PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 1

of 65 www.revenue.pa.gov

Table of Contents

Overview ................................................................................................................................................................................ 4

Definition of Gross Employee Compensation for Pennsylvania Personal Income Tax .................................................... 4

Income Items Taxable as Federal Compensation Compared to Income Items Taxable as PA Compensation .............. 4

Income Items Always Taxable as Pennsylvania CompensationIncome Items Never Taxable as PA Compensation ..... 5

Income Items Taxable as Pennsylvania Compensation Based on Facts and Circumstances ........................................ 7

Costs, Expenses, and Deductions Against Gross Compensation ................................................................................. 10

Pennsylvania Resident Compensation ........................................................................................................................... 10

Nonresident Pennsylvania Compensation ..................................................................................................................... 10

Pennsylvania Compensation – General Rules ................................................................................................................. 10

Pennsylvania Statutes, Regulations and Other Guidance ............................................................................................. 10

W–2 Wage and Tax Statement (PA-40 Schedule W2–S, Wage Statement Summary) ................................................ 11

Withholding Requirements ............................................................................................................................................. 11

Reciprocal Compensation Agreements .......................................................................................................................... 11

Federal/Pennsylvania Personal Income Tax Differences in Arriving at Box 16 Wages ................................................. 12

Current Compensation – Pennsylvania Wages ............................................................................................................... 12

Covenants Not-To-Compete or to Surrender a Right to Future Employment and Early Separation Incentive Payments .

12

Reduction In Force (“RIF”) Entitlements ......................................................................................................................... 12

Clergy ........................................................................................................................................................................... 14

Statutory Employees ....................................................................................................................................................... 14

Members of the U.S. Armed Forces or Foreign Service ................................................................................................ 15

Athletes and Entertainers ............................................................................................................................................... 18

Bonuses ........................................................................................................................................................................ 20

Incentive Pay .................................................................................................................................................................. 20

Commissions .................................................................................................................................................................. 20

Tips and Gratuities .......................................................................................................................................................... 20

Vacation Pay/Holiday Pay .............................................................................................................................................. 20

Sick Pay ........................................................................................................................................................................ 21

Commercial Accident and Health Insurance; Self-Insured Accident and Health Plan Coverage and Benefits ............. 21

Disability ..................................................................................................................

...................................................... 23

Strike Benefits ................................................................................................................................................................. 23

Group Term Life Insurance ............................................................................................................................................. 24

Unemployment Compensation ....................................................................................................................................... 24

Workers Compensation .................................................................................................................................................. 24

Occupational/Disability Act Benefits ............................................................................................................................... 24

Stipends ........................................................................................................................................................................ 24

Scholarships/Fellowships ............................................................................................................................................... 24

Moving Expense Reimbursements ................................................................................................................................. 24

Awards/Prizes from Employers ...................................................................................................................................... 24

National Service Education Awards and Income from Peace Corps ............................................................................. 25

Golden Parachute Agreement Payments ....................................................................................................................... 25

Supplemental Wage Payments ...................................................................................................................................... 25

Pennsylvania Taxation of Stock Options ......................................................................................................................... 25

Federal and Pennsylvania Personal Income Tax Differences Relating to Stock Options .............................................. 25

Pennsylvania Taxation of Stock Options ........................................................................................................................ 26

Substantial Restrictions/Constructive Receipt for Pennsylvania Income Tax ................................................................ 26

Stock Options Earned while a Pennsylvania Resident, but Exercised while a Nonresident .......................................... 26

Pennsylvania Taxation of Cafeteria Plans ........................................................................................................................ 32

Overview – Federal/Pennsylvania Differences ............................................................................................................... 32

Pennsylvania Taxable Benefits ...................................................................................................................................... 33

Pennsylvania Nontaxable Benefits ................................................................................................................................. 33

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 2

of 65 www.revenue.pa.gov

Pennsyvania Taxation of Fringe Benefits ......................................................................................................................... 33

Federal Income Tax – Overview ..................................................................................................................................... 33

Pennsylvania Nontaxable – Overview ............................................................................................................................ 33

Employee Expenses for Pennsyvania .............................................................................................................................. 34

Historical Background ..................................................................................................................................................... 34

Overview Federal/Pennsylvania Differences .................................................................................................................. 34

Accountable Plan ............................................................................................................................................................ 34

Unreimbursed Employee Expenses on PA-40 Schedule UE, Allowable Employee Business Expenses ...................... 34

Examples of Allowable Expenses and the Limitations on Those Expenses .................................................................. 35

Nonallowable Expenses ................................................................................................................................................. 38

Nonresidents and Part-Year Residents .......................................................................................................................... 38

Multiple Employers ......................................................................................................................................................... 39

Reimbursements ............................................................................................................................................................. 39

Statutory Employees ....................................................................................................................................................... 39

Allowance for Clothing .................................................................................................................................................... 40

Examples ........................................................................................................................................................................ 40

Critical Information on Schedule UE ............................................................................................................................... 41

Records and Records Retention .................................................................................................................................... 41

Damage Awards .................................................................................................................................................................. 41

Overview – Federal/Pennsylvania Differences ............................................................................................................... 41

Summary of Pennsylvania Personal Income Tax Treatment of Specific Damage Awards ............................................ 41

Damage Awards for Lost Profits for Pennsylvania Personal Income Tax ...................................................................... 41

Damage Awards for Return of Capital for Pennsylvania Personal Income Tax ............................................................. 41

Pennsylvania Treatment of Legal Expenses .................................................................................................................. 42

Guaranteed Payments ........................................................................................................................................................ 42

Gross Non-Employee Compensation ............................................................................................................................... 42

Honorarium ..................................................................................................................................................................... 42

Executor or Administrator Fees ...................................................................................................................................... 42

Expert Witness Fees

....................................................................................................................................................... 42

Jury Fees ........................................................................................................................................................................ 42

Director Fees .................................................................................................................................................................. 42

Foster Care Provider Payments ..................................................................................................................................... 42

Other Miscellaneous Compensation ............................................................................................................................... 43

Federal Form 1099–MISC Income ................................................................................................................................. 43

Pennsylvania Personal Income Tax Treatment of Household Employees .................................................................... 43

Nonresident – Allocation of Pennsylvania Compensation ............................................................................................. 43

Compensation from Sources within Pennsylvania ......................................................................................................... 43

Commissions .................................................................................................................................................................. 43

Compensation Based Upon Years of Continued Service............................................................................................... 43

Compensation Paid on a Daily, Weekly, Biweekly, Semimonthly, Monthly, Quarterly, Semiannual or Annual Basis ... 44

Miscellaneous Compensation ......................................................................................................................................... 44

Prepaid Compensation ................................................................................................................................................... 44

Working Day Explained .................................................................................................................................................. 44

Working Days Employed within Pennsylvania Explained ............................................................................................... 45

The Convenience of the Employer Doctrine ................................................................................................................... 45

Payment Accrual Period Explained ................................................................................................................................ 45

Retirement Income ......................................................................................................................................................... 46

Discharge of Indebtedness ................................................................................................................................................ 46

Discharge of Indebtedness Income for Pennsylvania Personal Income Tax ................................................................. 46

When Is It Taxable .......................................................................................................................................................... 46

Class of income .............................................................................................................................................................. 46

Annuities .............................................................................................................................................................................. 46

Employer Annuity Plan ................................................................................................................................................... 46

Nonqualified Annuities .................................................................................................................................................... 47

Non-Employee Benefit Annuities .................................................................................................................................... 48

Life Insurance Annuity Contracts .................................................................................................................................... 48

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 3

of 65 www.revenue.pa.gov

Pennsylvania Eligible Retirement Plans ........................................................................................................................... 48

Criteria for A Plan to Qualify as an Eligible Pennsylvania Retirement Plan ................................................................... 48

Contributions to a Retirement Plan ................................................................................................................................. 49

Exempt Distributions from an Employer Provided Retirement Plan ............................................................................... 49

Plan other than Employer Provided Retirement Plan ..................................................................................................... 49

Early Distributions from an Eligible Pennsylvania Retirement Plan ............................................................................... 49

Distributions to Beneficiaries and Rollovers ................................................................................................................... 49

Treatment of Investment Earnings by an Eligible Pennsylvania Retirement Trust Fund ............................................ 49

Employee Stock Ownership Plans ................................................................................................................................. 49

Nonqualified Deferred Compensation Plans .................................................................................................................... 50

Profit-Sharing Plans ............................................................................................................................................................ 50

Severance Pay ............................................................................................................................................................... 50

Taxable Employee Contributions .................................................................................................................................... 50

Non-Taxable Employer Contributions ............................................................................................................................. 50

Distributions .................................................................................................................................................................... 50

Employer Welfare Plans ..................................................................................................................................................... 50

Taxation of Certain Benefits for Pennsylvania Personal Income Tax ............................................................................ 50

Employee Contributions – Taxable ................................................................................................................................. 51

Pennsylvania Taxation of Contributions to and Distributions from Eligible Pennsylvania Retirement Plans ................. 51

Federal Form 1099-R Reconciliation for Pennsylvania Personal Income Tax .............................................................. 53

Code 1 & 2 Early Distribution ......................................................................................................................................... 53

Code 3 or 4 Death/Disability Distribution ........................................................................................................................ 54

Code 7 Normal Distribution ............................................................................................................................................ 54

Code G or H Rollover ..................................................................................................................................................... 54

Boxes 8 or 9b .................................................................................................................................................................. 54

Boxes 10 and 11 ............................................................................................................................................................. 54

IRA Distributions (60 day Rollover Rule) ........................................................................................................................ 54

Federal Form 1099-R Reconciliation for Pennsylvania Personal In

come Tax ............................................................... 55

Property Transferred in Connection with the Performance of Services ....................................................................... 62

Certain Transfers upon Death ........................................................................................................................................ 62

Forfeiture after Substantial Vesting ................................................................................................................................ 62

Election to Include in Gross Income in Year of Transfer ................................................................................................ 62

Unstated Interest Payments ........................................................................................................................................... 63

Sales which May Give Rise to Suit under Section 16(b) of the Securities Exchange Act of 1934................................. 63

Special Rule for Certain Accounting Rules .................................................................................................................... 63

Taxation of Nonqualified Stock Options ......................................................................................................................... 63

Applicability of Section and Transitional Rules ............................................................................................................... 64

Statutory Stock Options .................................................................................................................................................. 64

Secular Trust Arrangements ........................................................................................................................................... 64

Employer Annuity Plans ................................................................................................................................................. 65

Cross Reference ............................................................................................................................................................. 65

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 4

of 65 www.revenue.pa.gov

OVERVIEW

Definition of Gross Employee Compensation for Pennsylvania Personal Income Tax

For Pennsylvania personal income tax purposes, the term “compensation” includes salaries, wages, commissions,

bonuses and incentive payments whether based on profits or otherwise, fees, tips and similar remuneration received

for services rendered as an employee or casual employee, agent or officer of an individual, partnership, business or

nonprofit corporation, or government agency, whether directly or through an agent, and whether in cash or in property.

Compensation paid in any medium other than cash is valued at its fair market value. Examples of a medium other

than cash include, but are not limited to:

Foreign currency;

Check or other negotiable instruments;

Freely transferable readily marketable obligations or other cash equivalents;

Property interests;

Below-market-rate loans; and/or

Discharge of liabilities.

