1

CHAPTER FOUR

Financial Statement Analysis

I think Southwest has a great model. They're used to efficiency. They bought new

airplanes. They turned them (around) quickly on the ground. We loved the efficiency side

of the business, but we thought they may be a little too much of a prisoner to their

success.

-David Neeleman, the founder and former CEO of JetBlue Airways

and also founder of Azul Linhas Aéreas Brasileiras.

Based on an understanding of airline financial statements, the analysis of the statements is

performed using ratio analysis. Such financial indices as return on investment (ROI), profit

margin, debt-equity ratio, and price-earnings ratio are used not only internally by airlines, but

also externally by the investment community. Airline industry specific metrics, such as cost per

available seat mile (CASM) and revenue per revenue passenger mile (RRPM), are also

introduced. Using ratios and other financial analysis techniques, airline benchmarking of US

carriers, is performed to help recognize strong financial airlines and to understand how they are

successful by dissecting their financial statements.

o Financial ratio analysis

o Profitability ratios

o Liquidity ratios

o Long-term risk ratios

o Stock market ratios

o Financial ratios: Airline specific ratios

o Airline industry benchmarking

o Predicting insolvency

o Summary

o Appendix: IATA two-letter airline codes: US carriers

While financial statements are essential in helping to analyze a company, they are merely

the starting point for successful financial management. Financial statements provide the raw

figures on the company’s financial position; however, these numbers are only meaningful when

compared to other firms competing in the industry. The various tools that are used to compare

financial statements to assess a firm’s financial condition and performance are commonly

referred to as ratio analysis. Ratio analysis encompasses a wide variety of calculations and

2

metrics that enable a manager to quickly spot trends in the company’s performance, highlighting

historical performance and projections for the future.

Financial Ratio Analysis

There are two major comparisons that ratio analysis provides and these are comparisons

of the firm across time and comparisons of the firm with the industry. Using ratio analysis,

financial results can be standardized across time to help analyze a company’s financial

performance through various periods. This level of analysis is most effective when the time

period of analysis if fairly short so that actions can be taken in response to any trends the

company may be facing. The more powerful ratio analysis comparison is with other firms

competing in the same industry. With financial statements readily available for all publicly-

traded companies, benchmarking of competing firms can easily be undertaken to help understand

a company’s financial position within the industry. This benchmarking effectively enables firms

to recognize their strengths and weaknesses relative to the industry and, since firms vary in size

and composition, is only possible through the standardization that ratio analysis provides.

The various ratios used in the analysis can be classified into four categories based on

what portion of the company that they are analyzing:

Profitability ratios

Liquidity ratios

Long-term risk ratios

Stock market ratios

Profitability ratios help describe the efficiency or success of the business. Liquidity ratios

describe the firm’s ability to meet short term obligations. Long-term risk ratios analyze the

capital structure of a company and take a more macro-level approach to analyzing the company.

Finally, stock market ratios deal specifically with publicly-traded companies and describe the

company’s position in the stock market. Regardless of the type of ratio used, a single ratio by

itself does not accurately describe the firm; rather, a number of ratios should be used to help

provide a broader perspective on the company. This point is exacerbated by the fact that there

are multiple ratios that can be used to analyze the same part of the company. Therefore, there are

no set criteria for which ratios to be used when analyzing a company; however, the more ratios

that are used in the analysis, the better the picture that is painted of the company.

3

This chapter explains the various ratios that might be used in performing ratio analysis by

using these ratios to analyze the financial statements of Southwest Airlines. While all the ratios

can be used to adequately describe the financial position of a company, the uniqueness of the

airline industry requires additional calculations to understand the finances of an airline. Finally,

based on the common and airline-specific financial calculations, an exercise in the benchmarking

of various US airlines is presented to show the merits of ratio analysis and to provide a better

financial understanding of the airline industry.

Profitability Ratios

As mentioned previously, profitability ratios help describe the success of the business by

comparing the profits (or losses) generated against a variety of baselines. This helps standardize

the profits of companies, making it easier to compare the profitability of one company against

the profitability of another company. While this comparison helps standardize large and small

companies alike, it is not necessary the most useful tool in comparing companies across multiple

industries, since the industry dynamics can vastly distort how companies generate a profit. The

five profitability ratios that will be explained for Southwest Airlines in 2006 are:

- Operating profit margin ratio

- Profit margin ratio

- Return on assets

- Return on equity

- Asset turnover ratio

Operating Profit Margin Ratio

The operating profit margin ratio compares the operating profit of a company to the total

revenue generated. It enables a manager to determine how much operating profit is generated for

every dollar of revenue. The operating profit margin can be particularly useful when analyzing a

company as it excludes items such as interest expense and taxes, which are largely based on the

macro-structure of the company. Excluding these items generally enables a greater in-depth

analysis of the company’s operations. Also, because we are excluding special items on the

income statement in the calculation, this means that the operating profit margin ratio tends to

remain more stable over time; the formula for calculating the operating profit margin ratio is:

4

Operating Profit

Operating Profit Margin =

Total Revenue

Both items for calculating the gross profit margin ratio are found on the income

statement. Operating profit is also commonly referred to as EBIT, or Earnings before Interest

and Taxes. Referring back to chapter 3, the gross profit margin for Southwest Airlines in 2007

was actually calculated in the common-size income statement, since the third column contained

most of the items as a percentage of total revenue. As a refresher, Southwest Airlines 2007

operating profit margin was:

$791 million

Operating Profit Margin = x 100% = 8.02%

$9,861 million

Based on the gross profit margin calculated above, every dollar of revenue generated by

Southwest Airlines created roughly 8 cents of operating profit for the company. As a

comparison, the gross profit margin for Southwest Airlines was 10.3 % in 2006, in 2005 was

9.5% and 6.2% in 2004. Obviously, Southwest Airlines was able to increase its gross profit

margin during the period from 2004 to 2006, and this by itself is a positive signal; however,

profit margin declined in 2007. We can see from these ratios that revenue was increasing at a

greater rate than unit costs from 2004-2006. However, while these values appear to display a

strong company, they need to be compared with figures for the rest of the industry to understand

Southwest Airlines position in the market.

Profit Margin Ratio

The profit margin ratio is similar in methodology to the gross profit margin ratio and it

represents the net income of the company as a percentage of total revenue. The profit margin

takes into consideration all facets of a company’s financial structure and standardizes the

financial bottom-line of the firm. The profit margin enables million dollar companies to be

5

compared with billion dollar companies as it shows how much net income is generated for every

dollar of revenue. The profit margin formula and Southwest Airlines 2007 profit margin are:

6

Net Income

Profit Margin =

Total Revenue

NI

TR

$645 million

Profit Margin = x 100% = 6.5%

$9,861 million

Based on the audited financial statements of Southwest Airlines, every dollar generates

6.5 cents of profit for the company. Comparatively, 2006’s figure was 5.5%, down from 2005’s

profit margin of 6.4%, but a significant increase over 2004’s 3.3% profit margin ratio.

Interestingly, this displays a slightly different perspective on the company than the gross profit

margin ratio which displayed Southwest Airlines profit trend as continually increasing. This

paradox is the result of a significant one-time loss charge posted by Southwest Airlines in 2006.

1

This shows the importance of both calculations when performing ratio analysis, since the

airline’s gross profit margin declined from 2006 to 2007 while total profit margin increased. If

only one or the other of the ratios were calculated, the results could be potentially deceiving

when analyzing the company.

Return on Assets (ROA)

Another profitability ratio that can be used to help standardize large and small companies

is the return on assets ratio. This ratio measures the net income of the company after taxes

against the fixed assets of the company. This shows the investment return that assets have

provided. A company invests in fixed assets in an effort to generate increased profits, and

therefore the return on assets ratio analyzes a company at the very fundamental elements of

business. The formula for the return on assets is:

1

Refer to the income statement in figure 3 of Chapter 3 which displays a $150 million other net loss in 2006,

compared to a $90 million other net gain posted in 2005.

7

Net Income

Return on Assets (ROA) =

Total Assets

NI

TA

with Southwest Airlines 2007 return on assets being:

$645 million

ROA = x 100% = 3.85%

$16,772 million

Southwest Airlines 2007 return on assets ratio indicates that $100 spent on assets yielded

3.85 cents of profit for the company. The return on assets ratio varies considerably by industries,

since some industries are more highly capital intensive than others. The airline industry is highly

capital intensive, therefore the average industry return on assets is likely to be lower than in

other industries. Because of this, the best way to compare the return on assets ratio is between

companies competing within the same industry, providing a valuable benchmark by which to

judge the firm.

Return on Equity (ROE)

Similar in goal and methodology to the return on assets ratio, return on equity measures

the company’s performance against the total stockholders’ equity in the company. The general

formula for the return on equity formula and Southwest Airlines 2007 return on equity is once

again found by referring back to both the income statement and balance sheet:

Net Income

Return on Equity (ROE) =

Total Stockholders' Equity

$645 million

ROE = x 100% = 9.29%

$6,941 million

Unlike the return on assets ratio which may vary considerably from industry to industry,

the return on equity ratio does not vary as much between industries. However, it may contain a

8

larger variance between the companies competing within the industry. While this particular ratio

is beneficial to investors, distortions may exist due to the financial structure of a company. For

example, a company that is more heavily debt financed may have an artificially higher return on

equity ratio than a company that is more equity financed. Therefore, there are multiple issues to

consider when analyzing companies’ return on equity ratios.

Southwest Airlines 2007 return on equity ratio of 9.29% was slightly higher than 2006’s

return on equity of 7.74% and 2005’s return on equity of 7.25%.

2

This was due to Southwest

Airlines equity structure remaining stable while producing a similar level of profits. Ideally,

greater investment in the company should yield higher returns on equity since the company is

able to take the equity gained and use it in areas where profits can be made. However, in a

mature industry such as the airline industry, increased investment is not always possible as there

may be very few areas that could generate new profits.

Asset Turnover Ratio

The asset turnover ratio measures total revenue against the total assets of the company.

Similar in vain to the return on assets metric, the asset turnover ratio shows how much revenue

assets generate for the company. Asset turnover is calculated using the formula and the results

for Southwest for 2007 are calculated below:

Total Revenue

Asset Turnover =

Total Assets

TR

TA

$9,861 million

Asset Turnover = = 0.5879

$16,772 million

An asset turnover ratio of 0.5879 indicates that every $100 worth of assets generates

$58.79 of revenue. An interesting relationship between three of the profitability ratios is the

following:

2

Return on Equity (2005) = $484 million / $6,675 million = 7.25%

9

Return on Assets = Profit Margin * Asset Turnover

ROA = PM * ATO

Therefore, only two of the three ratios above need be calculated to determine the

remaining ratio. It also indicates how each ratio is looking at a similar component of the

company, but goes about analyzing the company in a unique way. Understanding how a

company’s profits are generated from assets is a critical component to understanding the

financial ratios and the concept of financial leverage.

Liquidity Ratios

The second set of financial ratios used to analyze a business is liquidity ratios. These

ratios analyze a company from a short-term perspective and focus on the company’s ability to

meet its current obligations. As mentioned in the previous chapter, liquidity refers to the ease

and quickness by which assets can be converted into cash; therefore, the ultimate goal of

liquidity ratios are the determination of how quickly the company can convert its assets into

tangible cash. The nine liquidity ratios that are to be presented are:

- Working capital

- Current ratio

- Acid-test ratio (Quick ratio)

- Accounts receivable turnover ratio

- Days of accounts receivables

- Accounts payable turnover ratio / Days of accounts payables

- Inventory turnover ratio / Days of inventory

Working Capital

Prior to calculating ratios, it is important to understand the concept of working capital,

which is essentially the difference between current assets and current liabilities.

10

Net Working Capital = Current Assets – Current Liabilities

NWC = CA – CL

Referring back to previous definitions, current assets are assets which can be easily convertible

into cash, while current liabilities are short-term financial obligations. Therefore, working capital

is the excess of short-term assets that are available for use and are not tied up by current

liabilities. A company always wants working capital so that its short-term obligations are being

met; if short-term obligations are not met the company faces a solvency problem.

For Southwest Airlines in 2007, its amount of working capital was -$395 million

3

. This could be

rather alarming since it might indicate that the airline did not have the necessary amount of

current assets to meet their short-term obligations. However, the company can still operate if

they are able to defer their liabilities to a later period or increase their current assets.

Current Ratio

One of the classic financial ratios, the current ratio measures the relationship between

current assets and current liabilities. The current ratio analyzes the working capital of the

company and helps determine if the company can meet its short-term obligations. However,

unlike the amount of working capital which will vary considerably based on the company’s size,

the current ratio provides standardization of working capital, enabling industry comparison. The

current ratio provides a proportion of how much of the company’s current liabilities are being

met by the company’s current assets (Ross, Westerfield and Jordan, 2008). The formula for the

current ratio is:

3

Working Capital (2006) = Current Assets – Current Liabilities = $4,443 million - $4,838 million = -$395 million

11

Current Assets

Current Ratio =

Current Liabilities

CA

CR

CL

Since it was previously determined that the amount of Southwest Airlines 2006 working

capital was negative, the current ratio will be less than one, since all the current liabilities are not

being met by current assets. In fact, the 2006 current ratio for Southwest Airlines is 0.90.

$4,443 million

Current Ratio (2006) = = 0.92

$4,838 million

A current ratio of 0.92 indicates that only 92% of Southwest Airlines’ current liabilities

will be satisfied with current assets, therefore the company will either attempt to defer their

liabilities, or acquire short-term financing through a variety of options, such as a business line of

credit. As a comparison, Southwest’s 2006 current ratio was 0.90

4

, indicating that Southwest was

in a similar predicament the previous year.

Acid-Test Ratio (Quick Ratio)

A similar metric to the current ratio is the quick ratio, except that the quick ratio is a

stricter measurement of the company’s ability to meet its short-term obligations. The reason for

this is the fact that not all current assets are used in the calculation. Current assets have a

considerable range in their liquidity since some short-term investments can be converted into

cash far more quickly than others, so these assets may be better indicators of the company’s

ability to meet its obligations. Therefore, in order to provide a more realistic view of assets that

4

Current Ratio (2006) = $2,601 million / $2,887 million = 0.90

12

can be converted into cash to meet short-term obligations; the acid-test ratio uses quick assets.

While the classification of quick assets is ultimately at the discretion of the analyst, common

current assets used as quick assets are cash and cash equivalents, marketable securities, and

current accounts receivable. Regardless of the classification of quick assets, inventory is almost

always removed from the acid-test ratio, as inventories are more likely to be slow moving,

indicating that the inventory is less liquid. Using a methodology where quick assets are simply

cash, short-term investments, and accounts receivable, Southwest Airlines 2007 quick ratio was:

Quick Assets

Quick Ratio =

Current Liabilities

($2,213 + $566 + $279) million

Quick Ratio (2007) = = 0.63

$4,838 million

QA

QR

CL

Where; Quick Assets = Cash and cash equivalents + Short-term investments + Current accounts

receivables

A quick ratio of 0.63 indicates that only 63% of Southwest’s current liabilities can be

quickly satisfied. Since the acid-test ratio is stricter than the current ratio, the quick ratio is

always going to be less than the current ratio. Ultimately, the quick ratio provides a stronger

analysis of a company’s working capital since it removes some uncertainty over the composition

of a company’s current assets. How much liquidity an airline needs depends on its operating

cycle. An airline’s operating cycle is the time between the cash is spent for goods and services to

the time that investment generates cash.

