Userid: CPM Schema:

instrx

Leadpct: 110% Pt. size: 10

Draft Ok to Print

AH XSL/XML

Fileid: … ns/i8938/202111/a/xml/cycle05/source (Init. & Date) _______

Page 1 of 16 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Instructions for Form 8938

(Rev. November 2021)

Statement of Specified Foreign Financial Assets

Department of the Treasury

Internal Revenue Service

Section references are to the Internal

Revenue Code unless otherwise noted.

Future Developments

For the latest information about

developments related to Form 8938

and its instructions, such as

legislation enacted after they were

published, go to IRS.gov/Form8938.

What’s New

Continuous-use form and instruc-

tions. Form 8938 and these

instructions have been converted from

an annual revision to continuous use.

Both the form and instructions will be

updated as needed. For the most

recent versions, go to

IRS.gov/

Form8938.

Reminders

Reporting obligations under sec-

tion 6038D not affected. Rev. Proc.

2020-17, available at IRS.gov/IRB/

2020-12_IRB#REV-PROC-2020-17,

exempts foreign trust information

reporting requirements on Forms

3520 and 3520-A, for certain U.S.

individuals’ transactions with, and

ownership of, certain tax-favored

foreign trusts that are established and

operated exclusively or almost

exclusively to provide pension or

retirement benefits, or to provide

medical disability or educational

benefits. This does not affect any

reporting obligations under section

6038D.

For more information about section

6038D information reporting, see

IRS.gov/Businesses/Corporations/

Basic-Questions-and-Answers-on-

Form-8938.

Specified domestic entity report-

ing. Certain domestic corporations,

partnerships, and trusts that are

considered formed or availed of for

the purpose of holding, directly or

indirectly, specified foreign financial

assets (specified domestic entities)

must file Form 8938 if the total value

of those assets exceeds $50,000 on

the last day of the tax year or $75,000

at any time during the tax year.

For more information on domestic

corporations, partnerships, and trusts

that are specified domestic entities

and must file Form 8938, and the

types of specified foreign financial

assets that must be reported, see

Who Must File, Specified Domestic

Entity, Specified Foreign Financial

Assets, Interests in Specified Foreign

Financial Assets, and Assets Not

Required To Be Reported, later.

General Instructions

Purpose of Form

Use Form 8938 to report your

specified foreign financial assets if the

total value of all the specified foreign

financial assets in which you have an

interest is more than the appropriate

reporting threshold. See Types of

Reporting Thresholds, later.

Filing Form 8938 does not

relieve you of the

requirement to file FinCEN

Form 114, Report of Foreign Bank

and Financial Accounts (FBAR), if you

are otherwise required to file the

FBAR. See FinCEN Form 114 and its

instructions for FBAR filing

requirements. Go to

IRS.gov/

Businesses/Comparison-of-

Form-8938-and-FBAR-Requirements

for a chart comparing Form 8938 and

FBAR filing requirements.

When and How To File

Attach Form 8938 to your annual

return and file by the due date

(including extensions) for that return.

You must specify the

applicable calendar year or

tax year to which your Form

8938 relates in the appropriate

space(s) at the top of the form.

CAUTION

!

CAUTION

!

An annual return includes the

following returns.

•

Form 1040.

•

Form 1040-NR.

•

Form 1040-SR.

•

Form 1041.

•

Form 1041-N.

•

Form 1065.

•

Form 1120.

A reference to an “annual return” or

“income tax return” in these

instructions includes a reference to

any return listed here, whether it is an

income tax return or an information

return.

Do not send a Form 8938 to

the IRS unless it is attached

to an annual return or an

amended return.

Who Must File

Unless an exception applies, you

must file Form 8938 if you are a

specified person (see Specified

Person, later) that has an interest in

specified foreign financial assets and

the value of those assets is more than

the applicable reporting threshold.

If you are required to file Form

8938, you must report the specified

foreign financial assets in which you

have an interest even if none of the

assets affects your tax liability for the

year. See

Specified Individual,

Specified Domestic Entity, and Types

of Reporting Thresholds, later.

Exception if no income tax

return required. If you do

not have to file an income tax

return for the tax year, you do not

have to file Form 8938, even if the

value of your specified foreign

financial assets is more than the

appropriate reporting threshold.

Specified Person

A specified person is either a

specified individual or a specified

domestic entity, defined later.

CAUTION

!

TIP

Dec 10, 2021

Cat. No. 55389W

Page 2 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Specified Individual

You are a specified individual if you

are one of the following.

•

A U.S. citizen.

•

A resident alien of the United States

for any part of the tax year (but see

Reporting Period, later).

•

A nonresident alien who makes an

election to be treated as a resident

alien for purposes of filing a joint

income tax return.

•

A nonresident alien who is a bona

fide resident of American Samoa or

Puerto Rico. See Pub. 570, Tax Guide

for Individuals With Income From U.S.

Possessions, for a definition of bona

fide resident.

Resident aliens. You are a resident

alien if you are treated as a resident

alien for U.S. tax purposes under the

green card test or the substantial

presence test. For more information,

see Pub. 519, U.S. Tax Guide for

Aliens. If you qualify as a resident

alien under either rule, you are a

specified individual.

Special rule for dual resident tax-

payers. If you are a dual resident

taxpayer (within the meaning of

Regulations section 301.7701(b)-7(a)

(1)), who determines his or her

income tax liability for all or a part of

the tax year as if he or she were a

nonresident alien as provided by

Regulations section 301.7701(b)-7,

file Form 8938 as follows.

Specified individual filing as a

nonresident alien at the end of his

or her tax year. You are not

required to report specified foreign

financial assets on Form 8938 for the

part of your tax year covered by Form

1040-NR, provided you comply with

the filing requirements of Regulations

section 301.7701(b)-7(b) and (c),

including the requirement to timely file

Form 1040-NR, as applicable, and

attach Form 8833, Treaty-Based

Return Position Disclosure Under

Section 6114 or 7701(b).

Specified individual filing as a

resident alien at the end of his or

her tax year. You are not required to

report specified foreign financial

assets on Form 8938 for the part of

your tax year reflected on the

schedule to Form 1040 or 1040-SR

required by Regulations section

1.6012-1(b)(2)(ii)(a), provided you

comply with the filing requirements of

Regulations section 1.6012-1(b)(2)(ii)

(a), including the requirement to timely

file Form 1040 or 1040-SR and attach

a properly completed Form 8833.

Specified Domestic Entity

You are a specified domestic entity if

you are one of the following.

•

A closely held domestic corporation

that has at least 50% of its gross

income from passive income.

•

A closely held domestic corporation

if at least 50% of its assets produce or

are held for the production of passive

income (see

Passive income and

Percentage of passive assets held by

a corporation or partnership, later).

•

A closely held domestic partnership

that has at least 50% of its gross

income from passive income.

•

A closely held domestic partnership

if at least 50% of its assets produce or

are held for the production of passive

income (see

Passive income and

Percentage of passive assets held by

a corporation or partnership, later).

