GLOBAL HEADQUARTERS • THE GREGOR BUiLDinG

716 WEST AvE • AUSTin, TX 78701-2727 • USA

hOW tO DEtECt AND PREvENt

fINANCIAL StAtEmENt fRAuD

General Techniques for Financial Statement Analysis

How to Detect and Prevent Financial Statement Fraud

117

VI. GENERAL TECHNIQUES FOR FINANCIAL STATEMENT ANALYSIS

Financial Statement Analysis

Financial statement analysis is a process that enables readers of a company’s financial reports to develop

and answer questions regarding the data presented. Financial statements express a company’s economic

condition in three ways: (1) the balance sheet reports assets, liabilities, and owners’ equity; (2) the

income statement accounts for the profit or loss of the company; (3) and the cash flow statement

displays the sources and uses of cash. At the end of these statements, there is a section for footnotes—a

more detailed description of several items on the financial statements including a discussion of changes

in accounting methods, related-party transactions, contingencies, and so on. Annual and quarterly

reports also typically include a section titled Management’s Discussion and Analysis (MD&A), which gives

management’s perspective on the financial results of the period in the report.

Reading the MD&A section of the financial report can give the fraud examiner a great deal of

information about management’s tone. Management frequently includes information about the financial

results compared with its expectations, as well as further details and insights into the values on the

financial statements. The footnotes to the financials can also give valuable tidbits about the changes that

have occurred in the organization. For example, if an organization has changed an accounting policy, a

fraud examiner might be interested in understanding the reason to determine whether the change was

legitimate or intended to benefit the organization or management.

Financial analysis techniques can help investigators discover and examine unexpected relationships in

financial information. These analytical procedures are based on the premise that relatively stable

relationships exist among economic events in the absence of conditions to the contrary. Known

contrary conditions that cause unstable relationships to exist might include unusual or nonrecurring

transactions or events, and accounting, environmental, or technological changes. Public companies

experiencing these events must disclose and explain the facts in their financial statements. Increasingly,

private and nonprofit companies follow best practices and do the same.

Unexpected deviations in relationships most likely indicate errors, but also might indicate illegal acts or

fraud. Therefore, deviations in expected relationships warrant further investigation to determine the

exact cause. Several methods of analysis assist the reader of financial reports in highlighting the areas

that most likely represent fraudulent accounting methods.

Analytical procedures are used to detect and examine relationships of financial information that do not

appear reasonable. They are useful in identifying:

