General Disclaimer

One or more of the Following Statements may affect this Document

This document has been reproduced from the best copy furnished by the

organizational source. It is being released in the interest of making available as

much information as possible.

This document may contain data, which exceeds the sheet parameters. It was

furnished in this condition by the organizational source and is the best copy

available.

This document may contain tone-on-tone or color graphs, charts and/or pictures,

which have been reproduced in black and white.

This document is paginated as submitted by the original source.

Portions of this document are not fully legible due to the historical nature of some

of the material. However, it is the best reproduction available from the original

submission.

Produced by the NASA Center for Aerospace Information (CASI)

DOE/NASA/20485-13

NASA TM-83035

(NASA-TA-83035) THE WORLDWIDE MARKET FOR

PHOTOTOLTAICS IN THE RURAL SECTOR (NASA)

15

P

HC A02/AF A01

CSCL 10A

N83-15840

Unclas

G3/44 02414

^

The

Worldwide Market for Photovoltaics

in the Rural Sector

William A. Brainard

National Aeronautics and Space Administration

Lewis Research Center

R

f

r

r

.

r

-

REC.'S'

NASA

ACCAASS Pff'

Work performed for

U.S. DEPARTMENT OF ENERGY

Conservation and Renewable Energy

Division of Photovoltaic Energy Systems

Prepared for

Sixteenth Photovoltaic Specialists Conference

sponsored by the Institute of Electrical and Electronics Engineers

San Diego, California, Septernoer 27-28, 1982

DOE/NASA/20485-13

NASA TM-83035

The Worldwide Market for Photovoltaics

in the Rural Sector

William A. Brainard

National Aeronautics and Space Administration

Lewis Research Center

Cleveland, Ohio 44135

Work performed for

U.S. DEPARTMENT OF ENERGY

Conservation and Renewable Energy

Division of Photovoltaic Energy Systems

Washington, D.C. 20545

Under Interagency Agreement DE-AI01-79ET20485

Prepared for

Sixteenth Photovoltaic Specialists Conference

sponsored by the institute of E

l

ectrical and Electronics Engineers

San Diego, California, September 27-28, 1982

THE WORLDWIDE MARKET FOR PHOTOVOLTAICS IN THE RURAL SECTOR

William A. Brainard

National Aeronautics and Space Administration

Lewis Research Center

Cleveland, Ohio 44135

ABSTRACT

The NASA Lewis Research Center manages the Stand-Alone Applications

Project for the U.`,. DOE. During the 1980-81 program year, that project

office sponsored tree major studies to determine the worldwide market for

stand-alone photovoltaic power systems in three specific segments of the

rural sector. The three studies addressed the worldwide market for

photovoltaic power systems for village power, cottage industry, and

.y

agricultural applications. The objectives of these studies were to:

o

Assess the market potential for small stand-alone photovoltaic

power system in specific application areas

o

Identify technical, social and institutional barriers to PV

utilization

o

Identify funding sources available to potential users

o

Recommend marketing strategies appropriate for each sector to

American PV product manufacturers.

The studies were prepared on the basis of data gathered from domestic

sources and from field trips to representative countries. This paper

summarizes the results of these three studies. Both country-specific and

sector-specific results are discussed, and broadly applicable barriers

pertinent to international marketing of PV products are presented. Generic

recommendations to American PV manufacturers of appropriate strategies for

the international market in general are also made.

INTRODUCTION

Very early in the National Photovoltaics Program, it was realized that

because of the widespread electrification of the United States and other

developed countries, most of the initial market for terrestrial photovoltaic

systems would be in the developing regions of the world. Such systems, it

was reasoned, were more likely to be cost-competitive with alternative

energy sources especially in rural areas. The basis for this thinking was

the realization that the real cost of supplying small amounts of power

dependably to remote areas is extremely high when one determines true cost

for transmission line installation or generator installation, operation and

maintenance.

The U.S. Department of Energy sponsored several activities designed to

help the establishment of a strong, competitive American photovoltaics

industry. One of these activities was to conduct assessments of the market

for photovoltaics in several sectors. The responsibility for conduct of

market assessments for small stand-alone (i.e., non-grid connected)

photovoltaic systems was assigned to the Stand-Alone Photovoltaic Systei

Project Office managed by the NASA Lewis Research Center. In response

this assignment, that office issued contracts to three organizations to

study the market for stand-alone photovoltaic systems in three specific

rural sectors which were felt to be large potential markets. The market

studied were: (1) the rural village PV power market, (2) the cottage

industry PV power market, and (3) the agricultural PV power market. The

three organizations who conducted these studies under NASA-Lewis-managed

contracts were Motorola, IIT Research Institute and DHR, Inc.,

respectively. These studies had four major objectives:

o

To assess the market for stand-alone photovoltaic power systems in

specific application areas

o

To identify the technical, social and institutional barriers to

widespread photovoltaic utilization

o

To identify sources of financing for potential purchasers

o

To recommend to American photovoltaic manufacturers strategies

appropriate to mar'c tinq photovoltaics in the developing world.

