2018 Associate Benefits Book | Questions? Log on to WalmartOne.com or the WIRE, or call People Services at 800 -421-1362

Walmar 401(k) Plan eligibility 3

Enrolling in the Plan 4

Your Walmar 401(k) Plan accounts 4

Making a rollover from a previous employer’s plan or IRA 4

Making contributions to your 401(k)Account 5

Walmar’s contributions to your Company Match Account 7

Investing your account 8

More about owning Walmar stock 9

Account balances and statements 10

Receiving a payout while working forWalmar 10

If you die: your designated beneficiary 11

If you get divorced 12

If you leave Walmar 13

If you leave and are rehired by Walmar 14

The income tax consequences of apayout 14

Filing a Walmar 401(k) Plan claim 16

Administrative information 16

Special tax notice addendum 19

The legal name of the Plan is the Walmar 401(k) Plan. This document is being provided solely by your employer.

No affiliate of Bank of America Corporation has reviewed or paricipated in the creation of the information

contained herein.

WHERE CAN I FIND?

The Walmart 401(k)

Plan

M

6

0

9

4

5

0

0

0

5

SUMMARY OF MATERIAL MODIFICATIONS

TO THE WALMART 401(K) PLAN

(and an important notice about summary heath information under the Associates’ Health and Welfare Plan)

This Summary notifies you of some recent changes to the Walmart 401(k) Plan (Plan) and how those changes may affect your Plan participation. These

changes are discussed in more detail below. You should keep this Summary with the 401(k) Plan section of the 2018 Associate Benefits Book

and read the documents together.

Update of Company N

ame

Effective February 1, 2018, Wal-Mart Stores, Inc. changed its legal name to Walmart Inc. Thus, the correct name of the sponsor of the Plan is Walmart

Inc. All references to Wal-Mart Stores, Inc. in the 401(k) Plan section of the Book are changed to Walmart Inc.

Extended Excess Deferral Correction Deadline

The total amount you can contribute to this Plan and to any other employer plan (including any other 401(k) plans, 403(b) annuity plans or simplified

employee pension plans) is $18,500 for the 2018 calendar year. (Your catch-up contributions do not count toward this limit.) This amount may be

increased from time to time by the IRS. If you contribute to more than one plan during the year, it is your responsibility to determine if you have

exceeded the legal limit.

If your total contributions go over the legal limit for a calendar year, the excess must be included in your income for that year and will be taxed. In

addition, you may be taxed a second time when the excess amount is later paid to you upon one of the Plan’s normal payout events. For this reason,

you may wish to request that the excess amount be returned to you. If you wish to request that the excess be returned to you from this Plan, you must

contact Benefits Customer Service at 800-421-1362.

Prior to February 1, 2019, you were required to contact Benefits Customer Service by March 1 of the year following the year in which the excess

contributions were made. On and after February 1, 2019, you will have until April 1 to notify Benefits Customer Service that you would like to have the

excess returned to you.

Hurricane Loan Relief

Note that if you were affected by Hurricane Harvey, Irma or Maria, or by the California wildfires, and you had a loan outstanding, you may be entitled to

extend your loan repayment.

Generally, you are eligible for this relief if your principal place of abode on August 23, 2017 for Hurricane Harvey, September 4, 2017 for Hurricane Irma,

or September 16, 2017 for Hurricane Maria, or between October 8, 2017 and December 31, 2017 for the California Wildfires, was located in the

designated disaster area and you sustained an economic loss as a result of such event. If you are eligible for this relief and you failed to pay any loan

repayments due between the applicable date above and December 31, 2018, you will have an additional year to repay the unpaid amounts plus interest.

If you do not repay these amounts by the end of the one-year extension, your loan will default and the outstanding balance will be taxable to you.

Hardship Withdrawal Changes

In the event you have a “financial hardship,” you may be permitted to withdraw a portion of your Plan accounts to help with your needs. Currently, if you

take a withdrawal for financial hardship, you may not contribute to this Plan or certain other retirement or stock purchase plans (including the Associate

Stock Purchase Plan) for six months after the date of your payout. Effective for financial hardship withdrawals processed on or after February 1, 2019,

however, you may continue to contribute to this Plan and other plans after you receive the withdrawal.

Plan Mergers

The following plans were merged into the Plan on the dates specified below.

x October 1, 2018 - Hayneedle, Inc. 401(k) Plan

x November 1, 2018 - ModCloth, Inc. 401(k) Profit Sharing Plan

x November 2, 2018 - Bonobos Retirement Plan

If you previously participated in one of these plans, you may have one or more of the following accounts, which will track the different types of

contributions merged into this Plan from your prior plan: Prior Plan Deferral Account, Prior Plan Associate Deferral Account, Prior Plan Roth 401(k)

Contribution Account, Prior Plan Match Account, Prior Plan QNEC Account, Prior Plan Rollover Account, and After-Tax Rollover Account. You are

always 100% vested in these accounts. These accounts are generally eligible for withdrawal at the same time as under your prior plan.

In the event of your death, note that these accounts will be paid according to your beneficiary designation on file in this Plan or, if you have not made a

beneficiary designation in this Plan, according to the Plan’s default provisions. If you have not made a beneficiary designation under this Plan, you

should make a designation now. If you previously made a designation with this Plan, you should review that designation to make sure it is still consistent

with your intent.

For More Information On These Changes

For more information regarding the changes to the Plan summarized above, please contact Benefits Customer Service at (800) 421-1362, or the Merrill

Lynch Customer Service Center at (888) 968-4015.

This notice serves as a "summary of material modifications" to the summary plan description for the 401(k) Plan. You should keep this with your

summary plan description. Complete details of the Plan are included in the official plan document. If there is a difference between this notice and the

legal document, the Plan document will govern in every instance. In addition, Walmart reserves the right to change or terminate the 401(k) Plan at any

time.

Availability of Summary of Health Information

As an associate, the health benefits available to you represent a significant component of your compensation package. They also provide important

protection for you and your family in the case of illness or injury. Your plan offers a series of health coverage options. Choosing a health coverage

option is an important decision. To help you make an informed choice, your plan makes available a Summary of Benefits and Coverage (SBC), which

summarizes important information about any health coverage option in a standard format, to help you compare options. The SBC is available on the

WIRE and WalmartOne.com/Benefits. A paper copy is also available, free of charge, by calling (800) 421-1362.

The Walmar 401(k) Plan

2

The Walmar 401(k) Plan

THE WALMART 401k PLAN RESOURCES

Find What You Need Online Other Resources

Enroll in or change your 401(k) contribution

and your catch-up contribution

Go to the WIRE, WalmarOne.com,

Workday or the Plan’s website at

benefits.ml.com

Call the Customer Service Center at

888-968-4015

• Request a rollover packet to make a

rollover contribution

• Get a fee disclosure sheet

• Get information about your Plan accounts

• Get a copy of your quarerly statement

• Request a hardship withdrawal or a

withdrawal after you reach age 59½

• Change your investment fund choices

• Request a payout when you leave Walmar

• Get information about your Plan

investment options

• Request a withdrawal of your rollover

contributions

• Request a loan from your Plan account

Go to benefits.ml.com Call the Customer Service Center at

888-968-4015

• Designate a beneficiary Go to the WIRE, or WalmarOne.com

or Workday

What you need to know about the Walmar 401(k) Plan

• You are eligible to make your own contributions to the Plan as soon as administratively feasible after your date of hire

is entered into the payroll system. You can contribute from 1% to 50% of your eligible pay each pay period.

• You will begin receiving matching contributions on the first day of the calendar month following your first anniversary

of employment with Walmart if you are credited with at least 1,000 hours of service during your first year and you are

contributing to your 401(k) Account. (Matching contributions will not be made with respect to contributions you make

before you become eligible for matching contributions.)

• The matching contribution will be a dollar-for-dollar match on each dollar you contribute to the Plan after you become

eligible for matching contributions, up to 6% of your eligible annual pay.

• You will always be 100% vested in the money you contribute to your 401(k) Account and the money Walmart

contributes to your Company Match Account.