• Differences that are not expected

• The absence of differences that are expected

General Techniques for Financial Statement Analysis

118

How to Detect and Prevent Financial Statement Fraud

• Potential errors

• Potential fraud and illegal acts

• Other unusual or non-recurring transactions or events

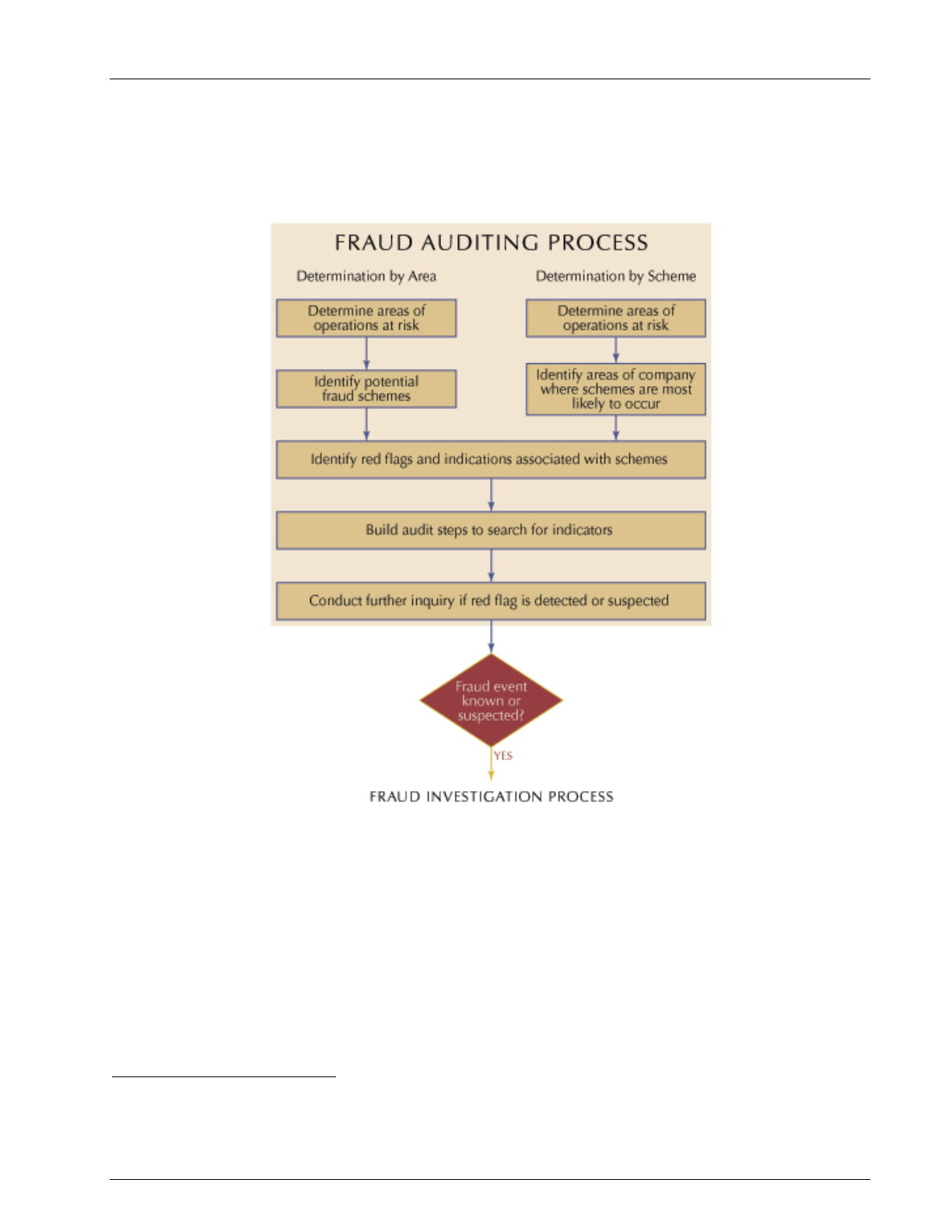

The previous diagram, “Fraud Auditing Process,”

6

depicts a series of steps that can be taken to audit for

fraud. Analytical techniques assist with the first steps in the fraud auditing process by enabling the fraud

examiner to identify areas of high risk, highlight the most likely schemes, and identify the red flags that

warrant further investigation.

6

“The Emerging Role of Internal Audit in Mitigating Fraud and Reputation Risks,” Internal Audit Services,

PricewaterhouseCoopers, 2004.

General Techniques for Financial Statement Analysis

How to Detect and Prevent Financial Statement Fraud

119

Comparative Techniques

Relationships among financial data that do not appear reasonable should be investigated. Fraud

examiners can employ the following techniques to help them identify such relationships:

• Compare current-period financial information to prior-period financial information, budgets, and

forecasts.

• Examine relationships among financial information. For instance, cost of goods sold is expected to

vary directly in relation to sales.

• Study relationships of financial information with related nonfinancial information. For example,

department store sales are expected to vary with the square footage of the sales floor.

• Compare information to that of other organizational units or entities within the same industry.

Financial Relationships

An understanding of general relationships between certain financial statement balances is necessary to

identify relationships that appear unusual. If sales increase, how should the cost of sales respond? If

commission expense decreases, what would be expected of sales? Answers to questions such as these are

the foundation of financial analysis. The following relationships are general, and traditionally occur

between financial accounts; however, unique circumstances may render different results.