These studies resulted in a series of reports (refs. 1 to 8) that were

distributed to the American photovoltaics industry over the last 18 months.

This paper hriefly summarizes the results of these studies.

MARKET STUDY RESULTS

The Market for Photovoltaics for Rural Village Power

The market for photovoltaics in the developing world for remote village

power systems was studied by Motorola (ref. 1). For the purposes of the

study a remote village was defined to be:

"A grouping of up to 2000 people living in a remote area, but in close

enough proximity to interact with each other on e.. daily basis."

The term remote as used in this definition implies that the village is

located such that it cannot be supplied economically with central station

utility power.

The methodology employed in this study had two major components: a

literature search, and a series of in-country surveys. The literature

search gathered pertinent information such as developing countries' rural

electrification plans, utility rates and costs of power line extension, and

performance and cost data of alternative forms of power generation such as

diesel generators. The information gathered was used to determine the key

regions and countries for further on-site investigation and to determine the

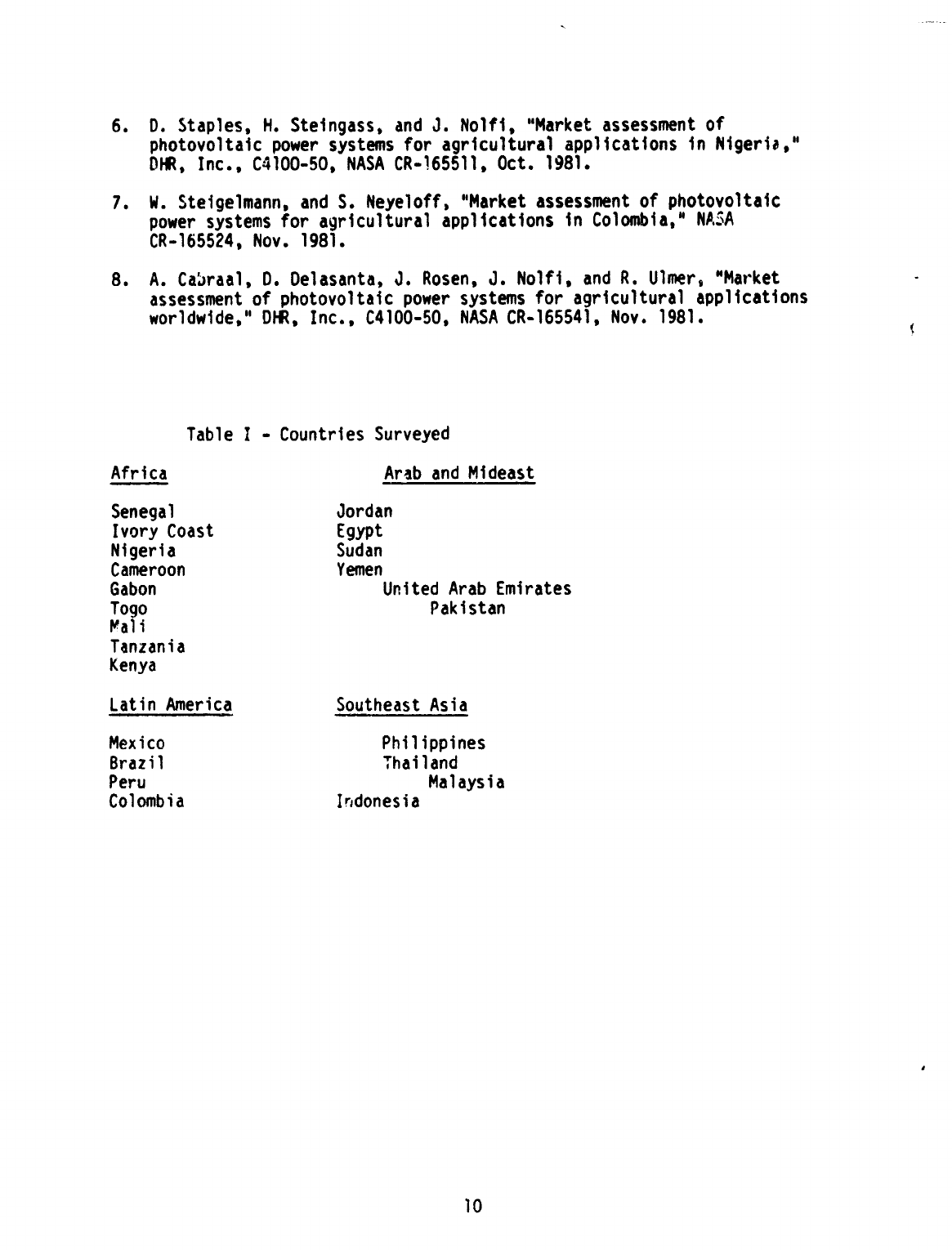

approach to be used in the in-depth in-country surveys. The countries

selected for the surveys were also selected so as to provide a

representative cross section of the developing world. The criteria for

selection included: (1) the country be located in or near the sun belt, (2)

the country possess a possibly sizable market potential, and (3) the country

be accessable to U.S. marketers. Additionally, the countries chosen

represented both the oil importing and oil exporting nations. The

in-country visits accomplished the following objectives:

o

Gathered new data and validated data acquired during literature

search

o

Acquainted local officials with present status and future plans of

U.S. PV industry

o

Determined potential obstacles or barriers to PV market development

o

Assessed the degree of possible penetration of potential market

A total of 23 countries (table I) was surveyed and over 800 key people

were contacted.