Accounts Receivables Turnover Ratio

Companies offer goods and services on credit to attract and maintain customers, since we

already know that a dollar today is more expensive than a dollar tomorrow. Since most

companies offer credit terms, it is important to monitor accounts receivables to make sure that

payment is collected in a timely matter. It may be better for a company to offer long credit terms;

13

however, if it takes the company a long time to collect accounts receivables, the company has

been unable to use that money over the time period.

Therefore, the accounts receivable turnover ratio is a measure of how many times

accounts receivable are collected during a specified time period. When calculating the accounts

receivable turnover ratio, net credit sales is usually used, since only the portion of revenue that is

collected on credit should be analyzed. However, since few companies report revenue between

cash and credit sales on their publicly available financial reports

5

, total revenue usually has to be

used. This can lead to distortion in calculating the accounts receivable turnover ratio.

Additionally, distortions can arise when using the accounts receivable balance at a point in time,

since the balance could have varied significantly during the time period. However, since the

average accounts receivable balance is only known internally, external analysis has to use the

stated value on the balance sheet, and note the possible potential of distortions. Because the

accounts receivable turnover ratio determines how quickly accounts receivables are turning over;

higher values indicate that accounts receivables are moving more quickly than lower values.

Southwest Airlines 2007 accounts receivable turnover ratio is:

Net Credit Sales

Accounts Receivable Turnover Ratio =

Average Accounts Receivables

$9,861 million

Accounts Receivable Turnover Ratio (2007) = = 37.93

$260 million

6

,

7

Days of Accounts Receivables

One of the problems with the accounts receivable turnover ratio is that the metric can be

difficult to interpret. Therefore, an associated ratio is the days of accounts receivable, which

5

The notes to the financial statements sometimes contain detail on the amount of revenue generated on credit.

6

Since net credit sales were unknown for Southwest Airlines, total operating revenue from the income statement is

used instead.

7

The average accounts receivable balance for Southwest Airlines was the average of accounts receivable balance at

December 31, 2006 and December 31, 2007.

14

converts the accounts receivable turnover ratio into the average time for accounts receivables

during the period. In 2006, the days of accounts receivables for Southwest Airlines were:

Number of Days in Period

Days of Accounts Receivables =

Accounts Receivable Turnover Ratio

365

Days of Accounts Receivables (2006) = = 9.62 days

37.93

8

,

9

A value for days of accounts receivables of 9.62 indicates that, on average, revenue

generated by Southwest Airlines is collected in approximately nine and a half days. For many

companies this is an extremely quick collection period; however, since the majority of airlines

collect revenue on a fairly immediate basis

10

, the industry is expected to have short days of

accounts receivables. For 2006, Southwest’s days of accounts receivables was 9.68 days, which

means that days of accounts receivables did not change significantly from 2006 to 2007.

Accounts Payable Turnover Ratio / Days of Accounts Payable

Nearly identical in methodology to the accounts receivable turnover ratio is the accounts

payable turnover ratio, which measures the number of times the accounts payable account turns

over. While analyzing accounts payable is not as important, since the goal is to pay as late as

possible, it is useful to compare the days of accounts payable with the days of accounts

receivable, to help estimate the days of working capital. The formula for the accounts payable

turnover ratio and days of accounts payable are:

8

Since net credit sales were unknown for Southwest Airlines, total operating revenue from the income statement is

used instead.

9

The average accounts receivable balance for Southwest Airlines was the average of accounts receivable balance at

December 31, 2006 and December 31, 2007.

10

For example, the majority of passenger travel is booked through the Internet, which collects credit card payment

seemingly immediately. However, a lag does occur between when the credit card company dispatches the revenue

collected for the flight to the airline, providing a short days of accounts receivable for credit card generated revenue.

15

Period Purchases

Accounts Payable Turnover Ratio =

Average Accounts Payable

Number of Days in Period

Days of Accounts Payable =

Accounts Payable Turnover Ratio

When referring to Southwest Airlines income statement, it is difficult to determine the

purchases made by the company during the period; therefore, total operating expenses, less

depreciation, which is a non-cash item, is used as a proxy for annual purchases. Using this

methodology, the accounts payable turnover ratio and days of accounts payable for Southwest

Airlines in 2007 was:

($9,070 - $555) million

Accounts Payable Turnover Ratio (2007) = = 12.15

$759+$643

( ) million

2

365

Days of Accounts Payable (2006) = = 30.04 days

12.15

Based on Southwest Airlines 2007 days of accounts payable, it appears the airline

operates on a policy of paying their account within thirty days. Of note is the 20.42 day

difference between the days of accounts receivable and accounts payable, indicating that the

airline, on average, is able to use the revenue generated for nearly an additional 21 days prior to

paying for the cost of flying the passenger. The days of working capital is increased by the fact

that the majority of passengers book their travel significantly ahead of the departure date, further

strengthening the airline’s cash flow and providing the airline the opportunity to use the cash

during that time period. Ideally, a company wants to maximize the difference between the days

of accounts payable and accounts receivable to provide the company with short-term investment

opportunities.

16

Inventory Turnover Ratio / Days of Inventory

The final area of liquidity to analyze is inventory. This is extremely important for

manufacturing firms, but is less important in the airline industry, since a passenger seat is not

inventoried. However, airline maintenance does contain inventoried parts to support the

operation. Since there is a cost associated with warehousing inventory, it is important to make

sure inventory is turning over quickly and not sitting idle in warehouses. On the other hand, the

airlines want to make sure flights are not cancelled or delayed as a result of a lack of inventory

and this creates conflicting goals. The generic inventory turnover ratio and days of inventory

calculations are:

Cost of Goods Sold

Inventory Turnover Ratio =

Average Inventory

Number of Days in Period

Days of Inventory =

Inventory Turnover Ratio

Since Southwest Airlines, or any airline, has a true cost of goods sold, the inventory

turnover ratio uses the expense categories for which the inventory is required. Making the

assumption that all inventory held by the airline are maintenance materials, the maintenance

materials and repairs category can be used as a proxy for the cost of goods sold when calculating

the inventory turnover ratio for airlines. Using this methodology, the inventory turnover ratio

and days of inventory for Southwest Airlines in 2007 was:

17

$616 million

Inventory Turnover Ratio (2007) = = 2.38

$259 million

365

Days of Inventory = = 153.36 days

2.38

For many industries, 153 days of inventory sitting idle would be unacceptable; however,

in the airline industry this length of time is fairly common. This is largely a result of numerous

parts that are required to support the operation and the fact that the usage of the parts is not very

high. Additionally, since airlines operate globally, parts must be stocked in multiple cities to

insure an on-time operation. This problem is compounded for Southwest Airlines which does not

operate hubs and has sizeable operations at multiple airports. This type of operation likely

requires increased inventory because of the numerous airports where maintenance problems

might occur. Like most of the ratios, the days of inventory needs to be compared solely within

the industry to determine how efficient the airline is operating.

Long Term Risk Ratios

While liquidity ratios help analyze a company’s financial position in the short-term, long-

term risk ratios, or solvency ratios, analyze a company’s ability to remain in business over the

long-term. Of all the categories of ratios, long-term risk ratios tend to provide the greatest

macro-perspective of a company. Because of this, the ratios focus on the underlying capital

structure of the company, which ultimately helps determine the company’s financial strength for

the future. The three major long-term risk ratios are:

o Debt-to-equity ratio

o Debt ratio

o Times interest earned ratio

18

Debt-to-equity ratio

The classic long-term risk ratio, the debt-to-equity ratio, determines the proportion of the

company’s capital structure that is composed of equity. It helps determine where the funding for

the company exists, and how heavily weighted the company is to either debt financing or equity

financing. The debt-to-equity structure of a company can also indicate the variability of future

earnings, as more heavily debt financed companies will incur larger swings in profitability as a

result of increased interest expenses. Additionally, the resultant financial structure of a company

helps determine the cost of capital, an important metric used in financial decision-making. While

numerous derivations of the debt-to-equity ratio exist, the generic formula is:

Total Liabilities

Debt-to-Equity Ratio (D/E) =

Total Stockholders' Equity

Using the generic debt-to-equity ratio and the data from Southwest Airlines balance

sheet, its 2007 debt-to equity ratio was 1.42.

11

This means that for every $1 of stockholders’

equity, Southwest Airlines has been able to leverage $1.42 of debt finance. This ratio also

indicates that Southwest Airlines is slightly more debt financed than equity funded, as evidenced

by a debt-to-equity ratio greater than one. Like so many other ratios, every industry and

company are unique, therefore there is no universal optimal debt-to-equity ratio. Comparisons

with similar companies competing in the same or similar industries help determine the potential

for variability of future earnings.

Debt Ratio

A common derivation of the debt-to-equity ratio is the debt ratio, which simply measures

the proportion of debt that is financing the assets of the company. Since either liabilities/debt or

stockholders’ equity is used to finance assets, the debt ratio ultimately provides the percentage of

debt in the capital structure. The debt ratio’s formula and Southwest Airlines 2007 debt ratio is:

13

Debt-to-Equity Ratio (2007) = $9,831 million / $6,941 million = 1.42

19

Total Liabilities

Debt Ratio =

Total Assets

$9,831 million

Debt Ratio (2007) = = 0.59 or 58.62%

$16,772 million

Since both sides of the balance sheet must be equal, the debt ratio is merely comparing

the proportion of liabilities held by the company against stockholders’ equity - essentially the

debt-to-equity ratio. Southwest Airlines debt ratio of 58.62% indicates that a little over half of

the company’s assets were funded by debt. As a comparison, Southwest Airlines 2006 debt ratio

was 52.08%;

12

the debt ratio increased slightly for Southwest Airlines in 2007. The comparison

of debt ratios over time is an effective tool in helping understand the company’s past and how it

is positioning itself for the future. Based on a stable debt ratio, the airline appears satisfied with

its mix of debt and equity in its capital portfolio, indicating a rather stable financial environment

for the company. If a company were to make radical changes in its capital structure, such as

dramatically increasing its proportion of equity, some financial implications could be drawn.

These might include the fact that the cost of debt for the company may be prohibitively high

(likely the result of poor bond ratings), or the company may be wishing to raise capital without

having any set payment schedules. Therefore, changes in capital structure, help to determine the

company’s ability to stay in business for the long-term.

Times Interest Earned Ratio

The times interest earned ratio measures the company’s ability to meet its interest

payments. To debt holders, the times interest earned ratio is critical in determining the amount of

risk the company presents to them. While calculated multiple ways, a simple method in

calculating the times interest earned ratio is:

12

Debt Ratio (2006) = Total Liabilities / Total Assets = $7,011 million / $13,460 million = 52.08%

20

Earnings Before Interest and Taxes (EBIT)

Times Interest Earned Ratio =

Interest Expense

Using information from the income statement, the times interest earned ratio for

Southwest Airlines was 6.64 in 2007.

13

This value indicates that in 2006, Southwest Airlines

operating income was nearly seven times the annual interest expense, showing that they were in

a fairly good position to be able to meet their interest payments. Therefore, the higher the times

interest earned ratio, the better able the company is to meet their interest requirements. Having a

higher times interest earned ratio ultimately helps lower the cost of debt as the company appears

more stable to creditors. For comparison purposes, the times interest earned ratio in 2006 and

2005 was 7.30 and 5.94 respectively for Southwest Airlines.

14

Based on these values, Southwest

Airlines has moved itself into a better position to meet their interest payments since 2005,

displaying a strengthening financial position over the three years.

Stock Market Ratios

The final set of ratios that can be used to analyze a company are stock market ratios;

these ratios analyze a company in relationship to its equity position. Because stock market ratios

analyze a company’s position in the stock market, the ratios can only be used for public

companies. The ratios provide good information when an individual is considering investing in a

company, and are used extensively by the investment banking community in determining a

company’s value. Since ultimately a company’s stock price is the result of analysis and

projections by investors, stock market ratios are important in determining the fiscal health of a

company. Since the goal of investing is to purchase low and have the company perform well in

the future, stock market ratios help analyze the current value of a company. Listed below are

13

Times interest earned ratio (2007) = $791 million / $119 million = 6.64

14

Times interest earned ratio (2006) = $934 million / $128 million = 7.30

Times interest earned ratio (2005) = $725 million / $122 million = 5.94

21

four common stock market ratios that are commonly used when assessing a company’s position

in the stock market:

o Earnings per share

o Price-earnings ratio

o Dividend payout ratio

o Dividend yield ratio

Earnings per share

Since earnings per share were covered in the previous chapter, extensive explanation of

the ratio is not required. As a refresher, earnings per share essentially state the net income of the

company on a per share basis, reflecting the amount of income earned for every outstanding

share of the company in the market. The simple formula for earnings per share is:

Net Income

Earnings per Share (EPS) =

Average Number of Shares Outstanding

Earnings per share helps standardize a company’s earnings based on their amount of

equity. In financial circles, net income is always stated on an earnings per share basis, as it

ultimately reflects the net income earned for every individual shareholder. Most publicly

available income statements provide earnings per share and Southwest Airlines EPS for the

period ending December 31, 2007 was $0.85 (Southwest Airlines, 2008, February 1).

Price-earnings ratio

The price-earnings ratio is the ultimate assessment of a company’s stock market value as

it compares the relationship between the performance of the company according to the income

statement and the stock market. Based upon the comparison of earnings and the stock price, the

price-earnings ratio helps enable one to determine if the stock price of a company is either

undervalued or overvalued. The P/E ratio is a measure every investor should be aware of to help

find good stock market values. The price-earnings ratio is calculated using the following

formula:

22

Current Market Price

Price-Earnings Ratio =

Earnings per Share

S

P

EPS

Since the price-earnings ratio is calculated using the current stock market price of the

company, the price-earnings ratio will be in constant flux based on the daily stock price. Based

on Southwest Airlines earnings per share of $0.85, and its stock price of $12.20 on December

31, 2007, the price-earnings ratio of Southwest on December 31, 2007 was:

$12.20

Price-Earnings Ratio (2006) = = 14.35

$0.85

A price-earnings ratio of 14.35 indicates that the stock price is 14.35 times greater than

the earnings of the company. Like many other financial ratios, there is no target value for what

the price-earnings ratio should be. The optimum price-earnings ratio is based on not only the

industry the firm competes in, but also the overall stock market. A high price-earnings ratio may

indicate that the stock price of the company is overvalued while the stock is likely undervalued

for low price-earnings ratios. However, determining if a price-earnings ratio is high or low is

ultimately a decision that the individual investor has to make, with the metric merely providing

the investor with a methodology of helping assess the value of a company’s stock.