Taxable employee compensation is not limited to remuneration received for positive action, remuneration that is

contractually enforceable or remuneration paid directly by the employer. Taxable employee compensation may also

include:

Tips and other amounts, over which the employer does not have the control, receipt, custody, or payment;

A sum in excess of salary given an athlete for signing with a team or other bonus;

Payments to current and former employees for a covenant not to compete; and/or

Back or front pay for a period of time during which an individual was wrongfully separated from his job and

front pay paid in lieu of reinstatement.

Certain items are excluded from the definition of taxable compensation. These items include, among other things:

Income received for active duty military service outside the Commonwealth of Pennsylvania;

Income received for active State duty for emergency within or outside the Commonwealth of Pennsylvania;

Periodic payments for sickness and disability other than regular wages received during a period of sickness or

disability;

Disability, retirement or other payments arising under workmen's compensation acts, occupational disease

acts and similar legislation by any government;

Payments commonly recognized as old age or retirement benefits paid to persons retired from service after

reaching a specific age or after a stated period of employment;

Public assistance or unemployment compensation payments by any governmental agency;

Payments to reimburse actual expenses;

Personal use of an employer's owned or leased property or of employer-provided services; or

Compensation does not include guaranteed payments to a partner even if they are for services.

The lists above are not exhaustive. Refer to the sections that follow for detailed rules regarding specific items of

compensation.

Income Items Taxable as Federal Compensation Compared to Income Items Taxable as Pennsylvania

Compensation

There are significant differences between Pennsylvania personal income tax (PA PIT) and federal income tax. Certain

income items that are not taxable for federal income tax are taxable for Pennsylvania personal income tax. Certain

income items that are taxable for federal income tax are not taxable for Pennsylvania personal income tax.

Please refer to the following tables for differences between federal and Pennsylvania:

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 5

of 65 www.revenue.pa.gov

Income Items Always Taxable as Pennsylvania Compensation illustrates what items are included in

compensation for Pennsylvania personal income tax purposes.

Income Items Never Taxable as Pennsylvania Compensation illustrates what items are not included in

compensation for Pennsylvania personal income tax purposes.

Income Items Taxable as Pennsylvania Compensation Based on Facts and Circumstances on the following

pages for descriptions of these items illustrates what items may be taxable based on the facts and

circumstances of the item for Pennsylvania personal income tax purposes.

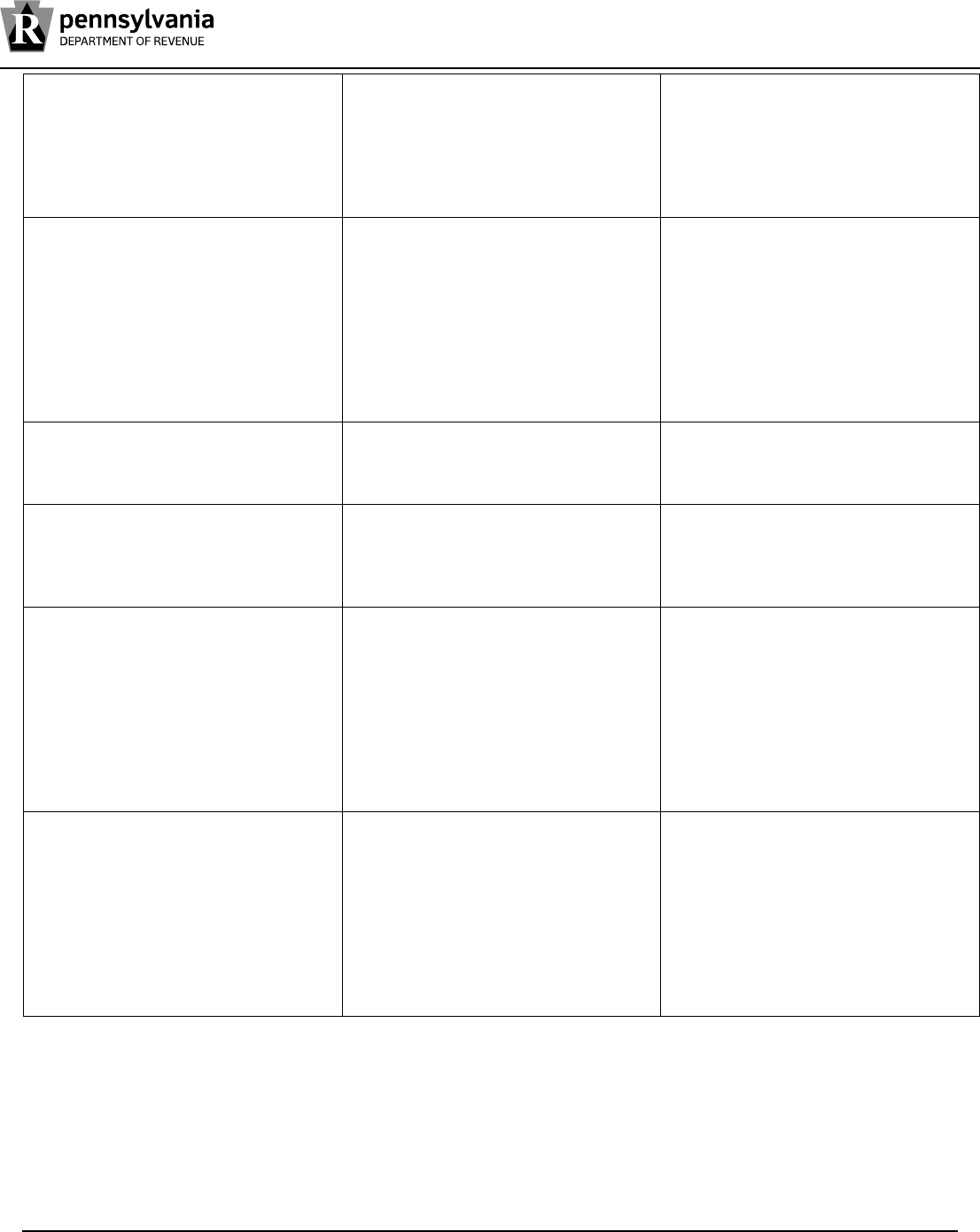

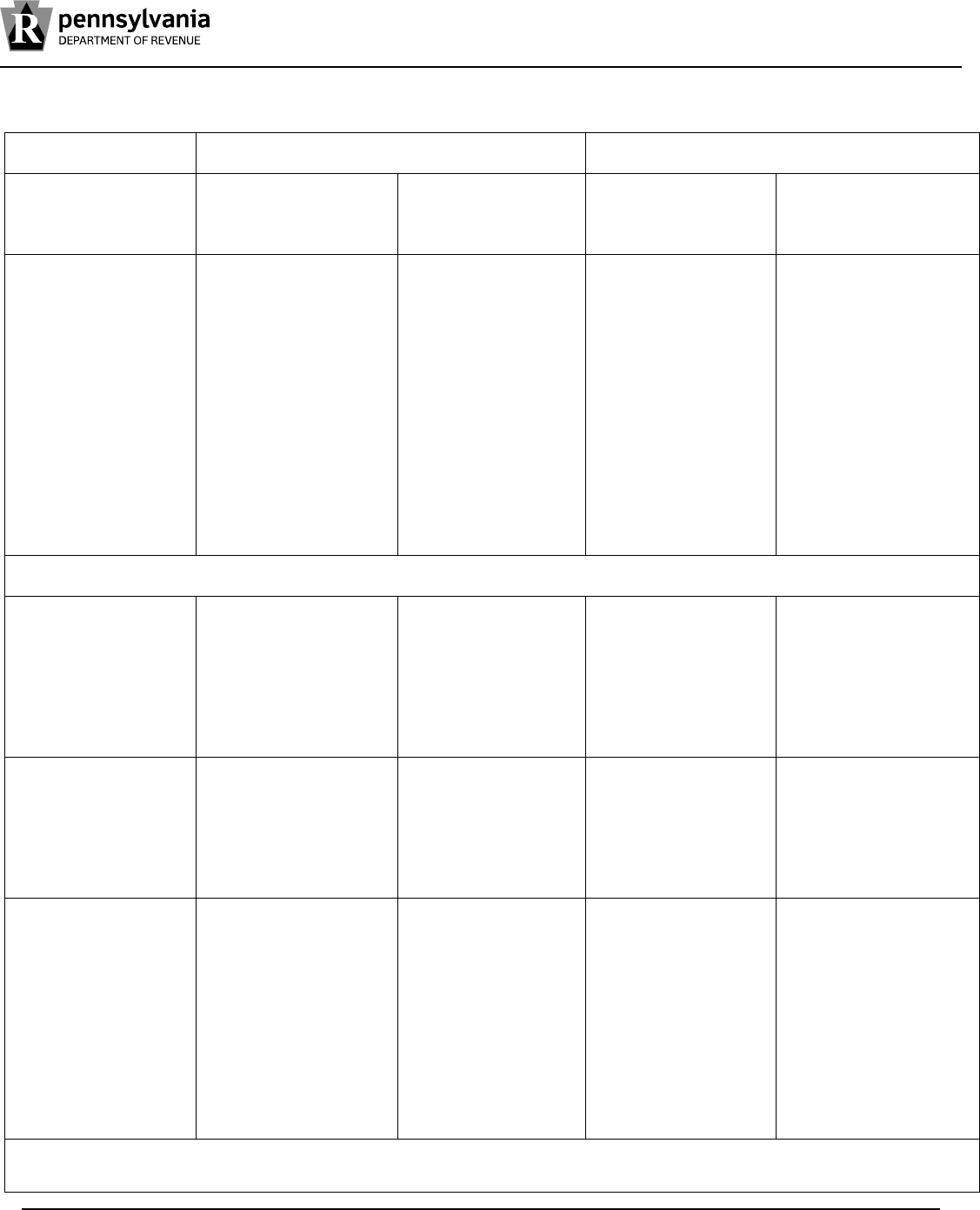

Income Items Always Taxable as Pennsylvania Compensation

Type of Compensation

Salaries

Wages

Tips received directly by the employee or through his or her employer

Gratuities

Commissions

Bonuses

Incentive pa

y

ments

Vacation/holiday pay

Termination/severance pay

Payment incentives for early retirement

Reimbursements and allowances in excess of allowable business expenses

Directors' fees (will constitute PA-40 Schedule C income if one’s profession is a director for multiple organizations or

corporations)

Jury fees

Witness fees (will constitute PA-40 Schedule C income if testifying as an expert in a field which is considered one’s line of

business)

Eligible reimbursed moving expenses in excess of allowable expenses on PA-40 Schedule UE

Honoraria

(

will constitute P

A

-40 Schedule C income if one’s profession is bein

g

a professional speaker

)

Executor's or administrator's fees (will constitute PA-40 Schedule C income if one’s profession is being an executor or

administrator)

Covenant not-to-compete or payments received as consideration for refraining from the performance of services

Proceeds from an employee stock ownership plan to extent of excess computed under cost-recovery method

Cash allowances for rent, utilities, or other expenses received b

y

ministers

Reimbursements made by an employer for dependent care, legal services, or other personal services