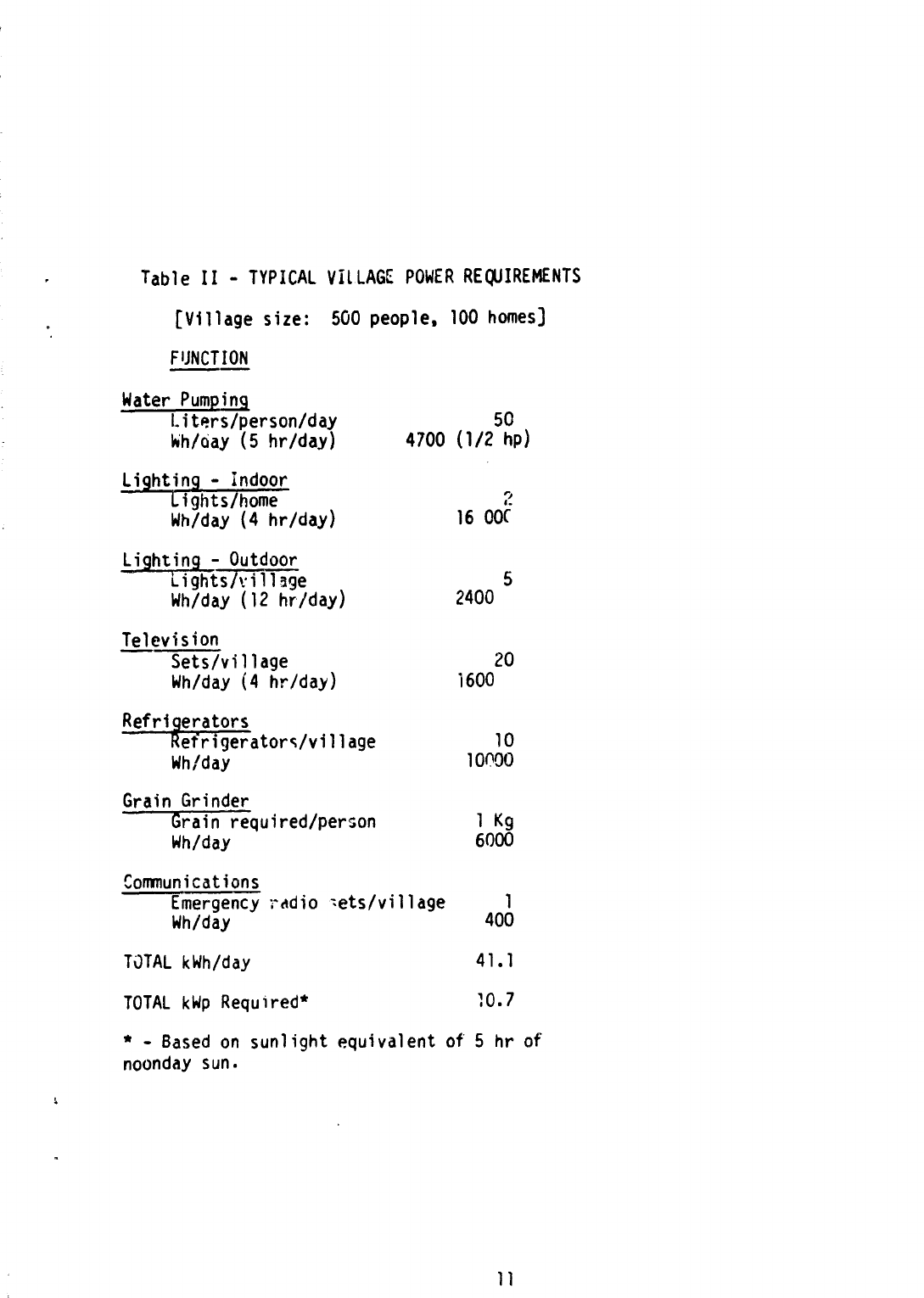

Village Power Study Conclusions. - In order to estimate the potential market

for photovoltaics in the village power sector, the power requirements for

representative remote villages were estimated. It was assumed that an

average remote village population would consist of about 500 people living

in 100 homes. Table II shows the assumptions made for village

electrification. It was estimated that about 10.7 kWp per village would be

required. Thus an average of 10 kWp per village was used for calculation

purposes.

Based on the approximate number of unelectrified villages identified

during the in-country survey, an extrapolation was made for the entire

developing world. This extrapolation estimated a total of 2 million

unelectrified villages. Multiplying 10 kWp per village by the 2 million

unelectrified villages results in a total potential market of 20 000 MWp.

This is probably a conservative estimate of the total village power

potential, because the potential for replacement of diesel generators

already installed in to a large number of villages was not included.

Assuming that the 20 000 MWp estimated nn

t

ential is relatively accurate,

the next question is, "How much of it can actually be achieved?" To answer

this requires other important factors pertinent to international PV

marketing be considered, such as availability of financing, existence of

import restrictions, knowledge of photovoltaics in the developing world, and

others. These can he thought of as the barriers to international PV

marketing, and tend to be the same regardless whether the market being

studied is the village power or the agricultural market. A discussion of

these barriers to international PV marketing will be presented later.

When the barriers are considered, the achievable village power market in

the near term (i.e., the next 10 years) was estimated to be not more than 5

percent (1 GWp) of the potential market. The primary reason for this

somewhat pessimistic estimate is that m.^,ving a new technology into a market

having limited financial resources and that is somewhat slow to accept new

ideas will take time. The first 5 years of the period will be devoted to

proving that photovoltaics is truly a viable alternative energy option. The

last 5 years will be the beginning o

f

the true commercial market.

3

However, even at this limited 5 percent market penetration, the 1 GWp real

market represents a multi-billion dollar export market and that can provide

a substantial portion of a significant production base.

Market for Photovoltaics for Cottage Industry Applications

The market for photovoltaics in the developing world in the cottage

industry sector was studied by the IIT Research Institute (ref. 2). For the

purposes of this study, cottage industries were defined as "small rural