•

A domestic trust described in

section 7701(a)(30)(E) that has one or

more specified persons (a specified

individual or a specified domestic

entity) as a current beneficiary.

Closely held domestic corporation.

A domestic corporation is closely held

if, on the last day of the corporation’s

tax year, a specified individual

directly, indirectly, or constructively

owns at least 80% of the total

combined voting power of all classes

of stock of the corporation entitled to

vote or at least 80% of the total value

of the stock of the corporation.

Closely held domestic partnership.

A domestic partnership is closely held

if, on the last day of the partnership’s

tax year, a specified individual

directly, indirectly, or constructively

holds at least 80% of the capital or

profits interest in the partnership.

Constructive ownership. Sections

267(c) and (e)(3) apply for purposes

of determining a specified individual’s

constructive ownership in a domestic

corporation or partnership, except that

section 267(c)(4) is applied as if the

family of an individual includes the

spouses of the specified individual’s

family members.

Passive income. Passive income

means the part of gross income that

consists of:

•

Dividends, including substitute

dividends;

•

Interest;

•

Income equivalent to interest,

including substitute interest;

•

Rents and royalties, other than

rents and royalties derived in the

active conduct of a trade or business

conducted, at least in part, by

employees of the corporation or

partnership;

•

Annuities;

•

The excess of gains over losses

from the sale or exchange of property

described in Regulations section

1.6038D-6(b)(3)(i)(F) and that gives

rise to the types of passive income

listed above;

•

The excess of gains over losses

from transactions (including futures,

forwards, and similar transactions) in

any commodity, but not including:

1. Any commodity hedging

transaction described in section

954(c)(5)(A), or

2. Active business gains or losses

from the sale of commodities, but only

if substantially all the corporation’s or

partnership’s commodities are

property described in paragraph (1),

(2), or (8) of section 1221(a);

•

The excess of foreign currency

gains over foreign currency losses (as

defined in section 988(b)) attributable

to any section 988 transaction; and

•

Net income from notional principal

contracts.

Exception from passive income

treatment for dealers. In the case of

a domestic corporation or partnership

regularly acting as a dealer in property

described in Regulations section

1.6038D-6(b)(3)(i)(F), forward

contracts, options contracts, or similar

financial instruments (including

notional principal contracts and all

instruments referenced to

-2-

Instructions for Form 8938 (Rev. 11-2021)

Page 3 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

commodities), passive income does

not include the following.

1. Any item of income or gain

(other than any dividends or interest)

from any transaction (including

hedging transactions and transactions

involving physical settlement) entered

into in the ordinary course of such

dealer’s trade or business as such a

dealer.

2. In the case of a corporation or

partnership that is a dealer in

securities (within the meaning of

section 475(c)(2)), any income from

any transaction entered into in the

ordinary course of the corporation’s or

partnership’s trade or business as a

dealer in securities.

Passive income or assets of rela-

ted corporations and partnerships.

For purposes of determining whether

a domestic corporation or partnership

meets the passive income or asset

test, domestic corporations and

domestic partnerships that are closely

held by the same specified individual

and that are connected through stock

or partnership ownership with a

common parent corporation or

partnership are treated as owning the

combined assets and receiving the

combined income of all members of

that group. For this purpose, any

contract, equity, or debt existing

between members of the group, as

well as any items of gross income

arising from that contract, equity, or

debt, is eliminated.

Connected stock or partnership

ownership. A domestic corporation

or partnership is considered

connected through stock or

partnership interest ownership with a

common parent corporation or

partnership in the following

circumstances.

1. Stock representing at least 80%

of the total combined voting power of

all classes of stock of the corporation

entitled to vote or of the value of such

corporation, other than stock of the

common parent, is owned by one or

more of the other connected

corporations, connected partnerships,

or the common parent.

2.

Partnership interests

representing at least 80% of the

profits interests or capital interests of

the partnership, other than

partnership interests in the common

parent, is owned by one or more of

the other connected corporations,

connected partnerships, or the

common parent.

Percentage of passive assets held

by a corporation or partnership.

For purposes of determining whether

at least 50% of your assets produce

or are held for the production of

passive income, the percentage of

passive assets held by the

corporation or partnership for a tax

year is the weighted average

percentage of passive assets

(weighted by total assets and

measured quarterly). The value of

assets of the corporation or

partnership is the fair market value or

the book value. The book value of

assets is the amount reflected on the

corporation’s or partnership’s balance

sheet and may be determined under

either a U.S. or an international

financial accounting standard. See

Example 1 below, which illustrates the

application of this weighted average

asset rule.

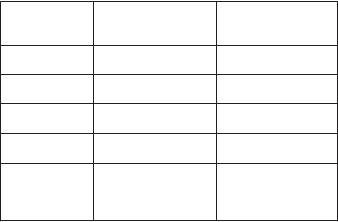

Example 1. Application of the

weighted average asset rule. The

following example illustrates the

application of the weighted average

asset rule.

DC is a domestic corporation, the total value

of the stock of which is owned by L, a

specified individual. DC is a calendar year

taxpayer. Less than 50% of DC’s gross

income for its tax year beginning January 1,

2021, is passive income. DC has the

following assets in 2021, measured quarterly:

Passive

Assets

Total Assets

Q1 $150 $200

Q2 $150 $300

Q3 $300 $500

Q4 $200 $1,000

Tax Year

Totals $800 $2,000

DC’s weighted passive asset percentage for

tax year 2021 is 40%, that is, DC’s total

passive assets divided by its total assets

($800 / $2,000 = 40%). Because fewer than

50% of DC’s assets produce or are held for

the production of passive income and less

than 50% of DC’s gross income for its tax

year is passive income, DC does not meet

the passive asset or passive income

threshold and would not be a specified

domestic entity.

Domestic trusts. A trust described

in section 7701(a)(30)(E) is

considered a specified domestic

entity if and only if the trust has one or

more specified persons (a specified

individual or a specified domestic

entity) as a current beneficiary for the

tax year.

Current beneficiary. With respect

to a tax year, a current beneficiary is

any person who at any time during the

tax year is entitled to, or at the

discretion of any person may receive,

a distribution from the principal or

income of the trust (determined

without regard to any power of

appointment to the extent that such

power remains unexercised at the end

of the tax year).

Special rule for general powers of

appointment. A current beneficiary

also includes any holder of a general

power of appointment, whether or not

exercised, that was exercisable at any

time during the tax year. A holder of a

general power of appointment that is

exercisable only on the death of the

holder is not a current beneficiary.

Excepted Specified Domestic

Entities

Entities described in section

1473(3). An entity described in

section 1473(3) and the regulations

thereunder, with the exception of a

trust that is exempt from tax under

section 664(c), is not a specified

domestic entity.

Certain domestic trust. A trust

described in section 7701(a)(30)(E) is

not considered a specified domestic

entity, provided that all of the following

apply.