The price-earnings ratio computed for Southwest Airlines on December 31, 2007 was

backward looking since it used the historical financial performance of the company. The price-

earnings ratio can also be forward looking by using projected earnings per share based upon a

projection of future earnings. Forward looking P/E ratios help signal if the current stock price is

either under- or overvalued for the company’s future prospects. Obviously, this methodology is

only as good as the accuracy in determining earnings per share for a company for a future

period, and these estimates can be influenced by a variety of factors.

Dividend payout ratio

23

An investor can earn a return on investment through two means: capital gains associated

with selling a stock at a higher price than the price at which it was purchased and through the

receipt of dividends issued by the company. The specific dividend policy of a company is

usually complex, incorporating a host of factors; however at a more general level, companies

issue dividends (either cash payments or additional stock issues) in an effort to attract equity.

Ultimately, the amount of dividends issued is reflected in the share price, with the assumption

being that all information is disseminated.

The dividend payout ratio measures the percentage of earnings paid out as dividends. It

reflects the level of dividends that the company is distributing. A company with a high dividend

payout ratio is attempting to signal that it is well off financially or that the company does not

have the need to re-invest the earnings for other activities. Conversely, a low dividend payout

ratio signals that a company is strapped for cash or wishes to re-invest the earnings in an attempt

to realize even greater earnings in future periods. The dividend payout ratio is calculated with

the formula:

Dividends Distributed per Share

Dividend Payout Ratio =

Earnings per Share

Using Southwest Airlines $0.85 earnings per share in 2007 and cash dividends of $0.018

per share issued during the year, the dividend payout ratio for Southwest Airlines would be:

$0.018

Dividend Payout Ratio (2006) = = 0.0212 or 2.12%

$0.85

A dividend payout ratio of 2.12% shows that Southwest Airlines decided to distribute

2.12% of its earnings during the period back to its shareholders. Once again, there is no optimum

dividend payout ratio, and equally successful companies can have wildly divergent dividend

24

payout ratios; however, the ratio does enable an investor to understand the dividend policy of the

company, and this helps an investor determine an expected value for the stock.

25

Dividend yield ratio

The dividend yield ratio measures the relationship between dividends distributed and the

market price of the company. The dividend yield ratio provides a similar level of analysis as the

dividend payout ratio and is important to investors, particularly shareholders’ dependent on

dividends as a return on their investment. The dividend yield ratio is calculated using the

following formula:

Dividends Distributed per Share

Dividend Yield Ratio =

Current Market Price

Using the cash dividend of $0.018 per share being distributed during 2007 and a market

price for Southwest Airlines stock at $12.20, the dividend yield ratio is 0.15%.

15

This indicates

that less than 1% of Southwest Airlines stock price has dividends that are being distributed, and

this in turn means that the stock has a low yield in terms of dividends. Since there are other ways

a stock can yield a return on investment (for example, capital gains), this ratio alone should not

distract investors; however, investors seeking dividends should probably focus their attention

elsewhere. By and large, the airline industry has very low dividend yield and payout ratios. This

is due in part to the volatility of the industry and the need to invest in extensive capital projects.

However, a few sectors, such as utility companies, are renowned for strong dividend yields,

representing a relatively safe investment opportunity for risk-adverse investors who wish to earn

returns from dividends. Further discussion of dividend policy is contained later in the text.

Financial Ratios: Airline Specific Ratios

Since every industry is unique, certain specific ratios are developed that help provide a

greater depth of analysis and understanding of the industry. The airline industry ratios are

centered on two major measures of an airline’s output: available seat miles (ASM) and revenue

15

Dividend Yield Ratio (2007) = $0.018 / $12.20 = 0.15%

26

passenger miles (RPM). These two measures, combined with various items on the income

statement and balance sheet, provide a substantial amount of airline-specific financial ratios.

Available seat miles is a measure of an airline’s output, since it represents the number of

miles that the airline has flown with its available seats, regardless of whether the seat is filled by

a passenger. To illustrate, a 200 seat aircraft flying a 1,000 mile flight would represent 20,000

ASM.

16

Available seat miles provides some standardization to an airline’s output; however,

ASM does not provide a complete standardization since airline’s can have the same amount of

ASM, but operate completely differently. For example, a short-haul airline with multiple

frequent flights could end up with a similar amount of ASM as a long-haul international airline

with less frequent flights, yet the two airlines have completely different operating structures. By

altering aircraft frequency of flight and flight distance, airlines can adjust their output either

upward or downward.

Revenue passenger miles represent the number of miles that revenue passengers fly on

the airline. Whereas ASM does not differentiate between whether the seat is occupied or not,

RPM are only calculated seats occupied by passengers. To further illustrate, the revenue

passenger miles for the 200 seat aircraft flying the 1,000 mile flight with 140 revenue passengers

would by 14,000 RPM.

17

As a result, RPM provides standardization for revenue while also

allowing for easy calculation of an airline’s load factor. Load factor is simply the proportion of

an airline’s seats that are filled by revenue passengers, and can be calculated by dividing RPM

by ASM.

RPM

Load Factor =

ASM

As an example, consider Southwest Airlines 2007 operating statistics:

16

ASMs = Number of Seats per Aircraft * Flight Distance = 200 seats * 1,000 miles = 20,000 ASM

17

RPMs = Number of Revenue Passengers * Flight Distance = 140pax * 1,000 miles = 14,000 RPM

27

Table 4.1

Southwest Airlines 2007 Operating Statistics

Available seat miles (millions)

99,636

Revenue passenger miles (millions)

72,319

Average load factor

72.58%

Source: Compiled by the authors from Southwest Airlines 2007 annual report

In the above example, Southwest Airlines 2007 load factor was 72.58%. While load

factor provides an understanding of the airline’s operation, it is not useful in determining the

profitability of an airline since it omits the two critical factors in determining profitability:

revenue and cost. Load factor merely highlights if seats are full, but high load factors alone do

not indicate profitability. For example, an airline could achieve a 100% load factor if it sold

every seat for one dollar; however, the flight would not be profitable as the costs would far

exceed the revenue. Two important airline-specific metrics that standardize revenue and costs

are respectively RASM (Revenue per Available Seat Mile) and CASM (Cost per Available Seat

Mile),

RASM (Revenue per Available Seat Mile) standardizes revenue by calculating the

amount of revenue that an airline receives for one available seat mile. It is calculated by taking

the total passenger revenue generated and dividing by total ASM. For Southwest Airlines, its

RASM is calculated below and was 9.49 cents for 2007.

Total Passenger Revenue

RASM =

Total ASM

$9,457 million

RASM (2006) = = 9.49 cents

99,636 million

28

This implies that for every seat mile that Southwest Airlines flies, it generates 9.49 cents of

revenue for that seat. Therefore, this ratio provides standardization for all airlines since their

revenue generation is based on their level of output.

A similar metric is CASM (Cost per Available Seat Mile), which standardizes the costs

of operating the airline, by providing the cost for one available seat mile. CASM is frequently

calculated using both total expenses and just operating expenses. Additionally, CASM for

individual line items can be calculated. For example, the maintenance, materials, and repairs

CASM can be calculated and this enables a comparison of airline’s maintenance operations with

other airlines. Regardless of which cost item is being compared, CASM simply provides the cost

on a seat mile basis.

Total Costs

CASM =

Total ASM

$9,216 million

CASM - Total (2006) = = 9.25 cents

99,636 million

$9,070 million

CASM - Operating (2006) = = 9.10 cents

99,636 million

For Southwest Airlines in 2007, its total CASM was 9.25 cents. This included all their operating

expenses, other expenses (such as interest and gains/losses), and income taxes. Since items such

as interest expenses and income taxes do not directly relate to the operation of the airline, and

ultimately the company’s output, a more accurate measure of an airline’s cost structure is its

operating CASM, which includes just operating expenses. For 2007, Southwest Airlines

operating CASM was 9.10 cents.

As described earlier, profit/net income is simply the resultant of total revenue less total

costs. Since both revenue and expenses are standardized by the same metric (ASM), profit can

29

also be stated in terms of available seat miles. Southwest Airlines total profit in 2007, stated in

terms of available seat miles was:

Total Profit per ASM = RASM – CASM

Total Profit per ASM (2006) = 9.49 cents – 9.25 cents = 0.24 cents

18

Southwest Airlines earned a profit of 0.24 cents for every seat mile that is flown. Therefore, a

137-seat aircraft flying a 500-mile route in 2007, earned Southwest Airlines, on average, a profit

of $164.40.

19

Obviously, if Southwest Airlines CASM was greater than their RASM, the

calculation would be the airline’s loss per ASM.

A common misconception made about RASM is that it equals the average fare paid by a

passenger for one mile. However, since RASM can be adjusted by either obtaining more revenue

from the same number of passengers or by increasing the total number of passengers, it does not

accurately reflect the revenue generated for just the paid seats. Thus, RASM reflects the revenue

generated for both paid and unpaid seats. Therefore, in order to determine the average amount of

revenue received for a paid seat, RRPM (Revenue per Revenue Passenger Mile) or yield is

calculated.

Total Passenger Revenue

RRPM =

Total RPM

$9,457 million

RRPM (2006) = = 13.08 cents

72,319 million

18

It should be noted that the calculation does not exactly represent Southwest Airlines total profit as RASM

excludes freight and other revenue. Freight revenue is rarely stated in terms of ASM, but instead have its own metric

stated in terms of ATM (Available Ton Miles). An ATM is simply one available freight ton transported for one

mile. As a result, RATM (Revenue per Available Ton Mile) and CATM (Cost per Available Ton Mile) can also be

calculated. These metrics are obviously more important for all-cargo airlines.

19

Total Profit = Aircraft Size * Stage Length * Profit per ASM = 137*500*$0.0024 = $164.40

30

In 2007, Southwest Airlines on average was able to generate 13.08 cents of revenue

from a paid passenger for one seat mile. Therefore, the average revenue received for a 500 mile

flight on Southwest Airlines in 2006 was just $65.40. It is important to note that the average fare

paid by the consumer was likely much higher as a result of taxes and fees. Yield is an important

airline metric since it ultimately measures the airline’s ability to maximize revenue. This is

accomplished through effective yield management and by providing a product that consumers

want and are willing to pay for.

As mentioned earlier, when calculating airline passenger load factor, the value is

generally irrelevant unless compared to the breakeven load factor. Breakeven load factor is

defined as the average percentage of an airline’s capacity that must be covered for the airline to

make zero profit. As a result, breakeven load factor takes into consideration the costs required to

provide the product. Based on breakeven load factor, any actual load factor greater than the

break even would provide a positive contribution, while any load factor less than breakeven

would represent a loss. The basic formula for breakeven load factor is:

CASM

B/E Load Factor =

RRPM

9.25 cents

B/E Load Factor (2006) = = 70.72%

13.08 cents

Based on calculations of Southwest Airlines’ actual load factor (72.58%) and breakeven load

factor (70.72%), the airline made a profit in 2007. Breakeven load factor can also be calculated

using direct operating CASM, with any actual load factor greater than breakeven representing a

positive contribution margin; however, it may not necessarily represent a profit since fixed

overhead costs would still need to be met. Therefore breakeven load factor is usually one of the

more important factors employed by an airline when assessing routes and flights on an

individual basis.

.

31

Airline Industry Benchmarking

As mentioned earlier, calculating various financial ratios is merely an academic exercise

unless they are compared to other firms competing in the same industry. Therefore, the

remainder of this chapter is devoted to using the financial ratios discussed above to benchmark

(compare) twelve US airlines to highlight their comparative effectiveness with respect to the

financial ratios. The twelve US airlines represent a mixture of low-cost and legacy carriers,

providing an interesting contrast between the business models for the respective categories.

Since it is mandatory that all US airlines provide financial and operating statistics to the

Department of Transportation (DOT), all the data are readily available from the Bureau of

Transportation Statistics (BTS), simplifying the process for performing industry benchmarking

20

.