• You choose how to invest all contributions to your Plan account.

• If you do not choose how your current contributions to the Plan will be invested, they will be automatically invested in

the Plan’s default investment option, currently the myRetirement Funds.

• You pay no federal income tax on contributions or any investment earnings until you receive a payout from the Plan.

• You can access and monitor your account any time at benefits.ml.com.

• You can withdraw your rollover contributions at any time.

• You may also request a loan from your Plan account. Loans are subject to certain requirements outlined later

in this summary.

This is a summary of benefits offered under the Plan as of October 1, 2017. Should any questions ever arise about the

nature and extent of your benefits, the formal language of the Plan document, not the informal wording of this summary,

will govern.

The Walmar 401(k) Plan

3

2018 Associate Benefits Book | Questions? Log on to WalmartOne.com or the WIRE, or call People Services at 800 -421-1362

Walmar 401(k) Plan eligibility

ASSOCIATES WHO ARE ELIGIBLE TO PARTICIPATE IN

THE PLAN

All associates of Wal-Mart Stores, Inc. or a participating

subsidiary are eligible to participate in the Plan, except:

• Leased employees; nonresident aliens with no income from

U.S. sources; independent contractors or consultants

• Anyone not treated as an employee of Walmart or its

participating subsidiaries

• Associates covered by a collective bargaining agreement,

to the extent that the agreement does not provide for

participation in this Plan

• Associates represented by a collective bargaining

representative after Walmart has negotiated in good

faith to impasse with the representative on the question

of benefits, and

• Certain other associates who may be jointly employed

by Walmart and a subsidiary that is not a participating

subsidiary in the Plan.

For purposes of this Summary Plan Description, all

participating subsidiaries are referred to as “Walmart.”

WHEN PARTICIPATION FOR PURPOSES OF YOUR

CONTRIBUTIONS BEGINS

Eligible associates may begin making their own

contributions to the Plan as soon as administratively feasible

after their date of hire is entered into the payroll system.

To begin making contributions to the Plan, you can

enroll on WalmartOne.com, the WIRE, Workday, or

through benefits.ml.com (see Enrolling in the Plan later

in this summary).

WHEN PARTICIPATION FOR PURPOSES OF MATCHING

CONTRIBUTION BEGINS

If you are an eligible associate, you will begin receiving

matching contributions on the first day of the calendar

month following your first anniversary of employment

with Walmart if you are credited with at least 1,000 hours

of service during the first year and are contributing to

your 401(k) Account. (Matching contributions will not be

made with respect to contributions you make before you

become eligible for matching contributions.) For example,

if your date of hire was December 15, 2017, and you are

credited with 1,095 hours by December 15, 2018 (your

first anniversary), then you will begin receiving matching

contributions on January 1, 2019, with respect to any

contributions you make to the Plan on or after that date.

As an additional example, if your date of hire was

December 1, 2017, and you are credited with 1,095 hours

by December 1, 2018 (your first anniversary), then you will

begin receiving matching contributions on January 1, 2019

with respect to any contributions you make to the Plan on

or after that date.

If you are not credited with 1,000 hours of service during

that first year, your eligibility for the matching contributions

will be determined on hours worked during the Plan year,

which runs from February 1 to January 31. You will be eligible

to receive matching contributions on any contributions

you make to the Plan on or after the February 1 that

follows the Plan year in which you are credited with at least

1,000 hours of service. For example, if your date of hire

is December15, 2017, and you are credited with only 595

hours by December15, 2018 (your first anniversary), but

you work 1,095 hours during the February 1, 2018–January

31, 2019 Plan year, you will begin receiving matching

contributions on February 1, 2019 with respect to any

contributions you make to the Plan on or after that date.

HOW HOURS OF SERVICE ARE CREDITED UNDER

THEPLAN

For hourly associates, the hours counted toward the

1,000-hour requirement are credited as follows:

• Hours, including overtime hours, worked by hourly

associates for Walmart or any subsidiary are counted.

• Hours for which an associate receives paid leave or

personal time off are also counted.

• When a payroll period overlaps two Plan years, hours are

credited toward the Plan year in which they are actually

worked. However, before February 1, 2015, hours for a

payroll period that overlapped Plan years were prorated

between the two years.

For salaried associates and truck drivers, the hours counted

toward the 1,000-hour requirement are credited as follows:

• Salaried associates and truck drivers are credited with 190

hours per month for each month in which they work at

least one hour for Walmart or a subsidiary.

• In general, you must work at least six months of the Plan

year to have 1,000 hours credited for the year. (Vacation

pay after you leave Walmart will not give you an additional

190 hours of credit.)

If you become an associate of Walmart or any subsidiary as

the result of the acquisition of your prior employer, special

service crediting rules may apply to you.

Under the Uniformed Services Employment and

Reemployment Rights Act of 1994 (USERRA), veterans

who return to Walmart or a subsidiary after a qualifying

deployment may be eligible to have their qualified military

service considered toward their hours of service under

the Plan. If you think you may be affected by this rule, call

People Services at 800‑421‑1362 for more details.

The Walmar 401(k) Plan

4

Enrolling in the Plan

Shortly after you become eligible to contribute to the Plan,

(i.e., shortly after your date of hire), you will receive an

enrollment packet at your home address on file. This packet

tells you how you can make contributions from your pay on

a pretax basis into your 401(k) Account and explains how you

can direct the investment of your Plan funds by choosing

from among a menu of investment options with varying

investment objectives and associated risks. Because the

Plan is intended to be an important source for your financial

security at retirement, you should read all information

pertaining to the Plan carefully, and consult with your family,

tax and financial advisors before making any decisions.

Once you satisfy the matching contribution eligibility

requirements, Walmart will match all of your subsequent

contributions dollar-for-dollar up to 6% of eligible annual

pay, as explained in the Walmart’s contributions to your

Company Match Account section.

To begin making contributions to the Plan, you can

enroll online at WalmartOne.com, the WIRE, Workday, or

benefts.ml.com. You can also call the Customer Service

Center at 888‑968‑4015. You can enroll at any time after

you become eligible.

When you enroll, you can choose:

• The percentage of your pay that you want to contribute on

a per-pay-period basis (see Making contributions to your

401(k) Account later in this summary), and

• How to invest your accounts among the Plan’s investment

options. The Plan’s investment options and procedures are

described in the enrollment packet.

After you enroll, a confirmation notice will be mailed to your

home address, or, if you have chosen electronic delivery of

Plan materials, you will receive an email notification when

the confirmation is available. The confirmation will show the

percentage of your pay that you have chosen to contribute

from each check and the investment option(s) you have

elected. You should review the confirmation to make sure

your enrollment information is correct.

Your contributions to the Plan will be effective as soon as

administratively feasible, normally within two pay periods.

No contributions will be taken from your pay before you

become an eligible participant in the Plan. Only participants

who elect to contribute their own funds to the Plan will

have those contributions matched by the Company (after

they meet the eligibility requirements for matching

contributions, as explained in the Walmart’s contributions

to your Company Match Account section).

It is your responsibility to review your paychecks to confirm

that your election was implemented. If you believe your

election was not implemented, you must promptly notify

the Customer Service Center at 888‑968‑4015, but in

no event later than six months after your election, for

corrective steps to be taken.

Your Walmar 401(k) Plan accounts

The Walmart 401(k) Plan consists of several accounts. You

will have some or all of the following accounts:

• 401(k) Account: This account holds your contributions to

the Plan (including your catch-up contributions, if any), as

adjusted for earnings or losses on those contributions.

• Company Match Account: This account holds Walmart’s

matching contributions, as adjusted for earnings or losses

on those contributions.

• 401(k) Rollover Account: This account holds any

contributions that you rolled over to this Plan from

another eligible retirement plan, as adjusted for earnings

or losses on those contributions.

• Company Funded 401(k) Account: This account holds

the discretionary Company contributions to the 401(k)

portion of the Plan made for Plan years ended on or

before January 31, 2011, as adjusted for earnings or losses

on those contributions.