manufacturers, employing less than 50 people, producing consumer and simple

products." It was known that stand-alone photovoltaic systems are not cost

competitive with grid generated electricity; therefore, the study focused on

rural areas of nonindustrialized countries, where commercial power is not

available.

The approach employed for this study was to initially establish the

existence of a potential market, to examine the economic advantages of a

photovoltaic system as compared to alternative means of supplying electric

power, to quantify the electric power needs of typical cottage industries,

and to identify countries which appeared to represent early market

opportunities.

Since data on cottage industries is extremely limited, especially in

developing nations, it was necessary to take an in-depth look at the cottage

industry sector of specific developing countries to determine how

photovoltaics might "fit" in. Four countries were selected for this

in-depth analysis -- the Philippines, Mexico, Morocco and Brazil.

In-country field investigations were made in the Philippines and Mexico.

After estimating the potential market for cottage industry power

systems, the next course of action was to determine the feasibility of

attaining that potential or, in other words, to determine the real market

for photovoltaic systems. The most significant factors which determine the

real market for stand-alone photovoltaic systems in cottage industry

applications were determined to be:

o

Is the system affordable to the purchaser?

o Does the system demonstrate itself to be the best option for

the purchaser over his current power source or the available

alternatives?

o

Will the system be accepted and utilized by the end-user?

Cottage Industry Study Conclusions. - The potential market is a theoretical

estimate of the gross demand for small-scale decentralized sources of

electric power for rural cottage industry applications. The underlying

assumptions are that the rural producer desires electricity and that the

purchaser can afford it. Factors considered in determining the potential

market include: rural population, importance of manufacturing and cottage

industry to the economy, the number of people engaged in fundamental

industries and the power consumption of typical cottage industries. It was

4

also considered that: some rural industries are electrified or soon to be

electrified by a grid network, in some areas hydro or wind

power may be more

appropriate, and some rural areas will have insufficient solar radiation for

effectively utilizing photovoltaics. Th- remainder of the market is assumed

to be the potential market for stand-alone photovoltaic systems,

diesel-driven generator sets or gasoline-driven generator sets. Based on

these factors, the potential market was found to be 70 000 megawatts.

