A Guide to Venture Capital Term Sheets

3 Clements Inn

London WC2A 2AZ

T 020-7025 2950

F 020-7025 2951

www.bvca.co.uk

term sheets COVER.indd 1term sheets COVER.indd 1 9/10/07 13:30:019/10/07 13:30:01

Original cover concept and guidelines by IUVO

www.iuvodesign.com

Designed and produced by Jeffrey Pellin Consultancy

www.pellin.co.uk

term sheets COVER.indd 2term sheets COVER.indd 2 9/10/07 13:30:389/10/07 13:30:38

Page

I Introduction 2

II What is a Term Sheet? 4

III The investment process 6

IV What terms may be included in a Term Sheet? 8

1. Type of share 8

2. Valuation and milestones 8

3. Dividend rights 9

4. Liquidation preference and deemed liquidation 10

5. Redemption 12

6. Conversion rights 12

7. Automatic conversion of share class/series 12

8. Anti-dilution (or price protection) 13

9.

Founder shares 14

10.

Pre-emption rights on new share issues 15

11. Right of first refusal, co-sale and tag along rights 15

12. Drag along or bring along 16

13. Representations and warranties 16

14.

Voting rights 17

15. Protective provisions and consent rights (class rights) 17

16. Board of Directors/Board Observer 18

17. Information rights 19

18.

Exit 19

19. Registration rights 20

20. Confidentiality, Intellectual Property Assignment and Management

Non-compete Agreements

20

21. Employee share option plan 21

22. Transaction and monitoring fees 21

23. Confidentiality 21

24. Exclusivity 21

25. Enforceability 22

26.

Conditions precedent 22

V Venture capital glossary of terms 23

VI Example of a Term Sheet for a Series A round 35

1

Index

W3858 Term sheets text.indd 1W3858 Term sheets text.indd 1 9/10/07 12:15:15 pm9/10/07 12:15:15 pm

The BVCA - The British Private Equity and Venture Capital Association is the industry body for the UK

private equity and venture capital industry. Our membership represents the overwhelming number

of UK-based private equity and venture capital firms and their advisers. The BVCA has many years

of experience representing the UK industry, which on the world stage is second only in size to the

United States, to government, the European Commission and Parliament, the media, regulatory and

other statutory bodies at home, across Europe and around the world. We promote the industry to

entrepreneurs and investors, as well as provide services and best practice standards to our members.

The venture capital investment process is now a well-established means of raising funds for early

stage companies, usually those involved in seeking to exploit new developments in technology or

life sciences. A privately funded company might have a number of funding rounds. The first round is

often to raise a small amount of money (seed capital), the investors often being friends and family or a

specialist early stage venture capital investor. For rounds without a venture capital investor there may or

may not be formal investment documents.

There is a big difference in the nature of venture capital investment depending on the stage of

investment and it is important to try to match the skills of an investor with those required for a particular

business. A first round of investment from venture capitalists is usually called a Series A round, with

subsequent rounds progressing through the alphabet. This Guide reviews those terms that may be

included in a Term Sheet for a Series A or for subsequent investment rounds, although not every term

discussed will be necessarily appropriate for every investment. Sometimes investments are made by

way of debt, but the majority of investments are made by way of a purchase of shares. This Guide deals

only with the latter.

The aim of this Guide is to provide those who are not familiar with the venture capital investment

process with an outline of how investments can be structured, the terms and terminology typically used

in a Term Sheet, and the broader investment process. It is hoped that this familiarity will assist those

who are trying to raise venture capital by helping them to understand the commercial implications of the

terms being offered. This in turn will hopefully expedite the negotiation of Term Sheets and completion

of the investment process.

After the section outlining the purpose of a Term Sheet, there is a section describing the investment

process with some worked examples of how the share structure alters in certain circumstances. There

is next a glossary of terms most often used in venture capital transactions. Where each term is used for

the first time in this Guide it is in italics. Finally, there is an example of a Term Sheet for a Series A round.

This has been included to show how the various terms described in this Guide might be set out in a

Term Sheet.

I Introduction

2

W3858 Term sheets text.indd 2W3858 Term sheets text.indd 2 9/10/07 12:15:16 pm9/10/07 12:15:16 pm

3

The selection of terms addressed in this Guide will not be appropriate for every venture capital

investment, but should cover most of the terms typically used in the UK today and point out a

few of the major differences with the practices in Continental European jurisdictions.

To complement this guide there are now available on the BVCA website (www.bvca.co.uk) standard

documents for venture capital investment, namely a subscription and shareholders' agreement and

articles of association, together with explanatory notes.

It should be noted that private equity is the generally accepted term used to describe the industry as a

whole, encompassing both management buy-out and buy-in activity and venture capital which relates

exclusively to the seed through to expansion stages of investment. This Guide is relevant primarily to

only the venture capital stages of investment and so this will be the term used.

The BVCA and I would like to thank the Venture Committee working group for the time and effort

made in preparing this Guide. This was co-chaired by John Heard (Abingworth Management Ltd) and

Simon Walker (Taylor Wessing) and also included Frédéric Court (Advent Venture Partners), Rob James

(DFJEspirit Capital Partners LLP), Roy Merritt (OrCapital), and Jeppe Zink (Amadeus Capital Partners).

Jo Taylor

Chairman, BVCA Venture Committee

October 2007

W3858 Term sheets text.indd 3W3858 Term sheets text.indd 3 9/10/07 12:15:16 pm9/10/07 12:15:16 pm

4

II What is a Term Sheet?

A Term Sheet is a document which outlines the key financial and other terms of a proposed investment.

Investors use a Term Sheet as a basis for drafting the investment documents. With the exception

of certain clauses – commonly those dealing with confidentiality, exclusivity and sometimes costs

– provisions of a Term Sheet are not usually intended to be legally binding. In addition to being subject

to negotiation of the legal documentation, a Term Sheet will usually contain certain conditions which

need to be met before the investment is completed and these are known as conditions precedent (see

paragraph 26, Section IV).

If a company seeks to raise venture capital in the UK the principal documents needed for an

investment round are generally a Subscription Agreement, a Shareholders' or Investors' Rights

Agreement (frequently these are combined into a single Subscription and Shareholders' Agreement or

Investment Agreement) and Articles of Association. The provisions of a Term Sheet will be included in

these documents.

The Subscription Agreement will usually contain details of the investment round, including number and

class of shares subscribed for, payment terms and representations and warranties (see paragraph 13,

Section IV) about the condition of the company. These representations and warranties will be qualified

by a disclosure letter and supporting documents that specifically set out any issues that the founders

believe the investors should know prior to the completion of the investment.

A Shareholders' or Investors' Rights Agreement will usually contain investor protections, including

consent rights (see paragraph 15, Section IV), rights to board representation and non-compete

restrictions. The provisions in this Agreement will hopefully be used as the basis for corresponding

provisions on subsequent funding rounds. The Articles of Association will include the rights attaching

to the various share classes, the procedures for the issue and transfer of shares and the holding of

shareholder and board meetings.

Some of the protective provisions in the Shareholders' Agreement may instead be contained (or indeed)

repeated in the Articles of Association. The decision to include terms in one or both of these documents

may be jurisdiction-specific, based primarily on company law restrictions (e.g. some Continental

European jurisdictions limit the rights that can be attached to clauses in the Articles of Association),

enforceability concerns (the investor protections can be difficult to enforce in some Continental

European jurisdictions) and confidentiality concerns (Articles of Association typically must be filed as a

public document with a relevant company registry while the other investment documents can often be

kept confidential).

A venture capital investment round is usually led by one venture capital firm. That firm will put together

a syndicate either before or after the Term Sheet is agreed and then co-ordinate the syndicate until the

round is completed. The syndicate will usually comprise some or all of the existing investors and some

new ones, one of whom will typically lead the round.

