Finance Technical Mock

Interviews 101

Today’s discussion

2

• Interview format

• Technical questions: Accounting

• Technical questions: Valuation

• Industry-based questions

• Other resources

Most investment banking interviews follow similar

formats, and most banks are looking for similar skills

3

Length

Interviewers

Question

types

Banking interviews are short and have both

qualitative and quantitative portions

Banks are looking for enthusiasm,

communication skills, analytical capacity and

cultural fit

• 30 minutes (occasionally 45

minutes)

• Typically 1-on-1 or 2-on-1

• Interviews mostly be current

investment bankers

• Qualitative: behavioral, random

questions

• Quantitative: technical (accounting

and finance)

Enthusiasm /

passion

Communication

skills

Cultural fit

• Interest in investment banking as

role (and thus willingness to learn

and work long hours)

• Test through technical and banking

knowledge

Analytical

capacity

• Verbal and written communication

style (banking is more writing than

most realize!)

• Quantitative aptitude (willingness

to learn and comfort with

numbers)

• Personality and workstyle similar

to that of other successful bankers

• “Airport” test (subject to

interviewer interpretation)

Investment banking interviews typically consist of similar

types of questions

4

Opening

Behavioral

Technical

Random

Closing

• “Tell me about yourself” “Walk me through your resume”

• Opportunity to go through your full story, start the interview with the

narrative you want

• “Tell me about a time when…”

• Opportunity to tell stories that paint you in the best light and highlight your

specific strengths / skills

• “Walk me through the financial statements” “How do you value a company”

• Opportunity to show your enthusiasm for banking by knowing the basics of

the quantitative aspects of the job

• Set of questions that are hard to predict and vary by interviewer

• Include strengths / weaknesses, level of commitment, sell yourself, and long

term future questions

• “Do you have any questions for me”

• Questions from you to the interviewer

• Important to not end on a bad note

Why…

• “Why banking” “Why this bank” “Why this city” “Why this group”

• Opportunity to show your knowledge of the specific bank or team, and

highlight why your passionate about them

Technical questions: Overview

• Preparing for technical questions is important to

show knowledge and passion for investment

banking

• Even if they like you, a poor performance on the

technical component will hurt your chances

• Conceptual understanding is most important

• Two primary types of questions will be Accounting

and Valuation

• Others include Enterprise/Equity value, Merger Model

and occasionally LBO

5

Today’s discussion

6

• Interview format

• Technical questions: Accounting

• Technical questions: Valuation

• Industry-based questions

• Other resources

Top accounting concepts to know

1. The three financial statements and what each one

means

2. How changes in individual items on each of the

financial statements affect one another and why

3. What individual line items on the statements mean

(i.e. Goodwill, shareholders equity, etc.)

4. Different methods of accounting (cash-based vs.

accrual) and when revenue and expenses are

recognized

5. When to expense something and when to capitalize it

7

What are the three financial

statements?