1. The trustee is:

Instructions for Form 8938 (Rev. 11-2021)

-3-

Page 4 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

a. A bank that is examined by the

Office of the Comptroller of the

Currency, the Board of Governors of

the Federal Reserve System, the

Federal Deposit Insurance

Corporation, or the National Credit

Union Administration;

b. A financial institution that is

registered with and regulated or

examined by the Securities and

Exchange Commission; or

c. A domestic corporation

described in section 1473(3)(A) or

(B), and the regulations issued with

respect to those provisions.

2. The trustee has supervisory

authority over or fiduciary obligations

with regard to the specified foreign

financial assets held by the trust.

3. The trustee files annual returns

and information returns by the due

date (including any applicable

extensions) on behalf of the trust.

Domestic trusts owned by one or

more specified persons. A trust

described in section 7701(a)(30)(E) to

the extent the trust or any part of the

trust is treated as owned by one or

more specified persons under

sections 671 through 678 and the

regulations.

Types of Reporting Thresholds

Reporting Thresholds Applying to

Specified Individuals

If you are a specified individual, your

applicable reporting threshold

depends upon whether you are

married, file a joint federal income tax

return, and live inside (or outside) the

United States.

Taxpayers living in the United

States. If you do not live outside the

United States, you satisfy the

reporting threshold discussed next

that applies to you, and no exception

applies, file Form 8938 with your

income tax return.

Unmarried taxpayers. If you are

not married, you satisfy the reporting

threshold only if the total value of your

specified foreign financial assets is

more than $50,000 on the last day of

the tax year or more than $75,000 at

any time during the tax year.

Married taxpayers filing a joint

income tax return. If you are

married and you and your spouse file

a joint income tax return, you satisfy

the reporting threshold only if the total

value of your specified foreign

financial assets is more than

$100,000 on the last day of the tax

year or more than $150,000 at any

time during the tax year.

Married taxpayers filing

separate income tax returns. If you

are married and file a separate

income tax return from your spouse,

you satisfy the reporting threshold

only if the total value of your specified

foreign financial assets is more than

$50,000 on the last day of the tax year

or more than $75,000 at any time

during the tax year.

Taxpayers living outside the Uni-

ted States. If your tax home is in a

foreign country, you meet one of the

presence abroad tests described

next, and no exception applies, file

Form 8938 with your income tax

return if you satisfy the reporting

threshold discussed next that applies

to you.

Unmarried taxpayers. If you are

not married, you satisfy the reporting

threshold only if the total value of your

specified foreign financial assets is

more than $200,000 on the last day of

the tax year or more than $300,000 at

any time during the tax year.

Married taxpayers filing a joint

income tax return. If you are

married and you and your spouse file

a joint income tax return, you satisfy

the reporting threshold only if the total

value of your specified foreign

financial assets is more than

$400,000 on the last day of the tax

year or more than $600,000 at any

time during the tax year.

Married taxpayers filing

separate income tax returns. If you

are married and file a separate

income tax return from your spouse,

you satisfy the reporting threshold

only if the total value of your specified

foreign financial assets is more than

$200,000 on the last day of the tax

year or more than $300,000 at any

time during the tax year.

Presence abroad. You satisfy the

presence abroad test if you are one of

the following.

•

A U.S. citizen who has been a bona

fide resident of a foreign country or

countries for an uninterrupted period

that includes an entire tax year.

•

A U.S. citizen or resident who is

present in a foreign country or

countries at least 330 full days during

any period of 12 consecutive months

that ends in the tax year being

reported.

Reporting Thresholds Applying to

Specified Domestic Entities

If you are a specified domestic entity,

you satisfy the reporting threshold

only if the total value of your specified

foreign financial assets is more than

$50,000 on the last day of the tax year

or more than $75,000 at any time

during the tax year.

Determining the Total Value of

Your Specified Foreign

Financial Assets

You must figure the total value of the

specified foreign financial assets in

which you have an interest to

determine if you satisfy the reporting

threshold that applies to you. To

determine if you have an interest in a

specified foreign financial asset, see

Interests in Specified Foreign

Financial Assets, later.

Valuing Specified Foreign

Financial Assets

The value of a specified foreign

financial asset for purposes of

determining the total value of

specified foreign financial assets in

which you have an interest during the

tax year or on the last day of the tax

year is the asset's fair market value.

For purposes of figuring the total value

of specified foreign financial assets,

the value of a specified foreign

financial asset denominated in a

foreign currency must first be

determined in the foreign currency

and then converted to U.S. dollars.

See

Foreign Currency Conversion,

-4-

Instructions for Form 8938 (Rev. 11-2021)

Page 5 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

later, for rules on determining and

applying the appropriate foreign

currency exchange rate.

Value of an Interest in a Foreign

Trust During the Tax Year

If you do not know or have reason to

know based on readily accessible

information the fair market value of

your interest in a foreign trust during

the tax year, the value to be included

in determining the total value of your

specified foreign financial assets

during the tax year is the maximum

value of your interest in the foreign

trust. See

Valuing Interests in Foreign

Trusts, later, for rules on determining

the maximum value of an interest in a

foreign trust.

Value of an Interest in a Foreign

Estate, Foreign Pension Plan, and

Foreign Deferred Compensation

Plan

If you do not know or have reason to

know based on readily accessible

information the fair market value of

your interest in a foreign estate,

foreign pension plan, or foreign

deferred compensation plan during

the tax year, the value to be included

in determining the total value of your

specified foreign financial assets

during the tax year is the fair market

value, determined as of the last day of

the tax year, of the currency and other

property distributed during the tax

year to you. If you received no

distributions during the tax year and

do not know or have reason to know

based on readily accessible

information the fair market value of

your interest, use a value of zero for

the interest.

Asset With No Positive Value

If the maximum value of a specified

foreign financial asset is less than

zero, use a value of zero for the asset.

Joint Interest Valuation

If you jointly own an asset with

someone else, the value that you use

to determine the total value of all of

your specified foreign financial assets

depends on whether the other owner

is your spouse and, if so, whether

your spouse is a specified individual

and whether you file a joint or

separate return.

Joint ownership with spouse filing

joint income tax return. If you and

your spouse file a joint income tax

return and, therefore, would file one

combined Form 8938 for the tax year,

include the value of the asset jointly

owned with your spouse only once to

determine the total value of all of the

specified foreign financial assets you

and your spouse own.

Joint ownership with spouse filing

separate income tax return. If you

and your spouse are specified

individuals and you each file a

separate annual return, include

one-half of the value of the asset

jointly owned with your spouse to

determine the total value of all of your

specified foreign financial assets.

Joint ownership with a spouse

who is not a specified individual or

someone other than a spouse.

Each joint owner includes the entire

value of the jointly owned asset to

determine the total value of all of that

joint owner's specified foreign

financial assets.