W3858 Term sheets text.indd 4W3858 Term sheets text.indd 4 9/10/07 12:15:16 pm9/10/07 12:15:16 pm

5

There are two main sources of institutional venture capital funding for Series A investment and beyond:

venture capital funds, including venture capital trusts (VCTs) and corporate strategic investors.

Once agreed by all parties, lawyers use the Term Sheet as a basis for drafting the investment documents.

The more detailed the Term Sheet, hopefully the fewer the issues which will need to be agreed during

the drafting process. The process can be complex and working with lawyers who are familiar with

venture capital transactions is recommended in order to minimise both timeframe and costs.

W3858 Term sheets text.indd 5W3858 Term sheets text.indd 5 9/10/07 12:15:16 pm9/10/07 12:15:16 pm

6

In order to help explain some of the concepts that will be contained in this Guide this section follows

a company through several stages of its life cycle from establishment to its Series A funding round.

This example should not be taken as representing a standard process or representing typical

valuations or percentage ownerships. At each stage each case will be different and will need

to be handled on an individual basis.

‘NewCo’ is a company spun out from an academic institution to exploit intellectual property developed

by the scientist (the founder) whilst working as an employee of that institution. The academic institution

has agreed to transfer (assign) its ownership rights in the intellectual property rights (IPR) to NewCo in

return for a 50% shareholding in the business. It has also agreed that the founder who has carried out

the research that led to the creation of the IPR should own the other 50% through a holding of founder

shares (see paragraph 9, Section IV). The capital structure of NewCo is as set out in Box 1.

Box 1. Capital structure for NewCo following establishment of the company and assignment

of intellectual property

The investment by the founder is satisfied by a cash payment and the investment by the academic

institution is satisfied by the transfer of IPR to NewCo. However, individuals who are acquiring shares

in NewCo and are also going to be employees should take tax advice before the shares are acquired

because of recently introduced regulations in the UK.

With the help of the academic institution and the founder's network of contacts, NewCo then

successfully attracts the investment of a venture capital company (seed investor) that specialises in

investing in very early stage companies.

On the basis of the world-class reputation of the scientist, the strength of the IPR and the potential

market for the products arising from the technology, the seed investor and NewCo agree that the pre-

money valuation (see paragraph 2, Section IV) for its business is £200,000. From discussions between

the seed investor and NewCo it is also agreed that the company needs to raise £200,000 to enable it

to carry out some key experiments to establish the proof of principle for the technology and therefore

enable it to raise its next funding round. The seed investor also requires that an option pool (see

paragraph 21, Section IV) be established that could be used to help attract new staff to join NewCo.

III The investment process

Start-up

Number of ordinary shares

Cash or cash equivalent

invested at £1 per share

Founder 50 £50

Institution 50 £50

Undiluted share capital 100

W3858 Term sheets text.indd 6W3858 Term sheets text.indd 6 9/10/07 12:15:17 pm9/10/07 12:15:17 pm

7

With these parameters agreed the capital structure of NewCo following the investment by the seed

investor is as set out in Box 2.

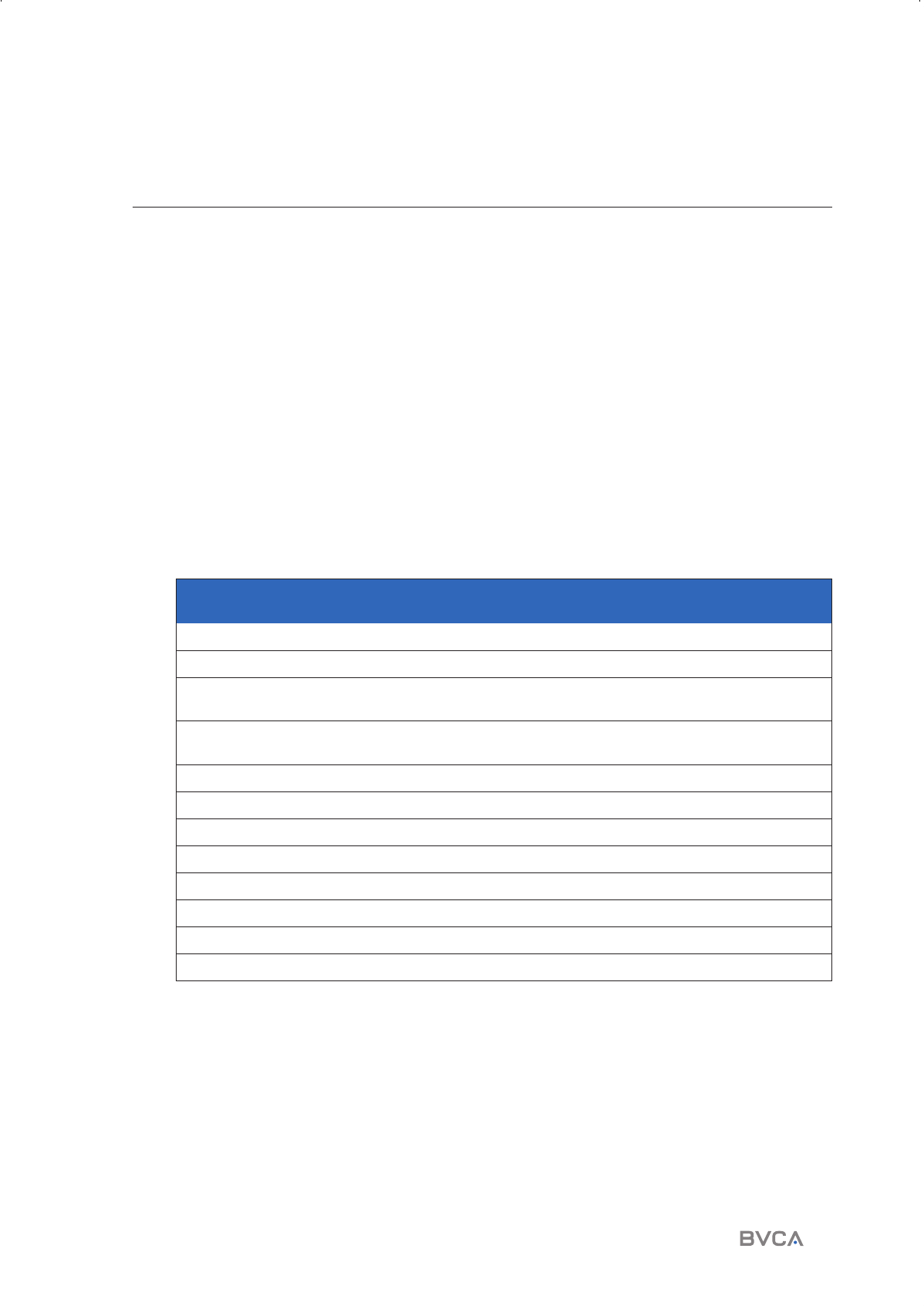

Box 2. Capital structure following seed round

Seed round

Cash or

cash

equivalent

invested

Number of

'A' shares

issued at

this round

Undiluted

total

ordinary

shares and

'A' shares

Options

Fully

diluted

equity

Value of

shares

Founder(s) £50 0 50 0 50 £100,000

Institution £50 0 50 0 50 £100,000

Seed investment £200,000 100 100 0 100 £200,000

Option pool 20 20

Total £200,100 100 200 20 220 £400,000

W3858 Term sheets text.indd 7W3858 Term sheets text.indd 7 9/10/07 12:15:17 pm9/10/07 12:15:17 pm

8

IV What terms may be included in a Term Sheet?