• Income Statement

• Cash Flow Statement

• Balance Sheet

8

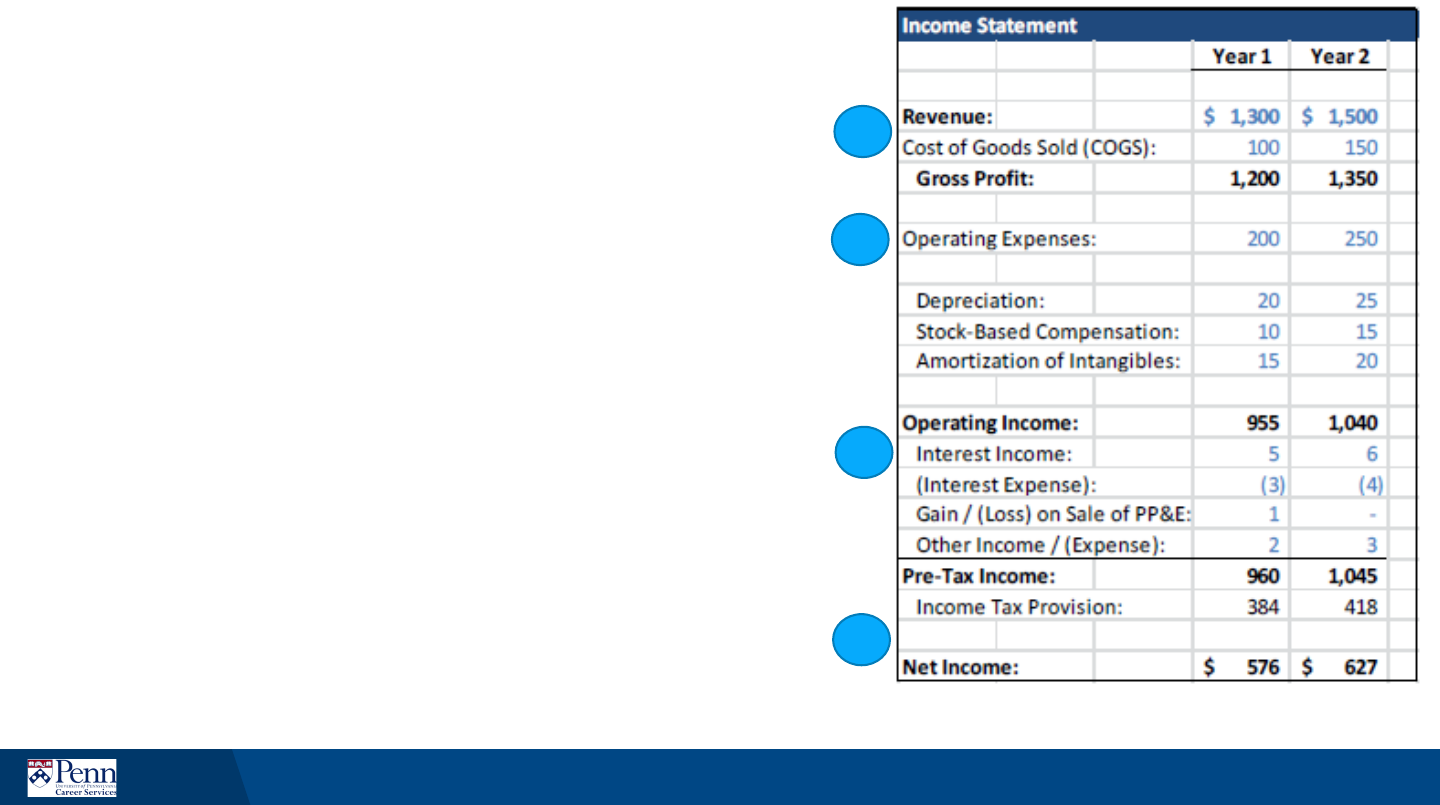

Income Statement

• The Income Statement (IS) shows

the company’s revenue and

expenses, taxes and after-tax profit

• Shows a company’s performance

over a period of time

• To appear on the income statement,

a line item must:

• Correspond to the period shown on the

statement

• Affect the company’s taxes

• i.e. interest paid on debt is tax-deductible

so it appears on the IS… but repaying

debt principal is not tax-deductible, so it

does not appear on the IS.

9

1

2

3

4

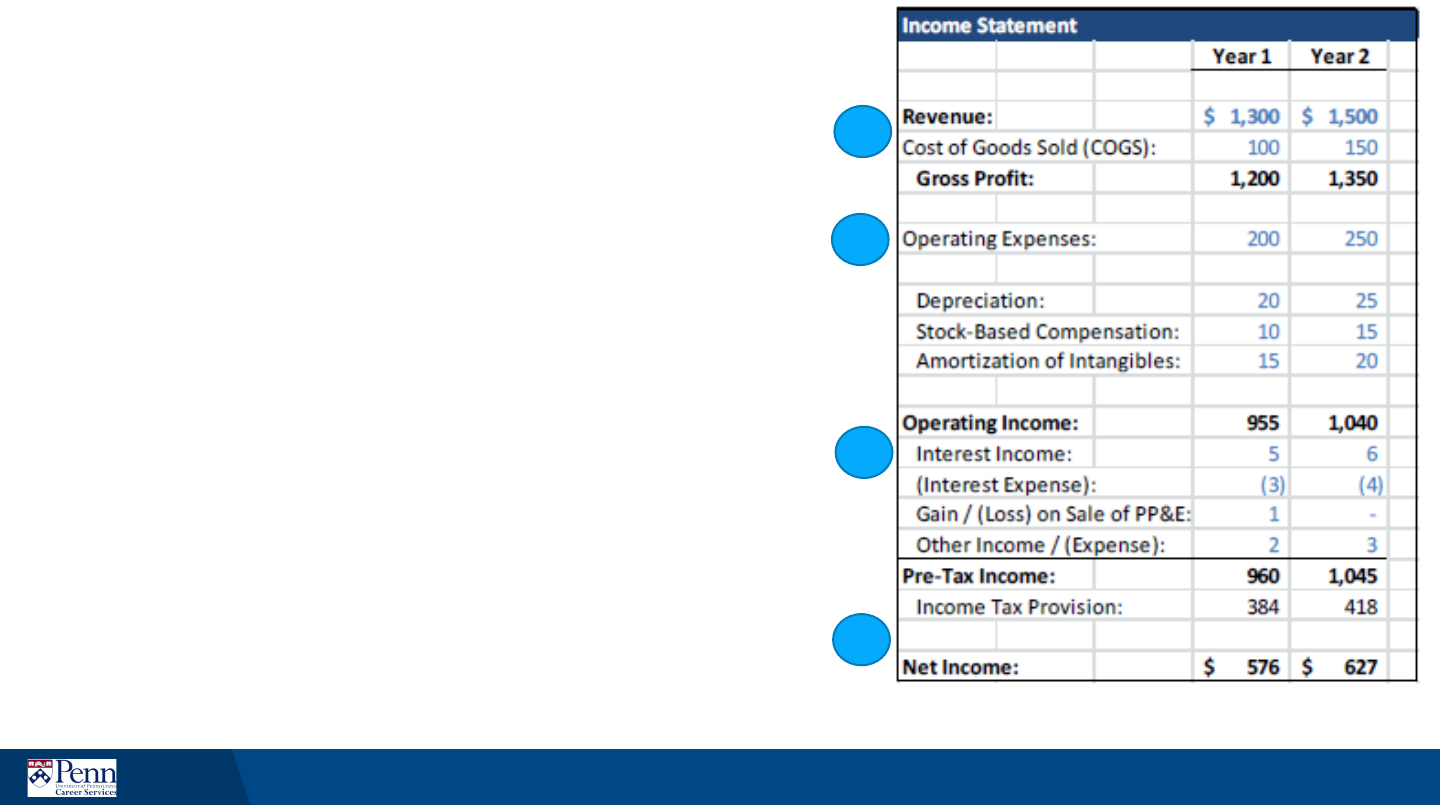

Income Statement

1. Revenue and Cost of Goods Sold (COGS):

Revenue is the value of the products/services

that a company sells in the period (Year 1 or

Year 2), and COGS represents the expenses that

are linked directly to the sale of those

products/services.

2. Operating Expenses: Items that are not directly

linked to product sales – employee salaries,

rent, marketing, research and development, as

well as non-cash expenses like Depreciation and

Amortization.

3. Other Income and Expenses: This goes

between Operating Income and Pre-Tax

Income. Interest shows up here, as well as

items such as Gains and Losses when Assets are

sold, Impairment Charges, Write-Downs, and

anything else that is not part of the company’s

core business operations.