Profitability Analysis

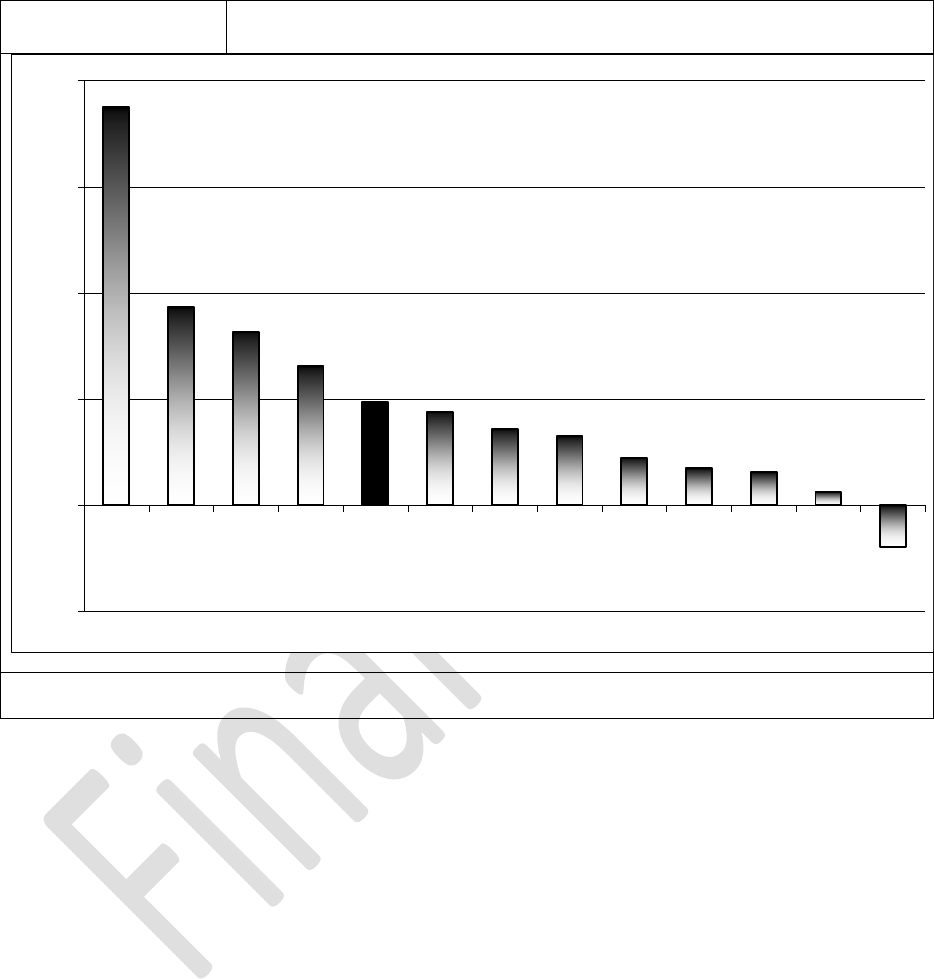

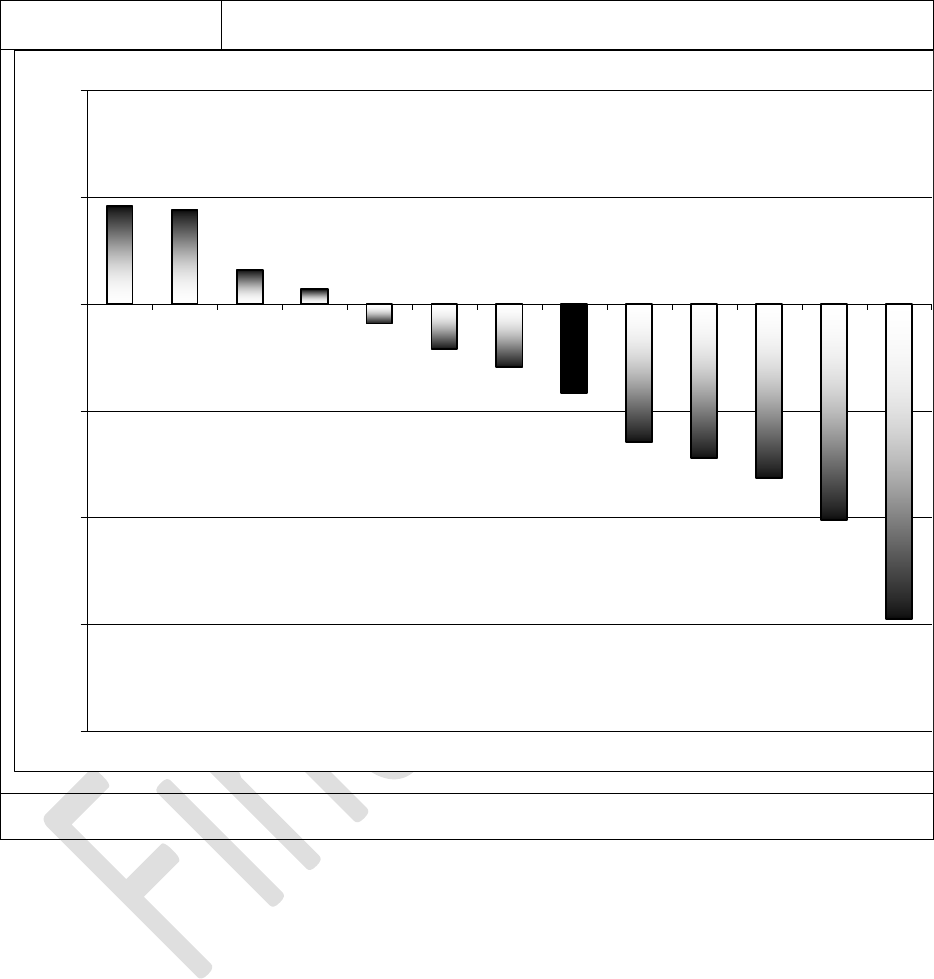

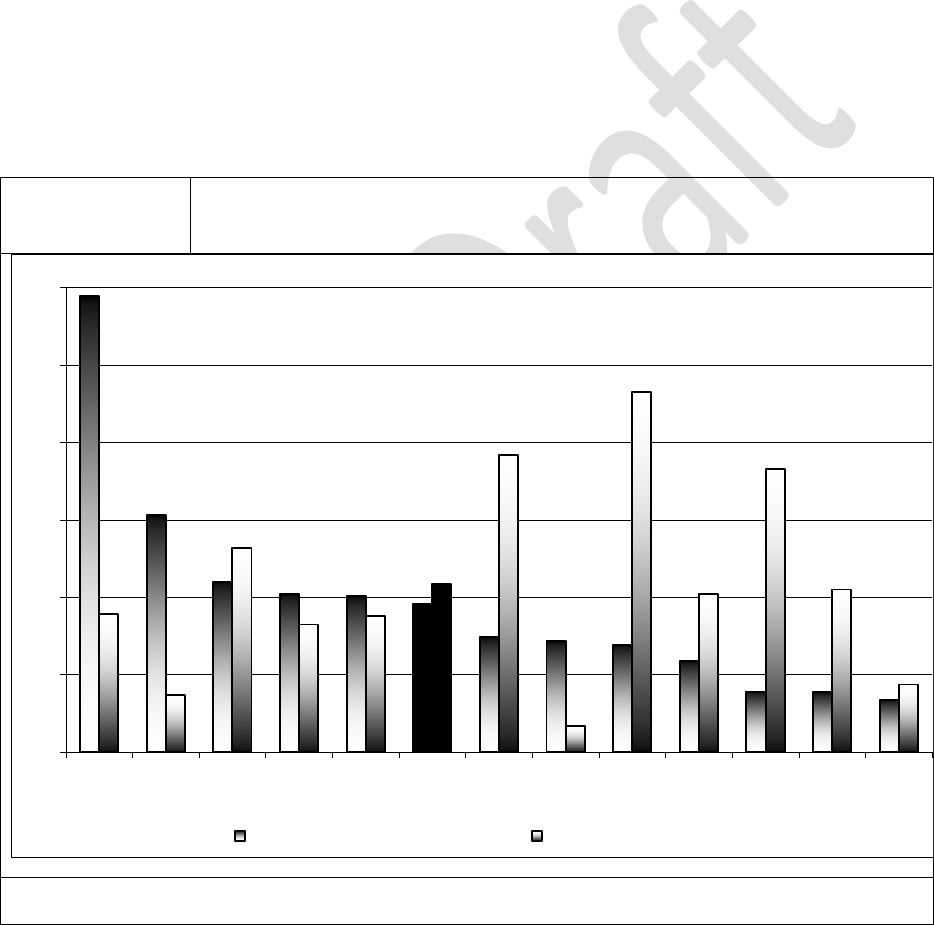

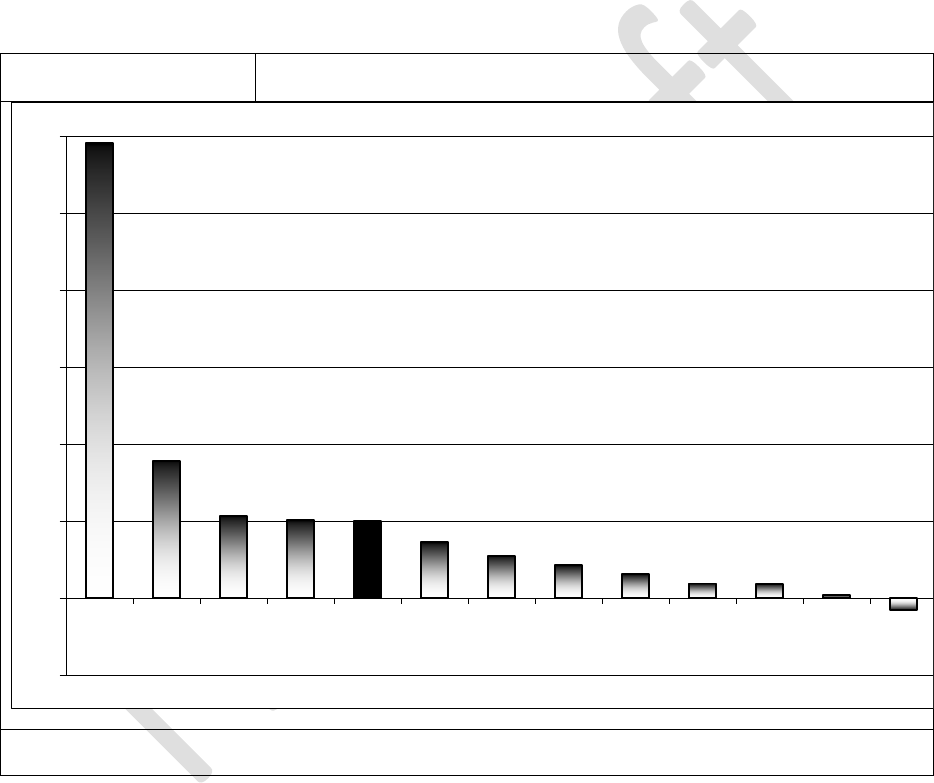

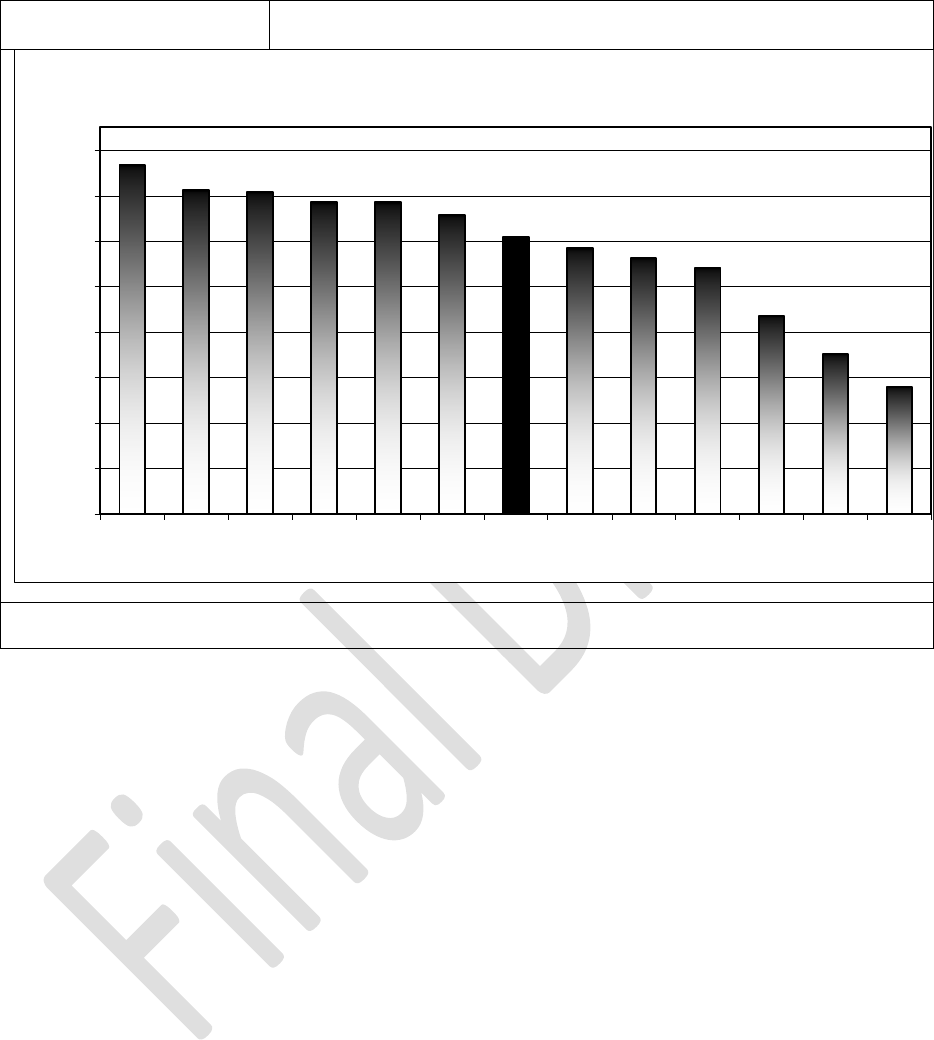

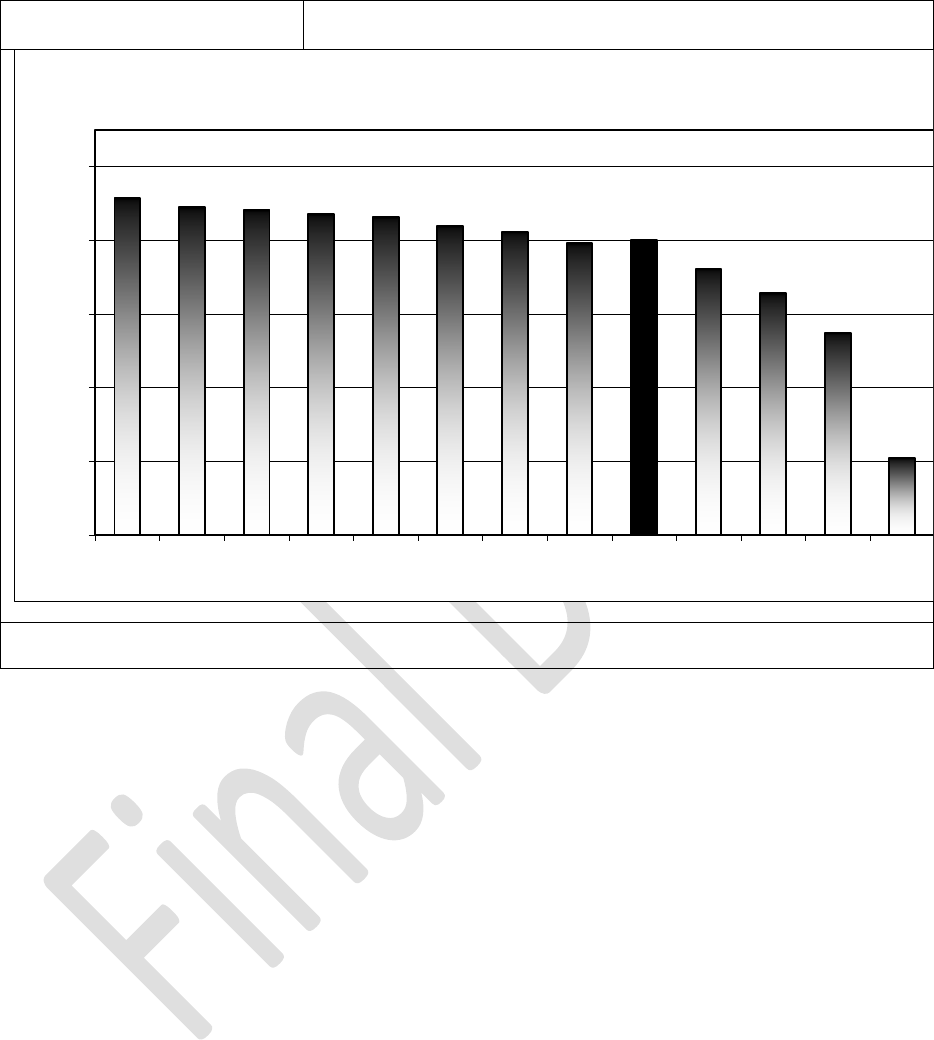

Figure 4.1 provides the profit margin for twelve United States airlines for 2007.