Assets Versus Liabilities

A financially healthy company tries to maintain a consistent balance between assets and liabilities. By

keeping a certain balance, the company displays its solidity to lenders or equity investors and keeps

financing costs down. A sudden change from historical norms means something has changed with

management’s view of its business. It also could indicate that management is trying to hide something. A

sudden increase in the ratio could mean that liabilities such as long-term debt have been hidden in off-

balance sheet entities. If the value of liabilities rises and the ratio spikes downward, it could reveal that

the company is borrowing heavily to finance operations and that the risk of fraud is acute.

Sales Versus Cost of Goods Sold

The company generates sales because it sells its merchandise. This merchandise had to be purchased,

manufactured, or both, all of which entail a cash outlay for materials, labor, and so on. Therefore, for

each sale, there must be a cost associated with it. If sales increase, then the cost of goods sold generally

increases proportionally. Of course, there are cases where a company has adopted a more efficient

method of producing goods, thus reducing its costs, but there still are costs associated with the sales that

are recognized upon the sale of the goods.

Sales Versus Accounts Receivable

When a company makes a sale to a customer, the company generally ships the merchandise to the

customer before the customer pays, resulting in an account receivable for the company. Therefore, the

General Techniques for Financial Statement Analysis

120

How to Detect and Prevent Financial Statement Fraud

relationship between the sales and the accounts receivable is directly proportional. If sales increase, then

accounts receivable should increase at approximately the same rate.

Sales Versus Inventory

A company’s inventory is merchandise that is ready to be sold. A company generally tries to anticipate

future sales, and in doing so, tries to meet these demands by having an adequate supply of inventory.

Therefore, inventory usually reflects the growth in sales. If sales increase, then inventory should increase

to meet the demands of sales. Inventory that grows at a faster pace than sales might indicate obsolete,

slow-moving merchandise or overstated inventory.

Profit Margins

Companies generate sales revenue by selling products or providing services. Likewise, companies incur

direct and indirect costs related to producing or acquiring the products they sell, or providing the

services for their customers. Gross, operating, and net profit margins are shown on the income

statement. Over time, profit margins should stay consistent as the company targets a certain profit in

order to stay in business. If the company encounters increased competition and must reduce the price

for its products, it has to find ways to cut expenses. Ongoing pressure on profit margins indicates

pressure on management, which could ultimately lead to fraud in the financial reporting.

Unexpected Relationships

When analytical procedures uncover an unexpected relationship among financial data, the fraud

examiner must investigate the results. The evaluation of the results should include inquiries and

additional procedures. Before asking the company’s employees and management about the variations,

the fraud examiner should first establish expectations for the causes of the variances. From expected

causes, the fraud examiner will be better suited to ask meaningful questions when interviewing company

personnel. Explanations derived from employees should then be tested through examination of

supporting evidence. For example, if the sales manager indicates that the increase in sales is due to a new

advertising campaign, examine the advertising expense account to verify that a campaign did occur. If

the advertising expense is similar to the prior year, the relationship is not reasonable and fraud may exist.

Analytical Procedures

Fraud examiners employ several techniques to manipulate plain, unconnected numbers into solid,

informative data to interpret the company’s financial standing. Investigating relationships between

numbers offers deep insight into the financial wellbeing of an organization. By comparing these

relationships with other industries or businesses within the same industry, a fraud examiner can

extrapolate viable evidential matter and gain a greater comprehension of the company’s financial

condition. Financial statement analysis includes the following:

General Techniques for Financial Statement Analysis

How to Detect and Prevent Financial Statement Fraud

121

• Percentage analysis, including vertical and horizontal analysis

• Ratio analysis

• Cash flow analysis

Percentage Analysis—Vertical and Horizontal

There are traditionally two methods of percentage analysis of financial statements: vertical analysis and

horizontal analysis. Vertical analysis is a technique for analyzing the relationships between the items on

any one of the financial statements in one reporting period. The analysis results in the relationships

between components expressed as percentages that can then be compared across periods. This method

is often referred to as “common sizing” financial statements. In the vertical analysis of an income

statement, net sales is assigned 100%; for a balance sheet, total assets is assigned 100% on the asset side,

and total liabilities and equity is expressed as 100% on the other side. All other items in each of the

sections are expressed as a percentage of these numbers.