4. Taxes and Net Income: Net Income represents

the company’s “bottom line” – how much in

after-tax profits it has earned. Net Income =

Revenue – Expenses – Taxes.

10

1

2

3

4

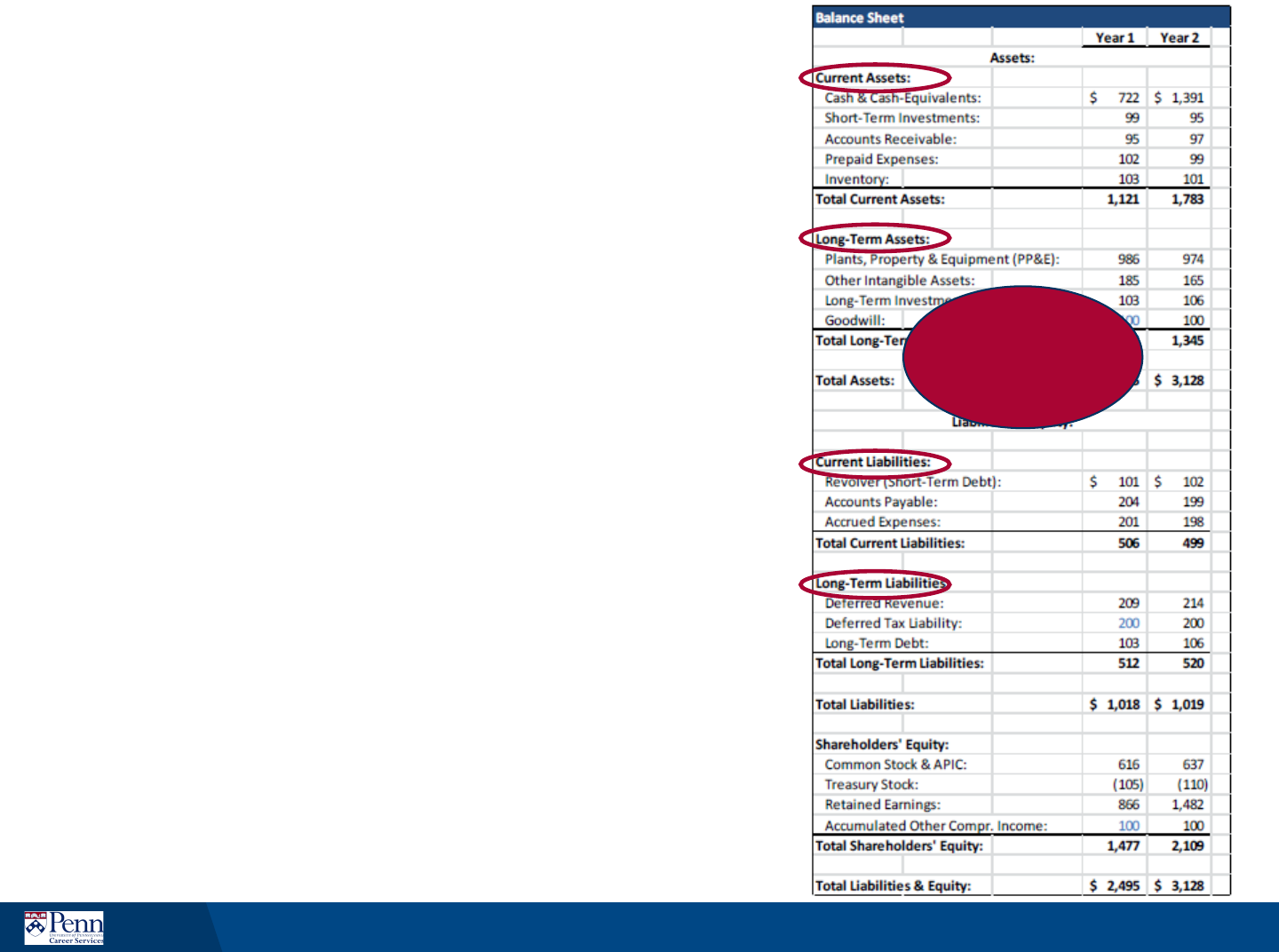

Balance Sheet

• The Balance Sheet (BS) shows the

company’s resources – its Assets - and

how it acquired those resources – its

Liabilities & Equity

• Snapshot of a company at a specific

point in time

• Key rules:

• Assets must always equal Liabilities +

Equity

• An Asset is an item that results in

additional cash in the future.

• A Liability is an item that will result in less

cash in the future. Liabilities are used to

fund a business.

• Equity line items similar to but they refer

to the company’s own internal

operations

11

For both assets and

liabilities : Current

is less than a year,

long-term is more

than a year

Balance Sheet

Let’s think about a relatable example. Your favorite

Aunt Susie owns a home. When thinking about her

balance sheet:

12

Assets Liabilities

Personal

investments

$50,000 Mortgage $380,000

Cash $30,000 Equity

House $500,000 After-tax savings

from earnings

$200,00

Total Assets = $580,000 Total Liabilities = $580,000

Just like a company’s balance sheet, your personal

balance sheet must always balance.