21

Profit

margin helps determine the carrier’s ability to turn revenue into profit. Based on the data for

2007, all US airlines were profitable except for Frontier Airlines (F9). Of all the carriers, it

appears that Northwest Airlines (NW) was the most successful; posting a profit margin that was

nearly double the next best carrier, Delta (DL). However, since data represent only one year,

they could be distorted due to special charges or one-time gains. Based on historical experience,

profit margins in excess of 10% are rare for the airline industry; therefore, it is likely that

Northwest’s statistics are distorted by some other factors.

20

It should be noted that the data obtained through the DOT and BTS is not perfect, as errors can exist in the data

and carriers do not always group into similar categories.

21

For a reference of the IATA two-letter carrier designation codes, refer to Appendix 1.

32

Figure 4.1

US Airlines’ 2007 Profit Margin

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

-5%

0%

5%

10%

15%

20%

NW DL G4 WN AV. AS US CO FL UA AA B6 F9

33

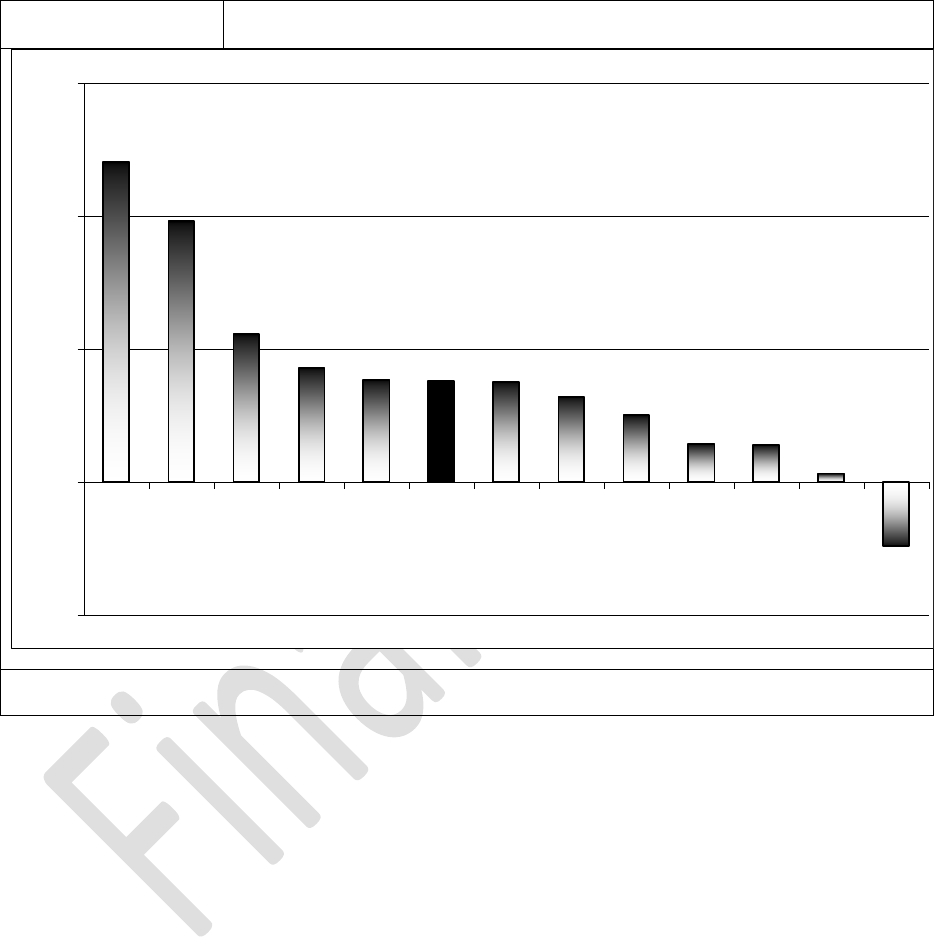

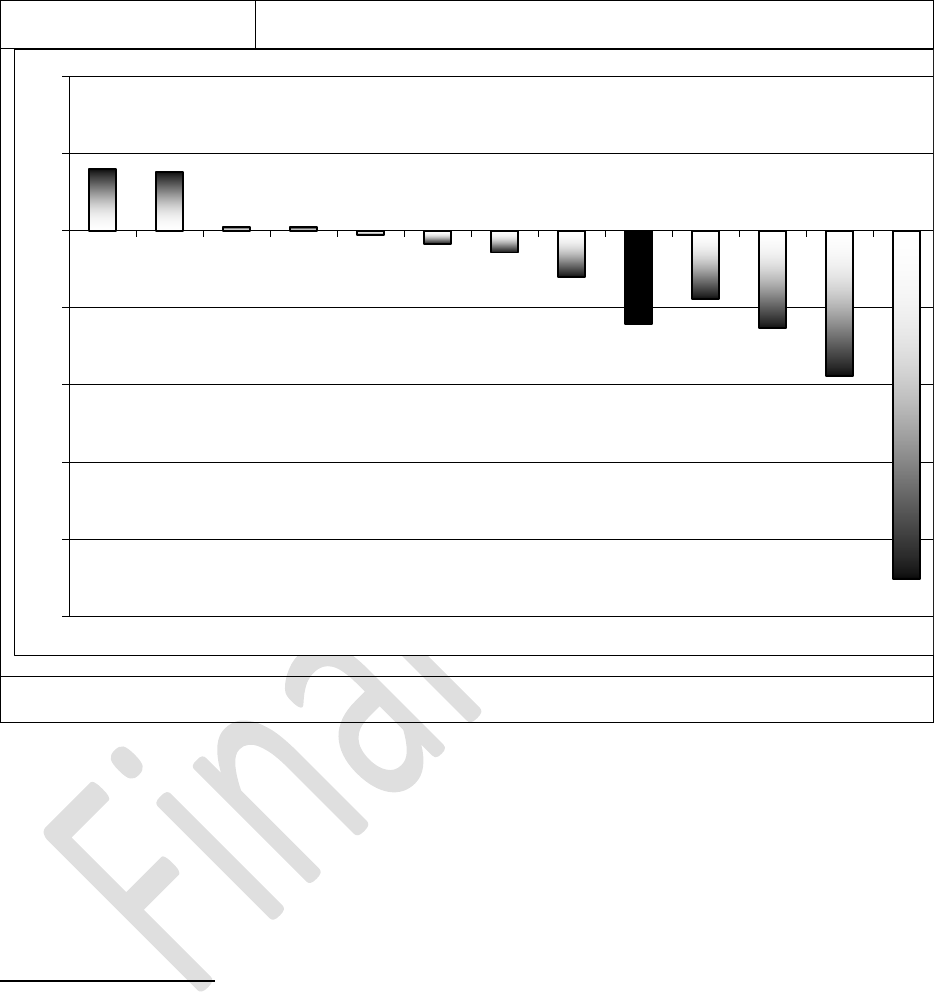

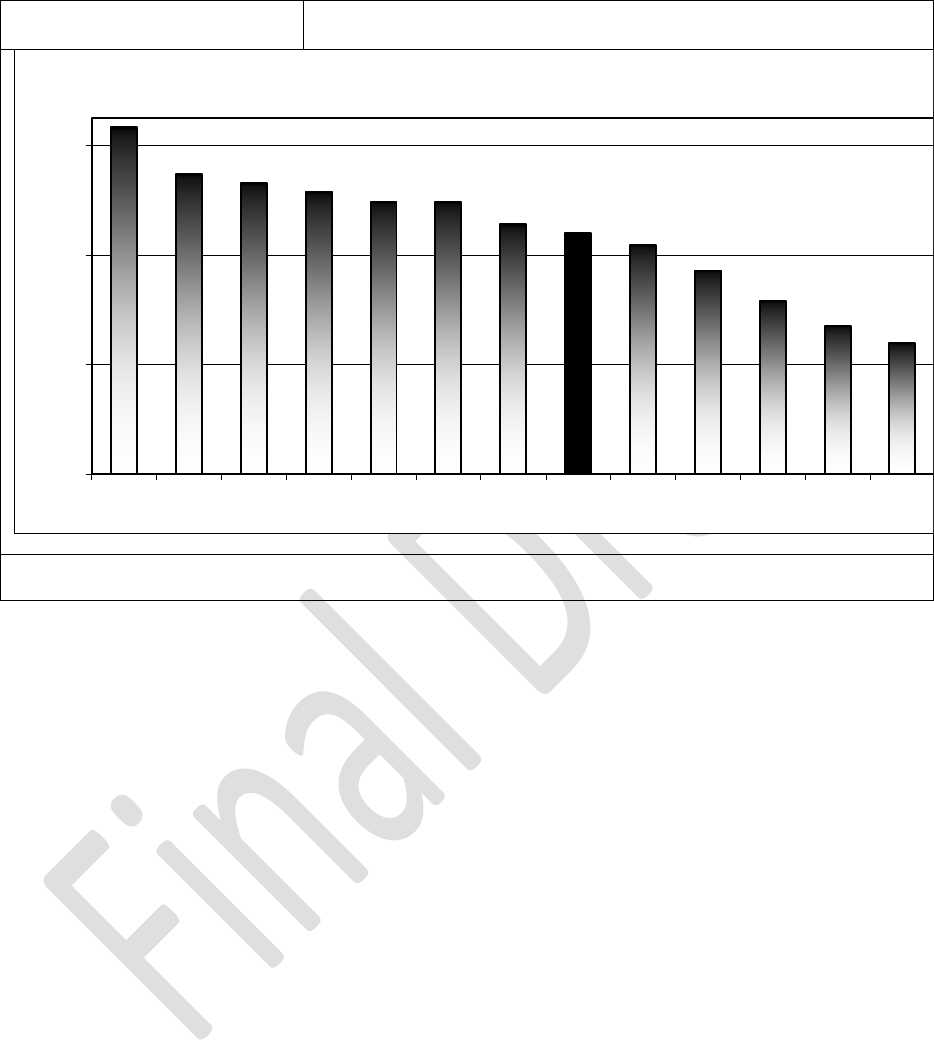

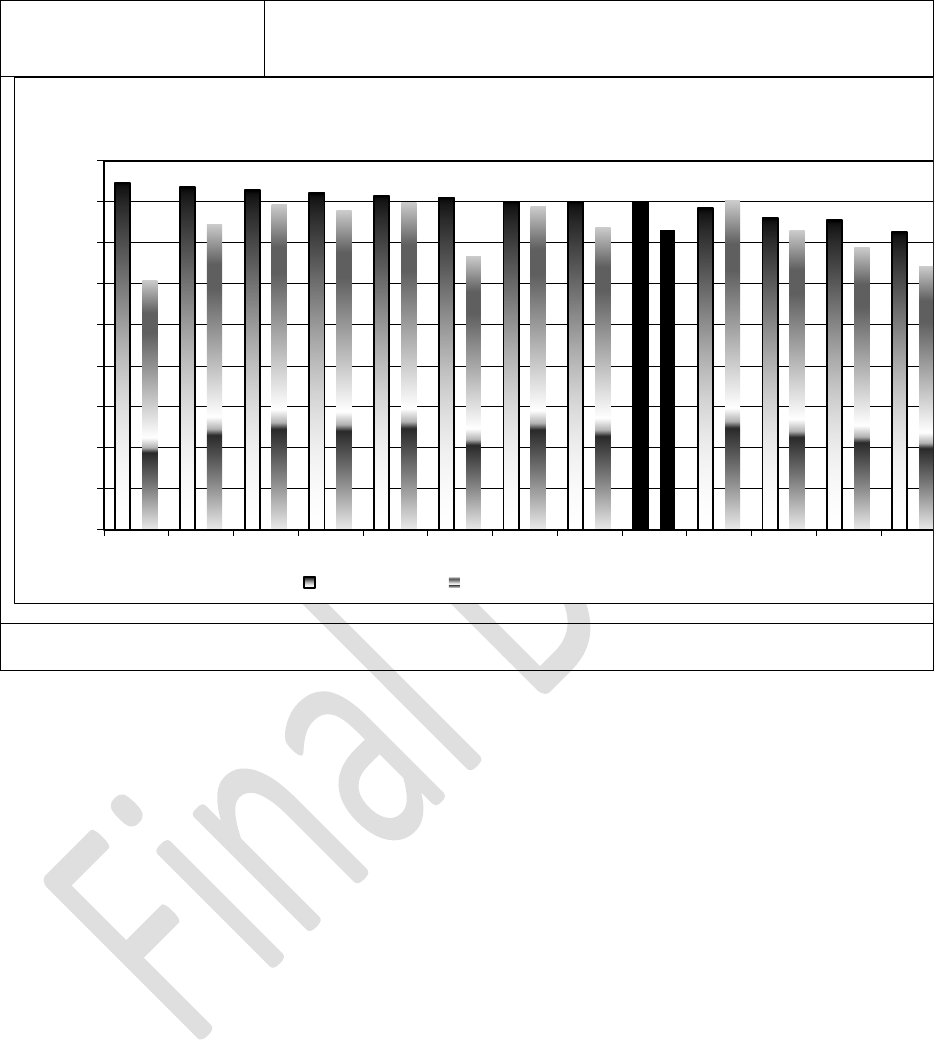

Figure 4.2

US Airlines’ 2008 Profit Margin

Source: Compiled by the authors using Back Aviation Form 41 data

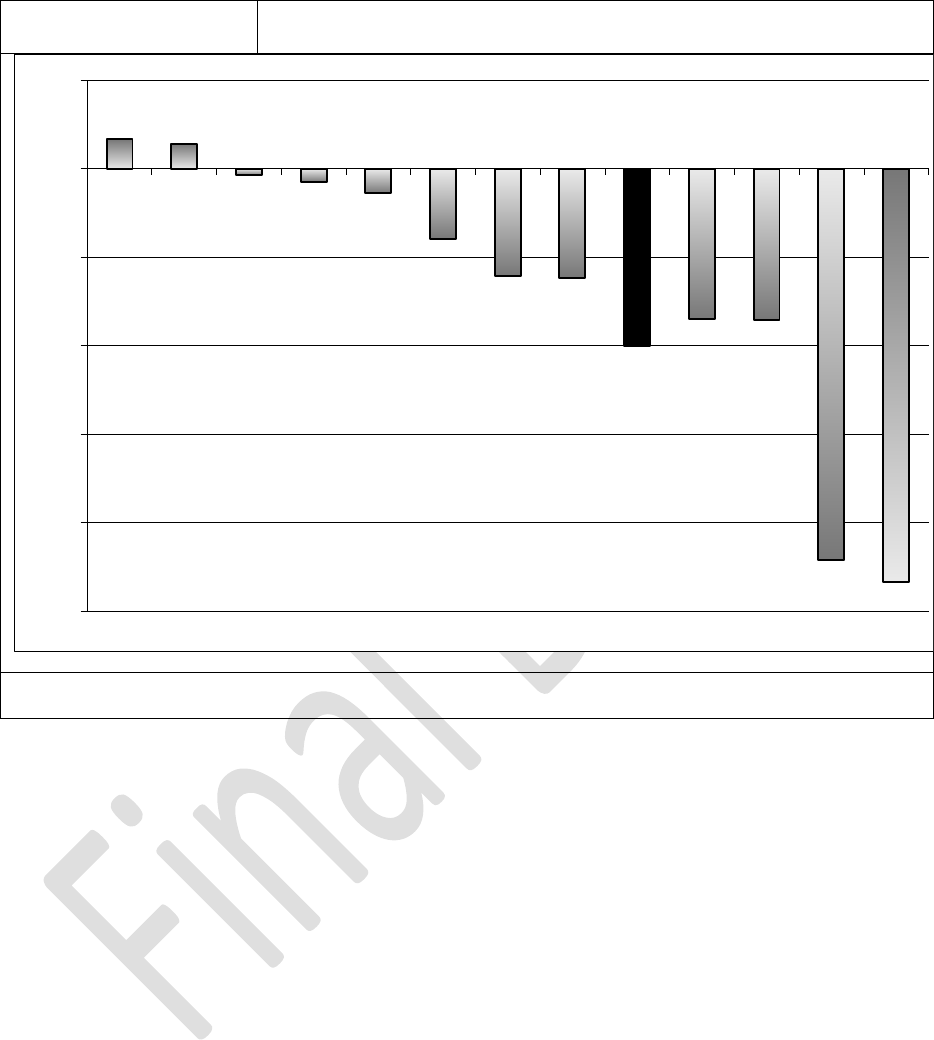

Figure 4.2 shows that while most major U.S. carriers were profitable in 2007; almost all

of the carriers were not in 2008. Only Allegiant Air (G4) and Southwest Airlines (WN) were

profitable in 2008, with the average profit margin being approximately -20%. The reasons for

the large negative profit margins include spiking fuel prices during the middle of 2008, reduced

demand at the end of 2008 and in the case of Northwest and Delta, one-time costs associated

with the merger.