Special Rules

Assets Reported on Another Form

Specified individual. If you are a

specified individual, include the value

of all specified foreign financial

assets, even if they are reported on

another form listed in

Part IV to

determine if you satisfy the reporting

threshold that applies to you. See

Part

IV. Excepted Specified Foreign

Financial Assets, later.

Specified domestic entity. If you

are a specified domestic entity,

exclude the value of any specified

foreign financial asset reported on

another form listed in

Part IV to

determine if you satisfy the applicable

reporting threshold.

Bona Fide Resident of a U.S.

Possession

Do not include the value of specified

foreign financial assets you are not

required to report because you are a

bona fide resident of a U.S.

possession. See

Bona Fide Resident

of a U.S. Possession under Assets

Not Required To Be Reported, later.

Owners of Certain Domestic Trusts

Do not include the value of specified

foreign financial assets you are not

required to report because you are an

owner of a domestic widely held fixed

investment trust or a domestic

liquidating trust created under

chapter 7 or chapter 11 of the

Bankruptcy Code. See

Domestic

Investment Trusts and Domestic

Bankruptcy Trusts, later.

Related Domestic Corporations

and Partnerships

To determine if you satisfy the

applicable reporting threshold, a

specified domestic entity that is a

corporation or partnership and that

has an interest in any specified

foreign financial asset is treated as

owning all specified foreign financial

assets held by all related corporations

or partnerships that are closely held

by the same specified individual

(excluding specified foreign financial

assets that are excluded from

reporting under

Part IV of Form 8938

or because you are the owner of a

domestic widely held fixed investment

trust or a domestic liquidating trust

created under chapter 7 or chapter 11

of the Bankruptcy Code).

Examples 2 through 11 may help

you decide if you have to file Form

8938.

Example 2. I am not married and

do not live abroad. The total value

of my specified foreign financial

assets does not exceed $49,000

during the tax year. You do not

have to file Form 8938. You do not

satisfy the reporting threshold of more

than $50,000 on the last day of the tax

year or more than $75,000 at any time

during the tax year.

Instructions for Form 8938 (Rev. 11-2021)

-5-

Page 6 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Example 3. I am not married and

do not live abroad. I sold my only

specified foreign financial asset on

October 15, when its value was

$125,000. You have to file Form

8938. You satisfy the reporting

threshold even though you do not hold

any specified foreign financial assets

on the last day of the tax year

because you did own specified

foreign financial assets of more than

$75,000 at any time during the tax

year.

Example 4. I am not married and

do not live abroad. An unrelated

U.S. resident and I jointly own a

specified foreign financial asset

valued at $60,000. You each have

to file Form 8938. You each satisfy the

reporting threshold of more than

$50,000 on the last day of the tax

year.

Example 5. I am not married and

do not live abroad. I own an entity

disregarded for tax purposes,

which owns one specified foreign

financial asset valued at $30,000.

In addition, I own a specified

foreign financial asset valued at

$25,000. You have to file Form 8938.

You own both the specified foreign

financial asset owned by the

disregarded entity and the specified

foreign financial asset you own

directly, for a total value of $55,000.

You satisfy the reporting threshold of

more than $50,000 on the last day of

the tax year.

Example 6. My spouse and I do

not live abroad. We file a joint

income tax return and jointly own

a single specified foreign financial

asset valued at $60,000. You and

your spouse do not have to file Form

8938. You do not satisfy the reporting

threshold of more than $100,000 on

the last day of the tax year or more

than $150,000 at any time during the

tax year.

Example 7. My spouse and I do

not live abroad. We file a joint

income tax return, and jointly and

individually own specified foreign

financial assets. On the last day of

the tax year, my spouse and I

jointly own a specified foreign

financial asset with a value of

$90,000. My spouse has a separate

interest in a specified foreign

financial asset with a value of

$10,000. I have a separate interest

in a specified foreign financial

asset with a value of $1,000. You

and your spouse have to file a

combined Form 8938. You and your

spouse have an interest in specified

foreign financial assets in the amount

of $101,000 on the last day of the tax

year. This is the entire value of the

specified foreign financial asset that

you jointly own, $90,000, plus the

value of the asset that your spouse

separately owns, $10,000, plus the

value of the asset that you separately

own, $1,000. You and your spouse

satisfy the reporting threshold of more

than $100,000 on the last day of the

tax year.

Example 8. My spouse and I do

not live abroad. We file separate

income tax returns and jointly own

a specified foreign financial asset

valued at $60,000 for the entire

year. Neither you nor your spouse

has to file Form 8938. You each use

one-half of the value of the asset,

$30,000, to determine the total value

of specified foreign financial assets

that you each own. Neither of you

satisfies the reporting threshold of

more than $50,000 on the last day of

the tax year or more than $75,000 at

any time during the tax year.

Example 9. My spouse and I file

separate income tax returns,

jointly and individually own

specified foreign financial assets,

and do not live abroad. On the last

day of the tax year, my spouse and

I jointly own a specified foreign

financial asset with a value of

$90,000. My spouse has a separate

interest in a specified foreign

financial asset with a value of

$10,000. I have a separate interest

in a specified foreign financial

asset with a value of $1,000. You

do not have to file Form 8938 but your

spouse does. Your spouse has an

interest in specified foreign financial

assets in the amount of $55,000 on

the last day of the tax year. This is

one-half of the value of the asset that

you jointly own, $45,000, plus the

entire value of the asset that your

spouse separately owns, $10,000.

You have an interest in specified

foreign financial assets in the amount

of $46,000 on the last day of the tax

year. This is one-half of the value of

the asset that you jointly own,

$45,000, plus the entire value of the

asset that you separately own,

$1,000. Your spouse satisfies the

reporting threshold of more than

$50,000 on the last day of the tax

year. You do not satisfy the reporting

threshold of more than $50,000 on the

last day of the tax year or more than

$75,000 at any time during the tax

year.

Example 10. My spouse and I

are U.S. citizens but live abroad for

the entire tax year and file a joint

income tax return. The total value

of our combined specified foreign

financial assets on any day of the

tax year is $150,000. You and your

spouse do not have to file Form 8938.

You do not satisfy the reporting

threshold of more than $400,000 on

the last day of the tax year or more

than $600,000 at any time during the

tax year for married individuals who

live abroad and file a joint income tax

return.

Example 11. My spouse and I

live abroad and file separate

income tax returns. My spouse is

not a specified individual. On the

last day of the tax year, my spouse

and I jointly own a specified

foreign financial asset with a value

of $150,000. My spouse has a

separate interest in a specified

foreign financial asset with a value

of $10,000. I have a separate

interest in a specified foreign

financial asset with a value of

$60,000. You have to file Form 8938

but your spouse, who is not a

specified individual, does not. You

have an interest in specified foreign

financial assets in the amount of

$210,000 on the last day of the tax

year. This is the entire value of the

asset that you jointly own, $150,000,

plus the entire value of the asset that

you separately own, $60,000. You

satisfy the reporting threshold for a

-6-

Instructions for Form 8938 (Rev. 11-2021)

Page 7 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

married individual living abroad and

filing a separate return of more than

$200,000 on the last day of the tax

year.