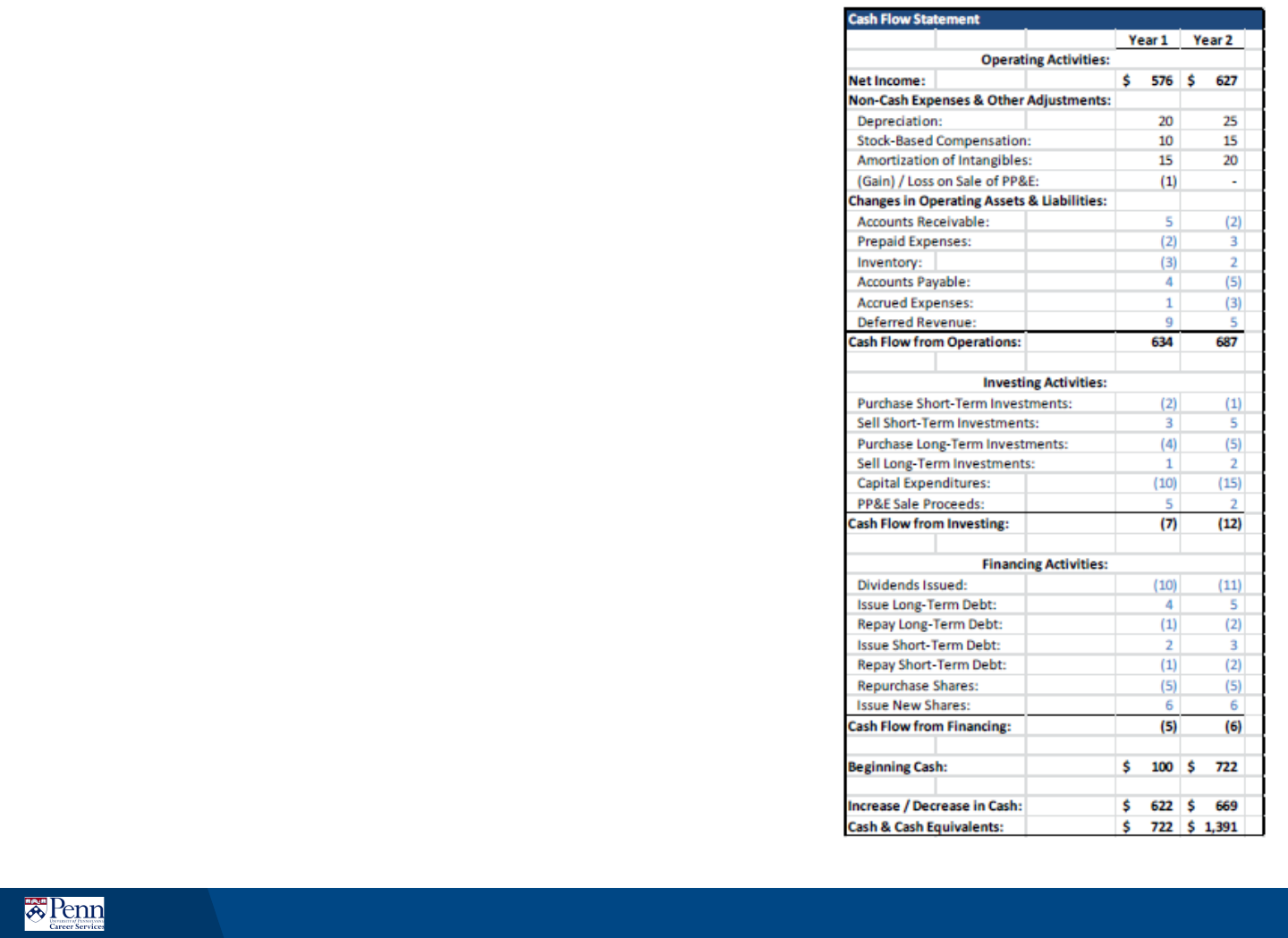

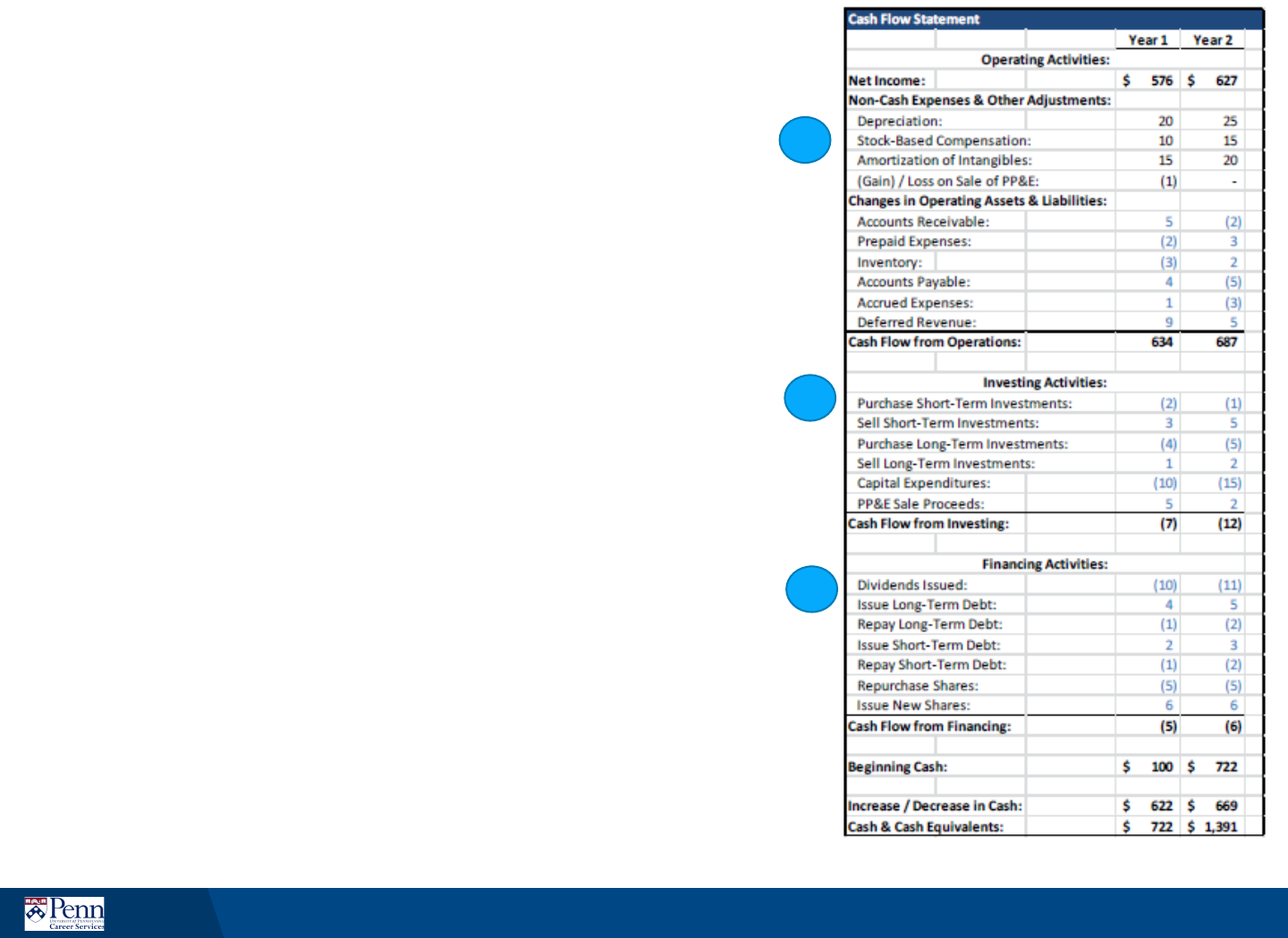

Cash Flow Statement

• The Cash Flow Statement (CFS)

tracks changes in a company’s

cash balance

• Shows flows over a period of

time

• Exists for 2 primary reasons

• Non-cash revenues and expenses

on the IS need to be adjusted to

show change in cash balance

• Show additional cash inflows and

outflows not yet on the IS

13

Cash Flow Statement

1. Cash Flow from Operations (CFO) – Net

Income from the Income Statement flows

in at the top. Then, you adjust for non-

cash expenses, and take into account how

operational Balance Sheet items such as

Accounts Receivable and Accounts

Payable have changed.

2. Cash Flow from Investing (CFI) –

Anything related to the company’s

investments, acquisitions, and PP&E

shows up here. Purchases are negative

because they use up cash, and sales are

positive because they result in more cash.

3. Cash Flow from Financing (CFF) – Items

related to debt, dividends, and issuing or

repurchasing shares show up here.

14

1

2

3

Primary questions on the three

financial statements

• Walk me through the three financial statements?

• How do the three financial statements link

together?

• If I were stranded on a desert island, only had 1

statement and I wanted to review the overall health

of a company – which statement would I use and

why?

• Let’s say I could only look at 2 statements to assess

a company’s prospects – which 2 would I use and

why?