National Service Education Awards

Income from Peace Corps, VISTA Job Corps and Americorp

Household employees pay

Employee contributions to an eligible Pennsylvania retirement plan and or contributions to a qualified deferred

compensation plan

Distributions from a nonqualified deferred compensation plan (unless the deferral was previously taxed under rules prior

to Act 40 of 2005)

Medicare waiver payments or difficulty of care payments

Student loan debt for

g

iveness/pa

y

ment if provided as emplo

y

ment incentive

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 6

of 65 www.revenue.pa.gov

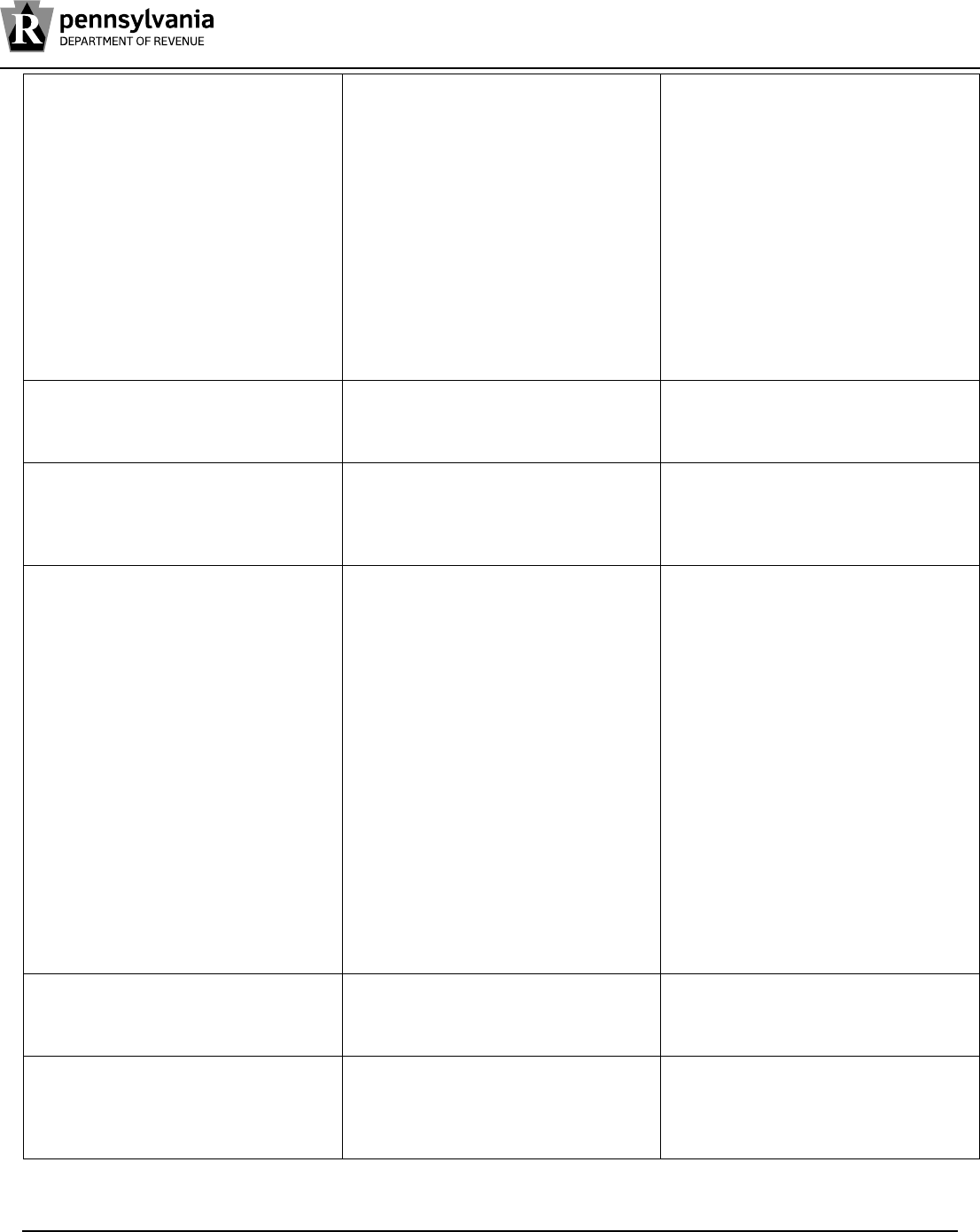

Income Items Never Taxable as PA Compensation

*Regarding what plans qualify as "eligible Pennsylvania retirement plans," the fact that a plan is a qualified plan for federal

income tax is not controlling for Pennsylvania personal income tax purposes.

Type of Compensation

Federal active-duty pay earned outside Pennsylvania

GI Bill benefits including tuition and living expenses

Alimony

Child suppor

t

Income in respect of a decedent

Inheritance

Social Security

Railroad retirement benefits

Public assistance

Unemployment compensation

Occupational Disease Act benefits (if included on the W–2 form attach explanation)

Meals and lodging provided to an employee by the employer

Personal use of employer-owned or leased property and/or services, at no cost or at a reduced cost. Personal use of

company automobile, airplane or other employer-owned or leased property. These amounts are not taxable fringe

benefits for Pennsylvania personal income tax

Employer-provided parking facilities. These amounts are nontaxable fringe benefits.

Employer-provided professional services paid for directly by the employer. These are nontaxable fringe benefits.

Premiums paid by an employer for group term life insurance (no limit)

Rental value of parsonage owned by the congregation and required to be occupied by the cleric

Foster care

Emplo

y

er-paid

g

roup term life insurance premiums

Amounts received for permanent loss of body function, disfigurement, or reimbursed medical expense

Disability payments paid by employer arising under occupational disease acts or other legislation

Strike benefits

Life insurance proceeds or settlements

Employee contributions or deferrals to a nonqualified deferred compensation plan (all IRC Section 409A plans and some

IRC Section 457b plans where the deferrals made are subject to a substantial risk of forfeiture or the employee deferrals

made to the plan are not funded by the employer)

The State Employees’ Retirement System, the Pennsylvania School Employees’ Retirement System, the Pennsylvania

Municipal Employees Retirement System and the U.S. Civil Service Commission Retirement Disability Plan are eligible

Pennsylvania retirement plans and all distributions are exempt from Pennsylvania personal income tax. Retired or

retainer pay of a member or former member of a uniform service calculated under Chapter 71 of Title 10, U.S. Code as