Specified Foreign

Financial Assets

Types of Specified Foreign

Financial Assets

Specified foreign financial assets

include the following assets.

1. Financial accounts maintained

by a foreign financial institution.

2. The following foreign financial

assets if they are held for investment

and not held in an account maintained

by a financial institution.

a. Stock or securities issued by

someone that is not a U.S. person

(including stock or securities issued

by a person organized under the laws

of a U.S. possession).

b. Any interest in a foreign entity.

c. Any financial instrument or

contract that has an issuer or

counterparty that is not a U.S. person

(including a financial contract issued

by, or with a counterparty that is, a

person organized under the laws of a

U.S. possession).

For foreign financial assets

excepted from reporting, see Assets

Not Required To Be Reported, later.

Financial Account

A financial account is any depository

or custodial account (under

Regulations section 1.1471-5(b)(1)(i)

or (ii)) maintained by a foreign

financial institution as well as any

equity or debt interest in a foreign

financial institution (other than

interests that are regularly traded on

an established securities market) or

any cash value life insurance or

annuity contract maintained by an

insurance company or other foreign

financial institution. A specified foreign

financial asset includes a financial

account maintained by a financial

institution that is organized under the

laws of a U.S. possession (American

Samoa, Guam, the Commonwealth of

the Northern Mariana Islands, Puerto

Rico, or the U.S. Virgin Islands).

Foreign financial institution. In

most cases, a foreign financial

institution is any financial institution

that is not a U.S. entity and satisfies

one or more of the following.

•

It accepts deposits in the ordinary

course of a banking or similar

business.

•

It holds financial assets for the

account of others as a substantial part

of its business.

•

It is engaged (or holds itself out as

being engaged) primarily in the

business of investing, reinvesting, or

trading in securities, partnership

interests, commodities, or any interest

(including a futures or forward

contract or option) in such securities,

partnership interests, or commodities.

Other Specified Foreign Financial

Assets

Examples of other specified foreign

financial assets include the following,

if they are held for investment and not

held in a financial account.

•

Stock issued by a foreign

corporation.

•

A capital or profits interest in a

foreign partnership.

•

A note, bond, debenture, or other

form of indebtedness issued by a

foreign person.

•

An interest in a foreign trust or

foreign estate.

•

An interest rate swap, currency

swap, basis swap, interest rate cap,

interest rate floor, commodity swap,

equity swap, equity index swap, credit

default swap, or similar agreement

with a foreign counterparty.

•

An option or other derivative

instrument with respect to any of

these examples or with respect to any

currency or commodity that is entered

into with a foreign counterparty or

issuer.

Assets held for investment. You

hold an asset, including a partnership

interest, for investment if you do not

use it in, or hold it for use in, the

conduct of any trade or business.

Stock is not considered used or

held for use in the conduct of a trade

or business.

If you are required to file

Form 8938, in addition to

reporting retirement and

pension accounts and nonretirement

savings accounts described in

Regulations section 1.1471-5(b)(2)(i),

you must report retirement and

pension accounts, nonretirement

savings accounts, and accounts

satisfying conditions similar to those

described in Regulations section

1.1471-5(b)(2)(i) that are otherwise

excluded from the definition of a

financial account by an applicable

Model 1 IGA or Model 2 IGA. Thus,

such accounts are subject to uniform

reporting rules and must be reported

without regard to whether the account

is maintained in a jurisdiction with an

IGA.

Interests in Specified Foreign

Financial Assets

You have an interest in a specified

foreign financial asset if any income,

gains, losses, deductions, credits,

gross proceeds, or distributions from

holding or disposing of the asset are

or would be required to be reported,

included, or otherwise reflected on

your income tax return.

You have an interest in a specified

foreign financial asset even if no

income, gains, losses, deductions,

credits, gross proceeds, or

distributions from holding or disposing

of the asset are included or reflected

on your income tax return for this tax

year.

Interests in Property Transferred

in Connection With the

Performance of Services

You are first considered to have an

interest in property transferred in

connection with the performance of

services on the first date that the

property is substantially vested (within

the meaning of Regulations section

1.83-3(b)) or, if you have made a valid

section 83(b) election with respect to

the property, on the date of transfer of

the property.

CAUTION

!

Instructions for Form 8938 (Rev. 11-2021)

-7-

Page 8 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Interests in Assets Held by

Disregarded Entities

If you are the owner of a disregarded

entity, you have an interest in any

specified foreign financial assets

owned by the disregarded entity.

Interests in Jointly Owned Assets

A joint owner of an asset has an

interest in the entire asset. For special

rules for interests in assets jointly

owned by spouses, see

Joint Interest

Valuation, earlier, and Reporting the

Value of Jointly Owned Assets, later.

Interests in Assets Held in

Financial Accounts

If you have an interest in a financial

account that holds specified foreign

financial assets, you do not have to

report the assets held in the account.

Interests in Assets Generating

Certain Unearned Income of

Children

If you file Form 8814, Parents'

Election To Report Child's Interest

and Dividends, with your income tax

return to elect to include in your gross

income certain unearned income of

your child (the “kiddie tax” election),

you have an interest in any specified

foreign financial asset held by the

child.

Interests in Assets Held by Entities

That Are Not Disregarded Entities

In most cases, you do not own an

interest in any specified foreign

financial asset held by a partnership,

corporation, trust, or estate solely as a

result of your status as a partner,

shareholder, or beneficiary.

Interests in Assets Held by

Grantor Trust

If you are considered the owner under

the grantor trust rules (sections 671

through 679) of any part of a trust, you

have an interest in any specified

foreign financial asset held by that

part of the trust you are considered to

own. For exceptions from reporting for

owners of certain domestic

investment or bankruptcy trusts, see

Domestic Investment Trusts and

Domestic Bankruptcy Trusts, later.

Interests in Foreign Estates and

Foreign Trusts

An interest in a foreign trust or a

foreign estate is not a specified

foreign financial asset unless you

know or have reason to know based

on readily accessible information of

the interest. If you receive a

distribution from the foreign trust or

foreign estate, you are considered to

know of the interest.

Interests in Foreign Pension Plans

and Foreign Deferred

Compensation Plans

Report in Part VI your interest in the

foreign pension plan or foreign

deferred compensation plan. Do not

separately report the assets held by

the plan. See

Valuing Interests in

Foreign Estates, Foreign Pension

Plans, and Foreign Deferred

Compensation Plans, later.

Reporting Period

Unless an exception applies, the

reporting period for Form 8938 is your

tax year.

Exception for Partial Tax Years

of Specified Individuals

If you are a specified individual for

less than the entire tax year, the

reporting period is the part of the year

that you are a specified individual.

Example 12. John is a calendar

year taxpayer. The Form 8938

reporting period begins on January 1

and ends on December 31.