15

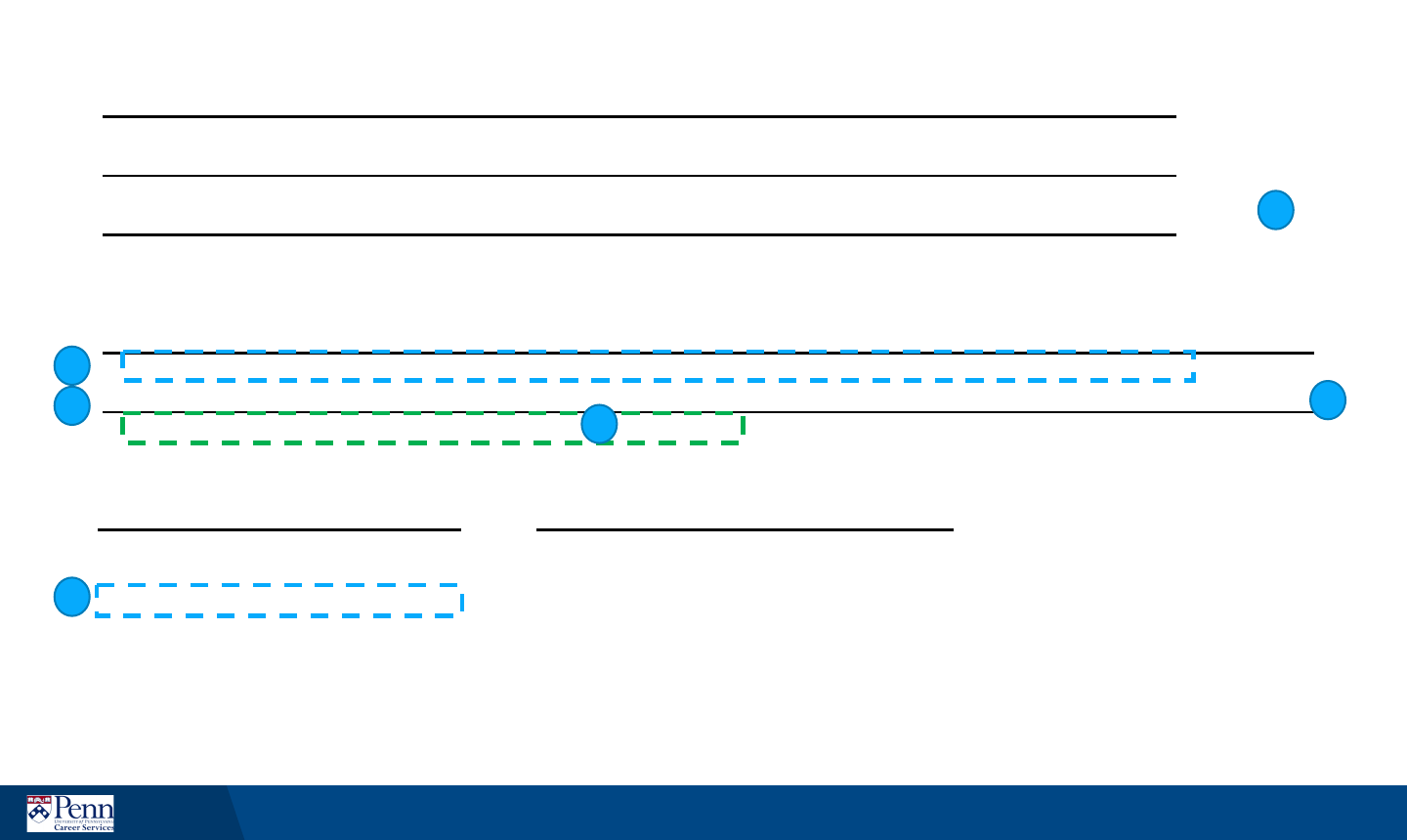

Walk me through the three financial

statements? How do the three financial

statements link together?

16

1

2

3

1

2

4

3

3

4

4

4

3

5

6

7

5

5

6

7

Don’t forget to flip the signs

of certain items!

(i.e. Gains and Losses)

Walk me through the three financial statements.

The 3 major financial statements are the Income Statement, Balance Sheet and

Cash Flow Statement.

The Income Statement shows the company’s revenue and expenses over a

period of time, and goes down to Net Income, the final line on the statement.

The Balance Sheet shows the company’s Assets – its resources – such as Cash,

Inventory and PP&E, as well as its Liabilities – such as Debt and Accounts

Payable – and Shareholders’ Equity – at a specific point in time. Assets must

equal Liabilities plus Shareholders’ Equity.

The Cash Flow Statement begins with Net Income, adjusts for non-cash

expenses and changes in operating assets and liabilities (working capital), and

then shows how the company has spent cash or received cash from Investing

or Financing activities; at the end, you see the company’s net change in cash.

How do the three financial statements link together?

1. Net Income from the bottom of the IS becomes the top line of the CFS.

2. Add back non-cash expenses from the IS (and flip the signs of items such

as Gains and Losses).

3. Reflect changes in operational BS line items – if an Asset goes up, cash

flow goes down and vice versa; if a Liability goes up, cash flow goes up

and vice versa.

4. Reflect Purchases and Sales of Investments and PP&E in Cash Flow from

Investing.

5. Reflect Dividends, Debt issued or repurchased, and Shares issued or

repurchased in Cash Flow from Financing.

6. Calculate the net change in cash at the bottom of the CFS, and then link

this into cash at the top of the next period’s BS.

7. Update the BS to reflect changes in Cash, Debt, Equity, Investments, PP&E,

and anything else that came from the CFS.

Watch out for these common pitfalls:

• BS doesn’t balance – it must always balance

• Duplicating effects of BS changes on the CFS

• Reflect each Balance Sheet item once and only once on the Cash Flow Statement, and vice versa.

• Affect an increase/decrease in assets or liabilities have on the BS

• If an Asset goes up, cash flow goes down; if a Liability goes up, cash flow goes up, and vice versa.

• Forgetting to flip signs on the CFS

• Common example is Gains or Losses on Asset Sale: Must list in both cash flow from operations and cash

flow from investing because you are re-classifying the cash flow. You subtract it from CFO and instead

include it as part of the full selling price of the assets in CFI instead.

• Accounts payable vs. Accrued expenses

• Mechanically, they are the same: Liabilities on the BS used when you’ve recorded an IS expense for a

product/service you have received, but have not yet paid for in cash. The difference is that Accounts

Payable is mostly for one-time expenses with invoices, such as paying for a law firm, whereas Accrued

Expenses is for recurring expenses without invoices, such as employee wages, rent, and utilities

• Accounts receivable vs. Deferred revenue

• Primary differences: (1) Accounts Receivable has not yet been collected in cash from customers,

whereas Deferred Revenue has been (2) Accounts Receivable is for a product/service the company has

already delivered but hasn’t been paid for yet, whereas Deferred Revenue is for a product/service the

company has not yet delivered

• Accounts Receivable is an Asset because it implies additional future cash whereas Deferred Revenue is a

Liability because it implies the opposite.

19

If I were stranded on a desert island only had 1

statement to review the overall health of a

company – which statement would I use and why?

The Cash Flow Statement!

• It gives a true picture of how much cash the company is

actually generating. This is ultimately the #1 thing you care

about when analyzing the financial health of any business –

its true cash flow

• Income Statement is misleading because it includes non-

cash expenses and excludes actual cash expenses such as

Capital Expenditures

20

If I had only two statements to use…which would I

use and why

Income Statement and Balance Sheet!

• You can create a rough cash flow statement from both of

those (assuming you have “Beginning” and “Ending” BSs

that correspond to the same period the IS is tracking)

21

Changes on the three financial

statements

• Single Step:

• Walk me through how depreciation going up by $10

would affect the three statements?

• Multi-step:

• A company makes a $100 cash purchase of equipment

on Dec. 31. How does this impact the three statements

this year and next year?

22

Helpful Tip - Use the following order when walking throw these

types of questions:

1. Income Statement 2. Cash Flow Statement 3. Balance Sheet

Walk me through how depreciation going up by

$10 would affect the three statements?

• Note: Before starting, always confirm what tax rate to use, given

recent changes to corporate tax – fair to assume 20%

• IS: Operating income and pre-tax income would decline by $10,

tax shield of +$2, net income is down -$8

• CFS: Net income at top goes down by $8, but $10 depreciation is

a non-cash expense so gets added back. Overall cash flow from

operations (CFO) goes up by $2. No other changes – net change in

cash is +$2

• BS: PPE decreases by $10 on asset side (depreciation), cash is +$2

from changes in CFS, so Assets down by $8. Net income was

down -$8, so is shareholders equity on Liabilities and Equity side.