Horizontal analysis is a technique for analyzing the percentage change in individual financial statement

items from one year to the next. The first period in the analysis is considered the base, and the changes

in the subsequent period are computed as a percentage of the base period. If more than two periods are

presented, each period’s changes are computed as a percentage of the preceding period. The resulting

percentages are then studied in detail. It is important to consider the amount of change as well as the

percentage in horizontal comparisons. A 5% change in an account with a very large dollar amount may

actually be much more of a change than a 50% change in an account with much less activity. Like

vertical analysis, this technique does not detect small, immaterial frauds. However, both methods

translate changes into percentages, which can then be compared to highlight areas of top concern.

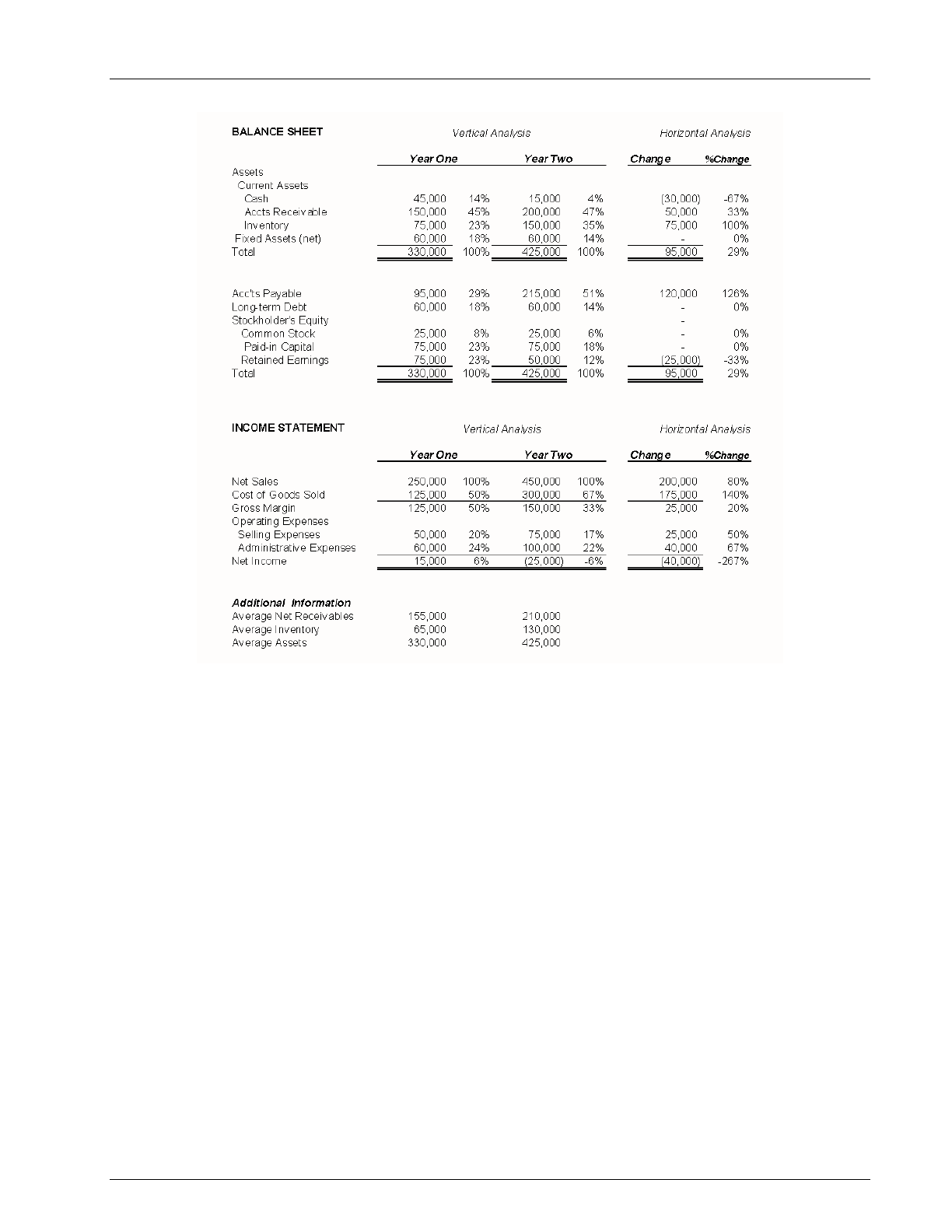

The following is an example of financial statements that are analyzed by both vertical and horizontal

analysis:

General Techniques for Financial Statement Analysis

122

How to Detect and Prevent Financial Statement Fraud

Vertical Analysis

As illustrated in the above example, vertical analysis of the income statement uses total sales as the base

amount, and all other items are then analyzed as a percentage of that total. Vertical analysis emphasizes

the relationship of statement items within each accounting period. These relationships can be used with

historical averages to determine statement anomalies.

In the above example, the fraud examiner can observe that accounts payable is 29% of total liabilities

and stockholders’ equity. Historically, they may find that this account averages slightly over 25%. In year

two, accounts payable rose to 51%. Although the change in the account total may be explainable

through a correlation with a rise in sales, this significant rise might be a starting point in a fraud

examination. Source documents should be examined to determine the rise in this percentage. With this

type of examination, fraudulent activity may be detected. The same type of change can be seen as selling

expenses decline as a part of sales in year two from 20 to 17%. Again, this change may be explainable

with higher volume sales or another bona fide explanation. But close examination may possibly cause a

General Techniques for Financial Statement Analysis

How to Detect and Prevent Financial Statement Fraud

123

fraud examiner to uncover fictitious sales, since there was not a corresponding increase in selling

expenses.

Horizontal Analysis

Horizontal statement analysis uses percentage comparison across accounting periods, or in a horizontal

manner. The percentage change is calculated by dividing the amount of increase or decrease for each

item by the prior-period amount.

In the previous example, cash declined by $30,000 from year one to year two, a 67% drop. Further

analysis reveals that the 80% increase in sales has a much greater corresponding increase in cost of

goods sold, which rose 140%. This is an unusual increase and displays a deteriorating financial

condition. If management employed fraudulent accounting in the period, it might mean that revenues

were understated for some reason. Management might have wanted to avoid a high tax bill or to shift

revenues to the next period for some reason. It might also mean that the cost of goods is rising, which

might pressure management to improve the appearance of the company’s financials by engaging in

fraudulent accounting in future periods.

Financial Ratio Analysis

Ratio analysis is a means of measuring the relationship between two different financial statement

amounts. Ratios are calculated from current year numbers and are then compared to previous years,

other companies, the industry, or even the economy to judge the performance of the company. This

form of financial statement analysis can be very useful in detecting red flags for a fraud examination.

Many professionals, including bankers, investors, business owners, and investment analysts, use this

method to better understand a company’s financial health.

Ratio analysis allows for internal evaluations using financial statement data. The relationship and

comparison are the keys to the analysis. For further insight, financial statement ratios are used in

comparisons to an entity’s industry averages.

As the financial ratios present a significant change from one year to the next, or over a period of years, it

becomes obvious that there might be a problem. As in all other analyses, specific changes are often

explained by changes in the business operations. When a change in a specific ratio or several related

ratios is detected, the appropriate source accounts should be researched and examined in detail to

determine if fraud has occurred. For instance, a significant decrease in a company’s current ratio might

point to an increase in current liabilities or a reduction in assets, both of which could be used to cover

fraud.

General Techniques for Financial Statement Analysis

124

How to Detect and Prevent Financial Statement Fraud

In the analysis of financial statements, each reader of the statements will determine which portions are

most important. As with the statement analysis discussed previously, the analysis of ratios is limited by

its inability to detect fraud on a smaller, immaterial scale.