amended is also exempt from Pennsylvania personal income tax

Distributions from eligible Pennsylvania retirement plans after retirement age

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 7

of 65 www.revenue.pa.gov

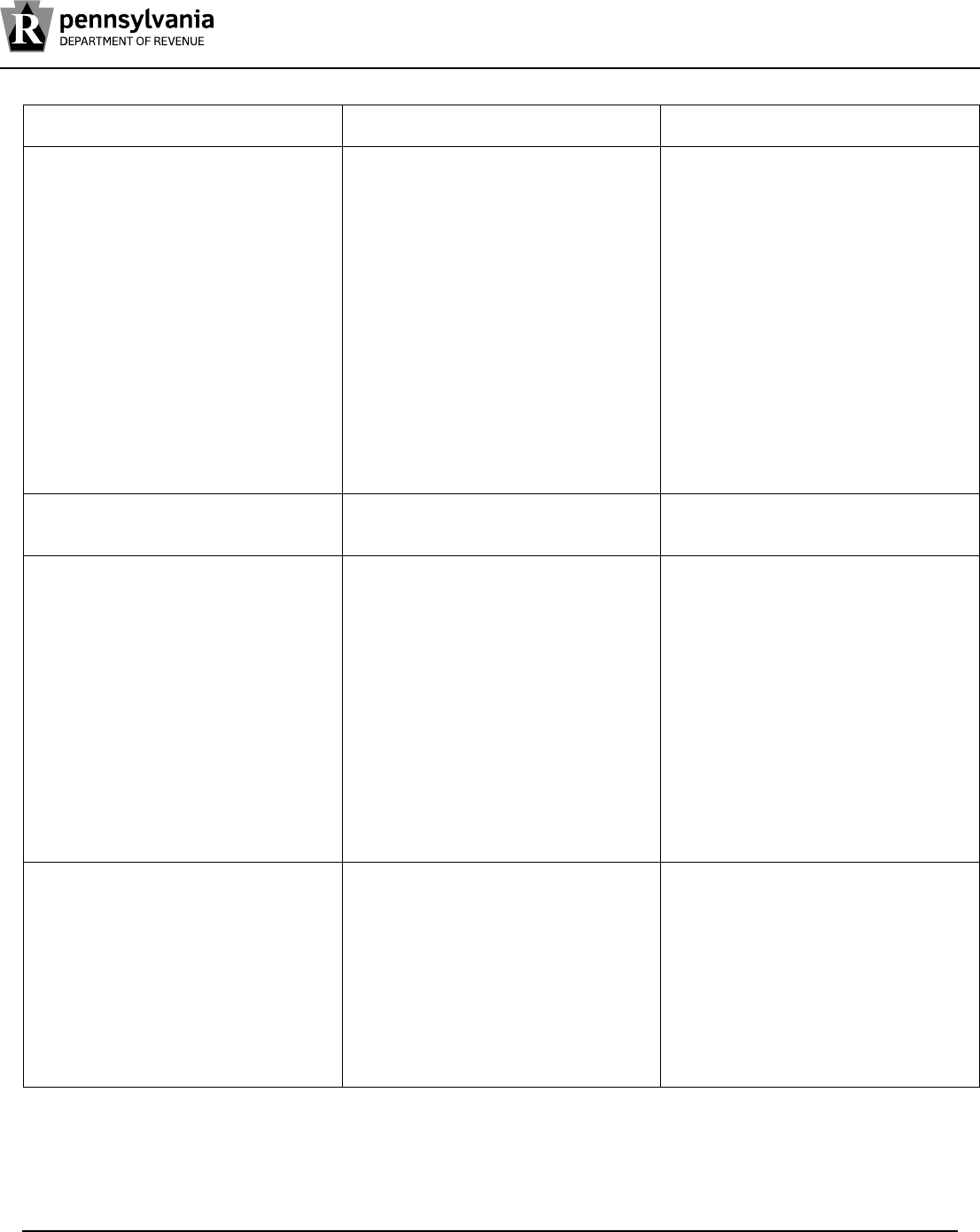

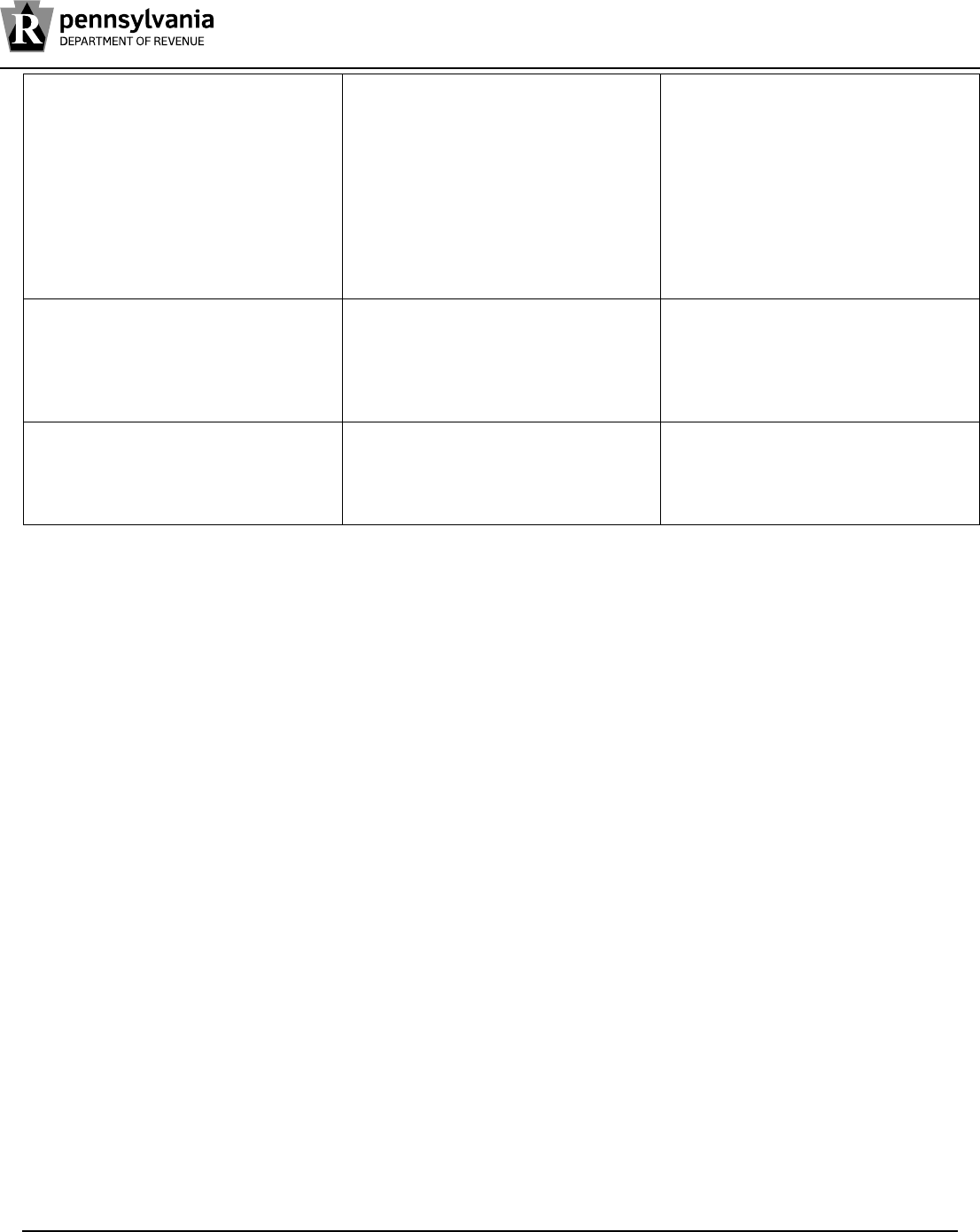

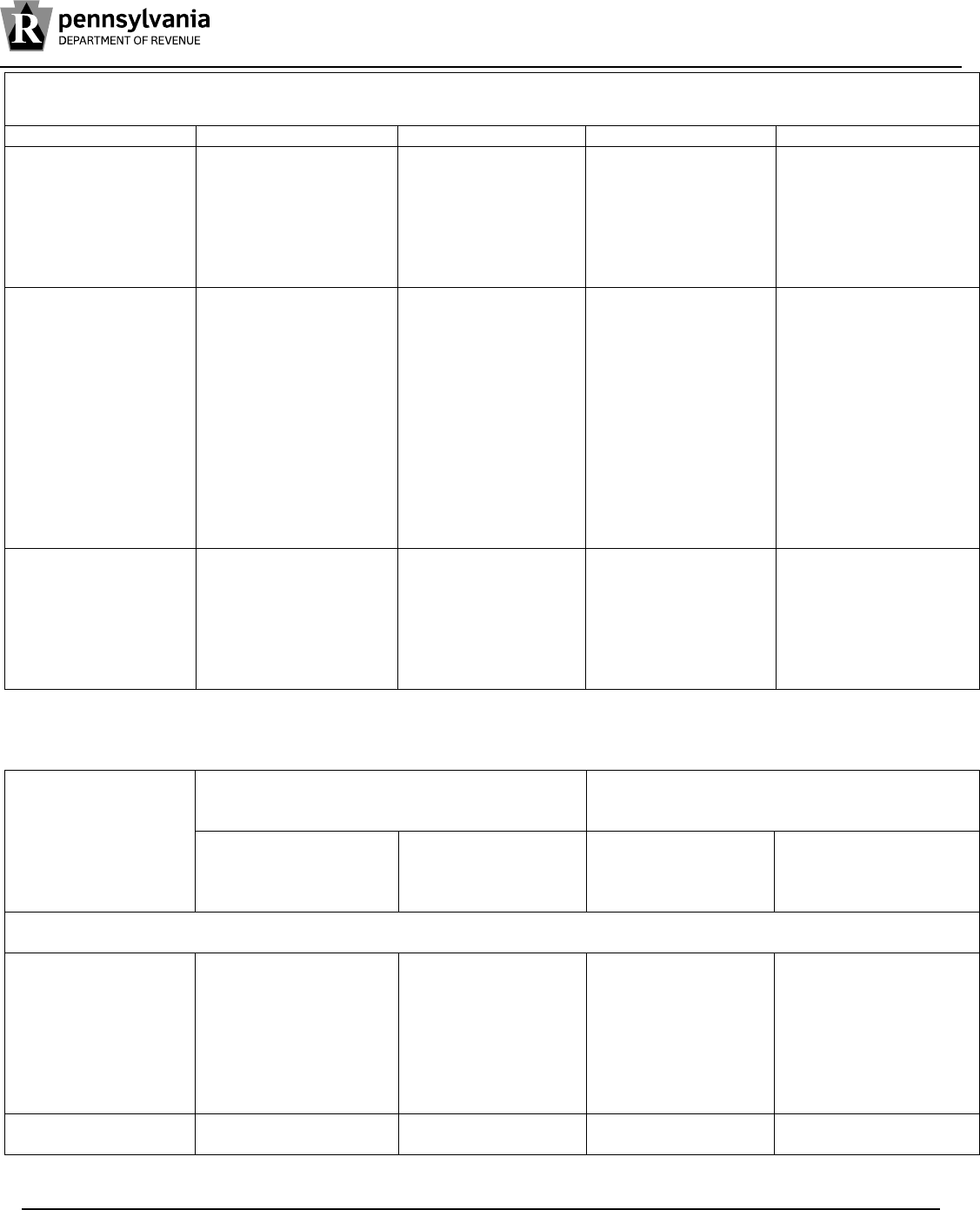

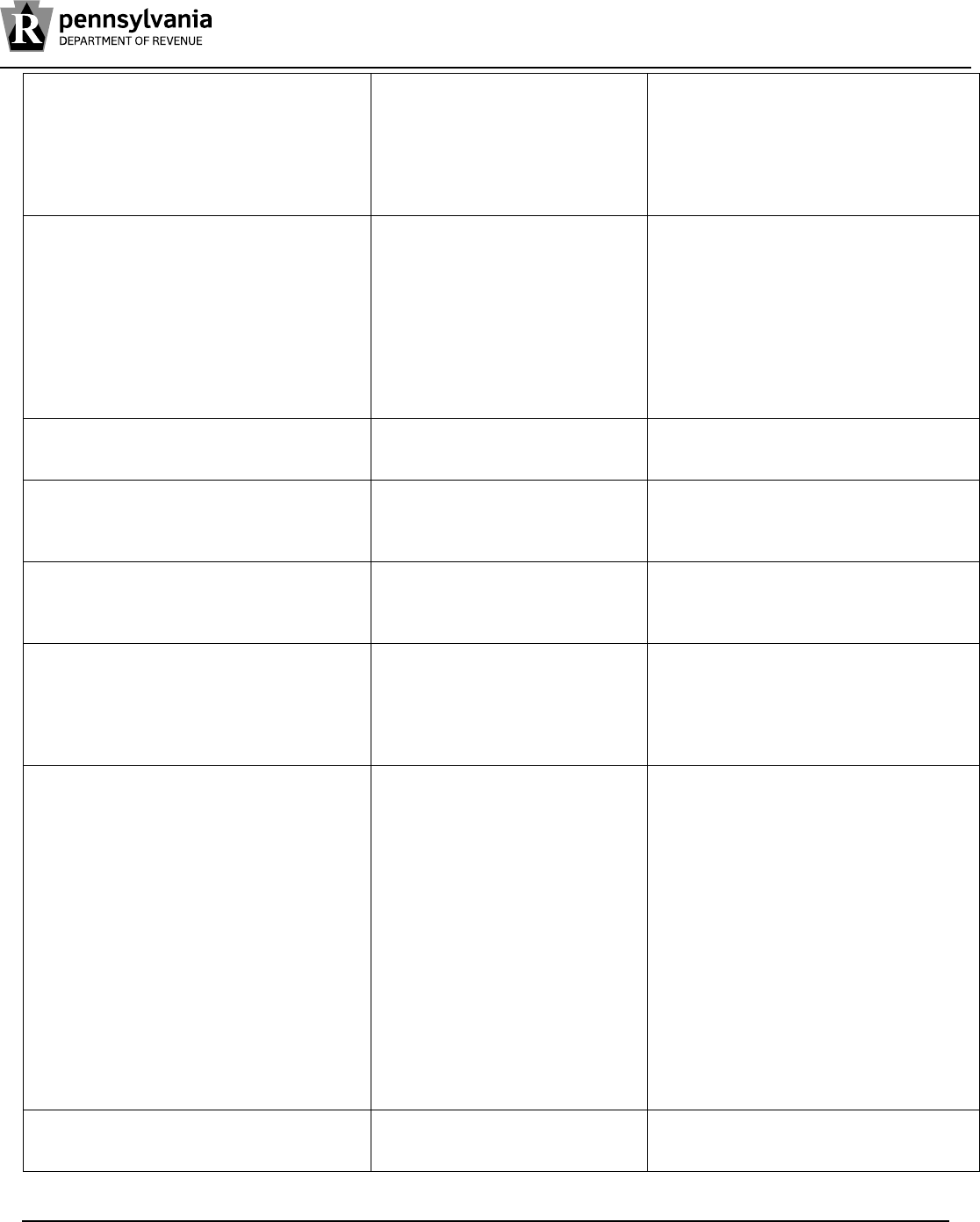

Income Items Taxable as Pennsylvania Compensation Based on Facts and Circumstances

Type of

Compensation

Taxable

Description

Non–Taxable

Description

Sick pay, sick leave Sick pay and sick leave are taxable

compensation when representing

regular wages. The employer must

include them as compensation and

withhold Pennsylvania tax. Request

REV–634, Employee Fringe Benefits

and Wage/Salary Supplements.

Payments, not representing regular

wages, including payments made by

third party insurers for sickness or

disability, are not taxable income for

Pennsylvania purposes.

Your employer should not include

periodic payments for sickness or

disability in Box 16 of your federal

Form W–2.