• Balance sheet is now balanced!

23

Walk me through how depreciation going up by

$10 would affect the three statements?

• Intuition: We save taxes on all non-cash charges

such as depreciation

• Further testing: ask yourself the same question

with different numbers, decreasing depreciation or

with changes in different line items, i.e. accrued

expenses, accounts receivable, inventory, etc.

• Feeling confident? Try out the next multi-step

example to see how comfortable you are with

accounting!

24

Multi-Step Scenario

1. Apple is buying $100 worth of new iPad factories

with debt. How are all 3 statements affected at the

start of Year 1?

2. In Year 2, Debt is high-yield, so no principal is paid off,

and assume an interest rate of 10%. Also assume the

factories Depreciate at a rate of 10% per year. What

happens now?

3. At end of Year 2, the factories break down and their

value is written down to $0. The loan must also be

paid back now. Walk me through how the 3

statements ONLY from the start of Year 2 to the end

of Year 2.

25

1. Apple is buying $100 worth of new iPad factories

with debt. How are all 3 statements affected at

the start of Year 1?

• IS: At the start of Year 1, no effect.

• CFS: $100 spend on capital expenditures, would decrease CFI -$100;

$100 cash inflow from debt financing would increase CFF +$100; No

change in cash.

• BS: On asset side, PPE has increased +$100 from factory purchases; On

liabilities side, debt has increased +$100

• BS balances!

26

2. In Year 2, Debt is high-yield, so no principal is paid

off, and has 10% interest rate. Also assume the

factories depreciate at a rate of 10% per year. What

happens now?

• At the start of Year 2, Apple must pay interest expense and record

depreciation.

• IS: Operating income decreases $10 (10% depreciation on $100

factories) and the additional $10 in interest expense, decreases pre-tax

income by $20. Assuming 20% tax, net income falls by -$16.

• CFS: Net income at top is down -$16, add back $10 depreciation in CFO

(non-cash expense); no further changes, so net change in cash is -$6

• BS: On asset side, Cash is -$6, PPE is -$10 (depreciation), bringing total

assets -$16. On liabilities, shareholder’s equity -$16 (linked to net

income changes)

• BS balances!

• Note: Debt number doesn’t change since we assume none of the

principal has been paid back.

27

3. At end of Year 2, the factories break down and

their value is written down to $0. The loan must also

be paid back now.

Walk me through how the 3

statements ONLY from the start of Year 2 to the end of

Year 2.

• After 2 years, given 10% annual depreciation, the factories are valued at

$80. This is the value we need to write down.

• IS: Operating income decreases $90 (10% depreciation on $100

factories + $80 write-down), and the additional $10 in interest expense.

Thereby decreasing pre-tax income by $100. Assuming 20% tax, net

income falls by -$80.

• CFS: Net income at top is down -$80; in CFO, add back $90 depreciation

+ write-down in CFO (non-cash expense); in CFF, -$100 due to paying

back the loan principle; so net change in cash is -$90

• BS: On asset side, Cash is -$90, PPE is -$90 (depreciation + write-down),

bringing total assets -$180. On liabilities, debt is -$100 (paid-off),

shareholder’s equity is -$80, thereby total liabilities -$180.

28

Common Pitfalls

• Recognizing a change in inventory on the IS

• Not understanding the difference between certain

line items

• Forgetting effect of tax

• When phrasing changes, i.e. “A company sells some

PP&E for $120 but it’s worth $100 on its BS. Walk

me through...”

• When in doubt, always ask a question to clarify!

29

Today’s discussion

30

• Interview format

• Technical questions: Accounting

• Technical questions: Valuation

• Industry-based questions

• Other resources

Top Valuation questions

• How can you value a company? What are the three

main valuation methodologies?

• Which methodology gives the highest value?

• How do you present these to a client?

• What is a DCF?

• How do you calculate free cash flow (FCF)? Walk me through

how you get from Revenue to FCF?

• How do you calculate WACC?

• How do you calculate cost of equity?

• What is beta?

• How do you calculate Terminal Value (TV)?

• How would you value this [random object]?

31

How can you value a company? What are

the three main valuation methodologies?

There are three primary ways to value a company:

1. Comparable companies analysis

2. Precendent transaction analysis

3. Discounted Cash Flow (DCF)

4. Leveraged Buyout (LBO)

5. Sum-of-the-parts

6. Merger consequences analysis

32

Relative Valuation

Intrinsic Valuation

A relative valuation uses financials from other public companies and recent M&A

deals to estimate what the company you are valuing may be worth.

For an intrinsic valuation you can: (1) Estimate future cash flows and discount them

back to their present value (money today is worth more than money tomorrow), or

(2) Value the firm’s assets and assume the firm’s total value is linked to its adjusted

asset value minus its liabilities

Be able to discuss benefits

and disadvantages of each

method!

Topics you must understand about a DCF

analysis

1. What it is and be able to walk through it

2. How to calculate and project Free Cash Flow

(FCF)

3. How to calculate the discount rate, and apply

WACC and cost of equity

4. How to calculate the Terminal Value, what it is

and how it affects a DCF

33

What is a DCF?

In a DCF analysis, you value a company with the Present Value of its

Free Cash Flows (FCF) plus the Present Value of its Terminal Value:

1. Project a company’s FCF over a 5-10 year period

2. Calculate the company’s Discount Rate, usually using WACC

(Weighted Average Cost of Capital).

3. Discount and sum up the company’s Free Cash Flows.

4. Calculate the company’s Terminal Value using either the

Multiples Method or Gordon’s Growth (Perpetuity) Method

5. Discount the Terminal Value to its Present Value.

6. Add the discounted Free Cash Flows to the discounted Terminal

Value

See where these steps happen on an actual DCF on the next page!