These ratios may also reveal frauds other than accounting frauds. If an employee is embezzling from the

company’s accounts, for instance, the amount of cash will decrease disproportionately and the current

ratio will decline. Liability concealment will cause a more favorable ratio. Similarly, a check-tampering

scheme will usually result in a decrease in current assets, namely cash, which will, in turn, decrease the

current ratio. In fact, these frauds might be more easily detected with ratio analysis because employees

other than management would not have access to accounting cover-ups of non-accounting frauds.

Anomalies in ratios could point directly to the existence of fraudulent actions. Accounting frauds can be

much more subtle and demand extensive investigation beyond the signal that something is out of the

norm.

The following calculations are based on the financial statement example presented earlier:

Current Ratio

The current ratio, current assets divided by current

liabilities, is probably the most frequently used ratio in

financial statement analysis. This comparison measures a

company’s ability to meet short-term obligations from its liquid assets. The number of times that current

assets exceed current liabilities has long been a measure of financial strength.

In detecting fraud, this ratio can be a prime indicator of manipulation of accounts involved.

Embezzlement will cause the ratio to decrease. Liability concealment will cause a more favorable ratio.

In the preceding example, the drastic change in the current ratio from year one (2.84) to year two (1.70)

should cause a fraud examiner to look at these accounts in more detail. For instance, a check-tampering

scheme will usually result in a decrease in current assets, or cash, which will in turn decrease the ratio.

Quick Ratio

The quick ratio, often referred to as the acid-test ratio,

compares assets that can be immediately liquidated to

liabilities that will be due in the next year. This calculation

divides the total cash, securities, and receivables by current liabilities. This ratio is a measure of a

company’s ability to meet sudden cash requirements. In turbulent economic times, it is used quite

prevalently, giving the analyst a worst-case look at the company’s working capital situation.

Current Assets

Current Liabilities

Cash+Securities+Receivables

Current Liabilities

General Techniques for Financial Statement Analysis

How to Detect and Prevent Financial Statement Fraud

125

A fraud examiner analyzes this ratio for fraud indicators. In year one of the example, the company

balance sheet reflects a quick ratio of 2.05. This ratio drops in year two to 1.00. In this situation, a closer

review of accounts receivable shows that they are increasing at an unusual rate, which could indicate that

fictitious accounts receivable have been added to inflate sales. Of more concern, perhaps, is the increase

in accounts payable that might require, at a minimum, a closer review to determine why. If the drop in

the ratio indicates a problem customer or significant slowing in the time to collection, it might reflect a

general decline in company prospects. That, in turn, would be a red flag that management could feel

pressured to report fraudulent financials.

Debt-to-Equity Ratio

The debt-to-equity ratio is computed by dividing total liabilities by

total equity. It indicates the proportion of equity and debt a

company uses to finance its assets. Because the ratio provides a

picture of the relative risk assumed by the creditors and owners, it is heavily considered by lending

institutions. The higher the ratio, the more difficult it will be for the owners to raise capital by increasing

long-term debt, and the greater the risk assumed by creditors. Debt-to-equity requirements are often

included as borrowing covenants in corporate lending agreements. The example displays a year one ratio

of 0.89. This is very favorable, as it shows that the company is financed more by equity than by debt.

However, year two shows a ratio of 1.84, meaning that debt is greatly increasing relative to equity. In

this case, the increase in the ratio corresponds with the rise in accounts payable. Sudden changes in this

ratio may signal a fraud examiner to look for fraud.

Profit Margin Ratio

The profit margin ratio is net income divided by sales. This

ratio is often referred to as the efficiency ratio, in that it

reveals profits earned per dollar of sales. This percentage of

net income to sales examines not only the effects of gross margin changes, but also changes in selling

and administrative expenses. If fraud is committed, net income may be artificially overstated, resulting in

a profit margin ratio that is abnormally high compared to other periods. False expenses cause an

increase in expenses and a decrease in the profit margin ratio. This ratio should be fairly consistent over

time.

In this example, the profit margin analysis is already calculated in the vertical and horizontal analyses.

While revenues increased by 80%, the cost of goods sold increased by 140%; this, in turn, dropped

profit margins from 6% to –6%. Further investigation could uncover fraudulent accounting that shifted

costs from one period to another, or might reveal another type of fraud in which inventory is being

stolen so costs appear to jump.