The amount of this potential market that can be achieved

in reality,

however, appears to be very small, at least in the near term. The major

reasons supporting this conclusion are that cottage industries, in general,

are severely capital constrained and are not good candidates for loans or

recipients of significant public sector support. Further, for many of the

most economically significant cottage industries, the power levels required

are high enough that stand-alone photovoltaic systems, at the system cost of

$6-$13/Wp assumed in this study, ma

y

not be the most economical means of

providing decentralized sources of electric power. For example, a barrel

making operation was estimated to require a 30 kW photovoltaic system in

order to fully electrify the "factory". Under the cost scenarios employed

in

this study, a diesel generator set was determined to be a better economic

choice than photovoltaics in the near term. Only those applications

requiring small amounts of electric power, such as lighting and small tools,

would be viable. "ollectively these applications amount to only a very

small fraction of t

►

,- potential market.

Market for Photovoltaics for Agricultural Applications

The market for photovoltaics in the agricultural sector was studied by

DHR, Incorporated (refs. 3 to 8). This study was conducted in a manner

similar to the other previously discussed studies. First, a domestic

literature search was conducted to characterize the agricultural sector of

developing countries and to develop an approach to be used during in-country

visits conducted under the second part of the study. Five countries were

selected for detailed in-country surveys: Nigeria, Morocco, Colombia,

Mexico and the Philippines. These countries were selected on the basis of

several factors including: economic importance of agricultural sector,

energy situation, extent of electrification, solar resources, and geographic

representation.