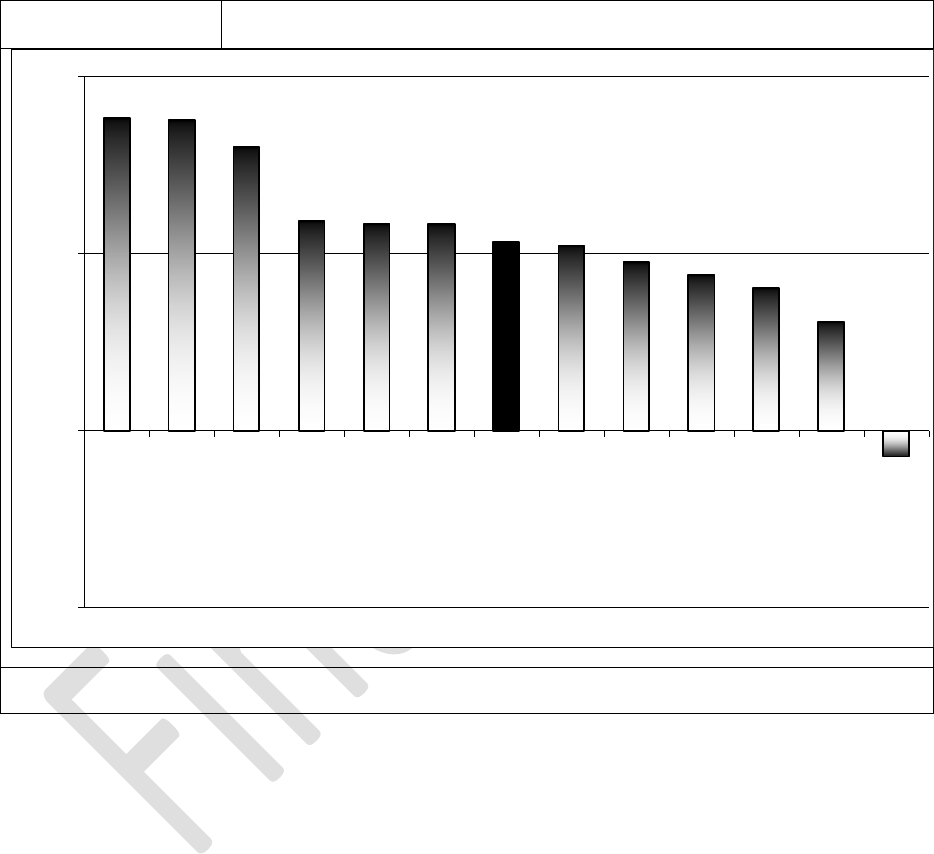

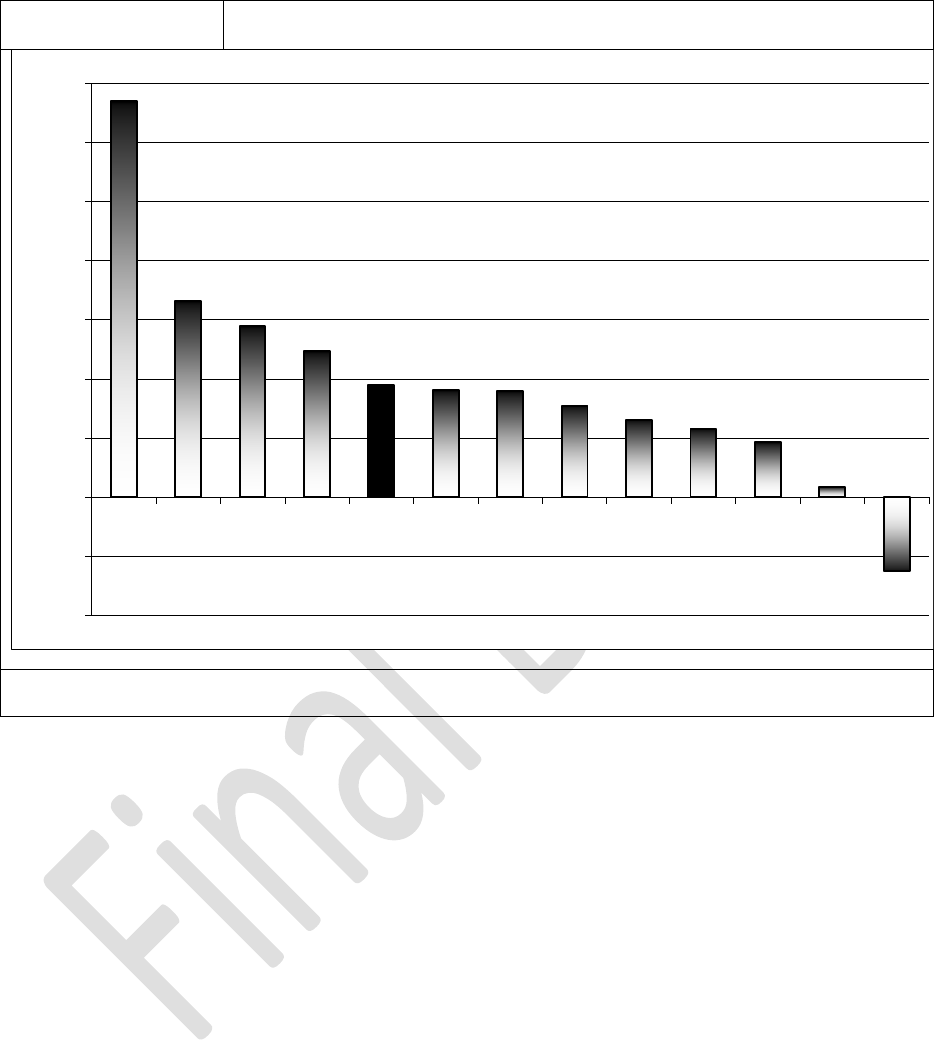

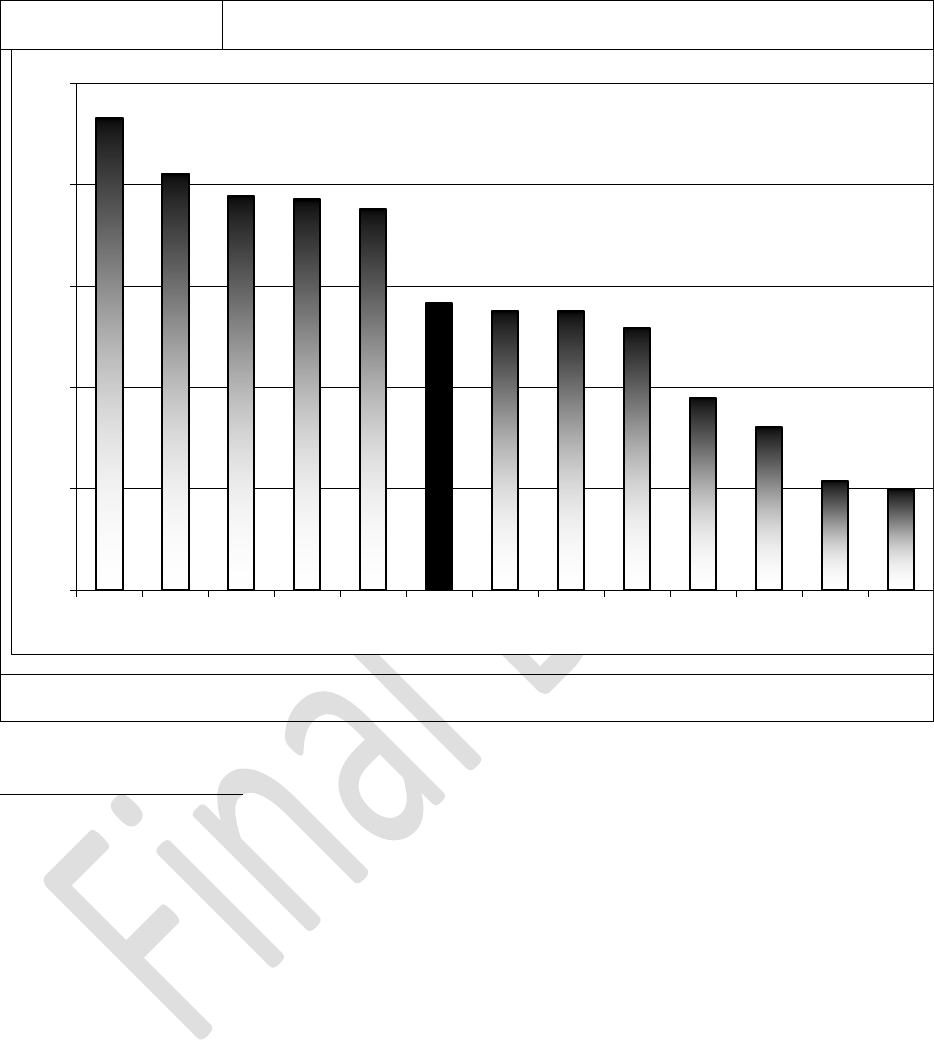

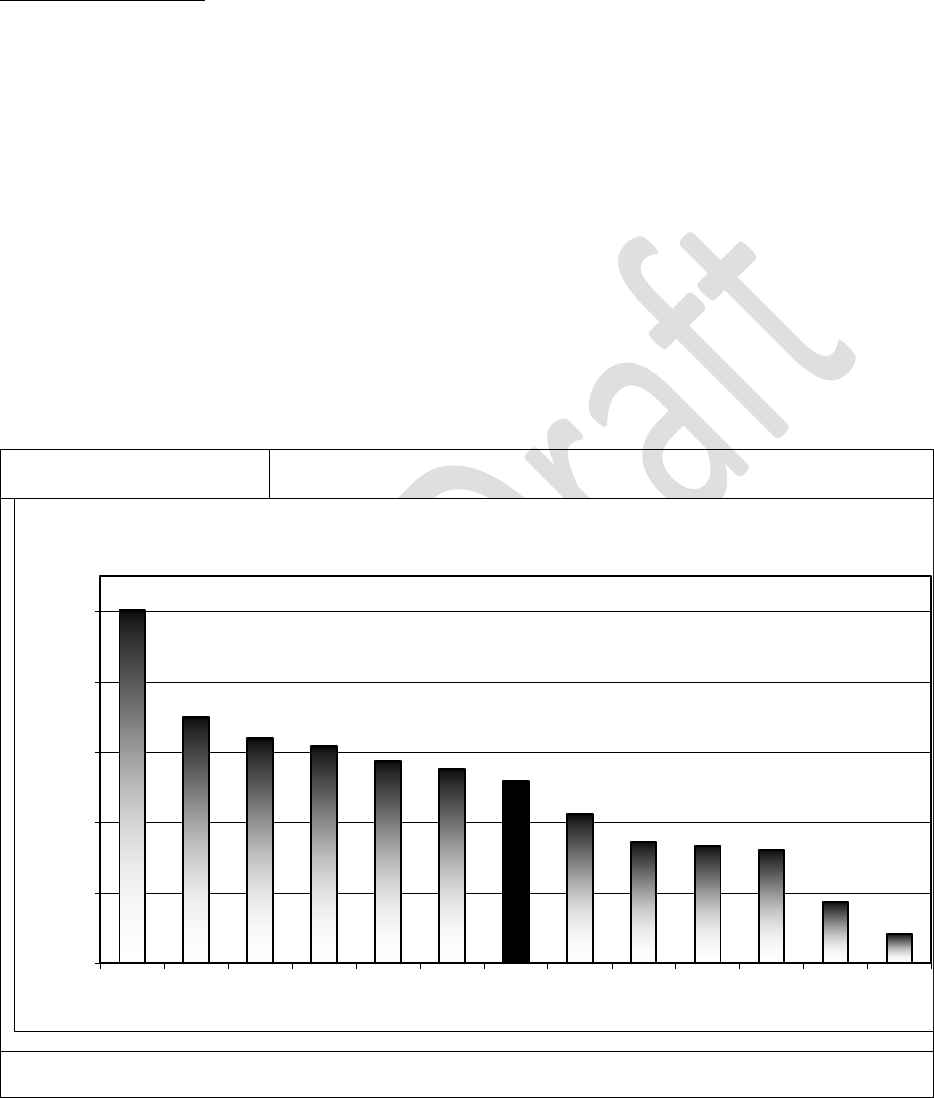

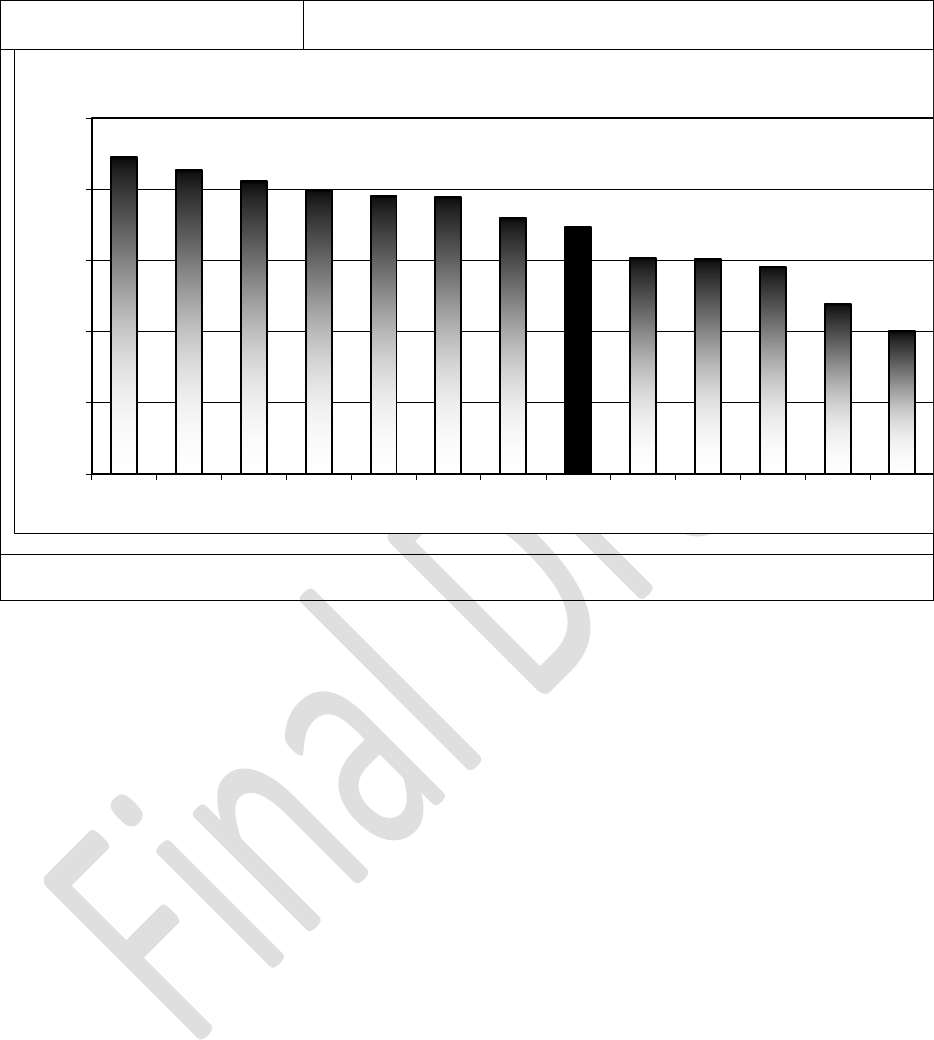

As mentioned previously, a more accurate assessment of an airline’s operations during

the period is the operating profit margin ratio, which helps remove distortions in the data. Using

the operating profit margin ratio, figure 4.3 shows that Northwest Airlines (NW) dominance in

2007 over the industry was much less than if one had only examined the total profit margin.

Northwest’s gross profit margin was on par with Allegiant Air (G4) and Southwest Airlines

(WN), with all three carriers around 8%., These three airlines present three divergent airline

-50%

-40%

-30%

-20%

-10%

0%

10%

G4 WN B6 AS CO FL AA F9 AVG. US UA NW DL

34

business models, with Northwest Airlines as a legacy international carrier, Allegiant as a leisure,

quasi-charter airline, and Southwest Airlines as a national low-cost carrier. All three airlines

found a way to turn roughly 8% of their revenue into an operating profit, highlighting their

ability to maintaining a spread between unit revenues and unit costs in 2007.

Figure 4.3

US Airlines’ 2007 Operating Profit Margin

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

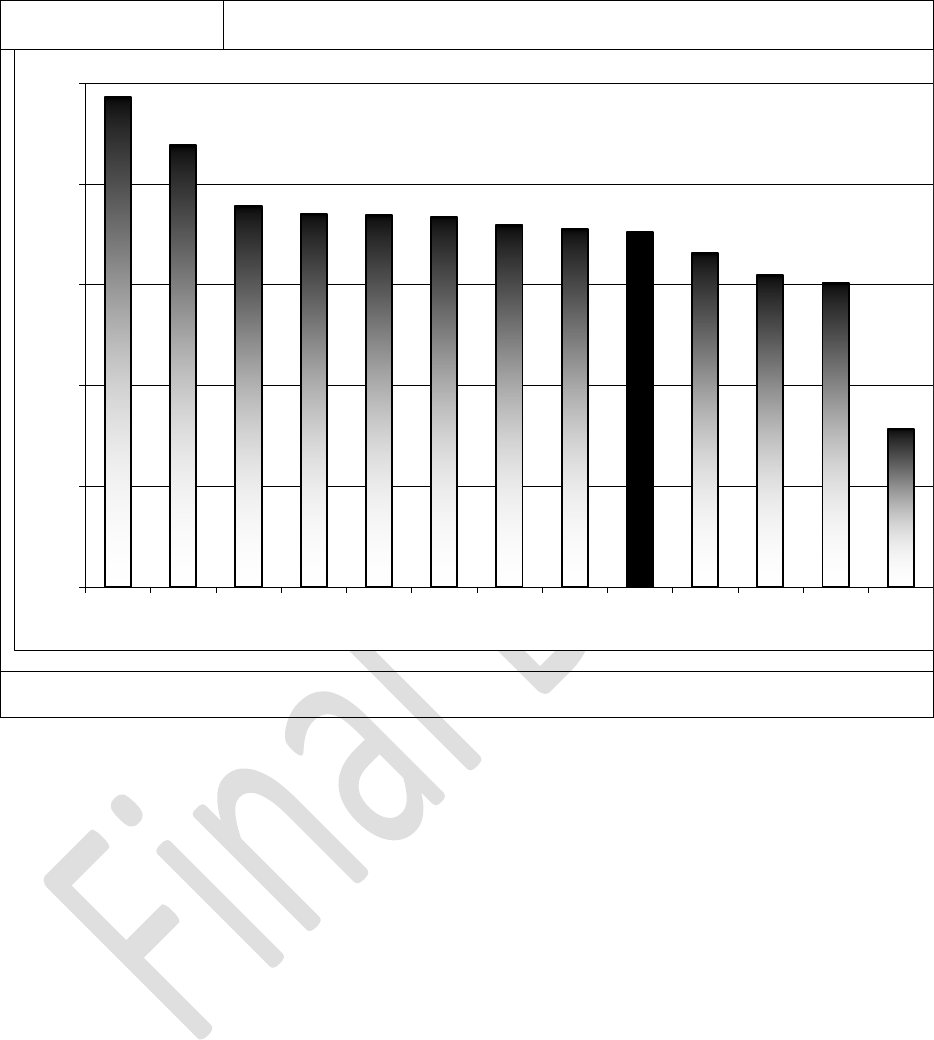

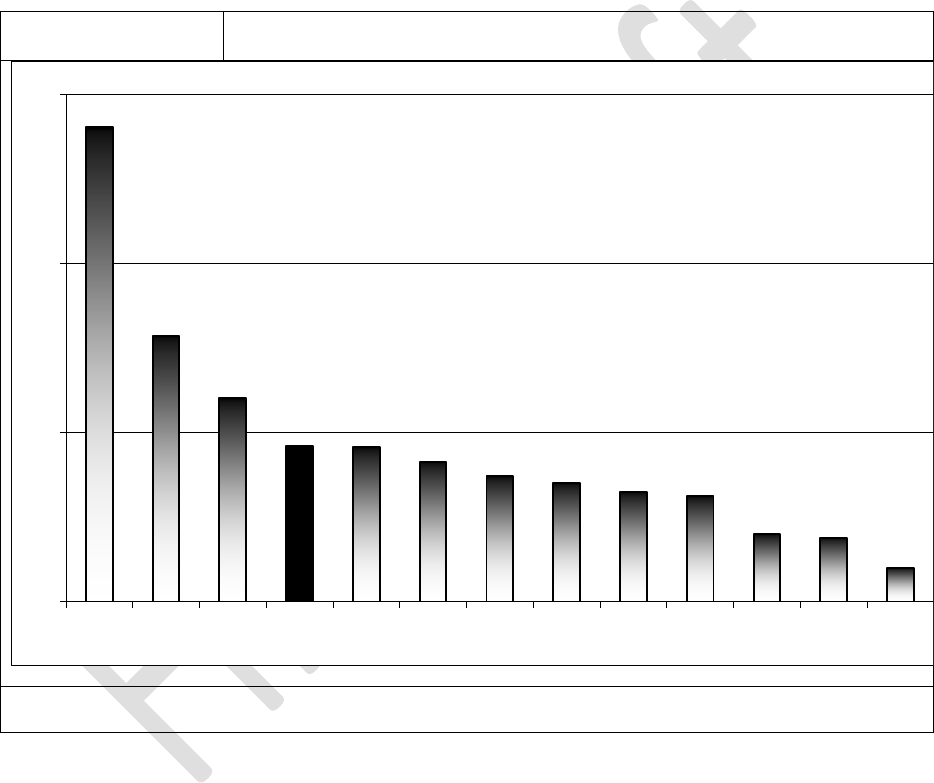

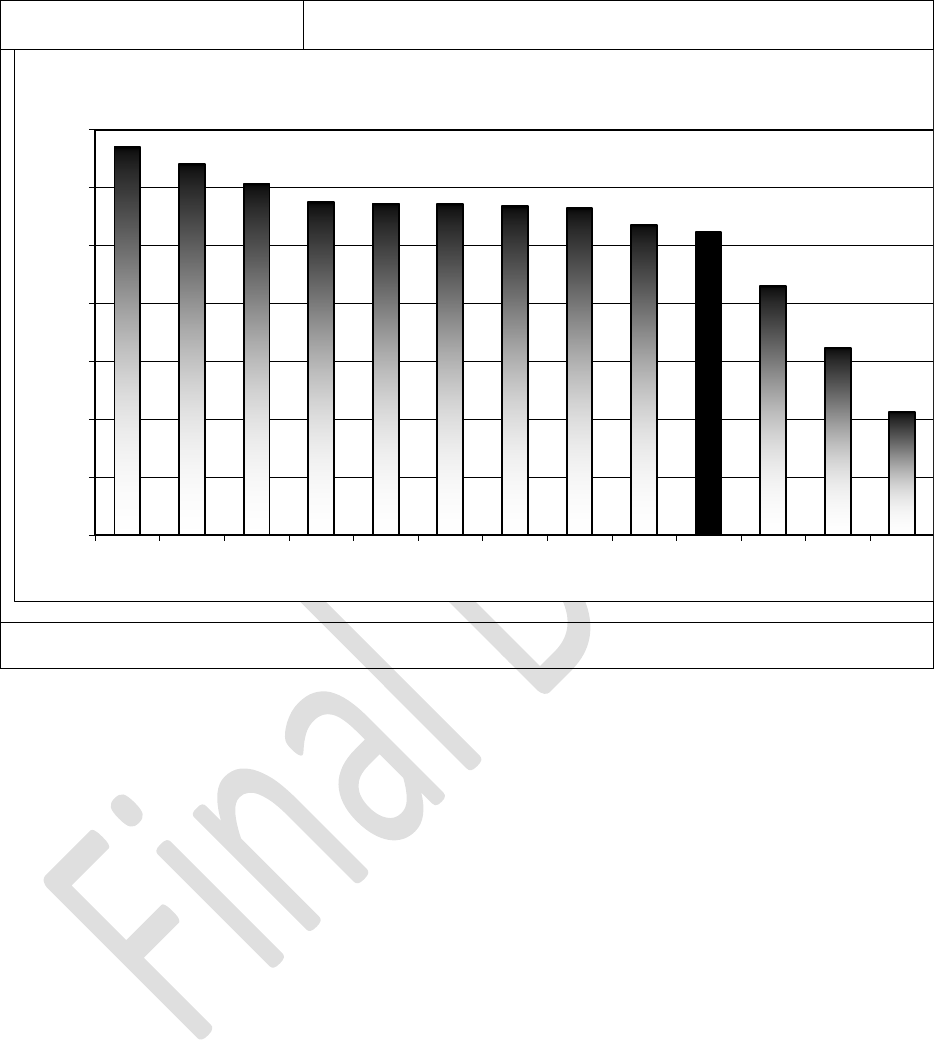

Figure 4.4 highlights the change between operating profit margins in 2008 and 2007. As with the