1. Type of share

A venture capital investor will normally only subscribe to a preferred class of shares. These are

shares to which certain rights attach, that are not shared by ordinary shares held by the founders

and others. Venture capital investors require these additional rights because in most cases they

are investing much larger sums than the founders (whose investment usually takes the form of

good ideas, time and a small amount of seed money) and at a much higher valuation. The venture

capital investors will also have less control over the company’s day-to-day operations than the

founders, who typically remain closely involved in management.

If a preferred share class already exists at the time of an investment round, the new round of

investors will typically create a new series of preferred shares to distinguish the rights (voting,

financial, etc.) that attach to their preferred series from those that attach to all prior series of

shares. Distinguishing the rights enjoyed by different series is common practice because the

investments made at the time of the creation of each series are usually based on different

company valuations and circumstances and, consequently, have different risk profiles.

In some Continental European jurisdictions, there are restrictions on the types of different shares

classes permissible. This can be compensated for to an extent by creating special rights for

certain shareholders in the investment documentation.

2. Valuation and milestones

The venture capital investors will agree with the company on a valuation for the company prior

to the new investment round (the pre-money valuation). The pre-money valuation is used to

determine the price per share to be paid by investors on the completion of the new investment

round (the purchase price). The purchase price is calculated by dividing the pre-money valuation

by the fully diluted number of shares of the company immediately prior to the time of completion.

In the example in Section III the pre-money valuation agreed is £200,000 and immediately prior to

completion there are 100 ordinary shares. The value of those shares and therefore the purchase

price of the incoming investor is £200,000/100 which equals £2,000 per share.

Fully diluted usually includes shares that have been issued by the company, shares allocated to

the employee option pool (see paragraph 21 below) and any other shares which the company

could be required to issue through options, warrants, convertible debt or other commitments.

The pre-money valuation should be distinguished from the post-money valuation, which refers

to the valuation of the company immediately following (and which includes the investment

proceeds from) the new round. Therefore, following completion of the example in Section III,

NewCo has an undiluted post-money valuation of £400,000 represented by £200,000 pre-money

valuation and £200,000 of investment. If the option pool is included in the calculation the fully

diluted post-money valuation is £440,000 i.e. £2,000 x (200 shares + 20 options).

W3858 Term sheets text.indd 8W3858 Term sheets text.indd 8 9/10/07 12:15:17 pm9/10/07 12:15:17 pm

9

Quite often, venture capital investors will not wish to make all of their investment on completion.

Instead they will invest in tranches, subject to various technical and/or commercial targets

(milestones) being met. These milestones will be set out in the Subscription Agreement. Failure

to meet a milestone does not automatically mean that the investors will not provide the additional

money, but it may mean that they will seek to negotiate different terms for these amounts.

Sometimes a mechanism, a ratchet is used to adjust the respective shareholdings of the investors

and the founders depending on either the company's performance or the level of returns on an

exit (exit ratchet). This technique is principally used to find a bridge between widely differing

views of a company's value, or to provide additional incentives/rewards to the founders for

delivering excellent returns to the investors. Ratchets can be complicated in operation and need

to be very carefully thought through due to tax issues and in order to avoid conflicts of interest

between the founders, the company and its other shareholders at a later date

3. Dividend rights

Venture capital investors often invest in early stage companies that are in an intense growth

phase. The objective is to grow the business and its value and to realise a return on investment

(ROI), typically targeting a multiple of the amounts invested – on exit. In most cases such

companies should be reinvesting all profits (without which a dividend cannot be paid) to

continue growing the company, rather than paying dividends to shareholders. Sometimes there

is a prohibition on the payment of any dividend, which may be for a limited period of time.

Even if the payment of a dividend is permitted, a common way of ensuring that a company is not

obliged to pay dividends while it is growing is to provide the investors with a share class that has

a preferential, cumulative dividend, usually fixed at a percentage of the purchase price paid for

each preferred share. The company will also be prevented from paying any dividend to other

shareholders until the dividend is paid to the holders of the preferred shares. Since that dividend

cumulates usually until an exit (see paragraph 18 below), it effectively prevents any other

dividend being paid until then. In addition, investors will often have an overriding right to veto

the payment of any dividend.

If a dividend is cumulative, it means that for each period that the dividend accrues (e.g. quarterly

or annually) any amounts not paid are cumulated until the company has the necessary cash.

At that time the cumulated accrued amounts must be paid to the investors’ share class in their

entirety, before any dividends can be paid to other share classes. If the preferred shares are

converted into ordinary shares, the investors will usually expect all accumulated dividends to be

paid or capitalised into ordinary shares on such conversion.

W3858 Term sheets text.indd 9W3858 Term sheets text.indd 9 9/10/07 12:15:18 pm9/10/07 12:15:18 pm

10

IV What terms may be included in a Term Sheet? continued

In addition to a dividend preference, venture capital investors typically require that the preferred

shares be entitled to participate in any distributions on the ordinary shares, or in other words,

to enjoy a pro rata share of any dividends paid to the ordinary shares on top of any dividend

preference paid only to the preferred shares. Allowing preferred participation ensures that a

company cannot declare a small preferential dividend to the preferred holders followed by a

much larger dividend to the ordinary shareholders.

In some jurisdictions, escalating dividend provisions can be used to encourage the company

to work towards an exit and to help its investors recover some of their investment if the

company fails. These require the company, if it has not achieved a successful exit (see paragraph

18 below) within a certain period of time, to declare and pay cumulative dividends to preferred

shareholders at rates that increase each year.

4. Liquidation preference and deemed liquidation

The liquidation preference is a right which can be required by venture capital investors in

recognition of the risk they bear on their capital contribution. While there are many variations,

the liquidation preference typically provides that, in the event the company is liquidated or

subject to a deemed liquidation (see below), the preferred shareholders will receive a certain

amount of the proceeds before any other shareholders. This preference amount may be equal to

the amount of the preferred shareholders’ investment, or a multiple of it.

The remaining proceeds are often then shared amongst the preferred and ordinary shareholders.

There are numerous ways in which this may be effected, but the most common are:

●

the remaining proceeds are shared pro rata, according to their percentage shareholding,

among the preferred and ordinary shareholders (in which case the preferred shares are

considered fully participating, i.e. after receiving the preference amount, the preferred

shareholders participate fully with the ordinary shareholders in sharing the remaining proceeds);

●

after payment of the liquidation preference amount, the ordinary shareholders may catch

up by receiving an amount equal to the amount paid by them or credited as paid by them

for their shares, thereafter the proceeds being shared out on a pro rata basis between all

shareholders (in which case the preferred shares are considered simple participating).

The size and structure of the liquidation preference will be negotiated to reflect the risk inherent

in each investment round: the higher the risk, the higher the required return. Many factors

(including the valuation of the company) will be considered in this calculation.

W3858 Term sheets text.indd 10W3858 Term sheets text.indd 10 9/10/07 12:15:18 pm9/10/07 12:15:18 pm

11

Venture capital investors usually require that the liquidation preference applies not only in connection

with a liquidation or winding up of the company, but also in the case of a deemed liquidation, a term

usually defined to include a merger, acquisition, change of control or consolidation of the company, or a

sale of all or most of its assets, but sometimes also includes an initial public offering (IPO) or a qualified

exit (see paragraph 18 below).

The example below shows what would happen if there were liquidity events at the value

of £200,000 or £1,000,000 in each of the following scenarios (all of which assume a fully

participating liquidation preference based upon the issued share capital following the seed round

described in Box 2 of Section III):

●

Where there is no liquidation preference attached to the 'A' shares

●

1 x liquidation preference

●

2 x liquidation preference.

In this example, in the event the company is only sold for £200,000 the investor will only get his

money back if he has negotiated a liquidation preference so that the first £200,000 from such an

event goes to the investor. In the event of a sale at £1,000,000 the calculation works so that in the

event of 1x preference the first £200,000 goes to the investor and then the remaining £800,000 is

shared pro rata in accordance with the shareholding, in this case 50:25:25.