Example 13. Agnes was a single

calendar year taxpayer who died on

March 6. The Form 8938 reporting

period begins on January 1 and ends

on March 6.

Example 14. George, a calendar

year taxpayer, is not a U.S. citizen or

married. George arrived in the United

States on February 1 and satisfied the

substantial presence test for the tax

year. The Form 8938 reporting period

begins on George's U.S. residency

starting date, February 1, and ends on

December 31.

Reporting Maximum Value

You must report the maximum value

during the tax year of each specified

foreign financial asset reported on

Form 8938. In most cases, the value

of a specified foreign financial asset is

its fair market value. An appraisal by a

third party is not necessary to

estimate the maximum fair market

value during the year. See

Valuing

Financial Accounts and Valuing Other

Specified Foreign Financial Assets,

later.

Assets With No Positive Value

If the maximum value of a specified

foreign financial asset is less than

zero, use a value of zero as the

maximum value of the asset.

Foreign Currency Conversion

If your specified foreign financial asset

is denominated in a foreign currency

during the tax year, the maximum

value of the asset must be determined

in the foreign currency and then

converted to U.S. dollars.

In most cases, you must use the

U.S. Treasury Bureau of the Fiscal

Service foreign currency exchange

rate for purchasing U.S. dollars. You

can find this rate on

fiscal.treasury.gov/fsreports/rpt/

treasRptRateExch/

treasRptRateExch_home.htm. If no

U.S. Treasury Bureau of the Fiscal

Service exchange rate is available,

you must use another publicly

available foreign currency exchange

rate for purchasing U.S. dollars and

disclose the rate on Form 8938.

Currency Determination Date

Use the currency exchange rate on

the last day of the tax year to figure

the maximum value of a specified

foreign financial asset or the value of

a specified foreign financial asset for

the purpose of determining the total

value of your specified foreign

financial assets to see whether you

have met the reporting threshold. Use

this rate even if you sold or otherwise

disposed of the specified foreign

-8-

Instructions for Form 8938 (Rev. 11-2021)

Page 9 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

financial asset before the last day of

the tax year.

Exception for Financial Account

Statement Currency Conversion

Rate

You may rely on the foreign currency

conversion rate reflected in a financial

account statement issued at least

annually by the financial institution

maintaining the account.

Reporting the Value of Jointly

Owned Assets

If you own an asset jointly with one or

more persons, you must report the

asset's maximum value as follows.

Married Specified Individuals

Filing a Joint Income Tax Return

If you are married and you and your

spouse file a joint income tax return,

report any specified foreign financial

asset that you jointly own only once

and include the maximum value of the

entire asset (and not just the

maximum value of your interest in the

asset). Also, you must report any

specified foreign financial asset that

you or your spouse separately owns

and include the maximum value of the

entire asset. If you and your spouse

file a joint income tax return that

includes Form 8814, you must report

any specified foreign financial asset

your child owns only once and include

the maximum value of the entire

asset.

Married Specified Individuals

Filing Separate Income Tax

Returns

If you are married and you and your

spouse are specified individuals who

file separate income tax returns, both

you and your spouse report any

specified foreign financial asset that

you jointly own on your separate

Forms 8938, and both you and your

spouse must include the maximum

value of the entire asset on your

separate Forms 8938. You must also

report any specified foreign financial

asset that you own individually on

your separate Form 8938 and include

the maximum value of the entire

asset. If you file Form 8814, you must

report any specified foreign financial

asset your child owns and include the

maximum value of the entire asset.

Other Joint Ownership

If you are a joint owner of a specified

foreign financial asset and you cannot

use one of the special rules for

married individuals who file a joint tax

return, you must report the specified

foreign financial asset and include the

maximum value of the entire asset.

Valuing Financial Accounts

You may rely on periodic account

statements for the tax year to report a

financial account's maximum value

unless you know or have reason to

know based on readily accessible

information that the statements do not

reflect a reasonable estimate of the

maximum account value during the

tax year.

Valuing Other Specified

Foreign Financial Assets

In most cases, you may use the value

of a specified foreign financial asset

that is not a financial account and that

is held for investment and not held in

an account maintained by a financial

institution as of the last day of the tax

year, unless you know or have reason

to know based on readily accessible

information that the value does not

reflect a reasonable estimate of the

maximum value of the asset during

the tax year.

Example 15. I have publicly

traded foreign stock not held in a

financial account that has a fair

market value as of the last day of

the tax year of $100,000, although,

based on daily price information

that is readily available, the

52-week high trading price for the

stock results in a maximum value

of the stock during the tax year of

$150,000. If you are required to file

Form 8938, the maximum value of the

foreign stock to be reported is

$150,000, based on readily available

information of the stock’s maximum

value during the tax year.

Valuing Interests in Foreign

Trusts

If you are a beneficiary of a foreign

trust, the maximum value of your

interest in the trust is the sum of the

following amounts.

•

The value of all of the cash or other

property distributed during the tax

year from the trust to you as a

beneficiary.

•

The value using the valuation tables

under section 7520 of your right as a

beneficiary to receive mandatory

distributions as of the last day of the

tax year.

Valuing Interests in Foreign

Estates, Foreign Pension Plans,

and Foreign Deferred

Compensation Plans

If you have an interest in a foreign

estate, foreign pension plan, or

foreign deferred compensation plan,

the maximum value of your interest is

the fair market value of your beneficial

interest in the assets of the estate,

pension plan, or deferred

compensation plan as of the last day

of the tax year. If you do not know or

have reason to know based on readily

accessible information the fair market

value as of the last day of the tax year,

the maximum value is the fair market

value, determined as of the last day of

the tax year, of the cash and other

property distributed during the tax

year to you as a beneficiary or

participant. If you received no

distributions during the tax year and

do not know or have reason to know

based on readily accessible

information the fair market value of

your interest as of the last day of the

tax year, use a value of zero as the

maximum value of the asset.

Assets Not Required To

Be Reported

You are not required to report the

following assets.

Certain Financial Accounts

The following financial accounts and

the assets held in such accounts are

not specified foreign financial assets

and do not have to be reported on

Form 8938.

Instructions for Form 8938 (Rev. 11-2021)

-9-

Page 10 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

1. A financial account that is

maintained by a U.S. payer, such as a

domestic financial institution. In

general, a U.S. payer also includes a

domestic branch of a foreign bank or

foreign insurance company and a

foreign branch or foreign subsidiary of

a U.S. financial institution. Examples

of financial accounts maintained by

U.S. financial institutions include:

•

U.S. mutual funds accounts,

•

IRAs (traditional or Roth),

•

Section 401(k) retirement accounts,

•

Qualified U.S. retirement plans, and

•

Brokerage accounts maintained by

U.S. financial institutions.

2. A financial account that is

maintained by a dealer or trader in

securities or commodities if all of the

holdings in the account are subject to

the mark-to-market accounting rules

for dealers in securities or an election

under section 475(e) or (f) is made for

all of the holdings in the account.