total profit margin, the 2008 operating profit margins were much lower than they were in 2007;

only four major U.S. airlines where able to make an operating profit in 2008; Southwest,

Allegiant, JetBlue and Delta. The average operating profit margin for all carriers in the figure

was about -4%.

-5%

0%

5%

10%

NW G4 WN FL B6 US AV. DL UA CO AS AA F9

35

Figure 4.4

US Airlines’ 2008 Operating Profit Margin

Source: Compiled by the authors from Back Aviation Form 41 Data

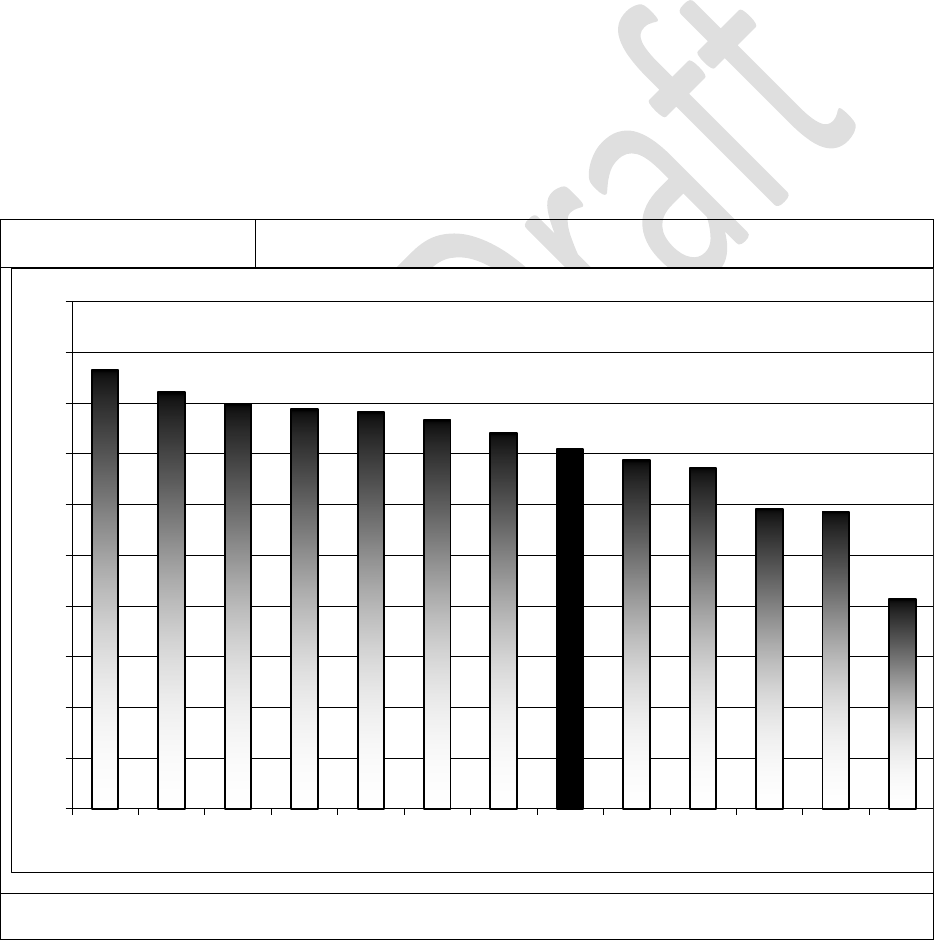

Other methods for analyzing profitability are return on assets and return on equity. These

metrics can be particularly important when deciding to invest in an airline, either through the

purchase of equity or through capital leases. Figure 4.5 provides the 2007 return on assets for

the twelve US airlines that are being compared. Here both Allegiant Airlines (G4) and Northwest

Airlines (NW) had very good return on asset ratios. Their success could largely be attributed to

the airlines having outright ownership of aircraft that are aging and are close to being fully

depreciated. Since aircraft represent the largest asset pool for airlines, an airline that is able to

generate decent returns with cheaper aircraft will generally have good ROA ratios. At the other

-20%

-15%

-10%

-5%

0%

5%

10%

WN G4 B6 DL NW AS CO AVG. FL UA F9 AA US

36

end of the spectrum, both JetBlue (B6) and Frontier (F9) have newer aircraft fleets, but were

unsuccessful in 2007 in parlaying these new aircraft into increased profitability.