• Company Funded Profit Sharing Account: This account

holds the discretionary Company contributions to the

profit-sharing portion of the Plan made for Plan years

ended on or before January 31, 2011, as adjusted for

earnings or losses on those contributions.

The chart on the following page provides a summary of some

of the differences between these accounts. These differences

are discussed in more detail throughout this summary.

Making a rollover from a previous

employer’s plan or IRA

When you come to work for Walmart, you may have pretax

funds owed to you from a previous employer’s retirement

plan (including a 401(k) plan, a profit-sharing plan, a

403(b) plan of a tax-exempt employer or a 457(b) plan of a

governmental employer). If so, you may be able to roll over

that money to this Plan. You may also roll over pretax funds

you have in an Individual Retirement Account (IRA). If you roll

over funds to this Plan, you should keep these points in mind:

• Once you roll funds into the Walmart 401(k) Plan, those

funds will be subject to the rules of this Plan, including

payout rules, and not the rules of your former employer’s

plan or your IRA

• Your rollover contribution will be placed in your 401(k)

Rollover Account and will be 100% vested, and

• You may withdraw all or any portion of your rollover

contributions at any time.

If you’re interested in making a rollover contribution to the

Plan, you should contact the Customer Service Center at

888‑968‑4015 or go online to benefits.ml.com to obtain a

rollover packet.

The Walmar 401(k) Plan

5

2018 Associate Benefits Book | Questions? Log on to WalmartOne.com or the WIRE, or call People Services at 800 -421-1362

Making contributions to your

401(k)Account

After you become a participant in the Plan, you may

generally choose to contribute from 1% up to 50% of each

paycheck to your 401(k) Account. Your contributions in

any calendar year, however, may not exceed a limit set by

the IRS. For 2017, the limit is $18,000. This amount will be

increased from time to time by the IRS. You are always 100%

vested in all amounts contributed into your 401(k) Account.

The IRS limits the amount of annual compensation that can

be taken into account under the Plan for any participant.

For 2017, this limit is $270,000.

Contributions to your 401(k) Account are deducted from

your pay before federal income taxes are withheld. This

means that you don’t pay federal income taxes on amounts

you contribute to the Plan. Earnings on these contributions

continue to accumulate tax-free and are not taxed until your

401(k) Account is actually distributed to you from the Plan.

You may also save on state and local taxes as well, depending

on your location. Please note that your contributions are

subject to Social Security taxes in the year the amount

is deducted from your pay. Distributions from the Plan,

however, are not subject to Social Security taxes.

In addition, if you contribute your own pay to your 401(k)

Account, you may be eligible for a “Saver’s Credit.” If you

are a married taxpayer who files a joint tax return with a

modified adjusted gross income (MAGI) of $62,000 or less

(for 2017) or a single taxpayer with $31,000 or less (for 2017)

in MAGI on your tax return, you are eligible for this tax

credit, which can reduce your taxes. For more details, your

tax preparer may refer to IRS Announcement 2001-106.

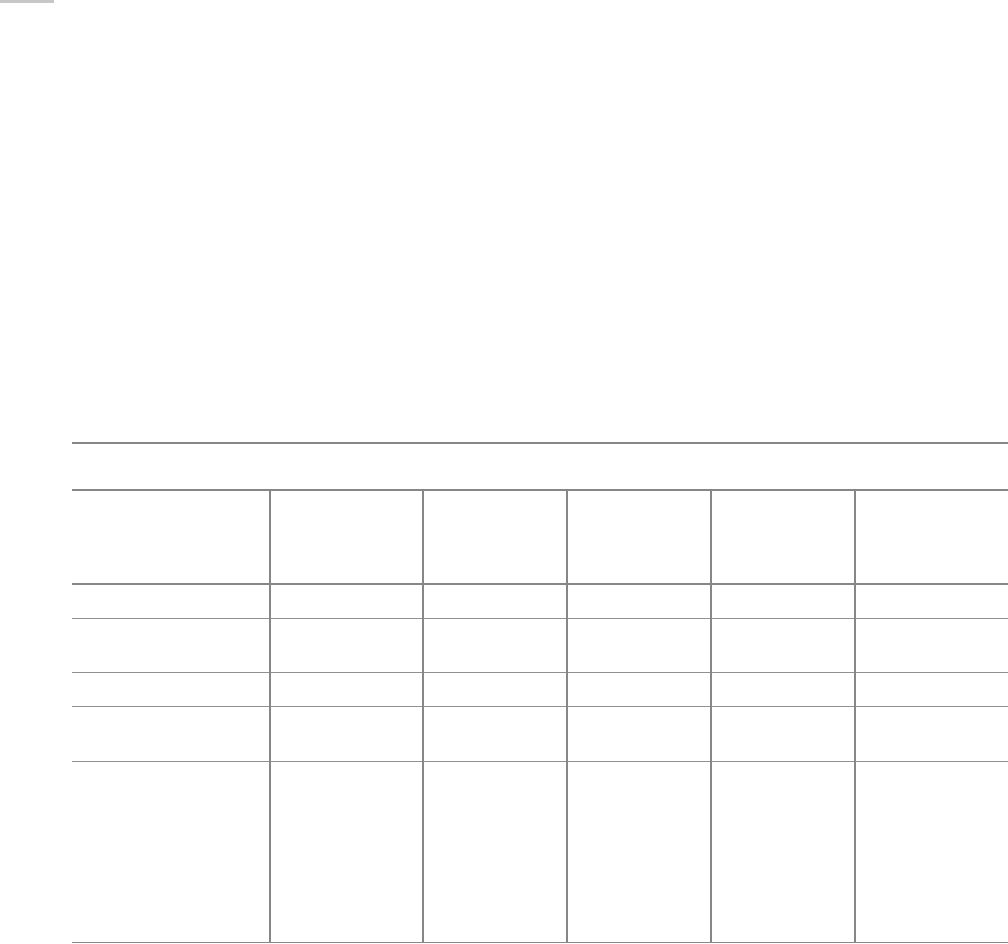

PROFIT SHARING AND 401k ACCOUNT DIFFERENCES

Source of

contributions

May paricipants

choose

investments?

Vesting

percentage

Are hardship

withdrawals

available?

Are in-service

withdrawals

available after

age 59⁄?

401(k) Account You Yes 100% Yes Yes

Company Match

Account

Walmar Yes 100% No Yes

All Rollover Accounts You Yes 100% Yes Yes

Company Funded

401(k) Account

Walmar Yes 100% No Yes

Company Funded Profit

Sharing Account

Walmar (except

for rollovers you

made to the Profit

Sharing Plan)

Yes 2 years — 20%

3 years — 40%

4 years — 60%

5 years — 80%

6 years — 100%

(Rollovers are

immediately

100% vested)

No Yes

(to the extent

vested)

The Walmar 401(k) Plan

6

HOW YOUR 401k CONTRIBUTION IS DETERMINED

The percentage of pay you elect to contribute to the Plan

will be applied to the following types of pay:

• Regular salary or wages, including bonuses and any pretax

dollars you use for your 401(k) contributions or to purchase

benefits available under Wal-Mart Stores, Inc. Associates’

Health and Welfare Plan

• Overtime, paid time off (used and paid out), bereavement,

jury duty and premium pay

• Most incentive plan payments

• Holiday bonuses

• Special recognition awards, such as the Outstanding

Performance Award

• Differential wage payments you receive from Walmart

while you are on a qualified military leave. This means that

the contribution you have in effect when you go on the

leave will continue to be applied to your differential wage

payments while you are on the leave unless you change

your election, and

• Effective February 1, 2018, transition pay designated as

relating to a WARN Act event.

The percentage of pay you elect to contribute to the

Plan will not be applied to the following types of pay:

• The 15% Walmart match on the Associate Stock

Purchase Plan

• Reimbursement for expenses like relocation

• Approved disability pay

• Equity income, including income from stock options or

restricted stock rights, or A final paycheck upon your

termination of employment that is paid prior to the end of

a normal pay cycle (unless it is administratively practicable

to withhold your contribution from that paycheck).