If your employer includes this income

and withholds Pennsylvania tax, you

must obtain and submit a corrected

federal Form W–2 or a statement

from your employer explaining the

error.

Disability benefit payments, including

payments made by third party

insurers for sickness or disabilit

y

Taxable if paid by employer. Nontaxable if paid by third-party

insurer.

A premature withdrawal from a

regular IRA or Roth IRA

A premature withdrawal from a

regular IRA or Roth IRA is taxable

compensation to the extent that the

taxpayer receives an amount that

exceeds his or her previously taxed

contributions. The cost-recovery

method of accounting must be used

to determine the taxable portion

unless timely rolled over into an

eligible Pennsylvania retirement plan.

Please consult your summary plan

description or plan administrator.

Payments received under worker’s

compensation acts, occupational

disease acts, or similar legislation,

including payments for injuries you

received while working, and damages

received, whether by suit or

otherwise, for personal injuries

(unless one is required to pay these

monies back to the employer and

receives re

g

ular salar

y

in return

)

Taxable when the employee must

turn over the worker’s compensation

payments to the employer in order to

receive his or her regular salary in

return. The employee does not report

the worker’s compensation payments,

but does report the full amount of his

or her regular salary.

All other payments received under

workers compensation acts is not

taxable compensation.

Occupational disease acts are not

taxable.

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 8

of 65 www.revenue.pa.gov

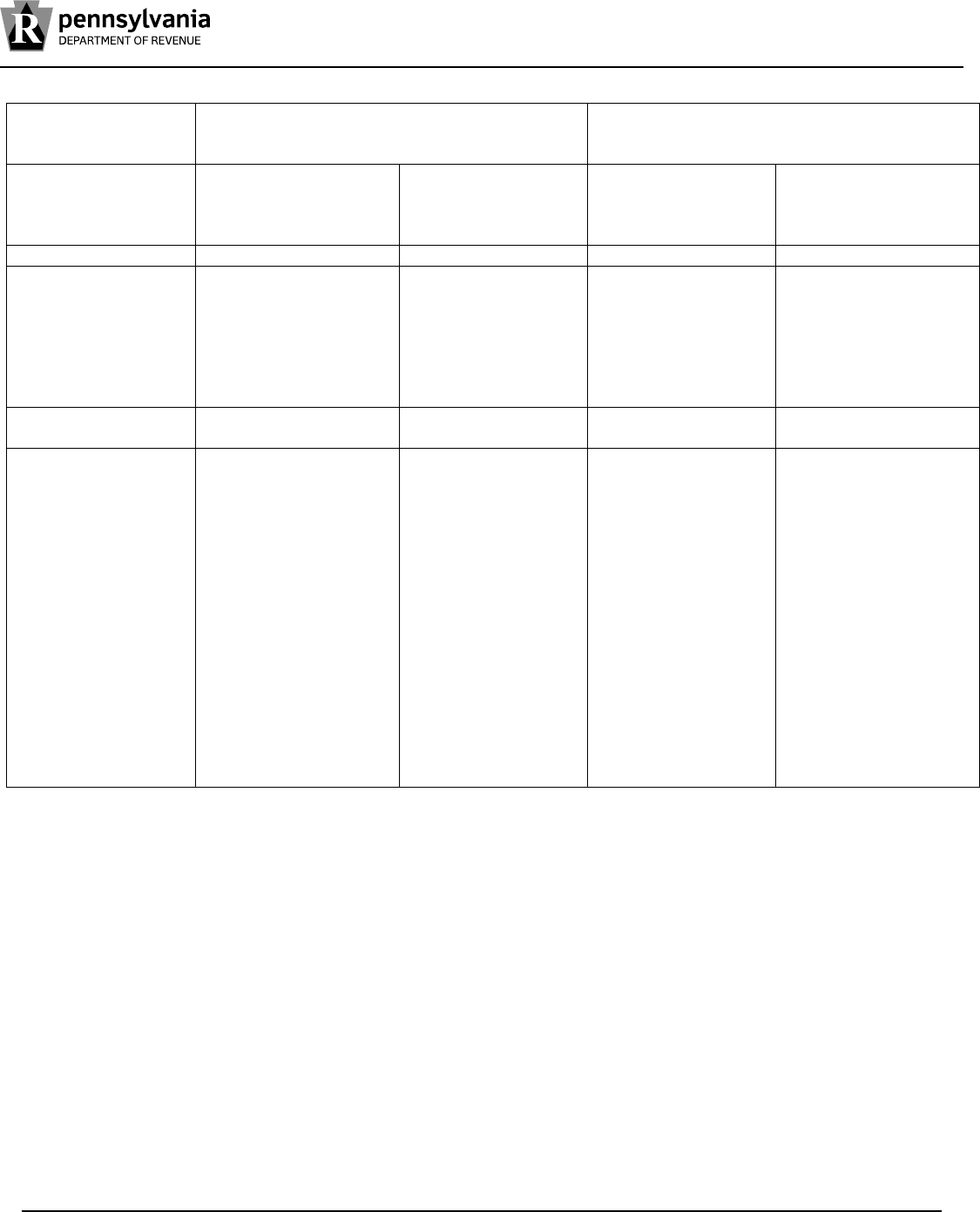

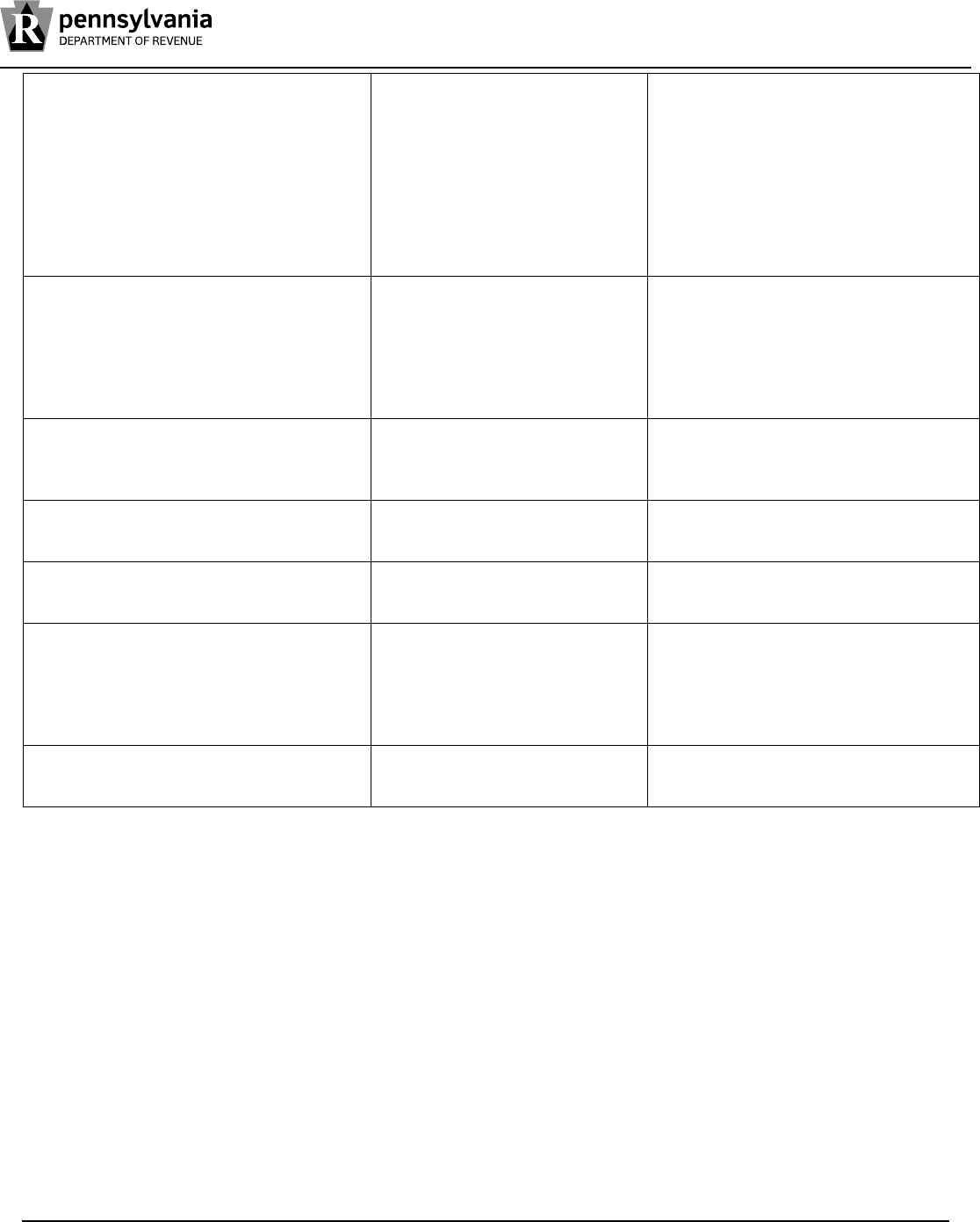

Scholarships or fellowships and

stipends

The recipient is required to apply the

skill and training to advance research,

creative work or some other project or

activity.

Made on the basis of need or

academic achievement, is not taxable

if awarded to encourage or allow the

recipient to further his or her

academic achievement is not taxable

compensation.

Employer-provided fringe benefits

Non-excludible fringes

Refer to Pennsylvania Taxation of

Fringe Benefits for a list of non-

excludable fringes including an option

to receive cash or reimbursement.

Excludible fringes (e.g. personal use

of an employer’s owned or leased

property and/or services, at no cost or

at a reduced cost, and using your

employer’s dependent care facilities)

is not taxable compensation.

Refer to Pennsylvania Taxation of

Frin

g

e Benefits.

Damage awards - Delayed damages

received in connection with a court

judgment or settlement

Delay damages received in

connection with a court judgment or

settlement is taxable compensation.

Federal-taxable punitive damages

awarded and settlements from

personal injury

Federal-taxable punitive damages

received for personal physical injury

or physical sickness, whether

received by suit or by settlement is

not taxable compensation.

Damages, awards, and settlements

from personal injury or sickness

Damage awards and settlements from

personal injury or sickness if pain and

suffering, emotional distress, or

another non-economic element was

or would have been a significant

evidentiary factor in determining the

amount of the taxpayer’s damages is

not taxable compensation.

Refer to Dama

g

e Awards.

All other damage awards Other damage awards that are also

taxable e.g. damage awards and

settlements to the extent that the

payments represent back wages or

other uncollected entitlement to

Pennsylvania-taxable incomes,

damage awards for lost profits, etc.) is

taxable compensation. Report on PA-

40 Schedule W-2S, Wage Statement

Summar

y

.

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 9

of 65 www.revenue.pa.gov

Television Show winnings

A prize awarded to a participant in a

game or “reality” show is considered

non-employee compensation for

Pennsylvania personal income tax

purposes.

The value of the prize should be

reported on PA-40 Schedule W-2S,

Wage Statement Summary.

If the prize is taxed in another state,

then the taxpayer can use PA-40

Schedule G–L to claim a resident

credit for taxes paid to other states.

Awards

Awards given in recognition for past

or future service are taxable

compensation.

All awards not given in recognition for

past or future service are not taxable

compensation.