Figure 4.5

US Airlines’ 2007 Return On Assets (ROA)

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

From a shareholders’ perspective, an airline’s ability to convert equity into profitability is

one of the clear signals for the success of the company. Figure 4.6 shows that Allegiant Airlines

(G4) had a tremendously high return on equity in 2007, while the rest of the industry also had

solid ROE values. Clearly, equity investments in Allegiant Airlines translated into strong

financial success in 2007. It is also worth noting that the grouping of carriers based on return on

equity is similar to the return on asset ratios presented in figure 4.5, with Allegiant and

Northwest Airlines (NW) at the top and JetBlue (B6) and Frontier Airlines (F9) near the bottom.

-5%

0%

5%

10%

15%

G4 NW DL US WN AV. CO AS FL UA AA B6 F9

37

Figure 4.6

US Airlines’ 2007 Return On Equity (ROE)

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

Based on the four profitability metrics, a more in depth picture of the financial success of

US airlines is possible. This is particularly true when applied to Allegiant Airlines (G4), a small

airline whose total profits only totaled $27 million, but whose financial performance was

outstanding. This is a major benefit of benchmarking since it allows both small and large

airlines, all with different operating philosophies, to be compared. Northwest Airlines (NW)

displayed some strong financial results; this could be the culmination of financial restructuring

and/or improved operational performance. Southwest Airlines (WN) maintained steady financial

results, proving yet again why it is continually regarded as one of the best managed US airlines.

As a whole, the US airlines displayed solid financial results in 2007, particularly when compared

to the disastrous financial performance of many previous years. However, 2008 saw a return to

unprofitability for most carriers as a combination of high fuel prices and reduced demand

reduced profit margins. While analyzing profitability helps one understand the historical

performance of the airlines, more analysis is required to help predict future performance.

-20%

-10%

0%

10%

20%

30%

40%

50%

60%

70%

G4 NW CO AA AV. US DL AS UA FL WN B6 F9

38

Liquidity Analysis

As mentioned previously, the goal of liquidity ratios is to analyze the short-term solvency

of an airline, in an effort to help determine if the airline can meet its short-term financial

commitments. In an industry with such tremendous volatility, efficient cash management is

critical to short-term success.

A key measurement of liquidity is the current ratio which compares the current assets of

the company to their current liabilities. Ideally, an airline wants a current ratio greater than 1,

indicating that its short-term liabilities can be covered by its current assets. For the twelve

airlines sampled in figure 4.7, only Northwest Airlines (NW) and Alaska Airlines (AS) had

current ratios in excess of 1 in 2007. This indicates that for the other ten airlines, if all their

current liabilities were to come due at once, they would not be covered. As it is, these airlines

will have to take measures in the short-term to help satisfy their current liabilities. While the

majority of the airlines have a current ratio in the 0.75 to 0.95 range, Allegiant Airlines (G4) has

a current ratio of 0.39, which is very low. However, Allegiant’s profitability ratios were above

average for the industry, indicating that the airline may hope that future profits will generate

cash, which in turn should help cover current liabilities. Regardless, Allegiant Airlines may need

to do some restructuring of their current liabilities and assets to satisfy short-term requirements.

While the current ratio and the quick ratio help analyze the overall immediate solvency

of a company, three separate liquidity ratios analyze the financial structure of the airlines from

an operational standpoint; these asses how effective the airlines are at cash management. Days of

accounts receivables, days of accounts payable, and days of inventory are all metrics that

analyze a different portion of an airline’s cash management. When combined, they display the

airline’s overall cash management efficiency.

39

Figure 4.7

US Airlines’ 2007 Current Ratio

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

Figure 4.8 provides a comparison of the airlines’ days of accounts receivables and days

of accounts payable. These metrics should be analyzed together since an airline wants to receive

its revenue as quickly as possible and pay its expenses as late as possible. Efficient cash

management occurs when the airline’s days of accounts receivables are low and when the

airline’s days of accounts payables are high. Based on figure 4.8, American Airlines (AA),

Continental Airlines (CO), and Allegiant Airlines (G4) all seem to have efficient cash

management since their spans between days of accounts receivable and accounts payable are all

in excess of 30 days. Through the introduction of electronic ticketing and the Internet, airlines

have been able to reduce their days of accounts receivables considerably, as evidenced by the

fact that the majority of the airlines have days of accounts receivable less than 20. The one

exception is Alaska Airlines (AS), whose 58 days of accounts receivables is quite high. One

possible reason behind Alaska Airlines high days of accounts receivables would be that a

substantial portion of their operating revenue is derived from cargo, which has on average

0.00

0.25

0.50

0.75

1.00

1.25

NW AS FL WN CO US F9 B6 AVG. DL UA AA G4

40

substantially longer days of accounts receivable than passenger revenue. At times, analyzing

accounts payable can be misleading since suppliers may provide cost concessions if the airline

pays earlier. Therefore, during negotiations with suppliers, purchasing departments must balance

lower unit costs with shorter days of accounts payable. Figure 4.8 shows that most airlines have

relatively short days of accounts payable. This is probably due to supplier negotiations for lower

unit costs (mentioned above) or other demands placed by suppliers on airlines because of the

financial uncertainty of the airline industry. At the extreme of this is US Airways (US) where the

days of accounts payable are 3 days. This makes it almost appear that the airline operates on a

cash basis. Therefore, the airline receives very little benefit from credit and from the ability to

hold onto cash.

Figure 4.8

US Airlines’ 2007 Days of Accounts Receivables and Days of Accounts

Payable

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

0

10

20

30

40

50

60

AS DL NW F9 UA AV. CO US AA B6 G4 WN FL

Accounts Receivable Turnover Accounts Payable Turnover

41

The final metric used to analyze an airline’s liquidity is the days of inventory, which

determines how long, on average, inventory sits before being used. Inventory that is rarely used

not only ties up cash that could be used elsewhere, but also incurs carrying costs for storing the

inventory. However, too little inventory can cause operational problems resulting in either

increased delays and cancellations or increased costs resulting from purchasing aircraft parts

from other airlines. Figure 4.9 displays the days of inventory for the twelve US airlines, with the

assumption that all inventories are related to aircraft maintenance and repair expenses.

22

From

figure 4.9, Northwest Airlines (NW) holds inventory the longest while Alaska Airlines (AS)

holds inventory the shortest. A possible explanation for Northwest Airlines long days of

inventory is that its aging aircraft require more maintenance, and this in turn means that a greater

stock of inventory is required. Another important factor that impacts the amount of inventory an

airline holds is the number of different aircraft types in the fleet. Obviously, the greater the

number of different aircraft types, the greater the inventory required. This means that inventory

is one department where airlines can receive the benefits of economies of scale through

operating streamlined aircraft fleets (i.e., operating less different types of aircraft). This

reasoning could potentially explain the fact that four of the five highest airlines, in terms of days

of inventory, operate diverse fleets. The exception is Southwest Airlines and the possible reasons

for this were discussed earlier in the chapter.

22

While this assumption is not completely accurate, the majority of inventory held by airlines, in terms of dollars, is

for aircraft maintenance. Other categories where inventory will be held includes catering (if applicable) and general

supplies.

42

Figure 4.9

US Airlines’ 2007 days of inventory

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

Long-Term Risk Analysis

While solvency analysis deals with assessing an airline’s ability to meet its short-term

commitments, long-term risk analysis attempts to help predict the strength of the company in the

future. Long-term risk analysis in the airline industry is usually analyzed using the debt to equity

ratio, the debt ratio, and the times interest earned ratio. These will be covered in turn.

The heavy debt structure of the airline industry can be seen by comparing the debt-to-equity

ratios of the twelve airlines. This heavy debt structure in the airline industry is ultimately the

result of the immense amount of capital involved in operating an airline, with very large capital

expenditures that are incurred for aircraft and facilities. Figure 4.10 shows the debt to equity

ratio for twelve US airlines. Note that all carriers have debt to equity ratios greater than 1,

indicating that all of the carriers’ capital structures are more heavily debt than equity weighted.

The airline with the most balanced capital structure is Southwest Airlines (WN) as its debt to

0

25

50

75

100

125

NW WN AA US CO AV. G4 DL F9 B6 UA FL AS

43

equity ratio is almost equal to 1. At the other end of the spectrum is American Airlines (AA),

whose debt to equity ratio of 14 indicates that for every $1 in equity, American Airlines has $14

in debt. The cost of debt financing is reflected in interest expense. An airline that is highly

leveraged in debt financing will incur greater amounts of interest expense and this increases the

volatility of the company’s earnings. On the other hand, the airline hopes that the use of debt

financing will increase profits sufficiently to offset the increased interest expense.

Figure 4.10

US Airlines’ 2007 Debt-to-Equity Ratio

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

Another debt based long-term risk metric is the debt ratio, which shows the total portion

of assets financed by debt. A high debt ratio generally indicates a firm with greater risk since

there are fewer assets that can be used to cover the debt. Also, this lack of assets may raise the

cost of debt in the future since there may be more uncertainty and risk to the lender. Therefore,

from a long-term risk perspective, an airline with a lower debt ratio is generally less risky than a

higher debt ratio airline. Based on the information contained in figure 4.11 and, using the

0

5

10

15

AA UA CO AV. G4 F9 B6 FL AS US NW DL WN

44

rational explained above, the riskiest airline is United Airlines (UA) with a debt ratio greater

than 0.80, and the least risky of the US airlines is Southwest Airlines (WN) with a debt ratio of

about 0.40. It is interesting to note that both Delta Air Lines (DL) and Northwest Airlines (NW)

have relatively low debt ratios. This is likely the result of bankruptcy reorganization where the

airlines could modify their debt structure. Note that Allegiant Airlines (G4), whose profitability

ratios were some of the best in the industry, has the second highest debt ratio. Clearly Allegiant

has used debt financing to generate increased profitability, but this has come with the increased

risk of taking on too much debt. In the long-term, Allegiant must continue maintaining

outstanding operational results, or the level of debt could be a problem in the future. This

example highlights the fact that all of the ratios need to be analyzed when evaluating the

financial strength or weakness of an airline.

Figure 4.11

US Airlines’ 2007 Debt Ratio

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

0.0

0.1

0.2

0.3

0.4

0.5

0.6

0.7

0.8

0.9

1.0

UA G4 AA F9 CO FL US AV. B6 AS NW DL WN

45

Airlines with high debt ratios can expect increased interest expenses resulting from a

larger debt load. The times interest earned ratio, displayed in figure 4.12 for twelve US airlines,

helps measure the airline’s ability to meet its debt payments. A times interest earned ratio of less

than one indicates that the airline does not generate enough earnings to cover its interest

expense. A negative times interest earned (TIE) ratio indicates that the airline could fail to meet

its interest payments and this could result in bankruptcy. Frontier Airlines’ (F9) negative times

interest earned ratio in 2007 was ultimately a signal of the airline declaring bankruptcy in 2008.

Figure 4.12

US Airlines’ 2007 Times Interest Earned Ratio

Source: Compiled by the authors from Bureau of Transportation Statistics (BTS) data

-5

0

5

10

15

20

25

30

FL WN NW G4 AV. DL AS US CO UA AA B6 F9

46

Figure 4.13

US Airlines’ 2008 Times Interest Earned Ratio

Source: Compiled by the authors using Back Aviation Form 41 Data

In 2008 the majority of the airlines shown in figure 4.13 had negative times interest earned

ratios. This indicates that these airlines have negative earnings, which severely impacts their

ability to pay their debt. The only airlines which could comfortably pay their debt (had TIE’s

over 1) were Southwest Airlines and Allegiant Air.

Stock Market Analysis

Another methodology used to analyze the airline industry is the external view of the

airline. The price of the stock of a company or an airline varies according to the external

perception of the company. The stock market is also the means by which airlines gain equity

investment and it also helps signal the long term financial prospects of the airline. Since stock

market prices change daily, ratios that contain these prices must be fixed at a certain point of

time. Therefore, for comparison purposes, the data contained in table 4.2 are based on market

-25

-20

-15

-10

-5

0

5

10

WN G4 DL B6 NW AS CO UA AVG. F9 AA US FL

47

statistics generated at market closing on March 5, 2009. Due to negative profits in 2008, all of

the earnings per share (EPS) ratios are going to be negative except for the two carriers who made

a profit in 2008, Allegiant and Southwest.

Table 4.2

US Airlines’ stock market data as of 03/05/2009

Airline Name

Company Ticker

Symbol

Market Price

(@ 03/05/09)

EPS

(@ 03/05/09)

AirTran

AAI

$2.56

($2.51)

Alaska Airlines

ALK

$14.80

($3.74)

Allegiant Airlines

ALGT

$33.83

$1.73

American Airlines

AMR

$2.54

($8.00)

Continental Airlines

CAL

$7.26

($5.52)

Delta Air Lines

DAL

$3.93

($19.06)

Frontier Airlines

FRNTQ.PK

$0.20

($3.49)

JetBlue

JBLU

$2.84

($0.34)

Southwest Airlines

LUV

$5.01

$0.24

United Airlines

UAUA

$3.06

($42.18)

US Airways

LCC

$1.97

($22.06)

Source: Compiled by the authors from Yahoo! Finance (3/6/09)

Based on the data compiled in table 4.2, the price-earnings ratio can be calculated, which

helps standardize the expectations of future earnings. Unlike many metrics which are backward

looking, the price-earnings ratio provides some forward-looking information. This is because the

price of the airline’s stock is based on future cash flows. Table 4.3 displays the price-earnings