Liquidated

preference

Investor

None

1x

2x

University

None

1x

2x

Founder

None

1x

2x

Percentage

shareholding

50%

25%

25%

£1,000,000 liquidity event cash return

£500,000

£200,000 (preference)

£400,000 (share in £800,000 balance)

£400,000 (preference)

£300,000 (share in £600,000 balance)

£250,000

£200,000

£150,000

£250,000

£200,000

£150,000

£100,000

£200,000

£200,000

£50,000

0

0

£50,000

0

0

£200,000 liquidity

event cash return

W3858 Term sheets text.indd 11W3858 Term sheets text.indd 11 9/10/07 12:15:18 pm9/10/07 12:15:18 pm

12

IV What terms may be included in a Term Sheet? continued

5. Redemption

The right of redemption is the right to demand under certain conditions that the company buys

back its own shares from its investors at a fixed price. This right may be included to require a

company to buy back its shares if there has not been an exit within a pre-determined period.

Failure to redeem shares when requested might result in the investors gaining improved rights,

such as enhanced voting rights.

A right of redemption is not appropriate for every investment and is not allowed or is limited

(e.g. to a certain percentage of the issued and outstanding shares) in some jurisdictions in

Continental Europe. In those parts of Europe where it is allowed, subject to certain restrictions,

redemption can be used to ensure that the venture capital investors recover some of their

investment if a company has not been able to achieve a successful exit (see paragraph 18 below)

within a certain period of time. However, in the UK and certain other jurisdictions, there are legal

requirements that must be satisfied before a company can redeem any of its shares.

A right of redemption can also be used by an investor where it needs to strongly discourage

a company from breaching certain obligations, by providing a way for the investor to dispose

quickly of its shareholding. In jurisdictions where redemption is not possible under local company

law, an alternative is to negotiate a conditional right for the investors to put (sell) their shares to

the founders at a fixed price.

6. Conversion rights

Where venture capital investors hold a preferred class of shares and it is permitted to convert

these to ordinary shares, they generally require the right to convert them at any time, at an initial

conversion ratio of 1:1. Conversion is normally delayed until exit so that investors are able to

avoid losing the rights attached to the preferred class of shares.

This conversion ratio will be adjusted to take account of any reorganisation of a company's capital

structure. In some jurisdictions, this conversion ratio can be adjusted to provide for a form of

anti-dilution protection (see paragraph 8 below). If a dilutive event has occurred and this ratio

has been increased, the investor may choose or may be compelled to convert its preferred shares

into ordinary shares immediately prior to a liquidity event (such as a trade sale or an IPO).

7. Automatic conversion of share class/series

In most cases, investors will be required to convert all of their shares into ordinary shares prior

to a company listing its shares on a publicly traded exchange. Venture capital investors often

require an automatic conversion mechanism for all share classes, effective immediately prior to an

IPO. Investors will only want this conversion mechanism to work where an IPO is likely to provide

W3858 Term sheets text.indd 12W3858 Term sheets text.indd 12 9/10/07 12:15:19 pm9/10/07 12:15:19 pm

13

a sufficient opportunity for them to dispose of their shares (liquidity) after the expiry of any lock

up periods. Accordingly the investors usually define certain criteria in advance that must be

met for an IPO to trigger automatic conversion (usually referred to as a Qualified IPO), e.g. only

offerings on certain exchanges, by recognised national underwriters, at a valuation exceeding a

certain threshold and raising at least a minimum amount of gross proceeds. Otherwise, preferred

shareholders would risk having their shares converted and losing all of their preferential rights

even if the company lists its shares at a low value on a minor exchange.

8. Anti-dilution (or price protection)

Venture capital investors often require anti-dilution protection rights to protect the value of

their stake in the company, if new shares are issued at a valuation which is lower than that at

which they originally invested (a down round). This protection usually functions by applying a

mathematical formula to calculate a number of new shares which the investors will receive, for no

or minimal cost, to offset the dilutive effect of the issue of cheaper shares.

There are several variations of the formula, each providing different degrees of protection. These

include full ratchet protection, which will maintain investors' full percentage ownership at the

same level or at the same value in down rounds. Other versions of the formula provide some

compensation for the dilution, but allow the ownership percentage to fall; the most common of

these is weighted average. The level of protection required by an investor depends on several

factors, including the valuation of the company at the time of the investment and the perceived

exposure to further financing requirements.

While the basic concept remains the same, there are several different mechanisms used in

Continental European jurisdictions to create this protection. In the UK, the mechanism of

adjusting the conversion ratio of preferred shares to ordinary shares to adjust for dilutions can be

used, although other methods, including the issue of shares for a nominal sum or bonus shares,

are also used. The latter might involve the granting of options (or warrants as they are sometimes

referred to), which are only exercisable if the anti-dilution provision is triggered.

In the example set out in Box 2 of Section III, if the project did not proceed as well as expected

and when the time came to raise another round from new investors it emerged that these

potential new investors were only prepared to invest at a pre-money valuation (for them) of

£200,000, this would imply that they would only pay £1,000 per share (£200,000/200). However

the existing investors paid £2,000 per share and therefore, under full anti-dilution provisions,

their shareholding would be adjusted in order to issue them with new shares, the effect of which

would be to bring the price they paid for the 'A' shares to £1,000 per share.

W3858 Term sheets text.indd 13W3858 Term sheets text.indd 13 9/10/07 12:15:19 pm9/10/07 12:15:19 pm

14

IV What terms may be included in a Term Sheet? continued

The result of the full anti-dilution provisions is that the existing investors would have to be

issued with a further 100 shares to bring their shareholding to 200 for which they paid a total

of £200,000 which equals £1,000 per share. In terms of the overall shareholding this brings the

ownership of the business between the founders, academic institution and investors to 50 shares:

50 shares: 200 shares or 16.6%:16.6%:66.6% (a change from 50 shares: 50 shares: 100 shares or

25%:25%:50%).

9. Founder shares

Founders and senior management are usually central to the decision of venture capital investors

to put money into a company. Having decided to put money behind a management team they

have confidence in, investors are usually keen to ensure that they remain in place to deliver their

business plan. Therefore, it is often the case that founders and key managers (and sometimes

all shareholders/employees who leave the company within a certain period of time are required

to offer to sell their shares back to the company or to other shareholders. The price paid for the

shares may depend upon circumstances of departure – it may be at market value if the founder/

manager is deemed to be a good leaver, or it might be considerably less in the case of a bad

leaver. A bad leaver may be someone who has breached his contract of employment, or it may

also be someone who resigns from the company within a particular period. The Board often

retains the right to determine whether to implement the bad leaver provisions.

In addition or as an alternative to good leaver/bad leaver provisions, investors may require that

shares held by founders who are employees or consultants be subject to a vesting schedule

in order to incentivise the founders not to leave employment with the company in the short

term. The effect of this is that anyone holding such shares must be employed or engaged as a

consultant by the company for a certain period of time if that person is to obtain unrestricted

ownership of all of their shares. Within that period shares may vest on a straight-line basis

or on whatever basis is negotiated. Sometimes founders have different vesting schedules in

recognition of their different levels of contribution to the company.

In NewCo it was decided that the founder's 50 shares would vest on a straight-line basis over 4

years, with the first year's allocation vesting on the completion of the venture capital investment.