Certain Financial Assets

You do not have to report any asset

that is not held in a financial account if

the asset is subject to the

mark-to-market accounting rules for

dealers in securities or commodities

or an election under section 475(e) or

(f) is made for the asset.

Foreign Equivalent to U.S.

Social Security

Payments or the rights to receive the

foreign social security equivalent to

U.S. social security, social insurance

benefits, or another similar program of

a foreign government are not

specified foreign financial assets and

are not reportable. The foreign social

security equivalent to U.S. social

security does not include an interest in

a foreign pension plan, which, as

described above, is subject to section

6038D reporting.

Exceptions To Reporting

Duplicative Reporting

You do not have to report any asset

on Form 8938 if you report it on one or

more of the following forms that you

timely file with the IRS for the same

tax year.

•

Form 3520, Annual Return To

Report Transactions With Foreign

Trusts and Receipt of Certain Foreign

Gifts (in the case of a specified person

who is a beneficiary of a foreign trust,

see Part III of Form 3520 and its

instructions).

•

Form 5471, Information Return of

U.S. Persons With Respect to Certain

Foreign Corporations.

•

Form 8621, Information Return by a

Shareholder of a Passive Foreign

Investment Company or Qualified

Electing Fund.

•

Form 8865, Return of U.S. Persons

With Respect to Certain Foreign

Partnerships.

Instead, you must identify on Form

8938 the form(s) on which you report

the specified foreign financial asset

and how many of these forms you file.

See Part IV. Excepted Specified

Foreign Financial Assets, later.

Joint Form 5471 or Form 8865

Filers

If you are included as part of a joint

Form 5471 or Form 8865 filing and

provide the notification required by

Regulations section 1.6038-2(i) or

1.6038-3(c), you are considered to

have filed that form for purposes of

the requirement to report specified

foreign financial assets on Form 8938.

See

Part IV. Excepted Specified

Foreign Financial Assets, later.

Foreign Grantor Trusts

If you are considered the owner under

the grantor trust rules (sections 671

through 679) of any part of a foreign

trust, you do not have to report any of

the specified foreign financial assets

held by the part of the trust you are

considered to own if you satisfy the

following conditions.

•

You report the trust on a Form 3520

that you timely file with the IRS for the

same tax year. See Part III of Form

3520 and its instructions.

•

You ensure that the trust timely files

Form 3520-A, Annual Information

Return of Foreign Trust With a U.S.

Owner, (or you timely file a substitute

Form 3520-A) with the IRS for the

same tax year. See Form 3520-A and

its instructions.

•

You report the filing of Form 3520

and 3520-A on Form 8938.

Instead, you must identify on Form

8938 how many of these forms you

file. See Part IV. Excepted Specified

Foreign Financial Assets, later.

If you are a specified

individual, you must include

the value of the assets

reported on Forms 3520, 3520-A,

5471, 8621, and 8865 in determining

whether you satisfy the reporting

threshold that applies to you. See

Reporting Thresholds Applying to

Specified Individuals, earlier.

Domestic Investment Trusts

If you are considered the owner under

the grantor trust rules (sections 671

through 679) of any part of a domestic

widely held fixed investment trust

under Regulations section 1.671-5,

you do not have to report any

specified foreign financial asset held

by the part of the trust you are

considered to own.

Domestic Bankruptcy Trusts

If you are considered the owner under

the grantor trust rules (sections 671

through 679) of any part of a domestic

liquidating trust under Regulations

section 301.7701-4(d) that is created

under chapter 7 or chapter 11 of the

Bankruptcy Code, you do not have to

report any specified foreign financial

asset held by the part of the trust you

are considered to own.

Bona Fide Resident of a U.S.

Possession

If you are a bona fide resident of a

U.S. possession (American Samoa,

Guam, the Commonwealth of the

Northern Mariana Islands, Puerto

Rico, or the U.S. Virgin Islands), do

not include the value of the following

assets to determine if you satisfy the

reporting threshold that applies to

you. If you are required to file Form

8938, you do not have to report the

following specified foreign financial

assets on Form 8938.

CAUTION

!

-10-

Instructions for Form 8938 (Rev. 11-2021)

Page 11 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

•

A financial account maintained by a

financial institution organized under

the laws of the U.S. possession of

which you are a bona fide resident.

•

A financial account maintained by a

branch of a financial institution not

organized under the laws of the U.S.

possession of which you are a bona

fide resident, if the branch is subject

to the same tax and information

reporting requirements that apply to a

financial institution organized under

the laws of the U.S. possession of

which you are a bona fide resident.

•

Stock or securities issued by an

entity organized under the laws of the

U.S. possession of which you are a

bona fide resident.

•

An interest in an entity organized

under the laws of the U.S. possession

of which you are a bona fide resident.

•

A financial instrument or contract

held for investment, provided each

issuer or counterparty that is not a

U.S. person is either an entity

organized under the laws of the U.S.

possession of which you are a bona

fide resident or a bona fide resident of

the U.S. possession of which you are

a bona fide resident.

Penalties

You may be subject to penalties if you

fail to timely file a correct Form 8938

or if you have an understatement of

tax relating to an undisclosed

specified foreign financial asset.

Failure-To-File Penalty

If you are required to file Form 8938

but do not file a complete and correct

Form 8938 by the due date (including

extensions), you may be subject to a

penalty of $10,000.

Continuing Failure To File

If you do not file a correct and

complete Form 8938 within 90 days

after the IRS mails you a notice of the

failure to file, you may be subject to an

additional penalty of $10,000 for each

30-day period (or part of a period)

during which you continue to fail to file

Form 8938 after the 90-day period

has expired. The maximum additional

penalty for a continuing failure to file

Form 8938 is $50,000.

Married Taxpayers Filing a Joint

Income Tax Return

If you are married and you and your

spouse file a joint income tax return,

the failure-to-file penalties apply as if

you and your spouse were a single

person. Your and your spouse’s

liability for all penalties is joint and

several.

Presumption of Maximum Value

If the IRS determines that you have an

interest in one or more specified

foreign financial assets and asks you

for information about the value of any

asset, but you do not provide enough

information for the IRS to determine

the value of the asset, you are

presumed to own specified foreign

financial assets with a value of more

than the reporting threshold that

applies to you. See

Determining the

Total Value of Your Specified Foreign

Financial Assets, earlier. In such

case, you are subject to the

failure-to-file penalties if you do not

file Form 8938.

Reasonable Cause Exception

No penalty will be imposed if you fail

to file Form 8938 or to disclose one or

more specified foreign financial assets

on Form 8938 and the failure is due to

reasonable cause and not to willful

neglect. You must affirmatively show

the facts that support a reasonable

cause claim.

The determination of whether a

failure to disclose a specified foreign

financial asset on Form 8938 was due

to reasonable cause and not due to

willful neglect will be determined on a

case-by-case basis, taking into

account all pertinent facts and

circumstances.