These surveys included a series of meetings with the country's energy,

agriculture, economic, financial, business and policy experts to obtain

current agricultural and energy development and policy data and an

evaluation of factors important to introducing PV power systems into the

agricultural sector. Site visits were made to obtain power requirements and

energy use profile data for several agricultural applications. The

information gathered provided a data base to characterize the environment in

which PV systems would be marketed and used. Data on applications were used

to identify cost-compet

i

tive end uses by year of competitiveness. An

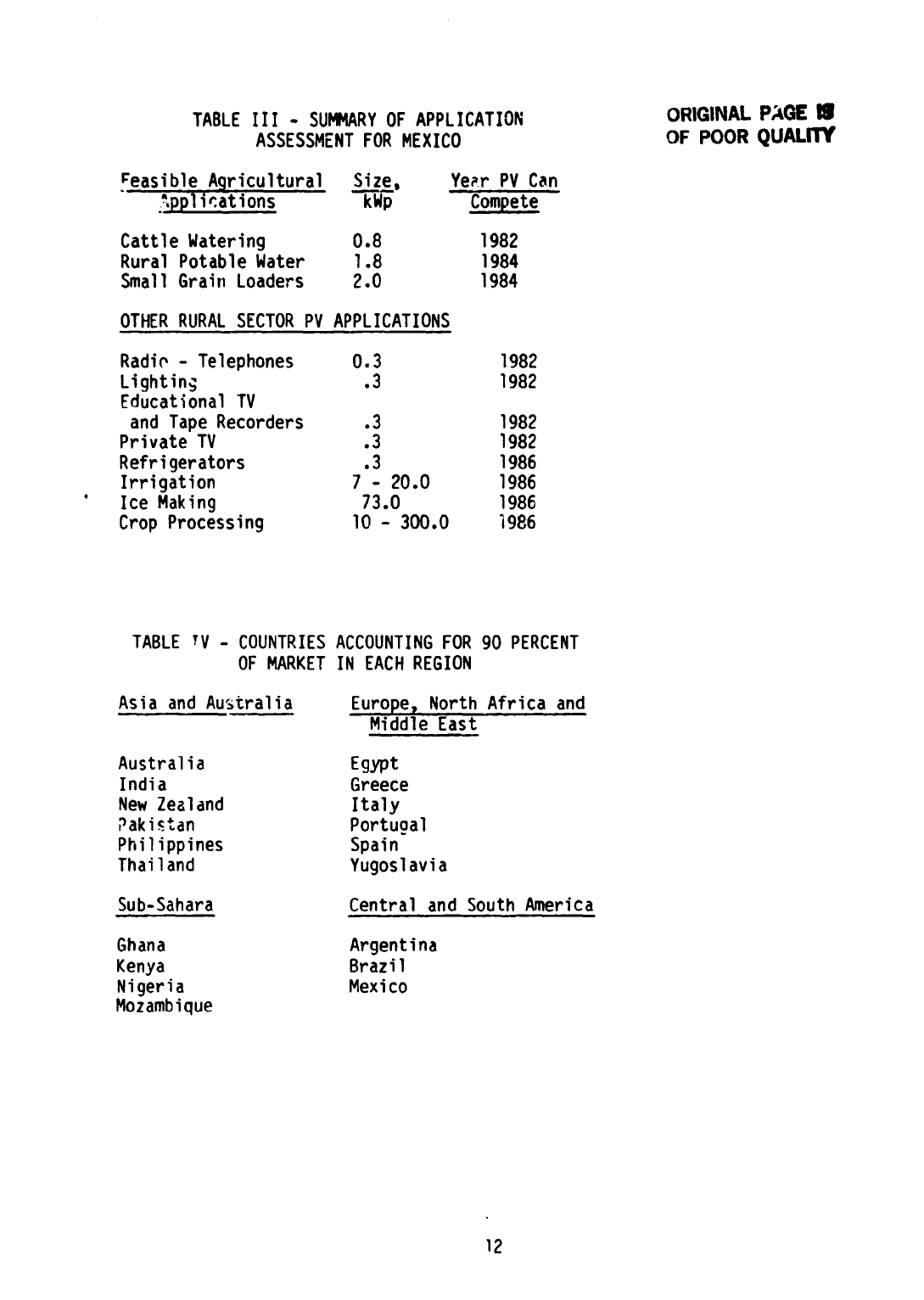

example of the cost-competitiveness end uses for a specific country, Mexico,

is shown in table III. Similar end uses were identified for the other four

countries in which the surveys were conducted.

The results obtained for the five countries surveyed in-depth were used

to prepare a projection for the photovoltaic market in the agricultural

sector worldwide. The methodology employed in that projection is detailed

i

in reference 8 and essentially involved quantifying the photovoltaics market

on the basis of the factors which were determined to be the most important

based on the in-country case studies: The estimates produced by the

methodology, while useful in drawing broad conclusions, should, because of

uncertainties in data accuracy, and the influence of nonquantifiable factors

such as distrust of new technology, be treated as only first order estimates.

Agricultural Study Conclusions. - The study estimated that the real

worldwide agricultural sector market ranges from 14 to 55 help between 1981

and 1986. These projections assumed that the DOE 1982 and 1986 cost goals

for both modules and systems were achieved. Clearly significant delays in

achieving the projected selling costs will cause reductions in the real

market. The countries which are projected to account for over 90 percent of

the regional market are shown in table IV.

In addition to the quantitative market estimates, the study made several

conclusions regarding the technical and economic feasibility of stand-alone

photovoltaic systems in the agricultural sector which are noted below.

o

In the next 2 to 3 years only small power needs can

economically

supplied by PV systems. They include battery charging, small field

irrigation and livestock watering from shallow depths, small

grinding mills and small produce coolers.

o

By about 1985-86, PV applications requiring 4 to 6 kW of power will

be economically feasible. The feasible applications expand to

include irrigation and livestock watering from deeper wells, larger

grinding/milling operations, produce coolers and freezers, and

aquicultural uses.

o

The relatively maintenance-free operation of PV systems may swing

the balance in favor of PV systems and away from diesel and

gasoline generators, even if PV power is more expensive, in

countries which have poor equipment-servicing facilities.

o

Except for livestock watering under open range conditions, the

ability of PV systems to operate unattended is not a significant

advantage in agriculture.

o

In the next 4 to 5 years the ultimate purchaser of larger PV

systems (through direct purchases or financing by development

banks) in developing countries will be ti;e government. Thus, PV

must be shown to be economically feasible when compared to its

nearest competitor.

o

The private sector may be able to afford (through outright

purchases or with commercial bank loans) small power systems since

capital investment is much less.

o

In countries where farmers are faced with high fuel prices, in 1982

a PV system will be cheaper to operate, on an annual cash flow

basis, than a gasoline powered generator of about 1 kW,

,

o

Although only small power needs can be economically served by PV

systems in agricultural applications, the market is significant.