Gifts

Taxable if gift is a transfer of cash or

property in payment for past or

present services or as an inducement

to perform future services.

Gifts made from detached or

disinterested generosity is not taxable

compensation.

Tuition assistance or educational

benefits unless the training or

education is either:

Required by law or regulation; or

Required of the employee by the

employer in order for the

employee to retain the skills

necessary for his or her present

position. If the course, degree

program, or training is designed to

enable the employee to enter a

new field or profession or to

obtain a promotion, the

reimbursement is taxable.

If employer reimburses employees for

education cost, then the

reimbursement is fully taxable and the

employee may deduct only those

amounts directly related to business

expenses allowed on PA-40 Schedule

UE, Allowable Employee Business

Expenses, to determine taxable

compensation.

Employees of an institution of higher

learning that receive free or low–cost

education receive the tuition

assistance tax free for Pennsylvania

personal income tax purposes unless

they receive cash grants (for

themselves or their children) as

reimbursements for the tuition paid at

their institution of employment or any

other institution of higher learning.

Since Pennsylvania personal income

tax has no distinction regarding

taxability with respect to the amount

of the benefits received for highly

compensated employees, these

benefits would also be considered tax

free for Pennsylvania personal

income tax purposes unless a cash

g

rant is received.

Employer contributions to eligible

Pennsylvania retirement plans and

non-qualifying deferred compensation

plans

Not taxable compensation

Employee contributions to non-

qualifying deferred compensation

plans

Refer to PA PIT Bulletin 2005–03 -

Deferred Compensation Under

Nonqualified Plans.

Refer to PA PIT Bulletin 2005–03 -

Deferred Compensation Under

Nonqualified Plans.

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 10

of 65 www.revenue.pa.gov

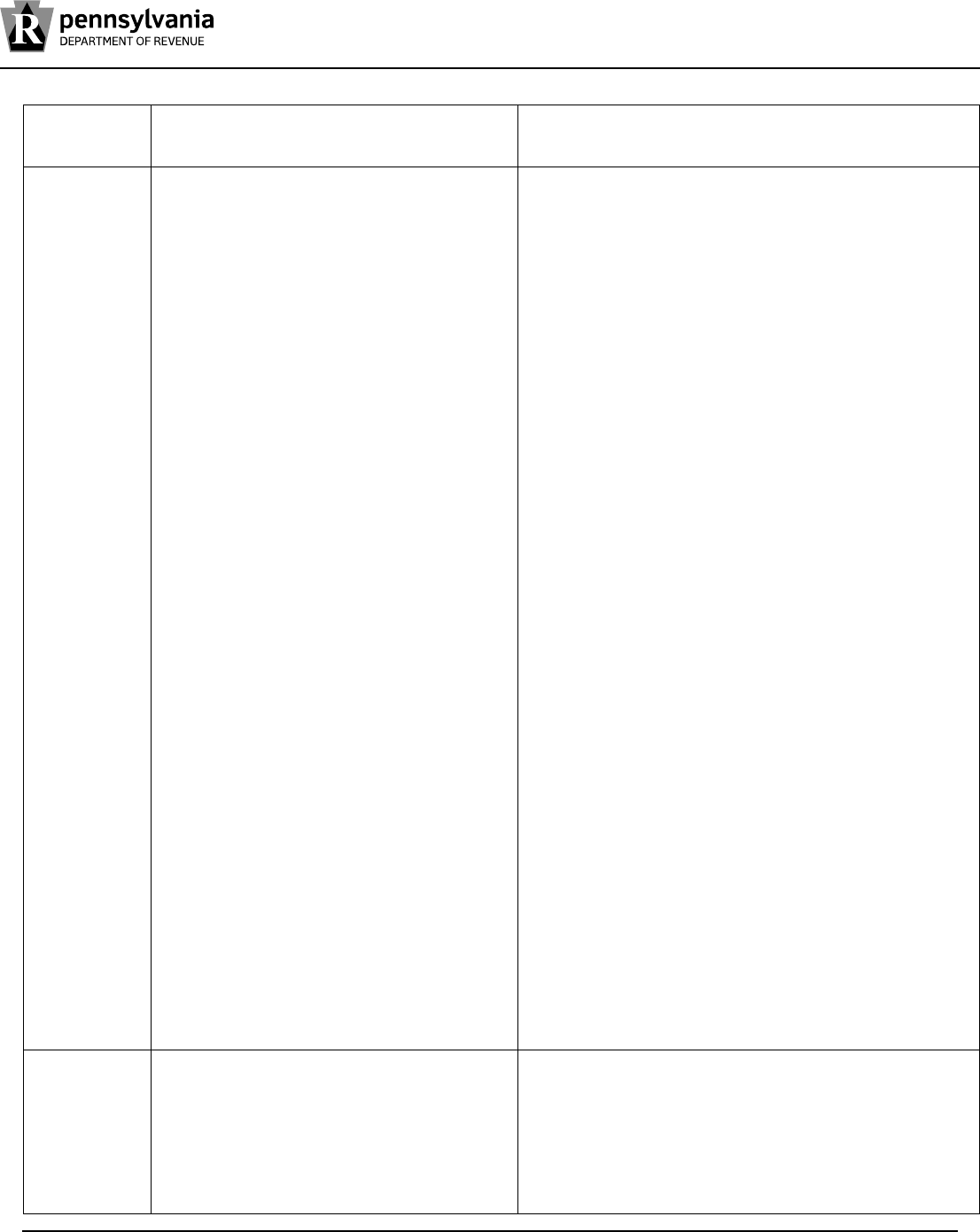

Distributions from eligible

Pennsylvania retirement plans and

non-qualifying deferred compensation

plans

Refer to PA PIT Bulletin 2005–03 -

Deferred Compensation Under

Nonqualified Plans and PA PIT

Bulletin 2005-05 - Qualified Employer

Plans.

Act 2005–40 established the general

rule that distributions from plans

described in IRC §409A(d)(1)

attributable to an elective deferral of

income or the income on any elective

deferral of income are taxable.

Contributions previously taxed using

the cost recovery method are not

taxable.

Federal or state active-duty pay inside

Pennsylvania for armed forces

personnel

If related to active duty at a base

located in Pennsylvania by

Pennsylvania resident military

personnel or for non-emergency

active-duty pay by Pennsylvania

National Guard reservists

Active duty pay for nonresident

taxpayers

Emergency active-duty pay under 35

Pa. C.S. §§ 7601-7604.

Federal active duty pay for

commissioned corps of the U.S.

Public Health Service or the National

Oceanic and Atmospheric

A

dministration

Pennsylvania resident taxpayers are

subject to tax on their active duty pay

regardless of where earned

Active duty pay for nonresident

taxpayers

Costs, Expenses, and Deductions Against Gross Compensation

No Deduction Against Gross Compensation

For individuals, Pennsylvania law does not exempt or exclude from income, or allow a deduction for, any

personal expenses, federal itemized deductions, or federal standard deductions. Pennsylvania only allows

direct unreimbursed employee business expenses and other direct costs to earn, receive, or realize income.

Exception - Unreimbursed Employee Expenses

Allowable employee business expenses for Pennsylvania purposes are similar to, but not exactly the same

as, expenses for federal purposes. Refer to the section below for guidance regarding unreimbursed employee

business expenses. Pennsylvania does not allow amounts of business expenses over and above the amount

reimbursed by an employer if the employer provides a fixed-mileage allowance, daily, weekly, monthly or

yearly reimbursement unless the reimbursement is included in compensation (W-2 wages). These expenses

should not be reported on PA Schedule UE and reimbursements should not be included in compensation or

on the reimbursement line of PA Schedule UE by the taxpayer.

In addition, business expenses are not to be reported if a taxpayer accounts for allowable business expenses

to an employer and the employer reimburses the business expenses in the exact amount of the expenses.

Pennsylvania Resident Compensation

A Pennsylvania resident is taxed on all compensation received regardless of the source.

Nonresident Pennsylvania Compensation

A nonresident of Pennsylvania is taxed on Pennsylvania-sourced compensation.

PENNSYLVANIA COMPENSATION – GENERAL RULES

Pennsylvania Statutes, Regulations and Other Guidance

The sections of the Tax Reform Code of 1971 relating to compensation can be found at 72 P.S. §§ 7301(d),

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 11

of 65 www.revenue.pa.gov

7303(a)(1). The department has issued regulations to interpret the definition of compensation and its exclusions. The

regulations relating to compensation can be found at 61 Pa. Code § 101.6. The department also issues guidance in

the form of tax bulletins, letter rulings, and other materials with can be found on the department’s website.

W–2 Wage and Tax Statement (PA-40 Schedule W2–S, Wage Statement Summary)

A W-2 Wage and Tax Statement (federal Form W-2) and/or PA-40 Schedule W2–S, Wage Statement Summary, must

be submitted with the PA–40 Individual Income Tax Return, as evidence of compensation paid and taxes withheld by

an employer. When submitting federal Form W–2, the taxpayer must submit a separate form for each employer.

If submitting PA-40 Schedule W2–S, Wage Statement Summary, the taxpayer copies the information from each

federal Form W-2 over to the PA-40 Schedule W2–S. Refer to the Instructions for PA-40 Schedule W-2S, available on

the department’s website, for detailed guidance on completing the PA-40 Schedule W2-S or when to include federal

Form W-2.

Use Part B of PA-40 Schedule W2–S, Wage Statement Summary, to list all the sources of non-employee and other

compensation. Report Pennsylvania-taxable compensation and any Pennsylvania tax withheld from that income.

Include Pennsylvania-taxable amounts from federal Form 1099 that show pensions, retirement plan distributions,

executor fees, jury duty pay and other miscellaneous compensation.

Withholding Requirements

Under the Tax Reform Code of 1971, every “employer” who has an office or transacts business within Pennsylvania

must deduct and withhold Pennsylvania personal income tax from all wages paid to its resident employees,

regardless if the services are performed inside the state or outside. The same is required for all wages paid to

nonresidents for services rendered inside Pennsylvania unless the employee is a resident of a reciprocal state. 72

P.S. §7316.

Refer to PA Personal Income Tax Guide - Income Subject to Withholding, Estimated Payments, Penalties, Interest

and Other Additions for detailed guidance regading withholding requirements.

Reciprocal Compensation Agreements

Pennsylvania currently has reciprocal agreements with Indiana, Maryland, New Jersey, Ohio, Virginia, and West

Virginia. See note: Ohio Reciprocal Compensation Agreement.

Under these agreements, one state will not tax a resident of the other state on compensation that is subject to

employer withholding. These agreements apply to employee compensation only. They do not apply to income

reported as compensation when there is no federal withholding requirement, such as executor fees or director fees,

nor does it apply to any other class of income.

Residents of these states may file an REV-419, Employee’s Nonwithholding Application Certificate, if your employer

agrees to withhold and remit your resident state’s income tax so your employer can discontinue withholding

Pennsylvania personal income tax from your pay. Complete a new

REV-419 every year or when your personal or

financial situation changes. Photocopies of this form are acceptable.

If you are a Pennsylvania resident working in one of these states and your employer withheld the other state’s income

tax, you must file for a refund from that state. File early so you will have your refund before the due date for paying

your Pennsylvania tax liability.