Effect of foreign jurisdiction laws.

The fact that a foreign jurisdiction

would impose a civil or criminal

penalty on you if you disclose the

required information is not reasonable

cause.

Accuracy-Related Penalty

If you underpay your tax as a result of

a transaction involving an undisclosed

specified foreign financial asset, you

may have to pay a penalty equal to

40% of that underpayment.

Examples of underpayments due to

transactions involving an undisclosed

specified foreign financial asset

include the following.

•

You do not report ownership of

shares in a foreign corporation on

Form 8938 and you received taxable

distributions from the company that

you did not report on your income tax

return.

•

You do not report ownership of

shares in a foreign company on Form

8938 and you sold the shares in the

company for a gain and did not report

the gain on your income tax return.

•

You do not report a foreign pension

on Form 8938 and you received a

taxable distribution from the pension

plan that you did not report on your

income tax return.

Fraud

If you underpay your tax due to fraud,

you must pay a penalty of 75% of the

underpayment due to fraud.

Criminal Penalties

In addition to the penalties already

discussed, if you fail to file Form 8938,

fail to report an asset, or have an

underpayment of tax, you may be

subject to criminal penalties.

Statute of Limitations

If you fail to file Form 8938 or fail to

report a specified foreign financial

asset that you are required to report,

the statute of limitations for the tax

year may remain open for all or a part

of your income tax return until 3 years

after the date on which you file Form

8938.

Extended Statute of Limitations for

Failure To Include Income

If you do not include in your gross

income an amount relating to one or

more specified foreign financial

assets, and the amount you omit is

more than $5,000, any tax you owe for

the tax year can be assessed at any

time within 6 years after you filed your

return.

Instructions for Form 8938 (Rev. 11-2021)

-11-

Page 12 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

For this purpose, specified foreign

financial assets include any specified

foreign financial assets in which you

have an interest without regard to the

reporting threshold that applies to you

and regardless of any exception from

reporting a specified foreign financial

asset on Form 8938.

Specific Instructions

Before you begin. If you are a

specified individual and report all of

your specified foreign financial assets

on a timely filed Form 3520, 3520-A,

5471, 8621, or 8865, you do not have

to report them on Form 8938. Instead,

enter your name(s) and taxpayer

identification number (TIN) at the top

of the form and complete

Part IV only.

If you are a specified individual or a

specified domestic entity and report

only a part of your specified foreign

financial assets on one or more of

these forms, report the remaining

assets on Form 8938 and complete

Part IV.

Additional statements. If you have

more than one account or asset to

report in Part V or VI, or more than

one issuer or counterparty to report in

Part VI, make additional copies of

page 2 of this form and attach them to

your form. Check the box at the top of

page 1 of the form to indicate that you

are attaching additional statements,

and enter the number of additional

statements in the space provided.

Period Covered

For filing calendar year and fiscal year

returns, fill in the tax year of the

specified individual or specified

domestic entity for whom you are

furnishing information in the space at

the top of the form.

Identifying Information

Lines 1 and 2

Enter your name(s) and TIN as shown

on the annual return you are filing with

Form 8938. If you are a specified

individual (see

Specified Individual,

earlier), enter the first TIN shown on

your income tax return. A TIN is a

social security number (SSN) or

individual taxpayer identification

number (ITIN). In the case of a

specified domestic entity (see

Specified Domestic Entity, earlier),

enter the entity’s employer

identification number (EIN).

Line 3

Indicate the type of filer by checking

the applicable box on line 3. If you are

a specified individual (see

Specified

Individual, earlier), check box 3a. In

the case of a specified domestic entity

(see

Specified Domestic Entity,

earlier), check the applicable box for

partnership (3b), corporation (3c), or

trust (3d).

Line 4

If you checked box 3a (specified

individual), do not complete this line 4.

If you checked box 3b (partnership) or

3c (corporation), enter the name and

TIN of the specified individual (see

Specified Individual, earlier) who

closely holds the partnership or

corporation. If you checked box 3d

(trust), enter the name and TIN of the

specified person (see

Specified

Person, earlier) who is a current

beneficiary of the trust.

Note. If you are a paper filer and you

have more than one specified

individual or specified person, attach

a statement listing the name and TIN

of each such specified individual or

specified person.

If you are a specified

individual (see Specified

Individual, earlier) for less

than the entire tax year, you only have

to report the information for the part of

the year that you are a specified

individual.

Part I. Foreign Deposit and

Custodial Accounts

Summary

Use Part I to summarize information

regarding foreign deposit and

custodial accounts reported in all

Parts V.

Line 5

Report the number of deposit

accounts reported in all

Parts V.

TIP

Line 6

Report the total maximum value of

these deposit accounts.

Line 7

Report the number of custodial

accounts reported in all Parts V.

Line 8

Report the total maximum value of

these custodial accounts.

Line 9

Indicate whether any foreign deposit

or custodial accounts were closed

during the tax year.

Part II. Other Foreign

Assets Summary

Use Part II to summarize information

regarding financial accounts (other

than foreign deposit and custodial

accounts) and other specified foreign

financial assets reported in all Parts

VI.

Line 10

Report the number of accounts and

assets reported in all Parts VI.

Line 11

Report the total maximum value of

these accounts and assets.

Line 12

Indicate whether any account was

opened or closed or any asset was

acquired or disposed of during the tax

year.

Part III. Summary of Tax

Items Attributable to

Specified Foreign

Financial Assets

Enter the following items for your total

assets reported in Part V or Part VI

and the schedule, form, or return on

which you reported the items.

•

Interest.

•

Dividends.

•

Royalties.

•

Other income.

•

Gains or (losses).

•

Deductions.

•

Credits.

-12-

Instructions for Form 8938 (Rev. 11-2021)

Page 13 of 16 Fileid: … ns/i8938/202111/a/xml/cycle05/source 14:59 - 10-Dec-2021

The type and rule above prints on all proofs including departmental reproduction proofs. MUST be removed before printing.

Part IV. Excepted

Specified Foreign

Financial Assets

If you reported a specified foreign

financial asset on certain other forms

listed below for the same tax year, you

may not have to report it on Form

8938. However, you must identify the

form where you reported the asset by

indicating how many forms you filed.

For more information, see

Duplicative Reporting, earlier. If you

reported a specified foreign financial

asset on one or more of the following

forms, enter the number of forms filed.

•

Form 3520.

•

Form 3520-A.

•

Form 5471.

•

Form 8621.

•

Form 8865.

Foreign Grantor Trusts

If you are treated as an owner of any

part of a foreign grantor trust, you may

have to file Form 8938 to report

specified foreign financial assets held

by the trust. If you are a beneficiary of

the foreign trust, you may have to file

Form 8938 to report your interest in

the trust. You do not have to report on

Form 8938 any specified foreign

financial asset held by the trust or

your interest in the trust if you report

the trust on a Form 3520, you timely

file for the tax year, and the trust