Barriers to International Photovoltaics Marketing

All of the studies identified barriers that must be overcome by American

photovoltaic product manufacturers before successful international marketing

in the developing world can be achieved. These barriers tend to be the same

regardless of the application sector. The most significant barriers are

summarized below.

o

Lack of awareness of PV technology and its applicability is a major

barrier to market development. Compounding the awareness problem

is the attitude that photovoltaics is an "energy source of the

future." This problem pervades all decision-making strata ranging

from government officials, financiers, dealers and distributors,

and users.

o

Other than the oil-exporting nations, most potential customers have

limited access to long-term financing. In addition, photovoltaics

will most lii,ely take a lower priority in the allocation of

government long-term capital financing particularly if other

renewable energy sources are judged to be economically superior.

o

Many developing nations are establishing government energy policies

that stress self-sufficiency. The import of U.S. photovoltaic

systems may be viewed as contradictory to that policy.

o

Consumer buying behavior in the developing nations is characterized

by high discount rates and consequently very fast payoff times on

investments. The high init

4

11

price of photovoltaic systems will

not be appealing to potential purchasers unaccustomed to life-cycle

cost decision making.

o

Many nations subsidize domestic fuel costs. This has the effect of

greatly restricting the market in the private sector when the

decision to purchase photovoltaics in contrast to a conventional

powered system will be made on a financial basis rather than an

economic basis.

o

German, French and Japanese photo

v

oltaic companies, through

demonstration projects supported by their governments and by

aggressive marketing, are establishing a strong presence in many

countries worldwide. Furthermore, some countries (e.g., Mexico,

Brazil, India) are developing indigenous PV industries.

o

The generally poor state of the world economy is severely affecting

the ability of developing countries to carry out rural development

plans which could have provided sources of financing for many

photovoltaic sales. Additionally, many developing countries are

imposing import restrictions, many of which may hinder

photovoltaics marketing efforts. Also the very strong U.S. dollar

relative to many developing countries' currency means increased

cost of imported photovoltaic products to consumers.

Recommendations to American PV Manufacturers of Strategies for

International Marketing

The three studies summarized in this paper made several strategy

recommendations to the U.S. manufacturers who wish to market their products

in the developing world to help overcome some of the barriers noted above.

These recommendations are summarized below and should be considered generic

suggestions to PV manufacturers and dealers based on field work. The actual

market strategies employed would depend significantly on the market

characteristics of the individual nations concerned.

Advertising/Information Dissemination. - A significant barrier to marketing

photovoltaics abroad is tie lack of information and awareness on the

technical and economic advantages of PV systems. To effectively reach the

potential customer and to create demand for PV products, demonstrations may

be the single most effective tool. With low literacy rates in developing

countries, information is often disseminated by word of mouth based on one

person's experience.

Financing and Pricing. - Customer financing of PV purchases may be the most

important factor in a developing country PV market. Low per capita income,

the lack of available long-term capital in some countries, and the high cost

of capital combine to severely restrict the ability of the customer to pay

for a Nigh first cost PV system. Some development banks will offer

long-term loans at low interest rates but only for cost-effective PV

systems. However, the total amount of money available may be small.

Focusing ,marketing efforts on corporations or government agencies that have

the money to buy PV systems will solve the financial problem, but the market

may be limited.

Another approach in overcoming difficulties is leasing the PV equipment

to -_he customer. Although leasing arrangements are generally not used in

developing countries, there are some advantages of leasing that make it an

attractive financial alternative. First, leasing a PV system will spread

costs over a period of years. Second, leasing programs can be operated by a

local distributor who would purchase systems from a U.S. manufacturer and in

turn rent systems to users. Thus the user does not have to make a 20 year

commitment, the U.S. PV manufacturer sells the PV panels outright, and the

healer realizes a substantial profit. Furthermore, it could be financed by

short-term working capital loans which are easier for users to obtain.

Distribution and Service Infrastructure. - Dealers and distributors are an

essential and costly component of any successful overseas marketing effort.

In the case of photovoltaics, the market to date is too small to support an

extensive distribution system within any developing country.

There are, however,a number of ways in which a distribution network

could be established: (1) piggyback onto existing pumps, electrical

generators, diesel and gasoline engine distributors; (2) establish a new

exclusive dealership within a country with a local entrepreneur; and (3)

8

develop an exclusive distribution system within a country by the PV

manufacturer.

Closely tied to the development of a distribution infrastructure is the

necessity of offering the customer quick and quality service for all

products sold plus maintaining r,dequate supplies to meet PV demand. As a

marketing tool, service availability is exceptionally effective.

Product-Market Fit. - In offering PV systems to the ThirL World community,

the PV manufacturer should initially offer small units that are economically

and financially viable as compared to other alternative energy sources.

Later as costs drop, the manufacturer may expand product lines to include

larger power outputs, offering an entire line. It is critically important

that complete systems as opposed to components be offered for sale. For

example, a PV-powered pump should be produced for sale rather than a PV

power supply for use with an electric pump.