Total Liabilities

Total Equity

Net Income

Net Sales

General Techniques for Financial Statement Analysis

126

How to Detect and Prevent Financial Statement Fraud

Receivables Turnover Ratio

Receivable turnover is defined as net sales on account divided

by average net receivables. It measures the number of times the

receivables balance is turned over during the accounting period.

In other words, it measures the time between sales on account

and the collection of funds. This ratio is one that uses both income statement and balance sheet

accounts in its analysis. If fictitious sales have been recorded, this bogus income will never be collected.

As a result, the turnover of receivables will decrease.

If the fraud is caused from fictitious sales, this bogus income will never be collected. In the example, the

accounts receivable turnover jumps from 1.61 to 2.14. The fraud examiner can use this ratio as an

indicator that revenues might be fake, thus requiring further examination of source documents.

Collection Ratio

Accounts receivable aging is measured by the collection ratio,

which divides 365 days by the receivable turnover ratio to

arrive at the average number of days to collect receivables. In

general, the lower the collection ratio, the faster receivables are collected.

A fraud examiner may use this ratio as a first step in detecting fictitious receivables or larceny and

skimming schemes. Normally, this ratio stays fairly consistent from year to year, but changes in billing

policies or collection efforts may cause a fluctuation. The example shows a favorable reduction in the

collection ratio from 226.3 in year one to 170.33 in year two. This means that the company is collecting

its receivables more quickly in year two than in year one.

Inventory Turnover Ratio

The relationship between a company’s cost of goods sold and its

average inventory is shown through the inventory turnover

ratio. This ratio measures the number of times the inventory is

sold during the period. This ratio is a good determinant of

purchasing, production, and sales efficiency. In general, a higher inventory turnover ratio is considered

more favorable.

For example, if cost of goods sold has increased due to theft of inventory (ending inventory has

declined, but not through sales), then this ratio will be abnormally high. In the case example, inventory

turnover increases in year two, signaling the possibility that an embezzlement is buried in the inventory

Net Sales on Account

Average Net Receivables

365

Receivable Turnover

Cost of Goods Sold

Average Inventory

General Techniques for Financial Statement Analysis

How to Detect and Prevent Financial Statement Fraud

127

account. A fraud examiner should look at the changes in the components of the ratio to determine a

direction in which to discover possible fraud.

Average-Number-of-Days-Inventory-Is-in-Stock Ratio

The average-number-of-days-inventory-is-in-stock ratio is a

restatement of the inventory turnover ratio expressed in days.

This rate is important for several reasons. An increase in the number of days that inventory stays in

stock causes additional expenses, including storage costs, risk of inventory obsolescence, and market

price reductions, as well as interest and other expenses incurred due to tying up funds in inventory

stock. Inconsistency or significant variance in this ratio is a red flag for fraud investigators. Fraud

examiners may use this ratio to examine inventory accounts for possible larceny schemes. Purchasing

and receiving inventory schemes can affect the ratio. Understating the cost of goods sold results in an

increase in the ratio as well. Significant changes in the inventory turnover ratio are good indicators of

possible fraudulent inventory activity.

Asset Turnover Ratio

Net sales divided by average operating assets is the calculation

used to determine the asset turnover ratio. This ratio measures

the efficiency with which asset resources are used. The case

example above displays a greater use of assets in year two than

in year one.

Cash Flow Analysis

Cash flow analysis is a specific application of horizontal analysis that helps highlight possible areas of

fraudulent accounting. Since the cash flow statement most directly reports how money flows into and

out of the company, cash flow analysis often helps detect misstatements.

The statement of cash flows details the sources and uses of the company’s cash. Earnings show up in

operating cash flows; purchases and sales of plant assets show up in investing cash flows; and changes in

equity and debt show up in financing cash flows.

Cash Provided by Operating Activities

• Receipts from sale of goods or services

• Interest and dividends received

• Payments to employees and suppliers

• Payments of interest

• Payments of taxes

Net Sales

Average Assets

365

Inventory Turnover