Number of shares

0 months –

12 months

12 months –

24 months

24 months –

36 months

36 months –

48 months

Annual vesting % 12.5 12.5 12.5 12.5

Cumulative vesting % 12.5 25 37.5 50

W3858 Term sheets text.indd 14W3858 Term sheets text.indd 14 9/10/07 12:15:19 pm9/10/07 12:15:19 pm

15

If a founder leaves within the requisite period, he will keep only that proportion of his shares that

are deemed to be vested. In this example, if the founder left between 12-24 months, 25 shares

or 50% of the shareholding would have vested. The remaining shares that are unvested lose

their value, either by being bought back by the company for a nominal amount or converted into

deferred shares which have no rights attaching to them. It may be decided that on certain events

such as death or incapacity or where a founder's employment may terminate through no fault of

their own, the vesting schedule is accelerated either partially or fully. The Board may retain the

right to determine such issues at the time, in the light of circumstances.

10. Pre-emption rights on new share issues

If the company makes any future share offering, a venture capital investor will require the right

to maintain at least its percentage stake in the company by participating in the new offering up

to the amount of its pro rata holding, under the same terms and conditions as other participating

investors. This pre-emption right is automatically provided for by law in the UK and most

Continental European jurisdictions, although it can be waived.

If the new offering is based on a company valuation lower than that used for an investor’s prior

investment, that investor may also receive shares under its anti-dilution rights (see paragraph 8

above). Certain issues will usually be exempted from the pre-emption rights, including the issue

of anti-dilution shares and the issue of shares on the exercise of share options.

11. Right of first refusal, co-sale and tag along rights

These are contractual terms between shareholders which are usually included in the Articles

of Association. If one shareholder wishes to dispose of shares that are subject to a right of first

refusal (ROFR), it must first offer them to those other shareholders who have the benefit of

the ROFR. There are usually certain exceptions to the ROFR, such as the right of individuals to

transfer shares to close relatives and trusts and investors to transfer shares freely to third parties,

each other or within an investor's group. The requirement to go through a ROFR process may

add several weeks to the timescale for selling shares.

If a shareholder wishes to dispose of shares that are the subject of a co-sale or tag along right,

the other shareholders who benefit from the right can insist that the potential purchaser agrees

to purchase an equivalent percentage of their shares, at the same price and under the same terms

and conditions. This may have the effect of making the shares more difficult to sell.

W3858 Term sheets text.indd 15W3858 Term sheets text.indd 15 9/10/07 12:15:20 pm9/10/07 12:15:20 pm

16

IV What terms may be included in a Term Sheet? continued

A venture capital investor’s decision to invest in a company is often based largely on the strength

of the technical and management experience of the founders and management. It does not

want these individuals to dispose of their shares in the company while it remains an investor.

Consequently, investors frequently require a ROFR as well as co-sale/tag along rights on any sale

of shares by a founder or key managers. Indeed they may sometimes require a prohibition on

founders and key managers selling shares for a stated period.

Sometimes in the UK the investor class will create a ROFR on each other's shares. Some investors

are strongly against this because it can make their shares more difficult to sell (less liquid) and

potentially less valuable since a prospective buyer will often be reluctant to make an offer for

shares that can be pre-empted by someone else.

12. Drag along or bring along

A drag along provision (sometimes called bring along) creates an obligation on all shareholders

of the company to sell their shares to a potential purchaser if a certain percentage of the

shareholders (or of a specific class of shareholders) vote to sell to that purchaser. Often in early

rounds drag along rights can only be enforced with the consent of those holding at least a

majority of the shares held by investors. These rights can be useful in the context of a sale where

potential purchasers will want to acquire 100% of the shares of the company in order to avoid

having responsibilities to minority shareholders after the acquisition. Many jurisdictions provide

for such a process, usually when a third party has acquired at least 90% of the shares (sometimes

referred to as a squeeze out), but the legal process is usually subject to possible court review.

Venture capital investors may require that certain exceptions are included in drag along

provisions for situations when they cannot be obligated to sell their shares. Among these are drag

along sales where the investors will not receive cash or marketable securities in return for their

shares or will be required to provide to the purchaser representations and warranties concerning

the company (or indemnify those given by the company or the founders) or covenants (such as

non-compete and non-solicitation of employees).

13. Representations and warranties

Venture capital investors expect appropriate representations and warranties to be provided

by key founders and management and, in jurisdictions where it is allowed, the company. The

primary purpose of the representations and warranties is to provide the investors with a complete

and accurate understanding of the current condition of the company and its past history so that

the investors can evaluate the risks of investing in the company prior to subscribing for its shares.

The representations and warranties will typically cover areas such as the legal existence of the

W3858 Term sheets text.indd 16W3858 Term sheets text.indd 16 9/10/07 12:15:20 pm9/10/07 12:15:20 pm

17

company (including all share capital details), the company’s financial statements, the business

plan, assets (in particular intellectual property rights), liabilities, material contracts, employees

and litigation.

It is very rare that a company is in a perfect state! The warrantors have the opportunity to set out

issues which ought to be brought to the attention of the new investors via the disclosure letter

or schedule of exceptions. This is usually provided by the warrantors and discloses detailed

information concerning any exceptions to or carve-outs from the representations and warranties

(e.g. specific company assets, contracts, shareholders, employees, etc.). If a matter is referred to

in the disclosure letter the investors are deemed to have notice of it and will not be able to claim

for breach of warranty in respect of that matter.

Investors expect those providing representations and warranties about the company to back

them up with a contractual obligation to reimburse them in the event that the representations and

warranties are inaccurate or if there are exceptions to them that have not been fully disclosed.

There are usually limits to the exposure of the warrantors, which are a matter for negotiation

when documentation is being drawn up, and vary according to the severity of the breach, the

size of the investment and the financial resources of the warrantors.

14. Voting rights

Venture capital investors will have certain consent and voting rights that attach to their class of

shares (see paragraph 15 below). Preferred shares may have equivalent voting rights to ordinary

shares in a general meeting, though it is also possible that they may carry more than one vote per

share under certain circumstances in jurisdictions where it is allowed.

Where an appropriate event has occurred that triggers a change in the conversion ratio, the

number of votes that the investors' shares will carry for any subsequent general shareholder

vote will often be automatically adjusted to reflect the change in the conversion ratio at the

time of the vote.

15. Protective provisions and consent rights (class rights)

The venture capital investors in an investment round normally require that certain actions cannot

be taken by the company without the consent of the holders of a majority (or other specific

percentage) of their class or series of shares (investor majority). Sometimes these consent rights

are split between consent of an investor majority, consent of the investor director(s) or consent of

the Board. Typically what requires investor majority consent and what requires investor director

consent would relate to major changes in the company such as those set out in the paragraph

below whereas operational matters that need more urgent consideration by the Board would

W3858 Term sheets text.indd 17W3858 Term sheets text.indd 17 9/10/07 12:15:20 pm9/10/07 12:15:20 pm

18

IV What terms may be included in a Term Sheet? continued

be left for board consent. Alternatively, each of the largest investors may have specific consent

rights. The purpose of these rights is to protect the investors from the company taking actions

which may adversely affect the value of their investment.

The types of actions covered include (among many others): changes to share classes and share

rights, changes to the company’s capital structure, issuance of new shares, mergers and acquisitions,

the sale of major assets, winding up or liquidating the company, declaring dividends, incurring debts

above a certain amount, appointing key members of the management team and materially changing

the company’s business plan. These shareholder rights are particularly important for investors who

do not appoint a director to the Board of Directors (see paragraph 16 below).

Note that in some Continental European jurisdictions, local company law requires that some of

the actions covered by these consent rights remain the unfettered right of the Board of Directors

to decide. In such cases, the Articles of Association of the company will usually require that the

level of majority needed for a board decision concerning these actions include the agreement of

an appropriate number of the directors appointed by the investors.