Trade Relationships. - Finally, the PV manufacturer should b^ flexible in

considering the benefits offered by a developing country in terms of

tariffs, license, taxes, trade allowances, etc. In a virgin PV market and

with possible heavy Japanese and Europe!n competition, the early loss of

market share to competitors by not taking aggressive advantage of financial,

tax and other incentives offered by a developing country may hinder market

development later as competitors establish themselves in the marketplace.

REFERENCES

1.

C. Ragsdale and P. Quashie, "Market definition study of photovoltaic

power for remote villages in developing countries," Motorola, Inc.,

FDR-1110, NASA CR-165287, Oct. 1980.

2.

T. M. Philippi, "International market assessment of stand-alone

photovoltaic power systems for cottage industry applications," IIT

Research Inst., IITRI-JO6519, NASA CR-165287, Nov. 1981.

3.

R. A. Cabraal, D. Delasanta, and G. Burrill, "Market assessment )f

photovoltaic power systems for agricultural applications in the

Philippines," Rural Development, Inc., C4100-50, NASA CR-165286, Apr.

1981.

4.

W. Steigelmann, and I. Asmon, "Market assessment of photovoltaic power

systems for agricultural applications in Mexico," NASA CR-165441, July

1981.

5.

H. Steingass, and I. Asmon, "Market assessment of photovoltaic power

systems for agricultural applications in Morocco," DHR, Inc., C4100-50,

NASA CR-165477, Sept. 1981.

g3

r^

6.

D. Staples, H. Steingass, and J. Nolfi, "Market assessment of

photovoltaic power systems for agricultural applications in Nigeria,"

DHR, Inc., C4100-50, NASA CR-165511, Oct. 1981.

7.

W. Steigelmann, and S. Neyeloff, "Market assessment of photovoltaic

power systems for agricultural applications in Colombia," NASA

CR-165524, Nov. 1981.

8.

A. Ca5raal, D. Delasanta, J. Rosen, J. Nolfi, and R. Ulmer, "Market

assessment of photovoltaic power systems for agricultural applications

worldwide," DHR, Inc., C4100-50, NASA CR-165541, Nov. 1981.

Table I - Countries Surveyed

Africa

Arab and Mideast

Senegal

Jordan

Ivory Coast

Egypt

Nigeria

Sudan

Cameroon

Yemen

Gabon

United Arab Emirates

Togo

Pakistan

Mali

Tanzania

Kenya

Latin America

Southeast Asia

Mexico

Philippines

Brazil

Thailand

Peru

Malaysia

Colombia

Indonesia

t

10

Table II - TYPICAL VILLAGE POWER REQUIREMENTS

[Village size: 500 people, 100 homes]

FUNCTION

Water Pumping

i_iters/person/day

50

Wh/oay (5 hr/day)

4700 (1/2 hp)

Li hting - Indoor

Wh/day

Lights/home

hr/day)

16 OOC

Lighting - Outdoor

Lights village

5

Wh/day (12 hr/day)

2400

Television

Sets/village

LO

Wh/day (4 hr/day)

1600

Refrigerators

Refrigerators/village

10

Wh/day

10000

Grain Grinder

rain required/person

1 Kg

Wh/day

6000

Communications

Emergency radio ,ets/village

1

Wh/day

400

TOTAL kWh/day

41.1

TOTAL kWp Required*

1.0.7

* - Based on sunlight equivalent of 5 hr of

noonday sun.

s

ORIGINAL PAGE 19

OF POOR QUALITY

TABLE III - SUMMARY OF APPLICATION

ASSESSMENT FOR MEXICO

F

easible A ricultural

Size,

Year PV Can

"pp rations

Rppp

Compete

Cattle Watering

0.8

1982

Rural Potable Water

1.8

1984

Small Grain Loaders

2.0

1984

OTHER RURAL SECTOR PV APPLICATIONS

Radio - Telephones

0.3

1982

Lighting

.3

1982

Educational TV

and Tape Recorders

.3

1982

Private TV

.3

1982

Refrigerators

.3

1986

Irrigation

7 - 20.0

1986

Ice Making

73.0

1986

Crop Processing

10 - 300.0

1986

TABLE

T

V

-

COUNTRIES ACCOUNTING FOR 90 PERCENT

OF MARKET IN EACH REGION

Asia and Australia

Europe, North Africa and

Australia

Egypt

India

Greece

New Zealand

Italy

Pakis"an

Portuoal

Philippines

Spain

Thailand

Yugoslavia

Sub-Sahara

Central and South America

Ghana

Argentina

Kenya

Brazil

Nigeria

Mexico

Mozambique

12