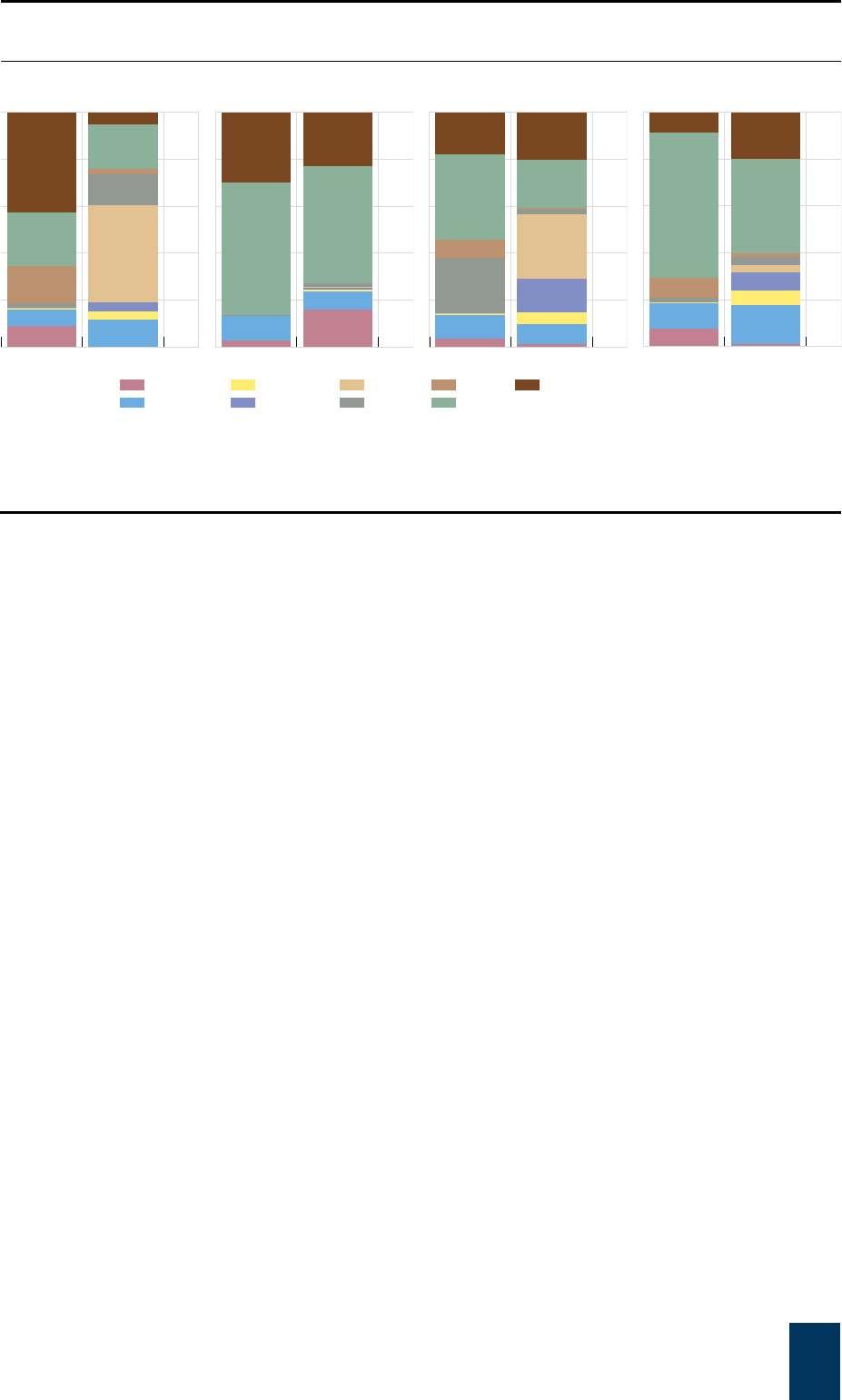

Table 2-1: Classification by economic functions

Economic function Definition

Typical entity types

31

EF1 Management of collective

investment vehicles with

features that make them

susceptible to runs

MMFs, fixed income funds, mixed funds,

credit hedge funds,

32

real estate

investment trusts and funds

EF2 Loan provision that is

dependent on short-term

funding

Finance companies, leasing/factoring

companies, consumer credit companies

EF3 Intermediation of market

activities that is dependent

on short-term funding or on

secured funding of client

assets

Broker-dealers, securities finance

companies

EF4 Facilitation of credit creation Credit insurance companies, financial

guarantors, monoline insurers