CHANGING YOUR 401k CONTRIBUTION AMOUNT

You can increase, decrease, stop, or begin your contributions

at any time by logging on to WalmartOne.com, the WIRE,

Workday or benefits.ml.com. You may also call the

Customer Service Center at 888-968-4015. Your change

will be effective as soon as administratively feasible,

normally within two pay periods. If you change your

contribution amount, a confirmation notice will be sent

to your home address or, if you have chosen electronic

delivery of Plan documents, you will receive an email

notification when the confirmation is available. It is your

responsibility to review your paychecks to confirm that

your election was implemented. If you believe your election

was not implemented, you must notify the Customer

Service Center at 888-968-4015 in a timely manner, so

that corrective steps can be taken. Your notification will

not be considered timely if it is more than six months after

the date your election is made. If you do not notify the

Customer Service Center in a timely manner, the amount

that is being withheld from your paycheck will be treated as

your deferral election.

IF YOU ARE AGE 50 OR OLDER

CATCHUP CONTRIBUTIONS

If you are age 50 or older (or will be age 50 by the end of

the applicable calendar year) and you are contributing up to

the Plan or legal limits, you are allowed to make additional

contributions. These are called catch-up contributions

and are made by payroll deduction just like your normal

contributions. For 2017, your catch-up contributions may

be any amount up to the lesser of $6,000 or 75% of your

eligible annual pay. This amount may be adjusted from time

to time by the IRS. Your catch-up contributions will be

credited to your 401(k) Account.

For example, if you elect to contribute the maximum

amount of $18,000 in the 2017 calendar year, or if you

elect to contribute the maximum percentage of your

eligible annual pay allowed under the Plan, you could elect

to contribute up to an additional $6,000 during the 2017

calendar year. If you are interested in making catch-up

contributions, you can enroll online at WalmartOne.com,

the WIRE, Workday or benefits.ml.com, or by calling the

Customer Service Center at 888-968-4015.

CONTRIBUTING TO MORE THAN ONE PLAN

DURING THE YEAR

The total amount you can contribute to this Plan and to

any other employer plan (including 403(b) annuity plans,

simplified employee pensions or other 401(k) plans) is $18,000

for the 2017 calendar year, or $24,000 if you are eligible for

catch-up contributions. This amount may be increased from

time to time by the IRS. If you contribute to more than one

plan during the year, it is your responsibility to determine if

you have exceeded the legal limit.

If your total contributions go over the legal limit for a

calendar year, you should request that the excess amount

be refunded to you. The excess amount must be included

in your income for that year and will be taxed. In addition,

if the excess amount is not refunded to you by April 15

following the year the amount was deferred, you will be

taxed a second time when the excess amount is distributed

to you. If you wish to request that the excess be returned

to you from this Plan, you must contact People Services at

800-421-1362 no later than March 1 following the calendar

year in which the excess contributions were made. Any

matching contributions related to refunded contributions

will be forfeited.

The Walmar 401(k) Plan

7

2018 Associate Benefits Book | Questions? Log on to WalmartOne.com or the WIRE, or call People Services at 800 -421-1362

IF YOU HAVE QUALIFIED MILITARY SERVICE

If you missed work because of qualified military service, you

may be entitled under the Uniformed Services Employment

and Reemployment Rights Act of 1994 (USERRA) to make up

contributions you missed during your military service (that is,

to make contributions equal to the amount you would have

been eligible to make if you were working for Walmart).

Because you will only have a certain period of time after you

return to work to make these contributions (generally three

times the period of military service, up to five years), you

should contact People Services at 800-421-1362 if you think

you may be affected by these rules.

Walmar’s contributions to your

Company Match Account

As explained above, you are eligible to receive matching

contributions on the first day of the calendar month

following your first anniversary of employment with

Walmart if you are credited with at least 1,000 hours of

service during the that year. Once you have satisfied these

requirements, Walmart will make matching contributions

to your Company Match Account equal to 100% of your

subsequent contributions to your 401(k) Account, including

catch-up contributions, up to 6% of your eligible annual

pay. Matching contributions will not be made with respect

to contributions you make before you become eligible

for matching contributions. After you become eligible

for matching contributions, the company matching

contribution will be made into your Company Match

Account each pay period until you reach the full amount

of the company matching contribution for which you are

eligible for that Plan year. Your eligible annual pay for this

purpose is the same as outlined above for determining

your 401(k) contributions to the Plan, but does not include

amounts paid to you before you become eligible to receive

matching contributions.

As previously noted, if you miss work because of qualified

military service, you may be entitled under USERRA to

make up 401(k) contributions that you missed during your

military service. If you do make up any 401(k) contributions,

Walmart is required to make up matching contributions you

would have received with respect to those contributions.

If you think this rule may apply to you, you should contact

People Services at 800-421-1362.

VESTING IN YOUR COMPANY MATCH ACCOUNT

You are always 100% vested in Walmart’s matching

contributions to your Company Match Account.

VESTING IN YOUR COMPANY FUNDED PROFIT

SHARING ACCOUNT

If you have a Company Funded Profit Sharing Account (see

Your Walmart 401(k) Plan accounts earlier in this summary),

the vested percentage of your Company Funded Profit

Sharing Account is the portion that you are entitled to

receive if you leave Walmart. Your account statements show

your vested percentage.

You become vested in your Company Funded Profit Sharing

Account (other than rollovers in that account, which are

always 100% vested) depending on your years of service

with Walmart as follows:

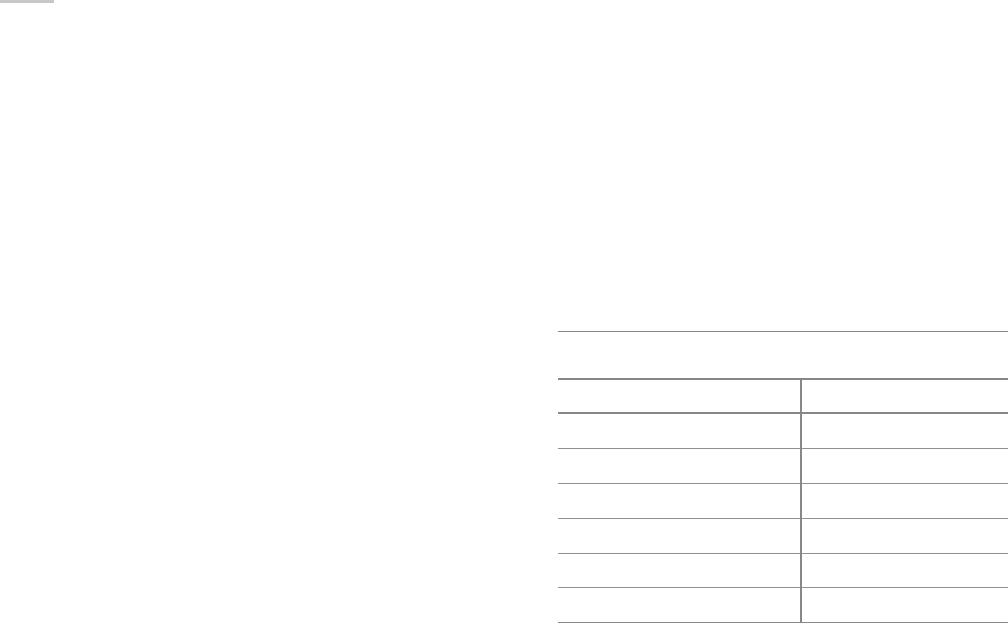

PROFIT SHARING VESTING SCHEDULE*

Years of Service Vested percentage

Less than two 0%

Two 20%

Three 40%

Four 60%

Five 80%

Six or more 100%

* Applies to paricipants actively employed on or after

January31, 2008.

NOTE: If you terminated employment before February 1, 2007,

your payout was based on the prior vesting schedule and not

the vesting schedule shown above.

A year of service for this purpose is a Plan year (February1–

January 31) in which you are credited with at least 1,000

hours of service under the hours of service rules (see How

hours of service are credited under the Plan earlier in this

summary). If you are credited with less than 1,000 hours in a

Plan year, your vesting does not increase. (Please note that

years of service for this purpose are not determined by your

anniversary date.)