Alongside these consent rights, there are usually various undertakings or covenants given by the

company or sometimes the founders to do certain acts. Typically these include taking steps to

protect intellectual property, applying investment monies in accordance with the business plan

and maintaining appropriate insurance. Other types of covenants are described in the sections

below headed Information Rights (see paragraph 17 below) and Confidentiality, Intellectual

Property Assignment and Management Non-compete Agreements (see paragraph 20 below).

16. Board of Directors/Board Observer

Venture capital investors require that the company has an appropriate Board of Directors

(note: in some Continental European jurisdictions, e.g. Germany, a two-tiered board is required:

a Management Board and a Supervisory Board and in other Continental European jurisdictions

where two-tiered board systems are optional, e.g. France, some investors prefer one board).

In accordance with what is regarded as UK corporate governance best practice, investors

usually prefer the Board to have a majority of non-executive directors (i.e. directors who are

not employees of the company). Although a majority of non-executives may be impractical for

small companies, it is usual for such companies to have at least one or two non-executives. One

or more of the non-executive directors will be appointed by the investors under rights granted

to them in the investment documentation. Some investors will never appoint a director, because

of potential conflicts of interest and liability issues and will instead require the right to appoint a

Board Observer, who can attend all board meetings, but who will not participate in any board

decisions. The Board of Directors tends to meet once a month in general, in particular for early

stage companies with active investors on the Board.

W3858 Term sheets text.indd 18W3858 Term sheets text.indd 18 9/10/07 12:15:21 pm9/10/07 12:15:21 pm

19

In many cases, investors will require that the Board has a Remuneration or Compensation

Committee to decide on compensation for company executives, including share option grants

(see paragraph 21 below), as well as an Audit Committee to oversee financial reporting. These

committees will be made up entirely or of a majority of non-executive directors and will include

the directors appointed by the investors. Each of these committees should have its own mandate

set out in writing.

By law, like all directors, the investor directors' responsibilities are to act in the interest of the

company rather than as a representative of the funds that they manage. Often venture capitalists

separate the investment decisions for the funds invested in the companies from the investor

director's decisions in order to avoid conflicts of interests for the investor director. This is typically

done by having another investment executive representing the funds' interests when dealing

with the company with respect to the Investor consent matters.

17. Information rights

In order for venture capital investors to monitor the condition of their investment, it is essential

that the company provides them with certain regular updates concerning its financial condition

and budgets, as well as a general right to visit the company and examine its books and records.

This sometimes includes direct access to the company's auditors and bankers. These contractually

defined obligations typically include timely transmittal of audited annual financial statements,

annual budgets, and unaudited monthly and quarterly financial statements. However it should

be noted that in some Continental European jurisdictions, a company is required to treat all

shareholders equally, so that any information provided to one shareholder will have to be provided

to all shareholders.

18. Exit

Venture capital investors want to see a path from their investment in the company leading to

an exit, most often in the form of a disposal of its shares following an IPO or by participating

in a sale. Sometimes the threshold for a liquidity event (see paragraph 4 above) or conversion

(see paragraph 6 above) will be a qualified exit. If used, it will mean that a liquidity event will

only occur and conversion of preferred shares will only be compulsory if an IPO falls within the

definition of a qualified exit. A qualified exit is usually defined as a sale or IPO on a recognised

investment exchange which in either case is of a certain value to ensure the investors get a

minimum return on their investment.

Consequently, investors usually require undertakings from the company and other shareholders

that they will endeavour to achieve an appropriate share listing or trade sale within a limited

W3858 Term sheets text.indd 19W3858 Term sheets text.indd 19 9/10/07 12:15:21 pm9/10/07 12:15:21 pm

20

IV What terms may be included in a Term Sheet? continued

period of time (typically five to seven years depending on the stage of investment and the maturity

of the company). If such an exit is not achieved, investors often build in structures which will allow

them to withdraw some or all of the amount of their investment (see paragraphs 3 and 5 above).

19. Registration rights

Registration rights are a US securities law concept that is alien to many European companies and

investors. Such rights are needed because securities can only be offered for public sale in the

US (with certain exceptions) if they have first been registered with the Securities and Exchange

Commission (SEC). The registration process involves the company whose shares are to be

offered providing significant amounts of information about its operations and financial condition,

which can be time consuming and costly.

Unlike in European jurisdictions, where all of a company’s shares usually become tradable upon

a public listing, a company registering shares to be traded in the US is not required to register

all of its outstanding shares. Any shares that are left unregistered can only be traded under very

restricted circumstances, which can greatly diminish their value. Consequently, investors in the

US or in companies which may consider pursuing a listing in the US, usually require the company

to enter into a Registration Rights Agreement. Among other things, this gives the investors rights

to demand registration of their shares (demand rights) and to have their shares registered along

with any other shares of the company being registered (piggy-back rights) and allocates costs

and potential liabilities associated with the registration process.

20. Confidentiality, Intellectual Property Assignment and Management Non-compete

Agreements

It is good practice for any company to have certain types of agreements in place with its

employees. For technology start-ups, this generally includes Confidentiality Agreements (to

protect against loss of company trade secrets, know-how, customer lists, and other potentially

sensitive information), Intellectual Property Assignment Agreements (to ensure that intellectual

property developed by academic institutions or by employees before they were employed by the

company will belong to the company) and Employment Contracts or Consultancy Agreements

(which will include provisions to ensure that all intellectual property developed by a company's

employees belongs to the company). Where the company is a spin-out from an academic

institution, the founders will frequently be consultants of the company and continue to be

employees of the academic institution, at least until the company is more established.

Investors also seek to have key founders and managers enter into Non-compete Agreements

with the company. In most cases, the investment in the company is based largely on the value

of the technology and management experience of the management team and founders. If they

W3858 Term sheets text.indd 20W3858 Term sheets text.indd 20 9/10/07 12:15:21 pm9/10/07 12:15:21 pm

21

were to leave the company to create or work for a competitor, this could significantly affect the

company’s value. Investors normally require that these agreements be included in the Investment

Agreement as well as in the Employment/Consultancy Agreements with the founders and senior

managers, to enable them to have a right of direct action against the founders and managers if

the restrictions are breached.

21. Employee share option plan

An employee share option plan (ESOP) is a plan that reserves and allocates a percentage of

the shares of the company for share option grants to current and future employees of the

company (and certain other individuals) at the discretion of a management committee. The

intention is to provide an incentive for the employees by allowing them to share in the financial

rewards resulting from the success of the company. Investors typically want 10%-20% of the

share capital of the company to be reserved in an ESOP creating an option pool. The company

will then be able to issue the shares under the plan without requiring further approval from the

investors. Founders and other management with significant shareholdings may be excluded from

participating in the ESOP.

22. Transaction and monitoring fees

Venture capital investors are usually paid a fee by the company to cover internal and external

costs incurred in connection with the investment process. Some investors may require an annual

monitoring fee to compensate for the level of their involvement with the investee company, in

addition to the usual compensation for travel and out-of-pocket expenses with relation to the

investment management.

23. Confidentiality

All exchanges of confidential information between potential venture capital investors and the

company need to be subject to a Confidentiality Agreement. This agreement should be executed

as soon as discussions with the company about a potential investment begin. If this has not been

done then a confidentiality restriction should be included in the Term Sheet.

24. Exclusivity

Once a Term Sheet is signed, venture capital investors will undertake various types of due

diligence on the company (any or all of technical, commercial, legal and financial). They will

usually provide the company with a list of areas which they would like to cover and information

which they would like to receive. The process can take several weeks or even months and

the investors may also use third party advisors to assist them in the process (e.g. lawyers,

W3858 Term sheets text.indd 21W3858 Term sheets text.indd 21 9/10/07 12:15:21 pm9/10/07 12:15:21 pm

22

accountants and consultants). This will involve expense and the investors will not want to

discover that while they are incurring this expense the company accepts investment from other

investors. To protect themselves, some investors will ask for an exclusivity period during which

the company is prohibited from seeking investment from any third parties. A breach of this

obligation will result in the company and founders incurring a financial penalty.