If you are a resident of a reciprocal agreement state working or performing services in Pennsylvania and your

employer withheld Pennsylvania income tax, you may request a refund of the Pennsylvania tax. You report zero

taxable compensation on Line 1a and the Pennsylvania tax withheld on Line 13. Submit federal Form W–2 or a

photocopy and

a copy of the resident income tax return that you filed/will file with your resident state. Also, submit a statement

explaining that you are a resident of a reciprocal agreement state.

Note: Ohio Reciprocal Compensation Agreement: Commencing Jan. 1, 2004, remuneration paid to a

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 12

of 65 www.revenue.pa.gov

Pennsylvania resident twenty percent shareholder-employee of an Ohio S corporation for services

performed in Ohio is not covered by the Pennsylvania/Ohio Reciprocal Compensation Agreement and is

subject to tax in Ohio. Likewise, remuneration paid to an Ohio resident twenty percent shareholder –

employee of a Pennsylvania S corporation for services performed in Pennsylvania is not covered by the

Pennsylvania/Ohio Reciprocal Compensation Agreement and is subject to tax in Pennsylvania.

Federal/Pennsylvania Personal Income Tax Differences in Arriving at Box 16 Wages

Under Act 2005-40, the federal constructive receipt rules relating to nonqualified deferred compensation plans and

unfunded section 457 deferred compensation plans were made applicable for personal income tax purposes. If you

receive distributions of previously taxed elective deferrals, complete and include with your return the PA-40

W-2 RW, Reconciliation Worksheet. Refer to PA Personal Income Tax Guide - Tax Income Subject to Withholding,

Estimated Payments, Penalties, Interest and Other Additions.

CURRENT COMPENSATION – PENNSYLVANIA WAGES

Covenants Not-To-Compete or to Surrender a Right to Future Employment and Early Separation Incentive

Payments

Payments for Covenant Not-To-Compete

A "covenant not-to-compete" is generally treated as compensation if the covenant is a separately negotiable

item in the sales contract and it is intended as remuneration for non-competition. If the "covenant not-to-

compete" is actually for goodwill, or to insure the goodwill purchased, the covenant is an asset and includable

in the sales of business assets on PA-40 Schedule D, Sale, Exchange, or Disposition of Property.

Any payment received on account of a covenant not to compete constitutes taxable compensation. The

personal deliberate failure to act is expressly what has been bargained for. Such personal refraining to

engage in competition constitutes the rendition of personal services. The terminology “services rendered”

does not have to involve some positive action; just affirmatively refraining from doing something the person

has the right to do (Snap-Drape v. Commissioner, 105 T.C. 16, Ullman v. Commissioner, 29 T.C. 129).

Amounts Paid to Surrender a Right to Future Gainful Employment

Payments constitute taxable compensation for the relinquishment of the right to future employment as

opposed to deferred compensation attributable to prior employment if:

o The employment agreement secures for the employee a right to future gainful employment; and

o The only consideration given by the employee to obtain that right is the promise to work in the future.

o “Front pay” paid in lieu of reinstatement also constitutes taxable compensation.

Reduction In Force (“RIF”) Entitlements

When reducing their workforces, many employers offer temporary incentives for employees voluntarily to separate

from employment, including affording early retirement incentives that are available only for a limited period of time.

Many employers also afford involuntarily terminated employees extra pay. The extra pay may be paid in return for

agreements releasing legal claims to avoid the risk of RIF-related litigation. It may also be paid to help workers

transition to new employments or simply to part ways with employees on as amicable a basis as possible. Conversely,

employers or labor organizations may establish or maintain supplemental unemployment benefit plans (“SUB plan”) or

early retirement incentives that are not limited or temporary in nature. The taxation of such entitlements is explained

in this subsection.

Limited Plans of Termination

o Taxation

All actual or constructive distributions of cash or property upon dismissal, termination or severance of

employment (whether by retirement or otherwise) under a limited plan of termination constitutes

severance pay for personal income tax purposes.

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 13

of 65 www.revenue.pa.gov

o Limited Plan of Termination Explained

A limited plan of termination is an employee benefit plan that has one or more of the following attributes:

The plan, when begun, is scheduled to be complete on a certain date or upon the occurrence of one

or more specified events.

The number, percentage or class of employees whose services are to be terminated are specified in

advance of the employees’ terminations of service.

The plan is otherwise temporary or limited.

Supplemental Unemployment Benefits

o Taxation

Amounts paid from a supplemental unemployment benefits trust (“SUB trust”) that forms part of a

permanent, nondiscriminatory supplemental unemployment benefit plan (“SUB plan”) are excludible from

tax. However, amounts actually or constructive paid by an employer under a temporary, limited, unfunded

or discriminatory SUB plan constitute taxable severance pay.

o Sub Plan Explained

A supplemental unemployment benefit plan is a plan established or maintained by an employer or by an

employee organization, or by both, that has all of the following attributes:

No benefit is payable to, or can be taken, assigned, pledged or otherwise charged or dealt with by,

any plan participant except upon lay-off or involuntary separation from the employment of the

employer (whether or not the separation is temporary) resulting directly from a reduction in force,

plant closing, change in organizational structure, discontinuance of an operation, the participant’s

failure to meet or maintain standards of performance for the position due to inability to carry out the

responsibilities of the position, health, obsolescence, failure to meet the changed responsibilities of

the position or similar circumstance beyond the control of the participant.

No benefit is payable to, or can be taken, assigned, pledged or otherwise charged or dealt with by,

any plan participant if the participant either voluntarily separates from service or is separated or

discharged from service for any of the following reasons:

• Refusal to accept another position with reasonably comparable compensation.

• The commission of illegal acts.

• Insubordination, failure or refusal to comply with rules or regulations or similar acts within the

control of the participant.

o Voluntary Discontinuance of Plan

The voluntary discontinuance of a SUB plan within 3 years after it has taken effect, for any reason other

than business necessity, will be evidence that the plan was temporary and limited.

Early retirement enhancements

o General Rule

Any portion of a payment that is only available for a limited period of time as an early retirement “window

benefit” is taxable as severance pay.

o Exceptions

The added benefits payable to retired persons under Federally qualified defined benefit plans that are

attributable to:

Adding additional years to the employee’s actual age and/or actual service to reduce or eliminate the

effect of actuarial reductions in benefits on account of early retirement;

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 14

of 65 www.revenue.pa.gov

Crediting additional years of service to the employee in calculating benefits under a plan’s benefit

formula;

Offering social security “bridge payments” to plan participants in order to increase benefits under the

employer’s retirement benefit plan until they become eligible for social security benefits; or

Offering subsidized joint and survivor annuities constitute excludible retirement benefits, even if

offered only on a temporary or limited basis.

Clergy

If a member of the clergy is considered a "common law employee," the cleric's occupancy of a parsonage owned by

the congregation and provided for the convenience of the congregation is not taxable as compensation. Likewise, if

the congregation pays the costs of housing directly and not as a reimbursement to the clergy, the direct costs are not

taxable. All housing allowances provided by the congregation to clergy are taxable as compensation, as cash is

always taxable. The clergy may deduct directly related business expenses (such as the business use of the house)

allowed on PA-40 Schedule UE, Allowable Employee Business Expenses.

If a member of the clergy is not a "common law employee" and is a sole proprietor who offers his services in a market

place (i.e. to a nonexclusive, indefinite number of individuals or congregations), income is considered to be derived

from a business or profession and is reported on PA-40 Schedule C, Profit or (Loss) From Business or Profession.

Statutory Employees

For federal employment tax purposes, a “statutory employee” is defined as an individual that performs services for

remuneration for any person:

As an agent-driver or commission-driver engaged in distributing meat products, vegetable products, fruit

products, bakery products, beverages (other than milk), or laundry or dry-cleaning services, for his principal;

As a full-time life insurance salesman;

As a home worker performing work, according to specifications furnished by the person for whom the services

are performed, on materials or goods furnished by such person which are required to be returned to such

person or a person designated by him; or

As a traveling or city salesman, other than as an agent-driver or commission-driver, engaged upon a full-time

basis in the solicitation on behalf of, and the transmission to, his principal (except for side-line sales activities

on behalf of some other person) of orders from wholesalers, retailers, contractors, or operators of hotels,

restaurants, or other similar establishments for merchandise for resale or supplies for use in their business

operations; if the contract of service contemplates that substantially all of such services are to be performed

personally by such individual; except that an individual shall not be included in the term "employee" under the

provisions of this paragraph if such individual has a substantial investment in facilities used in connection with

the performance of such services (other than in facilities for transportation), or if the services are in the nature

of a single transaction, not part of a continuing relationship with the person for whom the services are

performed.

“Statutory employees” are independent contractors who are deemed “employees” for Federal employment tax

purposes because of special Federal statutory rules.

For Pennsylvania personal income tax purposes, individuals shall report all taxable remuneration they receive as a

statutory employee as compensation unless their activities constitute a business, profession, or other activity engaged

in as a commercial enterprise. See PA Personal Income Tax Guide - Net Income (Loss) from the Operation of a

Business, Profession, or Farm. Those expenses that are not reported in a specific part of the PA-40 Schedule UE,

Allowable Employee Business Expenses should be itemized and claimed in Part C, Miscellaneous Expenses.

However, if such expenses are extensive, a PA-40 Schedule C, Profit or (Loss) From Business or Profession may be

used in lieu of the PA-40 Schedule UE, Allowable Employee Business Expenses, provided that the PA wages shown

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 15

of 65 www.revenue.pa.gov

on the W-2 are included on Line 1a, Gross Compensation, and the expenses from Schedule C are included on Line 1b,

Unreimbursed Business Expenses.

Members of the U.S. Armed Forces or Foreign Service

Unless there is an intention to change his or her domicile by following military procedures to do so, a person generally

does not change his or her domicile by entering the U.S. Armed Forces. A person in the U.S. Armed Forces is not

precluded from acquiring a new domicile where his or her family is stationed. A person in the U.S. Armed Forces or

Foreign Service, or a person living in a foreign country for other than a temporary or transitory purpose while a lawful

permanent resident or citizen of that country, is treated as a domiciliary of that country if the person:

Is not an employee of the U.S., its agencies, or instrumentalities (including members of the Armed Forces and

career appointees in the U.S. Foreign Service); and

Does not hold an appointive office in the executive branch of the U.S. government.

However, special rules may apply if the employee or officer maintains a permanent place or abode there. An

individual who has a domicile in Pennsylvania is considered a nonresident if meeting all three of the requirements

listed under Pennsylvania Resident in PA Personal Income Tax Guide – Brief Overview and Filing Requirements for

Pennsylvania Personal Income Tax.

Resident Members of the U.S. Armed Forces

Military pay, including housing allowances, earned or received by a Pennsylvania resident member of the

U.S. Armed Forces (Army, Air Force, Navy, Marine Corps, and Coast Guard) while not on federal active duty

or not on federal active duty training, is fully taxable regardless of where the military service is performed.

Also, military pay, including housing allowances, earned or received by a Pennsylvania resident for military

service on federal active duty in Pennsylvania is subject to the Pennsylvania personal income tax, 72 P.S. §

7303(a)(1).