If you leave Walmart because of retirement (at age 65

or older) or death, your Company Funded Profit Sharing

Account will be 100% vested, regardless of your years of

service. Your Company Funded Profit Sharing Account will

also be 100% vested if the Plan is ever terminated.

VESTING IN YOUR COMPANY FUNDED 401kACCOUNT

You are always 100% vested in Walmart’s contributions to

your Company Funded 401(k) Account.

The Walmar 401(k) Plan

8

Investing your account

YOUR INVESTMENT OPTIONS

You decide how your accounts will be invested. You

can choose:

• The myRetirement Funds. The myRetirement Funds are a

series of customized investment options created solely for

Plan participants by the Benefits Investment Committee,

and are commonly known as “target retirement date”

funds. The myRetirement Funds are diversified investment

options that automatically change their asset allocation

over time to become more conservative as a participant

gets closer to retirement. This is done by shifting the

amount of money that is invested in more aggressive

investments, such as stocks, and allocating those amounts

to more conservative investments, such as bonds, as a

participant gets closer to retirement. “myRetirement

Funds” is a term developed by Walmart for describing

these specific Plan investment options.

• From among a menu of investment options made available

under the Plan. Note that Walmart stock is an investment

option only for your Company Funded Profit Sharing

Account. Walmart stock is not available for investment

through any of your other Plan accounts (although to the

extent these other accounts hold Walmart stock, you may

always sell such shares, but no future purchases of Walmart

stock are allowed).

You may choose one of the investment options or you may

spread your money among the various investment options.

The investment gains or losses on your accounts will depend

upon the performance of the investments you choose.

If you do not make an investment choice for current

contributions to your account, they will be invested in one

of the myRetirement Funds based on your age. For more

information, refer to the Qualified Default Investment

Alternative (QDIA) notice and your enrollment packet. These

documents can both be obtained by going to benefits.ml.com

or by calling the Customer Service Center at 888‑968‑4015.

Because the Company Funded Profit Sharing Account is an

Employee Stock Ownership Plan, for Plan years ending prior

to January 31, 2006, all or a significant portion of Walmart’s

profit-sharing contribution was invested in Walmart stock.

If you were a participant in the Plan prior to that date, you

may have Walmart stock in your Company Funded Profit

Sharing Account. For Plan years ending January 31, 2007 or

later, Walmart’s profit-sharing contribution was not invested

in Walmart stock.

A description of all investment options, including the

myRetirement Funds, is included in the enrollment packet

you receive when you are eligible to enroll. You also may

obtain additional information for each investment option

by reviewing the Annual Participant Fee Disclosure

Notice. You may obtain a copy free of charge by accessing

your account online at benefits.ml.com or by calling the

Customer Service Center at 888‑968‑4015.

Please note that this Plan is intended to be an “ERISA

Section 404(c) plan.” This means that you assume all

investment risks connected with the investment options

you choose in the Plan, or in which your funds are invested

if you fail to make investment selections, including the

increase or decrease in market value. Walmart Stores, Inc.,

the Benefits Investment Committee and the trustee are not

responsible for losses to your accounts which are the direct

and necessary result of investment decisions you make or,

if you fail to make an affirmative investment decision, as a

result of your accounts being invested in a default fund.

If you have a Company Funded Profit Sharing Account (see

Your Walmart 401(k) Plan accounts earlier in this summary)

and you choose to invest some or all of your Company

Funded Profit Sharing Account in Walmart stock or retain

Walmart stock in your other accounts, be aware that since

this option is a single stock investment, it generally carries

more risk than the options offered through the Plan.

HOW TO OBTAIN MORE INVESTMENT INFORMATION

It is also important to periodically review your investment

portfolio, your investment objectives and the investment

options under the Plan to help ensure that your investments

are in line with your objectives and your risk tolerance. If

you would like more sources of information on individual

investing and diversification, you may go to the website of the

Department of Labor, http://www.dol.gov/ebsa/investing.html.

You may obtain more specific information regarding your

investment rights and investment options under the Plan at

benefits.ml.com or by calling the Customer Service Center

at 888‑968‑4015.

CHANGING YOUR INVESTMENT CHOICES

You can change your investment choices at any time online

at benefits.ml.com or by calling the Customer Service

Center at 888‑968‑4015. If you make an investment change,

a confirmation notice will be sent to your home address or

you will receive an email notification when the confirmation

is available if you have chosen electronic delivery of your

Plan materials. It is your responsibility to make sure your

change is made. If you do not receive a confirmation notice

or you do not see that your change has been applied, contact

the Customer Service Center at 888‑968‑4015.

If you call the Customer Service Center at 888‑968‑4015

prior to 3:00 p.m. Eastern time, your investment change

generally will be processed on the day you call. Depending

on the investment change, there may be up to a three-day

settlement period before your funds are invested in your

new election.

The Walmar 401(k) Plan

9

2018 Associate Benefits Book | Questions? Log on to WalmartOne.com or the WIRE, or call People Services at 800 -421-1362

DIVERSIFICATION

To help you diversify your retirement savings, the Plan

offers a variety of investment options with different levels

of risk and potential for increase in value. To “diversify”

means that you “put your eggs in more than one basket.”

To help achieve long-term retirement security, you should

give careful consideration to the benefits of a well-balanced

and diversified investment portfolio. This strategy can help

reduce risk and may provide consistent returns because a

decline in the value of one investment may potentially be

offset by an increase in the value of another. If you invest

more than 20% of your retirement savings in any one stock,

such as Walmart stock, or any one industry, your savings

may not be properly diversified. Although diversification

cannot ensure a profit or protect against loss, it can be an

effective strategy to help you manage investment risk.

When deciding how to invest your retirement savings, you

should take into account all of your assets, including any

retirement savings outside of the Plan. For example, you

may own Walmart stock through other means. No single

approach is right for everyone because, among other

factors, individuals have different financial goals, different

time horizons for meeting their goals, and different

tolerances for risk. Therefore, you should keep in mind your

rights to diversify your Plan account and carefully consider

how you choose to invest your Plan account. You can obtain

information about your right to diversify your account and

all of the investment options available under the Plan by

accessing your account online at benefits.ml.com or by

calling the Customer Service Center at 888‑968‑4015. It

is also important to periodically review your investment

portfolio, your investment objectives and the investment

options under the Plan to help ensure that your investments

remain appropriate for your retirement goals and your

tolerance for investment risk. If you would like more

sources on individual investing and diversification, you

may go to the website of the Department of Labor,

http://www.dol.gov/ebsa/investing.html.

More about owning Walmar stock

VOTING

If any of your account is invested in Walmart stock through

the Plan, each year you will receive all of the materials

generally distributed to the shareholders of Walmart,

including an instruction card telling the trustee how you

would like the shares in your Plan account to be voted.

The materials will be mailed to your home address or sent

electronically, based on your online elections.

You can instruct the trustee, through the company’s

transfer agent, to vote Walmart stock held in your Plan

accounts. This usually occurs in May of each year. Your

instructions to the transfer agent and the trustee are

kept confidential at all times. You will send your voting

instructions directly to the transfer agent, who will compile

the votes and notify the Benefits Investment Committee

of the total votes cast. The Benefits Investment Committee

will then notify the Plan trustee of the total votes that are

to be cast.

If you do not provide instruction to the trustee on how

you would like your shares voted, the Benefits Investment

Committee will vote those shares at its discretion. If neither

you nor the Benefits Investment Committee exercise voting

rights, the trustee or an independent fiduciary appointed by

the trustee may vote the unvoted shares.

CONFIDENTIALITY

Procedures have been designed to protect the

confidentiality of your rights with respect to shares of

Walmart stock held under the Plan, including the right to

purchase, sell, hold or vote on proxy matters. For example,

procedures with the Company’s transfer agent for Walmart

stock have been implemented that prevent Wal-Mart

Stores, Inc. and the Benefits Investment Committee from

finding out how any individual participant or beneficiary

voted (except as necessary to comply with securities laws)

and from having access to your individual proxy cards or

proxy card shareholder comments.