25. Enforceability

With the exception of clauses dealing with confidentiality, transaction fees and exclusivity, the

provisions of a signed Term Sheet will not be intended to be legally binding. It should, however,

be noted that in some Continental European jurisdictions there is an obligation to act in good

faith when deciding not to proceed with an investment either at all or on the terms set out in the

Term Sheet. If so, it might not be possible for the investors or the company to walk away from or

unilaterally seek to change the Term Sheet without a justifiable reason.

26. Conditions precedent

A full list of conditions to be satisfied before investment will be included in the Term Sheet. A

venture capital investment will usually be conditional on not only the negotiation of definitive

legal documents, but the satisfactory completion of due diligence and approval by the Investment

Committee of each of the venture capital investors.

Satisfactory completion of due diligence can include conclusion of commercial, scientific and

intellectual property due diligence, a review of current trading and forecasts, a review of existing and

proposed management service contracts, a review of the company's financial history and current

financial position, either a full legal review or one targeted on specific areas and, if it is not already in

place, obtaining key man insurance and satisfactory references and checks on key employees.

It is also common for investors to require the founders and senior management to sign up to

Employment or Consultancy Agreements in a form approved by the investors. In the case of

investment from VCTs it will also be a condition that before they invest the appropriate tax

clearance has been obtained from the HM Revenue & Customs.

IV What terms may be included in a Term Sheet? continued

23

Angels

High net worth individuals who provide seed money to very early stage companies, usually investing

their own money rather than that of institutional or other investors.

Anti-dilution provisions

Provisions which protect the holder's investment from dilution as the result of later issues of shares at

a lower price than the investor paid by adjusting the option price or conversion ratio or issuing new

shares (see paragraph 8, Section IV above).

As converted basis

The determination of preferred shares rights, such as vesting and participation in a dividend, on

the basis that those shares have been converted into ordinary shares, taking account of whatever

adjustments might be necessary.

Audit Committee

A committee of the Board of Directors consisting of a majority of independent (non-executive)

directors, responsible for selecting and overseeing the work of outside auditors and other audit

activities. The definition of an independent director may vary from one market to another (see

paragraph 16, Section IV above).

Bridge loan, bridge finance or bridge round

A loan or equity investment to provide financing for a relatively short time period until the issuer can

complete a longer term financing such as a public offering or new investment round.

Burn rate

The rate at which a company is consuming cash each month.

Capitalise

Converting a debt owed to a company into equity (see paragraph 3, Section IV above).

Capitalisation table (cap table)

A spreadsheet listing all shareholders and holders of options and any other securities, along with the

number of shares, options and convertible securities held (see Box 1 and Box 2 in Section III above).

Carried interest

The portion of any profits realised by a venture capital fund to which the fund managers are entitled, in

addition to any returns generated by capital invested by the fund managers. Carried interest payments

are customary in the venture capital industry. Also known as the carry.

V Venture capital glossary of terms

W3858 Term sheets text.indd 23W3858 Term sheets text.indd 23 9/10/07 12:15:22 pm9/10/07 12:15:22 pm

24

Completion or closing

In the context of a venture capital investment round, the release of investment funds to the company

and the issuance of shares to the investors following execution of the investment documents and

verification that all necessary conditions have been fulfilled.

Co-investment

See Syndication.

Conversion

The act of exchanging one form of security for another security of the same company, e.g. preferred

shares for ordinary shares, debt securities for equity (see paragraph 6, Section IV above).

Conversion ratio

The ratio indicating the number of underlying securities that can be acquired upon exchange of a

convertible security, e.g. the number of ordinary shares into which preferred shares are convertible

(see paragraph 6, Section IV above).

Convertible debt

A debt obligation of a company which is convertible into shares.

Convertible preferred shares

Preferred shares convertible into ordinary shares.

Co-sale or Tag along rights

A mechanism to ensure that if one investor or founder has an opportunity to sell shares the other

shareholders are also given that opportunity on a proportional basis. (see paragraph 11, Section IV above).

Covenants

Undertakings given to the investors by the company and sometimes the founders to do or not do

certain acts (see paragraph 15, Section IV above).

Cumulative dividends

A dividend which accumulates if not paid in the period when due and must be paid in full before other

dividends are paid on the company's ordinary shares (see paragraph 3, Section IV above).

Cumulative preferred shares

A form of preferred shares which provides that if one or more dividends is omitted, those dividends

accumulate and must be paid in full before other dividends may be paid on the company's ordinary

shares (see paragraph 3, Section IV above).

Debt/equity ratio

A measure of a company's leverage, calculated by dividing long-term debt by ordinary shareholders' equity.

V Venture capital glossary of terms continued

W3858 Term sheets text.indd 24W3858 Term sheets text.indd 24 9/10/07 12:15:22 pm9/10/07 12:15:22 pm

25

Debt financing

Financing by selling notes or other debt instruments.

Deed of adherence

An agreement that purchasers of shares (new or existing) may be required to sign to ensure they are

bound by the terms of an Investment Agreement.

Deemed liquidation or liquidity event

Term used to describe trigger events for a liquidation preference. Usually defined to cover, among other

things, a merger, acquisition, change of control or consolidation of the company, or a sale of all or most

of its assets (see paragraph 4, Section IV above).

Default

Failure to discharge a contractual obligation, e.g. to pay interest or principal on a debt when due.

Demand registration rights (US)

The contractual right of a security holder to require an issuer to file a registration statement to register

the holder's securities so that the holder may sell them in the public market without restriction (see

paragraph 19, Section IV above).

Dilution

The process by which an investor's percentage holding of shares in a company is reduced by the

issuance of new securities (see paragraph 8, Section IV above).

Directors & officers insurance

Directors and officers (D&O) insurance is professional liability coverage for legal expenses and liability to

shareholders, creditors or others caused by actions or omissions by a director or officer of a company.

Disclosure letter

A letter given by the founders, and maybe other key members of the management team, and the

company to the investors setting out exceptions to the representations and warranties.

Discounted cash flow (DCF)

An investment appraisal technique which takes into account both the time value of money and also the

total profitability of a project over a project's life.

Divestment

The disposal of a business or business segment.

Dividends

When a company makes a profit, it can pay part of these profits to its shareholders in the form of cash,

additional shares or other assets. Such payments are known as dividends (see paragraph 3, Section IV above).

W3858 Term sheets text.indd 25W3858 Term sheets text.indd 25 9/10/07 12:15:23 pm9/10/07 12:15:23 pm

26

V Venture capital glossary of terms continued

Down round

A round of venture capital financing in which the valuation of the company is less than the previous

round (see paragraph 8, Section IV above).

Drag along/bring along

A mechanism ensuring that if a specified percentage of shareholders agree to sell their shares, they can

compel the others to sell ensuring that a prospective purchaser can acquire 100% of a company (see

paragraph 12, Section IV above).

Due diligence

The process of researching a business and its management prior to deciding whether to proceed with

an investment in a company (see paragraph 26, Section IV above).

Early stage capital

Finance for companies to initiate commercial manufacturing and sales, following receipt of seed capital.

Earnings

Profits after expenses.

EBIT/EBITDA

Earnings before interest and taxes/earnings before interest, taxes, depreciation and amortisation:

financial measurements often used in valuing a company.

Employee share option plan (ESOP)

A scheme to enable employees to acquire shares in the companies in which they work (see paragraph

21, Section IV above).

Equity

Ownership interest in a company represented by shares.

Exclusivity Agreement

Often negotiated by a syndicate of investors, an agreed period of exclusivity during which the company

and/or its existing shareholders cannot negotiate with others for investment into the company.