Full-time federal active duty military pay and federal active duty for training pay, including housing allowances,

earned or received by a Pennsylvania resident member of the U.S. Armed Forces while serving outside the

state is not taxable for Pennsylvania personal income tax purposes. However, a taxpayer must include such

compensation when determining eligibility for tax forgiveness on PA-40 Schedule SP.

While on federal active duty or federal active duty for training, any other income that the Pennsylvania

resident earns, receives, or realizes remains taxable for Pennsylvania personal income tax purposes.

The taxpayer has the burden of establishing that income received for military service outside the

commonwealth was earned while on federal active duty. The Department of Revenue requires a copy of the

military orders directing the taxpayer to federal active duty outside the commonwealth. Residents must file a

Pennsylvania personal income tax return and include their W–2 form(s) and copies of their military orders as

evidence of active duty military pay earned outside Pennsylvania.

Nonresident Members of the U.S. Armed Forces

Nonresident military personnel who are serving in Pennsylvania are exempt from Pennsylvania personal

income tax on their federal active duty military pay and housing allowances. However, they are subject to tax

on any other Pennsylvania –source income normally taxable to nonresidents. This includes duty pay that is

not active duty pay, such as weekend drills. Refer to Military Spouses Residency Relief Act.

Resident Members of the U. S. Armed Forces Reserves or National Guard

Pennsylvania resident Reservists and National Guardsmen ordered to active duty for training at a two-week

summer encampment pursuant to Title 10 or Title 73 of the U.S. Code are presumed to be on federal active

duty. For example, all income received for inactive duty while attending weekend drills is taxable.

Military pay, including housing allowances (this includes a reserve unit's two-week summer training) received

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 16

of 65 www.revenue.pa.gov

for service performed while on federal active duty is excludable from taxable compensation provided the

active duty training is performed outside the commonwealth. In addition, scholarships or remuneration

received by cadets and midshipmen at U.S. military academies are not taxable because none of these

academies are within Pennsylvania and such individuals are on federal active duty.

Beginning with tax years after Dec. 31, 2006, compensation earned by National Guard members on active

duty and responding to an emergency shall not be considered taxable income. Act 182 of 2006 amended the

Tax Reform Code to expand the definition of active duty military income to include income from the U.S.

government or the Commonwealth of Pennsylvania for active state duty for emergencies within or outside the

commonwealth. This addition includes duty ordered pursuant to 35 PA.C.S. Ch. 76 (relating to the Emergency

Management Assistance Compact).

When a civilian employer voluntarily either makes up the difference in a National Guardsman's or U.S.

Reservist's regular wages or continues at full pay for the Guardsman or Reservist during the term of their

active duty, the differential or full pay continuation will be considered state taxable compensation subject to

Pennsylvania personal income tax withholding. The term differential pay includes military continuation pay,

active duty differential payments required by state statutes or payments made by certain states or

commonwealths that pay a stipend or a set dollar amount to their employees called to military active duty.

Unless otherwise excluded by a preceding section, military differential pay may be taxable non-employee

compensation, whether it is subject to withholding or not. Employers should report military differential pay on

federal Form 1099–MISC, Box 3 - Other Income.

A full-time Pennsylvania National Guardsman is taxed on all of the following components of military

compensation:

o Inactive State duty pay received for services both within and outside the commonwealth;

o Inactive federal duty pay received for services as a member of the U.S. Armed Forces both within and

outside the commonwealth;

o Active federal duty pay received for services within the commonwealth;

o Active State duty pay received for services both within and outside the commonwealth.

Military Spouses Residency Relief Act

The Military Spouses Residency Relief Act (MSRRA) affects the treatment of residency and income for

spouses of military personnel for state tax purposes for tax years 2009 and after. If a Pennsylvania resident

service member is serving outside Pennsylvania and their nonmilitary spouse earns income in that other state

– and the spouse claims relief under the MSRRA – the spouse’s income is only taxable to Pennsylvania. If a

Pennsylvania nonresident service member is serving in Pennsylvania and their nonmilitary spouse earns

income in Pennsylvania, the spouse’s income is not taxable to P

ennsylvania under MSRRA, when the service

member and spouse are both residents or domiciliaries of the same other state, and if the spouse is in

Pennsylvania solely to be with the service member. Pennsylvania source income, from a business,

profession, farm, rental or royalty property, related to a business or property located in Pennsylvania remains

taxable to Pennsylvania nonresident military personnel and their spouses and is not covered by the MSRRA.

For detailed information on how MSRRA impacts state taxation of income earned by a service member’s

nonmilitary spouse, please review Personal Income Tax Bulletin 2010-01 Military Spouses Residency Relief

Act on the department’s website, www.revenue.pa.gov.

U.S. Foreign Service

A Pennsylvania resident in the U.S. Foreign Service is not on active duty for Pennsylvania purposes, and his

or her compensation is subject to tax.

Merchant Marine Members and Employees of U.S. Public Health Service

Pennsylvania residents serving in the Merchant Marines, U.S. Public Health Service, or the National Oceanic

and Atmospheric Administration are subject to tax on compensation whether earned within or outside

Pennsylvania.

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 17

of 65 www.revenue.pa.gov

However, compensation earned by Pennsylvania residents serving in the Merchant Marines or U.S. Public

Health Service called to active duty in a combat zone or hazardous duty zone is not subject to tax in

Pennsylvania. Copies of executive orders calling the individual to active duty are required to be included with

the Pennsylvania personal income tax return.

Additionally, nonresidents in the commissioned corps of the U.S. Public Health Service or National Oceanic

and Atmospheric Administration serving on active duty within Pennsylvania are not subject to tax in

Pennsylvania. Copies of executive orders calling the individual to active duty are required to be included with

the Pennsylvania personal income tax return if Pennsylvania personal income tax is incorrectly withheld from

compensation for either of these employers.

Combat Zone and Hazardous Duty Service

o Military Personnel

Combat zone pay and hazardous duty zone pay received by a member in the U.S. Armed Forces is not

taxable for Pennsylvania personal income tax purposes (Refer to Title 72 P.S. §7301(d)(vii)). Combat

zone and hazardous duty zone pay received by a member of the U.S. Armed forces is not considered

"poverty income" for purposes of tax forgiveness (Refer to Title 72 P.S. §7301(o.2)(vii)).

Combat zone for Pennsylvania personal income tax purposes means any area designated by the

President of the U.S. by Executive Order as a combat zone for any time period designated by the

President by Executive Order as the period of combatant activities. Hazardous duty zone is also

designated by Executive Order.

U.S. reservists and Pennsylvania National Guardsmen are members of the U.S. Armed Forces while they

are serving in a combat zone for purposes of this exclusion. The $500 "combat zone" pay exclusion limit

for military officers contained in the Internal Revenue Code is not in the state taxing statute.

o Civilians Working in Combat Zones

The Internal Revenue Service has concluded that no civilian contractor, or other civilian employee,

working in a combat zone is eligible for the combat zone exclusion provided by U.S. Code Section 112.

Likewise, there exists no comparable exclusion or exemption provided by the Pennsylvania personal

income tax statutes or regulations.

Eligibility Income for Tax Forgiveness Purposes

While active duty pay and active duty for training pay received by a member of the U.S. Armed Forces is not

taxable for Pennsylvania personal income tax purposes, a taxpayer must include such compensation when

determining eligibility for tax forgiveness on PA-40 Schedule SP.

Combat zone and hazardous duty zone pay received by a member of the U.S. Armed forces is not considered

"poverty income" for purposes of tax forgiveness (Refer to Title 72 P.S. §7301(o.2)(vii)).

Military Differential Pay

Differential pay is defined as payments made voluntarily by an

employer to represent the difference between

the regular salary of an employee called to military active duty and the amount being paid by the military, if

the regular salary was higher. The term differential pay also includes military continuation pay, active duty

differential payments required by state statutes or payments made by certain states or commonwealths that

pay a stipend or a set dollar amount to their employees called to military active duty.

Unless otherwise excluded by a preceding section, military differential pay may be taxable non-employee

compensation, whether it is subject to withholding or not.

Employers should report military differential pay on federal Form 1099–MISC, Box 3 - Other Income.

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 18

of 65 www.revenue.pa.gov

Combat Zone and Hazardous Duty Service

Pennsylvanians serving in combat zones or qualified hazardous duty areas designated by the President of the

U.S. are given the same additional time to file and pay their Pennsylvania income tax returns and make

payments as allowed for federal income tax purposes. The deadline is automatically extended to 180 days

from the last day of service or the last day of continuous hospitalization for injury incurred in one of these

areas.

Print “COMBAT ZONE” at the top of your return. Mail your return and military orders to:

Regarding: COMBAT ZONE

PA DEPARTMENT OF REVENUE

BUREAU OF INDIVIDUAL TAXES

PO BOX 280600

HARRISBURG PA 17128-0600

If you are filing your return electronically, you must still fax or mail copies of your orders. Print “COMBAT

ZONE” at the top of your orders. Fax your orders to (717) 772-4193 or mail your orders to:

Regarding: COMBAT ZONE

PA DEPARTMENT OF REVENUE

ELECTRONIC FILING SECTION

PO BOX 280507

HARRISBURG PA 17128-0507

Military Family Relief Assistance Program

Help those who serve our Nation and commonwealth by making a gift to the Military Family Relief Assistance

Program. Your gift will help Pennsylvania service members and their families by providing financial assistance

to those with a direct and immediate financial need as a result of circumstances beyond their control.

You can also send a direct, tax-deductible, gift to the Military Family Relief Assistance Program, c/o

Department of Military and Veterans Affairs, Fort Indiantown Gap, Annville, PA 17003-5002. For more

information visit - www.dmva.state.pa.us or call toll free 1-866-292-7201.

Athletes and Entertainers

Resident Professional Athletes and Entertainment Performers

A professional athlete or entertainment performer who is a full-year resident of Pennsylvania must report all

the compensation he or she earns, directly or indirectly, from his or her professional sport or professional

athletic team, or from professional performances. Such compensation includes, but is not limited to, any prize,

contest, tournament or race winnings, and remuneration, such as, but not limited to - the individual's regular

wages; any signing bonus; any incentive payments or performance bonuses; any severance or termination

payments or any payments received for refraining from performing services (i.e., covenant not-to-compete

payment); or any reimbursements for travel expenses except to the extent the reimbursements are for

vouchered expenses which do not exceed the federal per diem rate for the city in which the athlete or

performer is located. In addition, product endorsement fees, honoraria for public speaking engagements, or

fees received for attendance at card shows, autograph signings, or sports memorabilia events, would all have

to be reported as Pennsylvania taxable compensation.

Nonresident Professional Athletes and Entertainment Performers

A nonresident professional athlete or performer is required to pay Pennsylvania personal income tax on

wages or compensation received for services rendered within Pennsylvania unless the individual is a resident

of one of the reciprocal agreement states.

Allocation and Apportionment Rules for Nonresident Professional Athletes and Performers

PA Personal Income Tax Guide

Gross Compensation

DSM-12 (08-2022) 19

of 65 www.revenue.pa.gov

Nonresident professional athletes or performers who are not members of professional athletic teams or

performing companies and who do not have an established employer-employee relationship with the payer of

their remuneration must report all of their remuneration received from professional sporting events or

professional performances in which they participate within the commonwealth as "net income from the