In addition, access to information about your decisions to

buy, sell or hold Walmart stock generally is limited to those

assisting in the administration of the Plan. The Benefits

Investment Committee is responsible for ensuring that these

procedures are sufficient to protect the confidentiality of

this information and that the procedures are being followed.

If the Benefits Investment Committee determines that a

situation has potential for undue influence by the Walmart

with respect to your rights as shareholder (through your

Plan Account), the Benefits Investment Committee will

appoint an independent party to perform activities that are

necessary to prevent undue influence.

DIVIDENDS ON YOUR WALMART STOCK

If you have Walmart stock in your accounts, your accounts

will be credited with any dividends paid by Wal-Mart Stores,

Inc. with respect to its stock. Dividends allocated to your

401(k) Account, your Company Funded 401(k) Account

or your 401(k) Rollover Account will be automatically

reinvested in Walmart stock. Dividends allocated to your

Company Funded Profit Sharing Account (and Profit

Sharing Rollover Account) will also be reinvested in Walmart

stock, except as noted below.

If you are an active participant (excludes beneficiaries

and alternate payees, as defined in the If you get divorced

section) with six or more years of service, you have an option

to take a cash payout of any dividends paid on Walmart stock

held in your Company Funded Profit Sharing Account or

The Walmar 401(k) Plan

10

Profit Sharing Rollover Account. Also, if you are a terminated

participant who had more than six years of service when you

terminated and you continue to maintain your accounts in

the Plan after you leave, you will have the option to elect a

cash payout of dividends paid on Walmart stock held in your

Company Funded Profit Sharing Account or Profit Sharing

Rollover Account. If you do not opt for the cash payout, your

dividends will be reinvested in Walmart stock.

You may make an election any time by calling the Customer

Service Center at 888‑968‑4015. Your most recently filed

election will apply to all subsequent dividends until you

change your election. (You may change your election only

once each business day.) Keep in mind that your election

must be made no later than the close of business on the

day prior to the record date for the dividend in order to be

effective for that dividend. You will not be able to make any

elections or election changes during the period from the

record date of the dividend through the dividend pay date

(which is usually three to four weeks after the record date).

Each year, Wal-Mart Stores, Inc. releases the quarterly

record dates for dividend payouts. You can find this

information on walmart.com. You may also contact the

Customer Service Center at 888‑968‑4015 if you need

information about upcoming record dates for dividends.

You should keep in mind that a dividend payout will be

taxable to you.

Please note that if you request a hardship payout from

your 401(k) Account within five business days of the record

date for a dividend and you have the right to elect a cash

distribution of the dividend, tax laws require that the

dividend be automatically paid to you in cash.

Account balances and statements

At least once a year, you’ll receive a statement on your

accounts showing contributions made by you and by

Walmart, if any, the performance of your investment

options, the values of your accounts and fees assessed

to your account during the quarter. You can easily get

information about your accounts, including a quarterly

statement, at any time online at benefits.ml.com or by

calling the Customer Service Center at 888‑968‑4015. You

can also request a paper copy of any quarterly statement

at any time free of charge by calling the Customer Service

Center at 888‑968‑4015.

FEES CHARGED TO YOUR ACCOUNT

Administrative and investment fees may be assessed

to your accounts. You can find information on fees in the

Annual Participant Fee Disclosure Notice and online at

benefts.ml.com.

Receiving a payout while working

forWalmar

Generally, you are not entitled to a payout from the

Walmart 401(k) Plan until you stop working for Walmart.

However, in the following limited situations you may be

entitled to receive a payout or loan of some or all of your

accounts while you’re still working:

• You may request a loan from your Plan account.

• Rollovers can be withdrawn at any time.

• In the case of a financial hardship or after you attain

age59½.

It’s important to understand how any type of payout or loan

from the Walmart 401(k) Plan affects your tax situation. For

more information, see The income tax consequences of a

payout later in this summary.

FINANCIAL HARDSHIP WITHDRAWALS

You may withdraw some or all of your 401(k) Account (other

than earnings on those contributions) and your 401(k)

Rollover Account as necessary to meet a “financial hardship.”

Under IRS guidelines, a financial hardship may exist if the

request is for:

• Payment of medical care expenses not covered by

insurance for you, your spouse, your dependents or your

affirmatively-designated primary beneficiary

• Costs directly related to the purchase of your primary

residence (home)

• Payment of tuition, fees, and room and board expenses for

up to the next 12 months of post-high school education for

you, your spouse, your dependents or your affirmatively-

designated primary beneficiary

• Payments necessary to prevent eviction from, or

foreclosure on, your primary residence

• Payment for burial or funeral expenses for your deceased

parent, spouse, children, dependent or your affirmatively-

designated primary beneficiary, or

• Expenses for the repair of damage to your principal

residence that would qualify for a casualty deduction

under federal income tax rules.

Federal tax law requires that you must have already

obtained all in-service payouts available (including in-service

withdrawals of rollover contributions or at age 59½ and any

nontaxable participant loans available to you under this Plan)

before you can request a financial hardship payout.

Also, federal tax laws will not allow you to contribute to this

Plan and certain other retirement or stock purchase plans

(including the Associate Stock Purchase Plan) for six months

after the date of your financial hardship payout. If you are

a management associate with stock options, you may not

The Walmar 401(k) Plan

11

2018 Associate Benefits Book | Questions? Log on to WalmartOne.com or the WIRE, or call People Services at 800 -421-1362

exercise options during this six-month period. Also, please

note that if you request a financial hardship payout within

five business days of the record date of a dividend and you

are entitled to elect a cash payout of that dividend, the

dividend will automatically be distributed to you in cash.

A financial hardship payout is immediately taxable to you,

including a 10% penalty tax if you are under age 59½ or if

the payout is not for certain medical purposes. For more

information, see The income tax consequences of a payout

later in this chapter.

You can make a request for a financial hardship payout

online at benefits.ml.com or by calling the Customer

Service Center at 888‑968‑4015.

WITHDRAWALS AFTER YOU REACH AGE 59½

Any time after you reach age 59½, you may elect to

withdraw all or any portion of your Plan accounts, to

the extent vested, even though you are still working for

Walmart. You can make a request for a withdrawal online at

benefits.ml.com or by calling the Customer Service Center

at 888‑968‑4015.

WITHDRAWALS OF ROLLOVER CONTRIBUTIONS

You may withdraw all or any portion of your 401(k)

Rollover Account and your Profit Sharing Rollover

Account at any time even if you are still working for

Walmart or its subsidiaries.

PLAN LOANS

You may apply for a loan from the vested portion of your

Plan account while you are still working for Walmart. The

Administrator has established a written loan program

which explains these requirements in more detail. You can

request a copy of the loan program or make a request for a

loan online at benefits.ml.com or by calling the Customer

Service Center at 888‑968‑4015.

Generally, the rules for loans include the following:

• The maximum loan amount is limited by IRS rules, which

generally limit your total loan balances to the lesser of

(1) 50% of the total of your vested Plan account or (2)

$50,000 (reduced by the excess, if any, of your highest

outstanding loan balance during the one-year period prior

to the date of the loan over your current outstanding

balance of loans). The minimum loan amount is $1,000.

• All loans must be secured by a pledge of up to one-half of

your vested Plan account.

• A fee will be charged to process your loan application.

Additional fees may be accessed for residential loans. (This

amount may change from time to time.)

• All loans will bear a commercially reasonable rate of

interest set by the Administrator from time to time.

• Loans must be repaid in regular installments over a one- to

five-year period, unless you are using the loan proceeds

to buy a house for yourself, in which case the repayment

period may be longer as set forth in the written loan

program from time to time.

• You may have only one general purpose loan and one

residential loan outstanding at any time.

• All loans will be considered a directed investment from

your account under the Plan. Your payments of principal

and interest on the loan will be credited to your Plan

accounts.

• If you fail to make payments when due under the loan,

you will be considered to be in default. Under certain

circumstances, a loan that is in default may be considered

a distribution from the Plan. The significance of the loan

balance being treated as a distribution is that the amount

of this distribution will be taxable to you as ordinary

income and could be subject to excise taxes. A Form

1099-R will be issued to you and the total amount of the

distribution will be reported to the IRS.