Exercise price

The price at which an option or warrant can be exercised.

Exit mechanism

Term used to describe the method by which a venture capitalist will eventually sell out of an investment

(see paragraph 18, Section IV above).

W3858 Term sheets text.indd 26W3858 Term sheets text.indd 26 9/10/07 12:15:23 pm9/10/07 12:15:23 pm

27

Exit strategy

Potential scenarios for liquidating an investment while achieving the maximum possible return. For

venture capital-backed companies, typical exit strategies include Initial Public Offerings (IPOs) and

acquisitions by or mergers with larger companies (see paragraph 18, Section IV above).

Flotation

To obtain a listing or IPO on a stock exchange (see paragraph 18, Section IV above).

Follow-on investment round

An additional investment by existing and/or new investors, which may be provided for in documentation

relating to the initial investment.

Founder shares

Shares issued to the founders of a company, usually at a low price in comparison to that paid by

investors (see paragraph 9, Section IV above). See also Sweat equity.

Full ratchet

Anti-dilution provisions that apply the lowest sale price for any ordinary shares (or equivalents) sold by

the company after the issuing of an option or convertible share as being the adjusted option price or

conversion price for those options or shares (see paragraph 8, Section IV above).

Fully diluted share capital

The issued share capital of a company if all options and other rights to subscribe for shares are exercised.

Fully participating

Term sometimes used to describe a liquidation preference which entitles beneficiaries to receive a

priority initial fixed payment and share pro rata with other share classes in any remaining proceeds (see

paragraph 4, Section IV above).

Generally accepted accounting principles (GAAP)

Rules and procedures generally accepted within the accounting profession.

Good leaver/bad leaver

A criteria applied to a shareholder employee who is ceasing to be employed to determine whether his

shares should be subject to a compulsory sale, and if so, at what price (see paragraph 9, Section IV above).

Independent or outside director

A non-executive member of the Board of Directors who is not an employee of a company nor affiliated

with a controlling stockholder of a company. The definition of independent may be further defined in

different countries or markets (see paragraph 16, Section IV above).

W3858 Term sheets text.indd 27W3858 Term sheets text.indd 27 9/10/07 12:15:23 pm9/10/07 12:15:23 pm

28

V Venture capital glossary of terms continued

Information rights

The contractual right to obtain information about a company, attend board meetings, etc. typically

received by venture capitalists investing in privately held companies (see paragraph 17, Section IV above).

Initial public offering (IPO)

The sale of shares to the public by a company for the first time. Prior to an IPO, companies that sell shares

to investors are considered privately held. This is the first time that a company has tried to raise funds on

a public market such as a stock exchange. Terms used to describe this are flotation, float, going public,

listing when a company obtains a quotation on a stock market (see paragraph 18, Section IV above).

Institutional investor

An organisation whose primary purpose is to invest assets owned by the organisation or entrusted to

them by others. Typical institutional investors are banks, pension funds, insurance companies, mutual

funds and university endowments.

Intangibles

The non-physical assets of a company that have a value, e.g. intellectual property rights including

trademarks and patents.

Intellectual property (IP)

Legal term used to describe the patents, licences, copyrights, trademarks and designs owned by a

company (see Section III above).

Internal rate of return (IRR)

An accounting term for the rate of return on an asset. It is defined as the interest rate that equates the

present value of future returns to the initial investment. It is greatly affected by the timing of the exit.

Investment Agreement

This is a summary of the main terms of the investment into the company. Typically it will describe the

amounts and types of shares to be issued and the specific rights of the investors such as veto rights and

information rights (see Investment Agreements in Section II above).

Key man insurance

Insurance obtained by the Company on the lives of key employees, usually the chief executive officer

and the person or persons ultimately responsible for continuing to develop the technology (see

paragraph 26, Section IV above).

Lead investor

In a substantial investment, the whole risk is often shared among a syndicate. Normally, one investor

will take the lead in negotiating the terms of the investment and managing due diligence (see

Syndication below).

W3858 Term sheets text.indd 28W3858 Term sheets text.indd 28 9/10/07 12:15:23 pm9/10/07 12:15:23 pm

29

Licence Agreement

An agreement under which certain commercial and/or intellectual property rights may be used by the

licensee, for example the institution may licence intellectual property rights to the investee company.

Liquidation or winding up

The sale of all of a company's assets, for distribution to creditors and shareholders in order of priority.

This may be as a result of the insolvency of the company or by agreement amongst shareholders (see

paragraph 4, Section IV above).

Liquidation preference

A negotiated term of a round of venture capital financing that calls for certain investors to have all or

most of their entire investment repaid if the company is liquidated. Often also triggered by a deemed

liquidation (see paragraph 4, Section IV above).

Liquidity

Converting an asset (such as shares) to cash (see paragraph 18, Section IV above).

Listing

When a company's shares are traded on a stock market it is said to be listed (see paragraph 18, Section

IV above).

Lock-up

A provision in the Underwriting Agreement between an investment bank and existing shareholders

that prohibits corporate insiders and private equity investors from selling for a certain period of time

following a public offering (usually 180 days after an IPO).

Milestone

A contractual target that must be met by the company. Often used by investors as a condition for

releasing further amounts of financing (see paragraph 2, Section IV above).

Net present value (NPV)

The current value of future cash flows discounted back to today's date using a stated discount rate.

NewCo

Word often used to describe a newly formed investee company (see Section III above).

New money

Investment funds coming from an investor who is not a current shareholder of the company.

W3858 Term sheets text.indd 29W3858 Term sheets text.indd 29 9/10/07 12:15:24 pm9/10/07 12:15:24 pm

30

V Venture capital glossary of terms continued

Non-executive director

Part-time directors who share all the legal responsibilities of their executive colleagues on the Board of

a company. The general view is that they can operate as an independent director able to take a long-

term view of a company and protect the interests of shareholders. An investor will often appoint a non-

executive to a board as one way of monitoring its investment (see paragraph 16, Section IV above).

Non-qualified IPO

An IPO which is not a qualified IPO.

Options

The right, but not the obligation, to buy or sell a security at a set price (or range of prices) in a given period.

Ordinary shares

These are equity shares that are entitled to all income and capital after the rights of all other classes of

capital and creditors have been satisfied.

Outside director

See Independent or outside director.

Par

The nominal cash amount assigned to a security by the issuer. For an equity security, par is usually a

very small amount that no longer bears any relationship to its market price.

Pari passu

Equally, rateably, without preference. Generally used to describe securities which are to be treated as

being of equal priority or preference.

Participating preferred shares

Preferred shares which entitle the holder not only to its stated dividend and liquidation preference, but

also allows the holder to participate in dividends and liquidating distributions declared on ordinary shares.

Patent

The right to exclude others from making, using, importing or selling an invention or a process for a

specific period of time.

Pay to play

A provision which requires investors to participate in subsequent rounds or forfeit certain rights such

as anti-dilution.

Piggy-back registration rights (US)

Contractual rights granted to security holders giving them the right to have their holdings included in a

registration statement if and when the issuer files a registration statement (see paragraph 19, Section IV above).

W3858 Term sheets text.indd 30W3858 Term sheets text.indd 30 9/10/07 12:15:24 pm9/10/07 12:15:24 pm

31

Post-money valuation

The value of a privately held company immediately after the most recent round of financing. This value

is calculated by multiplying the company's total (fully diluted) number of shares by the share price of the

latest financing (see paragraph 2, Section IV above).

Pre-emption right

The right of an investor to participate in a financing to the extent necessary to ensure that, if exercised,

its percentage ownership of the company's securities will remain the same after the financing as it

was before. Sometimes also used as a term for a right of first refusal on shares of other investors (see

paragraph 10, Section IV above).

Preferred ordinary shares (UK)