34

Lemonade Stand DCF

1 2

3

4 5

Revenues $10,800 $11,880

$13,068 $14,375 $15,812

- Cost of Goods Sold

($2,700)

($2,970) ($3,267) ($3,594)

($3,953)

Gross Profit $8,100 $8,910

$9,801 $10,781 $11,859

- Operating Expenses

($5,190)

($5,709)

($6,280) ($6,908) ($7,599)

Operating Income (EBIT)

$2,910 $3,201

$3,521 $3,873 $4,261

- Tax Expense

($291)

($320) ($352) ($387)

($426)

After-tax Profit

$2,619 $2,881

$3,169 $3,486 $3,834

-

Depr., Amort., and other non-cash charges ($10)

($10) ($10) ($10)

($10)

(-/+) Changes in Operating Assets and Liabilities ($20)

($20) ($20) ($20)

($20)

-

Capital Expenditures ($40)

($40) ($40)

($40) ($40)

Unlevered Free Cash Flow $2,549

$2,811

$3,099 $3,416 $3,764

Present Value (FCF/(1+Discount Rate^Year) $2,317 $2,783

$3,096 $3,416 $3,764

$47,997

DCF Valuation $63,373

Terminal

Value

35

Assumptions

Expected revenue growth 10%

Effective tax rate 10%

Discount rate (WACC) 10%

Terminal Growth rate 2%

Operating Expenses

Uber ($6/day) $540

Payroll ($50/day) $4,500

Park license ($150/summer) $150

Total $5,190

1

2

4

3

5

6

Why do you calculate a company’s FCF?

How?

A company’s FCF closely corresponds to the actual cash flow that the investor

would receive each year if s/he bought the entire company. To calculate this:

1. Project a company’s revenue growth (% expected to grow over projected

period)

2. Assume operating margin to calculate EBIT or operating income

3. Apply effective tax rate to calculate net operating profit after tax (NOPAT)

4. Use CFS to project 3 key items that impact FCF: non-cash charges

(depreciation and amortization), changes in operating assets and liabilities

(net working capital), and capital expenditures

• Add back non-cash charges

• Subtract if Assets increase more than liabilities

• Subtract capital expenditures

5. Now you have your Unlevered FCF!

36

Now what?.....Right, discount the FCFs to

the present value. How?

1. What discount rate would you use?

• Weighted Average Cost of Capital (WACC)

2. What is WACC?

• Calculates the company’s cost of debt and equity, weighted

based on it’s capital structure

• WACC = cost of debt *(% debt)*(1 – tax rate) + cost of

equity*(% equity) + Cost of Preferred * (% Preferred)

3. What is the cost of debt?

• It’s interest rate on it’s debt

4. What is the cost of equity?

• Cost of equity = risk-free rate + market (equity) risk

premium*beta

37

What next?.....Terminal value….How do

you calculate that?

Two different methods: Multiples method and Gordon

Growth Method

1. Multiples: Often used and based on public comps.

EBITDA multiple of ?x – would often provide a range

2. Gordon Growth or Perpetual Growth – assumes the

company operates indefinitely and sums future cash

flows

• TV = Final year FCF *(1 + Terminal FCF Growth Rate) /

(Discount Rate – Terminal FCF Growth Rate).

• What would you use for Terminal growth rate? It should be

very low – less or equal to country’s GDP growth rate or rate

of inflation

38

Then…

Add PV of TV to PV of FCF in the projected period to

get your final valuation!

Potential follow-ups questions:

• Which components of a DCF tend to have the

greatest impact on the valuation?

• Discount rate and terminal value

39

Additional rules to remember / to test on

regarding DCF components

Effect on Cost of Equity

Smaller companies and companies in fast growing industries or

countries have higher expected returns

Additional debt because it increases risk

Additional equity because it decreases percentage of debt

Effect on WACC

Smaller companies and companies in fast growing industries or

countries have higher expected returns

Higher interest rate because it increases cost of debt

Additional debt because debt is less expensive than equity

40

Today’s discussion

41

• Interview format

• Technical questions: Accounting

• Technical questions: Valuation

• Industry-based questions

• Other resources

Industry-based questions

• Explain the sub-prime mortgage crisis. What happened?

• Let’s say you had $10 million to invest in anything. What would you do

with it?

First ask what are the investor’s goals – base response on investment horizon

• If you owned a small business and were approached by a larger

company about an acquisition, how would you think about the offer,

and how would you make a decision on what to do?

• would you do with it?

Key terms to consider are: price, form of payment (cash, stock, debt), future

plans for company

• What trend or company in the industry have you been following?

Do research or specific industry beforehand

× Describe something irrelevant, don’t explain the “why” or impact on the market

• Talk about a company you admire. Why?

Focus on qualities investors would find appealing

× Don’t choose brand name, i.e. Apple, Google, Amazon, etc.

42

Today’s discussion

43

• Interview format

• Technical questions: Accounting

• Technical questions: Valuation

• Industry-based questions

• Other resources

Additional Resources

44

Mergers and

Inquisitions

• Blog with recruiting advice for breaking into investment banking

• Several articles on networking (how to approach information

sessions, what to ask during informational interviews, etc.)

• Additional resources for interview prep and non-IBD recruiting

as well

Wall Street Oasis

• Forum with dedicated rooms for banking, sales and trading, etc.

• Significant amount of quality content and advice – but have to

weed through equally significant amount of bad content and

advice; be careful!

Career Services

• Career advising appointments can be used to discuss

networking approach and strategy

• Mock interviews with career services staff for in-person

feedback

Many more!

• Countless articles, books and websites dedicated to advice on

networking and interviewing

• Networking can be used in more contexts than just

undergraduate recruiting – many of these resources can help!