When you are on an authorized unpaid leave of absence,

you may be excused from making scheduled loan

repayments for a period up to one year. If you have an

outstanding loan when you are called to qualified military

service, special rules under USERRA may apply. If you think

you may be affected by these rules, call the Customer

Service Center at 888‑968‑4015 for more details.

If you die: your designated beneficiary

In the event of your death, your entire Plan balance will be

paid out to your beneficiary. It is very important for you to

keep your beneficiary information up to date. Beneficiary

choices should be made at WalmartOne.com, the WIRE

or Workday. Since your spouse or partner has certain

rights in the death benefit, you should immediately update

your beneficiary election if there is a change in your

relationship status.

If you have a spouse and wish to name someone other than

your spouse as your designated beneficiary, your spouse

must consent to that designation. You must complete the

Alternate Beneficiary Form for Married Participants Form

B and your spouse must complete the Spousal Consent

portion of that form. The Spousal Consent form must

be notarized and must accompany the Form B in order

to be valid. Form B and the Spousal Consent form can

be found on the WIRE, or you may talk to the personnel

representative at your facility. Any beneficiary designation

you make will be effective for all of your Plan accounts.

The Walmar 401(k) Plan

12

If you do not designate a beneficiary, your death benefit

will be distributed in accordance with the Plan’s default

provisions in the following order, as stated below:

• Spouse or partner (as defined below); if none, then

• Living children (stepchildren are not included);

if none, then

• Living parents; if none, then

• Living siblings; if none, then

• The estate.

Please note that if you designate your spouse as your

beneficiary and you later divorce, your designation will not

be effective after the divorce unless you complete a new

designation form. Similarly, if you do not have a spouse and

you later marry, your prior beneficiary designation will not

be effective after the marriage unless you complete a new

designation form with your spouse’s consent.

Also, note that if you designate a beneficiary and your

beneficiary dies before the benefit check is issued, the

benefit will be paid to your contingent beneficiary or, if

none, under the default rules above. If your beneficiary dies

after the benefit check has been issued, the benefit will

be paid to your beneficiary’s estate. Note, however, that

if your spouse or partner is your beneficiary, the benefit

will always be paid to the spouse’s or partner’s estate if

he or she dies after you but before the benefit is paid.

Again, it is very important for you to keep your beneficiary

information up to date. Beneficiary choices should be made

at WalmartOne.com, the WIRE or Workday.

NOTE: Effective June 26, 2013, your same-sex spouse will

be treated in the same manner as an opposite-sex spouse

for Plan purposes. Keep in mind that if you had a same-sex

spouse on that date, any beneficiary designation you had in

effect which designated someone other than your spouse

as your beneficiary immediately became invalid on that

date. Your spouse will automatically be your beneficiary

unless you make a new beneficiary designation with your

spouse’s consent.

Effective January 1, 2014, if you have a “partner” and you

have not made an affirmative beneficiary designation, your

partner will be your beneficiary unless you affirmatively

designate a different beneficiary (regardless of whether

the designation occurred before or after your partnership

began). Your “partner” for Plan purposes means:

• Your domestic partner, as long as you and your domestic

partner:

– Are in an ongoing, exclusive and committed relationship

similar to marriage and have been for at least 12 months

and intend to continue indefinitely;

– Are not married to each other or to anyone else;

– Meet the age for marriage in your home state and are

mentally competent to consent to contract in that state;

– Are not related in a manner that would bar a legal

marriage in the state in which you live, and

– Are not in the relationship solely for the purpose of

obtaining benefits coverage, or

• Any other person to whom you are joined in a legal

relationship recognized as creating some or all of the

rights of marriage in the state or country in which the

relationship was created.

You should take action to ensure that your beneficiary under

the Plan reflects your current intent. Beneficiary choices

should be made at WalmartOne.com, the WIRE or Workday.

BENEFICIARY DESIGNATIONS MADE BEFORE

OCTOBER 31, 2003

If you made a beneficiary designation under the 401(k) Plan

on or before October 31, 2003, that designation will continue

to apply to your 401(k) Account, your Company Funded

401(k) Account, your Company Match Account, and your

401(k) Rollover Account. Similarly, if you made a beneficiary

designation under the Profit Sharing Plan on or before

October 31, 2003, that designation will continue to apply to

your Company Funded Profit Sharing Account and Profit

Sharing Rollover Account. If you change your beneficiary

designation after October 31, 2003, it will apply to all Plan

accounts and any prior designations will be ineffective.

Note that changes in your relationship status may affect

your beneficiary designation, as explained above.

Again, it is very important for you to keep your beneficiary

information up to date. Beneficiary designations should be

made at WalmartOne.com, the WIRE or Workday.

If you get divorced

If you go through a divorce, all or part of your Plan balance

may be awarded to an “alternate payee” in the court order,

called a “Qualified Domestic Relations Order” (QDRO).

An alternate payee may be your spouse or former spouse,

child or other dependent. (Federal law at this time does

not permit the recognition of a QDRO for a partner

unless the partner is also a dependent of the participant.)

Because there are very strict requirements for these

cases, you should contact the QDRO Administrator at

877-MER-QDRO (877‑637‑7376) for a free copy of the

procedures your attorney should use in drafting the court

order. After the court order is received by the QDRO

Administrator, it must be reviewed to determine if it meets

legal requirements for this type of order and will take a

period of time to be processed. The administrative fee for

processing your QDRO will be charged to your account or

as directed in the Order.

The Walmar 401(k) Plan

13

2018 Associate Benefits Book | Questions? Log on to WalmartOne.com or the WIRE, or call People Services at 800 -421-1362

If you leave Walmar

When you stop working for Walmart, you are entitled to

receive a payout of all of your vested accounts in the Plan.

It is important to understand how any type of payout from

the Walmart 401(k) Plan affects your tax situation. For more

information, see The income tax consequences of a payout

later in this summary.

You may elect to receive your payout 30 calendar days after

your termination is entered into the payroll system. For

example, if your termination is entered into and processed

by the payroll system on July 19, 2017, you may elect your

payout on or after August 18, 2017.

A notice will normally be mailed to your home address or

sent electronically, based on your delivery elections, after

you leave Walmart and its subsidiaries to inform you that

you are entitled to payment. Please make sure that your

address is correct on your payroll check when you leave

Walmart and its subsidiaries or that you give a forwarding

address during your exit interview. If you have not received

any information regarding your payout within 60 days of

your termination date, you should contact the Customer

Service Center at 888‑968‑4015. To request your payout,

you will need to access your account on benefits.ml.com or

by calling the Customer Service Center at 888‑968‑4015.

Your consent to the payout is not required and your payout

will automatically be made to you:

• If your total vested Plan balance (excluding your 401(k)

Rollover Account) is $1,000 or less at any time. This

automatic payout will be made as soon as possible

after the last business day of the third calendar month

following the calendar month in which your termination

date is entered into the payroll system, unless you

consent to an earlier payout. as described above. In the

example above, if your account is eligible for automatic

payout and you do not consent to payout on or after

August 19, 2017, your payout will automatically be made

to you as soon as possible after October 31, 2017, or

• If you are over age 70, regardless of the amount of your

total vested Plan balance. This automatic payout will

be made as soon as possible after the last business day

of the second calendar month following the calendar

month in which you turn age 70, unless you consent to

an earlier payout. as described above. For instance, if

you turn age 70 in July 2017 and your account is eligible

for automatic payout, and you do not consent to payout,

your payout would automatically be made on the first

scheduled date after September 30, 2017, according to

Plan provisions.

If your total vested Plan balance is more than $1,000

and you are under age 70, you must consent to your

payout. Payout will be made as soon as possible after your

consent is received by the Customer Service Center at

888‑968‑4015, but no earlier than 30 calendar days after

your termination is entered into the payroll system.

If your total vested Plan balance is more than $1,000,

you can choose to delay your payout until any date up to

age 70, but your Plan balance will be subject to an annual

maintenance fee and possibly other expenses. For more

information regarding these charges, refer to the Annual

Participant Fee Disclosure Notice. If you choose to delay

your payout, you will be able to continue to make changes

in your investment choices just as you did while you were an

active participant in the Plan.

If you return to work with Walmart before your payout is

completed, the payout will be canceled and no payout will

be made from your account.

THE AMOUNT OF YOUR PAYOUT

The entire value of your 401(k) Account, your Company

Funded 401(k) Account, your 401(k) Rollover Account

and the Company Match Account will be paid out to you.

In addition, if you have a Company Funded Profit Sharing

Account (see Your Walmart 401(k) Plan accounts earlier in

this summary), you will also be paid the value of the vested

portion of your Company Funded Profit Sharing Account.

You will forfeit (give up) the nonvested portion of your

Company Funded Profit Sharing Account, as explained

in the Vesting in your Company Funded Profit Sharing

Account earlier in this summary.

The amount you will receive will be based on the value of

your accounts as of the date the payout is processed. If a

cash payout is made directly to you rather than rolled over

to an IRA or other employer plan, applicable taxes will be

withheld from your check.

A check processing fee will be applied to your Plan balance

when it is paid out to you.

HOW YOU RECEIVE YOUR PAYOUT

You have several options for receiving your payout.

Your accounts will be distributed in a single lump-sum

payment directly to you, unless you elect to roll them over

to an IRA or to another employer’s retirement plan.

Your accounts will normally be paid to you in cash.

However, you may elect to have your Company Funded

Profit Sharing Account (and Profit Sharing Rollover

Account) distributed to you in the form of Walmart stock

(even if it is not invested in Walmart stock at the time

your payout is processed) or partly in cash and partly in

Walmart stock. You may also elect to have your 401(k)

Account, your Company Funded 401(k) Account and your

401(k) Rollover Account paid to you in Walmart stock to

the extent those accounts are invested in Walmart stock

The Walmar 401(k) Plan

14

at the time your payout is processed. Any part of those

accounts that is not invested in Walmart stock at the time

of your payout will be distributed in cash.

If the total of your vested accounts is $1,000 or less, or

if you are over age 70 (regardless of the amount of your

vested accounts), your payout will be made directly to you in

a single cash payout. If you wish to take any of your payout

in the form of Walmart stock or if you wish to roll over your

payout to an IRA or other employer plan, you must contact

the Customer Service Center at 888‑968‑4015 with your

payout instructions within the time period shown in your

payout notice. If you fail to contact the Customer Service

Center at 888‑968‑4015 in a timely manner, your payout

will be made in a single cash payment to you.

If the total of your vested accounts in the Plan is more

than $1,000, your payout will not be made until you make

an election regarding the form of payout and consent to

the distribution, or until you reach age 70. To obtain your

payout, you should contact the Customer Service Center at

888‑968‑4015.

If you leave and are rehired by Walmar

If you leave Walmart and its subsidiaries and are later

rehired as an eligible associate, you will be immediately

eligible to make your own contributions to the Plan on your

date of rehire.

If you leave Walmart and its subsidiaries after you became

eligible to receive matching contributions and are later

rehired by Walmart, you will automatically be eligible to

receive matching contributions on your rehire date. Similarly,

if you leave Walmart and its subsidiaries after you met the

1,000-hour requirement for matching contribution eligibility

but before your actual participation date, you will be eligible

to receive matching contributions beginning on the later

of the date you would have initially become a participant or

your rehire date (with respect to contributions you make

after that date). If you were not a participant when you left,

or had not satisfied the 1,000-hour requirement, you will be

treated as a new associate when you are rehired and will be

required to complete the eligibility requirements (see When

participation begins earlier in this summary) in order to be

eligible to receive matching contributions under the Plan.

THE NONVESTED PORTION OF YOUR COMPANY

FUNDED PROFIT SHARING ACCOUNT

When you terminate employment, the portion of your

Company Funded Profit Sharing Account that is not vested

(if any) will not be paid to you. This nonvested amount is

called a “forfeiture.”

• If you receive a total payout of your vested Plan balance

after your termination of employment and while your

Company Funded Profit Sharing Account is partially

vested, the nonvested portion of your Company Funded

Profit Sharing Account will be forfeited on the date of

your payout.

• If you do not receive a total payout of your vested Plan

balance after your termination of employment, the

nonvested portion of your Company Funded Profit

Sharing Account will not be forfeited until you have five

consecutive “breaks in service.” A break in service is a Plan

year (February 1–January 31) in which you are credited with

500 hours of service or less. If you are absent from work

due to an FMLA leave and have worked 500 hours or less

in the Plan year, you will be credited with enough hours to

bring you up to 500.01 hours so that you will not incur a

break in service.

The nonvested portion of your Company Funded Profit

Sharing Account that was forfeited will be reinstated (at its

former value) if you are rehired by Walmart or subsidiary

before you have five consecutive breaks in service and you

pay back to the Plan the total amount of your payout within

five years after you are rehired. If you return to work with

Walmart or a subsidiary after five or more consecutive

breaks in service, or if you chose not to repay your payout

as discussed above, the nonvested portion of your Company

Funded Profit Sharing Account that was forfeited will not

be reinstated.

If you were zero percent vested in your Company Funded

Profit Sharing Account when you terminated employment,

your nonvested Company Funded Profit Sharing Account

will automatically be reinstated if you are rehired prior to

five consecutive breaks in service.

Forfeitures of nonvested Company Funded Profit Sharing

Accounts of terminated participants generally are used to

pay Plan expenses and for certain other purposes, such as to

restore account balances as discussed above.

When you are rehired, your years of service with Walmart

before you left will be counted for purposes of determining

your vesting in Walmart’s contributions to your Company

Funded Profit Sharing Account.

The income tax consequences of

apayout

The tax consequences of your participation in the Plan

are your responsibility. This explanation is only a brief

description of the U.S. federal tax consequences related

to your participation in the Plan. This description is based

on current law and current interpretations of the law by

the Internal Revenue Service. Because the law is subject

to change and because the application of the law may

vary depending on your particular circumstances, this

description is general in nature and you should not rely on

it in determining your tax consequences. You are strongly

urged to consult a tax advisor.

The Walmar 401(k) Plan

15

2018 Associate Benefits Book | Questions? Log on to WalmartOne.com or the WIRE, or call People Services at 800 -421-1362

Walmart is entitled to a deduction on the amount of its

contributions, as well as your contributions, to the Plan.

Your contributions and Walmart’s contributions to the Plan,

as well as earnings on those contributions, generally are not

subject to federal income taxes until they are paid to you.

Special taxation rules apply to Roth contributions

transferred from another Plan as part of a Plan merger.

Contact the Plan Administrator or your tax advisor for more

information.

POSTPONE PAYING TAXES ON PAYOUTS THROUGH

AROLLOVER

Although payouts from the Plan are subject to federal

income taxes, the Internal Revenue Code provides favorable

tax treatment to payouts in certain circumstances. For

example, you can postpone paying taxes on your payout

if you direct the Plan to issue your payout directly to an

IRA or to another employer’s qualified retirement plan,

a 403(b) plan or a governmental 457 plan. This is called a

direct rollover. (The check will be made payable to the IRA

or other plan trustee and will be delivered to you or your

IRA or rollover institution. If the check is mailed to you, you

will be responsible for delivering it to the IRA or other plan

trustee within 60 days.)

If you elect this method for your payout, no taxes will be

withheld from the amount you are rolling over. It will not

be taxed until you later receive a payout from the IRA or

other plan.

If you do not elect to have your payout directly rolled over,

federal law requires that Walmart withhold 20% of the

payout for federal taxes, in addition to any required state

withholding. In some cases, 20% withholding may not be

enough, which could mean that you will owe additional taxes

when you file your income tax return.

If you do not elect a direct rollover (and instead receive an

actual payout from the Plan), you may still roll over those

funds to an IRA or an employer’s qualified retirement plan,

403(b) plan or governmental 457 plan, as long as you do so

within 60 calendar days after you received the distribution.